Deakin University MAF308 Assignment 2: Bond Valuation and Analysis

VerifiedAdded on 2022/11/30

|11

|1649

|416

Homework Assignment

AI Summary

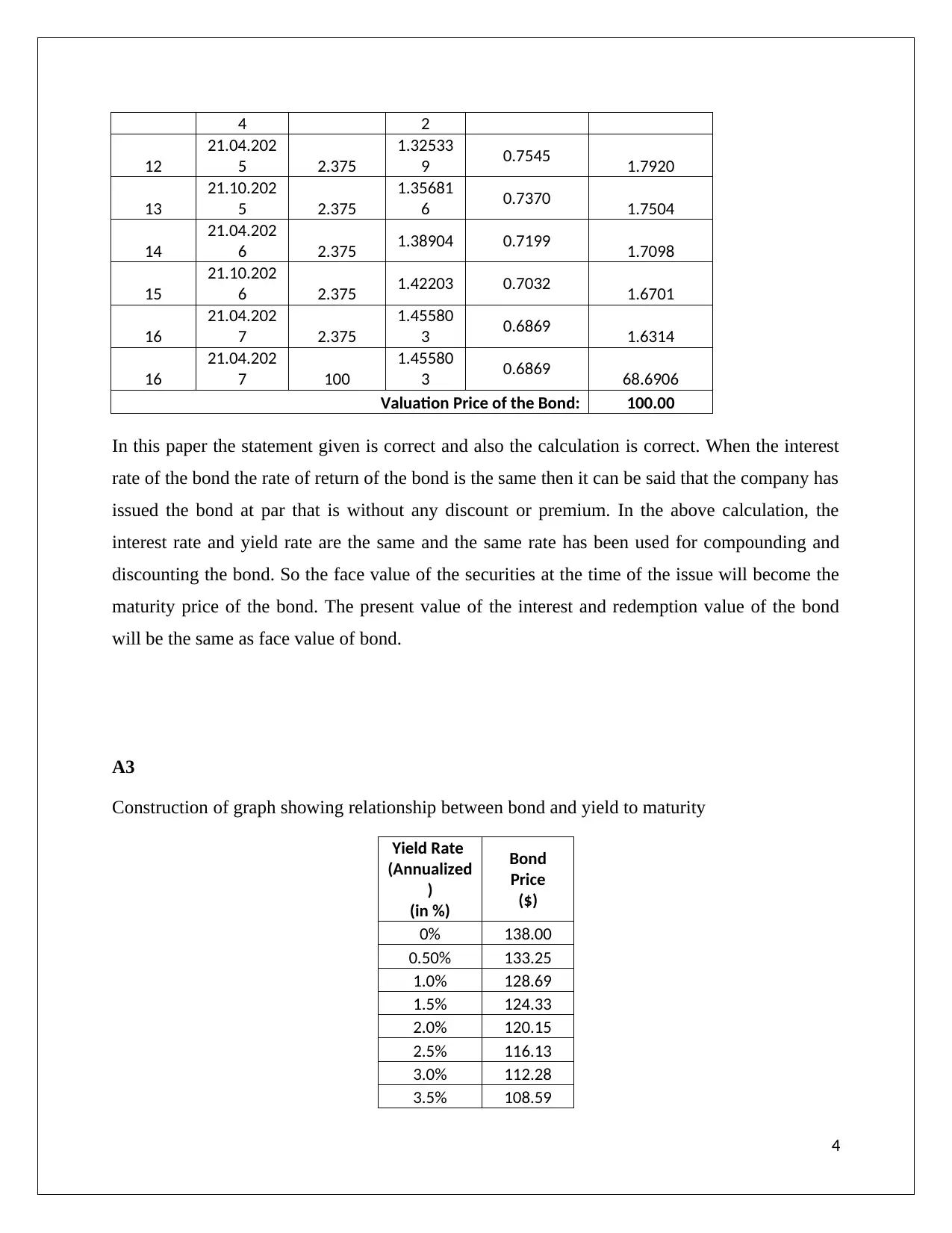

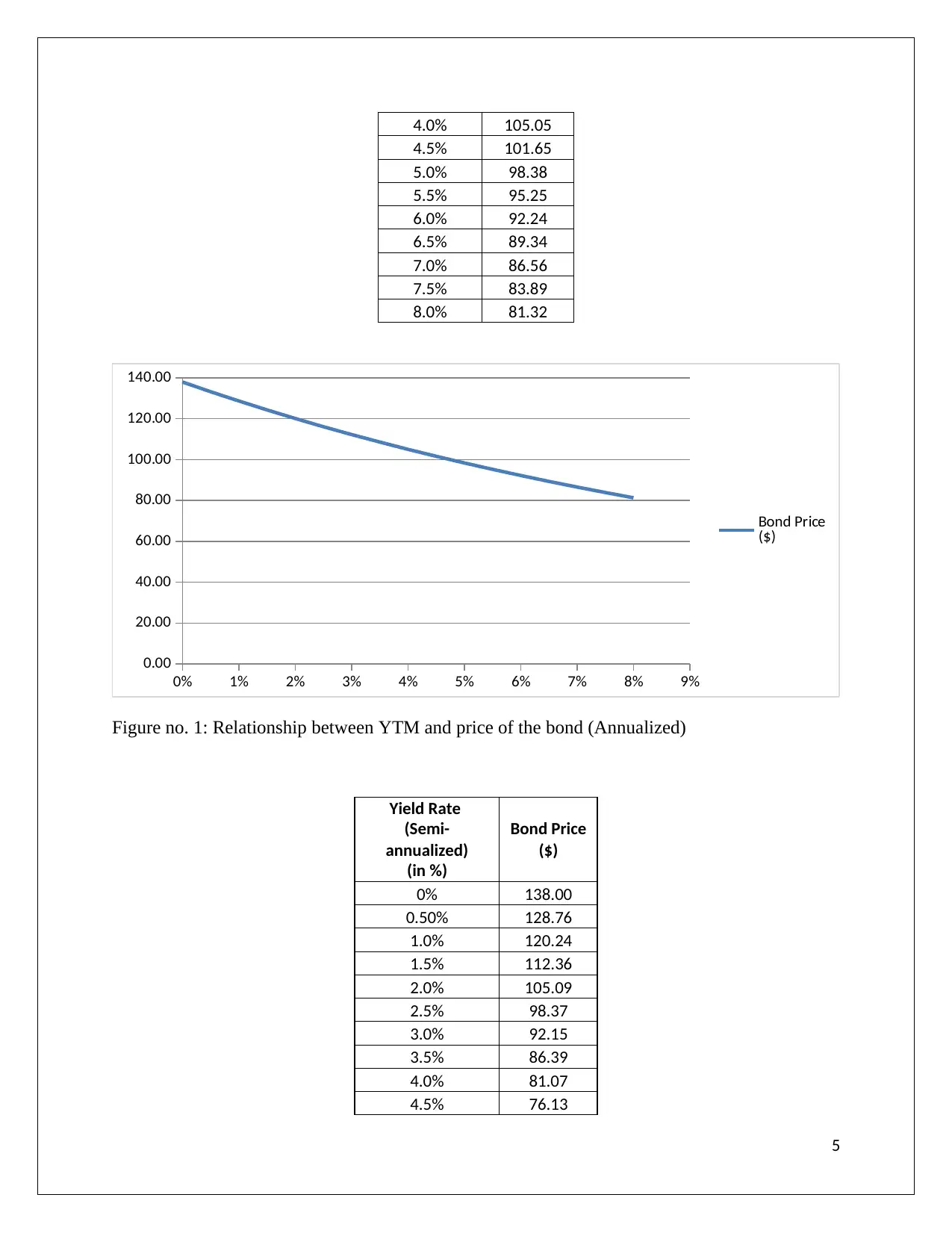

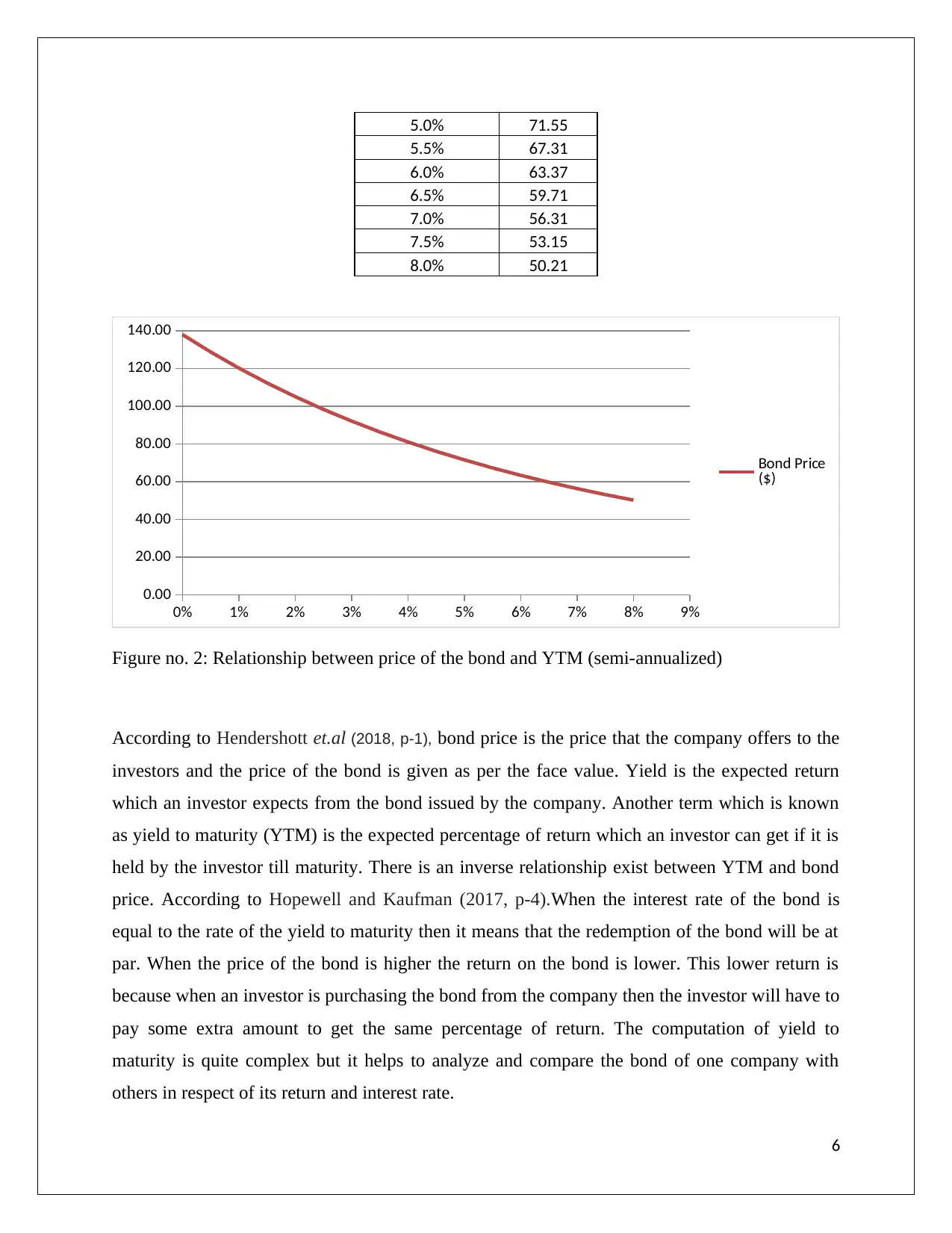

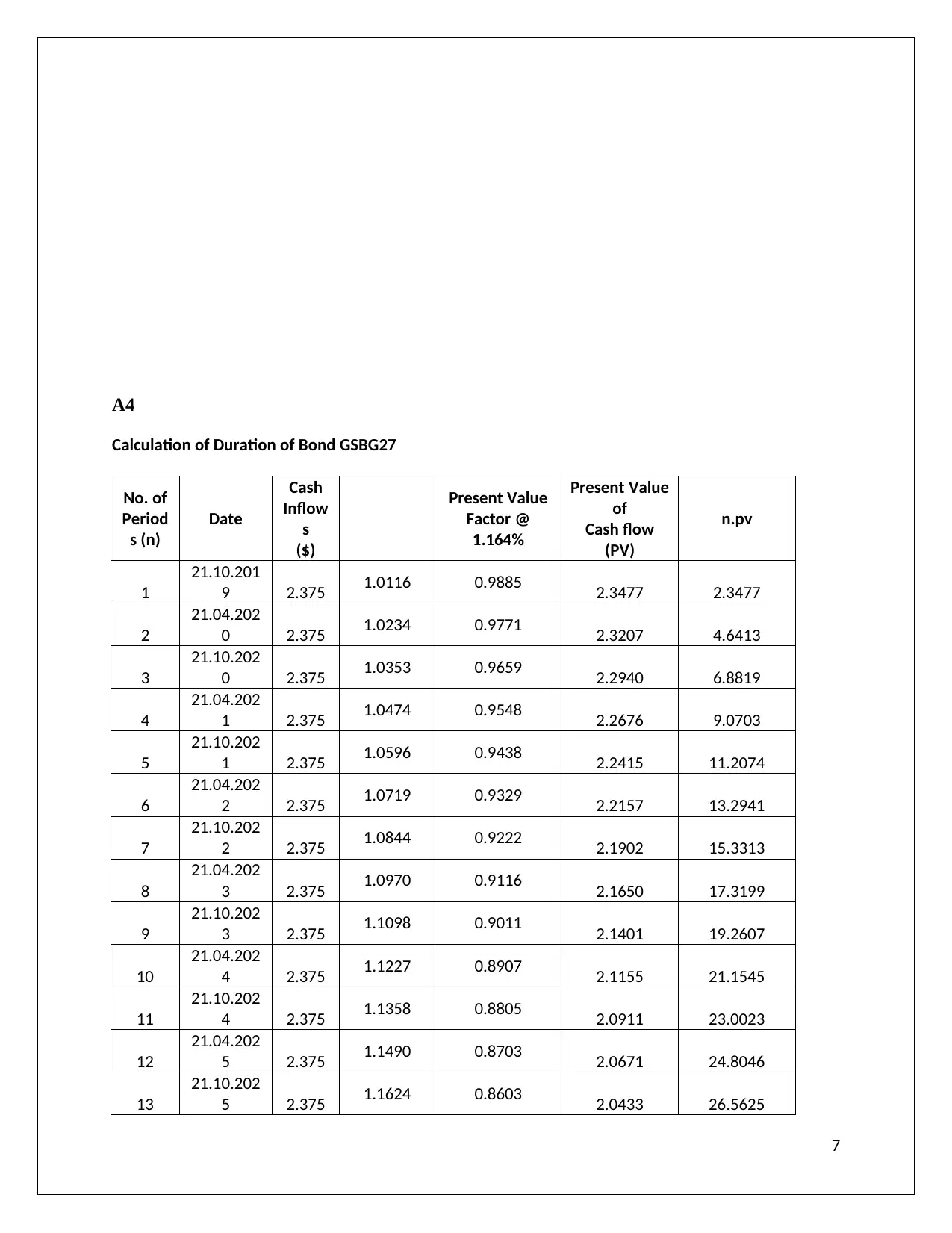

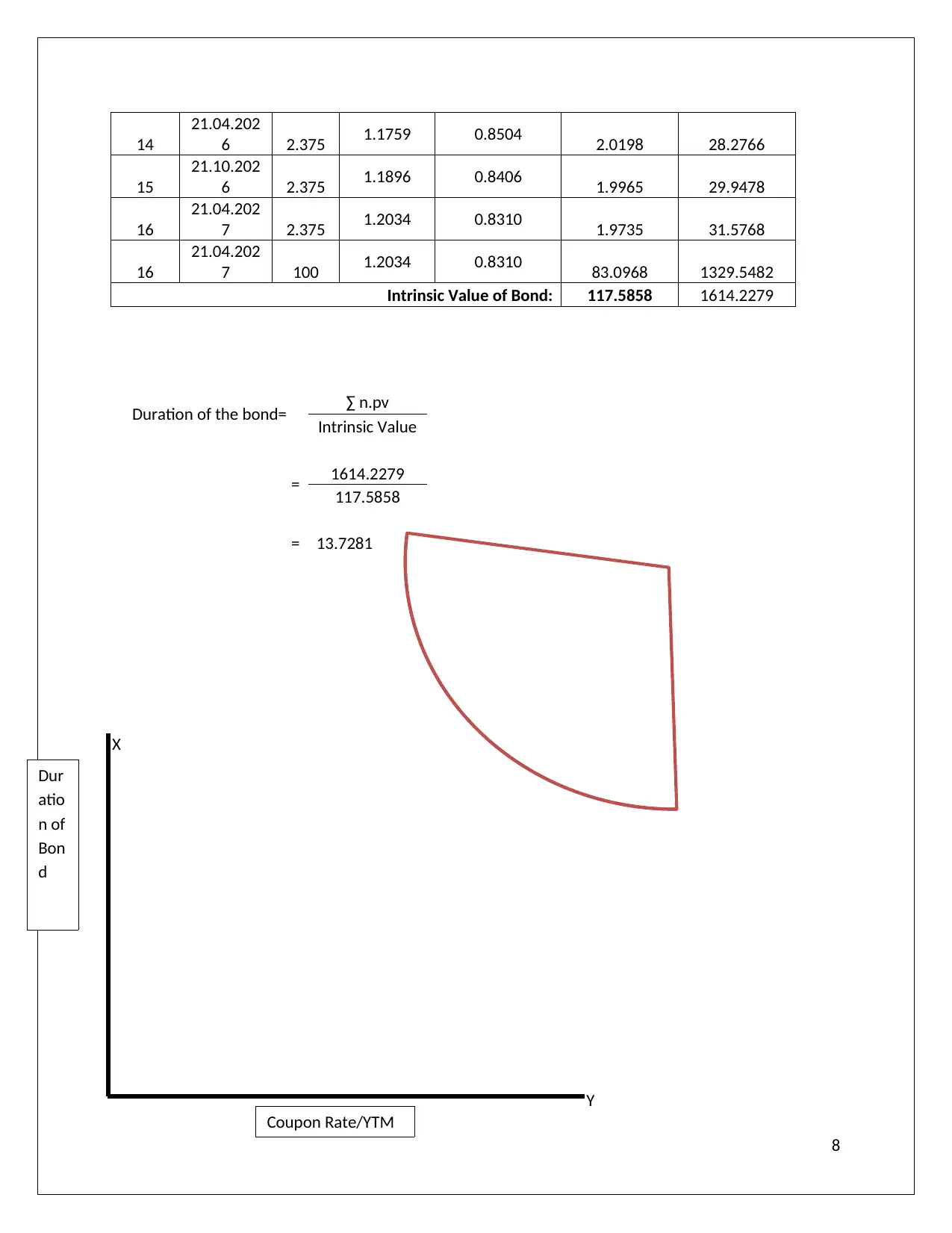

This assignment solution for MAF308, Derivatives and Fixed Income Securities, analyzes a bond issued by a company, calculating its yield to maturity (YTM) and comparing it to the market price. The solution provides a detailed calculation of YTM, considering the coupon rate, face value, and redemption date, and highlights the difference between approximate and IRR methods for YTM calculation. Furthermore, the assignment includes a bond valuation analysis, demonstrating how to determine the bond's present value and price based on its cash flows. It then constructs graphs illustrating the relationship between bond price and YTM, both annualized and semi-annualized, and calculates the bond's duration, which measures its price sensitivity to interest rate changes. The solution also references relevant literature to support the analysis, providing a comprehensive understanding of bond valuation and related concepts.

1 out of 11

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.