King's Own Institute ACC701: Mags Ltd Intangible Asset Analysis Report

VerifiedAdded on 2022/09/16

|12

|2497

|14

Report

AI Summary

This report provides an in-depth analysis of Mags Ltd's accounting practices concerning intangible assets, specifically addressing the application of AASB 138. The analysis focuses on the company's treatment of direct mailings, customer lists, and marketing costs. The report examines whether the capitalization of direct mail costs and the purchased customer list adheres to the guidelines of AASB 138, which deals with the recognition, measurement, and disclosure of intangible assets. It explores the criteria for recognizing intangible assets, the appropriate methods for measuring their carrying amount, and the implications of capitalization versus expensing marketing costs. The report also evaluates the amortization of the customer list and the need for impairment testing. It concludes that the direct mailing costs should be expensed and the customer list should be recognized as an intangible asset, amortized over its useful life, subject to impairment testing. The report provides calculations and recommendations based on the standard, offering a comprehensive understanding of accounting for intangible assets in the context of Mags Ltd.

Running head: RESEARCH INDIVIDUAL ASSIGNMENT

Research Individual Assignment

Name of the Student

Name of the University

Author Note

Research Individual Assignment

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

RESEARCH INDIVIDUAL ASSIGNMENT

Executive Summary

The aim of the assignment is to conduct an analysis on the Mags Ltd Company regarding the

procedures and actions that they specifically take for the purpose of treating Intangible Assets. In

order to well guide and apply the concepts of Intangible Assets in accordance with the Australian

Accounting Standards the key principles of AASB 138 has been applied. The application of the

guidelines and principles given by AASB 138 would be well helping the company in

understanding the recognition and measurement of the Intangible Assets of the company. Other

Issues like capitalization of the marketing costs which the company has incurred has also

discussed under the accounting standards of AASB 138. There are various set of guidelines

about the measurement of the carrying amount of the asset and the disclosures related to

intangible asset that has been well discussed and analysed.

RESEARCH INDIVIDUAL ASSIGNMENT

Executive Summary

The aim of the assignment is to conduct an analysis on the Mags Ltd Company regarding the

procedures and actions that they specifically take for the purpose of treating Intangible Assets. In

order to well guide and apply the concepts of Intangible Assets in accordance with the Australian

Accounting Standards the key principles of AASB 138 has been applied. The application of the

guidelines and principles given by AASB 138 would be well helping the company in

understanding the recognition and measurement of the Intangible Assets of the company. Other

Issues like capitalization of the marketing costs which the company has incurred has also

discussed under the accounting standards of AASB 138. There are various set of guidelines

about the measurement of the carrying amount of the asset and the disclosures related to

intangible asset that has been well discussed and analysed.

2

RESEARCH INDIVIDUAL ASSIGNMENT

Table of Contents

Introduction..................................................................................................................................2

AASB 138 guidelines on Intangible Assets.................................................................................2

Conclusion...................................................................................................................................6

References....................................................................................................................................8

RESEARCH INDIVIDUAL ASSIGNMENT

Table of Contents

Introduction..................................................................................................................................2

AASB 138 guidelines on Intangible Assets.................................................................................2

Conclusion...................................................................................................................................6

References....................................................................................................................................8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

RESEARCH INDIVIDUAL ASSIGNMENT

Introduction

The situation is related to Mags Ltd., an Australian mail order company. There has been a

significant growth in the sales and net income of the entity in the recent years. The future of the

company is believed to be very promising and the valuation of the company has also gone up

significantly in the recent times. However, the entity believes that the reasons for its success are

its marketing flair and expertise in the field. As a part of these innovations, the company is

undertaking some uncertain accounting practices related to the recognition and measurement of

intangible assets. One of them is the capitalisation of the direct mailings sent by it to the

customers and amortising them on a straight line basis (Steenkamp and Steenkamp, 2016). This

is because the company believes that the customers are obtained and retained with the help of

these mailings. Other intangible assets which have been recognised by the entity as a part of their

financial statements include customer list purchased from a competitor for $80000 on July 2019.

The final issue is related to the capitalising of the market costs (AASB, 2015). If these costs are

not capitalised and marketed instead, then the net income earned by the entity would be much

lower. The related solutions to these issues will be provided with the guidance of AASB 138,

which deals with the accounting for Intangible Assets in the Australian Territory (Russell 2014).

AASB 138 Guidelines on Intangible Assets

The main purpose of AASB 138 is to prescribe the treatment for intangible assets which

are not specifically dealt with the help of any other standard. In order to recognise an item as an

intangible asset, it is necessary that specified criteria related to the asset are met. There are also

certain guidelines about the measurement of the carrying amount of the asset and the disclosures

related to intangible assets (Kung et al., 2013). As per the paragraph 8 of AASB 138, an

intangible asset is a non-monetary asset which is identifiable but does not have substance.

RESEARCH INDIVIDUAL ASSIGNMENT

Introduction

The situation is related to Mags Ltd., an Australian mail order company. There has been a

significant growth in the sales and net income of the entity in the recent years. The future of the

company is believed to be very promising and the valuation of the company has also gone up

significantly in the recent times. However, the entity believes that the reasons for its success are

its marketing flair and expertise in the field. As a part of these innovations, the company is

undertaking some uncertain accounting practices related to the recognition and measurement of

intangible assets. One of them is the capitalisation of the direct mailings sent by it to the

customers and amortising them on a straight line basis (Steenkamp and Steenkamp, 2016). This

is because the company believes that the customers are obtained and retained with the help of

these mailings. Other intangible assets which have been recognised by the entity as a part of their

financial statements include customer list purchased from a competitor for $80000 on July 2019.

The final issue is related to the capitalising of the market costs (AASB, 2015). If these costs are

not capitalised and marketed instead, then the net income earned by the entity would be much

lower. The related solutions to these issues will be provided with the guidance of AASB 138,

which deals with the accounting for Intangible Assets in the Australian Territory (Russell 2014).

AASB 138 Guidelines on Intangible Assets

The main purpose of AASB 138 is to prescribe the treatment for intangible assets which

are not specifically dealt with the help of any other standard. In order to recognise an item as an

intangible asset, it is necessary that specified criteria related to the asset are met. There are also

certain guidelines about the measurement of the carrying amount of the asset and the disclosures

related to intangible assets (Kung et al., 2013). As per the paragraph 8 of AASB 138, an

intangible asset is a non-monetary asset which is identifiable but does not have substance.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

RESEARCH INDIVIDUAL ASSIGNMENT

Paragraph 12 of the standard states that the asset is identifiable if it is capable of being separated

and sold by the entity by either leasing, contracting or some other manner or arises due to a

contractual or legal right even if those assets cannot be sold by the entity. Paragraph 21 of the

standard states that the asset is to be recognised only if the future benefits which are attributable

to the asset will flow to the entity and the value of the asset can be measured reliably. Similarly,

the value of the benefits arising from the asset can be said to be reliably measured only if there

are reasonable and supporting assumptions to support the estimates of the management. These

set of economic conditions should also exist over the lifetime of the asset. Some other

expenditure which form the part of the cost of the asset include the R&D expenditure which is

related to an in-process R&D project acquired separately is recognised as an intangible asset (Su

and Wells, 2018).

Similarly, paragraph 68 of AASB 18 states that any expenditure on an asset should be

recognised as an intangible asset only if it is the part of an asset meeting the requirement criteria

(Steenkamp). This is also the case even when an expenditure is incurred but no recognisable

asset is created by the business. However, there are no generalised regulations or guidelines

which can be applied to any given situation to understand whether a particular expenditure can

be capitalised as a part of an intangible asset or not. As per paragraph 16 of AASB 138, any

business entity may have a portfolio of customers or a market share and expect that this market

share will likely to continue because of the efforts taken by the entity. However, as there is no

legal contract or a document binding this relationship, the entity does not have a measurable

control over the relationships with the customers or the expected economic benefits arising from

the relationship (Steele 2015). On the contrary, if the entity is able to prove that there is

sufficient evidence to suggest that it is able to control the economic benefits arising from such a

RESEARCH INDIVIDUAL ASSIGNMENT

Paragraph 12 of the standard states that the asset is identifiable if it is capable of being separated

and sold by the entity by either leasing, contracting or some other manner or arises due to a

contractual or legal right even if those assets cannot be sold by the entity. Paragraph 21 of the

standard states that the asset is to be recognised only if the future benefits which are attributable

to the asset will flow to the entity and the value of the asset can be measured reliably. Similarly,

the value of the benefits arising from the asset can be said to be reliably measured only if there

are reasonable and supporting assumptions to support the estimates of the management. These

set of economic conditions should also exist over the lifetime of the asset. Some other

expenditure which form the part of the cost of the asset include the R&D expenditure which is

related to an in-process R&D project acquired separately is recognised as an intangible asset (Su

and Wells, 2018).

Similarly, paragraph 68 of AASB 18 states that any expenditure on an asset should be

recognised as an intangible asset only if it is the part of an asset meeting the requirement criteria

(Steenkamp). This is also the case even when an expenditure is incurred but no recognisable

asset is created by the business. However, there are no generalised regulations or guidelines

which can be applied to any given situation to understand whether a particular expenditure can

be capitalised as a part of an intangible asset or not. As per paragraph 16 of AASB 138, any

business entity may have a portfolio of customers or a market share and expect that this market

share will likely to continue because of the efforts taken by the entity. However, as there is no

legal contract or a document binding this relationship, the entity does not have a measurable

control over the relationships with the customers or the expected economic benefits arising from

the relationship (Steele 2015). On the contrary, if the entity is able to prove that there is

sufficient evidence to suggest that it is able to control the economic benefits arising from such a

5

RESEARCH INDIVIDUAL ASSIGNMENT

relationship, then the customer relationships meet the criteria of the definition of an intangible

asset.

In case of Mags Ltd., there is no evidence to suggest that the cost of direct mailings

creates long lasting customer relationships for the entity. There is also no guarantee that the

economic inflow of the entity would be sustainable or consistent. Hence, the $4.2 million

incurred by the entity cannot be capitalised by the entity. They are a part of the promotional and

advertising expenditure incurred by the entity and should be expensed and reduced from the

profits of the entity.

The next asset regarding which the appropriateness of the accounting policy is to be

determined is the mailing list purchased from a competitor for $800000. According to the AASB

guidelines, if a mailing order company purchases a customer list from a competitor, then it will

be considered as an intangible asset of the company. It needs to be amortised on the basis of the

best estimates of the company. The period of amortisation, should not, under any circumstances

exceed the best estimates of the useful life initially estimated by the entity. In certain

circumstances, like the one faced by the entity, additional names may be added to the existing list

possessed by the entity. However, these additional names should not be considered as a part of

the additional benefits provided by the asset acquired by the entity. The expected benefits

received by the business should only be limited to the date the asset was acquired by the

business. Any impairment occurring on the customer list should also be constantly checked by

the business in accordance with the guidelines of AASB 136 Impairment of Assets. This should

be done by assessing the asset at the end of the accounting period and analysing whether there is

any indication of the asset being impaired.

RESEARCH INDIVIDUAL ASSIGNMENT

relationship, then the customer relationships meet the criteria of the definition of an intangible

asset.

In case of Mags Ltd., there is no evidence to suggest that the cost of direct mailings

creates long lasting customer relationships for the entity. There is also no guarantee that the

economic inflow of the entity would be sustainable or consistent. Hence, the $4.2 million

incurred by the entity cannot be capitalised by the entity. They are a part of the promotional and

advertising expenditure incurred by the entity and should be expensed and reduced from the

profits of the entity.

The next asset regarding which the appropriateness of the accounting policy is to be

determined is the mailing list purchased from a competitor for $800000. According to the AASB

guidelines, if a mailing order company purchases a customer list from a competitor, then it will

be considered as an intangible asset of the company. It needs to be amortised on the basis of the

best estimates of the company. The period of amortisation, should not, under any circumstances

exceed the best estimates of the useful life initially estimated by the entity. In certain

circumstances, like the one faced by the entity, additional names may be added to the existing list

possessed by the entity. However, these additional names should not be considered as a part of

the additional benefits provided by the asset acquired by the entity. The expected benefits

received by the business should only be limited to the date the asset was acquired by the

business. Any impairment occurring on the customer list should also be constantly checked by

the business in accordance with the guidelines of AASB 136 Impairment of Assets. This should

be done by assessing the asset at the end of the accounting period and analysing whether there is

any indication of the asset being impaired.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

RESEARCH INDIVIDUAL ASSIGNMENT

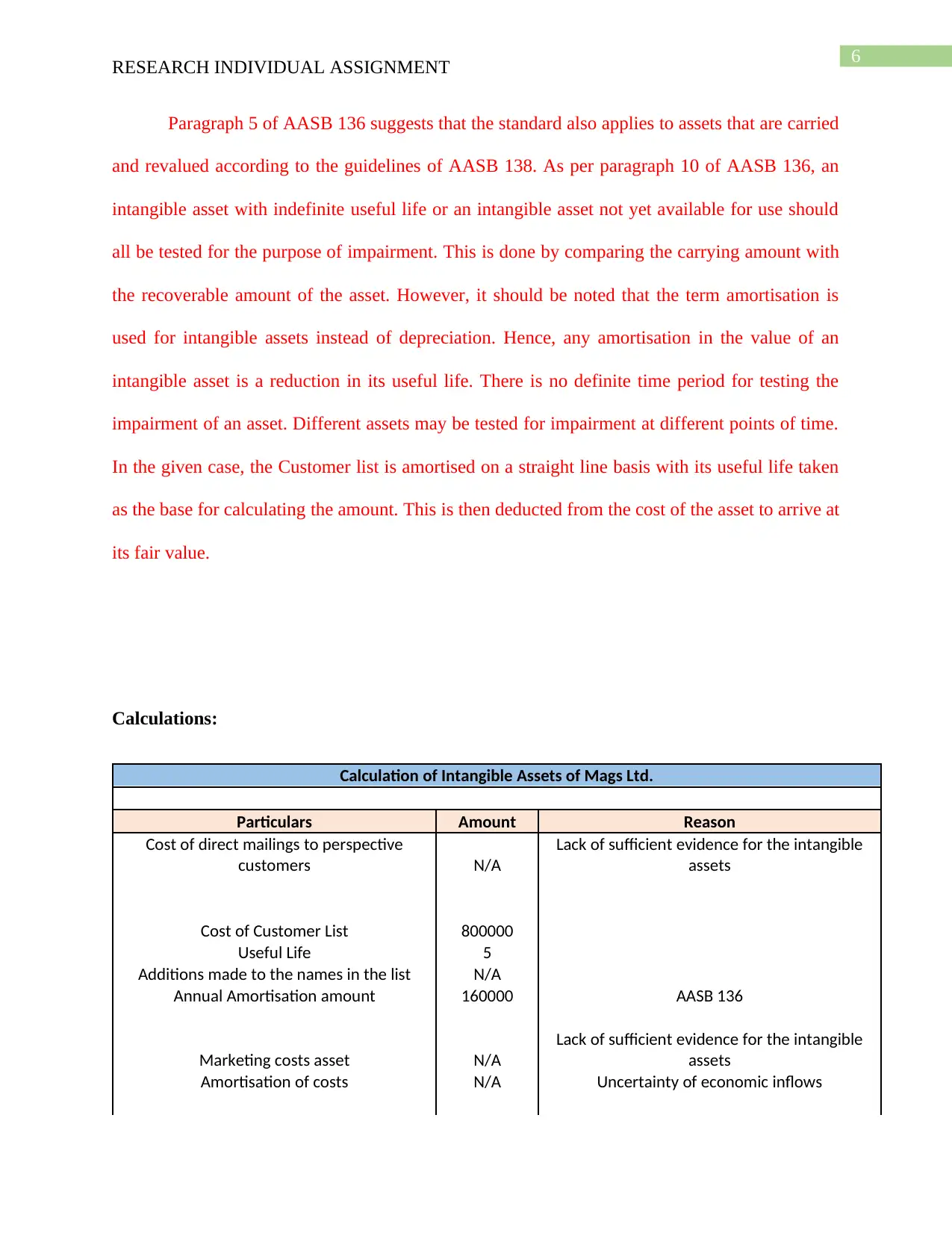

Paragraph 5 of AASB 136 suggests that the standard also applies to assets that are carried

and revalued according to the guidelines of AASB 138. As per paragraph 10 of AASB 136, an

intangible asset with indefinite useful life or an intangible asset not yet available for use should

all be tested for the purpose of impairment. This is done by comparing the carrying amount with

the recoverable amount of the asset. However, it should be noted that the term amortisation is

used for intangible assets instead of depreciation. Hence, any amortisation in the value of an

intangible asset is a reduction in its useful life. There is no definite time period for testing the

impairment of an asset. Different assets may be tested for impairment at different points of time.

In the given case, the Customer list is amortised on a straight line basis with its useful life taken

as the base for calculating the amount. This is then deducted from the cost of the asset to arrive at

its fair value.

Calculations:

Calculation of Intangible Assets of Mags Ltd.

Particulars Amount Reason

Cost of direct mailings to perspective

customers N/A

Lack of sufficient evidence for the intangible

assets

Cost of Customer List 800000

Useful Life 5

Additions made to the names in the list N/A

Annual Amortisation amount 160000 AASB 136

Marketing costs asset N/A

Lack of sufficient evidence for the intangible

assets

Amortisation of costs N/A Uncertainty of economic inflows

RESEARCH INDIVIDUAL ASSIGNMENT

Paragraph 5 of AASB 136 suggests that the standard also applies to assets that are carried

and revalued according to the guidelines of AASB 138. As per paragraph 10 of AASB 136, an

intangible asset with indefinite useful life or an intangible asset not yet available for use should

all be tested for the purpose of impairment. This is done by comparing the carrying amount with

the recoverable amount of the asset. However, it should be noted that the term amortisation is

used for intangible assets instead of depreciation. Hence, any amortisation in the value of an

intangible asset is a reduction in its useful life. There is no definite time period for testing the

impairment of an asset. Different assets may be tested for impairment at different points of time.

In the given case, the Customer list is amortised on a straight line basis with its useful life taken

as the base for calculating the amount. This is then deducted from the cost of the asset to arrive at

its fair value.

Calculations:

Calculation of Intangible Assets of Mags Ltd.

Particulars Amount Reason

Cost of direct mailings to perspective

customers N/A

Lack of sufficient evidence for the intangible

assets

Cost of Customer List 800000

Useful Life 5

Additions made to the names in the list N/A

Annual Amortisation amount 160000 AASB 136

Marketing costs asset N/A

Lack of sufficient evidence for the intangible

assets

Amortisation of costs N/A Uncertainty of economic inflows

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

RESEARCH INDIVIDUAL ASSIGNMENT

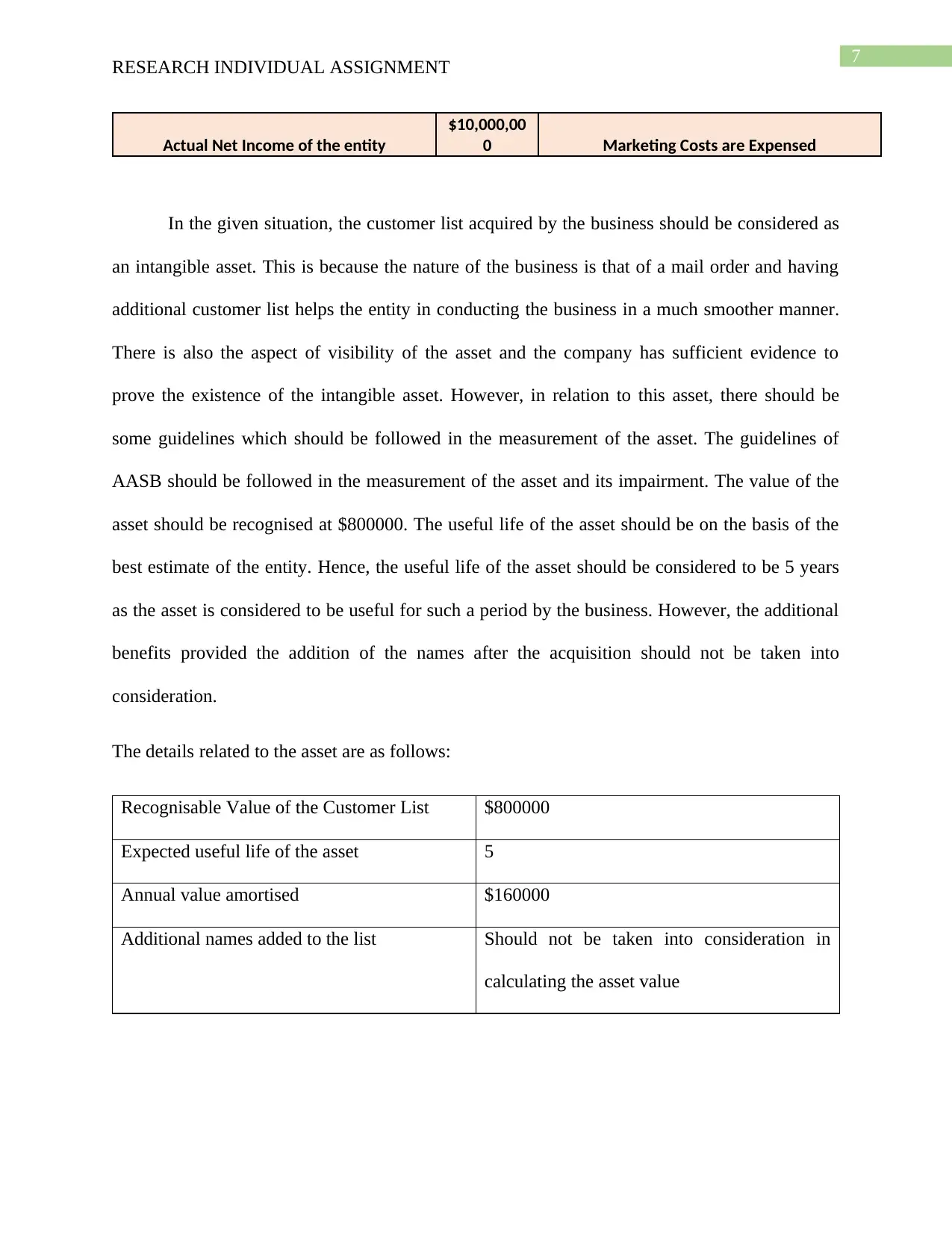

Actual Net Income of the entity

$10,000,00

0 Marketing Costs are Expensed

In the given situation, the customer list acquired by the business should be considered as

an intangible asset. This is because the nature of the business is that of a mail order and having

additional customer list helps the entity in conducting the business in a much smoother manner.

There is also the aspect of visibility of the asset and the company has sufficient evidence to

prove the existence of the intangible asset. However, in relation to this asset, there should be

some guidelines which should be followed in the measurement of the asset. The guidelines of

AASB should be followed in the measurement of the asset and its impairment. The value of the

asset should be recognised at $800000. The useful life of the asset should be on the basis of the

best estimate of the entity. Hence, the useful life of the asset should be considered to be 5 years

as the asset is considered to be useful for such a period by the business. However, the additional

benefits provided the addition of the names after the acquisition should not be taken into

consideration.

The details related to the asset are as follows:

Recognisable Value of the Customer List $800000

Expected useful life of the asset 5

Annual value amortised $160000

Additional names added to the list Should not be taken into consideration in

calculating the asset value

RESEARCH INDIVIDUAL ASSIGNMENT

Actual Net Income of the entity

$10,000,00

0 Marketing Costs are Expensed

In the given situation, the customer list acquired by the business should be considered as

an intangible asset. This is because the nature of the business is that of a mail order and having

additional customer list helps the entity in conducting the business in a much smoother manner.

There is also the aspect of visibility of the asset and the company has sufficient evidence to

prove the existence of the intangible asset. However, in relation to this asset, there should be

some guidelines which should be followed in the measurement of the asset. The guidelines of

AASB should be followed in the measurement of the asset and its impairment. The value of the

asset should be recognised at $800000. The useful life of the asset should be on the basis of the

best estimate of the entity. Hence, the useful life of the asset should be considered to be 5 years

as the asset is considered to be useful for such a period by the business. However, the additional

benefits provided the addition of the names after the acquisition should not be taken into

consideration.

The details related to the asset are as follows:

Recognisable Value of the Customer List $800000

Expected useful life of the asset 5

Annual value amortised $160000

Additional names added to the list Should not be taken into consideration in

calculating the asset value

8

RESEARCH INDIVIDUAL ASSIGNMENT

The next aspect regarding which the advice needs to be provided to the business is the

marketing expenses incurred by the entity as a part of conducting the business. As discussed

previously, AASB 138 suggests that an asset should be recognised as an intangible asset only if

the business has sufficient evidence to prove that the expenditure is relevant in providing

sustained returns to the business which are likely to continue for a foreseeable period in the

future (Hu, Percy and Yao, 2015). However, in this case, the only basis for the accounting

practice followed by the business is the past experience of the entity. These practices are also not

guaranteed by any copyright or protection by the entity. Hence, they are relatively easy to

replicate by the competitors. This is a reason for the uncertainty in the economic inflows

received by the business from the expenditure. Incorrect accounting practices by the entity also

result in the overstatement of the profits earned by the entity and the financial statements can

become misrepresented due to the accounting policies of the entity (Russell, 2017).

Conclusion

On the basis of the above discussion, it can be stated that the accounting for intangible

assets is done on the basis of the guidelines of AASB 138. This suggests that the cost of an

intangible asset should be capitalised only when the entity is certain that the economic benefits

arising out of the asset will be certain and continuous. In case of expenditure or assets which are

not evident to the outsiders, then the assets should have a sufficient evidence to prove that the

benefits received by the entity will be existing for a longer duration. In case of Mags Ltd., the

expenses incurred for the prospective customers cannot be considered to be a part of the

intangible assets of the company. The customer lists purchased by the entity should be a part of

the intangible assets of the company. However, any additions made to the list should not be

RESEARCH INDIVIDUAL ASSIGNMENT

The next aspect regarding which the advice needs to be provided to the business is the

marketing expenses incurred by the entity as a part of conducting the business. As discussed

previously, AASB 138 suggests that an asset should be recognised as an intangible asset only if

the business has sufficient evidence to prove that the expenditure is relevant in providing

sustained returns to the business which are likely to continue for a foreseeable period in the

future (Hu, Percy and Yao, 2015). However, in this case, the only basis for the accounting

practice followed by the business is the past experience of the entity. These practices are also not

guaranteed by any copyright or protection by the entity. Hence, they are relatively easy to

replicate by the competitors. This is a reason for the uncertainty in the economic inflows

received by the business from the expenditure. Incorrect accounting practices by the entity also

result in the overstatement of the profits earned by the entity and the financial statements can

become misrepresented due to the accounting policies of the entity (Russell, 2017).

Conclusion

On the basis of the above discussion, it can be stated that the accounting for intangible

assets is done on the basis of the guidelines of AASB 138. This suggests that the cost of an

intangible asset should be capitalised only when the entity is certain that the economic benefits

arising out of the asset will be certain and continuous. In case of expenditure or assets which are

not evident to the outsiders, then the assets should have a sufficient evidence to prove that the

benefits received by the entity will be existing for a longer duration. In case of Mags Ltd., the

expenses incurred for the prospective customers cannot be considered to be a part of the

intangible assets of the company. The customer lists purchased by the entity should be a part of

the intangible assets of the company. However, any additions made to the list should not be

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

RESEARCH INDIVIDUAL ASSIGNMENT

considered to be a part of the benefits received from it. Similarly, the marketing expenses are

also not to be included in the intangible assets earned by the company.

RESEARCH INDIVIDUAL ASSIGNMENT

considered to be a part of the benefits received from it. Similarly, the marketing expenses are

also not to be included in the intangible assets earned by the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

RESEARCH INDIVIDUAL ASSIGNMENT

References

AASB, C.A.S., 2014. Business Combinations. Disclosure, 66, p.77.

AASB, C.A.S., 2015. Intangible Assets.

Bugeja, M. and Loyeung, A., 2015. What drives the allocation of the purchase price to

goodwill?. Journal of Contemporary Accounting & Economics, 11(3), pp.245-261.

Hu, F., Percy, M. and Yao, D., 2015. Asset revaluations and earnings management: Evidence

from Australian companies. Corporate Ownership and Control, 13(1), pp.930-939.

Kung, F.H., James, K., Cheng, C.L. and Jaafar, S.B., 2013. The Association between Goodwill

Amortisation and the Dividend Payout Ratio. AJBA, 6(2).

Russell, M., 2014. Capitalization of intangible assets and firm performance. The University of

Queensland, pp.1-67.

Russell, M., 2017. Management incentives to recognise intangible assets. Accounting &

Finance, 57, pp.211-234.

Standard, I.A., 2015. Presentation of Financial Statements. Balance Sheet, 54, p.80A.

Steele, N., 2015. Accounting: Get the numbers right. Company Director, 31(5), p.41.

Steenkamp, N. and Steenkamp, S., 2016. AASB 138: catalyst for managerial decisions reducing

R&D spending?. Journal of Financial Reporting and Accounting.

Steenkamp, N.S.S., Journal of Financial Reporting and Accounting.

RESEARCH INDIVIDUAL ASSIGNMENT

References

AASB, C.A.S., 2014. Business Combinations. Disclosure, 66, p.77.

AASB, C.A.S., 2015. Intangible Assets.

Bugeja, M. and Loyeung, A., 2015. What drives the allocation of the purchase price to

goodwill?. Journal of Contemporary Accounting & Economics, 11(3), pp.245-261.

Hu, F., Percy, M. and Yao, D., 2015. Asset revaluations and earnings management: Evidence

from Australian companies. Corporate Ownership and Control, 13(1), pp.930-939.

Kung, F.H., James, K., Cheng, C.L. and Jaafar, S.B., 2013. The Association between Goodwill

Amortisation and the Dividend Payout Ratio. AJBA, 6(2).

Russell, M., 2014. Capitalization of intangible assets and firm performance. The University of

Queensland, pp.1-67.

Russell, M., 2017. Management incentives to recognise intangible assets. Accounting &

Finance, 57, pp.211-234.

Standard, I.A., 2015. Presentation of Financial Statements. Balance Sheet, 54, p.80A.

Steele, N., 2015. Accounting: Get the numbers right. Company Director, 31(5), p.41.

Steenkamp, N. and Steenkamp, S., 2016. AASB 138: catalyst for managerial decisions reducing

R&D spending?. Journal of Financial Reporting and Accounting.

Steenkamp, N.S.S., Journal of Financial Reporting and Accounting.

11

RESEARCH INDIVIDUAL ASSIGNMENT

Su, W.H. and Wells, P., 2018. Acquisition premiums and the recognition of identifiable

intangible assets in business combinations pre-and post-IFRS adoption. Accounting Research

Journal.

RESEARCH INDIVIDUAL ASSIGNMENT

Su, W.H. and Wells, P., 2018. Acquisition premiums and the recognition of identifiable

intangible assets in business combinations pre-and post-IFRS adoption. Accounting Research

Journal.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.