Impact of Employee Benefit Expenses on Mahindra & Mahindra Revenue

VerifiedAdded on 2022/12/19

|20

|4703

|1

Report

AI Summary

This report examines the impact of employee benefit expenses on the financial performance of Mahindra & Mahindra. The study utilizes secondary data, primarily from the company's annual reports over an eleven-year period, to assess the correlation between employee benefit expenses and revenue generation. The research employs SPSS for data analysis, focusing on regression analysis and correlation to determine the relationship between the two variables. The findings indicate a positive relationship, suggesting that increased investment in employee benefits correlates with higher revenue. The report explores the justification for this relationship, reviews relevant literature on employee benefits and revenue, and discusses the implications for employee motivation, job satisfaction, and retention. The methodology includes a deductive research approach with an exploratory design, using secondary data analysis. The conclusion and recommendations address the importance of employee benefits for financial success, with limitations acknowledged regarding data sources and research tools.

Impact of Employee Benefit Expenses on the

Financial Performance of Business

A Study on Mahindra & Mahindra

Financial Performance of Business

A Study on Mahindra & Mahindra

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

The job satisfaction among employees has become greater concern for firms to attain

desired performance. In present research report, relationship among employee benefit expenses

and revenue of Mahindra & Mahindra has been analysed. The results are derived from SPSS

tool. It shows that as spending of firm increases in employee benefits, revenue increases at a

greater pace as well. This implies that strong correlation is found among both variables.

The job satisfaction among employees has become greater concern for firms to attain

desired performance. In present research report, relationship among employee benefit expenses

and revenue of Mahindra & Mahindra has been analysed. The results are derived from SPSS

tool. It shows that as spending of firm increases in employee benefits, revenue increases at a

greater pace as well. This implies that strong correlation is found among both variables.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Problem Statement.......................................................................................................................1

Justification..................................................................................................................................1

Research Aim and Objectives......................................................................................................1

Research Questions......................................................................................................................2

Research Hypothesis....................................................................................................................2

CRITICAL LITERATURE REVIEW.............................................................................................2

Overview of the Employee Benefit Expenses.............................................................................2

Interrelationship between revenue generation and employee benefit expenses..........................3

Impact on the motivation and employees engagement................................................................4

RESEARCH METHODOLOGY....................................................................................................4

Research Type.............................................................................................................................4

Research Approach......................................................................................................................5

Research Design..........................................................................................................................5

Data collection.............................................................................................................................5

Data Analysis...............................................................................................................................6

Research Limitations...................................................................................................................6

FINDINGS AND DATA ANALYSIS............................................................................................6

Discussion....................................................................................................................................9

CONCLUSION AND RECOMMENDATIONS............................................................................9

Conclusion...................................................................................................................................9

Recommendations......................................................................................................................10

REFERENCES..............................................................................................................................11

APPENDIX....................................................................................................................................13

INTRODUCTION...........................................................................................................................1

Problem Statement.......................................................................................................................1

Justification..................................................................................................................................1

Research Aim and Objectives......................................................................................................1

Research Questions......................................................................................................................2

Research Hypothesis....................................................................................................................2

CRITICAL LITERATURE REVIEW.............................................................................................2

Overview of the Employee Benefit Expenses.............................................................................2

Interrelationship between revenue generation and employee benefit expenses..........................3

Impact on the motivation and employees engagement................................................................4

RESEARCH METHODOLOGY....................................................................................................4

Research Type.............................................................................................................................4

Research Approach......................................................................................................................5

Research Design..........................................................................................................................5

Data collection.............................................................................................................................5

Data Analysis...............................................................................................................................6

Research Limitations...................................................................................................................6

FINDINGS AND DATA ANALYSIS............................................................................................6

Discussion....................................................................................................................................9

CONCLUSION AND RECOMMENDATIONS............................................................................9

Conclusion...................................................................................................................................9

Recommendations......................................................................................................................10

REFERENCES..............................................................................................................................11

APPENDIX....................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

The retention of skilled employees is required in today’s era for company. Better

strategies are to be implemented by companies to enhance job satisfaction and morale of

workers. Present report deals with relationship of employees benefit expenses and revenue of

company by taking secondary research. Company being chosen is Mahindra & Mahindra. For

analysing data, usage of SPSS tool is done for identifying regression analysis and correlation

between two variables. With the help of this research, business can attain desired skilled

professionals and accomplish stated goals. As employee turnover decreases, overall financial

performance of Mahindra & Mahindra will rise.

Problem Statement

In today’s competitive environment, companies are facing issues related to skilled

employee’s retention (How to Build a Competitive Employee Benefits Package. 2010). This is

evident from the fact that employee turnover has risen leading to hamper firm’s productivity

(Appelbaum, 2017). By focusing on enhancing job satisfaction and retention of employees,

turnover will eventually deteriorate. For resolving this issue, this research is being conducted.

This falls under the relationship of employee benefit expenses and business’s revenue.

Justification

Importance of job satisfaction should be understood by company as it is the leading

indicator behind firm’s success in the market (García‐Sánchez & Noguera‐Gámez, 2018).

However, some believe that employee benefit expenses do not maximise revenue of enterprise

while, others understand that better strategies are to be implemented to increase employee’s job

satisfaction (Kristal, 2017). It can be justified that present research is undertaken to analyse

relationship among variables.

Research Aim and Objectives

Research Aim-

“To analyse the impact of employee benefit expenses on the financial performance of

business- A study on Mahindra & Mahindra”

Research Objectives-

To assess the impact of employee benefit expenses on employee’ productivity

1

The retention of skilled employees is required in today’s era for company. Better

strategies are to be implemented by companies to enhance job satisfaction and morale of

workers. Present report deals with relationship of employees benefit expenses and revenue of

company by taking secondary research. Company being chosen is Mahindra & Mahindra. For

analysing data, usage of SPSS tool is done for identifying regression analysis and correlation

between two variables. With the help of this research, business can attain desired skilled

professionals and accomplish stated goals. As employee turnover decreases, overall financial

performance of Mahindra & Mahindra will rise.

Problem Statement

In today’s competitive environment, companies are facing issues related to skilled

employee’s retention (How to Build a Competitive Employee Benefits Package. 2010). This is

evident from the fact that employee turnover has risen leading to hamper firm’s productivity

(Appelbaum, 2017). By focusing on enhancing job satisfaction and retention of employees,

turnover will eventually deteriorate. For resolving this issue, this research is being conducted.

This falls under the relationship of employee benefit expenses and business’s revenue.

Justification

Importance of job satisfaction should be understood by company as it is the leading

indicator behind firm’s success in the market (García‐Sánchez & Noguera‐Gámez, 2018).

However, some believe that employee benefit expenses do not maximise revenue of enterprise

while, others understand that better strategies are to be implemented to increase employee’s job

satisfaction (Kristal, 2017). It can be justified that present research is undertaken to analyse

relationship among variables.

Research Aim and Objectives

Research Aim-

“To analyse the impact of employee benefit expenses on the financial performance of

business- A study on Mahindra & Mahindra”

Research Objectives-

To assess the impact of employee benefit expenses on employee’ productivity

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

To ascertain how job satisfaction of workers is impacted by employee benefit expenses

To evaluate how firm’s revenue is increased by incurring employee benefit expenses

Research Questions

Q1. What is the relationship between employee benefit expenses and revenue of Mahindra &

Mahindra?

Q2. How job satisfaction is impacted by employee benefit expenses?

Research Hypothesis

The hypothesis being formulated for current research is highlighted below-

H0 (Null hypothesis)- There is negative relationship between employee benefit expenses and

business’s revenue

H1 (Alternative hypothesis) There is positive relationship between employee benefit expenses

and business’s revenue

Based on the above hypothesis, research has been conducted to find out which of the

hypothesis is selected and whether revenue is increased by incurring employee benefit expenses

or not.

CRITICAL LITERATURE REVIEW

This section focuses on the ongoing research works and other theoretical contributions in

context to a subject. Primarily it is based on the analysis part of secondary sources which are

related to findings of the methodical knowledge or the analytical survey of existing data. Herein

the subject is regards to the impact of the employee benefit expenses on the revenue generation

of Mahindra Company.

Overview of the Employee Benefit Expenses

According to Jackson, Looney & Ramnath (2017), it is clearly understandable that

benefit expenses is one of the lucrative points to attract any experienced or skilled employee.

Companies understand that the employees are the assets who must be valued and given benefits

for their growth and development. This is also important to meet with the expectations and needs

of the employees’ while taking up their services to complete the assigned tasks. Moreover,

Thompson, Gilbert & Hernandez (2012) emphasized that it acts as a protective shield to the

workers based on income protection deliverables such as medical insurance, retirement schemes,

2

To evaluate how firm’s revenue is increased by incurring employee benefit expenses

Research Questions

Q1. What is the relationship between employee benefit expenses and revenue of Mahindra &

Mahindra?

Q2. How job satisfaction is impacted by employee benefit expenses?

Research Hypothesis

The hypothesis being formulated for current research is highlighted below-

H0 (Null hypothesis)- There is negative relationship between employee benefit expenses and

business’s revenue

H1 (Alternative hypothesis) There is positive relationship between employee benefit expenses

and business’s revenue

Based on the above hypothesis, research has been conducted to find out which of the

hypothesis is selected and whether revenue is increased by incurring employee benefit expenses

or not.

CRITICAL LITERATURE REVIEW

This section focuses on the ongoing research works and other theoretical contributions in

context to a subject. Primarily it is based on the analysis part of secondary sources which are

related to findings of the methodical knowledge or the analytical survey of existing data. Herein

the subject is regards to the impact of the employee benefit expenses on the revenue generation

of Mahindra Company.

Overview of the Employee Benefit Expenses

According to Jackson, Looney & Ramnath (2017), it is clearly understandable that

benefit expenses is one of the lucrative points to attract any experienced or skilled employee.

Companies understand that the employees are the assets who must be valued and given benefits

for their growth and development. This is also important to meet with the expectations and needs

of the employees’ while taking up their services to complete the assigned tasks. Moreover,

Thompson, Gilbert & Hernandez (2012) emphasized that it acts as a protective shield to the

workers based on income protection deliverables such as medical insurance, retirement schemes,

2

involuntary unemployment income replacement, disability income replacement etc. These help

in outlining the flexibility and reliability factors between the administrations and the employees.

For instance, advance leave helps the employees to accommodate the personal emergencies that

further assist in maintaining the relations in positive way.

Alongside, Osibanjo, Adeniji, Falola & Heirsmac (2014) stated that the focus is on giving

a high level of living standards and bring a work-life balance of the taskforce. It also includes

incentives and rewards that lay the path of fulfilling the preferences, needs and requirements of

the employees. Moreover, it also improves the productivity levels and maintains the

communication channels as well. There is an unseen trust and loyalty that gets build up in the

employees’ attitude towards achieving the organizational goals and objectives. It not only

improves the potentiality in terms of economic benefits to both the employer and employees but

also emphasis on increasing the overall reputation and credibility among the competitors at both

local and global markets.

Interrelationship between revenue generation and employee benefit expenses

Novy-Marx & Rauh (2014) highlighted the focus on the recent developmental works in

the revenue generation due to the high number of employees’ benefits expenses. It is seen that

there is a positive correlation between these benefit schemes and the overall profitability of the

company. There is a direct proportionality between the amount of the pressure on the employees

to perform and reach the target on time and the estimated revenues. However, Horváthová (2012)

elucidated if the employees are given a flexible environment to work in, the results have

exceeded the estimated value whereas in the opposite environment of high-pressure levels has

resulted in terminations, resignations and a dip in the overall revenue management.

Furthermore, Adhvaryu, Chari & Sharma (2013) added that the government interventions

have played a pivotal role in making the companies especially from the private sector to be more

encouraging and understanding towards the employees’ needs. Here the government has raised

the upper limit from current 10 percent to 15 percent in the apprenticeship in order to provide

cohesive surroundings for growth and development. Regarding this, there is also an upsurge of

minimal charges on the corporate tax to relax the pressure belts and helping the job markets to

come out of the depressing zones. Therefore, the relationship is clear that positive employees’

relations through the adoption of several benefits and schemes would fetch the organization to

reach the desired economic gains of the prevailing competition.

3

in outlining the flexibility and reliability factors between the administrations and the employees.

For instance, advance leave helps the employees to accommodate the personal emergencies that

further assist in maintaining the relations in positive way.

Alongside, Osibanjo, Adeniji, Falola & Heirsmac (2014) stated that the focus is on giving

a high level of living standards and bring a work-life balance of the taskforce. It also includes

incentives and rewards that lay the path of fulfilling the preferences, needs and requirements of

the employees. Moreover, it also improves the productivity levels and maintains the

communication channels as well. There is an unseen trust and loyalty that gets build up in the

employees’ attitude towards achieving the organizational goals and objectives. It not only

improves the potentiality in terms of economic benefits to both the employer and employees but

also emphasis on increasing the overall reputation and credibility among the competitors at both

local and global markets.

Interrelationship between revenue generation and employee benefit expenses

Novy-Marx & Rauh (2014) highlighted the focus on the recent developmental works in

the revenue generation due to the high number of employees’ benefits expenses. It is seen that

there is a positive correlation between these benefit schemes and the overall profitability of the

company. There is a direct proportionality between the amount of the pressure on the employees

to perform and reach the target on time and the estimated revenues. However, Horváthová (2012)

elucidated if the employees are given a flexible environment to work in, the results have

exceeded the estimated value whereas in the opposite environment of high-pressure levels has

resulted in terminations, resignations and a dip in the overall revenue management.

Furthermore, Adhvaryu, Chari & Sharma (2013) added that the government interventions

have played a pivotal role in making the companies especially from the private sector to be more

encouraging and understanding towards the employees’ needs. Here the government has raised

the upper limit from current 10 percent to 15 percent in the apprenticeship in order to provide

cohesive surroundings for growth and development. Regarding this, there is also an upsurge of

minimal charges on the corporate tax to relax the pressure belts and helping the job markets to

come out of the depressing zones. Therefore, the relationship is clear that positive employees’

relations through the adoption of several benefits and schemes would fetch the organization to

reach the desired economic gains of the prevailing competition.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Impact on the motivation and employee’s engagement

Butts, Casper & Yang (2013) has shed light on the number of pros of giving a large pool

of schemes or benefits to the employees. The engagement levels with the motivating factor is

always on the positive side of the scale that aids in making the employees feel valuable and an

important part of the company. Additionally, the transparency and communication also get

fostered that makes the performance management more compact and effective in reaching the

optimum levels of revenues and financial gains. Their overall efforts are also in increasing

direction that helps in analysing their dedication and sincerity in attaining the expected

outcomes. With additional bonuses, incentives and rewards systems has not only promoted a

healthy competitive environment for the employees to up skill and outshine themselves but also

given a platform to maintain the desired levels. In addition to this, Kwon & Hein (2013) stated

that the employees’ benefit expenses have built a security for a better future for the people

working including their families. The medical insurance plans, retirement scheme, parental care

plans etc. have minimised the pressures on the employees and gave an assurance to overcome

any unforeseen challenge or situational crisis. Therefore, this is the catalyst that makes the

employees work with complete dedication.

RESEARCH METHODOLOGY

Research Type

The research type consists of quantitative and qualitative. As the name suggests,

qualitative data is used for determining theoretical aspect of study in hand (Bresler & Stake,

2017). However, quantitative type of research helps to ascertain numerical data, facts and figures

in effectual manner. In addition to this, present research is based on relationship between

employee benefit expenses and revenue of Mahindra & Mahindra. In order to perform this

research, quantitative research has been used by taking facts and figures on last eleven years

data. This means that relationship is of quantitative in nature and adequate results can be

obtained from it.

4

Butts, Casper & Yang (2013) has shed light on the number of pros of giving a large pool

of schemes or benefits to the employees. The engagement levels with the motivating factor is

always on the positive side of the scale that aids in making the employees feel valuable and an

important part of the company. Additionally, the transparency and communication also get

fostered that makes the performance management more compact and effective in reaching the

optimum levels of revenues and financial gains. Their overall efforts are also in increasing

direction that helps in analysing their dedication and sincerity in attaining the expected

outcomes. With additional bonuses, incentives and rewards systems has not only promoted a

healthy competitive environment for the employees to up skill and outshine themselves but also

given a platform to maintain the desired levels. In addition to this, Kwon & Hein (2013) stated

that the employees’ benefit expenses have built a security for a better future for the people

working including their families. The medical insurance plans, retirement scheme, parental care

plans etc. have minimised the pressures on the employees and gave an assurance to overcome

any unforeseen challenge or situational crisis. Therefore, this is the catalyst that makes the

employees work with complete dedication.

RESEARCH METHODOLOGY

Research Type

The research type consists of quantitative and qualitative. As the name suggests,

qualitative data is used for determining theoretical aspect of study in hand (Bresler & Stake,

2017). However, quantitative type of research helps to ascertain numerical data, facts and figures

in effectual manner. In addition to this, present research is based on relationship between

employee benefit expenses and revenue of Mahindra & Mahindra. In order to perform this

research, quantitative research has been used by taking facts and figures on last eleven years

data. This means that relationship is of quantitative in nature and adequate results can be

obtained from it.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Research Approach

The research approaches that are used by scholars are namely inductive and deductive

research approaches. The deductive goes through stage of theory, then hypothesis is made

(Kumar, 2019). Thereafter, observation or testing of hypothesis is done in order to accept or

reject the same. While, inductive approach is particularly used for forming general theory. In

current report, use of deductive approach has been used in order to attain desirable results from

the formulated hypothesis. Thus, whether employee benefit expenses and revenue possess

relationship or not can be determined with the help of this research approach with ease.

Research Design

The research design is used for providing overall schema of the research study. It

provides proper direction to researcher in the best manner possible. It consists mainly of two

types such as descriptive design and exploratory design (Ledford & Gast, 2018). It can be

analysed that descriptive is used to describe in detail regarding the issue. However, exploratory is

used for exploring issue being identified up to a major extent and as a result; scholar can attain

outcomes. In present report, exploratory design has been used for gathering results in effective

manner. This will help in getting outcome as to what relationship prevails between revenue of

Mahindra & Mahindra and employee benefit expenses.

Data collection

The data collection can be done from two broad sources such as primary source and

secondary source. Both sources are used by scholar to attain data (Fletcher, 2017). Without

getting appropriate data in hand, study cannot be completed. In present research, scholar has

made use of secondary data only. The data is already collected from various published sources.

These are eleven years of employee benefit expense and revenue from Mahindra & Mahindra’s

annual reports (Mahindra & Mahindra annual reports. 2019). Other than this, use of books,

journals and articles published on internet are taken as well. Below is the data of company for

two variables.

Mahindra & Mahindra

Year Revenue Employee Benefit

Expenses

2009 11671.64 852.45

5

The research approaches that are used by scholars are namely inductive and deductive

research approaches. The deductive goes through stage of theory, then hypothesis is made

(Kumar, 2019). Thereafter, observation or testing of hypothesis is done in order to accept or

reject the same. While, inductive approach is particularly used for forming general theory. In

current report, use of deductive approach has been used in order to attain desirable results from

the formulated hypothesis. Thus, whether employee benefit expenses and revenue possess

relationship or not can be determined with the help of this research approach with ease.

Research Design

The research design is used for providing overall schema of the research study. It

provides proper direction to researcher in the best manner possible. It consists mainly of two

types such as descriptive design and exploratory design (Ledford & Gast, 2018). It can be

analysed that descriptive is used to describe in detail regarding the issue. However, exploratory is

used for exploring issue being identified up to a major extent and as a result; scholar can attain

outcomes. In present report, exploratory design has been used for gathering results in effective

manner. This will help in getting outcome as to what relationship prevails between revenue of

Mahindra & Mahindra and employee benefit expenses.

Data collection

The data collection can be done from two broad sources such as primary source and

secondary source. Both sources are used by scholar to attain data (Fletcher, 2017). Without

getting appropriate data in hand, study cannot be completed. In present research, scholar has

made use of secondary data only. The data is already collected from various published sources.

These are eleven years of employee benefit expense and revenue from Mahindra & Mahindra’s

annual reports (Mahindra & Mahindra annual reports. 2019). Other than this, use of books,

journals and articles published on internet are taken as well. Below is the data of company for

two variables.

Mahindra & Mahindra

Year Revenue Employee Benefit

Expenses

2009 11671.64 852.45

5

2010 18801.46 1198.47

2011 23894.41 1431.52

2012 32319.31 1701.78

2013 40990.33 1866.45

2014 74506.02 2163.72

2015 39293.77 2317.00

2016 41739.83 2342.00

2017 47093.04 2595.00

2018 49444.99 2840.39

2019 53614.00 2980.22

Data Analysis

The data analysis is the last step in research methodology being used for carrying out

result by interpreting the same. There are various tools available for analysing data. However, in

present report, use of SPSS has been done offering wide range of aspects regarding the two

variables. This provides clarity regarding the relationship among variables is positive or negative

(Quinlan et.al, 2019). Hence, with the help of SPSS tool, scholar becomes able to attain best

results as authentic results are accomplished.

Research Limitations

The research limitations can be analysed as well. It can be assessed that though SPSS tool

has been used in present research, use of other tools could be made as well. Apart from this,

scholar has made use of secondary sources and not primary sources. On the other hand, literature

review has been written from previous researchers (Chen, Hung & Wang, 2018). It might be that

lack of previous studies could hinder in getting righteous results. Hence, besides these

limitations, research has accomplished results what we are being expected.

FINDINGS AND DATA ANALYSIS

1. Descriptive Statistics

Descriptive Statistics

N Minimum Maximum Mean Std. Deviation

Revenue 11 11671.64 74506.02 39397.1636 17567.84439

Employee_Benefit_Expense

s

11 852.45 2980.22 2026.2727 681.69184

6

2011 23894.41 1431.52

2012 32319.31 1701.78

2013 40990.33 1866.45

2014 74506.02 2163.72

2015 39293.77 2317.00

2016 41739.83 2342.00

2017 47093.04 2595.00

2018 49444.99 2840.39

2019 53614.00 2980.22

Data Analysis

The data analysis is the last step in research methodology being used for carrying out

result by interpreting the same. There are various tools available for analysing data. However, in

present report, use of SPSS has been done offering wide range of aspects regarding the two

variables. This provides clarity regarding the relationship among variables is positive or negative

(Quinlan et.al, 2019). Hence, with the help of SPSS tool, scholar becomes able to attain best

results as authentic results are accomplished.

Research Limitations

The research limitations can be analysed as well. It can be assessed that though SPSS tool

has been used in present research, use of other tools could be made as well. Apart from this,

scholar has made use of secondary sources and not primary sources. On the other hand, literature

review has been written from previous researchers (Chen, Hung & Wang, 2018). It might be that

lack of previous studies could hinder in getting righteous results. Hence, besides these

limitations, research has accomplished results what we are being expected.

FINDINGS AND DATA ANALYSIS

1. Descriptive Statistics

Descriptive Statistics

N Minimum Maximum Mean Std. Deviation

Revenue 11 11671.64 74506.02 39397.1636 17567.84439

Employee_Benefit_Expense

s

11 852.45 2980.22 2026.2727 681.69184

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

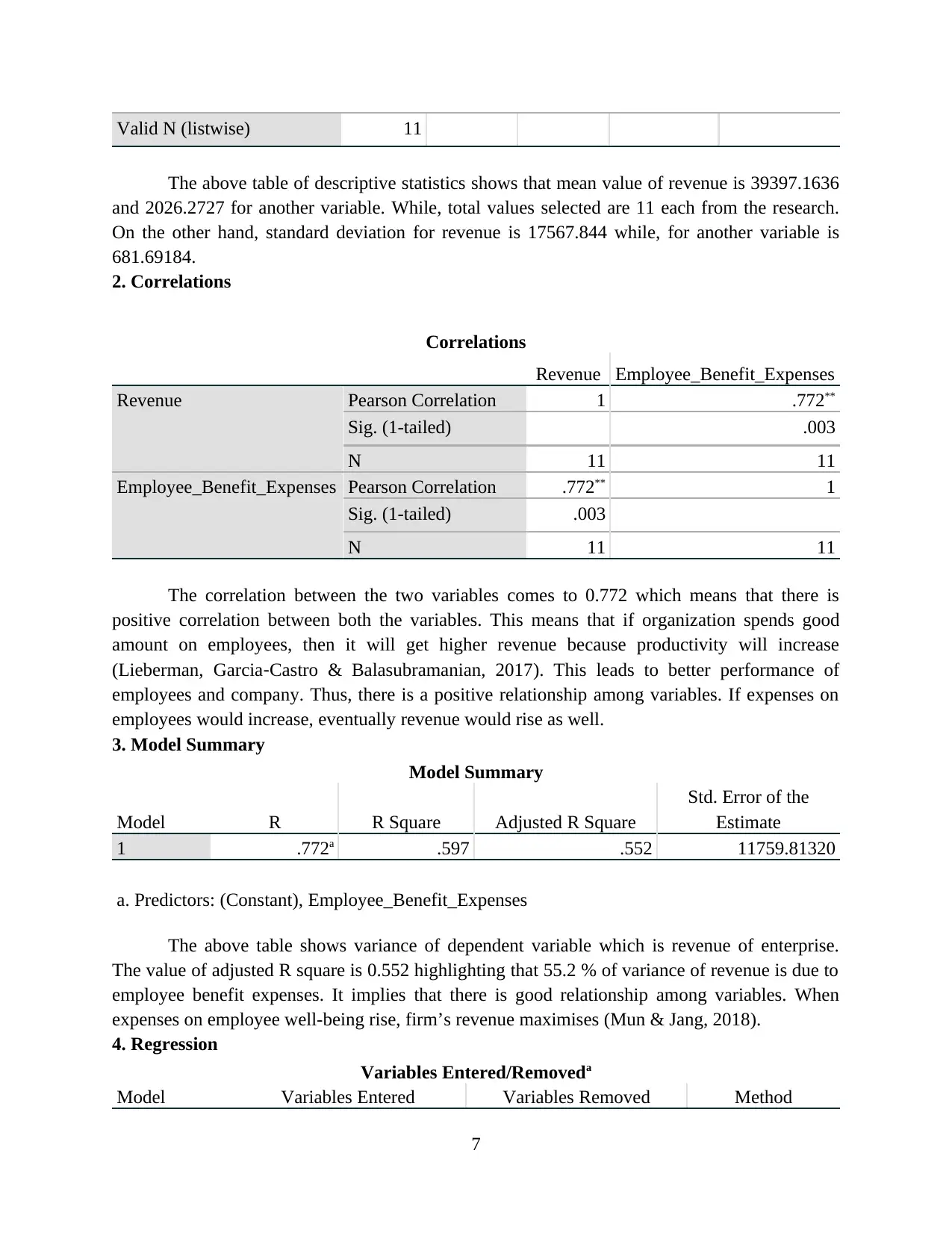

Valid N (listwise) 11

The above table of descriptive statistics shows that mean value of revenue is 39397.1636

and 2026.2727 for another variable. While, total values selected are 11 each from the research.

On the other hand, standard deviation for revenue is 17567.844 while, for another variable is

681.69184.

2. Correlations

Correlations

Revenue Employee_Benefit_Expenses

Revenue Pearson Correlation 1 .772**

Sig. (1-tailed) .003

N 11 11

Employee_Benefit_Expenses Pearson Correlation .772** 1

Sig. (1-tailed) .003

N 11 11

The correlation between the two variables comes to 0.772 which means that there is

positive correlation between both the variables. This means that if organization spends good

amount on employees, then it will get higher revenue because productivity will increase

(Lieberman, Garcia‐Castro & Balasubramanian, 2017). This leads to better performance of

employees and company. Thus, there is a positive relationship among variables. If expenses on

employees would increase, eventually revenue would rise as well.

3. Model Summary

Model Summary

Model R R Square Adjusted R Square

Std. Error of the

Estimate

1 .772a .597 .552 11759.81320

a. Predictors: (Constant), Employee_Benefit_Expenses

The above table shows variance of dependent variable which is revenue of enterprise.

The value of adjusted R square is 0.552 highlighting that 55.2 % of variance of revenue is due to

employee benefit expenses. It implies that there is good relationship among variables. When

expenses on employee well-being rise, firm’s revenue maximises (Mun & Jang, 2018).

4. Regression

Variables Entered/Removeda

Model Variables Entered Variables Removed Method

7

The above table of descriptive statistics shows that mean value of revenue is 39397.1636

and 2026.2727 for another variable. While, total values selected are 11 each from the research.

On the other hand, standard deviation for revenue is 17567.844 while, for another variable is

681.69184.

2. Correlations

Correlations

Revenue Employee_Benefit_Expenses

Revenue Pearson Correlation 1 .772**

Sig. (1-tailed) .003

N 11 11

Employee_Benefit_Expenses Pearson Correlation .772** 1

Sig. (1-tailed) .003

N 11 11

The correlation between the two variables comes to 0.772 which means that there is

positive correlation between both the variables. This means that if organization spends good

amount on employees, then it will get higher revenue because productivity will increase

(Lieberman, Garcia‐Castro & Balasubramanian, 2017). This leads to better performance of

employees and company. Thus, there is a positive relationship among variables. If expenses on

employees would increase, eventually revenue would rise as well.

3. Model Summary

Model Summary

Model R R Square Adjusted R Square

Std. Error of the

Estimate

1 .772a .597 .552 11759.81320

a. Predictors: (Constant), Employee_Benefit_Expenses

The above table shows variance of dependent variable which is revenue of enterprise.

The value of adjusted R square is 0.552 highlighting that 55.2 % of variance of revenue is due to

employee benefit expenses. It implies that there is good relationship among variables. When

expenses on employee well-being rise, firm’s revenue maximises (Mun & Jang, 2018).

4. Regression

Variables Entered/Removeda

Model Variables Entered Variables Removed Method

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

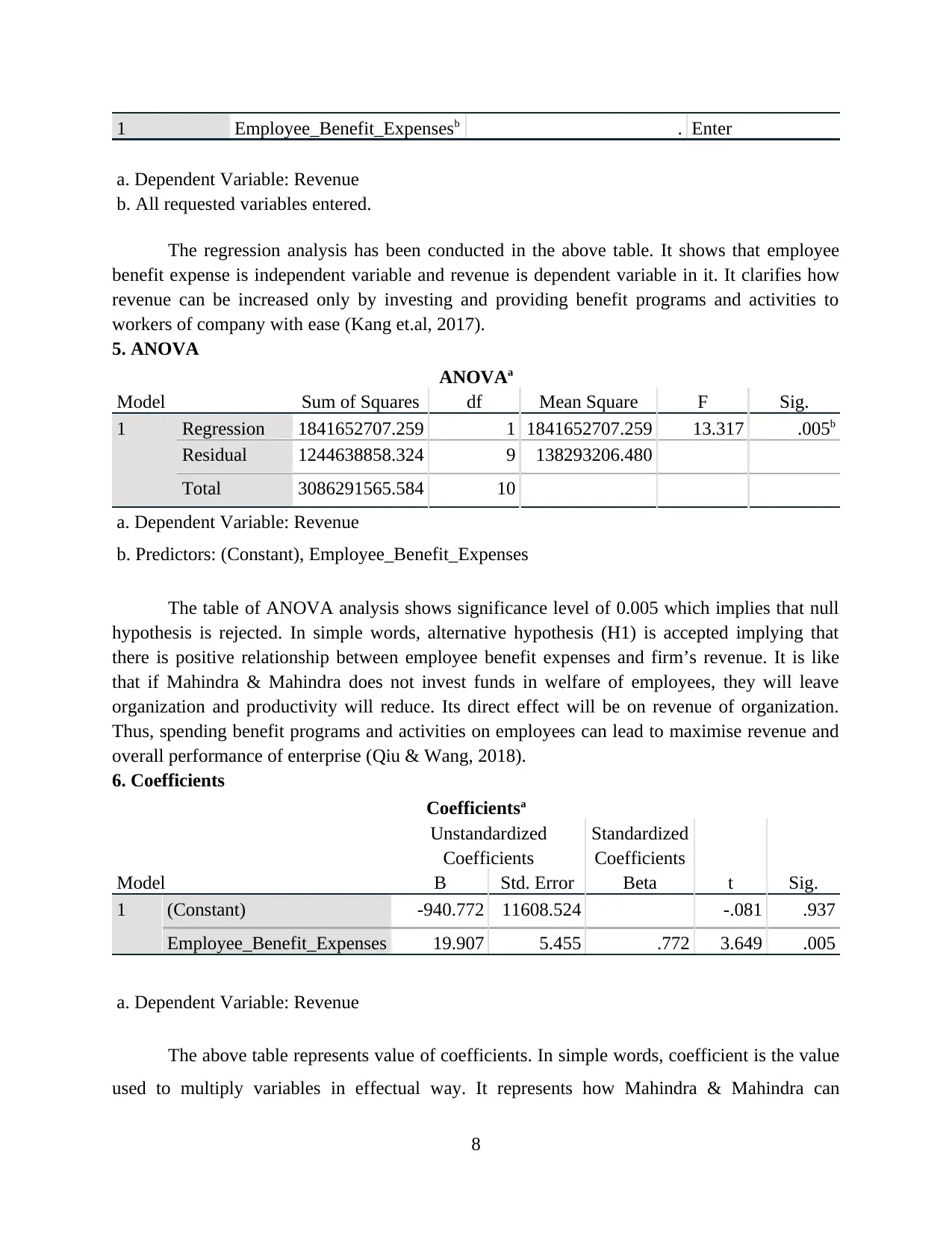

1 Employee_Benefit_Expensesb . Enter

a. Dependent Variable: Revenue

b. All requested variables entered.

The regression analysis has been conducted in the above table. It shows that employee

benefit expense is independent variable and revenue is dependent variable in it. It clarifies how

revenue can be increased only by investing and providing benefit programs and activities to

workers of company with ease (Kang et.al, 2017).

5. ANOVA

ANOVAa

Model Sum of Squares df Mean Square F Sig.

1 Regression 1841652707.259 1 1841652707.259 13.317 .005b

Residual 1244638858.324 9 138293206.480

Total 3086291565.584 10

a. Dependent Variable: Revenue

b. Predictors: (Constant), Employee_Benefit_Expenses

The table of ANOVA analysis shows significance level of 0.005 which implies that null

hypothesis is rejected. In simple words, alternative hypothesis (H1) is accepted implying that

there is positive relationship between employee benefit expenses and firm’s revenue. It is like

that if Mahindra & Mahindra does not invest funds in welfare of employees, they will leave

organization and productivity will reduce. Its direct effect will be on revenue of organization.

Thus, spending benefit programs and activities on employees can lead to maximise revenue and

overall performance of enterprise (Qiu & Wang, 2018).

6. Coefficients

Coefficientsa

Model

Unstandardized

Coefficients

Standardized

Coefficients

t Sig.B Std. Error Beta

1 (Constant) -940.772 11608.524 -.081 .937

Employee_Benefit_Expenses 19.907 5.455 .772 3.649 .005

a. Dependent Variable: Revenue

The above table represents value of coefficients. In simple words, coefficient is the value

used to multiply variables in effectual way. It represents how Mahindra & Mahindra can

8

a. Dependent Variable: Revenue

b. All requested variables entered.

The regression analysis has been conducted in the above table. It shows that employee

benefit expense is independent variable and revenue is dependent variable in it. It clarifies how

revenue can be increased only by investing and providing benefit programs and activities to

workers of company with ease (Kang et.al, 2017).

5. ANOVA

ANOVAa

Model Sum of Squares df Mean Square F Sig.

1 Regression 1841652707.259 1 1841652707.259 13.317 .005b

Residual 1244638858.324 9 138293206.480

Total 3086291565.584 10

a. Dependent Variable: Revenue

b. Predictors: (Constant), Employee_Benefit_Expenses

The table of ANOVA analysis shows significance level of 0.005 which implies that null

hypothesis is rejected. In simple words, alternative hypothesis (H1) is accepted implying that

there is positive relationship between employee benefit expenses and firm’s revenue. It is like

that if Mahindra & Mahindra does not invest funds in welfare of employees, they will leave

organization and productivity will reduce. Its direct effect will be on revenue of organization.

Thus, spending benefit programs and activities on employees can lead to maximise revenue and

overall performance of enterprise (Qiu & Wang, 2018).

6. Coefficients

Coefficientsa

Model

Unstandardized

Coefficients

Standardized

Coefficients

t Sig.B Std. Error Beta

1 (Constant) -940.772 11608.524 -.081 .937

Employee_Benefit_Expenses 19.907 5.455 .772 3.649 .005

a. Dependent Variable: Revenue

The above table represents value of coefficients. In simple words, coefficient is the value

used to multiply variables in effectual way. It represents how Mahindra & Mahindra can

8

accomplish higher gains in terms of good financial performance by investing on employees’

welfare. The value of significance level for independent variable is 0.005 which means that

dependent variable revenue cannot increase when employee benefit expenses are not maximised.

Hence, value of coefficient also interprets that there is strong relationship among variables. Thus,

firm must invest in employees for reaping higher revenues quite comfortably.

Discussion

The data analysis has been done with results being analysed and interpreted as per the

output gained by the SPSS tool. It shows that by making good investment in employees, firm can

increase its productivity, retain skilful employees, reduce employee turnover and as a result,

attain higher quantum of revenues (Ibrahim & Jebur, 2019). The job satisfaction is maximised

when employee seeks that firm is investing in his/her welfare for better growth. They become

committed to their work and thus, performance increases and company’s revenue soars high.

Moreover, they become loyal to company and they are motivated to perform even better out of

their potentials (Knox, 2018).

In addition to this, data analysis and results provide clarity that H1 is accepted as there is

a positive relationship between revenue of Mahindra & Mahindra and employee benefit

expenses. As per the annual report, company is constantly incurring higher expenses on

employees and simultaneously, revenue is maximising at great extent. The value of correlation is

0.772 which highlights positive relation between them. Thus, it shows that investing on

employees will surely reap higher financial performance for firm.

CONCLUSION AND RECOMMENDATIONS

Conclusion

Hereby it can be concluded that incurring expenses on employees leads to attainment of

higher financial performance of company quite effectively. Employees are main and integral part

of every organization and without providing benefits and related programs for them, they will

not get satisfied. If they are unsatisfied, they will leave jobs. It then results into decreased

productivity and as a result, revenue and overall performance is decreased. By increasing

employee benefit expense, Mahindra & Mahindra can effectively maximise its revenue and

become leader in the market. This will also help to lower employee turnover and thus, employees

can be retained as well.

9

welfare. The value of significance level for independent variable is 0.005 which means that

dependent variable revenue cannot increase when employee benefit expenses are not maximised.

Hence, value of coefficient also interprets that there is strong relationship among variables. Thus,

firm must invest in employees for reaping higher revenues quite comfortably.

Discussion

The data analysis has been done with results being analysed and interpreted as per the

output gained by the SPSS tool. It shows that by making good investment in employees, firm can

increase its productivity, retain skilful employees, reduce employee turnover and as a result,

attain higher quantum of revenues (Ibrahim & Jebur, 2019). The job satisfaction is maximised

when employee seeks that firm is investing in his/her welfare for better growth. They become

committed to their work and thus, performance increases and company’s revenue soars high.

Moreover, they become loyal to company and they are motivated to perform even better out of

their potentials (Knox, 2018).

In addition to this, data analysis and results provide clarity that H1 is accepted as there is

a positive relationship between revenue of Mahindra & Mahindra and employee benefit

expenses. As per the annual report, company is constantly incurring higher expenses on

employees and simultaneously, revenue is maximising at great extent. The value of correlation is

0.772 which highlights positive relation between them. Thus, it shows that investing on

employees will surely reap higher financial performance for firm.

CONCLUSION AND RECOMMENDATIONS

Conclusion

Hereby it can be concluded that incurring expenses on employees leads to attainment of

higher financial performance of company quite effectively. Employees are main and integral part

of every organization and without providing benefits and related programs for them, they will

not get satisfied. If they are unsatisfied, they will leave jobs. It then results into decreased

productivity and as a result, revenue and overall performance is decreased. By increasing

employee benefit expense, Mahindra & Mahindra can effectively maximise its revenue and

become leader in the market. This will also help to lower employee turnover and thus, employees

can be retained as well.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.