Make or Buy Decisions Report

VerifiedAdded on 2019/11/25

|10

|1220

|375

Report

AI Summary

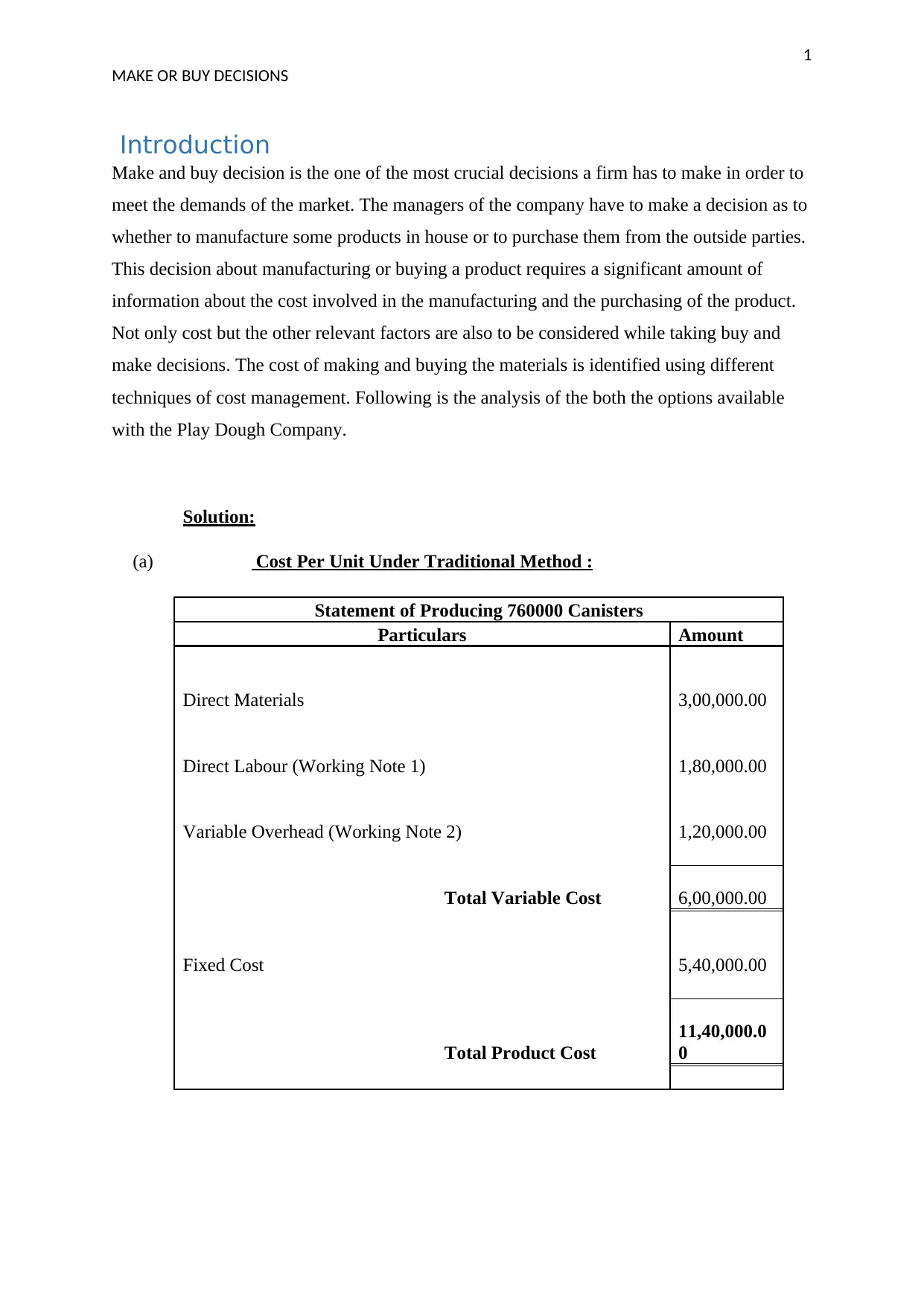

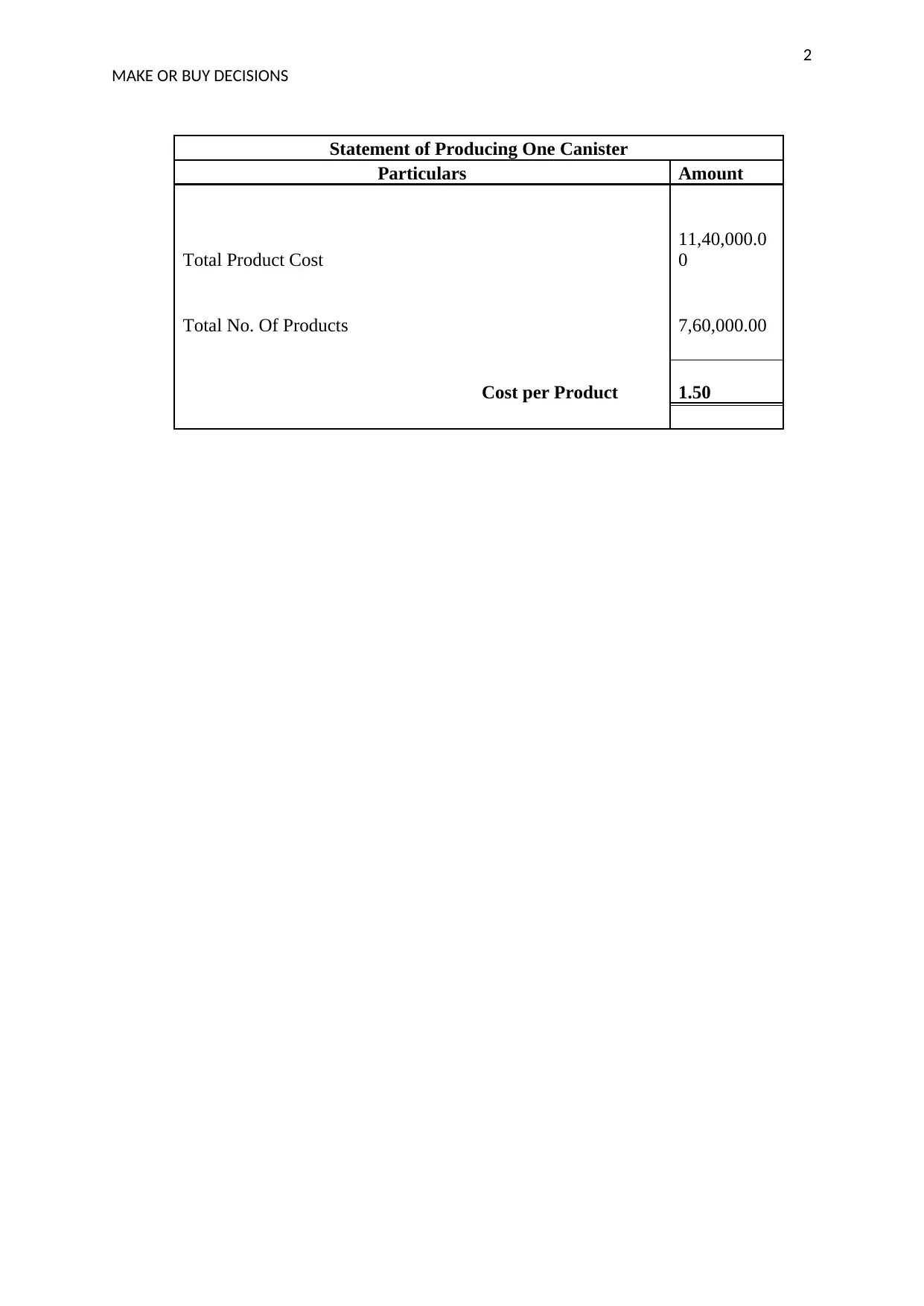

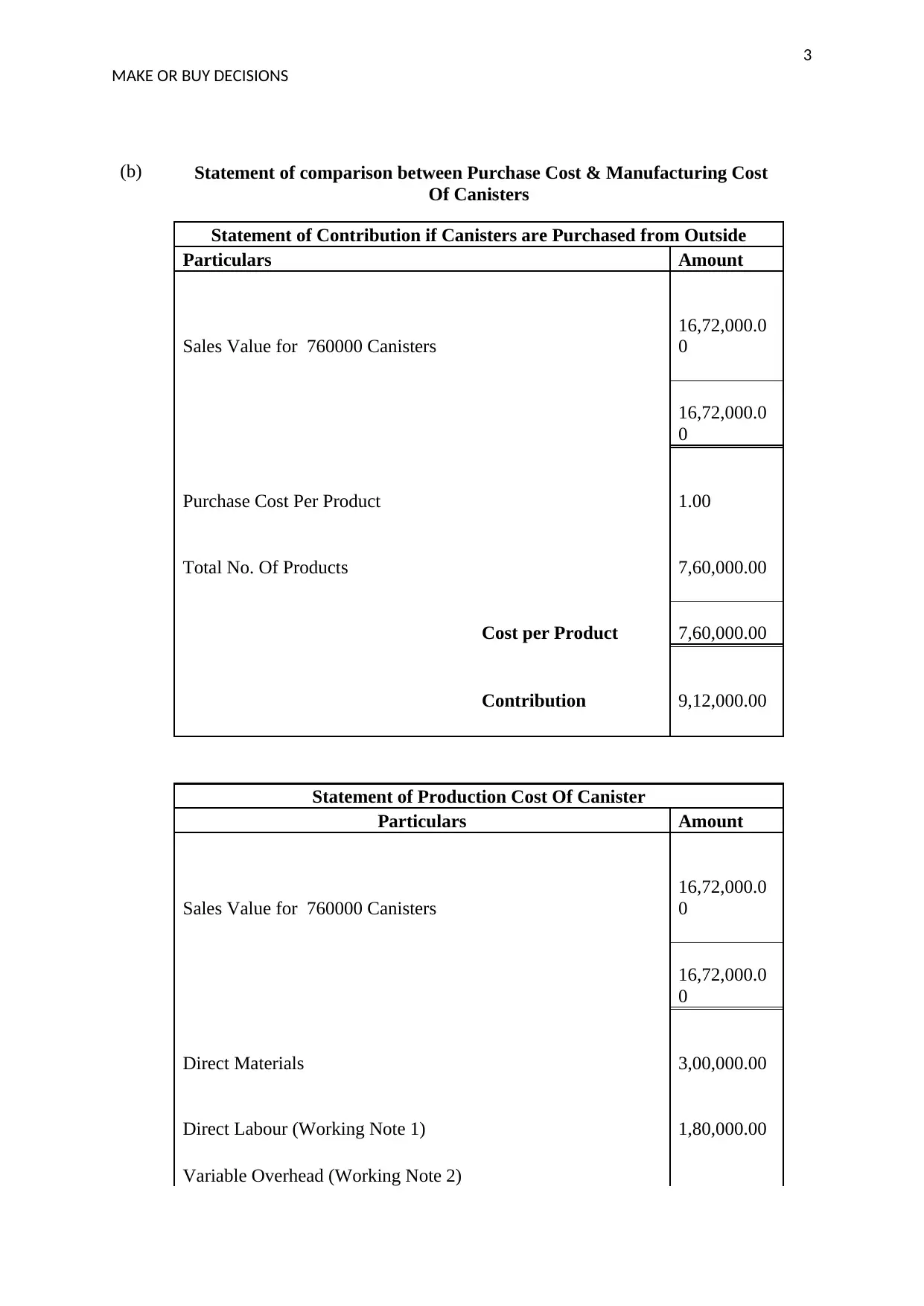

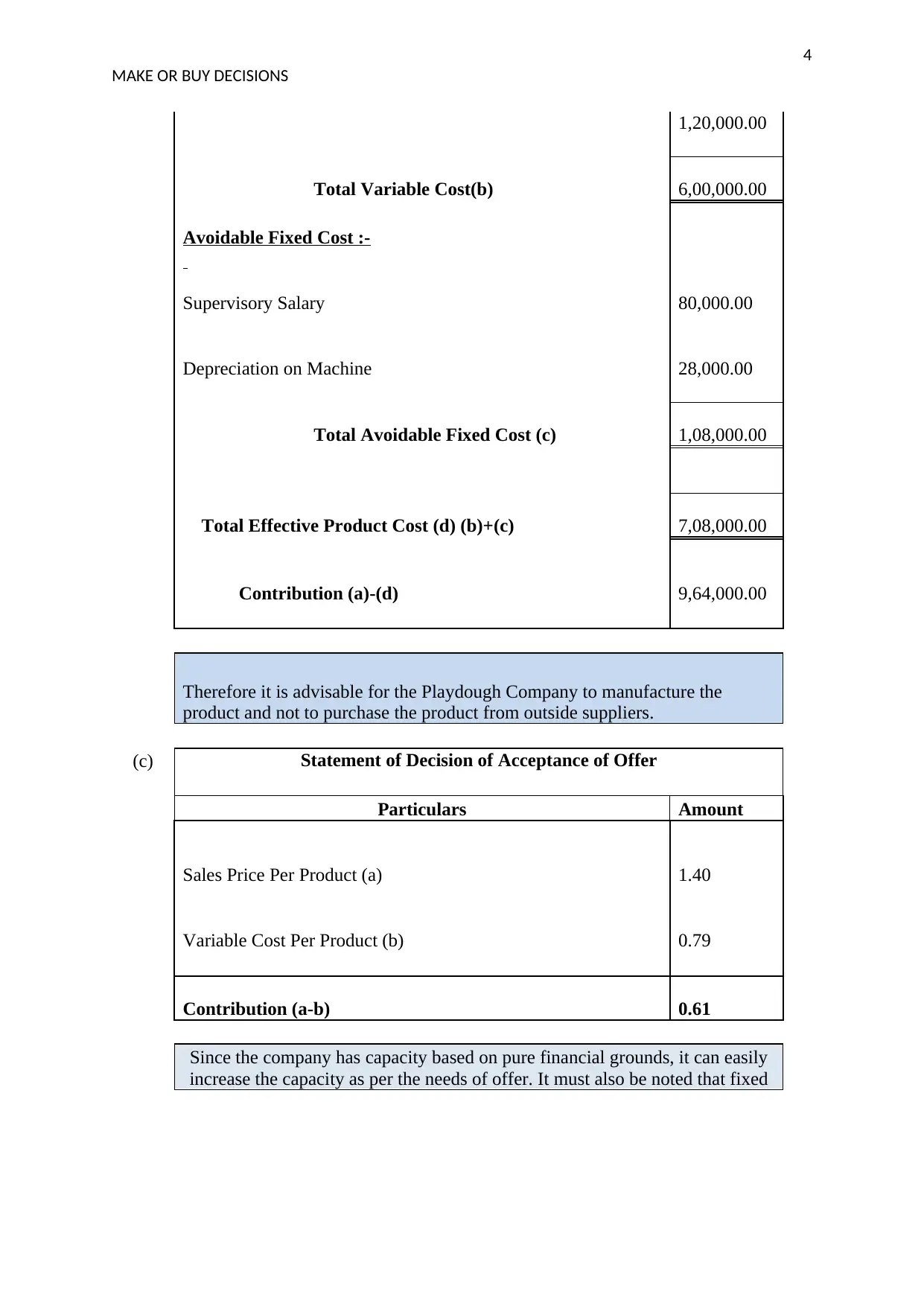

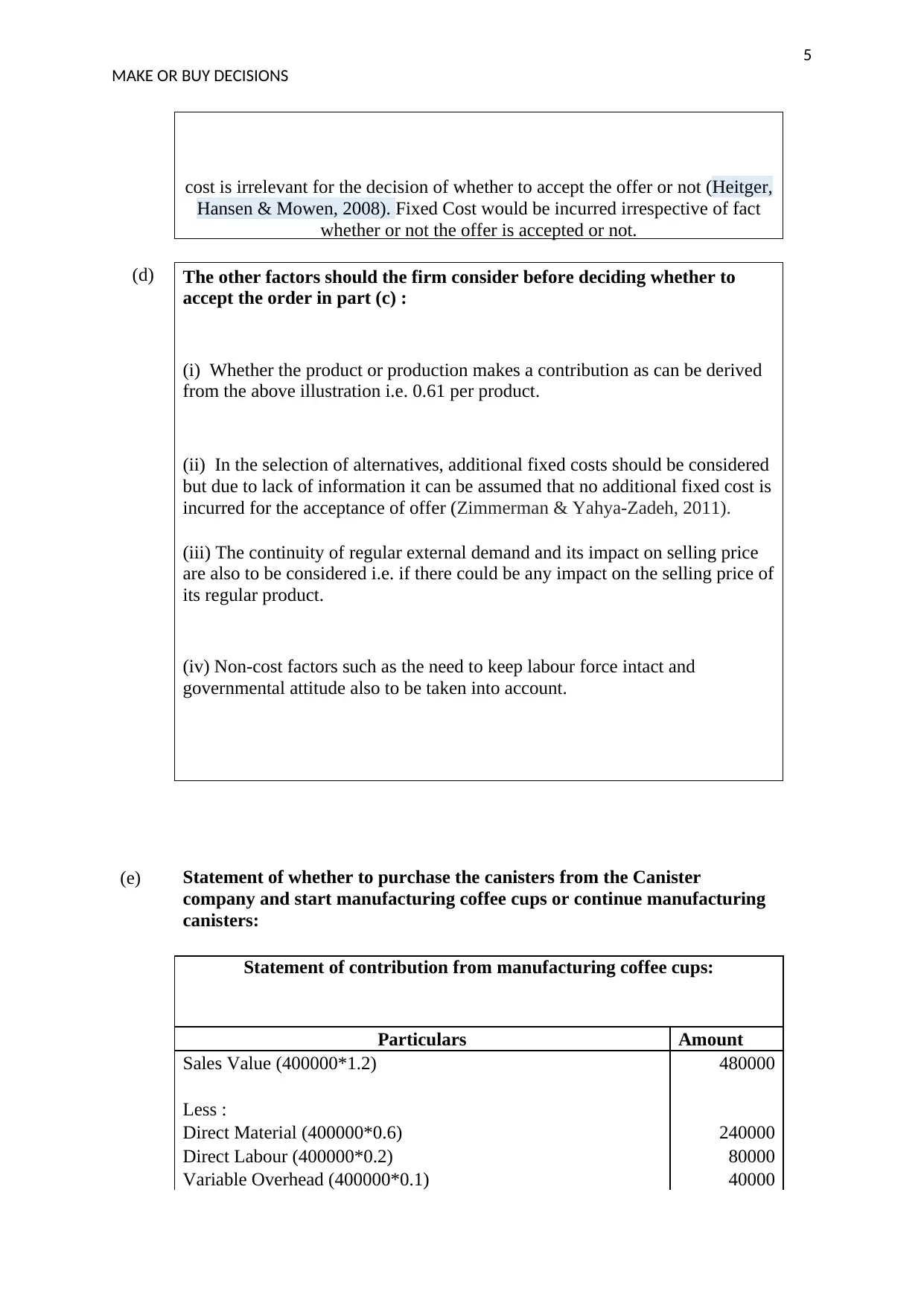

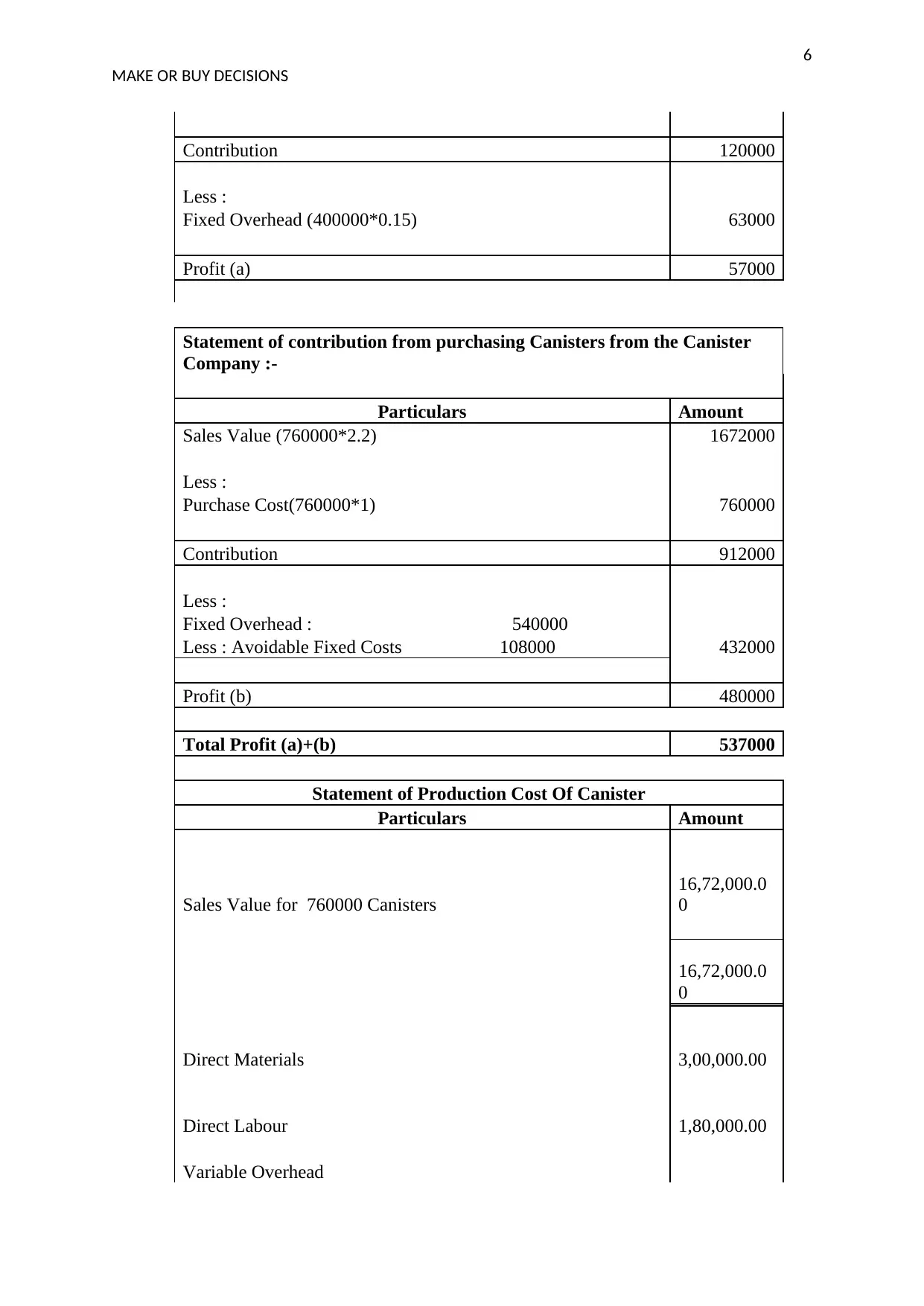

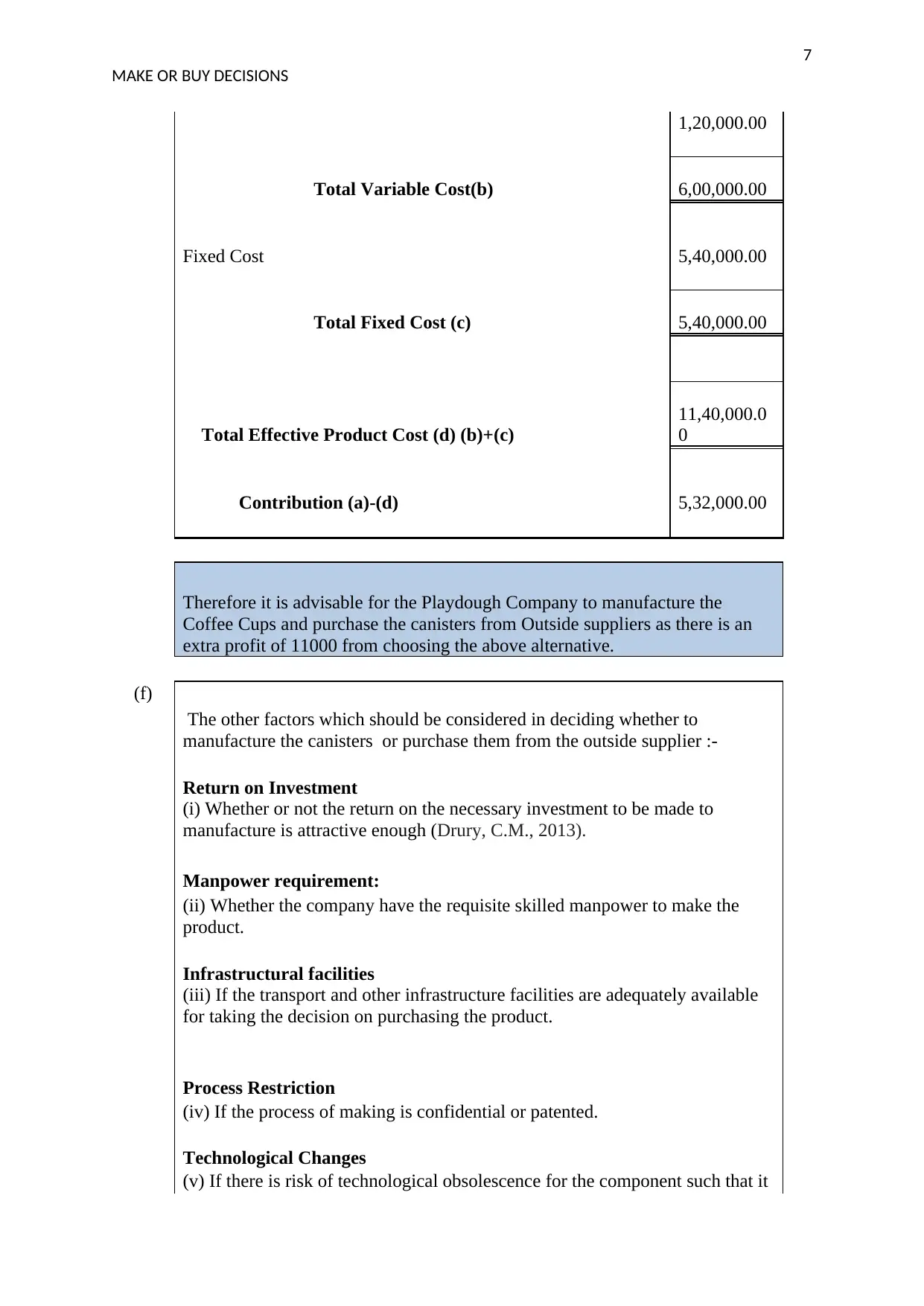

This report provides a detailed analysis of make-or-buy decisions for the Play Dough Company. It compares the cost of manufacturing canisters in-house versus purchasing them from external suppliers. The analysis includes a breakdown of direct materials, direct labor, variable overhead, and fixed costs. The report also considers the impact of accepting a special order for coffee cups and the implications of purchasing canisters from an external supplier while manufacturing coffee cups. Furthermore, it discusses non-cost factors such as manpower requirements, infrastructural facilities, process restrictions, technological changes, and the quality of goods supplied by external suppliers. The conclusion emphasizes the importance of considering both cost and non-cost factors when making make-or-buy decisions and suggests that the company should use advanced cost identification methods for a more accurate assessment.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.