Detailed Audit Program for Mako Gold Limited Financial Review

VerifiedAdded on 2023/01/19

|20

|985

|58

Report

AI Summary

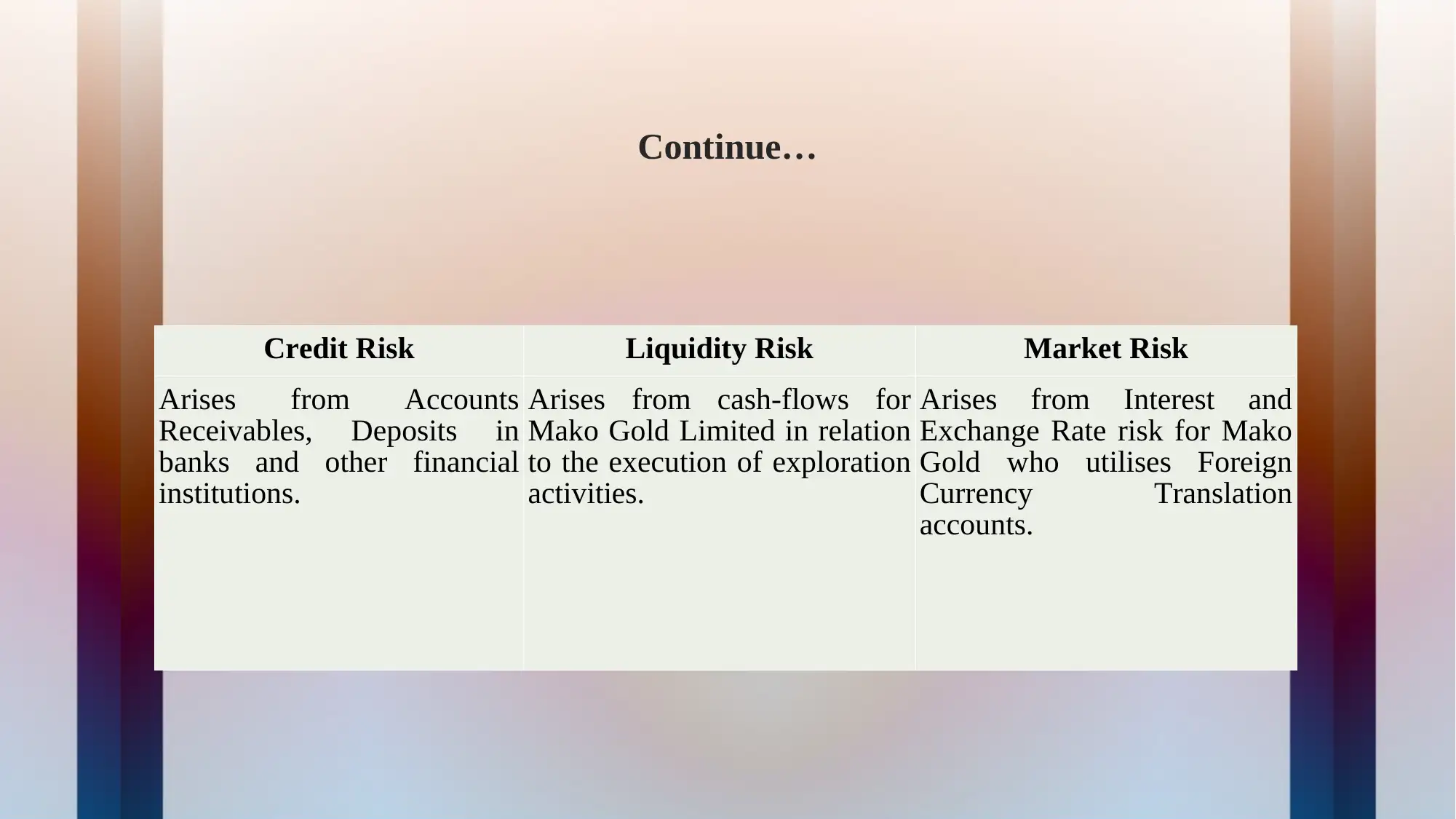

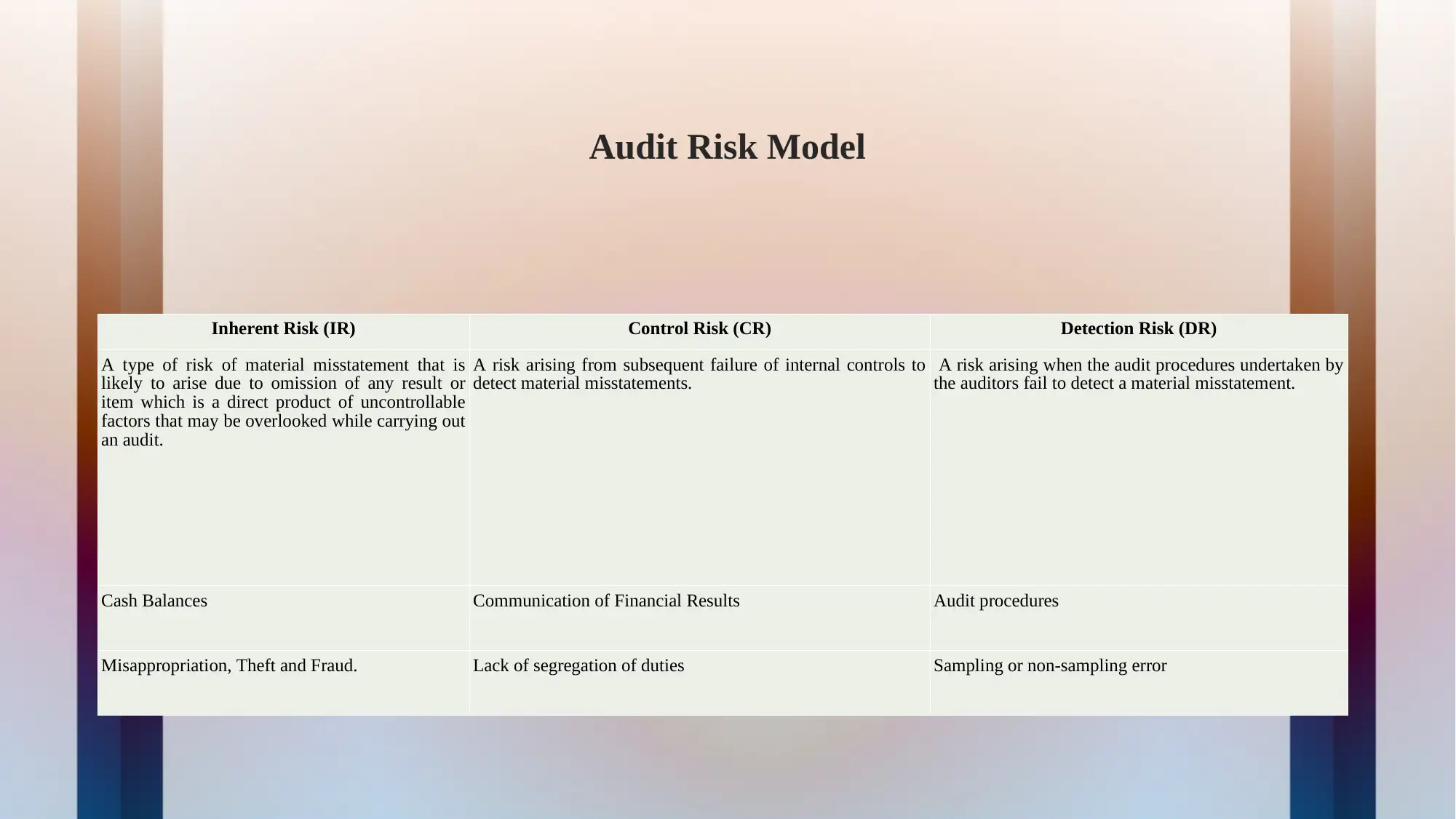

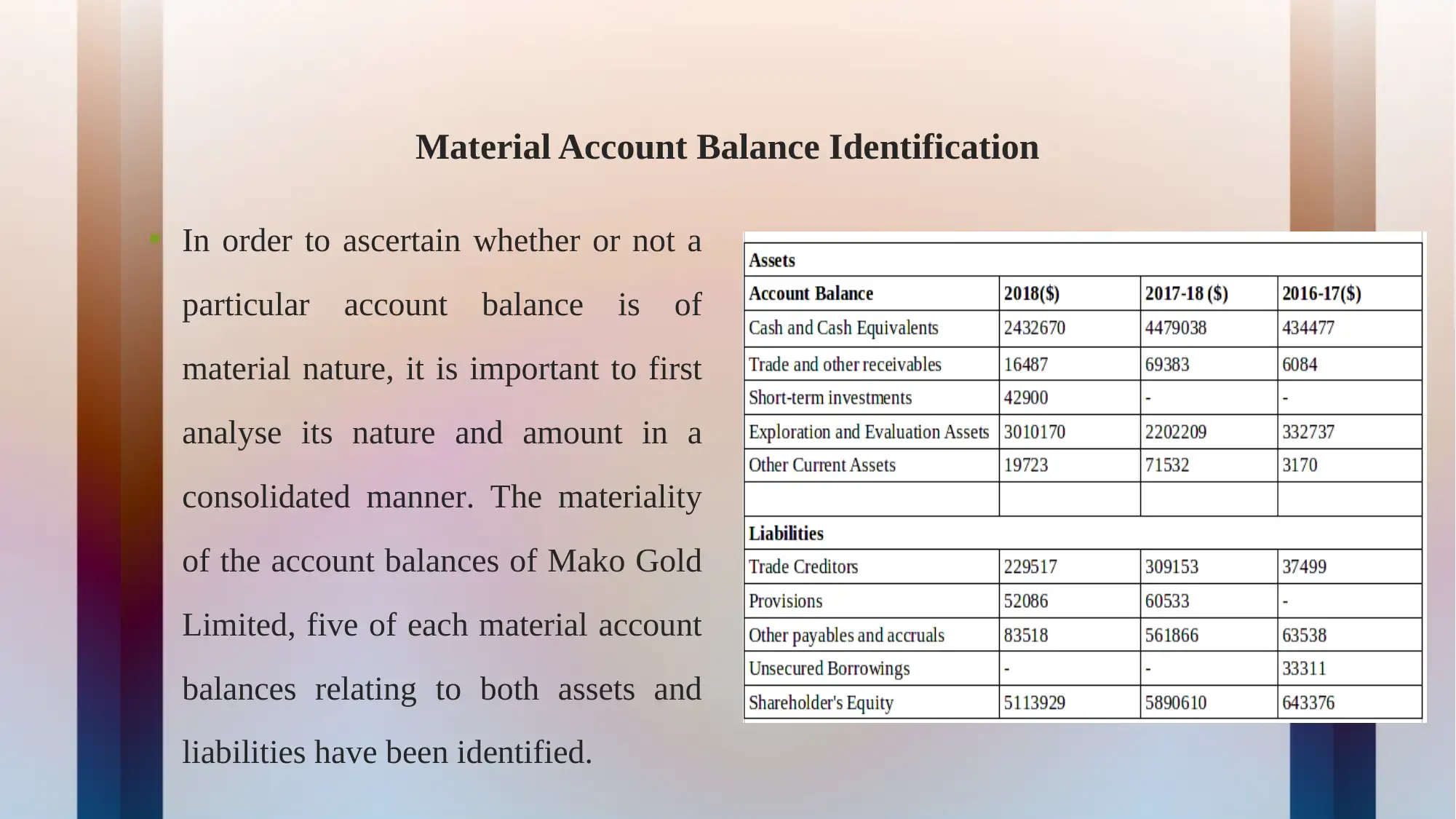

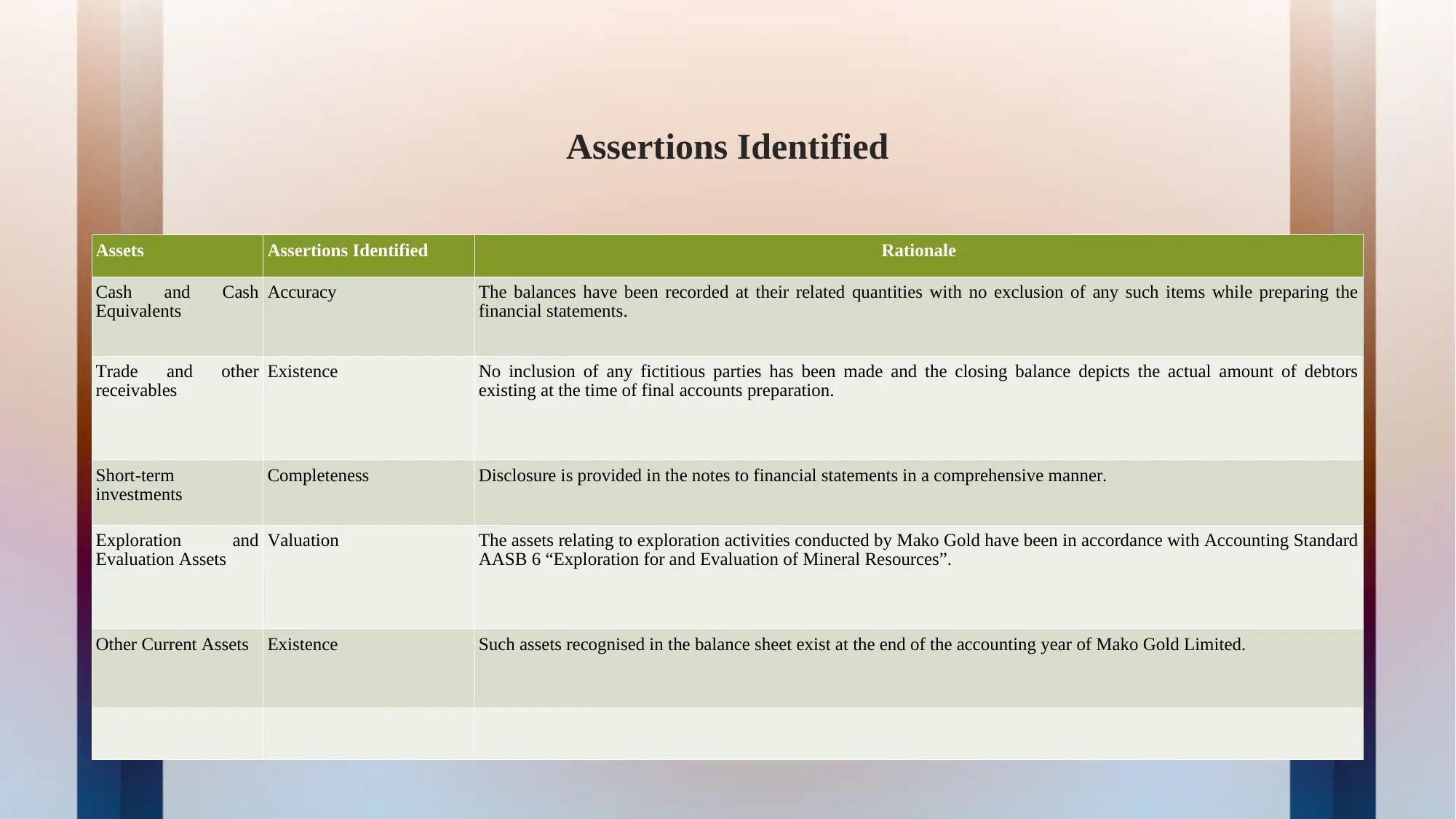

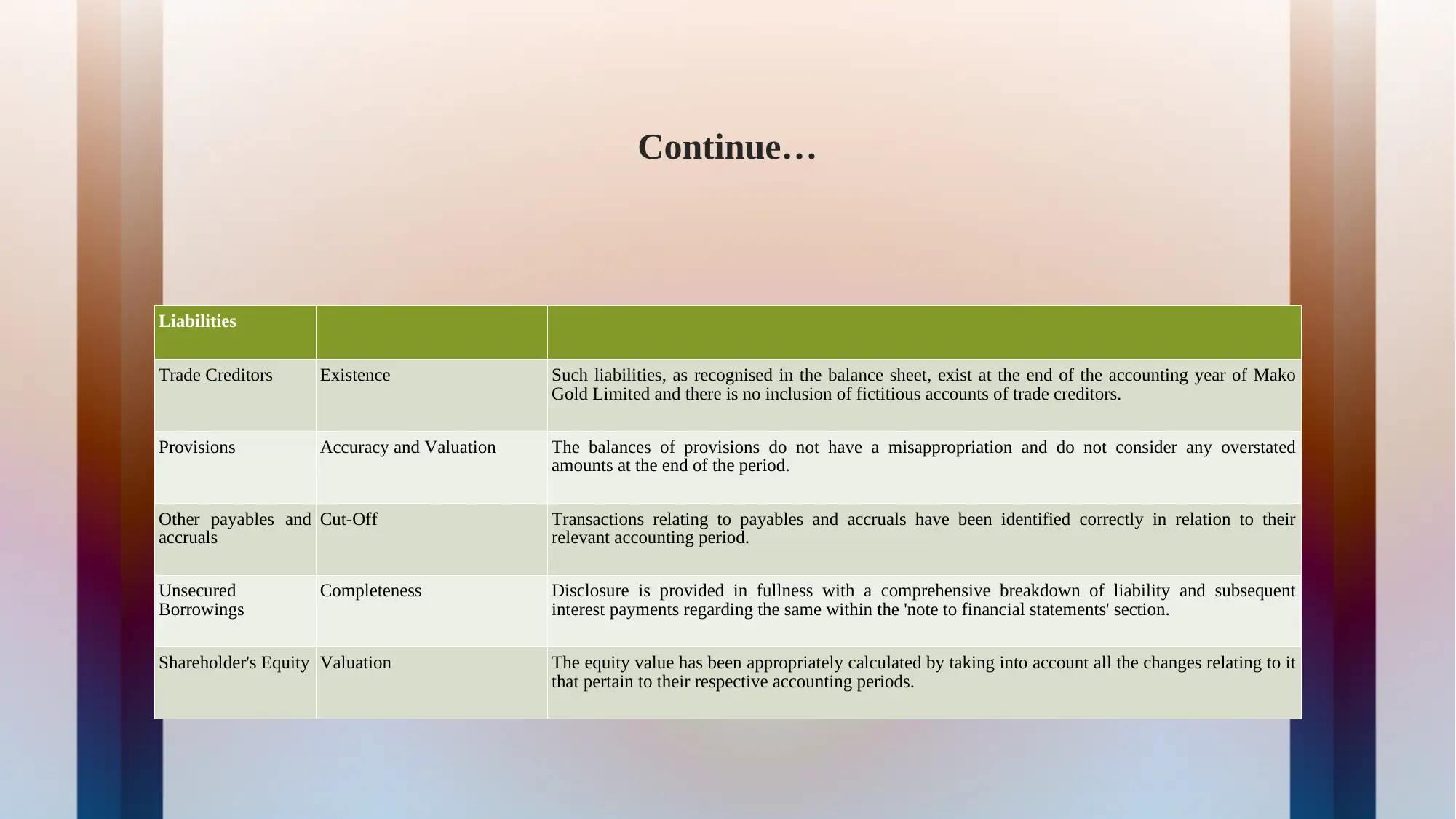

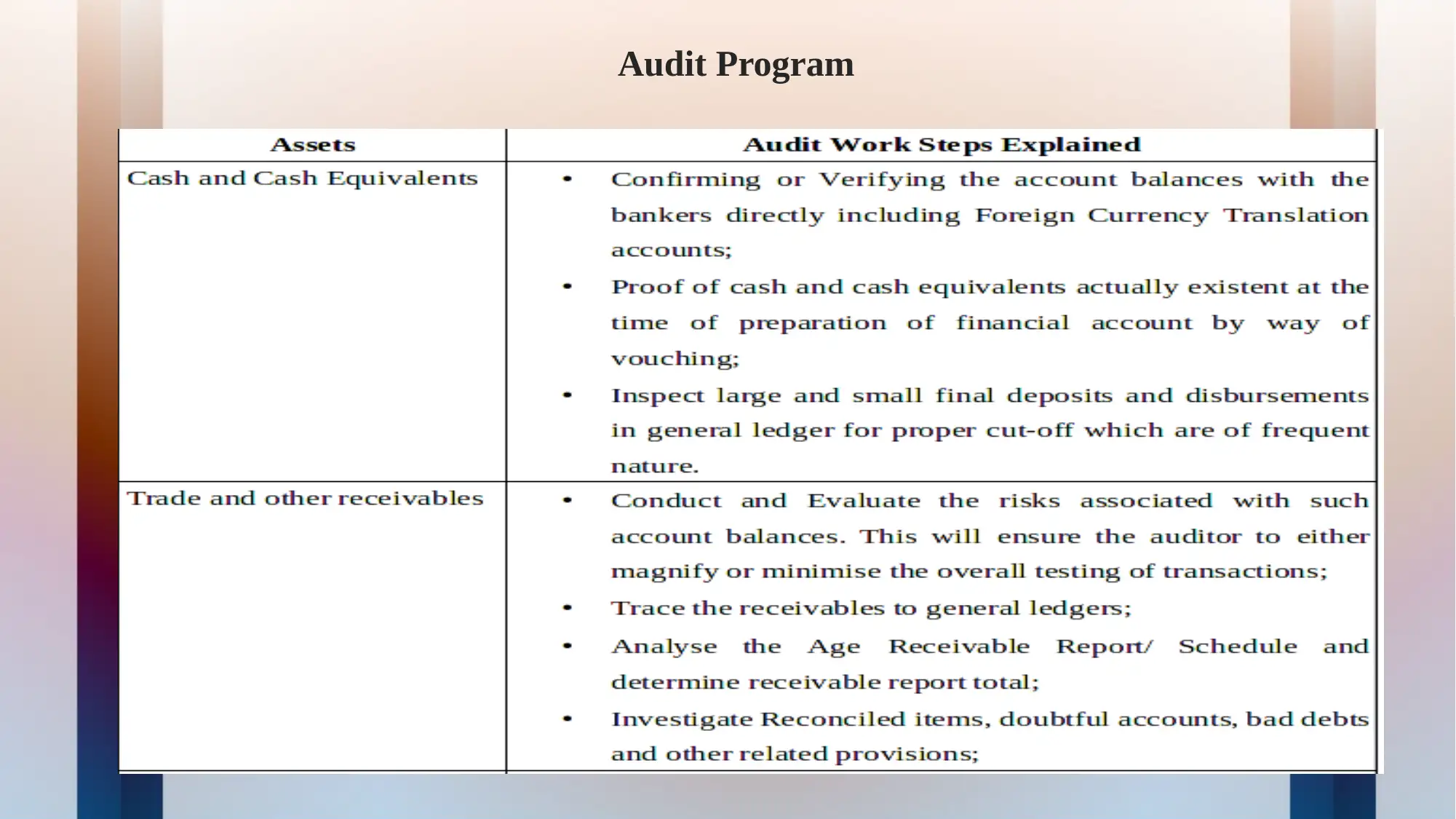

This report details the development of an audit program tailored for Mako Gold Limited, an Australian mining company. It begins with an overview of the industry and the company, followed by the identification of key business risks, including credit, liquidity, and market risks. The report then outlines the audit risk model, encompassing inherent, control, and detection risks. Analytical procedures are described, and material account balances are identified, along with their respective assertions. The audit program itself is presented, including a sampling plan for material account balances. The report concludes by emphasizing the impact of internal controls, legal compliance, and analytical procedures on audit program development. The report references relevant books, journal articles, and online resources, including Mako Gold Limited's annual reports.

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.