BH 101 Property Taxation: Regulations, Exemptions, and Penalties

VerifiedAdded on 2023/06/03

|11

|2859

|324

Report

AI Summary

This report provides an overview of property taxation in Malaysia, focusing on stamp duty and real capital gains tax. It discusses the nature of stamp duty under the Stamp Duty Act 1949 and Real Property Gains Tax Act 1976, highlighting key concepts such as chargeable persons, disposal price, and permitted expenses. The report also delves into the principles of taxation, including fairness, clarity, convenience, efficiency, and neutrality. Tax calculation examples for stamp duty and real property gains tax are provided to illustrate the practical application of these concepts. Finally, the report outlines various exemptions and penalties associated with both stamp duty and real property gains tax, offering a comprehensive understanding of the Malaysian property tax landscape.

PROPERTY TAX

TABLE OF CONTENT

TABLE OF CONTENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

S

Introduction................................................................................................................................1

Nature of stamp duty and Real capital gain tax......................................................................2

Real Property gains tax...........................................................................................................2

Describe tax fundamentals.....................................................................................................3

Give tax calculations examples..............................................................................................4

Discuss exemptions or penalties.............................................................................................5

REFERENCES...........................................................................................................................8

Introduction................................................................................................................................1

Nature of stamp duty and Real capital gain tax......................................................................2

Real Property gains tax...........................................................................................................2

Describe tax fundamentals.....................................................................................................3

Give tax calculations examples..............................................................................................4

Discuss exemptions or penalties.............................................................................................5

REFERENCES...........................................................................................................................8

INTRODUCTION

With the increasing changes in the external environment, an entity owner becomes

more cautious in terms of safeguarding its business interest from all the external competition

lies in the market to maintain its potential for capturing larger market share (Shafai, Amran

and Ganesan, 2018). To analyze the financial performance of an entity, it is essential to keep

a close watch on the tax structure of the country in which the firm is operating its business

empire as minute changes in the existing tax structure of the country will directly affect the

overall revenues earned by a business. The net profit will get affected with the increasing or

decreasing amount of tax as decreasing tax rate will increase the net profit of the company

and increasing tax rate will, in turn, decreases the net profit of an enterprise which has several

effects on an enterprise (Thompson and Neuzil, 2018). In this assignment, Malaysia taxation

is to be discussed by highlighting various concepts such as discussing the nature of stamp

duty, real capital gain tax. These will helps in stressing the tax fundamentals for different

parties related with the current tax structure such as assesses who is paying the tax which may

include all the individuals and the corporate parties that is the company (Lang, Pistone,

Schuch and Staringer, eds., 2018). Tax calculations examples are mentioned in the

assignment to give a crux about determining a tax return of an entity and lastly, this report

will discuss all the exemptions and penalties imposed on a party whose tax is assessed by an

assessor.

Malaysian taxation

The term taxation refers to imposition of taxes on all the individuals or corporate entities to

fund all the expenditures made by public authorities who may include government, statutory

bodies and property head who will collect different kinds of taxes on behalf of the

government from all the mentioned parties who are liable to pay tax for a particular year

(Adam and Yusof, 2018).

In Malaysia, a tax is collected by the federal government, state, and local Municipal

Corporation as per the mention tax slabs for either the individuals or the corporate bodies in

determining its annual tax return (Kasim, Umar, Martin and Yassin, 2018). Important and

primary tax legislation such as income tax act 1967, Real property gains tax act 1976,

Promotion of Investments act and lastly, petroleum income tax act 1967 are considered as the

major tax concepts in Malaysia’s taxation structure.

1

With the increasing changes in the external environment, an entity owner becomes

more cautious in terms of safeguarding its business interest from all the external competition

lies in the market to maintain its potential for capturing larger market share (Shafai, Amran

and Ganesan, 2018). To analyze the financial performance of an entity, it is essential to keep

a close watch on the tax structure of the country in which the firm is operating its business

empire as minute changes in the existing tax structure of the country will directly affect the

overall revenues earned by a business. The net profit will get affected with the increasing or

decreasing amount of tax as decreasing tax rate will increase the net profit of the company

and increasing tax rate will, in turn, decreases the net profit of an enterprise which has several

effects on an enterprise (Thompson and Neuzil, 2018). In this assignment, Malaysia taxation

is to be discussed by highlighting various concepts such as discussing the nature of stamp

duty, real capital gain tax. These will helps in stressing the tax fundamentals for different

parties related with the current tax structure such as assesses who is paying the tax which may

include all the individuals and the corporate parties that is the company (Lang, Pistone,

Schuch and Staringer, eds., 2018). Tax calculations examples are mentioned in the

assignment to give a crux about determining a tax return of an entity and lastly, this report

will discuss all the exemptions and penalties imposed on a party whose tax is assessed by an

assessor.

Malaysian taxation

The term taxation refers to imposition of taxes on all the individuals or corporate entities to

fund all the expenditures made by public authorities who may include government, statutory

bodies and property head who will collect different kinds of taxes on behalf of the

government from all the mentioned parties who are liable to pay tax for a particular year

(Adam and Yusof, 2018).

In Malaysia, a tax is collected by the federal government, state, and local Municipal

Corporation as per the mention tax slabs for either the individuals or the corporate bodies in

determining its annual tax return (Kasim, Umar, Martin and Yassin, 2018). Important and

primary tax legislation such as income tax act 1967, Real property gains tax act 1976,

Promotion of Investments act and lastly, petroleum income tax act 1967 are considered as the

major tax concepts in Malaysia’s taxation structure.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The government of Malaysia assigns tax base which will include income, property

possession, and commodity held by a user for a particular assessment year are categorizes on

which tax rate is applied to determines their total return held for that particular period (Hor

and Rahmat, 2018). The tax is directly determined by multiplying the tax base with the tax

rate applicable to the party whose tax is to be determined by a tax determiner to estimate its

tax for an assessment year.

Nature of stamp duty and Real capital gain tax

Stamp duty is a legal attested form governs under stamp duty act 1949 which will give

legal identity to any agreement to increase its legal value to give those legal rights to a party.

It is a written and legal evidence consider as a valid legal instruments used in various events

such as creating agreements, mortgaging of a house, building or shops, bill of sale and taking

an insurance policies, With the help of a stamp duty an individual can showcase its legality to

cross-question in the future in case of any discrepancies (Ismail and et.al., 2018). The stamp

duty payable on these instruments is to be payable to three designated parties who are the

representatives of the government in collecting the stamp duty revenue includes stamp duty

office and Inland Revenue board (Aziz and Hanif, 2018). As per section 33 under the

schedule of the stamp duty at, the responsibility of paying the stamp duty by all the parties

such as in case of a conveyance, the grantee or the transferee will pay the stamp duty on the

legal instruments. In case of a mortgage, the person liable to pay the duty on the mortgage

document is the mortgagor who lent its property on a mortgage to the party and in case of the

lease agreement the duty will be payable by Lessee. There are two kinds of stamp duties such

as Ad-Valorem duty and fixed duty to determine the duty to be payable on different

instruments (Guide, 2018). The amount of stamp duty payable by an individual is to be

determined by considering the purchase if the property and the lease or tenancy agreement

formed by a party with the owner of the premises.

Real Property gains tax

This act will be governed under real capital gains tax act 1976 which is levied by

Inland revenue board on the gains incurred on capital assets that is the chargeable asset in the

purview of the capital gain tax (Erdem, 2018). The chargeable gains arise when a property is

sold in Malaysia by deducting the cost of an improvement on that property is excluded from

the selling value or the market value of that asset to determine the chargeable gains which

will be taxed under this act. Real property gains tax comes into operation on 7 November

1975 is liable only on the building by excluding the land under this act.

2

possession, and commodity held by a user for a particular assessment year are categorizes on

which tax rate is applied to determines their total return held for that particular period (Hor

and Rahmat, 2018). The tax is directly determined by multiplying the tax base with the tax

rate applicable to the party whose tax is to be determined by a tax determiner to estimate its

tax for an assessment year.

Nature of stamp duty and Real capital gain tax

Stamp duty is a legal attested form governs under stamp duty act 1949 which will give

legal identity to any agreement to increase its legal value to give those legal rights to a party.

It is a written and legal evidence consider as a valid legal instruments used in various events

such as creating agreements, mortgaging of a house, building or shops, bill of sale and taking

an insurance policies, With the help of a stamp duty an individual can showcase its legality to

cross-question in the future in case of any discrepancies (Ismail and et.al., 2018). The stamp

duty payable on these instruments is to be payable to three designated parties who are the

representatives of the government in collecting the stamp duty revenue includes stamp duty

office and Inland Revenue board (Aziz and Hanif, 2018). As per section 33 under the

schedule of the stamp duty at, the responsibility of paying the stamp duty by all the parties

such as in case of a conveyance, the grantee or the transferee will pay the stamp duty on the

legal instruments. In case of a mortgage, the person liable to pay the duty on the mortgage

document is the mortgagor who lent its property on a mortgage to the party and in case of the

lease agreement the duty will be payable by Lessee. There are two kinds of stamp duties such

as Ad-Valorem duty and fixed duty to determine the duty to be payable on different

instruments (Guide, 2018). The amount of stamp duty payable by an individual is to be

determined by considering the purchase if the property and the lease or tenancy agreement

formed by a party with the owner of the premises.

Real Property gains tax

This act will be governed under real capital gains tax act 1976 which is levied by

Inland revenue board on the gains incurred on capital assets that is the chargeable asset in the

purview of the capital gain tax (Erdem, 2018). The chargeable gains arise when a property is

sold in Malaysia by deducting the cost of an improvement on that property is excluded from

the selling value or the market value of that asset to determine the chargeable gains which

will be taxed under this act. Real property gains tax comes into operation on 7 November

1975 is liable only on the building by excluding the land under this act.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The real property gains tax consists of various terms such as the chargeable person is a person

who is a resident or not resident of Malaysia for a particular year is considered as a

chargeable person under the real capital gains tax when they dispose of an asset (Alm, 2018).

It is essential to consider all the asset under the real property head to determine the capital

gains tax liability on the disposable of real property which consisting of land located in the

Malaysia and interest or right over the land in the possession of an individual. The disposal

price is the price used to sell the assets by excluding the number of costs incurred in

improving the property (Rao, 2018). The Real capital gain tax rate is 5% imposed on the gain

arises on the disposal of the capital asset without seeking the life of that asset.

While determining the real proper gains tax, it is also essential to know about all the

permitted expenses to get deducted out of the sales consideration in estimating the net capital

gain generated from that asset. Another term which will be discussed is incidental costs

incurred by an individual related that particular asset. Permitted expenses include various

expense such as expenses charged in accordance with the capital asset, expenses incurred

wholly related to an asset for preserving the title of taking the chargeable asset in determining

the capital gain arises from it (Zelenak, 2018). Another term is about the incidental costs

incurred in a entity related to an asset on which an individual will determine the capital gains

tax consisting of fees, commission or salary payable to the surveyor who offers its

professional services in estimating the actual worth or value of the property to give a basic

input in form of market value of an asset to determine the capital gain tax. This head will also

include the expenses incurred in transferring an asset to another party such as paying the

stamp duty and this will also cover the cost of giving advertisement in the newspapers to

invite the buyers to buy the property which the seller is selling will also cover under this head

as incidental costs are that costs which will incur by an entity unintentionally without prior

intimation and with no fixed tenure.

Describe tax fundamentals

Principles of taxation are considered as the tax fundamentals held responsible for

creating a strong base and fundamentals which is based on several pillars behind the

successful taxation structure such as Fairness, clarity and certainty, convenience, efficiency,

and neutrality (Fleurbaey and Maniquet, 2018). The fairness principles depicts the ability to

pay and receive the benefits received by an individual in terms of income received by a

person for a particular year and at the same time pay back all the expenses incurred for that

particular year whether related to an asset when talking about property gains tax in which a

3

who is a resident or not resident of Malaysia for a particular year is considered as a

chargeable person under the real capital gains tax when they dispose of an asset (Alm, 2018).

It is essential to consider all the asset under the real property head to determine the capital

gains tax liability on the disposable of real property which consisting of land located in the

Malaysia and interest or right over the land in the possession of an individual. The disposal

price is the price used to sell the assets by excluding the number of costs incurred in

improving the property (Rao, 2018). The Real capital gain tax rate is 5% imposed on the gain

arises on the disposal of the capital asset without seeking the life of that asset.

While determining the real proper gains tax, it is also essential to know about all the

permitted expenses to get deducted out of the sales consideration in estimating the net capital

gain generated from that asset. Another term which will be discussed is incidental costs

incurred by an individual related that particular asset. Permitted expenses include various

expense such as expenses charged in accordance with the capital asset, expenses incurred

wholly related to an asset for preserving the title of taking the chargeable asset in determining

the capital gain arises from it (Zelenak, 2018). Another term is about the incidental costs

incurred in a entity related to an asset on which an individual will determine the capital gains

tax consisting of fees, commission or salary payable to the surveyor who offers its

professional services in estimating the actual worth or value of the property to give a basic

input in form of market value of an asset to determine the capital gain tax. This head will also

include the expenses incurred in transferring an asset to another party such as paying the

stamp duty and this will also cover the cost of giving advertisement in the newspapers to

invite the buyers to buy the property which the seller is selling will also cover under this head

as incidental costs are that costs which will incur by an entity unintentionally without prior

intimation and with no fixed tenure.

Describe tax fundamentals

Principles of taxation are considered as the tax fundamentals held responsible for

creating a strong base and fundamentals which is based on several pillars behind the

successful taxation structure such as Fairness, clarity and certainty, convenience, efficiency,

and neutrality (Fleurbaey and Maniquet, 2018). The fairness principles depicts the ability to

pay and receive the benefits received by an individual in terms of income received by a

person for a particular year and at the same time pay back all the expenses incurred for that

particular year whether related to an asset when talking about property gains tax in which a

3

particular asset is disposed whole gain arises from that asset is to be generated after deducting

all the expenses arises from it (Söllner, 2018). Thus principles depict the honest and fairness

maintained by an individual or an entity by maintaining the dignity of the entire taxation

structure. Another principle is clarity and certainty which shows the clear taxation rules

maintained by an individual for determining the income tax return or capital gain tax earned

on an asset for a particular year. It is essential to use a convenience principle in which an

individual will be easy to calculate the tax return by using different methods according to its

preference and the knowledge as for the sake of all the taxpayers the taxation structure

develops various methods to give the extra method for all the individuals. The efficiency

principle says that taxation administers efficiently and economically handles the taxation

system to determine the overall tax return different from one party to another. The last

principle, neutrality depicts that the action of an individual or an entity should not be

offended as this will not affect the behaviour of other people like the tax returns calculated by

an entity should be as per the taxation rules prepare by an entity (Du Preez, 2018).

Give tax calculations examples

Stamp Duty Calculations

Purchase of Property

Particulars Amount

Market value of property RM 3560000

First RM 100,000@1% RM10000

RM 100,000-RM356000@2% RM 5120

Total Stamp duty payable RM 15120

Lease/Tenancy

Particulars Amount

Lease Period 3.5 years

First 1@1% 0.01

1-3.5@2% 0.05

Total lease period 0.06

Real gain property tax

4

all the expenses arises from it (Söllner, 2018). Thus principles depict the honest and fairness

maintained by an individual or an entity by maintaining the dignity of the entire taxation

structure. Another principle is clarity and certainty which shows the clear taxation rules

maintained by an individual for determining the income tax return or capital gain tax earned

on an asset for a particular year. It is essential to use a convenience principle in which an

individual will be easy to calculate the tax return by using different methods according to its

preference and the knowledge as for the sake of all the taxpayers the taxation structure

develops various methods to give the extra method for all the individuals. The efficiency

principle says that taxation administers efficiently and economically handles the taxation

system to determine the overall tax return different from one party to another. The last

principle, neutrality depicts that the action of an individual or an entity should not be

offended as this will not affect the behaviour of other people like the tax returns calculated by

an entity should be as per the taxation rules prepare by an entity (Du Preez, 2018).

Give tax calculations examples

Stamp Duty Calculations

Purchase of Property

Particulars Amount

Market value of property RM 3560000

First RM 100,000@1% RM10000

RM 100,000-RM356000@2% RM 5120

Total Stamp duty payable RM 15120

Lease/Tenancy

Particulars Amount

Lease Period 3.5 years

First 1@1% 0.01

1-3.5@2% 0.05

Total lease period 0.06

Real gain property tax

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

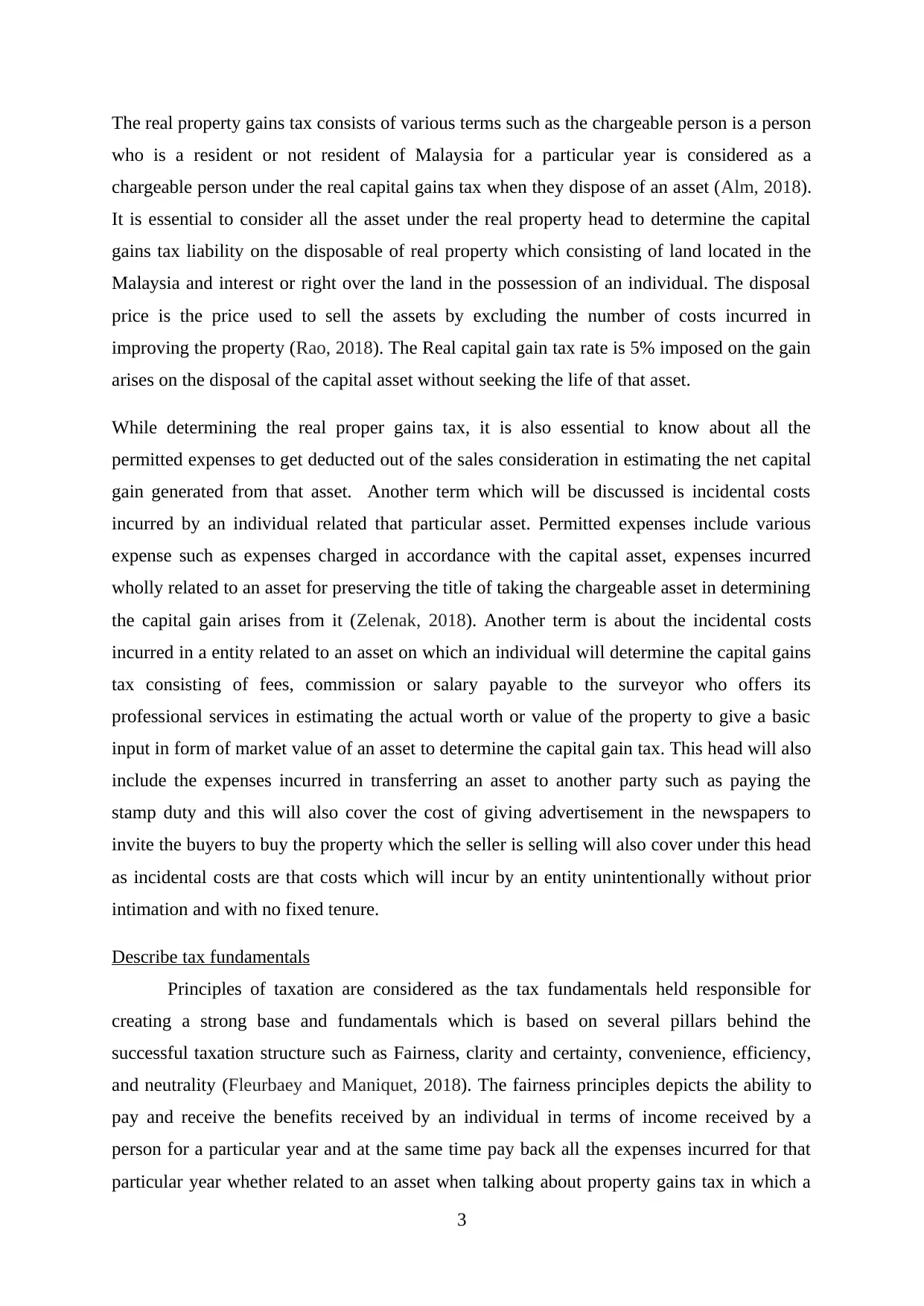

Particulars Amount

Sales consideration RM500,000

Less: Cost of improvement (RM100,000)

Capital Gain RM400,000

Capital gain tax @5% RM20000

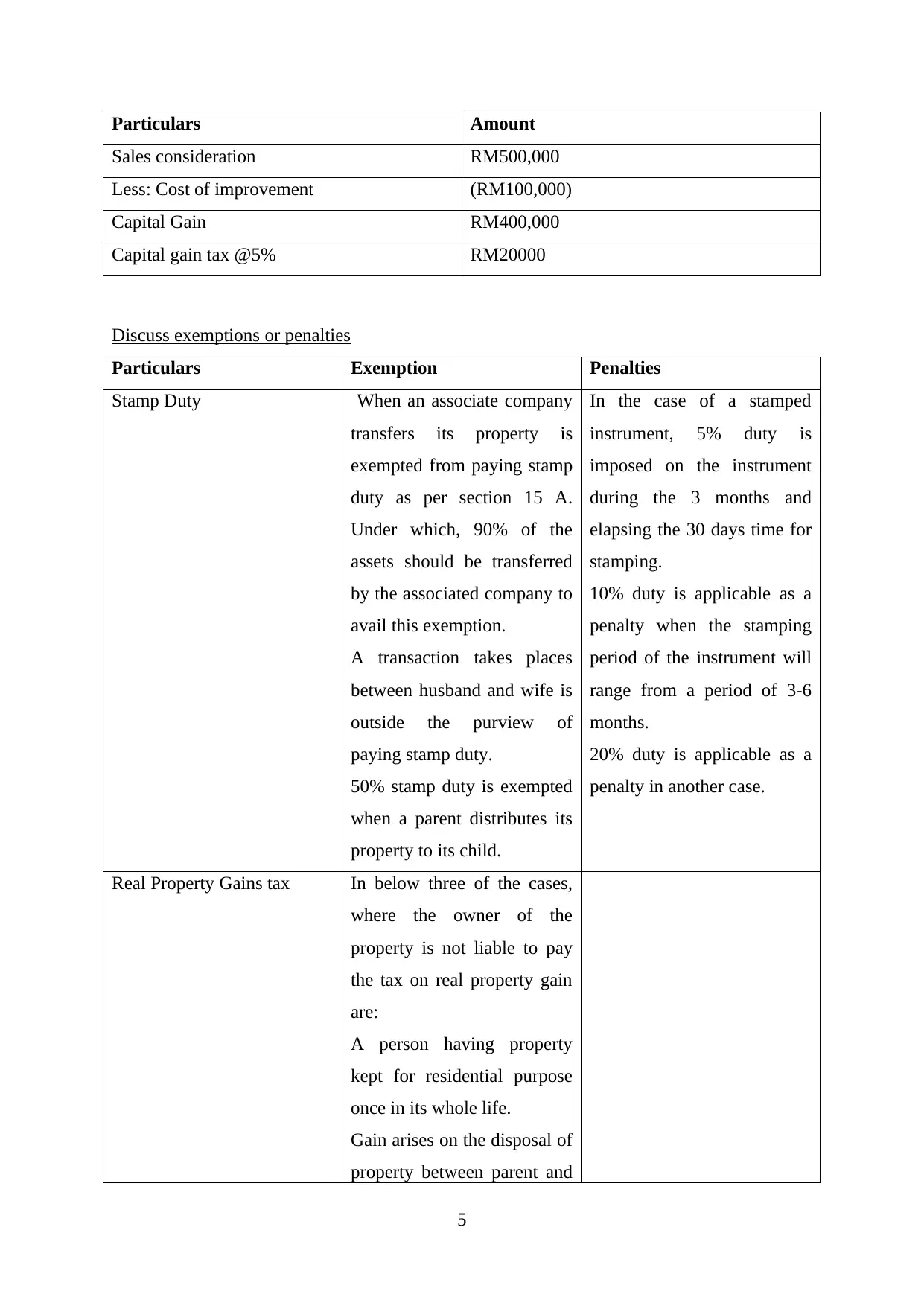

Discuss exemptions or penalties

Particulars Exemption Penalties

Stamp Duty When an associate company

transfers its property is

exempted from paying stamp

duty as per section 15 A.

Under which, 90% of the

assets should be transferred

by the associated company to

avail this exemption.

A transaction takes places

between husband and wife is

outside the purview of

paying stamp duty.

50% stamp duty is exempted

when a parent distributes its

property to its child.

In the case of a stamped

instrument, 5% duty is

imposed on the instrument

during the 3 months and

elapsing the 30 days time for

stamping.

10% duty is applicable as a

penalty when the stamping

period of the instrument will

range from a period of 3-6

months.

20% duty is applicable as a

penalty in another case.

Real Property Gains tax In below three of the cases,

where the owner of the

property is not liable to pay

the tax on real property gain

are:

A person having property

kept for residential purpose

once in its whole life.

Gain arises on the disposal of

property between parent and

5

Sales consideration RM500,000

Less: Cost of improvement (RM100,000)

Capital Gain RM400,000

Capital gain tax @5% RM20000

Discuss exemptions or penalties

Particulars Exemption Penalties

Stamp Duty When an associate company

transfers its property is

exempted from paying stamp

duty as per section 15 A.

Under which, 90% of the

assets should be transferred

by the associated company to

avail this exemption.

A transaction takes places

between husband and wife is

outside the purview of

paying stamp duty.

50% stamp duty is exempted

when a parent distributes its

property to its child.

In the case of a stamped

instrument, 5% duty is

imposed on the instrument

during the 3 months and

elapsing the 30 days time for

stamping.

10% duty is applicable as a

penalty when the stamping

period of the instrument will

range from a period of 3-6

months.

20% duty is applicable as a

penalty in another case.

Real Property Gains tax In below three of the cases,

where the owner of the

property is not liable to pay

the tax on real property gain

are:

A person having property

kept for residential purpose

once in its whole life.

Gain arises on the disposal of

property between parent and

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

child, husband and wife and

grandparents and

grandchildren

Exemption from the capital

gain in value up to RM

10000 or 10% of the net

gains whichever is higher.

Husband or wife transfers the

properties to each other are

outside from this act.

Getting a part of the property

in an inheritance from

deceased.

Transferring shares held by

an individual in a company is

transferred from a person to

that company does fall under

this act.

Transferring an asset which

is held as a collateral security

before taking a loan.

Acquisition of an asset by the

government.

Selling of any asset for

giving charity does not fall

under this act.

If the acquisition price of an

asset exceeds the disposable

price of the sold asset dies

not does under this act as this

event consider as an

allowable loss which will

separately recorded in the

books of account of an entity

6

grandparents and

grandchildren

Exemption from the capital

gain in value up to RM

10000 or 10% of the net

gains whichever is higher.

Husband or wife transfers the

properties to each other are

outside from this act.

Getting a part of the property

in an inheritance from

deceased.

Transferring shares held by

an individual in a company is

transferred from a person to

that company does fall under

this act.

Transferring an asset which

is held as a collateral security

before taking a loan.

Acquisition of an asset by the

government.

Selling of any asset for

giving charity does not fall

under this act.

If the acquisition price of an

asset exceeds the disposable

price of the sold asset dies

not does under this act as this

event consider as an

allowable loss which will

separately recorded in the

books of account of an entity

6

which will be carry forward

to the next year as in this way

the loss will get compensated

with the earned capital gain

of that year by checking the

similar category to redeem

the amount of loss from the

earned capital gain. The

amount of allowable loss is

multiplied with the real

proper gains tax rate and this

will get carried forward to

the future year to deduct the

amount of loss from the

capital gain of that year.

7

to the next year as in this way

the loss will get compensated

with the earned capital gain

of that year by checking the

similar category to redeem

the amount of loss from the

earned capital gain. The

amount of allowable loss is

multiplied with the real

proper gains tax rate and this

will get carried forward to

the future year to deduct the

amount of loss from the

capital gain of that year.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Adam, M. N. H. and Yusof, N. A. M., 2018. A Comparative Study on the Burden of Tax

Compliance Costs amongst GST Registered Companies in Malaysia and Abroad. Journal of

Science, Technology and Innovation Policy. 3(2).

Alm, J., 2018. What are the Costs of a New Tax Administration? The Case of a Personal

Income Tax in Kuwait(No. 1804).

Aziz, W. N. A. W. A. and Hanif, N. R., 2018. Housing policy in Malaysia: bridging the

affordability gap for medium-income households. In Housing Policy, Wellbeing and Social

Development in Asia (pp. 141-156). Routledge.

Du Preez, H., 2018. Constructing the Fundamental Principles of Taxation through

Triangulation. Journal of Legal Tax Research.

Erdem, N., 2018. The need for re-engineering in the real estate appraisal system in

Turkey. Survey Review, pp.1-13.

Fleurbaey, M. and Maniquet, F., 2018. Optimal income taxation theory and principles of

fairness. Journal of Economic Literature. 56(3). pp.1029-79.

Guide, G. P., 2018. Property in Malaysia| Malaysian Real Estate Investment.

Hor, K. and Rahmat, M. K., 2018. Analysis and recommendations for building energy

efficiency financing in Malaysia. Energy Efficiency. 11(1). pp.79-95.

Ismail, R., and et.al., 2018. Consumers Basic Right to Housing: The Role of Institutional

Frameworks in Malaysia. International Journal of Asian Social Science. 8(8). pp.501-508.

Kasim, R., Umar, M. A., Martin, D. and Yassin, A. M., 2018. Public Goods Delivery as a

Contributing Factor to the Property Tax Revenue Generation in Malaysian Local

Governments. Advanced Science Letters. 24(6). pp.4674-4678.

Lang, M., Pistone, P., Schuch, J. and Staringer, C. eds., 2018. Introduction to European tax

law on direct taxation. Linde Verlag GmbH.

Rao, S., 2018. Country notes: Coverage of OECD Multilateral Instrument on India and Its

Top 10 Tax Treaty Partners in Terms of Foreign Direct Investment. Intertax. 46(5). pp.434-

449.

8

Adam, M. N. H. and Yusof, N. A. M., 2018. A Comparative Study on the Burden of Tax

Compliance Costs amongst GST Registered Companies in Malaysia and Abroad. Journal of

Science, Technology and Innovation Policy. 3(2).

Alm, J., 2018. What are the Costs of a New Tax Administration? The Case of a Personal

Income Tax in Kuwait(No. 1804).

Aziz, W. N. A. W. A. and Hanif, N. R., 2018. Housing policy in Malaysia: bridging the

affordability gap for medium-income households. In Housing Policy, Wellbeing and Social

Development in Asia (pp. 141-156). Routledge.

Du Preez, H., 2018. Constructing the Fundamental Principles of Taxation through

Triangulation. Journal of Legal Tax Research.

Erdem, N., 2018. The need for re-engineering in the real estate appraisal system in

Turkey. Survey Review, pp.1-13.

Fleurbaey, M. and Maniquet, F., 2018. Optimal income taxation theory and principles of

fairness. Journal of Economic Literature. 56(3). pp.1029-79.

Guide, G. P., 2018. Property in Malaysia| Malaysian Real Estate Investment.

Hor, K. and Rahmat, M. K., 2018. Analysis and recommendations for building energy

efficiency financing in Malaysia. Energy Efficiency. 11(1). pp.79-95.

Ismail, R., and et.al., 2018. Consumers Basic Right to Housing: The Role of Institutional

Frameworks in Malaysia. International Journal of Asian Social Science. 8(8). pp.501-508.

Kasim, R., Umar, M. A., Martin, D. and Yassin, A. M., 2018. Public Goods Delivery as a

Contributing Factor to the Property Tax Revenue Generation in Malaysian Local

Governments. Advanced Science Letters. 24(6). pp.4674-4678.

Lang, M., Pistone, P., Schuch, J. and Staringer, C. eds., 2018. Introduction to European tax

law on direct taxation. Linde Verlag GmbH.

Rao, S., 2018. Country notes: Coverage of OECD Multilateral Instrument on India and Its

Top 10 Tax Treaty Partners in Terms of Foreign Direct Investment. Intertax. 46(5). pp.434-

449.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Shafai, N. A. B., Amran, A. B. and Ganesan, Y., 2018. Earnings Management, Tax

Avoidance and Corporate Social Responsibility: Malaysia Evidence. Management. 5(3).

pp.41-56.

Söllner, F., 2018. Road traffic taxation in Germany: the present system, its problems and a

proposal for reform. Journal of Tax Reform. 4(1). pp.57-72.

Thompson, J. and Neuzil, D., 2018. Valuing Bonus Depreciation Under the New Tax

Law. Business Valuation Review. 37(1). pp.15-19.

Zelenak, L. A., 2018. Leaving it up to Treasury: Congressional Abdication on Major Policy

Issues in the Early Years of the Income Tax. Law and Contemporary Problems. 81(2).

pp.137-165.

9

Avoidance and Corporate Social Responsibility: Malaysia Evidence. Management. 5(3).

pp.41-56.

Söllner, F., 2018. Road traffic taxation in Germany: the present system, its problems and a

proposal for reform. Journal of Tax Reform. 4(1). pp.57-72.

Thompson, J. and Neuzil, D., 2018. Valuing Bonus Depreciation Under the New Tax

Law. Business Valuation Review. 37(1). pp.15-19.

Zelenak, L. A., 2018. Leaving it up to Treasury: Congressional Abdication on Major Policy

Issues in the Early Years of the Income Tax. Law and Contemporary Problems. 81(2).

pp.137-165.

9

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.