Advanced Diploma of Leadership & Management: BSBFIM601 Project

VerifiedAdded on 2022/12/22

|21

|4546

|1

Project

AI Summary

This project, designed for the BSBFIM601 Manage Finances unit, presents a comprehensive analysis of Woolworths Ltd's financial performance. The assessment requires students to examine Woolworths' financial statements, including the Profit and Loss statement, Statement of Cash Flows, and Balance Sheet, to identify key trends and factors impacting revenue, profit, and cash flow. The project delves into specific components affecting revenue, such as petrol sales, and investigates the reasons behind the company's shift from profit to loss between 2015 and 2016. Students are tasked with analyzing the company's growth initiatives, cash flow changes, and the discrepancy between reported loss and reduction in cash. Furthermore, the assessment requires the identification and calculation of financial ratios, examination of accounting policies, and an understanding of the role of auditors and compliance with financial reporting standards. The project also explores Woolworths Ltd's investments in other companies and assesses their impact on the overall financial results, including the contribution of ALH Group Pty Ltd and Hydrox Holdings Pty Ltd. Finally, the project addresses the reasons behind the company's tax expense despite reporting a loss, offering a detailed and practical application of financial management principles.

BSBFIM601 Manage Finances

Advanced Diploma of Leadership & Management

Module 4 Project 1

Submission Instructions:

Key steps that must be followed:

1. Please complete the Declaration of Authenticity at the bottom of this page.

2. Once you have completed all parts of the assessment and saved it (e.g. to your desktop computer),

login to the Monarch Learning Management System (LMS) to submit your assessment.

3. In the LMS, click on the file” Submit ADLM Module 4 Project” in the Module 4 section of your course

and upload your assessment file/s by following the prompts.

4. Please be sure to click “Continue” after clicking “submit”. This ensures your assessor receives

notification – very important!

Declaration of Understanding and Authenticity *

I have read and understood the assessment instructions provided to me in the Learning Management System.

I certify that the attached material is my original work. No other person’s work has been used without due

acknowledgement. I understand that the work submitted may be reproduced and/or communicated for the

purpose of detecting plagiarism.

Student Name*: Date:

* I understand that by typing my name or inserting a digital signature into this box that I agree and am bound by

the above student declaration.

Advanced Diploma of Leadership & Management

Module 4 Project 1

Submission Instructions:

Key steps that must be followed:

1. Please complete the Declaration of Authenticity at the bottom of this page.

2. Once you have completed all parts of the assessment and saved it (e.g. to your desktop computer),

login to the Monarch Learning Management System (LMS) to submit your assessment.

3. In the LMS, click on the file” Submit ADLM Module 4 Project” in the Module 4 section of your course

and upload your assessment file/s by following the prompts.

4. Please be sure to click “Continue” after clicking “submit”. This ensures your assessor receives

notification – very important!

Declaration of Understanding and Authenticity *

I have read and understood the assessment instructions provided to me in the Learning Management System.

I certify that the attached material is my original work. No other person’s work has been used without due

acknowledgement. I understand that the work submitted may be reproduced and/or communicated for the

purpose of detecting plagiarism.

Student Name*: Date:

* I understand that by typing my name or inserting a digital signature into this box that I agree and am bound by

the above student declaration.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BSBFIM601 Manage Finances

Important assessment information

Aims of this assessment

This assessment task covers the fundamental skills and knowledge required to manage finances in an

organisation. The focus is on budgeting and variance considerations and requires an understanding of cost

behaviour, break even analysis as well as an understanding of basic financial statement ratio analysis.

This assessment uses financial data from Woolworths Ltd as well as some fictional case studies.

Marking and feedback

This project contains 3 assessment activities each containing specific instructions.

This particular assessment forms part of your overall assessment for the following unit of competency:

BSBFIM601 Manage Finances

Grading for this assessment will be deemed “competent” or “not-yet-competent” in line with specified

educational standards under the Australian Qualifications Framework.

What does “competent” mean?

These answers and portfolio evidence contain relevant and accurate information in response to the question/s

and task/s with limited serious errors in fact or application. If incorrect information is contained in an answer,

it must be fundamentally outweighed by the accurate information provided. This will be assessed against a

marking guide provided to assessors for their determination.

What does “not-yet-competent” mean?

This occurs when an assessment does not meet the marking guide standards provided to assessors. These

answers either do not address the question specifically, or are wrong from a legislative perspective, or are

incorrectly applied. Answers that omit to provide a response to any significant issue (where multiple issues

must be addressed in a question) may also be deemed not-yet-competent. Answers that have faulty reasoning,

a poor standard of expression or include plagiarism may also be deemed not-yet-competent. Please note,

additional information regarding Monarch’s plagiarism policy is contained in the Student Information Guide

which can be found here:

What happens if you are deemed not-yet-competent?

In the event you do not achieve competency by your assessor on this assessment, you will be given one more

opportunity to re-submit the assessment after consultation with your Trainer/ Assessor. You will know your

assessment is deemed ‘not-yet-competent’ if your grade book in the Monarch LMS says “NYC” after you have

received an email from your assessor advising your assessment has been graded.

Important: It is your responsibility to ensure your assessment resubmission addresses all areas deemed

unsatisfactory by your assessor. Please note, if you are still unsuccessful in meeting competency after

resubmitting your assessment, you will be required to repeat those units.

In the event that you have concerns about the assessment decision then you can refer to our Complaints &

Appeals process also contained within the Student Information Guide.

Expectations from your assessor when answering different types of assessment questions

Knowledge based questions:

A knowledge based question requires you to clearly identify and cover the key subject matter areas raised in

the question in full as part of the response.

Skill based questions:

Important assessment information

Aims of this assessment

This assessment task covers the fundamental skills and knowledge required to manage finances in an

organisation. The focus is on budgeting and variance considerations and requires an understanding of cost

behaviour, break even analysis as well as an understanding of basic financial statement ratio analysis.

This assessment uses financial data from Woolworths Ltd as well as some fictional case studies.

Marking and feedback

This project contains 3 assessment activities each containing specific instructions.

This particular assessment forms part of your overall assessment for the following unit of competency:

BSBFIM601 Manage Finances

Grading for this assessment will be deemed “competent” or “not-yet-competent” in line with specified

educational standards under the Australian Qualifications Framework.

What does “competent” mean?

These answers and portfolio evidence contain relevant and accurate information in response to the question/s

and task/s with limited serious errors in fact or application. If incorrect information is contained in an answer,

it must be fundamentally outweighed by the accurate information provided. This will be assessed against a

marking guide provided to assessors for their determination.

What does “not-yet-competent” mean?

This occurs when an assessment does not meet the marking guide standards provided to assessors. These

answers either do not address the question specifically, or are wrong from a legislative perspective, or are

incorrectly applied. Answers that omit to provide a response to any significant issue (where multiple issues

must be addressed in a question) may also be deemed not-yet-competent. Answers that have faulty reasoning,

a poor standard of expression or include plagiarism may also be deemed not-yet-competent. Please note,

additional information regarding Monarch’s plagiarism policy is contained in the Student Information Guide

which can be found here:

What happens if you are deemed not-yet-competent?

In the event you do not achieve competency by your assessor on this assessment, you will be given one more

opportunity to re-submit the assessment after consultation with your Trainer/ Assessor. You will know your

assessment is deemed ‘not-yet-competent’ if your grade book in the Monarch LMS says “NYC” after you have

received an email from your assessor advising your assessment has been graded.

Important: It is your responsibility to ensure your assessment resubmission addresses all areas deemed

unsatisfactory by your assessor. Please note, if you are still unsuccessful in meeting competency after

resubmitting your assessment, you will be required to repeat those units.

In the event that you have concerns about the assessment decision then you can refer to our Complaints &

Appeals process also contained within the Student Information Guide.

Expectations from your assessor when answering different types of assessment questions

Knowledge based questions:

A knowledge based question requires you to clearly identify and cover the key subject matter areas raised in

the question in full as part of the response.

Skill based questions:

BSBFIM601 Manage Finances

Where you are asked to write as though you presenting information to others, your answers must show your

ability to:

understand other people’s perspective/views

show empathy

display a professional response appropriate to the context

explain ideas clearly and simply so that others can understand the issues

Good luck

Finally, good luck with your learning and assessments and remember your trainers are here to assist you

Where you are asked to write as though you presenting information to others, your answers must show your

ability to:

understand other people’s perspective/views

show empathy

display a professional response appropriate to the context

explain ideas clearly and simply so that others can understand the issues

Good luck

Finally, good luck with your learning and assessments and remember your trainers are here to assist you

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BSBFIM601 Manage Finances

Assessment Activity 1

Case Study

Woolworths Ltd

Activity instructions to candidates

This is an open book assessment activity.

You are required to read this assessment and answer all 11 questions that follow.

Please ensure you have read “Important assessment information” at the front of this assessment

Assessment Activity 1

Case Study

Woolworths Ltd

Activity instructions to candidates

This is an open book assessment activity.

You are required to read this assessment and answer all 11 questions that follow.

Please ensure you have read “Important assessment information” at the front of this assessment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BSBFIM601 Manage Finances

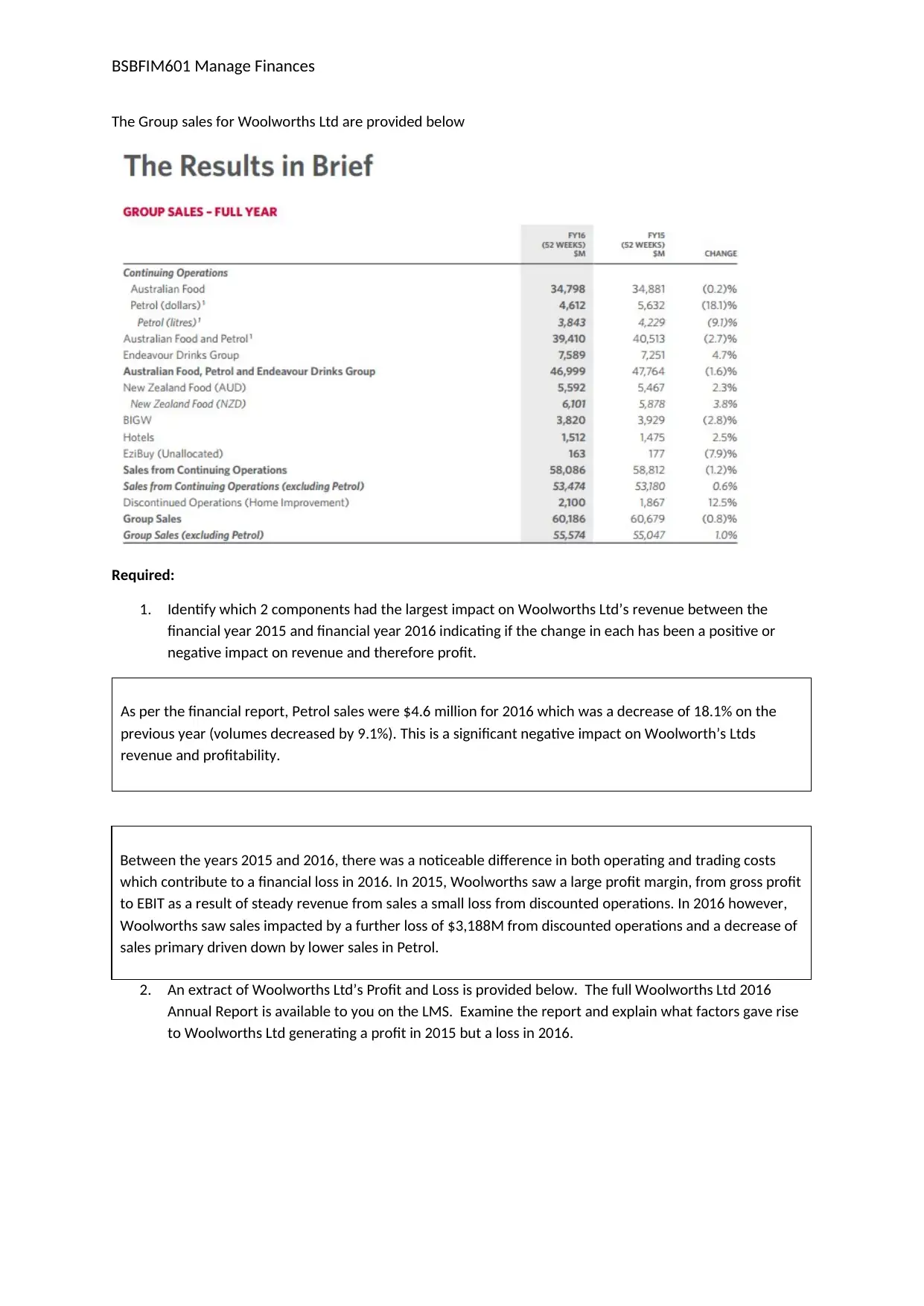

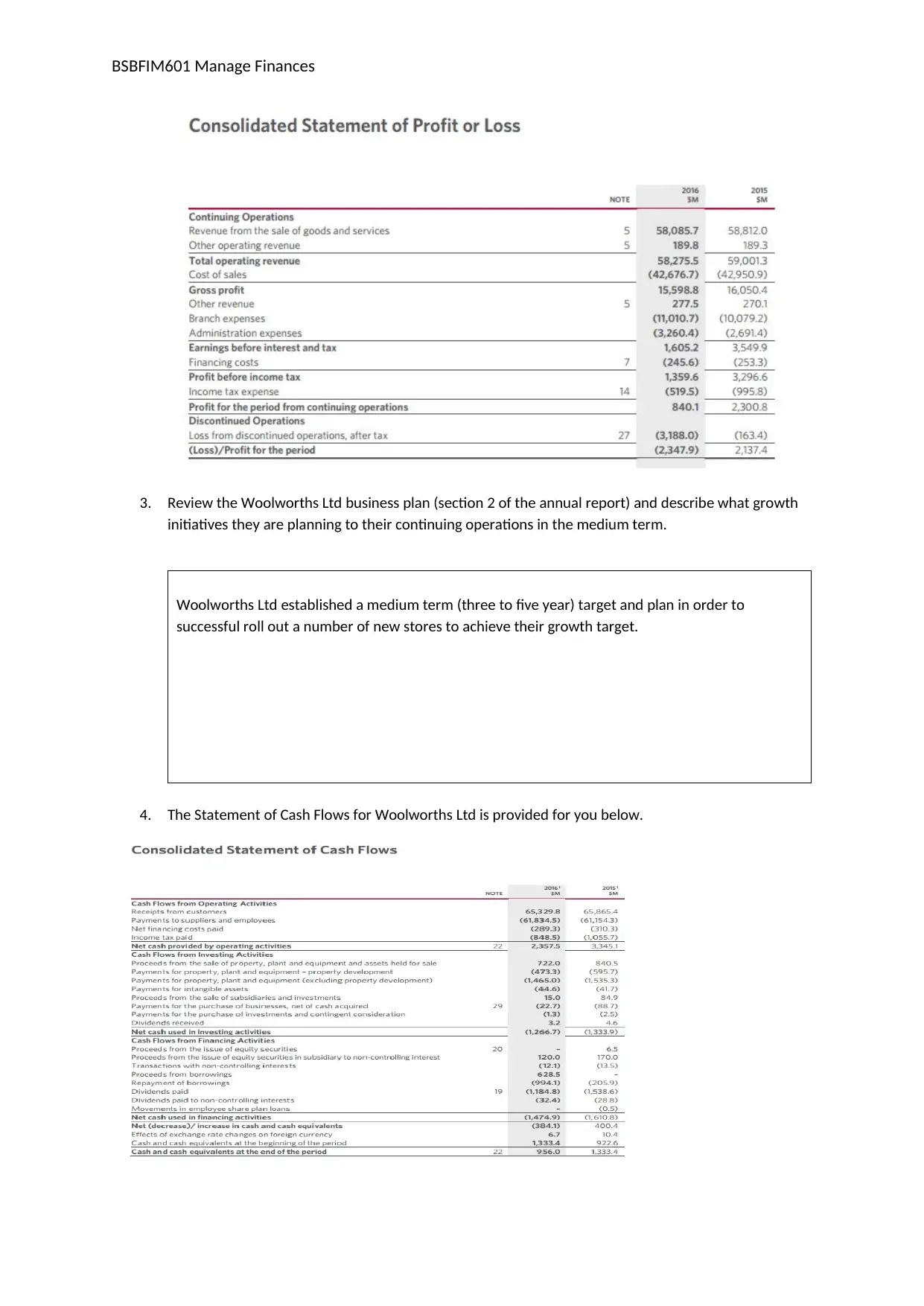

The Group sales for Woolworths Ltd are provided below

Required:

1. Identify which 2 components had the largest impact on Woolworths Ltd’s revenue between the

financial year 2015 and financial year 2016 indicating if the change in each has been a positive or

negative impact on revenue and therefore profit.

As per the financial report, Petrol sales were $4.6 million for 2016 which was a decrease of 18.1% on the

previous year (volumes decreased by 9.1%). This is a significant negative impact on Woolworth’s Ltds

revenue and profitability.

Between the years 2015 and 2016, there was a noticeable difference in both operating and trading costs

which contribute to a financial loss in 2016. In 2015, Woolworths saw a large profit margin, from gross profit

to EBIT as a result of steady revenue from sales a small loss from discounted operations. In 2016 however,

Woolworths saw sales impacted by a further loss of $3,188M from discounted operations and a decrease of

sales primary driven down by lower sales in Petrol.

2. An extract of Woolworths Ltd’s Profit and Loss is provided below. The full Woolworths Ltd 2016

Annual Report is available to you on the LMS. Examine the report and explain what factors gave rise

to Woolworths Ltd generating a profit in 2015 but a loss in 2016.

The Group sales for Woolworths Ltd are provided below

Required:

1. Identify which 2 components had the largest impact on Woolworths Ltd’s revenue between the

financial year 2015 and financial year 2016 indicating if the change in each has been a positive or

negative impact on revenue and therefore profit.

As per the financial report, Petrol sales were $4.6 million for 2016 which was a decrease of 18.1% on the

previous year (volumes decreased by 9.1%). This is a significant negative impact on Woolworth’s Ltds

revenue and profitability.

Between the years 2015 and 2016, there was a noticeable difference in both operating and trading costs

which contribute to a financial loss in 2016. In 2015, Woolworths saw a large profit margin, from gross profit

to EBIT as a result of steady revenue from sales a small loss from discounted operations. In 2016 however,

Woolworths saw sales impacted by a further loss of $3,188M from discounted operations and a decrease of

sales primary driven down by lower sales in Petrol.

2. An extract of Woolworths Ltd’s Profit and Loss is provided below. The full Woolworths Ltd 2016

Annual Report is available to you on the LMS. Examine the report and explain what factors gave rise

to Woolworths Ltd generating a profit in 2015 but a loss in 2016.

BSBFIM601 Manage Finances

3. Review the Woolworths Ltd business plan (section 2 of the annual report) and describe what growth

initiatives they are planning to their continuing operations in the medium term.

Woolworths Ltd established a medium term (three to five year) target and plan in order to

successful roll out a number of new stores to achieve their growth target.

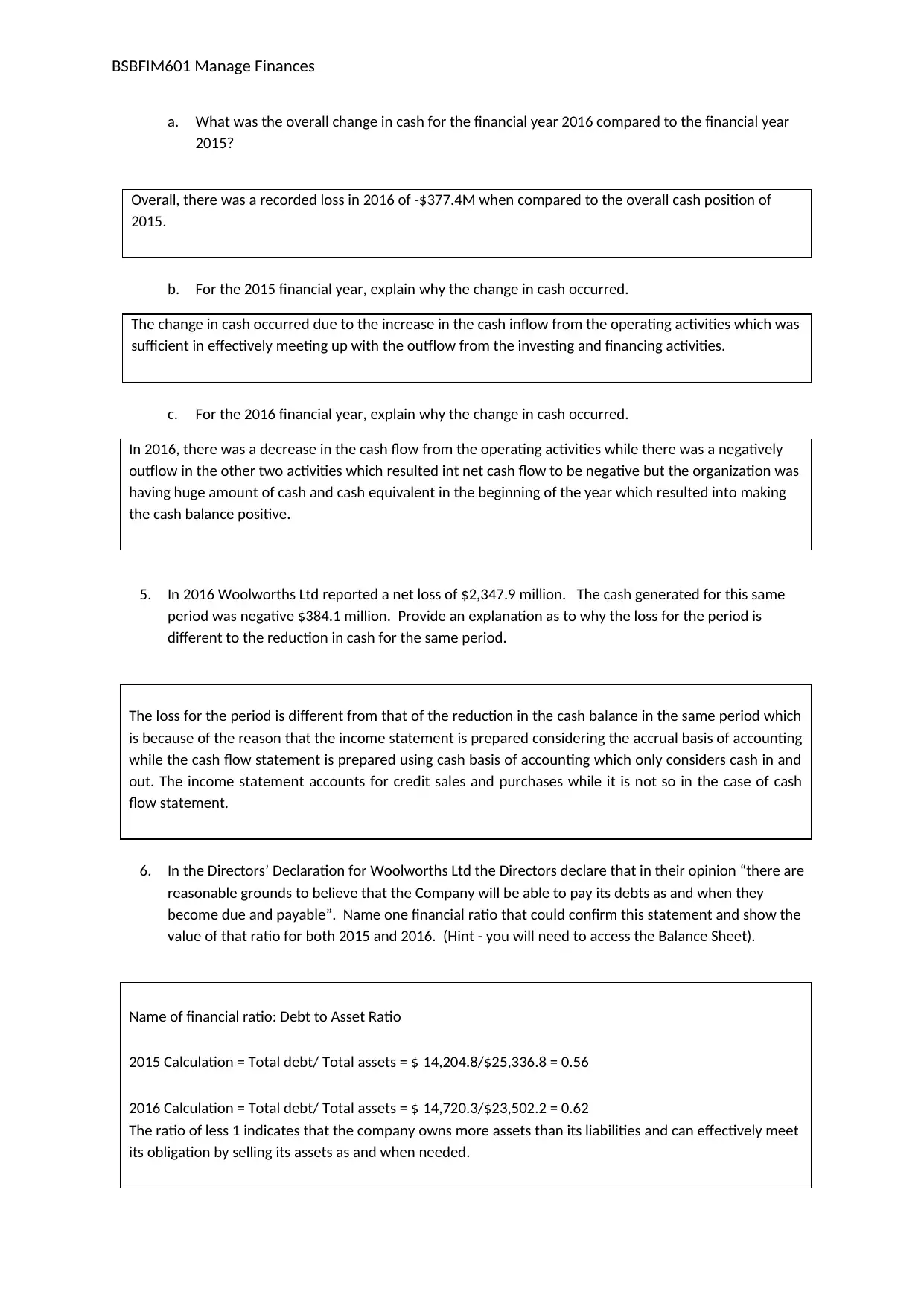

4. The Statement of Cash Flows for Woolworths Ltd is provided for you below.

3. Review the Woolworths Ltd business plan (section 2 of the annual report) and describe what growth

initiatives they are planning to their continuing operations in the medium term.

Woolworths Ltd established a medium term (three to five year) target and plan in order to

successful roll out a number of new stores to achieve their growth target.

4. The Statement of Cash Flows for Woolworths Ltd is provided for you below.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BSBFIM601 Manage Finances

a. What was the overall change in cash for the financial year 2016 compared to the financial year

2015?

Overall, there was a recorded loss in 2016 of -$377.4M when compared to the overall cash position of

2015.

b. For the 2015 financial year, explain why the change in cash occurred.

The change in cash occurred due to the increase in the cash inflow from the operating activities which was

sufficient in effectively meeting up with the outflow from the investing and financing activities.

c. For the 2016 financial year, explain why the change in cash occurred.

In 2016, there was a decrease in the cash flow from the operating activities while there was a negatively

outflow in the other two activities which resulted int net cash flow to be negative but the organization was

having huge amount of cash and cash equivalent in the beginning of the year which resulted into making

the cash balance positive.

5. In 2016 Woolworths Ltd reported a net loss of $2,347.9 million. The cash generated for this same

period was negative $384.1 million. Provide an explanation as to why the loss for the period is

different to the reduction in cash for the same period.

The loss for the period is different from that of the reduction in the cash balance in the same period which

is because of the reason that the income statement is prepared considering the accrual basis of accounting

while the cash flow statement is prepared using cash basis of accounting which only considers cash in and

out. The income statement accounts for credit sales and purchases while it is not so in the case of cash

flow statement.

6. In the Directors’ Declaration for Woolworths Ltd the Directors declare that in their opinion “there are

reasonable grounds to believe that the Company will be able to pay its debts as and when they

become due and payable”. Name one financial ratio that could confirm this statement and show the

value of that ratio for both 2015 and 2016. (Hint - you will need to access the Balance Sheet).

Name of financial ratio: Debt to Asset Ratio

2015 Calculation = Total debt/ Total assets = $ 14,204.8/$25,336.8 = 0.56

2016 Calculation = Total debt/ Total assets = $ 14,720.3/$23,502.2 = 0.62

The ratio of less 1 indicates that the company owns more assets than its liabilities and can effectively meet

its obligation by selling its assets as and when needed.

a. What was the overall change in cash for the financial year 2016 compared to the financial year

2015?

Overall, there was a recorded loss in 2016 of -$377.4M when compared to the overall cash position of

2015.

b. For the 2015 financial year, explain why the change in cash occurred.

The change in cash occurred due to the increase in the cash inflow from the operating activities which was

sufficient in effectively meeting up with the outflow from the investing and financing activities.

c. For the 2016 financial year, explain why the change in cash occurred.

In 2016, there was a decrease in the cash flow from the operating activities while there was a negatively

outflow in the other two activities which resulted int net cash flow to be negative but the organization was

having huge amount of cash and cash equivalent in the beginning of the year which resulted into making

the cash balance positive.

5. In 2016 Woolworths Ltd reported a net loss of $2,347.9 million. The cash generated for this same

period was negative $384.1 million. Provide an explanation as to why the loss for the period is

different to the reduction in cash for the same period.

The loss for the period is different from that of the reduction in the cash balance in the same period which

is because of the reason that the income statement is prepared considering the accrual basis of accounting

while the cash flow statement is prepared using cash basis of accounting which only considers cash in and

out. The income statement accounts for credit sales and purchases while it is not so in the case of cash

flow statement.

6. In the Directors’ Declaration for Woolworths Ltd the Directors declare that in their opinion “there are

reasonable grounds to believe that the Company will be able to pay its debts as and when they

become due and payable”. Name one financial ratio that could confirm this statement and show the

value of that ratio for both 2015 and 2016. (Hint - you will need to access the Balance Sheet).

Name of financial ratio: Debt to Asset Ratio

2015 Calculation = Total debt/ Total assets = $ 14,204.8/$25,336.8 = 0.56

2016 Calculation = Total debt/ Total assets = $ 14,720.3/$23,502.2 = 0.62

The ratio of less 1 indicates that the company owns more assets than its liabilities and can effectively meet

its obligation by selling its assets as and when needed.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BSBFIM601 Manage Finances

7. In the Directors’ Declaration for Woolworths Ltd the Directors declare that in their opinion, “the

attached financial statements are in compliance with International Financial Reporting Standards, as

stated in Note 1 to the financial statements” As part of Note 1 which is titled “Significant Accounting

Policies” there are 6 sections that relate to how Woolworths Ltd adheres to the Financial Reporting

Standards. List 4 of these areas.

1. Basics of consolidation

2. Cash and cash equivalents

3. Foreign currency

4. Goods and Services Tax (GST)

8. Which accounting firm were the auditors for Woolworths Ltd?

Deloitte Touch Tohmatsu

9. In the Independent Auditors’ Report, the audit opinion is provided. Which Regulations and Legislation

is referred to in this audit opinion?

In our opinion: (a) the financial report of Woolworths Limited is in accordance with the

Corporations Act 2001, including: (i) giving a true and fair view of the consolidated entity’s

financial position as at 26 June 2016 and of its performance for the financial year ended on

that date; and (ii) complying with Australian Accounting Standards and the Corporations

Regulations 2001; and (b) the consolidated financial statements also comply with

International Financial Reporting Standards as disclosed in the basis of preparation.

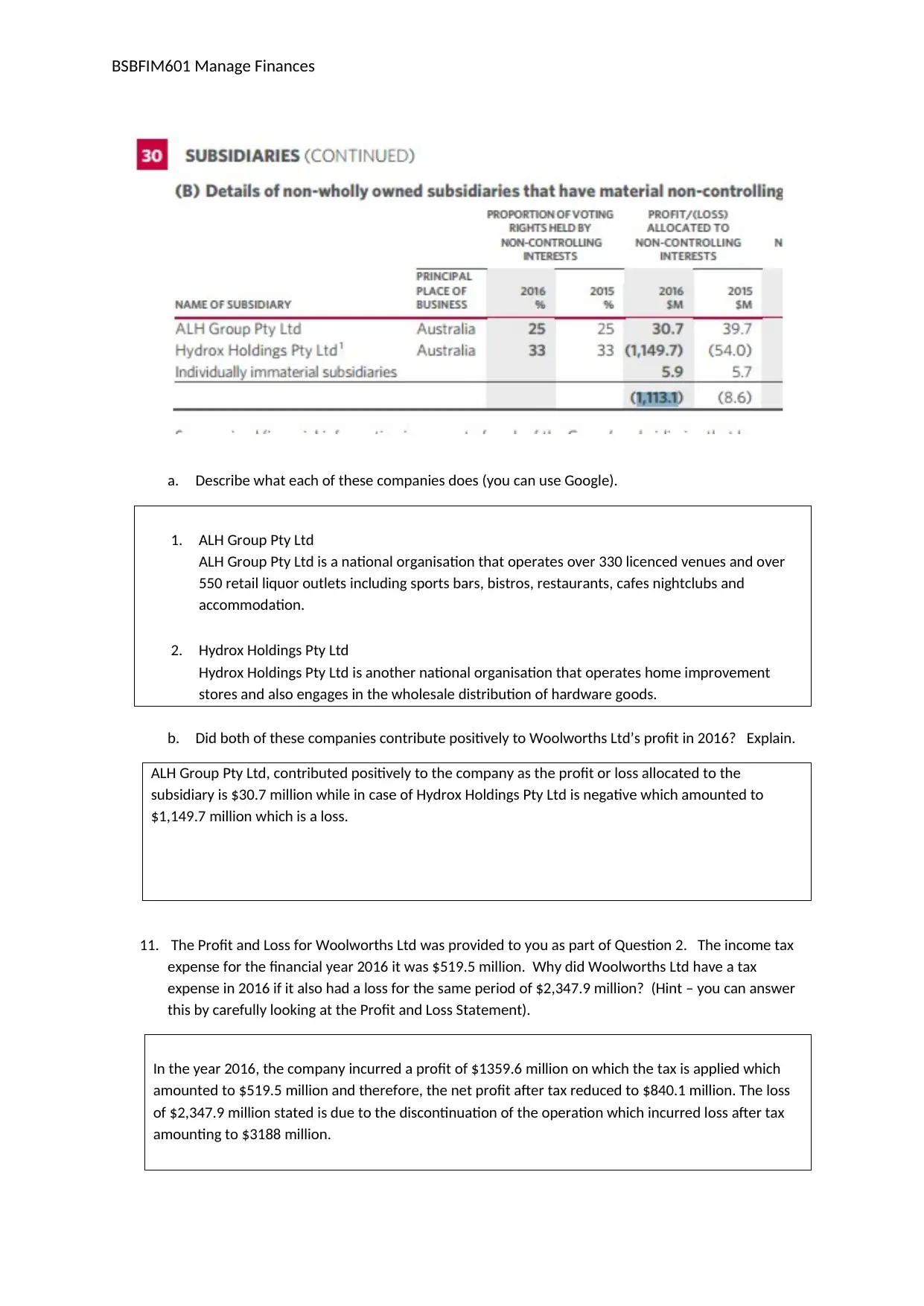

10. Note 30 to the financial statements (provided below), show the details of 2 companies that

Woolworths Ltd has part ownership of. The companies ALH Group Pty Ltd and Hydrox Holdings Pty

Ltd whilst not being 100% owned by Woolworths ltd, have had a significant effect on Woolworths

Ltd’s Profit or Loss.

7. In the Directors’ Declaration for Woolworths Ltd the Directors declare that in their opinion, “the

attached financial statements are in compliance with International Financial Reporting Standards, as

stated in Note 1 to the financial statements” As part of Note 1 which is titled “Significant Accounting

Policies” there are 6 sections that relate to how Woolworths Ltd adheres to the Financial Reporting

Standards. List 4 of these areas.

1. Basics of consolidation

2. Cash and cash equivalents

3. Foreign currency

4. Goods and Services Tax (GST)

8. Which accounting firm were the auditors for Woolworths Ltd?

Deloitte Touch Tohmatsu

9. In the Independent Auditors’ Report, the audit opinion is provided. Which Regulations and Legislation

is referred to in this audit opinion?

In our opinion: (a) the financial report of Woolworths Limited is in accordance with the

Corporations Act 2001, including: (i) giving a true and fair view of the consolidated entity’s

financial position as at 26 June 2016 and of its performance for the financial year ended on

that date; and (ii) complying with Australian Accounting Standards and the Corporations

Regulations 2001; and (b) the consolidated financial statements also comply with

International Financial Reporting Standards as disclosed in the basis of preparation.

10. Note 30 to the financial statements (provided below), show the details of 2 companies that

Woolworths Ltd has part ownership of. The companies ALH Group Pty Ltd and Hydrox Holdings Pty

Ltd whilst not being 100% owned by Woolworths ltd, have had a significant effect on Woolworths

Ltd’s Profit or Loss.

BSBFIM601 Manage Finances

a. Describe what each of these companies does (you can use Google).

1. ALH Group Pty Ltd

ALH Group Pty Ltd is a national organisation that operates over 330 licenced venues and over

550 retail liquor outlets including sports bars, bistros, restaurants, cafes nightclubs and

accommodation.

2. Hydrox Holdings Pty Ltd

Hydrox Holdings Pty Ltd is another national organisation that operates home improvement

stores and also engages in the wholesale distribution of hardware goods.

b. Did both of these companies contribute positively to Woolworths Ltd’s profit in 2016? Explain.

ALH Group Pty Ltd, contributed positively to the company as the profit or loss allocated to the

subsidiary is $30.7 million while in case of Hydrox Holdings Pty Ltd is negative which amounted to

$1,149.7 million which is a loss.

11. The Profit and Loss for Woolworths Ltd was provided to you as part of Question 2. The income tax

expense for the financial year 2016 it was $519.5 million. Why did Woolworths Ltd have a tax

expense in 2016 if it also had a loss for the same period of $2,347.9 million? (Hint – you can answer

this by carefully looking at the Profit and Loss Statement).

In the year 2016, the company incurred a profit of $1359.6 million on which the tax is applied which

amounted to $519.5 million and therefore, the net profit after tax reduced to $840.1 million. The loss

of $2,347.9 million stated is due to the discontinuation of the operation which incurred loss after tax

amounting to $3188 million.

a. Describe what each of these companies does (you can use Google).

1. ALH Group Pty Ltd

ALH Group Pty Ltd is a national organisation that operates over 330 licenced venues and over

550 retail liquor outlets including sports bars, bistros, restaurants, cafes nightclubs and

accommodation.

2. Hydrox Holdings Pty Ltd

Hydrox Holdings Pty Ltd is another national organisation that operates home improvement

stores and also engages in the wholesale distribution of hardware goods.

b. Did both of these companies contribute positively to Woolworths Ltd’s profit in 2016? Explain.

ALH Group Pty Ltd, contributed positively to the company as the profit or loss allocated to the

subsidiary is $30.7 million while in case of Hydrox Holdings Pty Ltd is negative which amounted to

$1,149.7 million which is a loss.

11. The Profit and Loss for Woolworths Ltd was provided to you as part of Question 2. The income tax

expense for the financial year 2016 it was $519.5 million. Why did Woolworths Ltd have a tax

expense in 2016 if it also had a loss for the same period of $2,347.9 million? (Hint – you can answer

this by carefully looking at the Profit and Loss Statement).

In the year 2016, the company incurred a profit of $1359.6 million on which the tax is applied which

amounted to $519.5 million and therefore, the net profit after tax reduced to $840.1 million. The loss

of $2,347.9 million stated is due to the discontinuation of the operation which incurred loss after tax

amounting to $3188 million.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BSBFIM601 Manage Finances

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BSBFIM601 Manage Finances

Assessment Activity 2

Analysis

Demo Company

Activity instructions to candidates

This is an open book assessment activity.

You are required to read this assessment and answer all 3 questions that follow.

Please ensure you have read “Important assessment information” at the front of this assessment

Assessment Activity 2

Analysis

Demo Company

Activity instructions to candidates

This is an open book assessment activity.

You are required to read this assessment and answer all 3 questions that follow.

Please ensure you have read “Important assessment information” at the front of this assessment

BSBFIM601 Manage Finances

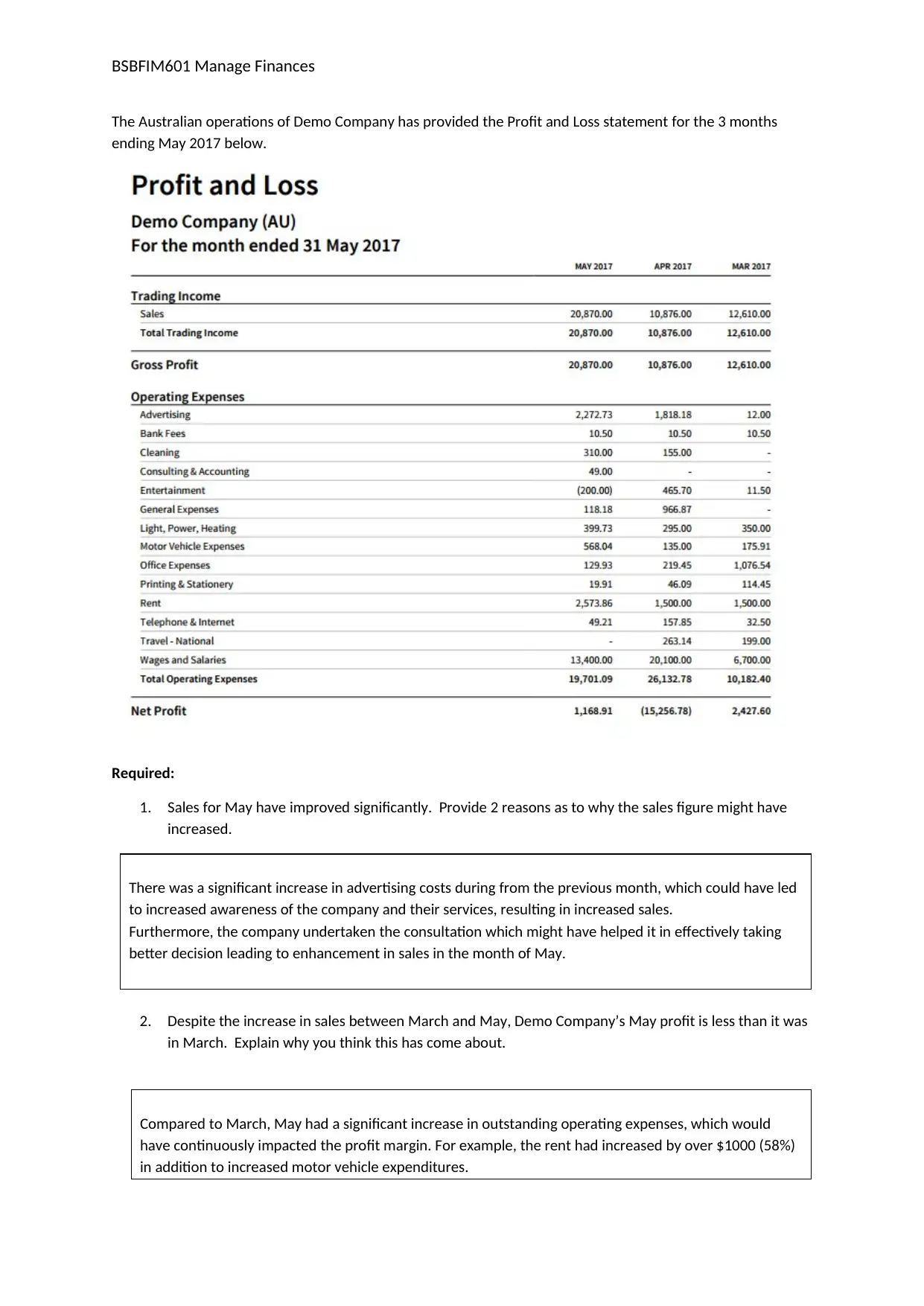

The Australian operations of Demo Company has provided the Profit and Loss statement for the 3 months

ending May 2017 below.

Required:

1. Sales for May have improved significantly. Provide 2 reasons as to why the sales figure might have

increased.

There was a significant increase in advertising costs during from the previous month, which could have led

to increased awareness of the company and their services, resulting in increased sales.

Furthermore, the company undertaken the consultation which might have helped it in effectively taking

better decision leading to enhancement in sales in the month of May.

2. Despite the increase in sales between March and May, Demo Company’s May profit is less than it was

in March. Explain why you think this has come about.

Compared to March, May had a significant increase in outstanding operating expenses, which would

have continuously impacted the profit margin. For example, the rent had increased by over $1000 (58%)

in addition to increased motor vehicle expenditures.

The Australian operations of Demo Company has provided the Profit and Loss statement for the 3 months

ending May 2017 below.

Required:

1. Sales for May have improved significantly. Provide 2 reasons as to why the sales figure might have

increased.

There was a significant increase in advertising costs during from the previous month, which could have led

to increased awareness of the company and their services, resulting in increased sales.

Furthermore, the company undertaken the consultation which might have helped it in effectively taking

better decision leading to enhancement in sales in the month of May.

2. Despite the increase in sales between March and May, Demo Company’s May profit is less than it was

in March. Explain why you think this has come about.

Compared to March, May had a significant increase in outstanding operating expenses, which would

have continuously impacted the profit margin. For example, the rent had increased by over $1000 (58%)

in addition to increased motor vehicle expenditures.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.