University Financial Budget Management Questionnaire and Case Study

VerifiedAdded on 2023/03/31

|19

|3265

|362

Homework Assignment

AI Summary

This assignment, focusing on financial budget management, is divided into two parts: a questionnaire and a case study. The questionnaire explores various aspects of budgeting, including the finance manager's role in budget communication, monitoring and control activities, sales variance reports, fixed and variable costs, vertical analysis, inventory turnover, budget information communication, controllable and uncontrollable costs, risk management, contingency plans, the responsibilities of budget holders, and the Corporations Act. The case study delves into accounting principles, government legislation, and their implications in financial contexts. The assignment aims to provide a comprehensive understanding of financial planning, budgeting, and control within a business setting.

Running head: MANAGE FINANCIAL BUDGET

Manage Financial Budget

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Manage Financial Budget

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGE FINANCIAL BUDGET

Table of Contents

Part 1: Questionnaire.......................................................................................................................3

Answer to Question 1:.................................................................................................................3

Answer to Question 2:.................................................................................................................3

Answer to Question 3:.................................................................................................................3

Answer to Question 4:.................................................................................................................4

Answer to Question 5:.................................................................................................................5

Answer to Question 6:.................................................................................................................5

Answer to Question 7:.................................................................................................................5

Answer to Question 8:.................................................................................................................6

Answer to Question 9:.................................................................................................................6

Answer to Question 10:...............................................................................................................7

Answer to Question 11:...............................................................................................................7

Answer to Question 12:...............................................................................................................7

Answer to Question 13:...............................................................................................................8

Answer to Question 14:...............................................................................................................8

Answer to Question 15:...............................................................................................................8

Answer to Question 16:...............................................................................................................9

Answer to Question 17:...............................................................................................................9

Table of Contents

Part 1: Questionnaire.......................................................................................................................3

Answer to Question 1:.................................................................................................................3

Answer to Question 2:.................................................................................................................3

Answer to Question 3:.................................................................................................................3

Answer to Question 4:.................................................................................................................4

Answer to Question 5:.................................................................................................................5

Answer to Question 6:.................................................................................................................5

Answer to Question 7:.................................................................................................................5

Answer to Question 8:.................................................................................................................6

Answer to Question 9:.................................................................................................................6

Answer to Question 10:...............................................................................................................7

Answer to Question 11:...............................................................................................................7

Answer to Question 12:...............................................................................................................7

Answer to Question 13:...............................................................................................................8

Answer to Question 14:...............................................................................................................8

Answer to Question 15:...............................................................................................................8

Answer to Question 16:...............................................................................................................9

Answer to Question 17:...............................................................................................................9

2MANAGE FINANCIAL BUDGET

Answer to Question 18:.............................................................................................................10

Answer to Question 19:.............................................................................................................10

Answer to Question 20:.............................................................................................................12

Answer to Question 21:.............................................................................................................12

Answer to Question 22:.............................................................................................................12

Answer to Question 23:.............................................................................................................13

Answer to Question 24:.............................................................................................................13

Part 2: Case Study..........................................................................................................................13

Section 1: Accounting Principles and Government Legislation................................................13

Answer to Question 1:...........................................................................................................13

Answer to Question 2:...........................................................................................................14

Answer to Question 3:...........................................................................................................14

Answer to Question 4:...........................................................................................................14

Answer to Question 5:...........................................................................................................15

Answer to Question 6:...........................................................................................................15

References:....................................................................................................................................16

Answer to Question 18:.............................................................................................................10

Answer to Question 19:.............................................................................................................10

Answer to Question 20:.............................................................................................................12

Answer to Question 21:.............................................................................................................12

Answer to Question 22:.............................................................................................................12

Answer to Question 23:.............................................................................................................13

Answer to Question 24:.............................................................................................................13

Part 2: Case Study..........................................................................................................................13

Section 1: Accounting Principles and Government Legislation................................................13

Answer to Question 1:...........................................................................................................13

Answer to Question 2:...........................................................................................................14

Answer to Question 3:...........................................................................................................14

Answer to Question 4:...........................................................................................................14

Answer to Question 5:...........................................................................................................15

Answer to Question 6:...........................................................................................................15

References:....................................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGE FINANCIAL BUDGET

Part 1: Questionnaire

Answer to Question 1:

Finance managers are primarily accountable to collate and submit institutional financial

estimations. Some process operates top-down approach, while the others follow bottom-up

approach. The financial manager provides advice regarding the most suitable approach that

would be deemed fit for the organisation (Atanasov and Black 2016). Moreover, the financial

manager is involved in general oversight by reviewing the monthly reports at least monthly for

his responsibility areas and increasing issues and accordingly, the same is communicated to the

top management.

Answer to Question 2:

For ensuring the success of the budget objectives, the occurrence of monitoring and

control activities would take place after the following:

Budget for the activity area for the entire period along with profiling for the year to date

Actual expenditure until date

Future commitments of expenditure

Balance of the remaining yearly budget

Evaluation and description of any favourable or unfavourable variances

Thus, monitoring and control activities primarily adjoin with execution activities owing

to their occurrence.

Part 1: Questionnaire

Answer to Question 1:

Finance managers are primarily accountable to collate and submit institutional financial

estimations. Some process operates top-down approach, while the others follow bottom-up

approach. The financial manager provides advice regarding the most suitable approach that

would be deemed fit for the organisation (Atanasov and Black 2016). Moreover, the financial

manager is involved in general oversight by reviewing the monthly reports at least monthly for

his responsibility areas and increasing issues and accordingly, the same is communicated to the

top management.

Answer to Question 2:

For ensuring the success of the budget objectives, the occurrence of monitoring and

control activities would take place after the following:

Budget for the activity area for the entire period along with profiling for the year to date

Actual expenditure until date

Future commitments of expenditure

Balance of the remaining yearly budget

Evaluation and description of any favourable or unfavourable variances

Thus, monitoring and control activities primarily adjoin with execution activities owing

to their occurrence.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGE FINANCIAL BUDGET

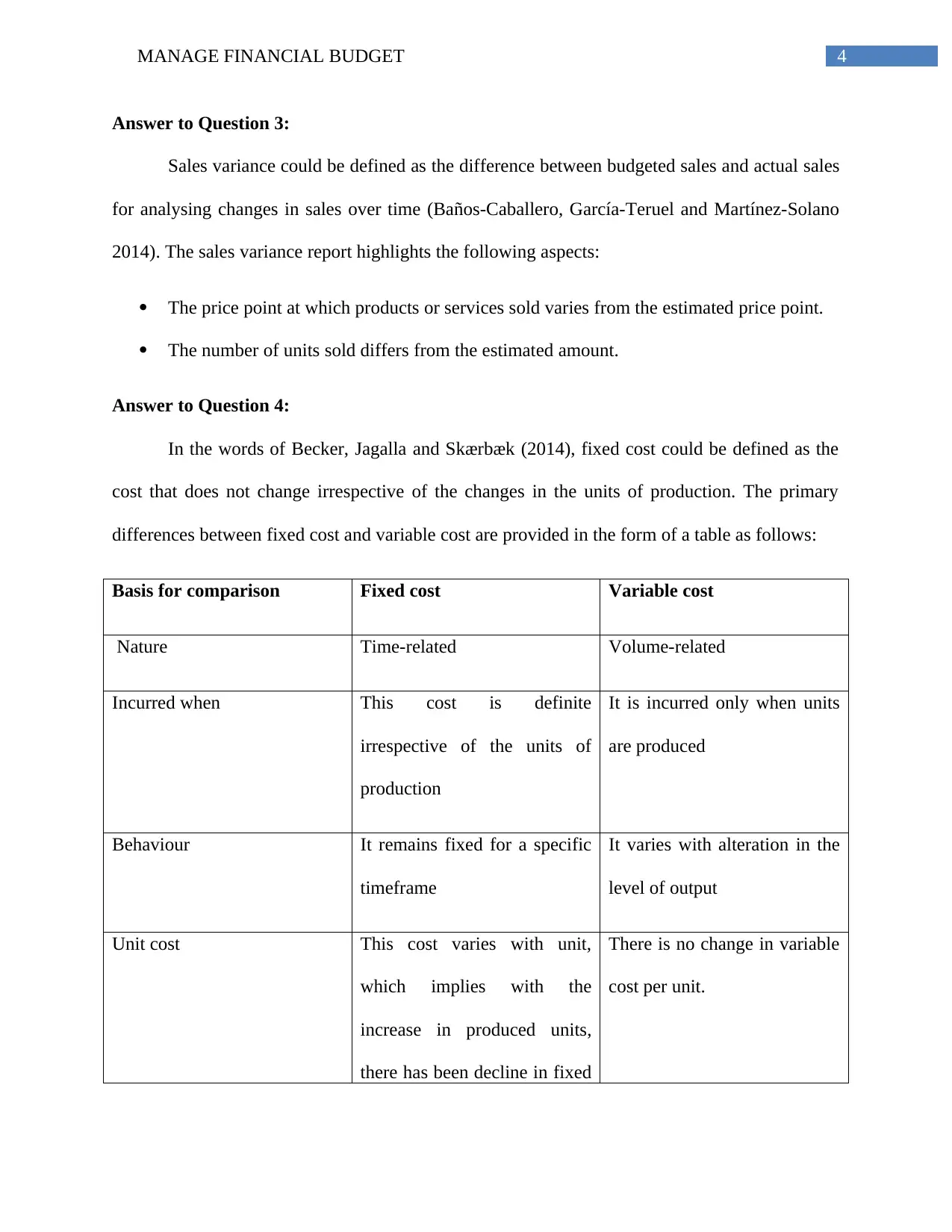

Answer to Question 3:

Sales variance could be defined as the difference between budgeted sales and actual sales

for analysing changes in sales over time (Baños-Caballero, García-Teruel and Martínez-Solano

2014). The sales variance report highlights the following aspects:

The price point at which products or services sold varies from the estimated price point.

The number of units sold differs from the estimated amount.

Answer to Question 4:

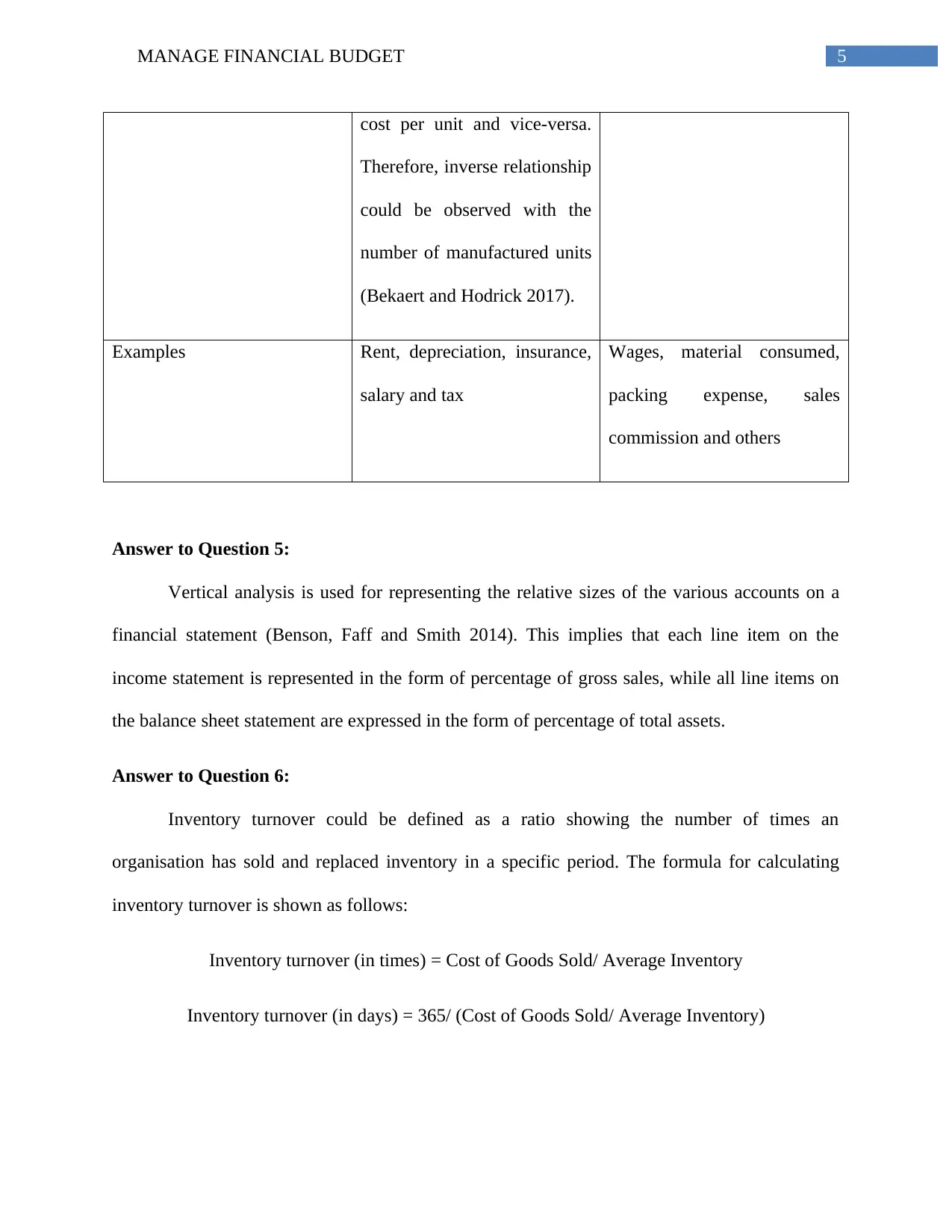

In the words of Becker, Jagalla and Skærbæk (2014), fixed cost could be defined as the

cost that does not change irrespective of the changes in the units of production. The primary

differences between fixed cost and variable cost are provided in the form of a table as follows:

Basis for comparison Fixed cost Variable cost

Nature Time-related Volume-related

Incurred when This cost is definite

irrespective of the units of

production

It is incurred only when units

are produced

Behaviour It remains fixed for a specific

timeframe

It varies with alteration in the

level of output

Unit cost This cost varies with unit,

which implies with the

increase in produced units,

there has been decline in fixed

There is no change in variable

cost per unit.

Answer to Question 3:

Sales variance could be defined as the difference between budgeted sales and actual sales

for analysing changes in sales over time (Baños-Caballero, García-Teruel and Martínez-Solano

2014). The sales variance report highlights the following aspects:

The price point at which products or services sold varies from the estimated price point.

The number of units sold differs from the estimated amount.

Answer to Question 4:

In the words of Becker, Jagalla and Skærbæk (2014), fixed cost could be defined as the

cost that does not change irrespective of the changes in the units of production. The primary

differences between fixed cost and variable cost are provided in the form of a table as follows:

Basis for comparison Fixed cost Variable cost

Nature Time-related Volume-related

Incurred when This cost is definite

irrespective of the units of

production

It is incurred only when units

are produced

Behaviour It remains fixed for a specific

timeframe

It varies with alteration in the

level of output

Unit cost This cost varies with unit,

which implies with the

increase in produced units,

there has been decline in fixed

There is no change in variable

cost per unit.

5MANAGE FINANCIAL BUDGET

cost per unit and vice-versa.

Therefore, inverse relationship

could be observed with the

number of manufactured units

(Bekaert and Hodrick 2017).

Examples Rent, depreciation, insurance,

salary and tax

Wages, material consumed,

packing expense, sales

commission and others

Answer to Question 5:

Vertical analysis is used for representing the relative sizes of the various accounts on a

financial statement (Benson, Faff and Smith 2014). This implies that each line item on the

income statement is represented in the form of percentage of gross sales, while all line items on

the balance sheet statement are expressed in the form of percentage of total assets.

Answer to Question 6:

Inventory turnover could be defined as a ratio showing the number of times an

organisation has sold and replaced inventory in a specific period. The formula for calculating

inventory turnover is shown as follows:

Inventory turnover (in times) = Cost of Goods Sold/ Average Inventory

Inventory turnover (in days) = 365/ (Cost of Goods Sold/ Average Inventory)

cost per unit and vice-versa.

Therefore, inverse relationship

could be observed with the

number of manufactured units

(Bekaert and Hodrick 2017).

Examples Rent, depreciation, insurance,

salary and tax

Wages, material consumed,

packing expense, sales

commission and others

Answer to Question 5:

Vertical analysis is used for representing the relative sizes of the various accounts on a

financial statement (Benson, Faff and Smith 2014). This implies that each line item on the

income statement is represented in the form of percentage of gross sales, while all line items on

the balance sheet statement are expressed in the form of percentage of total assets.

Answer to Question 6:

Inventory turnover could be defined as a ratio showing the number of times an

organisation has sold and replaced inventory in a specific period. The formula for calculating

inventory turnover is shown as follows:

Inventory turnover (in times) = Cost of Goods Sold/ Average Inventory

Inventory turnover (in days) = 365/ (Cost of Goods Sold/ Average Inventory)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGE FINANCIAL BUDGET

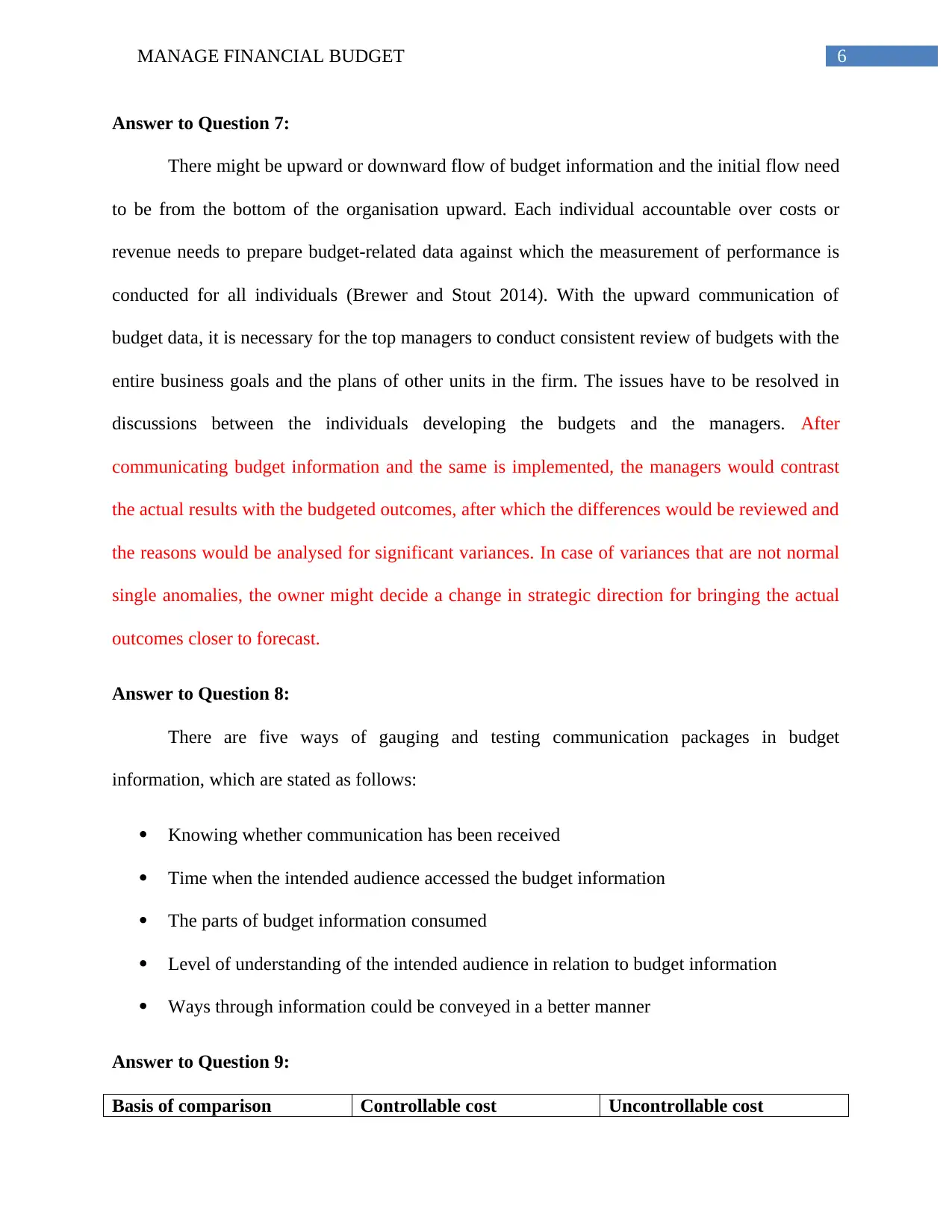

Answer to Question 7:

There might be upward or downward flow of budget information and the initial flow need

to be from the bottom of the organisation upward. Each individual accountable over costs or

revenue needs to prepare budget-related data against which the measurement of performance is

conducted for all individuals (Brewer and Stout 2014). With the upward communication of

budget data, it is necessary for the top managers to conduct consistent review of budgets with the

entire business goals and the plans of other units in the firm. The issues have to be resolved in

discussions between the individuals developing the budgets and the managers. After

communicating budget information and the same is implemented, the managers would contrast

the actual results with the budgeted outcomes, after which the differences would be reviewed and

the reasons would be analysed for significant variances. In case of variances that are not normal

single anomalies, the owner might decide a change in strategic direction for bringing the actual

outcomes closer to forecast.

Answer to Question 8:

There are five ways of gauging and testing communication packages in budget

information, which are stated as follows:

Knowing whether communication has been received

Time when the intended audience accessed the budget information

The parts of budget information consumed

Level of understanding of the intended audience in relation to budget information

Ways through information could be conveyed in a better manner

Answer to Question 9:

Basis of comparison Controllable cost Uncontrollable cost

Answer to Question 7:

There might be upward or downward flow of budget information and the initial flow need

to be from the bottom of the organisation upward. Each individual accountable over costs or

revenue needs to prepare budget-related data against which the measurement of performance is

conducted for all individuals (Brewer and Stout 2014). With the upward communication of

budget data, it is necessary for the top managers to conduct consistent review of budgets with the

entire business goals and the plans of other units in the firm. The issues have to be resolved in

discussions between the individuals developing the budgets and the managers. After

communicating budget information and the same is implemented, the managers would contrast

the actual results with the budgeted outcomes, after which the differences would be reviewed and

the reasons would be analysed for significant variances. In case of variances that are not normal

single anomalies, the owner might decide a change in strategic direction for bringing the actual

outcomes closer to forecast.

Answer to Question 8:

There are five ways of gauging and testing communication packages in budget

information, which are stated as follows:

Knowing whether communication has been received

Time when the intended audience accessed the budget information

The parts of budget information consumed

Level of understanding of the intended audience in relation to budget information

Ways through information could be conveyed in a better manner

Answer to Question 9:

Basis of comparison Controllable cost Uncontrollable cost

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGE FINANCIAL BUDGET

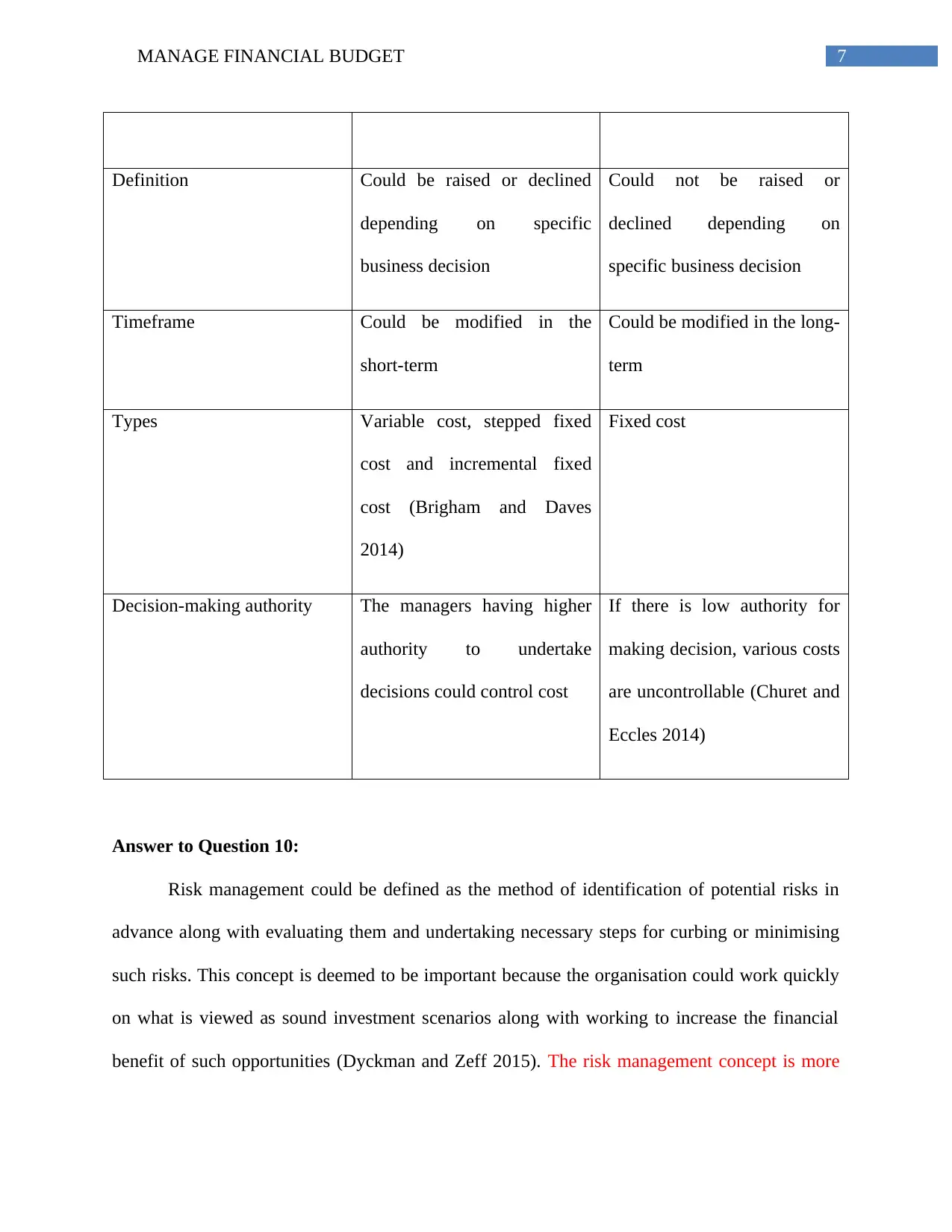

Definition Could be raised or declined

depending on specific

business decision

Could not be raised or

declined depending on

specific business decision

Timeframe Could be modified in the

short-term

Could be modified in the long-

term

Types Variable cost, stepped fixed

cost and incremental fixed

cost (Brigham and Daves

2014)

Fixed cost

Decision-making authority The managers having higher

authority to undertake

decisions could control cost

If there is low authority for

making decision, various costs

are uncontrollable (Churet and

Eccles 2014)

Answer to Question 10:

Risk management could be defined as the method of identification of potential risks in

advance along with evaluating them and undertaking necessary steps for curbing or minimising

such risks. This concept is deemed to be important because the organisation could work quickly

on what is viewed as sound investment scenarios along with working to increase the financial

benefit of such opportunities (Dyckman and Zeff 2015). The risk management concept is more

Definition Could be raised or declined

depending on specific

business decision

Could not be raised or

declined depending on

specific business decision

Timeframe Could be modified in the

short-term

Could be modified in the long-

term

Types Variable cost, stepped fixed

cost and incremental fixed

cost (Brigham and Daves

2014)

Fixed cost

Decision-making authority The managers having higher

authority to undertake

decisions could control cost

If there is low authority for

making decision, various costs

are uncontrollable (Churet and

Eccles 2014)

Answer to Question 10:

Risk management could be defined as the method of identification of potential risks in

advance along with evaluating them and undertaking necessary steps for curbing or minimising

such risks. This concept is deemed to be important because the organisation could work quickly

on what is viewed as sound investment scenarios along with working to increase the financial

benefit of such opportunities (Dyckman and Zeff 2015). The risk management concept is more

8MANAGE FINANCIAL BUDGET

important for some organisations like manufacturing companies because they are more prone to

environmental risk.

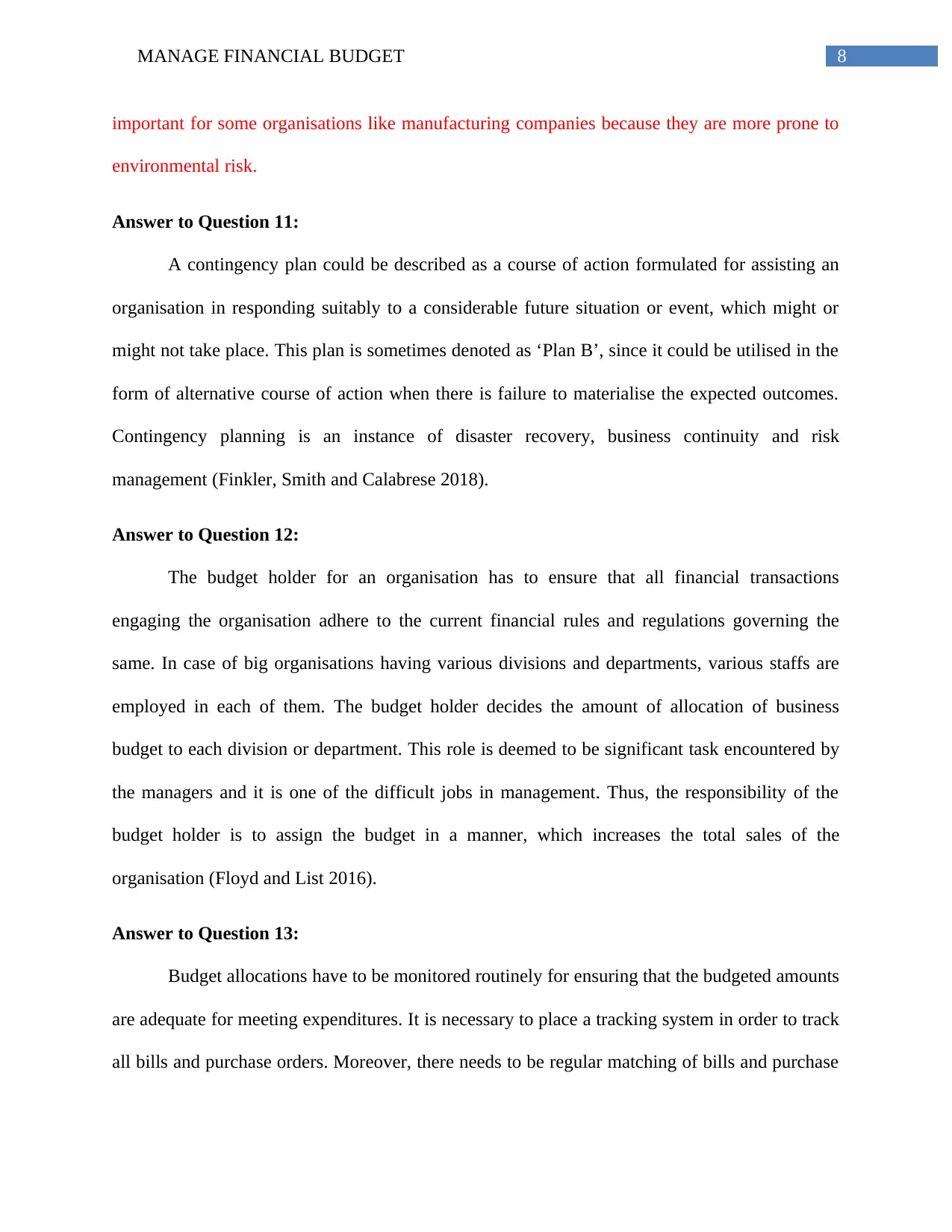

Answer to Question 11:

A contingency plan could be described as a course of action formulated for assisting an

organisation in responding suitably to a considerable future situation or event, which might or

might not take place. This plan is sometimes denoted as ‘Plan B’, since it could be utilised in the

form of alternative course of action when there is failure to materialise the expected outcomes.

Contingency planning is an instance of disaster recovery, business continuity and risk

management (Finkler, Smith and Calabrese 2018).

Answer to Question 12:

The budget holder for an organisation has to ensure that all financial transactions

engaging the organisation adhere to the current financial rules and regulations governing the

same. In case of big organisations having various divisions and departments, various staffs are

employed in each of them. The budget holder decides the amount of allocation of business

budget to each division or department. This role is deemed to be significant task encountered by

the managers and it is one of the difficult jobs in management. Thus, the responsibility of the

budget holder is to assign the budget in a manner, which increases the total sales of the

organisation (Floyd and List 2016).

Answer to Question 13:

Budget allocations have to be monitored routinely for ensuring that the budgeted amounts

are adequate for meeting expenditures. It is necessary to place a tracking system in order to track

all bills and purchase orders. Moreover, there needs to be regular matching of bills and purchase

important for some organisations like manufacturing companies because they are more prone to

environmental risk.

Answer to Question 11:

A contingency plan could be described as a course of action formulated for assisting an

organisation in responding suitably to a considerable future situation or event, which might or

might not take place. This plan is sometimes denoted as ‘Plan B’, since it could be utilised in the

form of alternative course of action when there is failure to materialise the expected outcomes.

Contingency planning is an instance of disaster recovery, business continuity and risk

management (Finkler, Smith and Calabrese 2018).

Answer to Question 12:

The budget holder for an organisation has to ensure that all financial transactions

engaging the organisation adhere to the current financial rules and regulations governing the

same. In case of big organisations having various divisions and departments, various staffs are

employed in each of them. The budget holder decides the amount of allocation of business

budget to each division or department. This role is deemed to be significant task encountered by

the managers and it is one of the difficult jobs in management. Thus, the responsibility of the

budget holder is to assign the budget in a manner, which increases the total sales of the

organisation (Floyd and List 2016).

Answer to Question 13:

Budget allocations have to be monitored routinely for ensuring that the budgeted amounts

are adequate for meeting expenditures. It is necessary to place a tracking system in order to track

all bills and purchase orders. Moreover, there needs to be regular matching of bills and purchase

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGE FINANCIAL BUDGET

orders for assuring the existence of considerable funds for the remaining budget period (Karadag

2015).

Answer to Question 14:

The Corporations Act 2001 is an act of the Commonwealth of Australia, which is

administered by the Australian Securities and Investments Commission (ASIC) in Australia.

Answer to Question 15:

The Corporations Act 2001 is involved in setting out the laws dealing with the business

organisations in Australia at the interstate and federal levels. It is involved in dealing mainly with

the organisations along with other entities like managed investment schemes and partnerships. It

is the primary basis associated with the Australian Corporations Law (Kelly and Rivenbark

2014). It covers the following legislations:

Australian Securities and Investments Commissions Act 2001

Insurance Contracts Act 1984

Life Insurance Act 1995

Answer to Question 16:

Variance analysis could be defined as an evaluation of the difference between actual and

planned figures. The total of all variances provide a picture of overall under-performance or

over-performance for a specific reporting period (Loughran and McDonald 2016). For all

individual items, an organisation analyses its favourability by contrasting standard costs with

actual costs and the standard industrial costs. The reason that variance occurs could be explained

with the help of the following example.

orders for assuring the existence of considerable funds for the remaining budget period (Karadag

2015).

Answer to Question 14:

The Corporations Act 2001 is an act of the Commonwealth of Australia, which is

administered by the Australian Securities and Investments Commission (ASIC) in Australia.

Answer to Question 15:

The Corporations Act 2001 is involved in setting out the laws dealing with the business

organisations in Australia at the interstate and federal levels. It is involved in dealing mainly with

the organisations along with other entities like managed investment schemes and partnerships. It

is the primary basis associated with the Australian Corporations Law (Kelly and Rivenbark

2014). It covers the following legislations:

Australian Securities and Investments Commissions Act 2001

Insurance Contracts Act 1984

Life Insurance Act 1995

Answer to Question 16:

Variance analysis could be defined as an evaluation of the difference between actual and

planned figures. The total of all variances provide a picture of overall under-performance or

over-performance for a specific reporting period (Loughran and McDonald 2016). For all

individual items, an organisation analyses its favourability by contrasting standard costs with

actual costs and the standard industrial costs. The reason that variance occurs could be explained

with the help of the following example.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGE FINANCIAL BUDGET

If the standard cost is more than the actual cost for raw materials by taking into

consideration the same quantity of materials, it would result in favourable price variance or in

other words, cost savings. However; in case, the standard quantity has been 5,000 units and the

required production units have been 10,000 units, unfavourable quantity variance would occur

owing to the usage of more materials compared to the estimation.

Answer to Question 17:

A flexible budget termed as variable budget, could be defined as a financial plan of

projected expenses and revenues depending on the existing actual output level. More

specifically, a flexible budget is involved in utilising expenses and revenues produced in the

existing production in the form of a baseline along with estimating the changes in expenses and

revenues depending on variations in output. This is the main reason; it is termed as a variable

budget as well (Pandey 2015). The management of an organisation utilises flexible budget for

the coming accounting period. This allows “what if” view at the future of the financial

performance of the concerned organisation.

Answer to Question 18:

A remedial action could be defined as the change undertaken to a non-conforming service

or product for addressing the deficiency. This could be denoted as the restoration of landscape

from industrial activity. Generally, repairs and reworks are the remedial measures undertaken on

products, while services generally need additional services to be conducted for assuring

satisfaction.

The factors that might influence the appropriate remedial actions include the following:

Environmental factors:

If the standard cost is more than the actual cost for raw materials by taking into

consideration the same quantity of materials, it would result in favourable price variance or in

other words, cost savings. However; in case, the standard quantity has been 5,000 units and the

required production units have been 10,000 units, unfavourable quantity variance would occur

owing to the usage of more materials compared to the estimation.

Answer to Question 17:

A flexible budget termed as variable budget, could be defined as a financial plan of

projected expenses and revenues depending on the existing actual output level. More

specifically, a flexible budget is involved in utilising expenses and revenues produced in the

existing production in the form of a baseline along with estimating the changes in expenses and

revenues depending on variations in output. This is the main reason; it is termed as a variable

budget as well (Pandey 2015). The management of an organisation utilises flexible budget for

the coming accounting period. This allows “what if” view at the future of the financial

performance of the concerned organisation.

Answer to Question 18:

A remedial action could be defined as the change undertaken to a non-conforming service

or product for addressing the deficiency. This could be denoted as the restoration of landscape

from industrial activity. Generally, repairs and reworks are the remedial measures undertaken on

products, while services generally need additional services to be conducted for assuring

satisfaction.

The factors that might influence the appropriate remedial actions include the following:

Environmental factors:

11MANAGE FINANCIAL BUDGET

If the environment of an organisation becomes polluted because of the outcomes of the

business operations or other events on certain occasions, the pollution needs to be cleaned for

reasons of welfare and society. This would generally involve the organisation either funding the

remedial action or application for the finances to conduct the same (Quattrone 2016). When the

organisation is not found to be at fault, the government might fund the remediation.

Replacement or repair factors:

When any product is found to be ineffective either by the public exposure or by the

organisation, it is necessary to place recall plan into action including the compensation for the

consumers on certain occasions.

Answer to Question 19:

The important factors for ensuring the success of the remedial action are provided as

follows:

Planning:

Planning is the necessary prerequisite for ensuring the success of the remedial action. It is

necessary to assure that the objectives should be specific in order to ascertain their achievement

and the predetermined course of action has to be used for fulfilling different objectives. The

remedial action would be effective only when the plans and objectives are set, if they are

enforced properly.

Action:

If the environment of an organisation becomes polluted because of the outcomes of the

business operations or other events on certain occasions, the pollution needs to be cleaned for

reasons of welfare and society. This would generally involve the organisation either funding the

remedial action or application for the finances to conduct the same (Quattrone 2016). When the

organisation is not found to be at fault, the government might fund the remediation.

Replacement or repair factors:

When any product is found to be ineffective either by the public exposure or by the

organisation, it is necessary to place recall plan into action including the compensation for the

consumers on certain occasions.

Answer to Question 19:

The important factors for ensuring the success of the remedial action are provided as

follows:

Planning:

Planning is the necessary prerequisite for ensuring the success of the remedial action. It is

necessary to assure that the objectives should be specific in order to ascertain their achievement

and the predetermined course of action has to be used for fulfilling different objectives. The

remedial action would be effective only when the plans and objectives are set, if they are

enforced properly.

Action:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.