Management Accounting Report: Evaluation of TPG Processing System

VerifiedAdded on 2020/12/10

|25

|7683

|231

Report

AI Summary

This report provides a detailed analysis of management accounting principles and their practical application within TPG Processing, a manufacturing company. It begins with an introduction to management accounting, differentiating it from financial accounting and emphasizing its role in internal decision-making. The report then explores the functions of management accounting, including planning, control, cost accounting, and decision-making. It delves into various management accounting systems such as cost accounting, inventory management, job costing, and price optimization, illustrating their use within TPG Processing. Furthermore, the report examines different types of management accounting reports, including budget reports, accounts receivable aging reports, and performance reports. It critically evaluates how management accounting is integrated within the organization and highlights the benefits of these systems, such as improved cost control and better decision-making. The report also covers cost analysis techniques and the advantages and disadvantages of budgetary control planning tools. It explores how management accounting can be used to address financial problems and lead an organization toward sustainable success. The report concludes by summarizing the key findings and emphasizing the importance of management accounting in modern business operations.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

PART A...........................................................................................................................................1

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

P1 Management Accounting Explanation..............................................................................1

Roles Functions of Management accounting.........................................................................2

Management Accounting System...........................................................................................2

P2 Types Of Reports..............................................................................................................4

D1 Critical evaluation of how management accounting is integrated within the organization5

M1 Benefits of the system and their application....................................................................5

CONCLUSION................................................................................................................................6

PART B............................................................................................................................................6

INTRODUCTION...........................................................................................................................6

P3 Calculate cost using appropriate techniques of cost analysis............................................7

P4 Advantage and disadvantage of different types of planning tools of budgetary control.13

M3 Use of different planning tools and their application.....................................................17

P5 Organisation could use management accounting to respond to financial problem.........17

M4 Financial problems, management accounting can lead organisation to sustainable success

..............................................................................................................................................21

D3 Planning tools effectively respond to solving financial problems to lead organisation to

sustainable success...............................................................................................................21

CONCLUSION..............................................................................................................................21

REFERENCES..............................................................................................................................22

PART A...........................................................................................................................................1

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

P1 Management Accounting Explanation..............................................................................1

Roles Functions of Management accounting.........................................................................2

Management Accounting System...........................................................................................2

P2 Types Of Reports..............................................................................................................4

D1 Critical evaluation of how management accounting is integrated within the organization5

M1 Benefits of the system and their application....................................................................5

CONCLUSION................................................................................................................................6

PART B............................................................................................................................................6

INTRODUCTION...........................................................................................................................6

P3 Calculate cost using appropriate techniques of cost analysis............................................7

P4 Advantage and disadvantage of different types of planning tools of budgetary control.13

M3 Use of different planning tools and their application.....................................................17

P5 Organisation could use management accounting to respond to financial problem.........17

M4 Financial problems, management accounting can lead organisation to sustainable success

..............................................................................................................................................21

D3 Planning tools effectively respond to solving financial problems to lead organisation to

sustainable success...............................................................................................................21

CONCLUSION..............................................................................................................................21

REFERENCES..............................................................................................................................22

PART A

INTRODUCTION

Management accounting is the process of preparing management reports and accounts

that provide authentic and relatable information on time (Saleem Salem Alzoubi, 2016). These

information presented in financial and statical way in front of managers which is helping to make

day to day and short term decisions. It is different from financial accounting because in

management accounting reports and accounts are presented in front of managers on weekly and

monthly basis while in financial accounting reports are presented to investors, creditors, clients

and managers to annually basis. To understand the concept of the report selected company TPG

Processing which is related to manufacturing sector. In the report consist of explanation of

management accounting and their role. Apart from report define elements of different types of

management accounting system and different methods of management accounting reporting.

Further, evaluation the benefits of system and integrated with organisational process.

MAIN BODY

P1 Management Accounting Explanation

As per the IMA (Institute of management accountants): The management accounting may

be defined as a kind of process which is related with the decision making, planning and

performance management system in the aspect of the financial reporting. The aim of doing so, is

to control the assist management in the formulation and implementation of the strategies.

(Cleary, 2015).

From the definition it has been understand that management accounting is continuous

process which can help to manage performance of company in effective manner.

As per the the Chartered Institute of Management Accountants (CIMA): The

management accounting can be defined as the process that involves measurement, accumulation,

preparation and communicating the information and data which is being used by the managers to

make suitable decisions (Suprianto and et.al, 2017).

As per the above definition it has been understand that in management accounting

information include different types information which can help to assess of performance.

1

INTRODUCTION

Management accounting is the process of preparing management reports and accounts

that provide authentic and relatable information on time (Saleem Salem Alzoubi, 2016). These

information presented in financial and statical way in front of managers which is helping to make

day to day and short term decisions. It is different from financial accounting because in

management accounting reports and accounts are presented in front of managers on weekly and

monthly basis while in financial accounting reports are presented to investors, creditors, clients

and managers to annually basis. To understand the concept of the report selected company TPG

Processing which is related to manufacturing sector. In the report consist of explanation of

management accounting and their role. Apart from report define elements of different types of

management accounting system and different methods of management accounting reporting.

Further, evaluation the benefits of system and integrated with organisational process.

MAIN BODY

P1 Management Accounting Explanation

As per the IMA (Institute of management accountants): The management accounting may

be defined as a kind of process which is related with the decision making, planning and

performance management system in the aspect of the financial reporting. The aim of doing so, is

to control the assist management in the formulation and implementation of the strategies.

(Cleary, 2015).

From the definition it has been understand that management accounting is continuous

process which can help to manage performance of company in effective manner.

As per the the Chartered Institute of Management Accountants (CIMA): The

management accounting can be defined as the process that involves measurement, accumulation,

preparation and communicating the information and data which is being used by the managers to

make suitable decisions (Suprianto and et.al, 2017).

As per the above definition it has been understand that in management accounting

information include different types information which can help to assess of performance.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Roles Functions of Management accounting

Planning – It is important function of management accounting which can help to provide

all required information and authentic data. For example – The management Accountant of TPG

has been planning about manufacturing which can help to manager regarding to short term

decision (Golyagina and Valuckas, 2016).

Control – In the management sense, it has been described as the process which is part of

management process. It is helping to managers to ensure about that resources to acquired and

used in effective manner as well as obtain goals of an organisation. For example – For

manufacturing process use by this function by TPG processing to control activities to manage

business in effective manner (Arnaboldi, Busco and Cuganesan, 2017) .

Cost accounting – The function of cost accounting to manage information of

management accounting regarding to cost of production by assessing the input costs of each step

of production. For example – TPG company can predict cost of different products which is

manufacturing in company (Florio and Leoni, 2017).

Decision Making – The main role and function of management accounting to provide all

necessary information to top management. It can help to take day to day and short term decision

in effective manner. For example – for investment purpose management of TPG analysis of all

financial information (Solovida and Latan, 2017).

Financial Management – The management accountant can arrange all data and

information which is related to financial condition. The management use financial information to

take decision without any difficulty. For example – The accountant of TPG prepare report in

statistical way and present in front of to management.

Auditing – Management accounting play role to analysis books of company and rectify in

appropriate manner. For example – On monthly basis TPG can appoint internal auditor to cross

verify their books (Bernon, Cullen and Gorst, 2016) .

Management Accounting System

Cost Accounting System – It is a accounting system that can that determine that a

company is doing and helps manager make decisions based on the costs of doing business. Cost

accounting system mainly used by manufactures to record production activities after applying

perceptual inventory system. The particular system coordinate with other department because

they are providing all appropriate information to evaluate cost. On the basis of these information

2

Planning – It is important function of management accounting which can help to provide

all required information and authentic data. For example – The management Accountant of TPG

has been planning about manufacturing which can help to manager regarding to short term

decision (Golyagina and Valuckas, 2016).

Control – In the management sense, it has been described as the process which is part of

management process. It is helping to managers to ensure about that resources to acquired and

used in effective manner as well as obtain goals of an organisation. For example – For

manufacturing process use by this function by TPG processing to control activities to manage

business in effective manner (Arnaboldi, Busco and Cuganesan, 2017) .

Cost accounting – The function of cost accounting to manage information of

management accounting regarding to cost of production by assessing the input costs of each step

of production. For example – TPG company can predict cost of different products which is

manufacturing in company (Florio and Leoni, 2017).

Decision Making – The main role and function of management accounting to provide all

necessary information to top management. It can help to take day to day and short term decision

in effective manner. For example – for investment purpose management of TPG analysis of all

financial information (Solovida and Latan, 2017).

Financial Management – The management accountant can arrange all data and

information which is related to financial condition. The management use financial information to

take decision without any difficulty. For example – The accountant of TPG prepare report in

statistical way and present in front of to management.

Auditing – Management accounting play role to analysis books of company and rectify in

appropriate manner. For example – On monthly basis TPG can appoint internal auditor to cross

verify their books (Bernon, Cullen and Gorst, 2016) .

Management Accounting System

Cost Accounting System – It is a accounting system that can that determine that a

company is doing and helps manager make decisions based on the costs of doing business. Cost

accounting system mainly used by manufactures to record production activities after applying

perceptual inventory system. The particular system coordinate with other department because

they are providing all appropriate information to evaluate cost. On the basis of these information

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

set cost of different products and maintain purchase system and storage system. Through the

system recognise management problems and try to sort out it. For example – TPG Processing

follow the system to know flexibility and simplicity in products as well as cooperation with

several departments to gather all appropriate information.

Inventory Management System – It is considering as type of management accounting

system to manage inventory at each level of manufacturing process. There are supervising of

management of stock and non capitalized asset of business. It is depending on the company that

which method apply by company to manage their inventories, thee methods are LIFO (Last in

first out) , FIFO (First in first out) and AVOC. The TPG processing has been applied FIFO

method to manufacture products in order to use in sufficient manner. There are focusing on every

aspects like production to retail, warehousing to shipping and movements of the stock. For

example TPG company apply first in first out inventory system in order to manage stocks in

storage. The requirement of this system treat inventory as money, aware for regular stock to

understand how much inventory utilise for production process.

Job Costing System – In this system tracking record of manufacturing process while

prepare report of job costing. With the help of this system monitor of each activity and included

direct material, direct labour and overhead. In TPG has been applied particular system to identify

problem regarding to manufacturing process. They can take all detailed information to manage

all thing and produce products to know management things. For example – Through this report

TPG can determine cost of different aspects (Agrawal, 2018) . The requirement of this system

that It is categorised into different cost like direct material, direct labour and overhead expenses.

There are fixed cost and variable cost are identified and use to calculate of cost.

Price Optimisation System – The system has been used to control price of different

products and develop a effective structure which can set prices of their products. With the help of

this system analysis of market trends and know perception of people regarding to their products.

The manufacturing company TPG has been produced different types of products ans there is

need to set prices of their products. So company set price structure and analysis demand of their

product after that decide price of various products. For example – TPG has been produce

different types of products and for this need to set price structure so this system has been applied.

3

system recognise management problems and try to sort out it. For example – TPG Processing

follow the system to know flexibility and simplicity in products as well as cooperation with

several departments to gather all appropriate information.

Inventory Management System – It is considering as type of management accounting

system to manage inventory at each level of manufacturing process. There are supervising of

management of stock and non capitalized asset of business. It is depending on the company that

which method apply by company to manage their inventories, thee methods are LIFO (Last in

first out) , FIFO (First in first out) and AVOC. The TPG processing has been applied FIFO

method to manufacture products in order to use in sufficient manner. There are focusing on every

aspects like production to retail, warehousing to shipping and movements of the stock. For

example TPG company apply first in first out inventory system in order to manage stocks in

storage. The requirement of this system treat inventory as money, aware for regular stock to

understand how much inventory utilise for production process.

Job Costing System – In this system tracking record of manufacturing process while

prepare report of job costing. With the help of this system monitor of each activity and included

direct material, direct labour and overhead. In TPG has been applied particular system to identify

problem regarding to manufacturing process. They can take all detailed information to manage

all thing and produce products to know management things. For example – Through this report

TPG can determine cost of different aspects (Agrawal, 2018) . The requirement of this system

that It is categorised into different cost like direct material, direct labour and overhead expenses.

There are fixed cost and variable cost are identified and use to calculate of cost.

Price Optimisation System – The system has been used to control price of different

products and develop a effective structure which can set prices of their products. With the help of

this system analysis of market trends and know perception of people regarding to their products.

The manufacturing company TPG has been produced different types of products ans there is

need to set prices of their products. So company set price structure and analysis demand of their

product after that decide price of various products. For example – TPG has been produce

different types of products and for this need to set price structure so this system has been applied.

3

P2 Types Of Reports

Budget Reports – Budget managerial accounting reports plays significant role to

measure performance of the company. It is prepare by every organisation such as small

business, department wise and large organization. It is prepared by TPG processing to

predict their future income and expenses and analysis business activities of each

departments. TPG can try to achieve their goals and objectives. It can help to manager to

guide regarding to prepare plans and manage incomes and expenses to achieve goals and

objectives.

Account Receivable Agin Report – It is a critical report which can use to manage cash

flow in order to extend credit of customers for their business. There are most of the report

keep separate column for invoice and its presented as 30 days, 60 days and 90 days. With

the help of particular report identify problems regarding to collection process. In the

context to TPG processing identify those people who can not pay on time so for collect

payment on time prepare effective strategy (Commerford and et.al, 2016).

Cost Material Accounting Report – With the help of particular report compute the cost

of articles which is manufacturing. There are including raw material, labour and

overhead. These amounts has been categorised in produced products to realise cost of

various items versus their selling prices. In order to TPG identify cost of their material

after that analyse of market trends to its products and services.

Performance Report – The particular report has been developed to get review regarding

to individual employee and organizational performance in reference to specific

accounting period. These types of report mainly develop by large organization because

there is need to know about their employees skills. To evaluate the performance of

employees applied various indicator in order to provide rewards to their employees.

Job costing Report - In this report present expenses for specific project which has been

finance by companies. With the help of this report predict about revenues then match

with actual revenues after then analysis to know differences. The job costing report can

help to recognise higher earning process and focus on additional efforts rather than

wasting time and money. The particular report used by TPG to know correct areas an

track to progress of report.

4

Budget Reports – Budget managerial accounting reports plays significant role to

measure performance of the company. It is prepare by every organisation such as small

business, department wise and large organization. It is prepared by TPG processing to

predict their future income and expenses and analysis business activities of each

departments. TPG can try to achieve their goals and objectives. It can help to manager to

guide regarding to prepare plans and manage incomes and expenses to achieve goals and

objectives.

Account Receivable Agin Report – It is a critical report which can use to manage cash

flow in order to extend credit of customers for their business. There are most of the report

keep separate column for invoice and its presented as 30 days, 60 days and 90 days. With

the help of particular report identify problems regarding to collection process. In the

context to TPG processing identify those people who can not pay on time so for collect

payment on time prepare effective strategy (Commerford and et.al, 2016).

Cost Material Accounting Report – With the help of particular report compute the cost

of articles which is manufacturing. There are including raw material, labour and

overhead. These amounts has been categorised in produced products to realise cost of

various items versus their selling prices. In order to TPG identify cost of their material

after that analyse of market trends to its products and services.

Performance Report – The particular report has been developed to get review regarding

to individual employee and organizational performance in reference to specific

accounting period. These types of report mainly develop by large organization because

there is need to know about their employees skills. To evaluate the performance of

employees applied various indicator in order to provide rewards to their employees.

Job costing Report - In this report present expenses for specific project which has been

finance by companies. With the help of this report predict about revenues then match

with actual revenues after then analysis to know differences. The job costing report can

help to recognise higher earning process and focus on additional efforts rather than

wasting time and money. The particular report used by TPG to know correct areas an

track to progress of report.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Project Report – In the report defined all appropriate information regarding to project

which can handle by company. In the report record all detailed information regarding to

project. It will help to understand requirement and according to that prepare strategies.

Competitors Analysis Report – In competitive market need to analysis their competitors

so there is need to prepare report regarding to their strategies. When company want to get

competitive advantage that time track all information to their rivals and record in report.

It can help to prepare strategy in effective manner (van Helden, 2016).

Inventory & manufacturing Management report – In the report mentioned

information regarding to direct material, direct labour and variable overhead. These are

used in manufacturing to product as well as provide information of inventories. The

report defined that in the stage of manufacturing process how much material has been

used for product. In TPG track all record and provide to management to evaluate actual

cost and budgeted cost.

D1 Critical evaluation of how management accounting is integrated within the organization

Management accounting important part of every organisation and it can adopted by TPG

to manage business operations in effective manner. Management accounting systems and reports

are play significant role in organisational process due to smoothly running business activities.

These are related to various departments and show business activities to manage all result to

control process system. These reports present all required information which is related to internal

system of TPG and system manage issues which is origin in business during to manufacturing

process (Yang and Liu, 2017) .

M1 Benefits of the system and their application

The management accounting system has been applied by different organization in

appropriate manner and it can provide befits to TPG processing these are -

Cost Accounting System – The particular system has been applied by TPG processing in

order to know effectiveness of processes then use for appropriate modification. In the company

of TPG use cost accounting system to set and deduct the prices. The system can help to gather all

required information of different system and set purchase system, order system.

Inventory Management System – Through the system track all records of invention at

the time of manufacturing process. The company TPG processing apply particular system

5

which can handle by company. In the report record all detailed information regarding to

project. It will help to understand requirement and according to that prepare strategies.

Competitors Analysis Report – In competitive market need to analysis their competitors

so there is need to prepare report regarding to their strategies. When company want to get

competitive advantage that time track all information to their rivals and record in report.

It can help to prepare strategy in effective manner (van Helden, 2016).

Inventory & manufacturing Management report – In the report mentioned

information regarding to direct material, direct labour and variable overhead. These are

used in manufacturing to product as well as provide information of inventories. The

report defined that in the stage of manufacturing process how much material has been

used for product. In TPG track all record and provide to management to evaluate actual

cost and budgeted cost.

D1 Critical evaluation of how management accounting is integrated within the organization

Management accounting important part of every organisation and it can adopted by TPG

to manage business operations in effective manner. Management accounting systems and reports

are play significant role in organisational process due to smoothly running business activities.

These are related to various departments and show business activities to manage all result to

control process system. These reports present all required information which is related to internal

system of TPG and system manage issues which is origin in business during to manufacturing

process (Yang and Liu, 2017) .

M1 Benefits of the system and their application

The management accounting system has been applied by different organization in

appropriate manner and it can provide befits to TPG processing these are -

Cost Accounting System – The particular system has been applied by TPG processing in

order to know effectiveness of processes then use for appropriate modification. In the company

of TPG use cost accounting system to set and deduct the prices. The system can help to gather all

required information of different system and set purchase system, order system.

Inventory Management System – Through the system track all records of invention at

the time of manufacturing process. The company TPG processing apply particular system

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

because in manufacturing process need to different types material at different stage. So for this

need to evaluate detailed information regarding to inventory.

Job Costing System – It is beneficial for company to predict cost of various types

products which is manufactured by company. TPG Processing has been adopted job costing

system to know about processing system and cost of assorted products. After then evaluate the

quality of products (Qian, Hörisch and Schaltegger, 2018) .

Price Optimisation System – The particular system can help to set price structure of their

products which is manufactured by company. TPG manufacturing several types products and

price of these products set on the basis of market analysis and help to generate much more profit.

CONCLUSION

Management accounting is important part of any organisation which can mange all

aspects in effective manner. Through management accounting prepare reports and books to

present financial information of company in front of top management and it can help to take

decision regarding to business. Management accounting consist of different types of system

which can maintain business activities and identify all appropriate information. The reports has

been provide all sufficient information then it will compare with actual information to know

actually differences.

PART B

INTRODUCTION

Management Accounting is the presentation of accounting information in order to

formulate the policies to followed by the management and assist its day to day activities. It will

provide help to management to conduct functions such as planning, organising, staffing,

directing and controlling (Dauth, Pronobis and Schmid, 2017). Through management accounting

analysis of internal business activities then presented information in front of top management

which can help in decision making process. To understand the concept of the report selected

company TPG Processing which is related to manufacturing sector. In the report consist of

different types of planning tools of budgetary control and its advantage and disadvantage. In

addition recognise financial problem through comparison with other company then sort out with

management accounting system and approach.

6

need to evaluate detailed information regarding to inventory.

Job Costing System – It is beneficial for company to predict cost of various types

products which is manufactured by company. TPG Processing has been adopted job costing

system to know about processing system and cost of assorted products. After then evaluate the

quality of products (Qian, Hörisch and Schaltegger, 2018) .

Price Optimisation System – The particular system can help to set price structure of their

products which is manufactured by company. TPG manufacturing several types products and

price of these products set on the basis of market analysis and help to generate much more profit.

CONCLUSION

Management accounting is important part of any organisation which can mange all

aspects in effective manner. Through management accounting prepare reports and books to

present financial information of company in front of top management and it can help to take

decision regarding to business. Management accounting consist of different types of system

which can maintain business activities and identify all appropriate information. The reports has

been provide all sufficient information then it will compare with actual information to know

actually differences.

PART B

INTRODUCTION

Management Accounting is the presentation of accounting information in order to

formulate the policies to followed by the management and assist its day to day activities. It will

provide help to management to conduct functions such as planning, organising, staffing,

directing and controlling (Dauth, Pronobis and Schmid, 2017). Through management accounting

analysis of internal business activities then presented information in front of top management

which can help in decision making process. To understand the concept of the report selected

company TPG Processing which is related to manufacturing sector. In the report consist of

different types of planning tools of budgetary control and its advantage and disadvantage. In

addition recognise financial problem through comparison with other company then sort out with

management accounting system and approach.

6

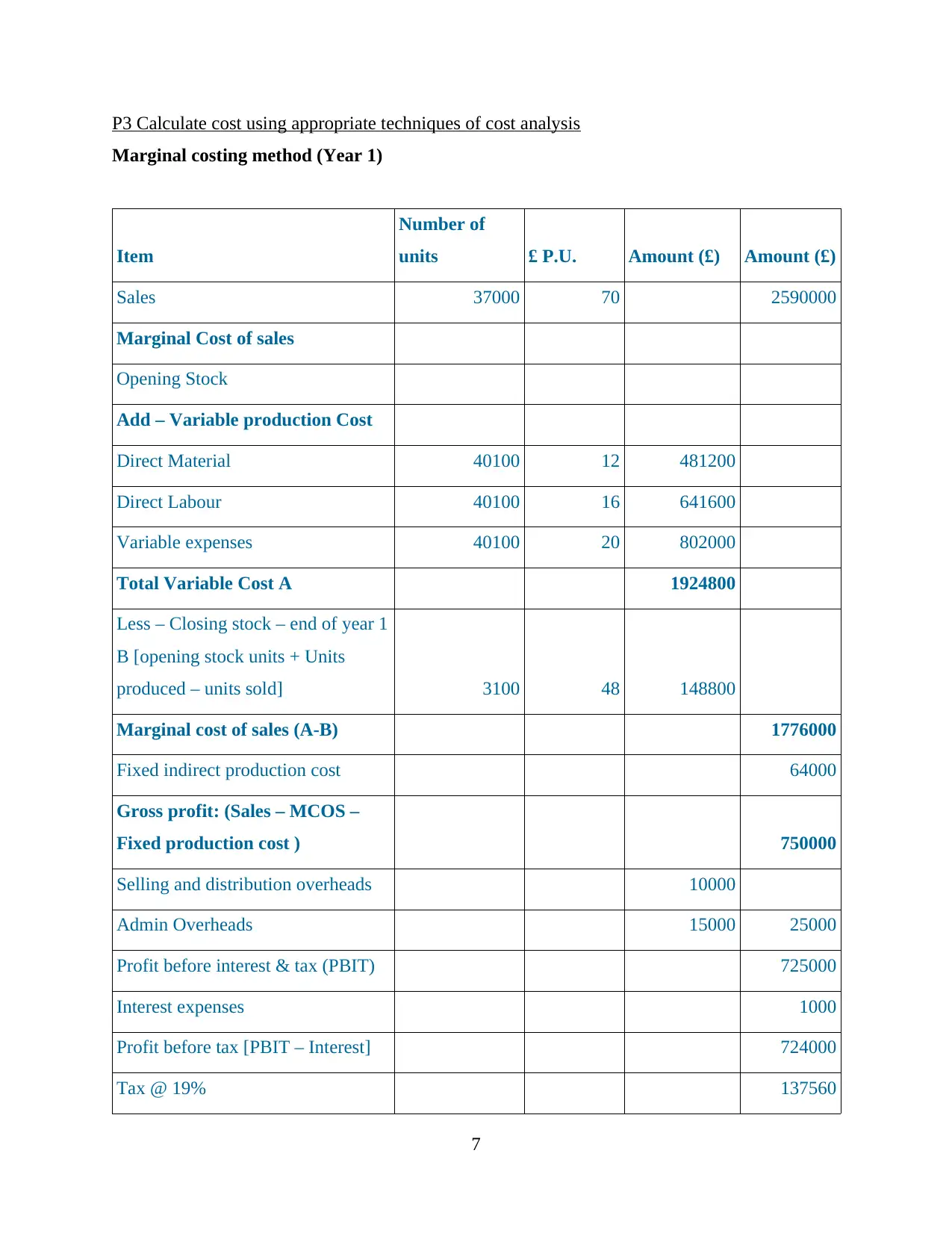

P3 Calculate cost using appropriate techniques of cost analysis

Marginal costing method (Year 1)

Item

Number of

units £ P.U. Amount (£) Amount (£)

Sales 37000 70 2590000

Marginal Cost of sales

Opening Stock

Add – Variable production Cost

Direct Material 40100 12 481200

Direct Labour 40100 16 641600

Variable expenses 40100 20 802000

Total Variable Cost A 1924800

Less – Closing stock – end of year 1

B [opening stock units + Units

produced – units sold] 3100 48 148800

Marginal cost of sales (A-B) 1776000

Fixed indirect production cost 64000

Gross profit: (Sales – MCOS –

Fixed production cost ) 750000

Selling and distribution overheads 10000

Admin Overheads 15000 25000

Profit before interest & tax (PBIT) 725000

Interest expenses 1000

Profit before tax [PBIT – Interest] 724000

Tax @ 19% 137560

7

Marginal costing method (Year 1)

Item

Number of

units £ P.U. Amount (£) Amount (£)

Sales 37000 70 2590000

Marginal Cost of sales

Opening Stock

Add – Variable production Cost

Direct Material 40100 12 481200

Direct Labour 40100 16 641600

Variable expenses 40100 20 802000

Total Variable Cost A 1924800

Less – Closing stock – end of year 1

B [opening stock units + Units

produced – units sold] 3100 48 148800

Marginal cost of sales (A-B) 1776000

Fixed indirect production cost 64000

Gross profit: (Sales – MCOS –

Fixed production cost ) 750000

Selling and distribution overheads 10000

Admin Overheads 15000 25000

Profit before interest & tax (PBIT) 725000

Interest expenses 1000

Profit before tax [PBIT – Interest] 724000

Tax @ 19% 137560

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Net profit: Profit before tax – tax 586440

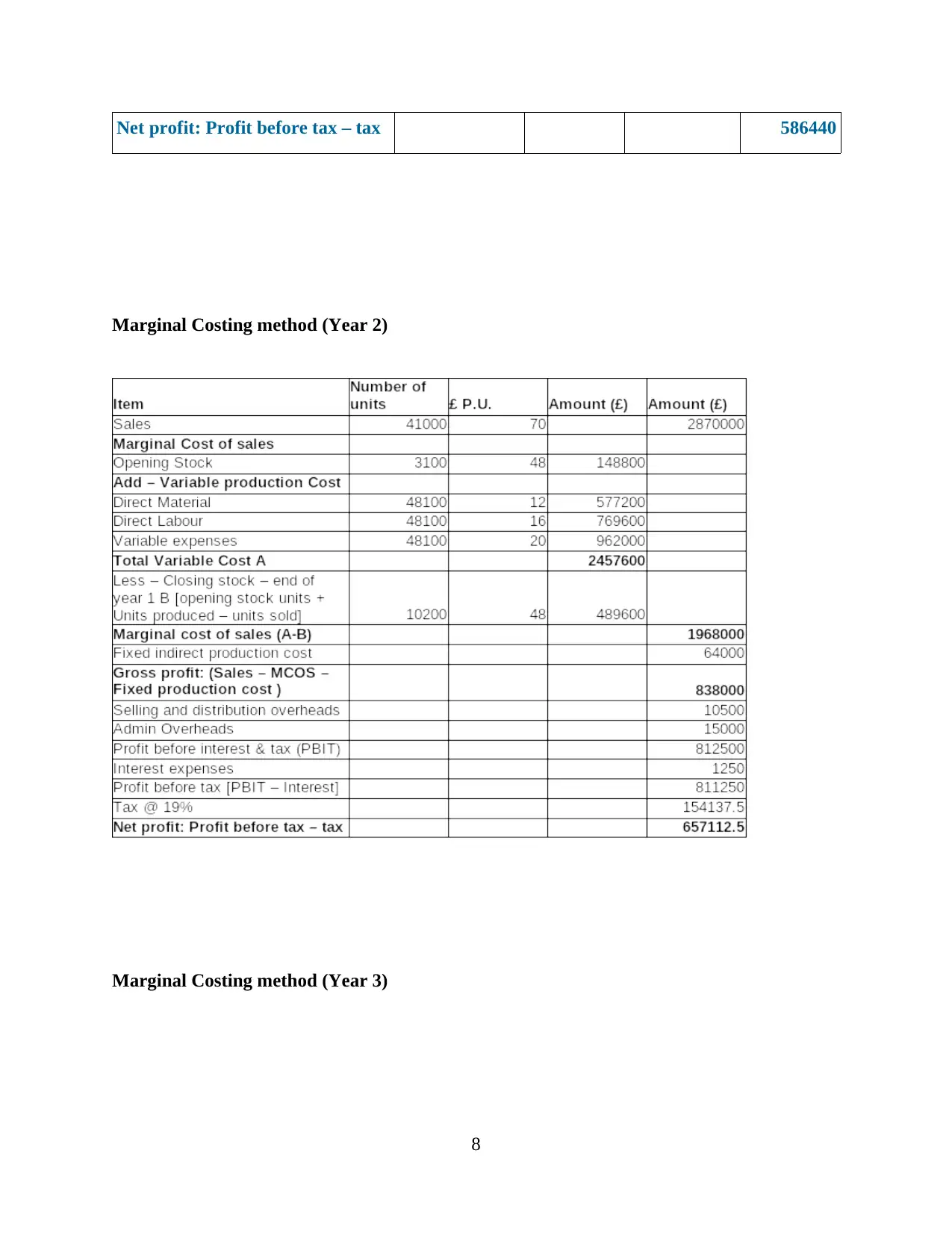

Marginal Costing method (Year 2)

Marginal Costing method (Year 3)

8

Marginal Costing method (Year 2)

Marginal Costing method (Year 3)

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

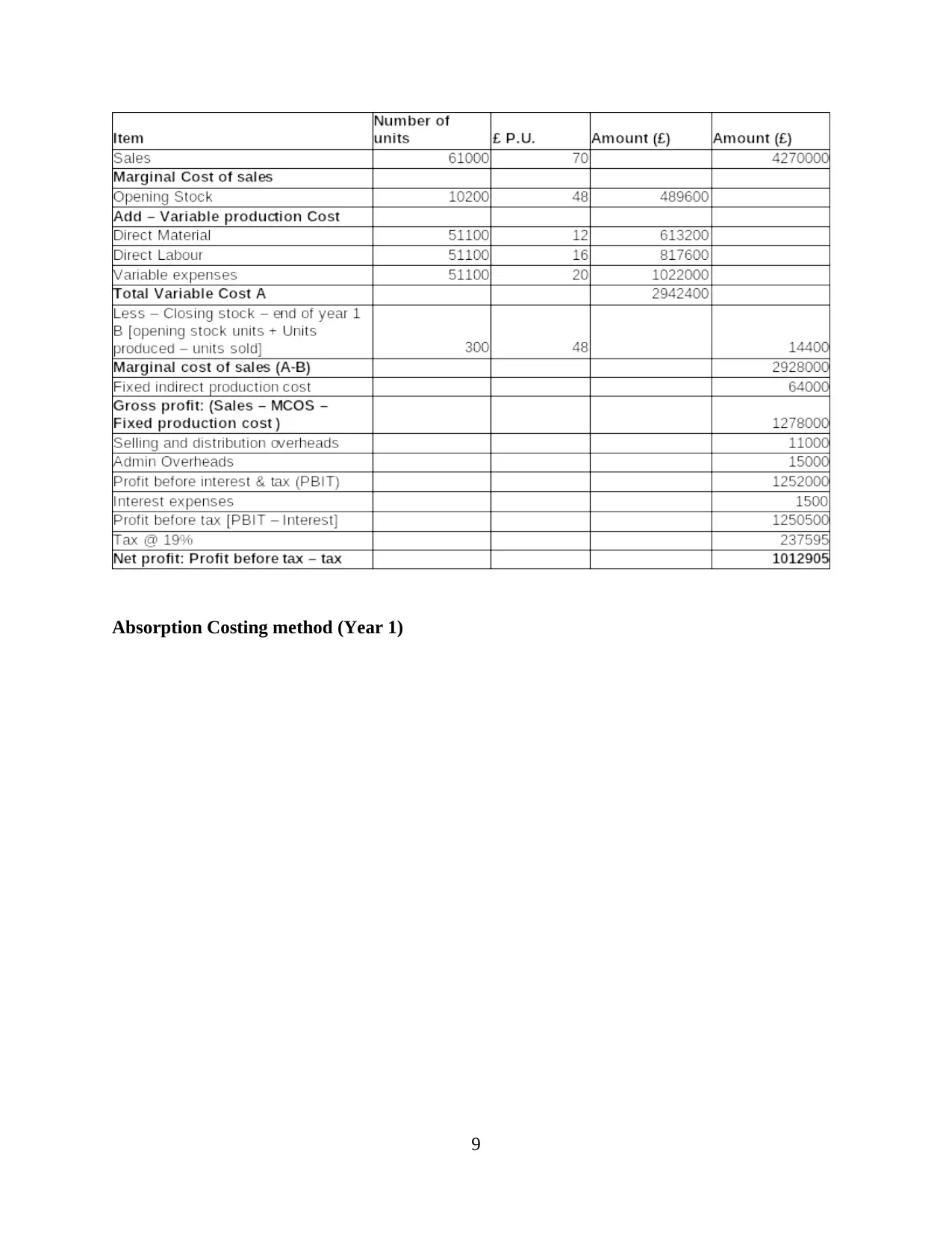

Absorption Costing method (Year 1)

9

9

Absorption Costing Method (Year 2)

Item

Number of

units £ P.U. Amount (£) Amount (£)

Sales 41000 70 2870000

Absorption Cost of sales

Opening Stock 3100 48 148800

Add – Absorption production

Cost

Direct Material 48100 12 577200

Direct Labour 48100 16 769600

Variable expenses 48100 20 962000

Fixed indirect production cost 64000

10

Item

Number of

units £ P.U. Amount (£) Amount (£)

Sales 41000 70 2870000

Absorption Cost of sales

Opening Stock 3100 48 148800

Add – Absorption production

Cost

Direct Material 48100 12 577200

Direct Labour 48100 16 769600

Variable expenses 48100 20 962000

Fixed indirect production cost 64000

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.