Management Accounting Report: Financial Analysis and Budgeting

VerifiedAdded on 2020/10/05

|12

|3587

|160

Report

AI Summary

This report provides a detailed analysis of management accounting principles and their application within Tech (UK) Limited. It differentiates between management and financial accounting, emphasizing the importance of management accounting information for decision-making, and explaining cost accounting and inventory management systems. The report then explores financial information preparation, including various managerial accounting reports such as budget reports and accounts receivable aging reports. It also covers the preparation of income statements using both absorption and marginal costing methods, comparing their profitability implications. Furthermore, the report delves into different kinds of budgets (operating, financial, cash, and fixed) and the budget preparation process, highlighting the significance of budgeting for planning and controlling financial resources. The report concludes by summarizing the use of management accounting systems in addressing financial problems. The content helps students understand core financial concepts.

MANAGEMENT ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Explain management accounting and the important requirements of management

accounting system?.................................................................................................................1

P2 Financial information preparation.....................................................................................2

TASK 2............................................................................................................................................3

P3 Prepare income statement..................................................................................................3

TASK 3............................................................................................................................................5

P4 (a) Different kinds of budget.............................................................................................5

P4 (b) Budget preparation process.........................................................................................6

P4 (c) Importance of budget for planning and controlling.....................................................7

TASK 4............................................................................................................................................7

P5 Use of management accounting system in responding financial problems......................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Explain management accounting and the important requirements of management

accounting system?.................................................................................................................1

P2 Financial information preparation.....................................................................................2

TASK 2............................................................................................................................................3

P3 Prepare income statement..................................................................................................3

TASK 3............................................................................................................................................5

P4 (a) Different kinds of budget.............................................................................................5

P4 (b) Budget preparation process.........................................................................................6

P4 (c) Importance of budget for planning and controlling.....................................................7

TASK 4............................................................................................................................................7

P5 Use of management accounting system in responding financial problems......................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION

Management accounting includes all the department of an organisation to manage their

income and expenses and to control the whole system to achieve the firm objectives. In this

project report we consider the Tech (UK) limited and working in this company as a trainee

management accountant (Christ and Burritt, 2017). This company is produce charger for mobile

phones and carry on gadgets and this company have retail outlet in UK. In this report we discuss

the system of management accounting, and the essential requirements of it. Also discuss the

different type of managerial accounting reports. In this report we explain the different the kinds

of budgets and their advantages and disadvantages and the main importance of budget as a tool .

In this report we also explain the balanced scored approach in reference the Tech (UK) limited.

TASK 1

P1 Explain management accounting and the important requirements of management accounting

system?

Difference between management accounting and financial accounting:

Their are some basis which is easily distinguish between both of them. These are: Aim: Financial accounting main aim is to provide the information which is related to

finance and it is given to the shareholders and investor of the firm. Where as management

accounting main aim is to take the business decision by management (Cooper, Ezzamel

and Qu, 2017). Regulatory requirements: in financial management it is compulsory to consider the

regulatory frameworks , and in management accounting there is not important or

compulsory for following a regulation framework. Governing principles : Financial accounting is prepared by Generally accepted

accounting principles. And in management accounting there is not to set any standardized

principles (Leotta, Rizza and Ruggeri, 2017).

Importance of management accounting information in decision making

Management accounting is the essential part of an organisation. Accounting refers to the

base information and provide most information to management to take the decision and to

forecast and to interpret this information . Decision making is very important in a management

accounting information . Management accounting has main part to provide the reliable

1

Management accounting includes all the department of an organisation to manage their

income and expenses and to control the whole system to achieve the firm objectives. In this

project report we consider the Tech (UK) limited and working in this company as a trainee

management accountant (Christ and Burritt, 2017). This company is produce charger for mobile

phones and carry on gadgets and this company have retail outlet in UK. In this report we discuss

the system of management accounting, and the essential requirements of it. Also discuss the

different type of managerial accounting reports. In this report we explain the different the kinds

of budgets and their advantages and disadvantages and the main importance of budget as a tool .

In this report we also explain the balanced scored approach in reference the Tech (UK) limited.

TASK 1

P1 Explain management accounting and the important requirements of management accounting

system?

Difference between management accounting and financial accounting:

Their are some basis which is easily distinguish between both of them. These are: Aim: Financial accounting main aim is to provide the information which is related to

finance and it is given to the shareholders and investor of the firm. Where as management

accounting main aim is to take the business decision by management (Cooper, Ezzamel

and Qu, 2017). Regulatory requirements: in financial management it is compulsory to consider the

regulatory frameworks , and in management accounting there is not important or

compulsory for following a regulation framework. Governing principles : Financial accounting is prepared by Generally accepted

accounting principles. And in management accounting there is not to set any standardized

principles (Leotta, Rizza and Ruggeri, 2017).

Importance of management accounting information in decision making

Management accounting is the essential part of an organisation. Accounting refers to the

base information and provide most information to management to take the decision and to

forecast and to interpret this information . Decision making is very important in a management

accounting information . Management accounting has main part to provide the reliable

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

information from that the managers take the right decision towards the business to growing fast.

It is important to understand the firm financial condition and used to take the right decision . Its

effect the long term decision for the firm betterment (Narasimhan, 2017). Their is a relationship

between the management accounting information and decision making and it is cover the all the

departments which is related to the accounting.

Explain cost accounting system

It is an estimation of cost of the firm for calculating their profitability and inventory

valuation. Cost accounting systems includes cash flows assumption, cost accumulation method ,

input measurement basis. This system is used to evaluate correct cost of products. And the firm

should know the which product is profitable and this will be used after calculating the accurate

cost of product (Shojaeezand, Mohammad-Khani and Azmi, 2018). Cost accounting system also

helps in to calculate the work in progress and finished goods inventory for the purpose of

financial statement preparation. Cost accounting system is divided into two main systems these

are, Job order costing and process costing . In job order costing in this calculates the

manufacturing cost which is separate from each job of the firm. And process costing is calculates

the manufacturing cost separate by each process of the firm.

Inventory management system

It is considered as essential tool that supports the organisation in making effective

management of inventories. By maintaining records managers can analysis inventories requires

to meet with the demand (Wachira, 2017). All transactions are related with purchase of raw

material, selling of final products and delivering of goods etc. If Tech (UK) limited manage its

inventory well then it would be beneficial for the organization in delivering products to the

consumers on time without any failure.

Job costing system:

Job costing can be defined as tool that is used by organizations in order to analysis

batches, jobs and unit produces in the firm. It takes into consideration to the variables that has

variation in costs at the time of production. Thus, company set prices on the bases of production

cost or over the produced goods (Wei and Xima, 2017).

P2 Financial information preparation

Managerial accounting reports

2

It is important to understand the firm financial condition and used to take the right decision . Its

effect the long term decision for the firm betterment (Narasimhan, 2017). Their is a relationship

between the management accounting information and decision making and it is cover the all the

departments which is related to the accounting.

Explain cost accounting system

It is an estimation of cost of the firm for calculating their profitability and inventory

valuation. Cost accounting systems includes cash flows assumption, cost accumulation method ,

input measurement basis. This system is used to evaluate correct cost of products. And the firm

should know the which product is profitable and this will be used after calculating the accurate

cost of product (Shojaeezand, Mohammad-Khani and Azmi, 2018). Cost accounting system also

helps in to calculate the work in progress and finished goods inventory for the purpose of

financial statement preparation. Cost accounting system is divided into two main systems these

are, Job order costing and process costing . In job order costing in this calculates the

manufacturing cost which is separate from each job of the firm. And process costing is calculates

the manufacturing cost separate by each process of the firm.

Inventory management system

It is considered as essential tool that supports the organisation in making effective

management of inventories. By maintaining records managers can analysis inventories requires

to meet with the demand (Wachira, 2017). All transactions are related with purchase of raw

material, selling of final products and delivering of goods etc. If Tech (UK) limited manage its

inventory well then it would be beneficial for the organization in delivering products to the

consumers on time without any failure.

Job costing system:

Job costing can be defined as tool that is used by organizations in order to analysis

batches, jobs and unit produces in the firm. It takes into consideration to the variables that has

variation in costs at the time of production. Thus, company set prices on the bases of production

cost or over the produced goods (Wei and Xima, 2017).

P2 Financial information preparation

Managerial accounting reports

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

There are various kinds of accounting reports that are essential to be prepared by the

organization. All these report help the company in identifying the profit and growth of business

unit (WHAT IS INVENTORY MANAGEMENT, 2015). This information assist in making sound

decision for the growth of the firm in the future.

Budge report

It is the type of report that supports business unit in understanding the cost of each

activities and determining the financial resources require for each task. By preparing this report

Tech (UK) limited take decision of budget and predetermine the cost for each activity in near

future.

Account receivable ageing report

It is another kind of report which is essential to be prepared by Tech (UK) limited. This

report helps organization in analysing situation of debtors such as suppliers, distributors etc. This

helps in ensuring the amount that are paid by debtors (What is management accounting, 2018).

By looking at the status of report manager can identify capabilities of debtors to make payment.

This assists in identifying the customers those are not paying payment on time and unused credit

memos by date range.

Importance of presenting information in accurate manner

It is very important for the organizations that to present their information in accurate

manner. By this way stakeholders, investors can understand the situation of company in effective

manner and can make sound decision. If Tech (UK) limited gets failed to present reports in

effective manner then investors and other stakeholders may get fail to make their decisions of

investment (Shojaeezand, Mohammad-Khani and Azmi, 2018).

TASK 2

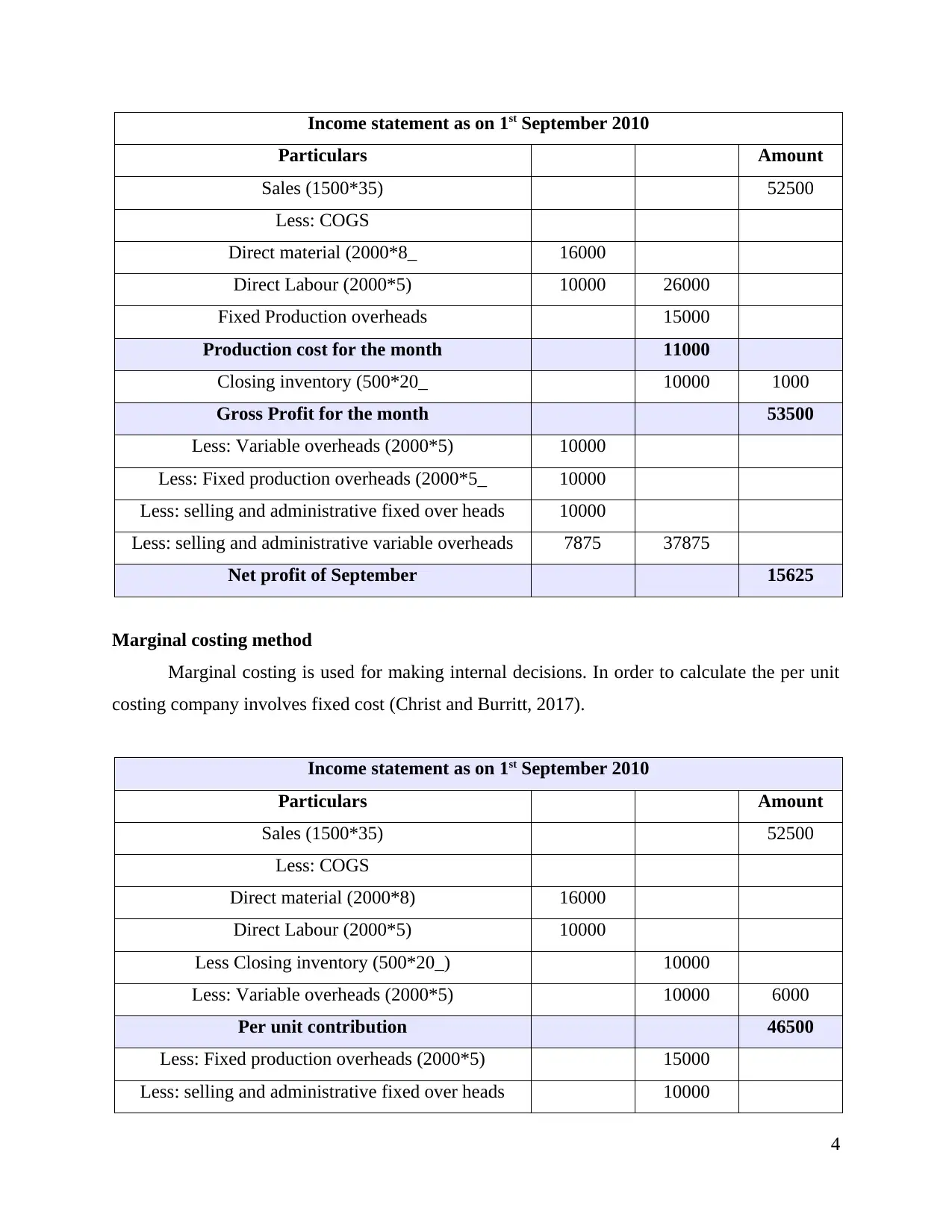

P3 Prepare income statement

There are two main methods of preparing income statement. These are absorption and

marginal costing methods. Both these tools are helpful in identifying the profit generated by the

firm at the end of financial year (Leotta, Rizza and Ruggeri, 2017). Income statement of Tech

(UK) limited for the month of September is as following

Absorption costing

It is the type of costing method which includes all type of costs such as fixed, variable in

order to calculate profit. By this way entity can calculate total cost of production.

3

organization. All these report help the company in identifying the profit and growth of business

unit (WHAT IS INVENTORY MANAGEMENT, 2015). This information assist in making sound

decision for the growth of the firm in the future.

Budge report

It is the type of report that supports business unit in understanding the cost of each

activities and determining the financial resources require for each task. By preparing this report

Tech (UK) limited take decision of budget and predetermine the cost for each activity in near

future.

Account receivable ageing report

It is another kind of report which is essential to be prepared by Tech (UK) limited. This

report helps organization in analysing situation of debtors such as suppliers, distributors etc. This

helps in ensuring the amount that are paid by debtors (What is management accounting, 2018).

By looking at the status of report manager can identify capabilities of debtors to make payment.

This assists in identifying the customers those are not paying payment on time and unused credit

memos by date range.

Importance of presenting information in accurate manner

It is very important for the organizations that to present their information in accurate

manner. By this way stakeholders, investors can understand the situation of company in effective

manner and can make sound decision. If Tech (UK) limited gets failed to present reports in

effective manner then investors and other stakeholders may get fail to make their decisions of

investment (Shojaeezand, Mohammad-Khani and Azmi, 2018).

TASK 2

P3 Prepare income statement

There are two main methods of preparing income statement. These are absorption and

marginal costing methods. Both these tools are helpful in identifying the profit generated by the

firm at the end of financial year (Leotta, Rizza and Ruggeri, 2017). Income statement of Tech

(UK) limited for the month of September is as following

Absorption costing

It is the type of costing method which includes all type of costs such as fixed, variable in

order to calculate profit. By this way entity can calculate total cost of production.

3

Income statement as on 1st September 2010

Particulars Amount

Sales (1500*35) 52500

Less: COGS

Direct material (2000*8_ 16000

Direct Labour (2000*5) 10000 26000

Fixed Production overheads 15000

Production cost for the month 11000

Closing inventory (500*20_ 10000 1000

Gross Profit for the month 53500

Less: Variable overheads (2000*5) 10000

Less: Fixed production overheads (2000*5_ 10000

Less: selling and administrative fixed over heads 10000

Less: selling and administrative variable overheads 7875 37875

Net profit of September 15625

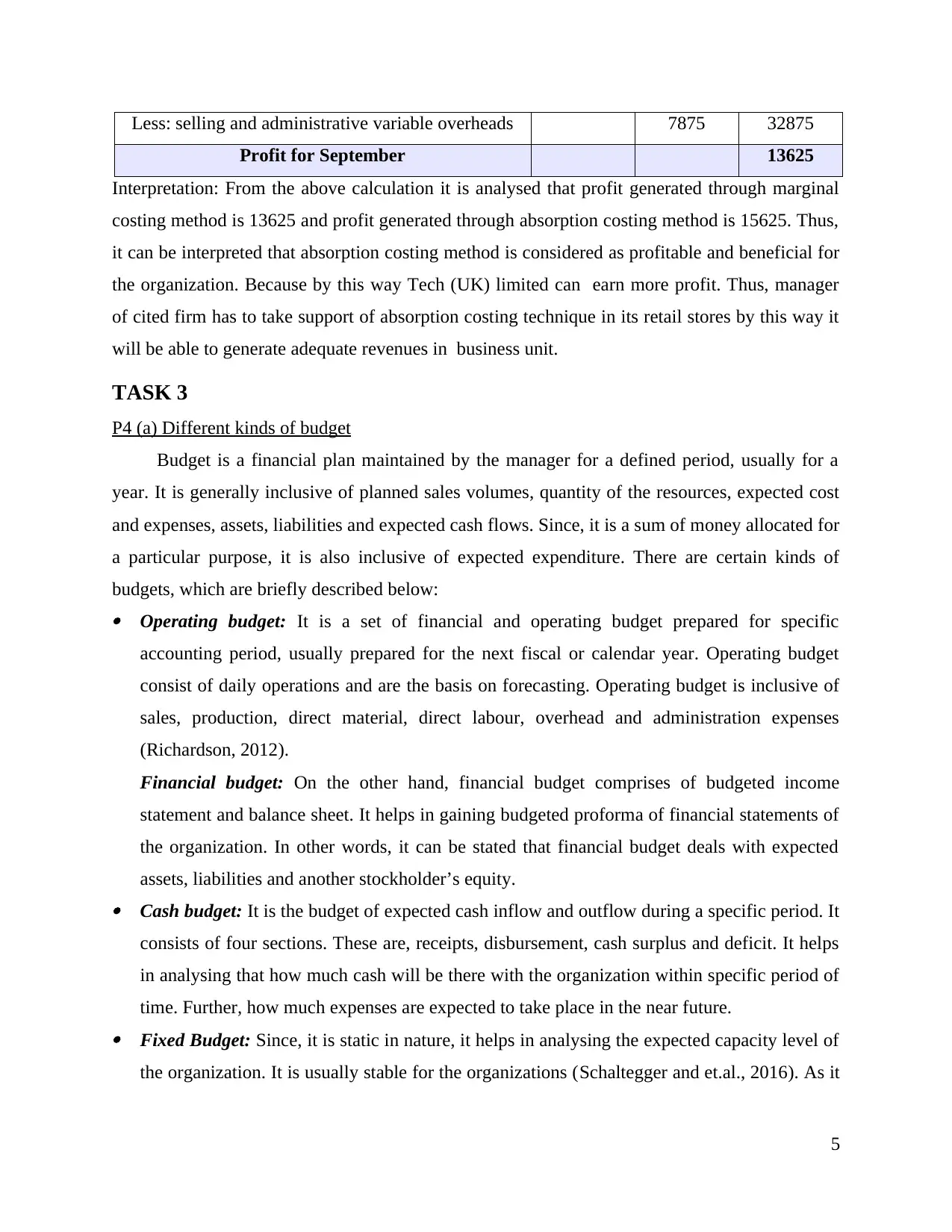

Marginal costing method

Marginal costing is used for making internal decisions. In order to calculate the per unit

costing company involves fixed cost (Christ and Burritt, 2017).

Income statement as on 1st September 2010

Particulars Amount

Sales (1500*35) 52500

Less: COGS

Direct material (2000*8) 16000

Direct Labour (2000*5) 10000

Less Closing inventory (500*20_) 10000

Less: Variable overheads (2000*5) 10000 6000

Per unit contribution 46500

Less: Fixed production overheads (2000*5) 15000

Less: selling and administrative fixed over heads 10000

4

Particulars Amount

Sales (1500*35) 52500

Less: COGS

Direct material (2000*8_ 16000

Direct Labour (2000*5) 10000 26000

Fixed Production overheads 15000

Production cost for the month 11000

Closing inventory (500*20_ 10000 1000

Gross Profit for the month 53500

Less: Variable overheads (2000*5) 10000

Less: Fixed production overheads (2000*5_ 10000

Less: selling and administrative fixed over heads 10000

Less: selling and administrative variable overheads 7875 37875

Net profit of September 15625

Marginal costing method

Marginal costing is used for making internal decisions. In order to calculate the per unit

costing company involves fixed cost (Christ and Burritt, 2017).

Income statement as on 1st September 2010

Particulars Amount

Sales (1500*35) 52500

Less: COGS

Direct material (2000*8) 16000

Direct Labour (2000*5) 10000

Less Closing inventory (500*20_) 10000

Less: Variable overheads (2000*5) 10000 6000

Per unit contribution 46500

Less: Fixed production overheads (2000*5) 15000

Less: selling and administrative fixed over heads 10000

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Less: selling and administrative variable overheads 7875 32875

Profit for September 13625

Interpretation: From the above calculation it is analysed that profit generated through marginal

costing method is 13625 and profit generated through absorption costing method is 15625. Thus,

it can be interpreted that absorption costing method is considered as profitable and beneficial for

the organization. Because by this way Tech (UK) limited can earn more profit. Thus, manager

of cited firm has to take support of absorption costing technique in its retail stores by this way it

will be able to generate adequate revenues in business unit.

TASK 3

P4 (a) Different kinds of budget

Budget is a financial plan maintained by the manager for a defined period, usually for a

year. It is generally inclusive of planned sales volumes, quantity of the resources, expected cost

and expenses, assets, liabilities and expected cash flows. Since, it is a sum of money allocated for

a particular purpose, it is also inclusive of expected expenditure. There are certain kinds of

budgets, which are briefly described below: Operating budget: It is a set of financial and operating budget prepared for specific

accounting period, usually prepared for the next fiscal or calendar year. Operating budget

consist of daily operations and are the basis on forecasting. Operating budget is inclusive of

sales, production, direct material, direct labour, overhead and administration expenses

(Richardson, 2012).

Financial budget: On the other hand, financial budget comprises of budgeted income

statement and balance sheet. It helps in gaining budgeted proforma of financial statements of

the organization. In other words, it can be stated that financial budget deals with expected

assets, liabilities and another stockholder’s equity. Cash budget: It is the budget of expected cash inflow and outflow during a specific period. It

consists of four sections. These are, receipts, disbursement, cash surplus and deficit. It helps

in analysing that how much cash will be there with the organization within specific period of

time. Further, how much expenses are expected to take place in the near future. Fixed Budget: Since, it is static in nature, it helps in analysing the expected capacity level of

the organization. It is usually stable for the organizations (Schaltegger and et.al., 2016). As it

5

Profit for September 13625

Interpretation: From the above calculation it is analysed that profit generated through marginal

costing method is 13625 and profit generated through absorption costing method is 15625. Thus,

it can be interpreted that absorption costing method is considered as profitable and beneficial for

the organization. Because by this way Tech (UK) limited can earn more profit. Thus, manager

of cited firm has to take support of absorption costing technique in its retail stores by this way it

will be able to generate adequate revenues in business unit.

TASK 3

P4 (a) Different kinds of budget

Budget is a financial plan maintained by the manager for a defined period, usually for a

year. It is generally inclusive of planned sales volumes, quantity of the resources, expected cost

and expenses, assets, liabilities and expected cash flows. Since, it is a sum of money allocated for

a particular purpose, it is also inclusive of expected expenditure. There are certain kinds of

budgets, which are briefly described below: Operating budget: It is a set of financial and operating budget prepared for specific

accounting period, usually prepared for the next fiscal or calendar year. Operating budget

consist of daily operations and are the basis on forecasting. Operating budget is inclusive of

sales, production, direct material, direct labour, overhead and administration expenses

(Richardson, 2012).

Financial budget: On the other hand, financial budget comprises of budgeted income

statement and balance sheet. It helps in gaining budgeted proforma of financial statements of

the organization. In other words, it can be stated that financial budget deals with expected

assets, liabilities and another stockholder’s equity. Cash budget: It is the budget of expected cash inflow and outflow during a specific period. It

consists of four sections. These are, receipts, disbursement, cash surplus and deficit. It helps

in analysing that how much cash will be there with the organization within specific period of

time. Further, how much expenses are expected to take place in the near future. Fixed Budget: Since, it is static in nature, it helps in analysing the expected capacity level of

the organization. It is usually stable for the organizations (Schaltegger and et.al., 2016). As it

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

is based on capacity level, it is determined by management of every department. For

instance, fixed budget of production department will be different from that of sales budget.

P4 (b) Budget preparation process

There are various steps that are involved in preparation of budget. These steps are

discussed below in detail: Obtaining estimates: It is important to obtain estimates of sales, production levels,

availability of resources and expected cost from each of the units, subunits, divisions and

departments in the organization. The departmental heads and managers are responsible for

estimating the future requirements in such a manner that it can help in fulfilling the

necessities of the organizations. Informal discussion can be made with managers and written

detailed reports can be initiated that can then be submitted to budget committee of the

organization for approval. Coordinating with the estimates: The committee then prepares the evaluation based upon the

submission being made by various departments or organizational units in order to assess that

whether it has enough potential to serve the requirements of the business or not. Further, its

potentiality to fulfil the objectives of the business are also assessed so as analyse that whether

in this manner, the resources can be appropriately allocated to the departments or not.

Communicating budget: After analysing the overall budget and making adequate changes in

it will help in assessing that it has been framed appropriately. The final budget will then be

communicated to the departmental managers. After approval of budget plans, adequate

resources allocated to them and their budget for fiscal year will then be assessed by the

managers and assess that whether there is any requirements of changes or not. Any changes

required will then be communicated back to the budget committee. It helps in ensuring that

adequate cooperation has been received by the committee with respect to departmental

managers. Implementing the budget plan: The final budget, after bringing all the changes, will then be

communicated to the concerned managers and they can then adopt the same in their

operational aspects. With the implementation, various resources are made available to the

managers, in the form of raw material, labour facilities and other available resources so as to

carry out the budget that has already been prepared.

6

instance, fixed budget of production department will be different from that of sales budget.

P4 (b) Budget preparation process

There are various steps that are involved in preparation of budget. These steps are

discussed below in detail: Obtaining estimates: It is important to obtain estimates of sales, production levels,

availability of resources and expected cost from each of the units, subunits, divisions and

departments in the organization. The departmental heads and managers are responsible for

estimating the future requirements in such a manner that it can help in fulfilling the

necessities of the organizations. Informal discussion can be made with managers and written

detailed reports can be initiated that can then be submitted to budget committee of the

organization for approval. Coordinating with the estimates: The committee then prepares the evaluation based upon the

submission being made by various departments or organizational units in order to assess that

whether it has enough potential to serve the requirements of the business or not. Further, its

potentiality to fulfil the objectives of the business are also assessed so as analyse that whether

in this manner, the resources can be appropriately allocated to the departments or not.

Communicating budget: After analysing the overall budget and making adequate changes in

it will help in assessing that it has been framed appropriately. The final budget will then be

communicated to the departmental managers. After approval of budget plans, adequate

resources allocated to them and their budget for fiscal year will then be assessed by the

managers and assess that whether there is any requirements of changes or not. Any changes

required will then be communicated back to the budget committee. It helps in ensuring that

adequate cooperation has been received by the committee with respect to departmental

managers. Implementing the budget plan: The final budget, after bringing all the changes, will then be

communicated to the concerned managers and they can then adopt the same in their

operational aspects. With the implementation, various resources are made available to the

managers, in the form of raw material, labour facilities and other available resources so as to

carry out the budget that has already been prepared.

6

Reporting interim progress towards budgeted objectives: It is the full and final stage of

budgeting process where the budget is brought into operations by the managers for the

upcoming budgeting period. Reports are then prepared based on the outputs and performance

of managers are investigated so as to ensure that budget cn then be revised as per the

available flaw in the system. Feedback from the managers are gathered regarding budget for

the previous year and then improvements are brought in the current year.

P4 (c) Importance of budget for planning and controlling

Budgeting plays a vital role in planning and controlling process. It helps in developing a

plan of action for the organization which act as a framework for the organization to assess future

estimates related to revenues and cost, anticipation of future events and decrease uncertainty of

the events. It helps in increasing the chances of achieving goals and objectives for the company

when departments tend to coordinate with the plans. It helps in anticipating the uncertain

revenues and expenditure of the organization as well and helps in fulfilling the overall objectives

of the organization (Dhaliwal, Salamon and Smith, 2012).

Control is another important process of using feedback on actual performances and results,

comparing the same with the actual results as well so that deviations can be measured and

corrective actions can be undertaken. It helps in analysing the impact of policies and procedures

on functioning of the business which can effectively help in achievements of overall goals and

objectives of the business. Hence, it can be stated that budget help in keeping forward all the

future activities that are aligned to sole addressing of the business (Fullerton, Kennedy and

Widener, 2013).

Planning helps in identifying and receiving the desired outputs for the company by

managing overall inputs. Management tend to use planning as a tool to achieve overall business

goals by altering current policies and regulations in the best possible manner.

TASK 4

P5 Use of management accounting system in responding financial problems

Case scenario presents that Tech ltd has incurred a loss of £1.5 millions in the concerned

financial year. By reviewing overall performance auditors have suggested balance scorecard

approach to the management team of business unit. Such strategic management tool measures g

performance of the company from several perspectives such as customers, financials, learning &

growth and internal process (Leotta, Rizza and Ruggeri, 2017). This metric helps management

7

budgeting process where the budget is brought into operations by the managers for the

upcoming budgeting period. Reports are then prepared based on the outputs and performance

of managers are investigated so as to ensure that budget cn then be revised as per the

available flaw in the system. Feedback from the managers are gathered regarding budget for

the previous year and then improvements are brought in the current year.

P4 (c) Importance of budget for planning and controlling

Budgeting plays a vital role in planning and controlling process. It helps in developing a

plan of action for the organization which act as a framework for the organization to assess future

estimates related to revenues and cost, anticipation of future events and decrease uncertainty of

the events. It helps in increasing the chances of achieving goals and objectives for the company

when departments tend to coordinate with the plans. It helps in anticipating the uncertain

revenues and expenditure of the organization as well and helps in fulfilling the overall objectives

of the organization (Dhaliwal, Salamon and Smith, 2012).

Control is another important process of using feedback on actual performances and results,

comparing the same with the actual results as well so that deviations can be measured and

corrective actions can be undertaken. It helps in analysing the impact of policies and procedures

on functioning of the business which can effectively help in achievements of overall goals and

objectives of the business. Hence, it can be stated that budget help in keeping forward all the

future activities that are aligned to sole addressing of the business (Fullerton, Kennedy and

Widener, 2013).

Planning helps in identifying and receiving the desired outputs for the company by

managing overall inputs. Management tend to use planning as a tool to achieve overall business

goals by altering current policies and regulations in the best possible manner.

TASK 4

P5 Use of management accounting system in responding financial problems

Case scenario presents that Tech ltd has incurred a loss of £1.5 millions in the concerned

financial year. By reviewing overall performance auditors have suggested balance scorecard

approach to the management team of business unit. Such strategic management tool measures g

performance of the company from several perspectives such as customers, financials, learning &

growth and internal process (Leotta, Rizza and Ruggeri, 2017). This metric helps management

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

team in identifying and improving various internal functions or aspects more effectually. Hence,

by using such tool management team of Tech ltd would become able to find out deficiencies

from both financial as well as non-financial perspective and take corrective measure for

improvement.

Key performance indicators: There are certain key performance indicators, based on which it

can be assessed that management accounting system that is being adopted by the organization it

contributing adequately in achieving business goals and objectives or not (Renz, 2016). In this

scenario, key performance indicators can be revenue, profitability, sales etc.

Benchmarking: Quality benchmarking is the other aspect that is related to appropriate

implementation of management information system in the organization. Further, comparing the

quality of developed product can also help in assessing that whether benchmark quality of the

products has been achieved or not. MIS helps in ensuring that products with appropriate quality

are produced which can help in achieving overall financial objectives of the organization

(Horngren, 2012).

Financial governance: Financial governance is the stringent set of rules and regulations which

helps the organization in guiding it to financial processes. MIS ensures that all the policies, rules

and regulations are appropriately being fulfilled in such a manner that maximum profitability out

of it can be achieved.

CONCLUSION

By summing up this report, it has been articulated that using management accounting

tools Tech Ltd can exert control on cost and thereby maximizes profit level. It can be seen in the

report that managerial accounting reports provide deeper insight about departmental performance

and thereby help in taking strategic action for improvement. It can be summarized from the

evaluation that budgeting tools and techniques aid in financial planning to a great extent. By

undertaking budgeting tools and techniques Tech Ltd can exert control on negative results within

the suitable time frame. Further, it has assessed from the evaluation that referring both fixed and

variable expenses business organization can assess suitable manufacturing cost. Besides this, it

can be stated that using balance scorecard tool Tech Ltd can develop suitable strategies as well as

policy framework and thereby attain success.

8

by using such tool management team of Tech ltd would become able to find out deficiencies

from both financial as well as non-financial perspective and take corrective measure for

improvement.

Key performance indicators: There are certain key performance indicators, based on which it

can be assessed that management accounting system that is being adopted by the organization it

contributing adequately in achieving business goals and objectives or not (Renz, 2016). In this

scenario, key performance indicators can be revenue, profitability, sales etc.

Benchmarking: Quality benchmarking is the other aspect that is related to appropriate

implementation of management information system in the organization. Further, comparing the

quality of developed product can also help in assessing that whether benchmark quality of the

products has been achieved or not. MIS helps in ensuring that products with appropriate quality

are produced which can help in achieving overall financial objectives of the organization

(Horngren, 2012).

Financial governance: Financial governance is the stringent set of rules and regulations which

helps the organization in guiding it to financial processes. MIS ensures that all the policies, rules

and regulations are appropriately being fulfilled in such a manner that maximum profitability out

of it can be achieved.

CONCLUSION

By summing up this report, it has been articulated that using management accounting

tools Tech Ltd can exert control on cost and thereby maximizes profit level. It can be seen in the

report that managerial accounting reports provide deeper insight about departmental performance

and thereby help in taking strategic action for improvement. It can be summarized from the

evaluation that budgeting tools and techniques aid in financial planning to a great extent. By

undertaking budgeting tools and techniques Tech Ltd can exert control on negative results within

the suitable time frame. Further, it has assessed from the evaluation that referring both fixed and

variable expenses business organization can assess suitable manufacturing cost. Besides this, it

can be stated that using balance scorecard tool Tech Ltd can develop suitable strategies as well as

policy framework and thereby attain success.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Christ, K. L. and Burritt, R. L., 2017. Water management accounting: A framework for

corporate practice. Journal of Cleaner Production. 152. pp.379-386.

Cooper, D. J., Ezzamel, M. and Qu, S. Q., 2017. Popularizing a management accounting idea:

The case of the balanced scorecard. Contemporary Accounting Research. 34(2). pp.991-

1025.

Leotta, A., Rizza, C. and Ruggeri, D., 2017. Management accounting and leadership

construction in family firms. Qualitative Research in Accounting & Management. 14(2).

pp.189-207.

Narasimhan, M.S., 2017. Variance Analysis: General Framework.

Shojaeezand, T., Mohammad-Khani, G. R. and Azmi, P., 2018. Variance Analysis of the New

Method of Applying Multiuser Detection in a GPS Receiver in High Dynamic

Conditions. Wireless Personal Communications. 98(2). pp.2107-2119.

Wachira, M., 2017. Determinants of corporate social disclosures in Kenya: A longitudinal study

of firms listed on the Nairobi securities exchange. European Scientific Journal,

ESJ. 13(11).

Wei, W. E. I. and Xima, Y. U. E., 2017. Research on Accunting Development Cost Per Graduate

Student in University. Canadian Social Science. 13(1). pp.11-15.

Dhaliwal, D.S., Salamon, G.L. and Smith, E.D., 2012. The effect of owner versus management

control on the choice of accounting methods. Journal of accounting and economics. 4(1).

pp.41-53.

Fullerton, R. R., Kennedy, F. A. and Widener, S. K., 2013. Management accounting and control

practices in a lean manufacturing environment. Accounting, Organizations and

Society. 38(1). pp.50-71.

Horngren, C.T., 2012. Cost accounting: A managerial emphasis, 13/e. Pearson Education India.

Renz, D. O., 2016. The Jossey-Bass handbook of nonprofit leadership and management. John

Wiley & Sons.

9

Books and Journals

Christ, K. L. and Burritt, R. L., 2017. Water management accounting: A framework for

corporate practice. Journal of Cleaner Production. 152. pp.379-386.

Cooper, D. J., Ezzamel, M. and Qu, S. Q., 2017. Popularizing a management accounting idea:

The case of the balanced scorecard. Contemporary Accounting Research. 34(2). pp.991-

1025.

Leotta, A., Rizza, C. and Ruggeri, D., 2017. Management accounting and leadership

construction in family firms. Qualitative Research in Accounting & Management. 14(2).

pp.189-207.

Narasimhan, M.S., 2017. Variance Analysis: General Framework.

Shojaeezand, T., Mohammad-Khani, G. R. and Azmi, P., 2018. Variance Analysis of the New

Method of Applying Multiuser Detection in a GPS Receiver in High Dynamic

Conditions. Wireless Personal Communications. 98(2). pp.2107-2119.

Wachira, M., 2017. Determinants of corporate social disclosures in Kenya: A longitudinal study

of firms listed on the Nairobi securities exchange. European Scientific Journal,

ESJ. 13(11).

Wei, W. E. I. and Xima, Y. U. E., 2017. Research on Accunting Development Cost Per Graduate

Student in University. Canadian Social Science. 13(1). pp.11-15.

Dhaliwal, D.S., Salamon, G.L. and Smith, E.D., 2012. The effect of owner versus management

control on the choice of accounting methods. Journal of accounting and economics. 4(1).

pp.41-53.

Fullerton, R. R., Kennedy, F. A. and Widener, S. K., 2013. Management accounting and control

practices in a lean manufacturing environment. Accounting, Organizations and

Society. 38(1). pp.50-71.

Horngren, C.T., 2012. Cost accounting: A managerial emphasis, 13/e. Pearson Education India.

Renz, D. O., 2016. The Jossey-Bass handbook of nonprofit leadership and management. John

Wiley & Sons.

9

Richardson, A. J., 2012. Paradigms, theory and management accounting practice: A comment on

Parker (forthcoming)“Qualitative management accounting research: Assessing deliverables

and relevance”. Critical Perspectives on Accounting. 23(1). pp.83-88.

Schaltegger and et.al., 2016. Sustainability accounting and reporting (Vol. 21). Springer Science

& Business Media.

Online

WHAT IS INVENTORY MANAGEMENT?. 2015. [Online]. Available through

:<https://www.fishbowlinventory.com/inventory-management/>.

What is management accounting?. 2018. [Online]. Available through

:<https://www.cimaglobal.com/Starting-CIMA/Why-CIMA/what-is-management-

accounting/>.

10

Parker (forthcoming)“Qualitative management accounting research: Assessing deliverables

and relevance”. Critical Perspectives on Accounting. 23(1). pp.83-88.

Schaltegger and et.al., 2016. Sustainability accounting and reporting (Vol. 21). Springer Science

& Business Media.

Online

WHAT IS INVENTORY MANAGEMENT?. 2015. [Online]. Available through

:<https://www.fishbowlinventory.com/inventory-management/>.

What is management accounting?. 2018. [Online]. Available through

:<https://www.cimaglobal.com/Starting-CIMA/Why-CIMA/what-is-management-

accounting/>.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.