Financial Analysis and Management Accounting for Flying Airlines

VerifiedAdded on 2020/06/04

|7

|1218

|45

Report

AI Summary

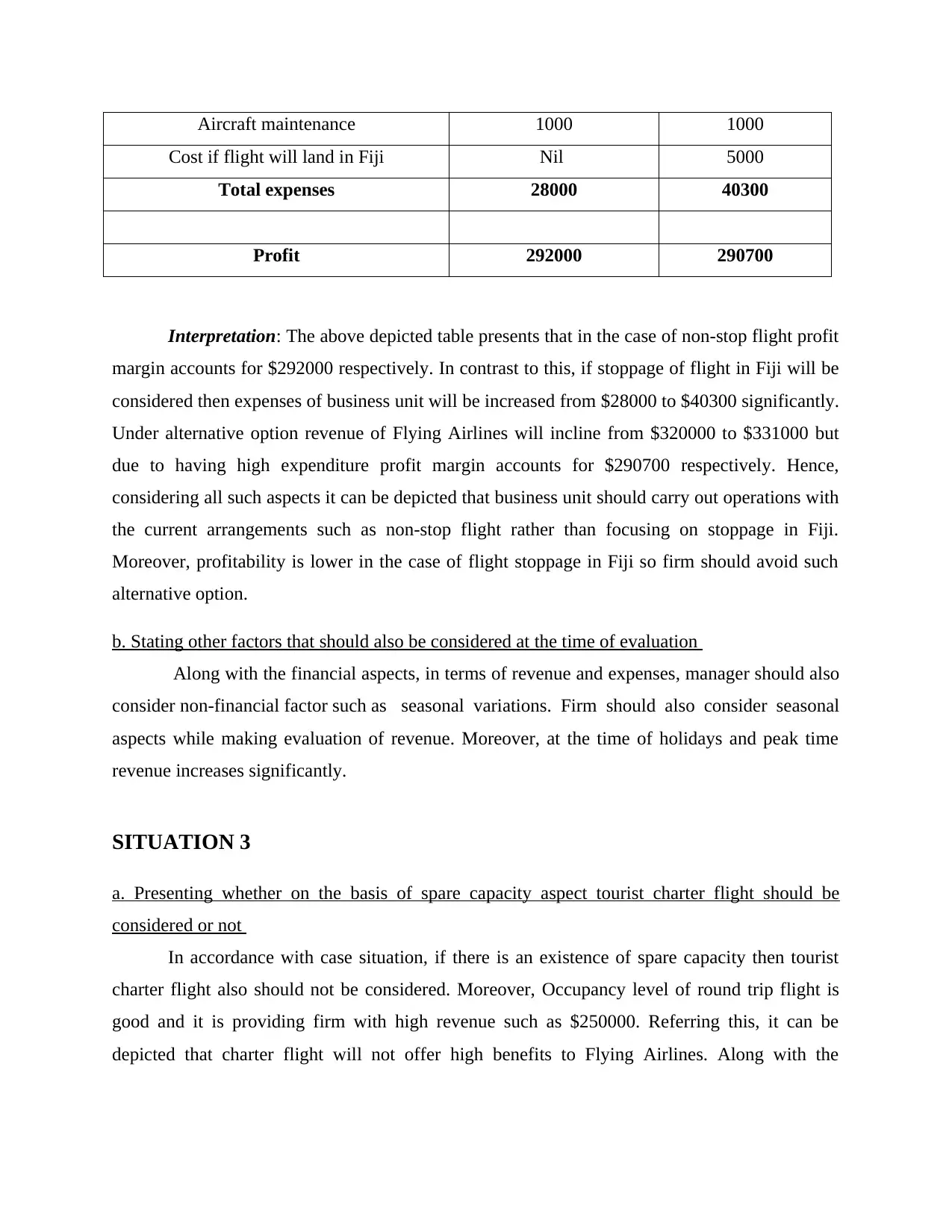

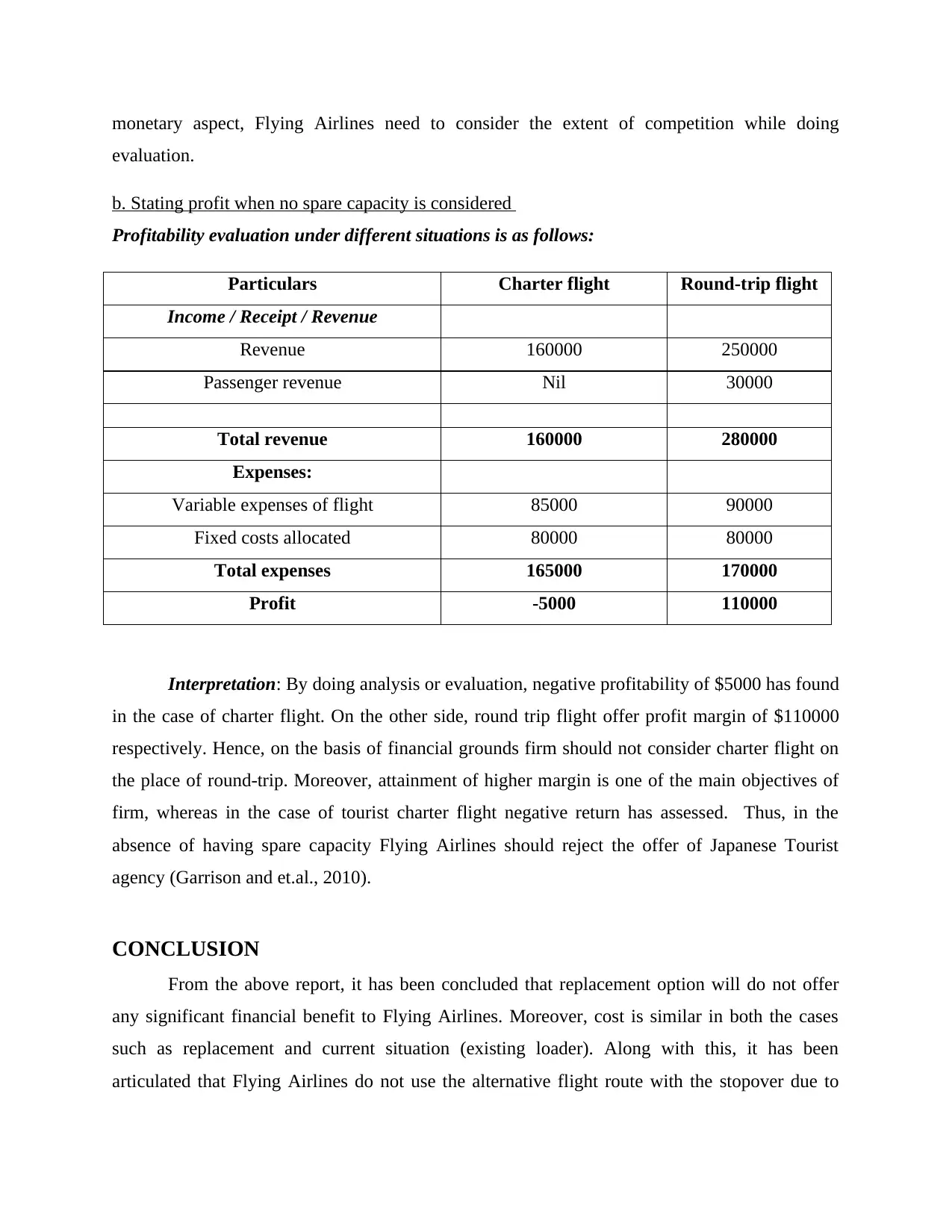

This report provides a comprehensive management accounting analysis of Flying Airlines, evaluating key financial decisions. The analysis covers three situations: the replacement of a loader truck, the evaluation of a flight route with a stopover in Fiji, and the consideration of a tourist charter flight. The report uses cost and profit analysis to determine the most financially sound decisions for the airline. The findings indicate that replacing the loader truck offers no significant financial benefit, the stopover flight route is less profitable than the non-stop route, and the charter flight should not be considered due to negative profitability. The report emphasizes the importance of considering both financial and non-financial factors in decision-making, such as seasonal variations and competition.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.