Report on Management Accounting Systems and Applications at KEF Ltd

VerifiedAdded on 2021/02/20

|16

|3587

|39

Report

AI Summary

This report provides a comprehensive analysis of management accounting systems and their applications within the context of KEF Ltd., a medium-sized manufacturing business. The report, prepared by a junior accountant, explores various management accounting (MA) techniques, including cost accounting, job costing, inventory control, and price optimization systems. It details the requirements and applications of each system, emphasizing their importance in financial management and decision-making. The report also covers MA reporting, including cost reports, inventory reports, performance reports, and budgetary reports, highlighting their benefits for KEF Ltd. Furthermore, the assignment includes practical applications of marginal and absorption costing techniques to calculate costs, prepare profitability statements, and analyze financial performance. The report concludes with a critical evaluation of the MA system and its reporting, emphasizing their role in improving financial management, internal controls, and overall business efficiency. The analysis covers key aspects of MA systems and their implementation within a manufacturing business, offering valuable insights into financial reporting and cost management.

Management

Accounting Systems and

its Applications

Accounting Systems and

its Applications

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

A system and a process for using professional skills, knowledge in order to managing all

the financial activities and development effective strategies and plans for improving overall

financial position of company is known as management accounting system (Boiral, O., 2016.).

KEF Ltd. is a medium sized manufacturing business unit. The study includes a report made by

junior accountant of the company which has a brief description of MA and its system including

MA reporting. It shows various MA techniques in context to preparing the profitability statement

of the company. In addition, it also shows description of a numerous planning tools to be used by

a company for preparing more beneficial plans for the company. At the end of assignment, the

report shows adoption of different MA systems by companies for facing problems relating to

financial activities.

TASK 1

Management accounting system, its requirements and different types of system of management

accounting (MA)

MA

"MA is that branch of accounting of a company which concerns with the preparation of

various statements with a view to provide various information regarding activities relating to

accounting and financial transactions made by company by using professional skills and

knowledge (Boučková, 2015). In addition, this system of accounting also includes development

of effective plans for the organisation so as to improve financial performance of business in the

competitive market."

Kinds of MA system

These are some types of MA system that can be adopted by managers of the company in

order to develop an effective management of financial performance of the company. Essential

MA systems are as under:

Cost accounting system: That system which is adopted by a financial manager and

management accountant in order to monitor overall cost incurred by a company and

developing effective strategies and plans in order to develop cost efficiency in business. It

is required to be adopted by the KEF Ltd. due to following reasons:

▪ This system is mostly required by a manufacturing concern as it helps for

determining cost involved in firm's each stage of production.

1

A system and a process for using professional skills, knowledge in order to managing all

the financial activities and development effective strategies and plans for improving overall

financial position of company is known as management accounting system (Boiral, O., 2016.).

KEF Ltd. is a medium sized manufacturing business unit. The study includes a report made by

junior accountant of the company which has a brief description of MA and its system including

MA reporting. It shows various MA techniques in context to preparing the profitability statement

of the company. In addition, it also shows description of a numerous planning tools to be used by

a company for preparing more beneficial plans for the company. At the end of assignment, the

report shows adoption of different MA systems by companies for facing problems relating to

financial activities.

TASK 1

Management accounting system, its requirements and different types of system of management

accounting (MA)

MA

"MA is that branch of accounting of a company which concerns with the preparation of

various statements with a view to provide various information regarding activities relating to

accounting and financial transactions made by company by using professional skills and

knowledge (Boučková, 2015). In addition, this system of accounting also includes development

of effective plans for the organisation so as to improve financial performance of business in the

competitive market."

Kinds of MA system

These are some types of MA system that can be adopted by managers of the company in

order to develop an effective management of financial performance of the company. Essential

MA systems are as under:

Cost accounting system: That system which is adopted by a financial manager and

management accountant in order to monitor overall cost incurred by a company and

developing effective strategies and plans in order to develop cost efficiency in business. It

is required to be adopted by the KEF Ltd. due to following reasons:

▪ This system is mostly required by a manufacturing concern as it helps for

determining cost involved in firm's each stage of production.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

▪ It is required to determine the appropriate price of a product.

▪ It is essential for spreading of total cost in several departments of the KEF Ltd.

Application: CA system is required to be used by all the companies as being cost

effective helps in business in improving its profitability and efficiency of working.

Job costing system: That system which is being adopted by those business units which

manufactures customised products and services for different customers (Chenhall and

Moers,2015). Essential requirement of job costing systems are as under:

▪ To identify total expenses of company for manufacturing its of product or

services.

▪ For setting the most appropriate price of all customised product by adding

sufficient amount of profit in it.

▪ To provide a detailed information about different costs incurred by the company

on different stages of the production.

Application: Job costing system is generally adopted by only those concerns that

manufactures customised product or services.

Inventory control system: Inventory management is a type of MA system that enables

managers in monitoring movement of each stock within and outside of the business

organisation. It is required by those companies that keeps inventory within the firm for

either further processing or for selling purpose. It essential requirements are:

▪ To monitor movement of inventory of a business.

▪ To control wastage of inventories.

▪ To check the maximum amount of stock needed by a business unit during a

specific time period.

Application: Inventory control system is adopted adopted by the manaufacturing units as

they need to maintain a range of inventory with them (Dekker, , 2016). In addition they also

require to maintain record of movement of stock held by them.

Price optimisation system: This system concerns with setting up the most appropriate

price of the goods and service provided by a company to its customers. This system helps

the management accountant in evaluating the maximum price which the customer will

pay for the product easily and the minimum price that needs to be set by the firm in order

2

▪ It is essential for spreading of total cost in several departments of the KEF Ltd.

Application: CA system is required to be used by all the companies as being cost

effective helps in business in improving its profitability and efficiency of working.

Job costing system: That system which is being adopted by those business units which

manufactures customised products and services for different customers (Chenhall and

Moers,2015). Essential requirement of job costing systems are as under:

▪ To identify total expenses of company for manufacturing its of product or

services.

▪ For setting the most appropriate price of all customised product by adding

sufficient amount of profit in it.

▪ To provide a detailed information about different costs incurred by the company

on different stages of the production.

Application: Job costing system is generally adopted by only those concerns that

manufactures customised product or services.

Inventory control system: Inventory management is a type of MA system that enables

managers in monitoring movement of each stock within and outside of the business

organisation. It is required by those companies that keeps inventory within the firm for

either further processing or for selling purpose. It essential requirements are:

▪ To monitor movement of inventory of a business.

▪ To control wastage of inventories.

▪ To check the maximum amount of stock needed by a business unit during a

specific time period.

Application: Inventory control system is adopted adopted by the manaufacturing units as

they need to maintain a range of inventory with them (Dekker, , 2016). In addition they also

require to maintain record of movement of stock held by them.

Price optimisation system: This system concerns with setting up the most appropriate

price of the goods and service provided by a company to its customers. This system helps

the management accountant in evaluating the maximum price which the customer will

pay for the product easily and the minimum price that needs to be set by the firm in order

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

to generate profits. In this order, the managers become able to set the most appropriate

price of the product or service. Its requirements for KEF Ltd. are as under:

▪ To generate the appropriate profits from the sale of product or services.

▪ For deciding the most economical price of product.

▪ To attract maximum customers towards the product or services by setting best

price.

Application: Price optimisation system is needed to be used by those business

organisations that are engaged in either production of any product or services or distribution of

various products manufactured by other companies.

Therefore, it is analysed that these several MA system are essentially required by

numerous business concerns (Hopper and Bui, 2016.).

Management accounting reporting:

It is that process of preparing several reports containing summary of all the financial

transactions firm so as to maintain record of each activities and helping the managers for their

performance of managerial functions in more effective way.

Following methods are being used for developing MA reporting:

Cost report:

Cost reports includes each information regarding cost incurred by the business

organisation. These report provides detailed information regarding various costs incurred at

different stages of business such as material, labour, commission, etc.

Benefits: Benefits of preparation of cost reports are as under:

It would help in determining cost of each department of the KEF Ltd.

It will help the managers in identifying areas in of wastage.

It enables managers in determining total cost of production of a single unit by KEF Ltd.

Inventory reports:

Those reports that includes in depth information regarding movement of stock in the

company. Being a manufacturing concern, the KEF Ltd. needs to analyse use of inventory in

various stages of manufacture.

Benefits: benefits of preparation of inventory reports to KEF Ltd, are as under:

3

price of the product or service. Its requirements for KEF Ltd. are as under:

▪ To generate the appropriate profits from the sale of product or services.

▪ For deciding the most economical price of product.

▪ To attract maximum customers towards the product or services by setting best

price.

Application: Price optimisation system is needed to be used by those business

organisations that are engaged in either production of any product or services or distribution of

various products manufactured by other companies.

Therefore, it is analysed that these several MA system are essentially required by

numerous business concerns (Hopper and Bui, 2016.).

Management accounting reporting:

It is that process of preparing several reports containing summary of all the financial

transactions firm so as to maintain record of each activities and helping the managers for their

performance of managerial functions in more effective way.

Following methods are being used for developing MA reporting:

Cost report:

Cost reports includes each information regarding cost incurred by the business

organisation. These report provides detailed information regarding various costs incurred at

different stages of business such as material, labour, commission, etc.

Benefits: Benefits of preparation of cost reports are as under:

It would help in determining cost of each department of the KEF Ltd.

It will help the managers in identifying areas in of wastage.

It enables managers in determining total cost of production of a single unit by KEF Ltd.

Inventory reports:

Those reports that includes in depth information regarding movement of stock in the

company. Being a manufacturing concern, the KEF Ltd. needs to analyse use of inventory in

various stages of manufacture.

Benefits: benefits of preparation of inventory reports to KEF Ltd, are as under:

3

It helps in determining minimum amount of stock needed by company within a specific

period.

These reports are required fir maintaining record of each movement of stock within the

business.

Through this report, managers can become able to detect wastage of inventory at various

stages of production (Kaplan and Atkinson, 2015).

Through inventory reports, the managers of KEF Ltd. will be able to develop effective

plan for elimination of wastage.

Performance reports:

The performance reports made by a business units contains information regarding overall

performance of the organisation. Preparation of this report can help the managers of KEF Ltd. in

analysis of performance of various departments of the company including their own

performance. In this order, these reports are needed to be used by the business so as to determine

the efficiency of the company.

Benefits: Essential benefits of performance report to KEF Ltd. are as under:

Through this report a KEF Ltd. can easily determine the improvement or decline in the

efficiency of overall company's performance (ACCOUNTING REPORTS. 2018.).

These reports can enable the managers in detecting inefficiencies in various departments

of the business of KEF Ltd.

It improves ability of the managers in determination of performance of the business at a

certain level of production.

Budgetary reports:

These reports are the most importance element of the MA reporting system. These are

formulated by the managers for the purpose of setting short term goals through which company

could become able to achieve its actual goals and improve its efficiency and profitability as well.

(Maas, Schaltegger and Crutzen, 2016). In this order, these reports helps the managers in

ensuring effective achievement of goals and objectives of company.

Benefits: Benefits of budgetary reports are as under:

It helps in setting short term goals for the business.

By the use of budgetary reports managers become capable to identify the need of various

resources in company in near future.

4

period.

These reports are required fir maintaining record of each movement of stock within the

business.

Through this report, managers can become able to detect wastage of inventory at various

stages of production (Kaplan and Atkinson, 2015).

Through inventory reports, the managers of KEF Ltd. will be able to develop effective

plan for elimination of wastage.

Performance reports:

The performance reports made by a business units contains information regarding overall

performance of the organisation. Preparation of this report can help the managers of KEF Ltd. in

analysis of performance of various departments of the company including their own

performance. In this order, these reports are needed to be used by the business so as to determine

the efficiency of the company.

Benefits: Essential benefits of performance report to KEF Ltd. are as under:

Through this report a KEF Ltd. can easily determine the improvement or decline in the

efficiency of overall company's performance (ACCOUNTING REPORTS. 2018.).

These reports can enable the managers in detecting inefficiencies in various departments

of the business of KEF Ltd.

It improves ability of the managers in determination of performance of the business at a

certain level of production.

Budgetary reports:

These reports are the most importance element of the MA reporting system. These are

formulated by the managers for the purpose of setting short term goals through which company

could become able to achieve its actual goals and improve its efficiency and profitability as well.

(Maas, Schaltegger and Crutzen, 2016). In this order, these reports helps the managers in

ensuring effective achievement of goals and objectives of company.

Benefits: Benefits of budgetary reports are as under:

It helps in setting short term goals for the business.

By the use of budgetary reports managers become capable to identify the need of various

resources in company in near future.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It can help the managers of the KEF Ltd. in maintaining sufficient amount of funds and

other resources when they are needed by the company.

It improves the strength of business in responding various uncertainty that may arise in

near future.

In this regard, it can be seen that the MA reporting is an essential part of the MA. It

enables managers in completing their managerial functions in more effective way. In addition, It

also helps them in ensuring development of effective plans for the company's financial growth.

Critical evaluation of MA system and its reporting:

Adoption of an effective MA system within the business organisation can help KEF Ltd.

in improving the overall financial management in firm. It helps in improving the management

their monitoring and controlling over various departments and activities of the company. In

addition, by adopting appropriate management accounting reporting and preparing all the

required management accounting reports, the managers become able to analyse the overall

financial activities in an effective way (Otley, 2016). further, it also helps them in maintaining

proper record of all the financial records of KEF Ltd. Whereas, if the KEF Ltd. adopts MA

systems and management accounting reporting, it will increase their workings. In addition, it will

also require a huge time and cost of the company. Although, these costs can be recovered by the

KEF Ltd. if it adopts all the systems and reports in an effective way.

Therefore, it can be analysed both MA system and its reporting is essentially needed by

the KEF Ltd. It will improve the internal controlling system of business and improving the

efficiency of the business as well. Further, as the cost and time incurred by the business would be

effectively recovered by the company, it should adopt them within its business.

TASK 2

Calculating cost and preparing profitability statements through marginal and absorption cost

techniques.

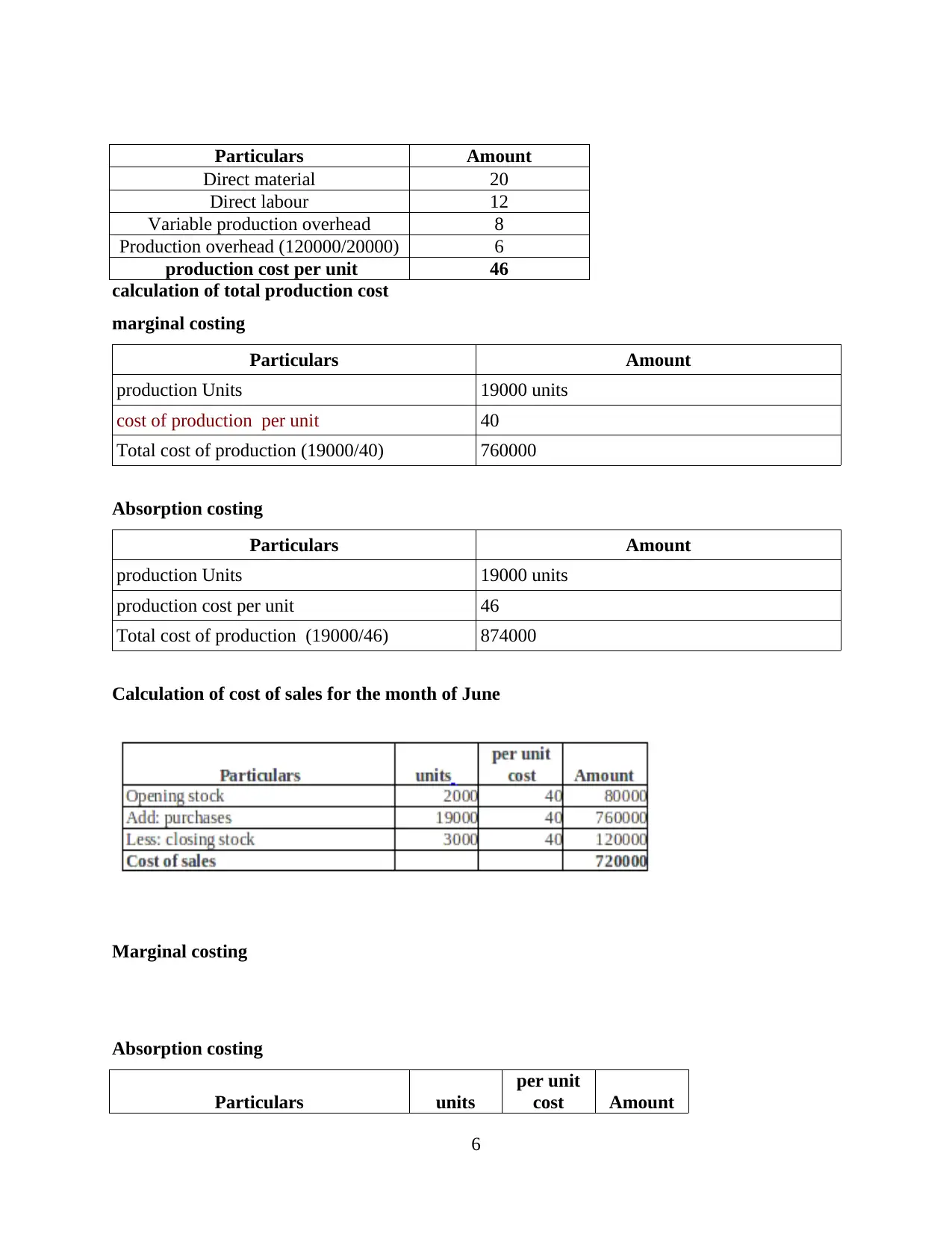

Calculation of cost of production per unit

Marginal costing

Direct material 20

Direct labour 12

Variable production overhead 8

Per unit production cost 40

Absorption costing

5

other resources when they are needed by the company.

It improves the strength of business in responding various uncertainty that may arise in

near future.

In this regard, it can be seen that the MA reporting is an essential part of the MA. It

enables managers in completing their managerial functions in more effective way. In addition, It

also helps them in ensuring development of effective plans for the company's financial growth.

Critical evaluation of MA system and its reporting:

Adoption of an effective MA system within the business organisation can help KEF Ltd.

in improving the overall financial management in firm. It helps in improving the management

their monitoring and controlling over various departments and activities of the company. In

addition, by adopting appropriate management accounting reporting and preparing all the

required management accounting reports, the managers become able to analyse the overall

financial activities in an effective way (Otley, 2016). further, it also helps them in maintaining

proper record of all the financial records of KEF Ltd. Whereas, if the KEF Ltd. adopts MA

systems and management accounting reporting, it will increase their workings. In addition, it will

also require a huge time and cost of the company. Although, these costs can be recovered by the

KEF Ltd. if it adopts all the systems and reports in an effective way.

Therefore, it can be analysed both MA system and its reporting is essentially needed by

the KEF Ltd. It will improve the internal controlling system of business and improving the

efficiency of the business as well. Further, as the cost and time incurred by the business would be

effectively recovered by the company, it should adopt them within its business.

TASK 2

Calculating cost and preparing profitability statements through marginal and absorption cost

techniques.

Calculation of cost of production per unit

Marginal costing

Direct material 20

Direct labour 12

Variable production overhead 8

Per unit production cost 40

Absorption costing

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Particulars Amount

Direct material 20

Direct labour 12

Variable production overhead 8

Production overhead (120000/20000) 6

production cost per unit 46

calculation of total production cost

marginal costing

Particulars Amount

production Units 19000 units

cost of production per unit 40

Total cost of production (19000/40) 760000

Absorption costing

Particulars Amount

production Units 19000 units

production cost per unit 46

Total cost of production (19000/46) 874000

Calculation of cost of sales for the month of June

Marginal costing

Absorption costing

Particulars units

per unit

cost Amount

6

Direct material 20

Direct labour 12

Variable production overhead 8

Production overhead (120000/20000) 6

production cost per unit 46

calculation of total production cost

marginal costing

Particulars Amount

production Units 19000 units

cost of production per unit 40

Total cost of production (19000/40) 760000

Absorption costing

Particulars Amount

production Units 19000 units

production cost per unit 46

Total cost of production (19000/46) 874000

Calculation of cost of sales for the month of June

Marginal costing

Absorption costing

Particulars units

per unit

cost Amount

6

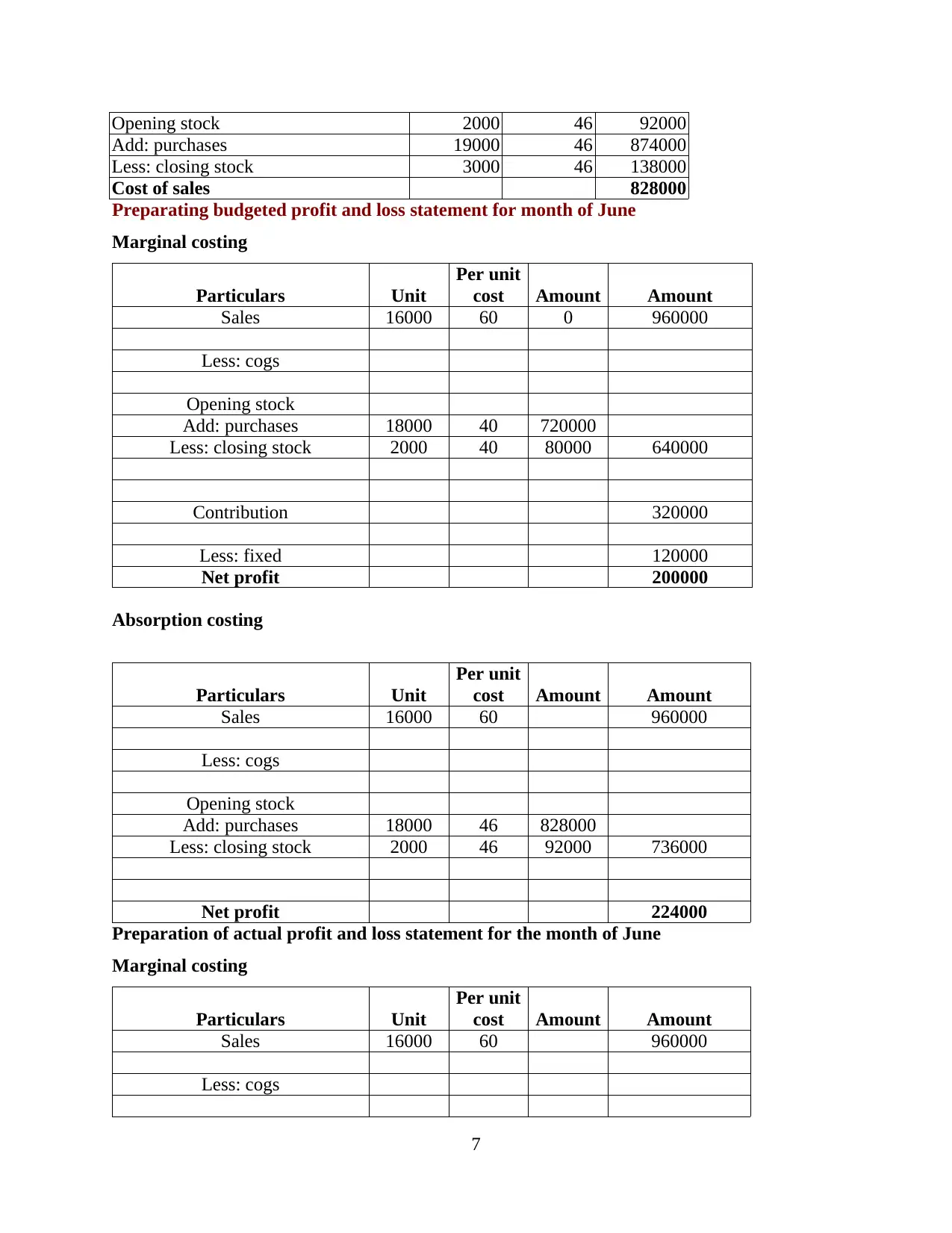

Opening stock 2000 46 92000

Add: purchases 19000 46 874000

Less: closing stock 3000 46 138000

Cost of sales 828000

Preparating budgeted profit and loss statement for month of June

Marginal costing

Particulars Unit

Per unit

cost Amount Amount

Sales 16000 60 0 960000

Less: cogs

Opening stock

Add: purchases 18000 40 720000

Less: closing stock 2000 40 80000 640000

Contribution 320000

Less: fixed 120000

Net profit 200000

Absorption costing

Particulars Unit

Per unit

cost Amount Amount

Sales 16000 60 960000

Less: cogs

Opening stock

Add: purchases 18000 46 828000

Less: closing stock 2000 46 92000 736000

Net profit 224000

Preparation of actual profit and loss statement for the month of June

Marginal costing

Particulars Unit

Per unit

cost Amount Amount

Sales 16000 60 960000

Less: cogs

7

Add: purchases 19000 46 874000

Less: closing stock 3000 46 138000

Cost of sales 828000

Preparating budgeted profit and loss statement for month of June

Marginal costing

Particulars Unit

Per unit

cost Amount Amount

Sales 16000 60 0 960000

Less: cogs

Opening stock

Add: purchases 18000 40 720000

Less: closing stock 2000 40 80000 640000

Contribution 320000

Less: fixed 120000

Net profit 200000

Absorption costing

Particulars Unit

Per unit

cost Amount Amount

Sales 16000 60 960000

Less: cogs

Opening stock

Add: purchases 18000 46 828000

Less: closing stock 2000 46 92000 736000

Net profit 224000

Preparation of actual profit and loss statement for the month of June

Marginal costing

Particulars Unit

Per unit

cost Amount Amount

Sales 16000 60 960000

Less: cogs

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

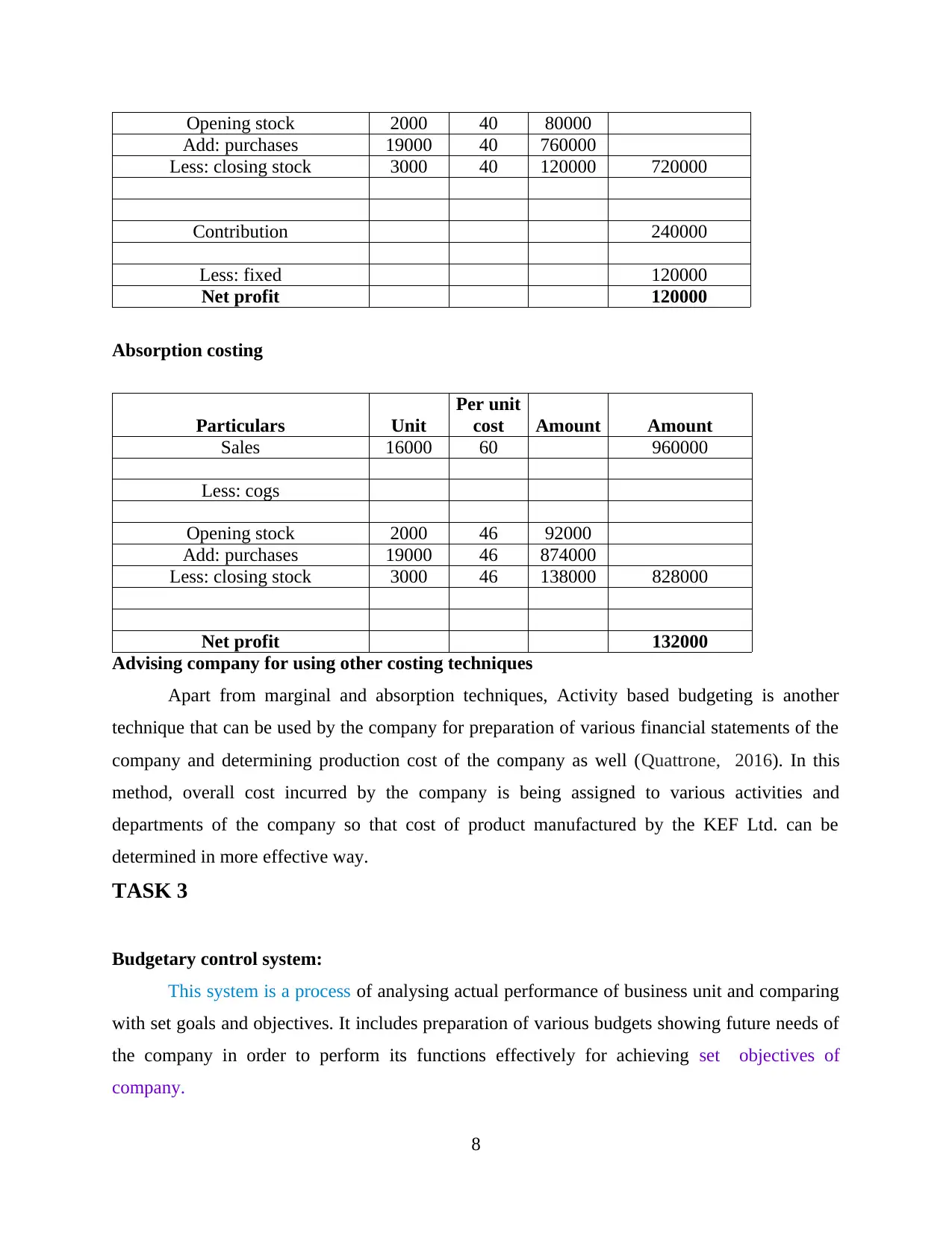

Opening stock 2000 40 80000

Add: purchases 19000 40 760000

Less: closing stock 3000 40 120000 720000

Contribution 240000

Less: fixed 120000

Net profit 120000

Absorption costing

Particulars Unit

Per unit

cost Amount Amount

Sales 16000 60 960000

Less: cogs

Opening stock 2000 46 92000

Add: purchases 19000 46 874000

Less: closing stock 3000 46 138000 828000

Net profit 132000

Advising company for using other costing techniques

Apart from marginal and absorption techniques, Activity based budgeting is another

technique that can be used by the company for preparation of various financial statements of the

company and determining production cost of the company as well (Quattrone, 2016). In this

method, overall cost incurred by the company is being assigned to various activities and

departments of the company so that cost of product manufactured by the KEF Ltd. can be

determined in more effective way.

TASK 3

Budgetary control system:

This system is a process of analysing actual performance of business unit and comparing

with set goals and objectives. It includes preparation of various budgets showing future needs of

the company in order to perform its functions effectively for achieving set objectives of

company.

8

Add: purchases 19000 40 760000

Less: closing stock 3000 40 120000 720000

Contribution 240000

Less: fixed 120000

Net profit 120000

Absorption costing

Particulars Unit

Per unit

cost Amount Amount

Sales 16000 60 960000

Less: cogs

Opening stock 2000 46 92000

Add: purchases 19000 46 874000

Less: closing stock 3000 46 138000 828000

Net profit 132000

Advising company for using other costing techniques

Apart from marginal and absorption techniques, Activity based budgeting is another

technique that can be used by the company for preparation of various financial statements of the

company and determining production cost of the company as well (Quattrone, 2016). In this

method, overall cost incurred by the company is being assigned to various activities and

departments of the company so that cost of product manufactured by the KEF Ltd. can be

determined in more effective way.

TASK 3

Budgetary control system:

This system is a process of analysing actual performance of business unit and comparing

with set goals and objectives. It includes preparation of various budgets showing future needs of

the company in order to perform its functions effectively for achieving set objectives of

company.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Planning tools of budgetary control

Numerous planning tools are being used by managers for formulation of budgets for the

company in an effective way. All planning tools used by the managers for performing their

budgetary control systems are as under:

Cash budgets: Cash budgets refers to those budgets that includes details about various

areas that would result in movement of cash within the business organisation due to

performance of various business operations. cash budget of KEF Ltd. can help its

managers in determining need of cash and cash equivalents by the company in the near

future. Along with it, it also enables then in identifying all sources from which they can

generate funds for meeting requirement of cash and cash equivalents.

Benefits:

▪ It helps in predetermination of need of cash..

▪ It improves ability of KEF Ltd. in repayment of debts

Limitations

▪ It limits the power of company in spending its cash.

▪ Estimation of cash is the most typical task and contains huge uncertainties as well.

Zero based budgets: Those budgets that are being formulated by managers by avoiding

the actual performance of the company (Schaltegger, Burritt and Petersen, 2017). While

preparing these budgets, managers starts with the zero. They evaluates the goals and

objectives of the company and prepared budgets for achieving them effectively.

Benefits:

▪ It results in achievement of goals and objectives more efficiently.

▪ It contains a huge accuracy in the budgeted incomes and expenses.

Limitations:

It enhances workings of the managers of KEF Ltd.

It may attract manipulation of various activities by the managers.

Operating budgets: Those budgets that are being prepared for estimation of overall

operations of the company are known as operational budgets. These budgets provide

information regarding several areas where the KEF Ltd. would require to expend its

resources and need of various financial resources by the business in its near future in

order to meet its debts (Renz, 2016).

9

Numerous planning tools are being used by managers for formulation of budgets for the

company in an effective way. All planning tools used by the managers for performing their

budgetary control systems are as under:

Cash budgets: Cash budgets refers to those budgets that includes details about various

areas that would result in movement of cash within the business organisation due to

performance of various business operations. cash budget of KEF Ltd. can help its

managers in determining need of cash and cash equivalents by the company in the near

future. Along with it, it also enables then in identifying all sources from which they can

generate funds for meeting requirement of cash and cash equivalents.

Benefits:

▪ It helps in predetermination of need of cash..

▪ It improves ability of KEF Ltd. in repayment of debts

Limitations

▪ It limits the power of company in spending its cash.

▪ Estimation of cash is the most typical task and contains huge uncertainties as well.

Zero based budgets: Those budgets that are being formulated by managers by avoiding

the actual performance of the company (Schaltegger, Burritt and Petersen, 2017). While

preparing these budgets, managers starts with the zero. They evaluates the goals and

objectives of the company and prepared budgets for achieving them effectively.

Benefits:

▪ It results in achievement of goals and objectives more efficiently.

▪ It contains a huge accuracy in the budgeted incomes and expenses.

Limitations:

It enhances workings of the managers of KEF Ltd.

It may attract manipulation of various activities by the managers.

Operating budgets: Those budgets that are being prepared for estimation of overall

operations of the company are known as operational budgets. These budgets provide

information regarding several areas where the KEF Ltd. would require to expend its

resources and need of various financial resources by the business in its near future in

order to meet its debts (Renz, 2016).

9

Benefits

▪ It improves debt meeting ability of the business.

▪ It helps managers in long term planning for the company

Limitations

▪ It results in development of rigidity in all the operating activities of the company.

▪ It fails to provide accurate results if the company performs any operation beyond

its budgeted activities.

In this order, it can be analysed that different planning tools available in the MA system

that helps the managers in improving their planning procedures and formulate more effective

plans and strategies for the business in such a way so that the overall financial position of the

company could be improved (Spraakman and et.al., 2015).

TASK 4

10

▪ It improves debt meeting ability of the business.

▪ It helps managers in long term planning for the company

Limitations

▪ It results in development of rigidity in all the operating activities of the company.

▪ It fails to provide accurate results if the company performs any operation beyond

its budgeted activities.

In this order, it can be analysed that different planning tools available in the MA system

that helps the managers in improving their planning procedures and formulate more effective

plans and strategies for the business in such a way so that the overall financial position of the

company could be improved (Spraakman and et.al., 2015).

TASK 4

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.