Comprehensive Analysis: Management Accounting Report for Zylla Company

VerifiedAdded on 2020/06/04

|16

|5019

|385

Report

AI Summary

This report, prepared for Zylla Company, delves into the core principles of management accounting, emphasizing its critical role in organizational decision-making. It begins by defining management accounting and its essential requirements, exploring various accounting systems like cost accounting, inventory management, and price optimization. The report then examines different management accounting reporting techniques, highlighting their importance for internal stakeholders and external financial reporting. It further analyzes the merits of using management accounting, including its impact on profitability and resource optimization. The report covers different costing methods and their application, along with an analysis of income statements. Furthermore, it explores planning techniques, their benefits and limitations, and the critical evaluation of financial issues, offering recommendations for resolving financial problems. The report concludes with a comprehensive overview of financial analysis and decision-making processes, providing valuable insights for the company's sustainable growth and financial stability. The report references various academic sources to support the analysis and recommendations.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

FROM: MANAGEMENT ACCOUNTING OFFICER..................................................................1

TO,...................................................................................................................................................1

GENERAL MANAGER..................................................................................................................1

ZYLLA COMPANY.......................................................................................................................1

SUB: MANAGEMENT ACCOUNTING SYSTEM .....................................................................1

INTRODUCTION...........................................................................................................................1

TASK1.............................................................................................................................................1

P1. Management accounting and essential requirements of its different accounting system 1

P2: Various techniques for management accounting reporting..............................................3

M1: Merits of using management accounting........................................................................5

D1: Critical evaluation of reporting system ..........................................................................5

TASK 2............................................................................................................................................6

P3: Different costing methods................................................................................................6

M2: Use of management accounting techniques....................................................................7

D2: Critical analysis of income statements............................................................................8

TASK 3............................................................................................................................................8

P4: Benefits and limitation of using planning techniques......................................................8

M3: Analysis of planning techniques...................................................................................10

D3: Critical evaluation of financial issues............................................................................10

TASK 4..........................................................................................................................................10

P5: Different measures to resolve financial issues...............................................................10

M4: Analysis of financial problem.......................................................................................11

CONCLUSION .............................................................................................................................12

REFERENCES..............................................................................................................................13

FROM: MANAGEMENT ACCOUNTING OFFICER..................................................................1

TO,...................................................................................................................................................1

GENERAL MANAGER..................................................................................................................1

ZYLLA COMPANY.......................................................................................................................1

SUB: MANAGEMENT ACCOUNTING SYSTEM .....................................................................1

INTRODUCTION...........................................................................................................................1

TASK1.............................................................................................................................................1

P1. Management accounting and essential requirements of its different accounting system 1

P2: Various techniques for management accounting reporting..............................................3

M1: Merits of using management accounting........................................................................5

D1: Critical evaluation of reporting system ..........................................................................5

TASK 2............................................................................................................................................6

P3: Different costing methods................................................................................................6

M2: Use of management accounting techniques....................................................................7

D2: Critical analysis of income statements............................................................................8

TASK 3............................................................................................................................................8

P4: Benefits and limitation of using planning techniques......................................................8

M3: Analysis of planning techniques...................................................................................10

D3: Critical evaluation of financial issues............................................................................10

TASK 4..........................................................................................................................................10

P5: Different measures to resolve financial issues...............................................................10

M4: Analysis of financial problem.......................................................................................11

CONCLUSION .............................................................................................................................12

REFERENCES..............................................................................................................................13

FROM: MANAGEMENT ACCOUNTING OFFICER

TO,

GENERAL MANAGER

ZYLLA COMPANY

SUB: MANAGEMENT ACCOUNTING SYSTEM

INTRODUCTION

Management accounting plays a crucial and vital role in managing accounting activities

and records of an organisation. Therefore it is essentially required for every business

organisation whether small or large in size. Every organisation need to record their financial

transactions during the year which helps them in getting accurate financial position of an

enterprise. This projects includes various activities based on different accounting system and

reporting. It also covers various costing methods which help company to analyse their

profitability (Suomala and Lyly-Yrjänäinen, 2012). In order to monitor financial issues the

company need to use different planning tools and techniques in budgetary control. Thus, the

overall project covers all aspect related with management accounting system which helps in

formulating effective decisions for future growth. Company named 'Zylla' is selected for the

purpose of preparation this report.

TASK1

P1. Management accounting and essential requirements of its different accounting system

Management accounting: Management accounting refers to managing the accounting

information and reports in such a manner that will help in taking effective decisions for the

operation of an organisation. Through management accounting company able to operate the

business in more effective and efficient way which also help them in improving financial

stability (Arjaliès and Mundy, 2013). Manager is the one who perform and contribute his efforts

in analysing and monitoring all relevant accounting information which supports in knowing the

accurate financial position of business. This will also help in minimising the risk of uncertainty

and increases chances of generating profit. Therefore management accounting plays an important

role in the success of an organisation for longer period of time. In order to formulate decision

1

TO,

GENERAL MANAGER

ZYLLA COMPANY

SUB: MANAGEMENT ACCOUNTING SYSTEM

INTRODUCTION

Management accounting plays a crucial and vital role in managing accounting activities

and records of an organisation. Therefore it is essentially required for every business

organisation whether small or large in size. Every organisation need to record their financial

transactions during the year which helps them in getting accurate financial position of an

enterprise. This projects includes various activities based on different accounting system and

reporting. It also covers various costing methods which help company to analyse their

profitability (Suomala and Lyly-Yrjänäinen, 2012). In order to monitor financial issues the

company need to use different planning tools and techniques in budgetary control. Thus, the

overall project covers all aspect related with management accounting system which helps in

formulating effective decisions for future growth. Company named 'Zylla' is selected for the

purpose of preparation this report.

TASK1

P1. Management accounting and essential requirements of its different accounting system

Management accounting: Management accounting refers to managing the accounting

information and reports in such a manner that will help in taking effective decisions for the

operation of an organisation. Through management accounting company able to operate the

business in more effective and efficient way which also help them in improving financial

stability (Arjaliès and Mundy, 2013). Manager is the one who perform and contribute his efforts

in analysing and monitoring all relevant accounting information which supports in knowing the

accurate financial position of business. This will also help in minimising the risk of uncertainty

and increases chances of generating profit. Therefore management accounting plays an important

role in the success of an organisation for longer period of time. In order to formulate decision

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

regarding minimise cost and overhead expenses the Zylla needs to analyse its financial

performance in an efficient manner. The manager need to prepare financial report include

accurate and true accounting information which help them in directing to achieve desired goals

and objectives. Manager should also need to focus on improving existing technology and

introduce the latest and updated technology in order to get better outcomes. If company fails to

adopt updated technology due to its cost then it will make negative impact on the performance of

company. This will help company in gaining competitive advantage as well as maximising

profitability as well.

Objectives of Management accounting:

Main objective of management accounting is to provide relevant and accurate financial

information which help manager to take effective decision for the success of an organisation.

Some objectives are mentioned as below:

Helps in assisting plans and formulation of effective polices.

Helps in interpreting the financial data in order to use them in an effective and efficient

manner.

Helps in providing solution of strategies problems.

Helps in motivating employees and coordinating business operations.

Therefore the manager needS to use various types of accounting system which help in

monitoring business operations. Such accounting system are as follows:

Cost accounting system: This system is related to analysing the cost which is incurred in

the production process. Its main motive is to ascertain profitability, cost control and other various

aspects which incurred in production and operational activities (Cost Accounting Systems, 2013).

Therefore manager need to use cost accounting system which allow them to eliminate irrelevant

cost and utilize money in important areas of department. For example product manager uses

various cost such as normal, actual and standard price in order to evaluate expenses incurred in

production process.

Inventory management system: This system has main objective is to minimising the total

cost of inventories in order to generate high return. The manager has to decide that when to order

inventory and how much to order through which it reduces the inventory storage cost and any

spoilage or wastage of inventory. Therefore the manager of Zylla needs to manage company's

2

performance in an efficient manner. The manager need to prepare financial report include

accurate and true accounting information which help them in directing to achieve desired goals

and objectives. Manager should also need to focus on improving existing technology and

introduce the latest and updated technology in order to get better outcomes. If company fails to

adopt updated technology due to its cost then it will make negative impact on the performance of

company. This will help company in gaining competitive advantage as well as maximising

profitability as well.

Objectives of Management accounting:

Main objective of management accounting is to provide relevant and accurate financial

information which help manager to take effective decision for the success of an organisation.

Some objectives are mentioned as below:

Helps in assisting plans and formulation of effective polices.

Helps in interpreting the financial data in order to use them in an effective and efficient

manner.

Helps in providing solution of strategies problems.

Helps in motivating employees and coordinating business operations.

Therefore the manager needS to use various types of accounting system which help in

monitoring business operations. Such accounting system are as follows:

Cost accounting system: This system is related to analysing the cost which is incurred in

the production process. Its main motive is to ascertain profitability, cost control and other various

aspects which incurred in production and operational activities (Cost Accounting Systems, 2013).

Therefore manager need to use cost accounting system which allow them to eliminate irrelevant

cost and utilize money in important areas of department. For example product manager uses

various cost such as normal, actual and standard price in order to evaluate expenses incurred in

production process.

Inventory management system: This system has main objective is to minimising the total

cost of inventories in order to generate high return. The manager has to decide that when to order

inventory and how much to order through which it reduces the inventory storage cost and any

spoilage or wastage of inventory. Therefore the manager of Zylla needs to manage company's

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

inventory on daily basis and should be focused on identifying the accurate position of stock

through using ABC costing and Stock turnover ratios.

Price optimisation system: This system is considered as important tool which is used for

statistical planning. Therefore manager needs to first calculate that how whether the demand of

products changes at different price levels and after which they need to fix the prices of their

product which help in fulfilling the requirements of customers. It is also important for manager

to forecast the demand of product and accordingly developing prices and promotional strategies.

In short the manager has to carefully decide the price of their product which can be easily

afforded by large number of customers (Bebbington, Unerman and O'Dwyer, 2014). This will

helps company in generating huge profits as well as future sustainability.

Job costing system: The job costing system is used by company only when the products

they manufactured are different from each other. It is important for manager to create a job cost

record for each and every item and thereafter assign direct material and direct labour to each job

which help in improving efficiency level of each item.

P2: Various techniques for management accounting reporting

Accounting reporting is deal with systematic measurement of economic activities those

are affecting inflow and outflow of resources in order to develop vital information for decision

making. The financial accountant is related with reporting to external such as shareholder and

owner of the business, revenue and other regulatory agency (Kotas, 2014). The management

accountant reports accounting data is based on internal to the management and employees of

Zylla company. The main information sources is used by financial department is comes from

bookkeeping system. A report is complete detail of crucial accounting statements which is

recorded by Zylla company.

It is related with balance sheet and income statements. It is an effective communication

system which is used by plenty of investors and shareholder to take valuable decision for better

future. With the help of proper reporting system every detail information about financial position

of the company is identified. It is prepared after collecting necessary information from every

department such as finance, HR and operational etc. The transformation of data to higher level of

division to lower level is need to be more effective so that an ideas can be generated regarding

the need of reporting system. Certain procedure is required to record data into the books of

accounts of Zylla company.

3

through using ABC costing and Stock turnover ratios.

Price optimisation system: This system is considered as important tool which is used for

statistical planning. Therefore manager needs to first calculate that how whether the demand of

products changes at different price levels and after which they need to fix the prices of their

product which help in fulfilling the requirements of customers. It is also important for manager

to forecast the demand of product and accordingly developing prices and promotional strategies.

In short the manager has to carefully decide the price of their product which can be easily

afforded by large number of customers (Bebbington, Unerman and O'Dwyer, 2014). This will

helps company in generating huge profits as well as future sustainability.

Job costing system: The job costing system is used by company only when the products

they manufactured are different from each other. It is important for manager to create a job cost

record for each and every item and thereafter assign direct material and direct labour to each job

which help in improving efficiency level of each item.

P2: Various techniques for management accounting reporting

Accounting reporting is deal with systematic measurement of economic activities those

are affecting inflow and outflow of resources in order to develop vital information for decision

making. The financial accountant is related with reporting to external such as shareholder and

owner of the business, revenue and other regulatory agency (Kotas, 2014). The management

accountant reports accounting data is based on internal to the management and employees of

Zylla company. The main information sources is used by financial department is comes from

bookkeeping system. A report is complete detail of crucial accounting statements which is

recorded by Zylla company.

It is related with balance sheet and income statements. It is an effective communication

system which is used by plenty of investors and shareholder to take valuable decision for better

future. With the help of proper reporting system every detail information about financial position

of the company is identified. It is prepared after collecting necessary information from every

department such as finance, HR and operational etc. The transformation of data to higher level of

division to lower level is need to be more effective so that an ideas can be generated regarding

the need of reporting system. Certain procedure is required to record data into the books of

accounts of Zylla company.

3

Reports are more essential components for the company as they are delivering more

effective outcomes in the form of profit during the year. There are basically, more effective

administrators those are responsible for up coming planning and analysis of results. It is said to

be continuous process that is done through out the year (Herzig and et. al., 2012). Thus, it is

important to have a well effective reporting system which can generate positive outcomes for the

company. The main purpose of using reporting system is take crucial decisions on the basis of

financial performances during the year. It is more effective techniques to collect data from

various activities such as operational, investing and financing. It is done to determine whether

daily operations of an organisations are operating in well organised manner or not. With this,

managers can plan to attain their organisational efficiency by allocating resources of Zylla

company in more effective manner.

Report are more accurate with it is prepared by taking reliable data of the company

without any mistakes into the books of accounts. This will help in safeguard of data to be stolen

by other parties. Reporting can help to determine exact cost a company is incurring during the

production of products and services. It has been found that organisation can only achieve their

aims, if they are utilising company resources in more economical manner. By this, the chances of

increasing there reputation in the market can be become more (DRURY, 2013). The sources of

data collecting can be of any mode such as internal and external, financial and non-financial.

It is important for the manages to keep in mind about the social aspects during

preparation of report so that it will be easy to take decision in the benefits of them. In order to

gain the market share and future growth for Zylla company is necessary to have proper data

regarding the current and previous year performances. Hence, they required to use reporting

system in their business to remove obstacles and other barriers that can be make huge impacts on

the performance of the company. Importance of reporting system are:

Effective tools in recording system: With the help of this, managers can have complete

overlooks over employees to identify whether they are delivering the services in correct

manner in achieving aims of zylla company.

Chances of increasing profitability: The primary objectives of every business is to

maximise productivity by allocating resources in more accurate manner. This will make

easy for managers to increase profitability for the company.

Types of reporting system:

4

effective outcomes in the form of profit during the year. There are basically, more effective

administrators those are responsible for up coming planning and analysis of results. It is said to

be continuous process that is done through out the year (Herzig and et. al., 2012). Thus, it is

important to have a well effective reporting system which can generate positive outcomes for the

company. The main purpose of using reporting system is take crucial decisions on the basis of

financial performances during the year. It is more effective techniques to collect data from

various activities such as operational, investing and financing. It is done to determine whether

daily operations of an organisations are operating in well organised manner or not. With this,

managers can plan to attain their organisational efficiency by allocating resources of Zylla

company in more effective manner.

Report are more accurate with it is prepared by taking reliable data of the company

without any mistakes into the books of accounts. This will help in safeguard of data to be stolen

by other parties. Reporting can help to determine exact cost a company is incurring during the

production of products and services. It has been found that organisation can only achieve their

aims, if they are utilising company resources in more economical manner. By this, the chances of

increasing there reputation in the market can be become more (DRURY, 2013). The sources of

data collecting can be of any mode such as internal and external, financial and non-financial.

It is important for the manages to keep in mind about the social aspects during

preparation of report so that it will be easy to take decision in the benefits of them. In order to

gain the market share and future growth for Zylla company is necessary to have proper data

regarding the current and previous year performances. Hence, they required to use reporting

system in their business to remove obstacles and other barriers that can be make huge impacts on

the performance of the company. Importance of reporting system are:

Effective tools in recording system: With the help of this, managers can have complete

overlooks over employees to identify whether they are delivering the services in correct

manner in achieving aims of zylla company.

Chances of increasing profitability: The primary objectives of every business is to

maximise productivity by allocating resources in more accurate manner. This will make

easy for managers to increase profitability for the company.

Types of reporting system:

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Inventory management system: According to this system, managers can enter vital

information regarding inventories in the various statements of the company. It is one of

the effective system that can provide more quick results regarding stock position in the

storehouses. There are some effective techniques by which it can be done such as EOQ

and inventory turnover ratio.

Account receivable report: This specific report is used to analyse complete information

about unpaid customer and bills those are allocated with a particular date. It is the more

effective tools which is helpful in examine exact time required to regain all the amounts.

Performance reporting: As per this system, accounting information are determine

according to the information collected from current and past year performance of Zylla

company. The financial statements of companies are determine by using right tools so

that productivity can be enhanced.

Job costing reporting: It consists of total cost Zylla company is incurring for the

production of every job size of a product during one financial year. It record information

about total labour, material and costs that used at that time.

Operating budget report: This report is based on total income generated by the

company and for this exactly amount of expenses are been used. All these are analyse

under this report so that to gain positive outcomes for the company.

M1: Merits of using management accounting

Management accounting helps manager in managing and monitoring company's financial

transactions which help them in taking effective decision for the growth of an organisation. With

the help of this system the company can utilize its available resources in an optimum manner.

Price optimisations and job costing system are such accounting system which help company in

earning high profits. Thus it has been clearly noted that accounting system help in overall

performance and profitability of company. Zylla therefore needs to use such accounting system

in order to make sustainable future.

D1: Critical evaluation of reporting system

It has been noticed that every business organisation whether small and large must

required a system that can help them to record various financial transactions that are done done

by the company during its operations. Reporting can be an effective tools for Zylla company to

manage and record its transactions. It can be beneficial for increasing profitability as well as

5

information regarding inventories in the various statements of the company. It is one of

the effective system that can provide more quick results regarding stock position in the

storehouses. There are some effective techniques by which it can be done such as EOQ

and inventory turnover ratio.

Account receivable report: This specific report is used to analyse complete information

about unpaid customer and bills those are allocated with a particular date. It is the more

effective tools which is helpful in examine exact time required to regain all the amounts.

Performance reporting: As per this system, accounting information are determine

according to the information collected from current and past year performance of Zylla

company. The financial statements of companies are determine by using right tools so

that productivity can be enhanced.

Job costing reporting: It consists of total cost Zylla company is incurring for the

production of every job size of a product during one financial year. It record information

about total labour, material and costs that used at that time.

Operating budget report: This report is based on total income generated by the

company and for this exactly amount of expenses are been used. All these are analyse

under this report so that to gain positive outcomes for the company.

M1: Merits of using management accounting

Management accounting helps manager in managing and monitoring company's financial

transactions which help them in taking effective decision for the growth of an organisation. With

the help of this system the company can utilize its available resources in an optimum manner.

Price optimisations and job costing system are such accounting system which help company in

earning high profits. Thus it has been clearly noted that accounting system help in overall

performance and profitability of company. Zylla therefore needs to use such accounting system

in order to make sustainable future.

D1: Critical evaluation of reporting system

It has been noticed that every business organisation whether small and large must

required a system that can help them to record various financial transactions that are done done

by the company during its operations. Reporting can be an effective tools for Zylla company to

manage and record its transactions. It can be beneficial for increasing profitability as well as

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

growth efficiency for the company. The goal of company should be attain in more quick time

with managing total costs and expenses that are incur at the time of production process.

TASK 2

P3: Different costing methods

In every segment of business, cost is the most crucial aspects that can be used up to

develop or produce something or deliver a services. In business, the cost may be one of acquiring

under which the amount of money expended to acquire is termed as cost. Whereas, costing is a

systematic process of recording, classifying, examine and summarising alternate courses of

actions for the control of costs (Cadez and Guilding, 2012). It can involve assessment of variable

costs which are those costs that are changes with extra production of activities.

This types of costs are said to be direct costs. Full costing can be other managerial

accounting techniques that describes when every fixed and variable costs that consists

production costs which is used to calculate cost per units. It can be said that total costs those are

varies with some alternative to operate a business through allocation of income and expenses at

various stages of manufacturing phases. It has been seen that scope of cost accounting is very

narrow as compare to accounting system. Under this, it is the primary responsibilities of

managers to set target and make an estimation about total costs and expenses that are going to be

incur by the company are recorded in it. There are certain techniques of costing that can be more

effective in making profitability for the company. Such as :

Absorption costing: These are said to be that cost which is incurred over every stages of

production. It means that both fixed and variable costs are considered during manufacturing of

products and services. Thus, such methods are used as long term basis.

Marginal costing: It is said to be that costs which is incur by the company during

production of one extra units of products (Merchant, 2012). It is divided into two parts such as

fixed and variables. But for the production purpose only variable costs are taken into

consideration.

Comparison:

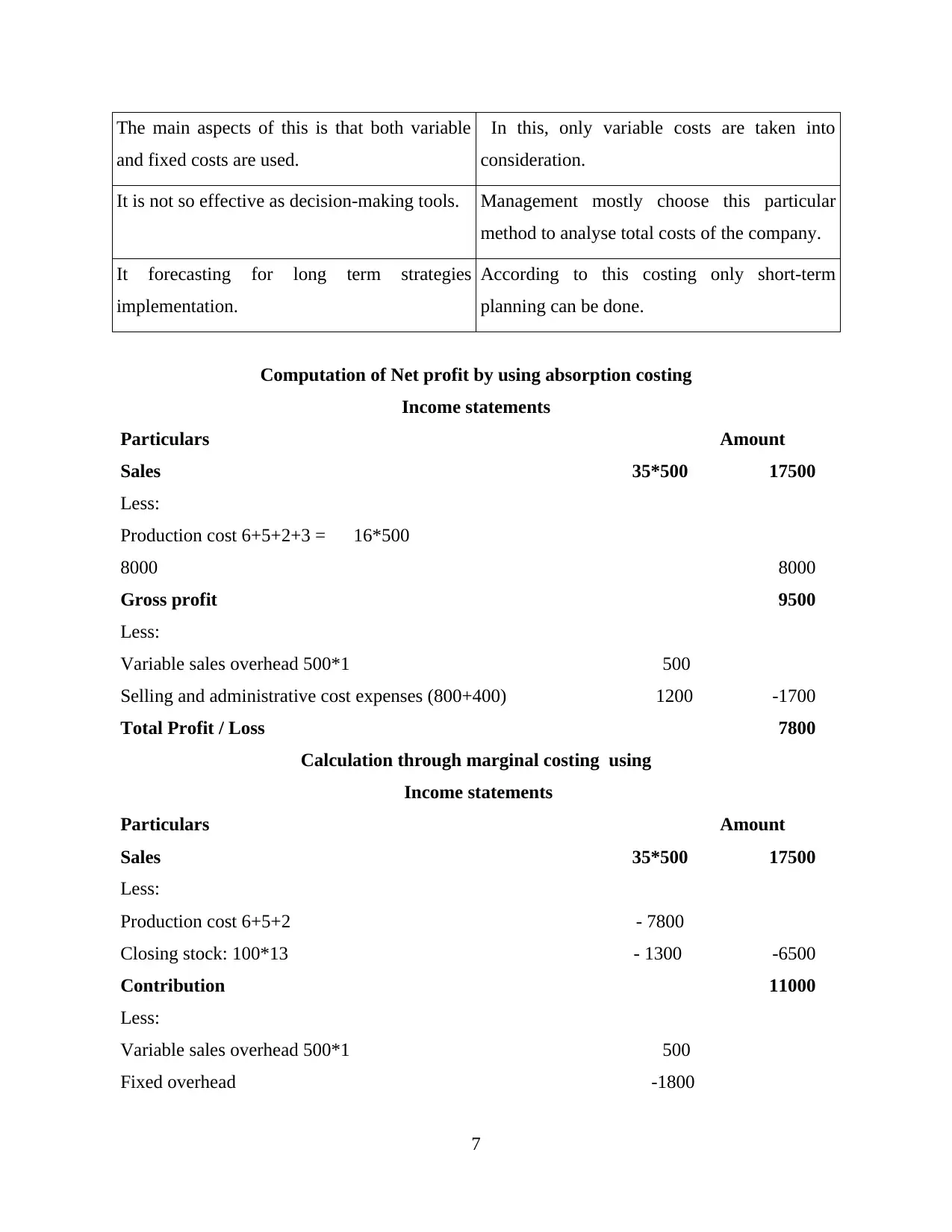

Absorption costing Marginal costing

In this particular method, cost is used as

conventional basis.

By the use of such costing method, data is

shown through contribution per units.

6

with managing total costs and expenses that are incur at the time of production process.

TASK 2

P3: Different costing methods

In every segment of business, cost is the most crucial aspects that can be used up to

develop or produce something or deliver a services. In business, the cost may be one of acquiring

under which the amount of money expended to acquire is termed as cost. Whereas, costing is a

systematic process of recording, classifying, examine and summarising alternate courses of

actions for the control of costs (Cadez and Guilding, 2012). It can involve assessment of variable

costs which are those costs that are changes with extra production of activities.

This types of costs are said to be direct costs. Full costing can be other managerial

accounting techniques that describes when every fixed and variable costs that consists

production costs which is used to calculate cost per units. It can be said that total costs those are

varies with some alternative to operate a business through allocation of income and expenses at

various stages of manufacturing phases. It has been seen that scope of cost accounting is very

narrow as compare to accounting system. Under this, it is the primary responsibilities of

managers to set target and make an estimation about total costs and expenses that are going to be

incur by the company are recorded in it. There are certain techniques of costing that can be more

effective in making profitability for the company. Such as :

Absorption costing: These are said to be that cost which is incurred over every stages of

production. It means that both fixed and variable costs are considered during manufacturing of

products and services. Thus, such methods are used as long term basis.

Marginal costing: It is said to be that costs which is incur by the company during

production of one extra units of products (Merchant, 2012). It is divided into two parts such as

fixed and variables. But for the production purpose only variable costs are taken into

consideration.

Comparison:

Absorption costing Marginal costing

In this particular method, cost is used as

conventional basis.

By the use of such costing method, data is

shown through contribution per units.

6

The main aspects of this is that both variable

and fixed costs are used.

In this, only variable costs are taken into

consideration.

It is not so effective as decision-making tools. Management mostly choose this particular

method to analyse total costs of the company.

It forecasting for long term strategies

implementation.

According to this costing only short-term

planning can be done.

Computation of Net profit by using absorption costing

Income statements

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2+3 = 16*500

8000 8000

Gross profit 9500

Less:

Variable sales overhead 500*1 500

Selling and administrative cost expenses (800+400) 1200 -1700

Total Profit / Loss 7800

Calculation through marginal costing using

Income statements

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2 - 7800

Closing stock: 100*13 - 1300 -6500

Contribution 11000

Less:

Variable sales overhead 500*1 500

Fixed overhead -1800

7

and fixed costs are used.

In this, only variable costs are taken into

consideration.

It is not so effective as decision-making tools. Management mostly choose this particular

method to analyse total costs of the company.

It forecasting for long term strategies

implementation.

According to this costing only short-term

planning can be done.

Computation of Net profit by using absorption costing

Income statements

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2+3 = 16*500

8000 8000

Gross profit 9500

Less:

Variable sales overhead 500*1 500

Selling and administrative cost expenses (800+400) 1200 -1700

Total Profit / Loss 7800

Calculation through marginal costing using

Income statements

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2 - 7800

Closing stock: 100*13 - 1300 -6500

Contribution 11000

Less:

Variable sales overhead 500*1 500

Fixed overhead -1800

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Selling and administrative cost expenses (800+400) -1200 -3500

Total Profit / Loss 7500

M2: Use of management accounting techniques

There are different factors which affect the financial position of Zylla . Such factors

include internal and external environment of an organisation. Therefore manager need to adopt

different management accounting techniques in order to eliminate financial errors and mistakes

which helps in taking effective decision for the growth of an organisation. ABC costing or micro

economic tool such as cost volume profit help company to reduce irrelevant cost and thus

generate profits which also help an organisation to survive for longer period of time.

D2: Critical analysis of income statements

As per the above computation of company's net profit. Zylla company is using both

absorption and marginal costing. It has been seen that both are more effective methods from

calculating profit for the company. If they are going with marginal costing, profit of 7500 is

generated. While, if using absorption methods they are getting profit of 7800. The difference of

300 is analyses which is occur because of fixed costs adjustments in marginal cost calculation. In

order to make crucial decision-making, marginal cost methods are more effective and reliable. It

can be further utilised in improving the future performances.

TASK 3

P4: Benefits and limitation of using planning techniques

Budget is said to be an effective techniques by which Zylla company and estimate their

future investments plans. It will help them to determine an assumption of total cost and expenses

those are going to be incur by them. It is termed as well planned mode of collection for a

particular period of time (Arroyo, 2012). It is known as more complete framework of operations

and strategies that are crucial for attain future targets. Generally, it is prepared for that time in

which they can advance there costs.

Budgetary-control: It is known as a techniques by which managers can determine total

utility of budgets to monitor and control total costs and operations during a financial time. On the

other hand, it is the process for managers to set financial and performances objectives with

budgets.

Process of budgetary-control:

8

Total Profit / Loss 7500

M2: Use of management accounting techniques

There are different factors which affect the financial position of Zylla . Such factors

include internal and external environment of an organisation. Therefore manager need to adopt

different management accounting techniques in order to eliminate financial errors and mistakes

which helps in taking effective decision for the growth of an organisation. ABC costing or micro

economic tool such as cost volume profit help company to reduce irrelevant cost and thus

generate profits which also help an organisation to survive for longer period of time.

D2: Critical analysis of income statements

As per the above computation of company's net profit. Zylla company is using both

absorption and marginal costing. It has been seen that both are more effective methods from

calculating profit for the company. If they are going with marginal costing, profit of 7500 is

generated. While, if using absorption methods they are getting profit of 7800. The difference of

300 is analyses which is occur because of fixed costs adjustments in marginal cost calculation. In

order to make crucial decision-making, marginal cost methods are more effective and reliable. It

can be further utilised in improving the future performances.

TASK 3

P4: Benefits and limitation of using planning techniques

Budget is said to be an effective techniques by which Zylla company and estimate their

future investments plans. It will help them to determine an assumption of total cost and expenses

those are going to be incur by them. It is termed as well planned mode of collection for a

particular period of time (Arroyo, 2012). It is known as more complete framework of operations

and strategies that are crucial for attain future targets. Generally, it is prepared for that time in

which they can advance there costs.

Budgetary-control: It is known as a techniques by which managers can determine total

utility of budgets to monitor and control total costs and operations during a financial time. On the

other hand, it is the process for managers to set financial and performances objectives with

budgets.

Process of budgetary-control:

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Consult with concern department managers: It is essential for them to make effective

analysis about budget needs in Zylla company. Because, it can only be prepared after taking

proper information about concern department.

Determine effective assumption: The next step would be collection of information from

department is implemented. These sources are gathered from finance, HR and other necessary

sectors. It is done so to make strategies for coming time.

Set data for budget to attain objectives: Under this process, a perfect list of

information is frame by assembling information those are collected from every persons.

Measurement of data with actual: The position of Zylla company is evaluated through

comprising the outcomes with actual budgets. With this a well effective solution can be gain in

order to make bright future.

Review stage: Under this final stage, complete overview of budgets are analyses with

necessary feedback if any rectification needed then it would be solved before transferring it to

higher level.

Planning tools: In an organisation, it is seen that proper planning can make there

business more profitable. It can operate there business growth chances in right manner according

to its vision and mission. Some of them are discussed underneath:

Forecasting tools: As from the name it is clearly stated that this tools is based on

assumption. It is for internal control management that includes effective ability, knowledge and

decision-making (Bodie, Kane and Marcus, 2014). It is typically relies on historical data for

estimating future aims. Such kind of tools are used according to the capability of organization

that can deliver positive outcomes for the company in future times.

Advantages:

It is an important aspects for industries in order to evaluate pre-determine objectives. By

this, managers can identify an estimation of total cost and revenue that are incurred by company

during the time.

Disadvantage:

In some situation, it is not considered as much effective. Because it is totally based on

assumption.

9

analysis about budget needs in Zylla company. Because, it can only be prepared after taking

proper information about concern department.

Determine effective assumption: The next step would be collection of information from

department is implemented. These sources are gathered from finance, HR and other necessary

sectors. It is done so to make strategies for coming time.

Set data for budget to attain objectives: Under this process, a perfect list of

information is frame by assembling information those are collected from every persons.

Measurement of data with actual: The position of Zylla company is evaluated through

comprising the outcomes with actual budgets. With this a well effective solution can be gain in

order to make bright future.

Review stage: Under this final stage, complete overview of budgets are analyses with

necessary feedback if any rectification needed then it would be solved before transferring it to

higher level.

Planning tools: In an organisation, it is seen that proper planning can make there

business more profitable. It can operate there business growth chances in right manner according

to its vision and mission. Some of them are discussed underneath:

Forecasting tools: As from the name it is clearly stated that this tools is based on

assumption. It is for internal control management that includes effective ability, knowledge and

decision-making (Bodie, Kane and Marcus, 2014). It is typically relies on historical data for

estimating future aims. Such kind of tools are used according to the capability of organization

that can deliver positive outcomes for the company in future times.

Advantages:

It is an important aspects for industries in order to evaluate pre-determine objectives. By

this, managers can identify an estimation of total cost and revenue that are incurred by company

during the time.

Disadvantage:

In some situation, it is not considered as much effective. Because it is totally based on

assumption.

9

Scenario analysis: It is more common as sensitivity analysis, but it takes into

consideration about the changes of several important variables at the same times. It can be more

effectively used by managers to make there decision according to the current market trends.

Advantages: By the help of this, managers can generate more effective ideas about future

opportunities that are beneficial for the company.

Disadvantage: It has been observed that few times, it is not that much effective because

of changes in policies. It is difficult to incur more effective outcomes with the available

resources.

Contingency tools: It is a management techniques which is used to evaluate impact of

potential problem and ensure that appropriate arrangements are made in prior to respond in

allotted time (Fourie and et. al., 2015). In order to implement this plan, proper experienced

managers are required.

Advantages: It is considered to be more effective tool to control extra cost for the

company.

Disadvantage: Such kind of tools are more uncertain and hard to manage because

appropriate skills are required to do so.

M3: Analysis of planning techniques

For every organisation, it is important to have a perfect market share in order to build

good image in the market in front of competitors. This resources are totally utilised by using

innovative techniques that can help in attain more effective outcomes for them. Some of them are

scenario analysis which is useful in control issues those are available in the production process.

However, forecasting tools are another tools which is used in order to estimate profitability and

total revenue for the company.

D3: Critical evaluation of financial issues

It has been seen that performance and growth of an organisation is getting impact because

of various issues such as financial and non-financial. The performance and control measures are

needed to be implemented in right manner to overcome financial problems. It can increase

profitability as well as chance of better goodwill in the market. Some issues can be solved by

using balance scorecard system which is made for such kind of situations.

10

consideration about the changes of several important variables at the same times. It can be more

effectively used by managers to make there decision according to the current market trends.

Advantages: By the help of this, managers can generate more effective ideas about future

opportunities that are beneficial for the company.

Disadvantage: It has been observed that few times, it is not that much effective because

of changes in policies. It is difficult to incur more effective outcomes with the available

resources.

Contingency tools: It is a management techniques which is used to evaluate impact of

potential problem and ensure that appropriate arrangements are made in prior to respond in

allotted time (Fourie and et. al., 2015). In order to implement this plan, proper experienced

managers are required.

Advantages: It is considered to be more effective tool to control extra cost for the

company.

Disadvantage: Such kind of tools are more uncertain and hard to manage because

appropriate skills are required to do so.

M3: Analysis of planning techniques

For every organisation, it is important to have a perfect market share in order to build

good image in the market in front of competitors. This resources are totally utilised by using

innovative techniques that can help in attain more effective outcomes for them. Some of them are

scenario analysis which is useful in control issues those are available in the production process.

However, forecasting tools are another tools which is used in order to estimate profitability and

total revenue for the company.

D3: Critical evaluation of financial issues

It has been seen that performance and growth of an organisation is getting impact because

of various issues such as financial and non-financial. The performance and control measures are

needed to be implemented in right manner to overcome financial problems. It can increase

profitability as well as chance of better goodwill in the market. Some issues can be solved by

using balance scorecard system which is made for such kind of situations.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.