Comprehensive Management Accounting Report: Imperial Brands Plc

VerifiedAdded on 2023/01/19

|24

|7531

|68

Report

AI Summary

This report provides a detailed analysis of management accounting practices at Imperial Brands Plc, a UK-based tobacco company. It examines the role and necessity of various management accounting systems (MAS), including inventory management, price optimization, and cost accounting systems. The report contrasts MAS with financial accounting, highlighting their differences in terms of information scope, timeframes, and obligations. It further explores various management accounting reports (MAR) such as account receivable aging, cost accounting, performance, and stock reports, detailing their advantages and applications within the organization. The report also delves into the amalgamation of MAS and management reporting within Imperial Brands Plc's organizational activities. Furthermore, the report investigates the usage of tools for cost evaluation, including building income statements, and analyzes planning tools for budgetary control, evaluating both their positive and negative aspects. Finally, it contrasts different management accounting system styles to address financial concerns and examines how MA enables the company to respond to financial challenges for sustainability, along with the usage of planning tools to take action against financial concerns for gaining potential outcomes.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Examine the MA and necessities of various kinds of MA systems in organisation. ..................3

Evaluate various tools and methods of MAR. ............................................................................5

Advantages of MA system...........................................................................................................6

Amalgamation of MAS and MR in organisational activities. .....................................................7

TASK 2............................................................................................................................................7

Usage of right kind of tools for evaluation of cost by building income statement. ....................7

Usage of MA techniques..............................................................................................................9

By framing financial reports by interpret by various activities. ...............................................10

Evaluate both positive and negative aspects of planning tools for control budgets. ................10

Evaluate the various kinds of planning techniques and their applicability in context of framing

and forecasting budgets. ............................................................................................................12

TASK 4..........................................................................................................................................12

Contrast the various styles of management accounting systems to give response in against

financial concerns. ....................................................................................................................12

How MA enables to respond against the financial concerns for gaining sustainability. ..........14

Examine the usage of planning tools to take action against the concerns related with finance

for gaining potential outcomes...................................................................................................15

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Examine the MA and necessities of various kinds of MA systems in organisation. ..................3

Evaluate various tools and methods of MAR. ............................................................................5

Advantages of MA system...........................................................................................................6

Amalgamation of MAS and MR in organisational activities. .....................................................7

TASK 2............................................................................................................................................7

Usage of right kind of tools for evaluation of cost by building income statement. ....................7

Usage of MA techniques..............................................................................................................9

By framing financial reports by interpret by various activities. ...............................................10

Evaluate both positive and negative aspects of planning tools for control budgets. ................10

Evaluate the various kinds of planning techniques and their applicability in context of framing

and forecasting budgets. ............................................................................................................12

TASK 4..........................................................................................................................................12

Contrast the various styles of management accounting systems to give response in against

financial concerns. ....................................................................................................................12

How MA enables to respond against the financial concerns for gaining sustainability. ..........14

Examine the usage of planning tools to take action against the concerns related with finance

for gaining potential outcomes...................................................................................................15

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................17

INTRODUCTION

MA is one of crucial aspect of accounting system for an administration that connect or

linked the tools and techniques for analysing and evaluating the knowledge and information both

for economic and non economic aspects to accumulate position of an administration . Major goal

of MA is to prepare internal and external reports related to management accounting to proceed in

business functions. In today’s world the organisations by availing economic accounting tools and

techniques to gather potential data and information about the financial projection and estimated

cost and expenditures in near future to take appropriate kind of decisions. Respective assignment

rely on Imperial Brands Plc which is an UK based Tobacco manufacturing company,

headquarters is in Bristol, UK. This report is based on MA and essential requirements of various

kinds of MA system for an organization. Further it includes various acting used by management

accounting reporting to collect data and information for gaining potential outcomes. It also

includes the calculation of cost by using the tools and method by using the marginal and

absorption costing systems to evaluate various factors. By elaborating the benefit and disfavour

by using kinds of planning tools to measure various budgetary control. At last it includes

comparison in various organisations in between management accounting systems to respond

financial problems.

TASK 1

Examine the MA and necessities of various kinds of MA systems in organisation.

Imperial brands Plc:

Respective organisation formerly known as Imperial Tobacco Group Plc which is an

multinational Tobacco company headquartered in Bristol in UK. It is the fourth largest

international Cigarette company measured by market share and world's largest producer of

Cigars, tobacco papers and many more.

Role of Management accounting:

MA is very much potential for an organisation as it plan the each and every aspect with in

organisation. Such as resources, budgets and forecasting and many more attributes. After

planning each and every event in proper manner it control it by using various tools and

techniques for setting standards in order to gain accurate results. By using benchmarking, key

performance indicators and many more to control the activities for gaining desirable outcomes.

MA is one of crucial aspect of accounting system for an administration that connect or

linked the tools and techniques for analysing and evaluating the knowledge and information both

for economic and non economic aspects to accumulate position of an administration . Major goal

of MA is to prepare internal and external reports related to management accounting to proceed in

business functions. In today’s world the organisations by availing economic accounting tools and

techniques to gather potential data and information about the financial projection and estimated

cost and expenditures in near future to take appropriate kind of decisions. Respective assignment

rely on Imperial Brands Plc which is an UK based Tobacco manufacturing company,

headquarters is in Bristol, UK. This report is based on MA and essential requirements of various

kinds of MA system for an organization. Further it includes various acting used by management

accounting reporting to collect data and information for gaining potential outcomes. It also

includes the calculation of cost by using the tools and method by using the marginal and

absorption costing systems to evaluate various factors. By elaborating the benefit and disfavour

by using kinds of planning tools to measure various budgetary control. At last it includes

comparison in various organisations in between management accounting systems to respond

financial problems.

TASK 1

Examine the MA and necessities of various kinds of MA systems in organisation.

Imperial brands Plc:

Respective organisation formerly known as Imperial Tobacco Group Plc which is an

multinational Tobacco company headquartered in Bristol in UK. It is the fourth largest

international Cigarette company measured by market share and world's largest producer of

Cigars, tobacco papers and many more.

Role of Management accounting:

MA is very much potential for an organisation as it plan the each and every aspect with in

organisation. Such as resources, budgets and forecasting and many more attributes. After

planning each and every event in proper manner it control it by using various tools and

techniques for setting standards in order to gain accurate results. By using benchmarking, key

performance indicators and many more to control the activities for gaining desirable outcomes.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MA as stated above, is significant aspect for an organisation that helps to proceed by

controlling both the qualitative and quantitative data and statistics to prepare the reports to gain

important insights to gain potential outcomes in positive manner (Ward, 2012). Here are the few

advantages of MAS that are as follows:

MAS is very much beneficial for an organization to accumulate and effectively utilize the

knowledge and information collected by a firm. It proved beneficial for organization in order to

estimate the futuristic actions and activities of organisational income and expenditures to gain

potential outcomes to plan and coordinate with their teams to coordinate them in proper way.

The another major benefit of MAS that it helps in control all the major works and

activities that it helps in control all the financial activities such as accumulation of financial

activities, budgeting and controlling by measuring various events for gaining potential outcomes

(Otley and Emmanuel, 2013). The another crucial kind of contribution of management

accounting system that after building fiscal reports organization can be able to evaluate various

factors that helps in decision making process. In context of Imperial brands Plc they analyse

financial reports, accounting methodologies and concepts in order to acknowledge financial

status of an organization.

So from the above discussion it has been summarized that MAS proved very much

beneficial for an organization to gain important insights and knowledge for taking effective kind

of decisions.

Comparison in between the MAS and FAS:

Basis MA Financial accounting

Important aspects MA elaborates both financial and non

financial kind of information and

data.

In financial accounting only financial

data and statistics should be covered

in order to reach at ultimate goal.

Time required to

prepare or build

reports

In this accounting, the reports are

prepared as per the requirement of the

organization in order to gain potential

outcomes.

In financial accounting the reports

collect with the help of norms of

IFRS in order to accumulate

necessary information.

Obligation MA system is not obligatory for On other hand financial accounting

controlling both the qualitative and quantitative data and statistics to prepare the reports to gain

important insights to gain potential outcomes in positive manner (Ward, 2012). Here are the few

advantages of MAS that are as follows:

MAS is very much beneficial for an organization to accumulate and effectively utilize the

knowledge and information collected by a firm. It proved beneficial for organization in order to

estimate the futuristic actions and activities of organisational income and expenditures to gain

potential outcomes to plan and coordinate with their teams to coordinate them in proper way.

The another major benefit of MAS that it helps in control all the major works and

activities that it helps in control all the financial activities such as accumulation of financial

activities, budgeting and controlling by measuring various events for gaining potential outcomes

(Otley and Emmanuel, 2013). The another crucial kind of contribution of management

accounting system that after building fiscal reports organization can be able to evaluate various

factors that helps in decision making process. In context of Imperial brands Plc they analyse

financial reports, accounting methodologies and concepts in order to acknowledge financial

status of an organization.

So from the above discussion it has been summarized that MAS proved very much

beneficial for an organization to gain important insights and knowledge for taking effective kind

of decisions.

Comparison in between the MAS and FAS:

Basis MA Financial accounting

Important aspects MA elaborates both financial and non

financial kind of information and

data.

In financial accounting only financial

data and statistics should be covered

in order to reach at ultimate goal.

Time required to

prepare or build

reports

In this accounting, the reports are

prepared as per the requirement of the

organization in order to gain potential

outcomes.

In financial accounting the reports

collect with the help of norms of

IFRS in order to accumulate

necessary information.

Obligation MA system is not obligatory for On other hand financial accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

organisations to comply with rules

and regulations.

proved useful for organisations to

accumulate information at regular

intervals.

So from the above discussion it has been summarized that MAS is very much essential

for an organization to accumulate necessary knowledge and information to take decisions

appropriately.

Management accounting systems

Inventory management system:

Inventory management system is a software that proved useful for tracking the level of

inventory, orders and sales with deliverables. Respective system proved useful for manufacturing

industries in order to create work order, bill of materials and other kind of production related

documents. Respective tool proved beneficial for organisation to track level of inventory to fulfil

the consumers needs and demands in appropriate manner.

Respective system of MA is significant for a firm that helps to track the movement of

relative products and services until it reached to ultimate consumer base. Also it enables to verify

the raw material and quantity of final goods to ultimate consumer base so ultimately it proved

beneficial for Imperial Brands Plc to facilitate the path to meet the demands of consumers in

positive manner. The most important function of respective system of management to maintain

records of overall transfer and also keep balance of demand and supply side to gain optimum

kinds of outputs.

Price optimization system:

Price optimisation system is one of most useful tool for an organisation to analyse or

evaluated by an organisation the way consumers respond in against different price range

regarding the products and services by using statistics and data in appropriate manner.

Respective tool proved beneficial for organisation to choose one of best prices for products and

services.

Pricing is one of the most essential function of MA which directly impacts on the demand

and supply side of the business (Parker, 2012). It is very much essential for the organisation to

affix one of best price of goods for gaining potential outcomes. Respective system proved

beneficial to set one of best price that are suitable for organisation as well as individual to track

the behaviour of consumers at every tier of their purchasing behaviour. In context of Imperial

and regulations.

proved useful for organisations to

accumulate information at regular

intervals.

So from the above discussion it has been summarized that MAS is very much essential

for an organization to accumulate necessary knowledge and information to take decisions

appropriately.

Management accounting systems

Inventory management system:

Inventory management system is a software that proved useful for tracking the level of

inventory, orders and sales with deliverables. Respective system proved useful for manufacturing

industries in order to create work order, bill of materials and other kind of production related

documents. Respective tool proved beneficial for organisation to track level of inventory to fulfil

the consumers needs and demands in appropriate manner.

Respective system of MA is significant for a firm that helps to track the movement of

relative products and services until it reached to ultimate consumer base. Also it enables to verify

the raw material and quantity of final goods to ultimate consumer base so ultimately it proved

beneficial for Imperial Brands Plc to facilitate the path to meet the demands of consumers in

positive manner. The most important function of respective system of management to maintain

records of overall transfer and also keep balance of demand and supply side to gain optimum

kinds of outputs.

Price optimization system:

Price optimisation system is one of most useful tool for an organisation to analyse or

evaluated by an organisation the way consumers respond in against different price range

regarding the products and services by using statistics and data in appropriate manner.

Respective tool proved beneficial for organisation to choose one of best prices for products and

services.

Pricing is one of the most essential function of MA which directly impacts on the demand

and supply side of the business (Parker, 2012). It is very much essential for the organisation to

affix one of best price of goods for gaining potential outcomes. Respective system proved

beneficial to set one of best price that are suitable for organisation as well as individual to track

the behaviour of consumers at every tier of their purchasing behaviour. In context of Imperial

Brands Plc by using respective kind of management accounting system examine various factors

which directly contributes in formation of pricing to gain best prices in respect of their product.

Cost accounting system:

Cost accounting system is one of most potential framework used by an organisation to

estimate the cost of products and services in proper manner. In context of Imperial Brands Plc

they by using respective tool determine cost of products and services in proper manner.

Respective system is one of most structured format to figure out the cost of products and

services to accumulate information regarding the profit and losses occurred by the organisation

at every tier of production and consumption. It proved beneficial for organisation who deals in

large product portfolio by categorised into two forms such as job order costing and process

costing system. In context of Imperial Brands Plc they by avail both kind of costing system

determine actual cost of related products of firm.

Evaluate various tools and methods of MAR.

Management accounting reports:

MAR defined as kind of reports which are composed or prepared by the organization to

control the financial and non-financial knowledge and information. There are various kinds of

reports of MA that are as follows:

Account receivable ageing reports:

Respective kinds of reports used by an organization by gathering information from

various debtors by including various kinds of debt information (Otley, 2016). The main role of

respective reports to provide assistance to financial department to provide necessary knowledge

and information to such as amount due to debtors. In context of Imperial Brand company, they

by using respective kind of financial reports their financial manager utilizes key knowledge to

prepare and collect debts.

Cost accounting report:

Respective reports after utilization of the information and knowledge by using the cost

accounting system. By using such kinds of reports by accumulating each and every activity by

predicting future actions and plan accordingly (Schaltegger and Csutora, 2012). In context of

Imperial Brands Plc they accumulate necessary information related to cost by operating various

activities related to tobacco production and consumption.

Performance report:

which directly contributes in formation of pricing to gain best prices in respect of their product.

Cost accounting system:

Cost accounting system is one of most potential framework used by an organisation to

estimate the cost of products and services in proper manner. In context of Imperial Brands Plc

they by using respective tool determine cost of products and services in proper manner.

Respective system is one of most structured format to figure out the cost of products and

services to accumulate information regarding the profit and losses occurred by the organisation

at every tier of production and consumption. It proved beneficial for organisation who deals in

large product portfolio by categorised into two forms such as job order costing and process

costing system. In context of Imperial Brands Plc they by avail both kind of costing system

determine actual cost of related products of firm.

Evaluate various tools and methods of MAR.

Management accounting reports:

MAR defined as kind of reports which are composed or prepared by the organization to

control the financial and non-financial knowledge and information. There are various kinds of

reports of MA that are as follows:

Account receivable ageing reports:

Respective kinds of reports used by an organization by gathering information from

various debtors by including various kinds of debt information (Otley, 2016). The main role of

respective reports to provide assistance to financial department to provide necessary knowledge

and information to such as amount due to debtors. In context of Imperial Brand company, they

by using respective kind of financial reports their financial manager utilizes key knowledge to

prepare and collect debts.

Cost accounting report:

Respective reports after utilization of the information and knowledge by using the cost

accounting system. By using such kinds of reports by accumulating each and every activity by

predicting future actions and plan accordingly (Schaltegger and Csutora, 2012). In context of

Imperial Brands Plc they accumulate necessary information related to cost by operating various

activities related to tobacco production and consumption.

Performance report:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It is the one of most essential kind of report by evaluating outcomes after estimated the

presented variations in between the two events in proper manner. in context of Imperial Brands

Plc their managers by using respective reports take appropriate kind of decisions by using

promotional events for gaining potential outcomes.

Stock reports:

Respective kind of financial reports is very much similar to cost accounting reports that

build by the after integrating the strong inventory management system. Respective kind of

information give detailed description about quantity that are accumulated in the warehouses as

well as in he production of the products and services in order to gaining potential outcomes by

collecting data and statistics properly. In context of Imperial brands Plc they accumulate

necessary information regarding the purchasing the raw material to compete in business

environment. With the help of various stock methods such as LIFO, FIFO and other aspects, in

context of Imperial brands Plc they for manufacture the tobacco products and services to keep

eye on every aspect for taking essential kind of decisions.

Advantages of MA system

Inventory management system:

Major advantage of IMS is to link with various processes of quantity and cost factors by

using kinds of materials utilized by an organization. In context of Imperial Brand plc they gain

important benefits from accounting system to the production system of tobacco in cost effective

manner.

Price optimization system:

Respective kind of MAS is proved beneficial by administration to get revise by using the

pricing strategies as per the need and wants of consumers (Fullerton and et. al., 2014).

Respective organization revise their pricing strategies as per the competitors pricing to gain

optimum kinds of results.

Cost accounting system:

With the help of CAS, by using overall production and expenditure by evaluating

various aspects in controlled manner in best effective way or manner. in context of Imperial

Brand Plc in their financial department optimize key financial information by controlling over

the cost by controlling various events.

presented variations in between the two events in proper manner. in context of Imperial Brands

Plc their managers by using respective reports take appropriate kind of decisions by using

promotional events for gaining potential outcomes.

Stock reports:

Respective kind of financial reports is very much similar to cost accounting reports that

build by the after integrating the strong inventory management system. Respective kind of

information give detailed description about quantity that are accumulated in the warehouses as

well as in he production of the products and services in order to gaining potential outcomes by

collecting data and statistics properly. In context of Imperial brands Plc they accumulate

necessary information regarding the purchasing the raw material to compete in business

environment. With the help of various stock methods such as LIFO, FIFO and other aspects, in

context of Imperial brands Plc they for manufacture the tobacco products and services to keep

eye on every aspect for taking essential kind of decisions.

Advantages of MA system

Inventory management system:

Major advantage of IMS is to link with various processes of quantity and cost factors by

using kinds of materials utilized by an organization. In context of Imperial Brand plc they gain

important benefits from accounting system to the production system of tobacco in cost effective

manner.

Price optimization system:

Respective kind of MAS is proved beneficial by administration to get revise by using the

pricing strategies as per the need and wants of consumers (Fullerton and et. al., 2014).

Respective organization revise their pricing strategies as per the competitors pricing to gain

optimum kinds of results.

Cost accounting system:

With the help of CAS, by using overall production and expenditure by evaluating

various aspects in controlled manner in best effective way or manner. in context of Imperial

Brand Plc in their financial department optimize key financial information by controlling over

the cost by controlling various events.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Amalgamation of MAS and MR in organisational activities.

In MAS the wide range of accounting system are included in each and every item by

inclined to gain continuous process and objectives. In context of Imperial Brands Plc there all

departments integrated with one another by sharing the cognition and information to one another

to reach at optimum objectives (Arroyo, 2012). They integrate the goals of finance department

with marketing and human resource by aligned their various aspects. For an example in

respective organization by using various reports such as cost accounting reporting, stock reports

they allocate roles and responsibilities to them.

TASK 2

Usage of right kind of tools for evaluation of cost by building income statement.

For an organization to prepare the income statement it is very much necessary to optimize

the different kinds of cost factors which enables to gain important insights and information such

as deliver one of best prices to consumers, to analyse competitors pricing and many more factors.

In context of Imperial Brands Plc, they use various kinds of costs that are as follows:

Absorption costing:

Respective kind of cost helps to organization by using various kind of technique by

relating the fixed and non-fixed kind of cost to prepare financial statements by examine every

factor associated with the firm. In context of Imperial Brands Plc, they by using idea both fixed

and non-fixed cost related to their project to bring it into practice.

Marginal costing:

In marginal costing the organization use the both fixed cost by relating the periodical

units of cost in order for gaining potential outcomes. In context of Imperial Brands by using the

Marginal costing system they evaluate both fixed and non-fixed cost by demonstrating various

factors (Maas, Schaltegger and Crutzen, 2016).

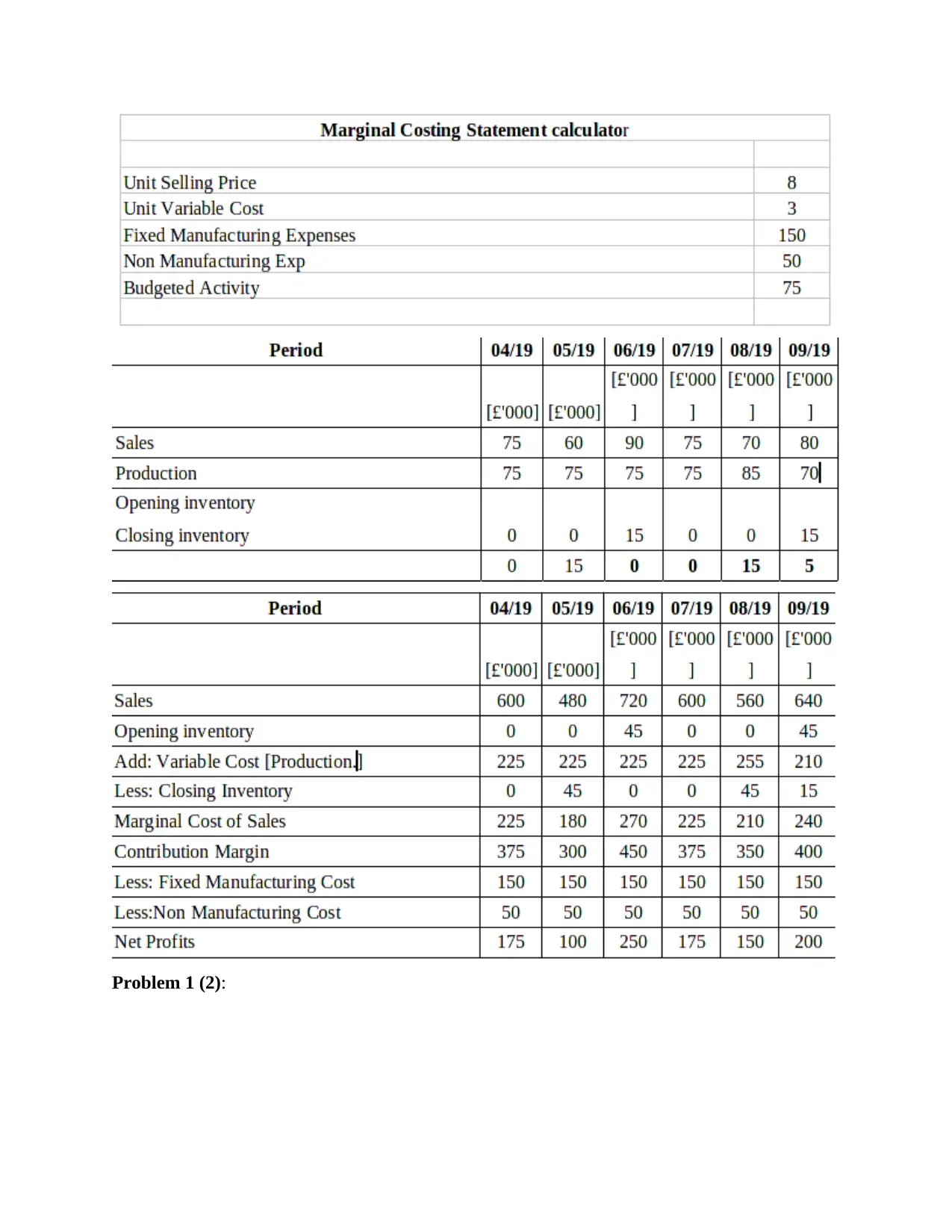

Problem 1.

Problem 1 (1):

In MAS the wide range of accounting system are included in each and every item by

inclined to gain continuous process and objectives. In context of Imperial Brands Plc there all

departments integrated with one another by sharing the cognition and information to one another

to reach at optimum objectives (Arroyo, 2012). They integrate the goals of finance department

with marketing and human resource by aligned their various aspects. For an example in

respective organization by using various reports such as cost accounting reporting, stock reports

they allocate roles and responsibilities to them.

TASK 2

Usage of right kind of tools for evaluation of cost by building income statement.

For an organization to prepare the income statement it is very much necessary to optimize

the different kinds of cost factors which enables to gain important insights and information such

as deliver one of best prices to consumers, to analyse competitors pricing and many more factors.

In context of Imperial Brands Plc, they use various kinds of costs that are as follows:

Absorption costing:

Respective kind of cost helps to organization by using various kind of technique by

relating the fixed and non-fixed kind of cost to prepare financial statements by examine every

factor associated with the firm. In context of Imperial Brands Plc, they by using idea both fixed

and non-fixed cost related to their project to bring it into practice.

Marginal costing:

In marginal costing the organization use the both fixed cost by relating the periodical

units of cost in order for gaining potential outcomes. In context of Imperial Brands by using the

Marginal costing system they evaluate both fixed and non-fixed cost by demonstrating various

factors (Maas, Schaltegger and Crutzen, 2016).

Problem 1.

Problem 1 (1):

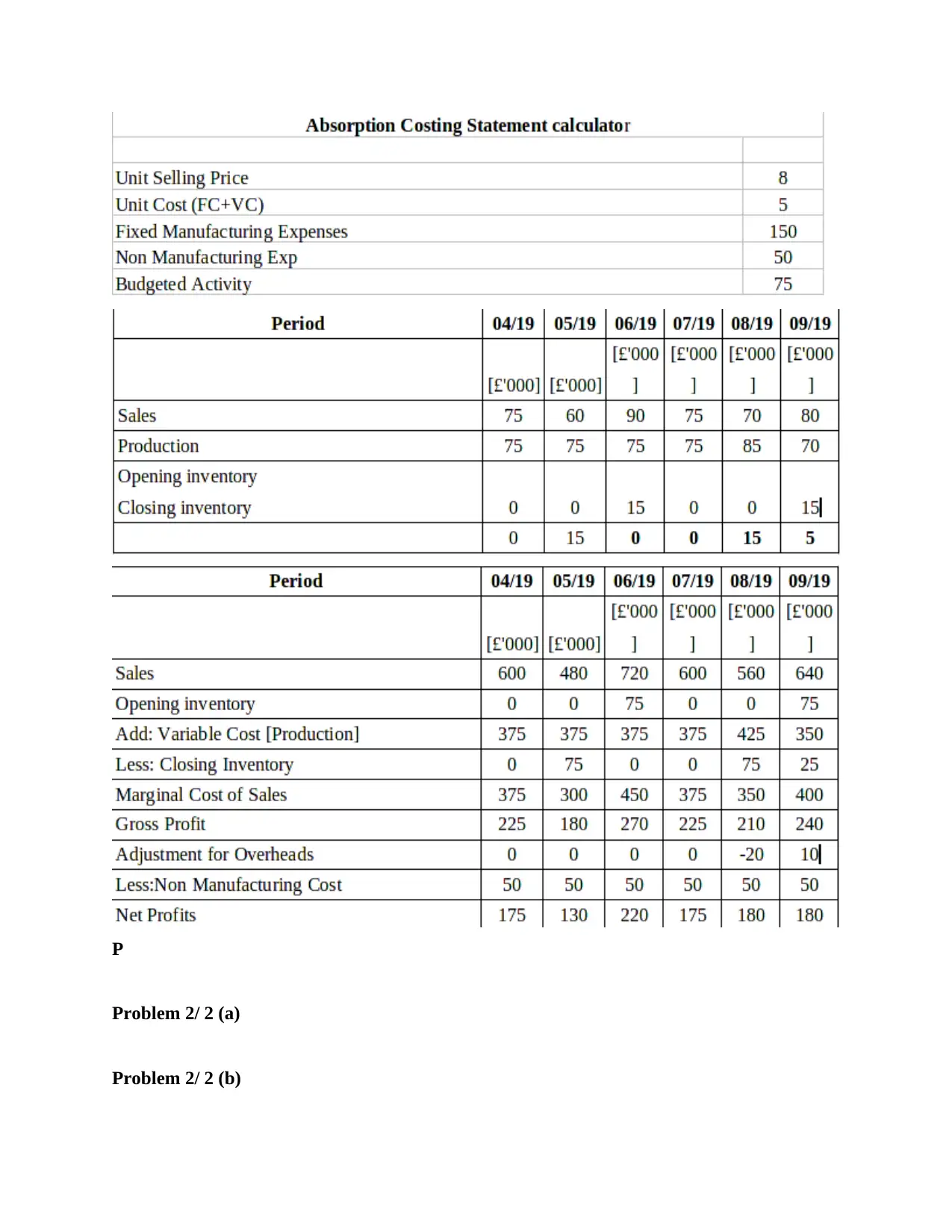

Problem 1 (2):

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

P

Problem 2/ 2 (a)

Problem 2/ 2 (b)

Problem 2/ 2 (a)

Problem 2/ 2 (b)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

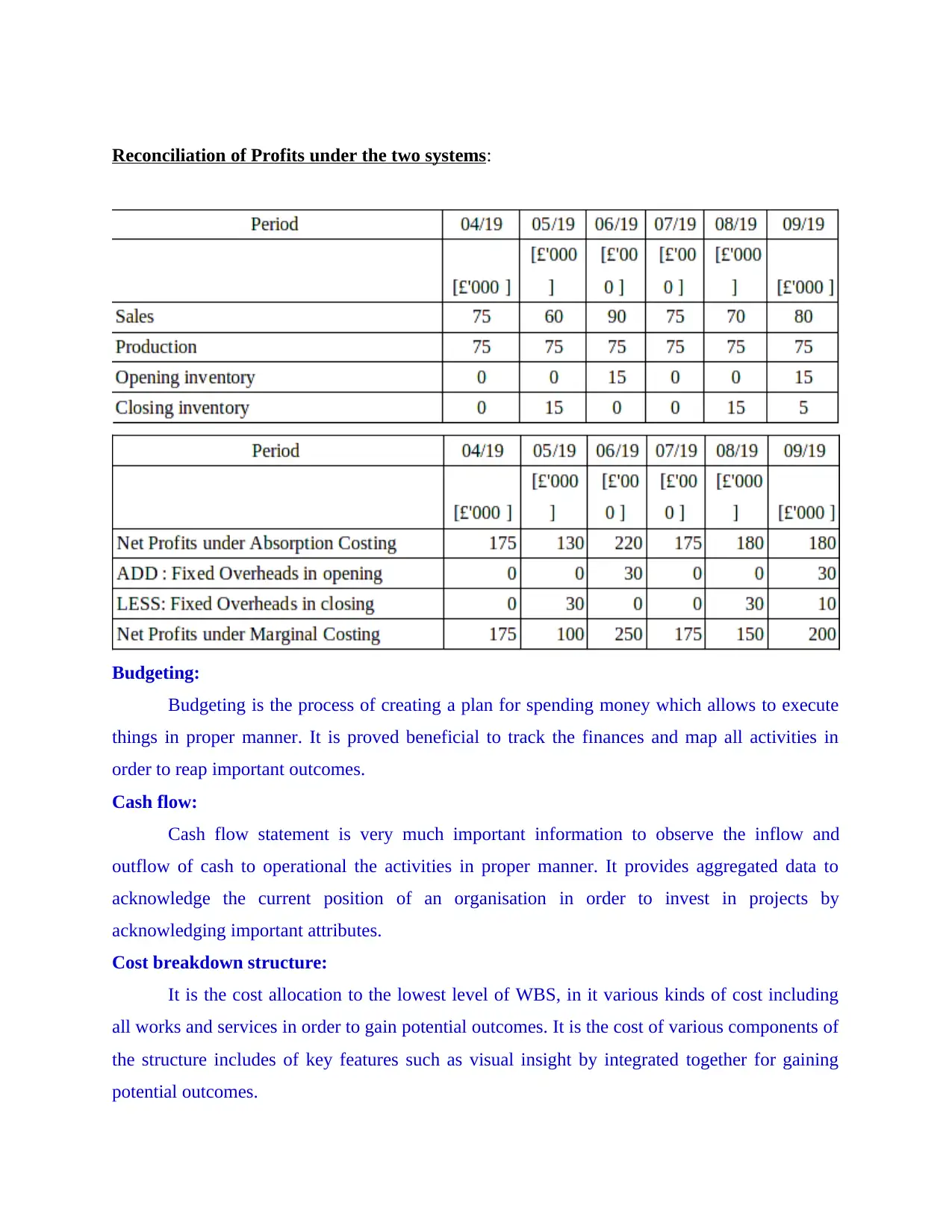

Reconciliation of Profits under the two systems:

Budgeting:

Budgeting is the process of creating a plan for spending money which allows to execute

things in proper manner. It is proved beneficial to track the finances and map all activities in

order to reap important outcomes.

Cash flow:

Cash flow statement is very much important information to observe the inflow and

outflow of cash to operational the activities in proper manner. It provides aggregated data to

acknowledge the current position of an organisation in order to invest in projects by

acknowledging important attributes.

Cost breakdown structure:

It is the cost allocation to the lowest level of WBS, in it various kinds of cost including

all works and services in order to gain potential outcomes. It is the cost of various components of

the structure includes of key features such as visual insight by integrated together for gaining

potential outcomes.

Budgeting:

Budgeting is the process of creating a plan for spending money which allows to execute

things in proper manner. It is proved beneficial to track the finances and map all activities in

order to reap important outcomes.

Cash flow:

Cash flow statement is very much important information to observe the inflow and

outflow of cash to operational the activities in proper manner. It provides aggregated data to

acknowledge the current position of an organisation in order to invest in projects by

acknowledging important attributes.

Cost breakdown structure:

It is the cost allocation to the lowest level of WBS, in it various kinds of cost including

all works and services in order to gain potential outcomes. It is the cost of various components of

the structure includes of key features such as visual insight by integrated together for gaining

potential outcomes.

Usage of MA techniques.

Management accounting tools to build reports in context of an organization. In today’s

scenario the MAR plays very major role in the life of an individual as well as organization to

gain important insights such as financial projections, future plans and policies and concepts to

build one of best strategies to remain always competitive in market place (Shah and et. al., 2011).

The major objective behind preparation of financial reports that it elaborates the internal and

external information to share with the stakeholders to acknowledge the facts and figures which

proved beneficial in decision making. To prepare and gather information there are various kinds

of cost accounting reports proved beneficial such as marginal costing, absorption costing and

other too. In context of chosen organization, they on periodically basis prepare the financial

reports and then share with their both internal and external stakeholders by setting standards and

then compare by it that how far organization near to their goals and objectives.

Except from the above mentioned tools and techniques organization uses other cost

accounting tools to build financial statements such as standard costing, activity based accounting

and zero based accounting which devotes to deliver one of best attributes in life of an individual

as well as organization to provide the basis framework before their stakeholders to demonstrate

crucial outcomes.

By framing financial reports by interpret by various activities.

From above practical, it has been summarized that income statement is very much

important for an organization to shows the financial position and loop falls in order to put one of

best efforts in right direction to co relate with past data and statistics. It has been observed that

from the MC technique the net profit of organization is £555000 and by evaluating the marginal

costing organisations net profit is £781000. There is huge difference in both kinds of financials

data and information and reason behind it that is 226000 organization using various techniques.

Communication Matrix:

Communication Purpose Medium frequency Audience

Project team

meetings

Review status of

a project

Face to face or

conference call

Weekly Project team

Technical and To discuss and In person or face As needed Technical team

Management accounting tools to build reports in context of an organization. In today’s

scenario the MAR plays very major role in the life of an individual as well as organization to

gain important insights such as financial projections, future plans and policies and concepts to

build one of best strategies to remain always competitive in market place (Shah and et. al., 2011).

The major objective behind preparation of financial reports that it elaborates the internal and

external information to share with the stakeholders to acknowledge the facts and figures which

proved beneficial in decision making. To prepare and gather information there are various kinds

of cost accounting reports proved beneficial such as marginal costing, absorption costing and

other too. In context of chosen organization, they on periodically basis prepare the financial

reports and then share with their both internal and external stakeholders by setting standards and

then compare by it that how far organization near to their goals and objectives.

Except from the above mentioned tools and techniques organization uses other cost

accounting tools to build financial statements such as standard costing, activity based accounting

and zero based accounting which devotes to deliver one of best attributes in life of an individual

as well as organization to provide the basis framework before their stakeholders to demonstrate

crucial outcomes.

By framing financial reports by interpret by various activities.

From above practical, it has been summarized that income statement is very much

important for an organization to shows the financial position and loop falls in order to put one of

best efforts in right direction to co relate with past data and statistics. It has been observed that

from the MC technique the net profit of organization is £555000 and by evaluating the marginal

costing organisations net profit is £781000. There is huge difference in both kinds of financials

data and information and reason behind it that is 226000 organization using various techniques.

Communication Matrix:

Communication Purpose Medium frequency Audience

Project team

meetings

Review status of

a project

Face to face or

conference call

Weekly Project team

Technical and To discuss and In person or face As needed Technical team

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.