Financial Decision Making: Ratio Analysis and Performance Evaluation

VerifiedAdded on 2022/12/02

|14

|4307

|469

Report

AI Summary

This report provides a comprehensive analysis of financial decision-making, focusing on SKANSKA PLC. It begins with an introduction to the company and its operations, followed by an in-depth exploration of management accounting techniques, including financial planning, financial statement analysis, cost accounting, cash flow analysis, decision-making processes, budgetary control, and marginal costing. A critical analysis of these techniques is also presented, evaluating their impact on planning, controlling, and decision-making within the company, along with their limitations. The second part of the report delves into the calculation and interpretation of various financial ratios, such as Return on Capital Employed (ROCE), net profit margin, current ratio, debtor collection period, and creditor collection period, for the years 2018 and 2019. The analysis compares these ratios to assess SKANSKA PLC's financial performance, offering insights into its efficiency, profitability, and potential areas for improvement, with recommendations based on the findings.

FINNACIAL DECISION

MAKING

MAKING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

TASK-1............................................................................................................................................3

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Management accounting techniques............................................................................................3

Critical analysis...........................................................................................................................5

TASK-2............................................................................................................................................7

Calculation of ratios.....................................................................................................................7

Analysis of the performance of SKANSKA PLC.......................................................................8

CONCLUSION AND RECOMMENDATION............................................................................12

REFERENCES................................................................................................................................1

TASK-1............................................................................................................................................3

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Management accounting techniques............................................................................................3

Critical analysis...........................................................................................................................5

TASK-2............................................................................................................................................7

Calculation of ratios.....................................................................................................................7

Analysis of the performance of SKANSKA PLC.......................................................................8

CONCLUSION AND RECOMMENDATION............................................................................12

REFERENCES................................................................................................................................1

TASK-1

INTRODUCTION

SKANSKA PLC is one of the famous and well known construction company of the entire

world including UK. It performs and execute various famous construction projects across the

globe. It was founded in 1984. It renders its services in many countries including Poland,

Romania, Nordic region, Hungary, Slovakia and many more. The current number of employees

are 32463. The revenue share of the company is SEK 158.6 bn (Skanska in brief, 2021). It is

counted as top construction company of the UK which is famous for its timely constructed

projects.

In every company including SKANSKA PLC accounting and finance functions plays an

important role. Accounting function would enable the company to have a recording of all the

financial transactions along with preparing of financial statement. Likewise, finance function

also assist the company to have an adequate availability of finance in the company so that its

business operation would not be suffer due to shortage of funds (Cockcroft and Russell, 2018).

Along with recording and preparation of financial statements, accounting also enable the

company to have an analysis of its own financial and business performance. These functions are

considered as a base on which financial decisions of the company are made.

This report will discuss about the concept of management accounting which is also an

important concept and part of accounting system. An analysis of the various management

accounting techniques along with their implication and role with regard to the company’s

decision making, controlling, and planning is also presented in the report. Lastly, a critical

evaluation of implementation of management accounting and the concerned techniques are also

included in the report.

However, the second part of the report is all related with the calculation of ratios including

current ratio, ROCE, Net profit, debtor and creditor collection period along with their

interpretation. This part also followed up by recommendation on the basis of analysis of financial

performance.

MAIN BODY

Management accounting techniques

Management accounting:

INTRODUCTION

SKANSKA PLC is one of the famous and well known construction company of the entire

world including UK. It performs and execute various famous construction projects across the

globe. It was founded in 1984. It renders its services in many countries including Poland,

Romania, Nordic region, Hungary, Slovakia and many more. The current number of employees

are 32463. The revenue share of the company is SEK 158.6 bn (Skanska in brief, 2021). It is

counted as top construction company of the UK which is famous for its timely constructed

projects.

In every company including SKANSKA PLC accounting and finance functions plays an

important role. Accounting function would enable the company to have a recording of all the

financial transactions along with preparing of financial statement. Likewise, finance function

also assist the company to have an adequate availability of finance in the company so that its

business operation would not be suffer due to shortage of funds (Cockcroft and Russell, 2018).

Along with recording and preparation of financial statements, accounting also enable the

company to have an analysis of its own financial and business performance. These functions are

considered as a base on which financial decisions of the company are made.

This report will discuss about the concept of management accounting which is also an

important concept and part of accounting system. An analysis of the various management

accounting techniques along with their implication and role with regard to the company’s

decision making, controlling, and planning is also presented in the report. Lastly, a critical

evaluation of implementation of management accounting and the concerned techniques are also

included in the report.

However, the second part of the report is all related with the calculation of ratios including

current ratio, ROCE, Net profit, debtor and creditor collection period along with their

interpretation. This part also followed up by recommendation on the basis of analysis of financial

performance.

MAIN BODY

Management accounting techniques

Management accounting:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It is an important part of the accounting system that is concerned with the management

and used for the internal purpose. As it is comprised of two words that includes management and

accounting which clearly define its meaning that the accounting that is being used by the

management of the company is known as management accounting (Abdusalomova, 2019). It is

mainly used for the internal purpose and for decision making.

Techniques:

Financial planning:

It is the first and the important technique and tool concerning with managerial

accounting. Since the main objective of every company is to raise and generate profits so by

assisting the financial planning management accounting enable the SKANSKA PLC to grab its

objectives (Ameen, Ahmed and Abd Hafez, 2018).

Analysis of financial statement:

Profit and loss, cash flow statement, balance sheet are counted as an important financial

statement of the company. Analysis of these statement and taking decisions accordingly would

enable the company to raise their financial and company’s performance (Robinson, 2020). This

will assist the SKANSKA PLC towards the growth. As for example SKANSKA PLC also

prepares its financial statement at the end of the years so that the managers of the company will

take the adequate and appropriate decision in respect of the company in terms of betterment.

Likewise, as per the analysis of the financial statement of SKANSKA PLC if managers found

that any activity is leading loss then they take adequate and appropriate steps.

Cost accounting:

It is also an important tool and technique of the management accounting on the basis of

which management will determine best decision with respect to company. As per this technique

both the historical and standard costing is to be included. Historical costing refers to the cost that

is associated with the company’s product or the service (Pagare, 2020). However, standard cost

refers to the estimated cost on the basis of experiments and historical cost. By having a

comparison of the actual incurred cost with the standard cost, management can determine the

cause and take the adequate decision of improvement with regard to any deviation of cost in

concern with SKANSKA PLC.

Cash flow analysis:

and used for the internal purpose. As it is comprised of two words that includes management and

accounting which clearly define its meaning that the accounting that is being used by the

management of the company is known as management accounting (Abdusalomova, 2019). It is

mainly used for the internal purpose and for decision making.

Techniques:

Financial planning:

It is the first and the important technique and tool concerning with managerial

accounting. Since the main objective of every company is to raise and generate profits so by

assisting the financial planning management accounting enable the SKANSKA PLC to grab its

objectives (Ameen, Ahmed and Abd Hafez, 2018).

Analysis of financial statement:

Profit and loss, cash flow statement, balance sheet are counted as an important financial

statement of the company. Analysis of these statement and taking decisions accordingly would

enable the company to raise their financial and company’s performance (Robinson, 2020). This

will assist the SKANSKA PLC towards the growth. As for example SKANSKA PLC also

prepares its financial statement at the end of the years so that the managers of the company will

take the adequate and appropriate decision in respect of the company in terms of betterment.

Likewise, as per the analysis of the financial statement of SKANSKA PLC if managers found

that any activity is leading loss then they take adequate and appropriate steps.

Cost accounting:

It is also an important tool and technique of the management accounting on the basis of

which management will determine best decision with respect to company. As per this technique

both the historical and standard costing is to be included. Historical costing refers to the cost that

is associated with the company’s product or the service (Pagare, 2020). However, standard cost

refers to the estimated cost on the basis of experiments and historical cost. By having a

comparison of the actual incurred cost with the standard cost, management can determine the

cause and take the adequate decision of improvement with regard to any deviation of cost in

concern with SKANSKA PLC.

Cash flow analysis:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Under this analysis management can take the decision with respect to cash. As this

statement enable the company to have to an analysis of the movement of cash that in and out

from the company (Soboleva and et.al., 2018). This statement also enables the management to

determine and implement the best practice so that the cash will be management by the

SKANSKA PLC.

Decision making:

As the occurrence of problems with regard to the business is quite common but

determination of the best solution with regard to the business and the problem is associated with

the management accounting (Weygandt and et.al., 2018). With the help of decision making

approach and the technique the best decision with regard to the SKANSKA PLC’s betterment is

to be taken by the management.

Budgetary control:

It is also an important and beneficial technique associated with the management

accounting of SKANSKA PLC. As per this technique and estimated budgets concerning the

expected income and expenses are to be made and prepared (Mohd Ali, 2021). After that the

actual performance of the company is being measured and analysed again the budgeted

statement. Occurrence of any deviation would be corrected by taking adequate decisions and

implementing adequate technique so that the loopholes will be corrected.

Marginal costing:

It is also an important technique related with management accounting. As per this

technique sales prices with regard to the products are to be determined by keeping an adequate

share of profit for the company (Nan, 2019). Here determination of selling prices is to be done

by keeping an adequate margin for the SKANSKA PLC’s operating cost and profit share.

Critical analysis

From the above techniques concerning the management accounting it can be analysed that

it plays an important role with regard to planning, controlling and decision making. Since plans

refers to a roadmap that guides the company towards the direction of its objectives. So by having

an analysis of the financial statement and making of financial plans the company including the

SKANSKA PLC can determine their future plan. along with determination of plan it will also

assist the company to grab their objective with regard to growth and development. Likewise, by

statement enable the company to have to an analysis of the movement of cash that in and out

from the company (Soboleva and et.al., 2018). This statement also enables the management to

determine and implement the best practice so that the cash will be management by the

SKANSKA PLC.

Decision making:

As the occurrence of problems with regard to the business is quite common but

determination of the best solution with regard to the business and the problem is associated with

the management accounting (Weygandt and et.al., 2018). With the help of decision making

approach and the technique the best decision with regard to the SKANSKA PLC’s betterment is

to be taken by the management.

Budgetary control:

It is also an important and beneficial technique associated with the management

accounting of SKANSKA PLC. As per this technique and estimated budgets concerning the

expected income and expenses are to be made and prepared (Mohd Ali, 2021). After that the

actual performance of the company is being measured and analysed again the budgeted

statement. Occurrence of any deviation would be corrected by taking adequate decisions and

implementing adequate technique so that the loopholes will be corrected.

Marginal costing:

It is also an important technique related with management accounting. As per this

technique sales prices with regard to the products are to be determined by keeping an adequate

share of profit for the company (Nan, 2019). Here determination of selling prices is to be done

by keeping an adequate margin for the SKANSKA PLC’s operating cost and profit share.

Critical analysis

From the above techniques concerning the management accounting it can be analysed that

it plays an important role with regard to planning, controlling and decision making. Since plans

refers to a roadmap that guides the company towards the direction of its objectives. So by having

an analysis of the financial statement and making of financial plans the company including the

SKANSKA PLC can determine their future plan. along with determination of plan it will also

assist the company to grab their objective with regard to growth and development. Likewise, by

implementing the practice of standard costing, budgetary control SKANSKA PLC can easily

control the functioning of its business operation and direct it towards the way of raising

efficiency. These techniques will not only lead the company to monitor and control their

operation but at the same time it will also enable the company to take the most corrective actions

so that the loopholes and the deviation in the current business practices can be recovered and

minimised (Jiambalvo, 2019). As it is to be noted that the management accounting is also related

with the decision making accounting, marginal costing so the best decision with respect to the

solving of business issues and the setting up of the best selling prices can be easily taken by the

company. Thus, it would not be wrong to said that an implementation of the management

accounting and its concerned techniques and concepts would lead to rise the performance of the

SKANSKA PLC and its business.

However, on a critical note it is being analysed that performance and implementation of

the management accounting concepts and techniques requires an adequate degree of time and

money. This means although it benefits the business of the SKANSKA PLC but at the same time

its implication requires time and money, which indicate that its application is not suitable for the

emergency situation and for the normal expenditure bearing companies. Likewise, as under this

accounting the entire decision making power is in the hands of the managers of the company so

occurrence of any personal biasness may put a major impact over the company and the

concerned decisions (Davis and Davis, 2019). It is also be noted that as the management

accounting is concerned with the reference of past data and the historical data which is not

mandatory and required that it would be equally applicable in the present and the future

decisions. This means a rigidness towards the decision-making approach of the management may

sometime bring negative impact towards the SKANSKA PLC in terms of affecting its business.

Thus, from the above critical analysis regarding the management accounting and its

techniques it would not be wrong to said that the application of the management accounting and

its concepts would lead to adequate planning, controlling and decision making of the company

but at the same time its implementation may also include certain limitations in the form of

personal biasness, past preference of information and many more.

control the functioning of its business operation and direct it towards the way of raising

efficiency. These techniques will not only lead the company to monitor and control their

operation but at the same time it will also enable the company to take the most corrective actions

so that the loopholes and the deviation in the current business practices can be recovered and

minimised (Jiambalvo, 2019). As it is to be noted that the management accounting is also related

with the decision making accounting, marginal costing so the best decision with respect to the

solving of business issues and the setting up of the best selling prices can be easily taken by the

company. Thus, it would not be wrong to said that an implementation of the management

accounting and its concerned techniques and concepts would lead to rise the performance of the

SKANSKA PLC and its business.

However, on a critical note it is being analysed that performance and implementation of

the management accounting concepts and techniques requires an adequate degree of time and

money. This means although it benefits the business of the SKANSKA PLC but at the same time

its implication requires time and money, which indicate that its application is not suitable for the

emergency situation and for the normal expenditure bearing companies. Likewise, as under this

accounting the entire decision making power is in the hands of the managers of the company so

occurrence of any personal biasness may put a major impact over the company and the

concerned decisions (Davis and Davis, 2019). It is also be noted that as the management

accounting is concerned with the reference of past data and the historical data which is not

mandatory and required that it would be equally applicable in the present and the future

decisions. This means a rigidness towards the decision-making approach of the management may

sometime bring negative impact towards the SKANSKA PLC in terms of affecting its business.

Thus, from the above critical analysis regarding the management accounting and its

techniques it would not be wrong to said that the application of the management accounting and

its concepts would lead to adequate planning, controlling and decision making of the company

but at the same time its implementation may also include certain limitations in the form of

personal biasness, past preference of information and many more.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK-2

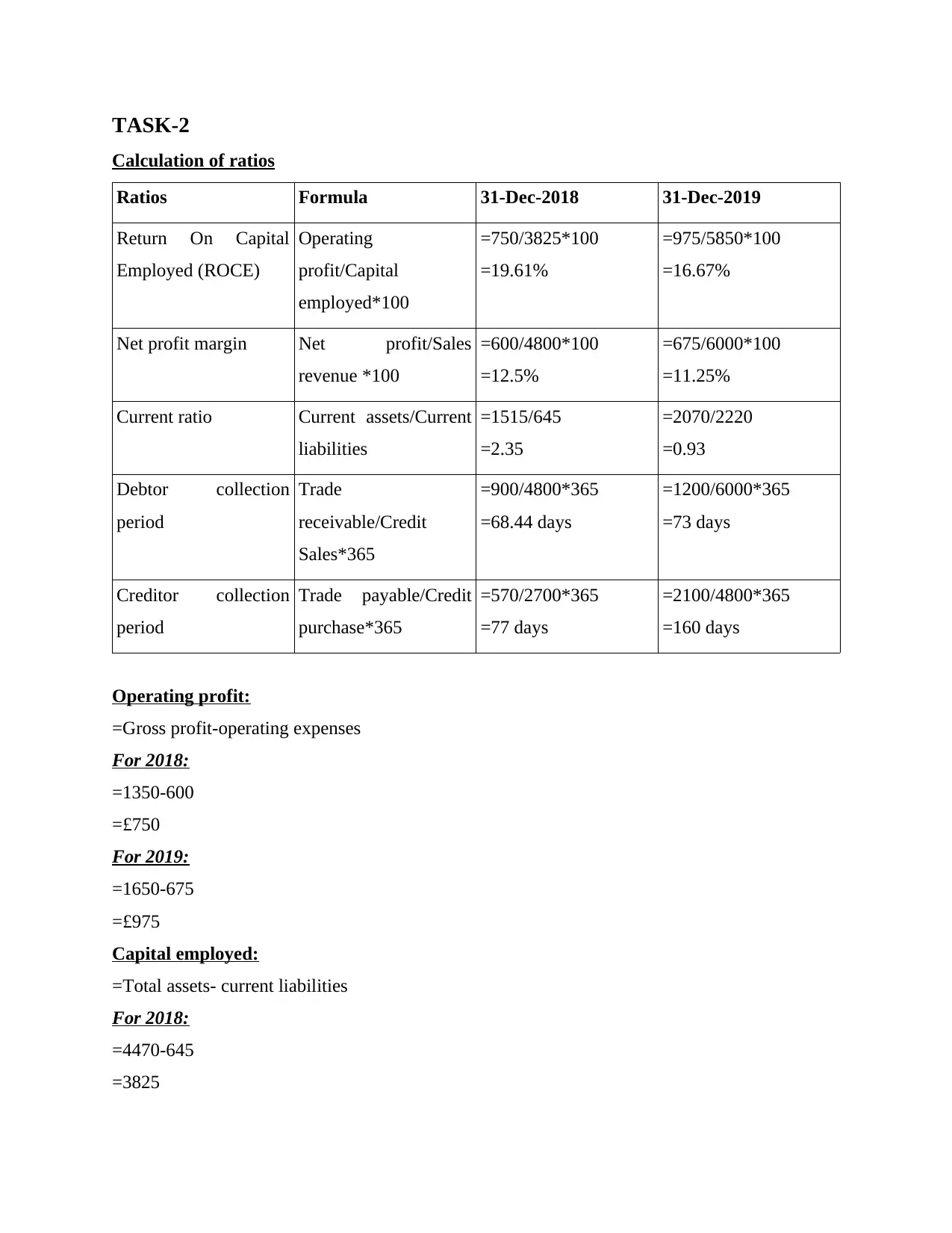

Calculation of ratios

Ratios Formula 31-Dec-2018 31-Dec-2019

Return On Capital

Employed (ROCE)

Operating

profit/Capital

employed*100

=750/3825*100

=19.61%

=975/5850*100

=16.67%

Net profit margin Net profit/Sales

revenue *100

=600/4800*100

=12.5%

=675/6000*100

=11.25%

Current ratio Current assets/Current

liabilities

=1515/645

=2.35

=2070/2220

=0.93

Debtor collection

period

Trade

receivable/Credit

Sales*365

=900/4800*365

=68.44 days

=1200/6000*365

=73 days

Creditor collection

period

Trade payable/Credit

purchase*365

=570/2700*365

=77 days

=2100/4800*365

=160 days

Operating profit:

=Gross profit-operating expenses

For 2018:

=1350-600

=£750

For 2019:

=1650-675

=£975

Capital employed:

=Total assets- current liabilities

For 2018:

=4470-645

=3825

Calculation of ratios

Ratios Formula 31-Dec-2018 31-Dec-2019

Return On Capital

Employed (ROCE)

Operating

profit/Capital

employed*100

=750/3825*100

=19.61%

=975/5850*100

=16.67%

Net profit margin Net profit/Sales

revenue *100

=600/4800*100

=12.5%

=675/6000*100

=11.25%

Current ratio Current assets/Current

liabilities

=1515/645

=2.35

=2070/2220

=0.93

Debtor collection

period

Trade

receivable/Credit

Sales*365

=900/4800*365

=68.44 days

=1200/6000*365

=73 days

Creditor collection

period

Trade payable/Credit

purchase*365

=570/2700*365

=77 days

=2100/4800*365

=160 days

Operating profit:

=Gross profit-operating expenses

For 2018:

=1350-600

=£750

For 2019:

=1650-675

=£975

Capital employed:

=Total assets- current liabilities

For 2018:

=4470-645

=3825

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

For 2019:

=8070-2220

= 5850

Analysis of the performance of SKANSKA PLC

Accounting ratio:

It refers to the ratios that are concerned with the accounting of the company. in other

words in order to have an analysis of the company’s accounting information and financial

information accounting ratios are calculated (Karale, 2020). Here a comparison is made between

the financial statement of two or more than two periods.

Importance:

Calculation of accounting ratio is important for both the company and the concerned

stakeholders. This is because with the analysis of ratio the company’s financial performance is

also analysed and on the basis of which company can determine its efficiency and the concerned

stakeholders including owners, employees, investors and the shareholder can take their decision

with respect to company.

Return on capital employed (ROCE):

It is one of the important ratio concerning with accounting ratio. As per this ratio an

analysis of the return over the capital employed is being determined (Casielles, 2019). In simple

words as per this ratio the company can determined the rate of return which it has earned and

generated over the use of capital.

Importance:

It is an important ratio for the SKANSKA PLC because as per this ratio it can determine

its efficiency and profitability. Since through this ratio the return is being calculated so with the

help of this ratio the SKANSKA PLC can analyse the efficiency of its business operation with

regard to the return percentage.

Comparison:

By having a comparison of the ROCE ratio of the SKANSKA PLC of 2018 and 2019, it

is being analysed that the percentage of ratio is declining from 19.61 to 16.67%. This declining

percentage is a clear indicator of the poor efficiency of the company.

=8070-2220

= 5850

Analysis of the performance of SKANSKA PLC

Accounting ratio:

It refers to the ratios that are concerned with the accounting of the company. in other

words in order to have an analysis of the company’s accounting information and financial

information accounting ratios are calculated (Karale, 2020). Here a comparison is made between

the financial statement of two or more than two periods.

Importance:

Calculation of accounting ratio is important for both the company and the concerned

stakeholders. This is because with the analysis of ratio the company’s financial performance is

also analysed and on the basis of which company can determine its efficiency and the concerned

stakeholders including owners, employees, investors and the shareholder can take their decision

with respect to company.

Return on capital employed (ROCE):

It is one of the important ratio concerning with accounting ratio. As per this ratio an

analysis of the return over the capital employed is being determined (Casielles, 2019). In simple

words as per this ratio the company can determined the rate of return which it has earned and

generated over the use of capital.

Importance:

It is an important ratio for the SKANSKA PLC because as per this ratio it can determine

its efficiency and profitability. Since through this ratio the return is being calculated so with the

help of this ratio the SKANSKA PLC can analyse the efficiency of its business operation with

regard to the return percentage.

Comparison:

By having a comparison of the ROCE ratio of the SKANSKA PLC of 2018 and 2019, it

is being analysed that the percentage of ratio is declining from 19.61 to 16.67%. This declining

percentage is a clear indicator of the poor efficiency of the company.

Cause:

The major cause for the declining ratio is poor utilization of assets. Likewise, as this ratio

is related with the return over capital so a declining ratio also indicate that the company is not

utilising its assets adequately (Lisek, Luty and Zioło, 2020). Similarly, a declining sales

percentage may also bring poor return.

Improvement:

In order to improve this ratio the SKANSKA PLC have to adopt the policy of raising the

sales percentage along with focussing over lowering the cost. Likewise, disposal of the non-

productive and non-useful assets may also assist the company to raise the percentage of the ratio.

Net profit margin:

It refers a ratio that is concerned with the net profit that is being earned by the company

over its total revenue (Rodica, Petre and Simon, 2019). This means that NP ratio is the

percentage of net income or profit over the net revenue that is being earned by the sales.

Importance:

This is an important ratio for the SKANSKA PLC because through this ratio it can

determine the actual percentage of profit that is being earned over the period of time. This ratio

also enables the company to analyse that whether by absorbing its overall cost is it able to

generate the adequate share of profit or not.

Comparison:

From the analysis of the calculation of NP ratio it is said that the NP ratio of SKANSKA

PLC is declining from 12.5 to 11.25% from 2018 to 2019. This means that the company’s ability

with regard to generation of the profit is declining from the past year and as a result of that the

ratio is declining.

Cause:

One of the major cause for the declining ratio is related with the declining the percentage

of sales of the company. As if the company’s sales will decline then it will directly affect the

profit earning capacity of the company (Abeyrathna and Priyadarshana, 2019). Likewise, a poor

pricing strategy of the company along with inadequate cost structure may also lead to decline in

the ratio.

Improvement:

The major cause for the declining ratio is poor utilization of assets. Likewise, as this ratio

is related with the return over capital so a declining ratio also indicate that the company is not

utilising its assets adequately (Lisek, Luty and Zioło, 2020). Similarly, a declining sales

percentage may also bring poor return.

Improvement:

In order to improve this ratio the SKANSKA PLC have to adopt the policy of raising the

sales percentage along with focussing over lowering the cost. Likewise, disposal of the non-

productive and non-useful assets may also assist the company to raise the percentage of the ratio.

Net profit margin:

It refers a ratio that is concerned with the net profit that is being earned by the company

over its total revenue (Rodica, Petre and Simon, 2019). This means that NP ratio is the

percentage of net income or profit over the net revenue that is being earned by the sales.

Importance:

This is an important ratio for the SKANSKA PLC because through this ratio it can

determine the actual percentage of profit that is being earned over the period of time. This ratio

also enables the company to analyse that whether by absorbing its overall cost is it able to

generate the adequate share of profit or not.

Comparison:

From the analysis of the calculation of NP ratio it is said that the NP ratio of SKANSKA

PLC is declining from 12.5 to 11.25% from 2018 to 2019. This means that the company’s ability

with regard to generation of the profit is declining from the past year and as a result of that the

ratio is declining.

Cause:

One of the major cause for the declining ratio is related with the declining the percentage

of sales of the company. As if the company’s sales will decline then it will directly affect the

profit earning capacity of the company (Abeyrathna and Priyadarshana, 2019). Likewise, a poor

pricing strategy of the company along with inadequate cost structure may also lead to decline in

the ratio.

Improvement:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

In order to improve the ratio SKANSKA PLC can adopt the method of reducing the cost

of operation so that the company can save its cost and raise the profit margin. In the same way it

can also work towards the direction of raising the percentage of sales so that with high sales,

profit will raise. Likewise, selling of its projects at high selling price may also bring more profit.

Current ratio:

The another name of this ratio is liquidity ratio. As per this ratio the company’s liquidity

position can be analysed and measured (ANGADI, 2020). It is the ratio of current asset to current

liabilities. The ideal ratio is 2:1.

Importance:

It is an important ratio for the SKANSKA PLC because through this ratio it can

determine its liquidity position and thereby analyse that whether it is able to pay its short term

debts and obligations or not. This means that with the help of current ratio, investors can also

determine that whether the company is in the position of repaying its short term debts or not.

Comparison:

By having a comparison of the current ratio of 2018 and 2019 of SKANSKA PLC it is

analysed that the current ratio is declining from 2.35 to 0.93. This declining ratio directly means

that the company is not efficient in terms of making repayment of its short term obligations and

current liabilities.

Causes:

Over-accumulation of current liabilities due to non-payment, shortage of cash, shortage

of funds, non-capacity of the company, following the practice of late payment and various other

are considered as a major reason of the declining percentage of current ratio (Chasanah and

Sucipto, 2019).

Improvement:

However, it can be improved with the adoption of faster conversion cycle in which faster

recovers from debtors may lead to raising of current assets. Likewise, paying off current

liabilities, selling of non-useful assets are all such methods that can improve the current ratio.

Debtor collection period:

It refers to a period that is concerned with the time which is required by the company in

order to collect the due debts from the market (Mithare, 2020). In simple words it is the period

concerning with the collection of due amount of debtors.

of operation so that the company can save its cost and raise the profit margin. In the same way it

can also work towards the direction of raising the percentage of sales so that with high sales,

profit will raise. Likewise, selling of its projects at high selling price may also bring more profit.

Current ratio:

The another name of this ratio is liquidity ratio. As per this ratio the company’s liquidity

position can be analysed and measured (ANGADI, 2020). It is the ratio of current asset to current

liabilities. The ideal ratio is 2:1.

Importance:

It is an important ratio for the SKANSKA PLC because through this ratio it can

determine its liquidity position and thereby analyse that whether it is able to pay its short term

debts and obligations or not. This means that with the help of current ratio, investors can also

determine that whether the company is in the position of repaying its short term debts or not.

Comparison:

By having a comparison of the current ratio of 2018 and 2019 of SKANSKA PLC it is

analysed that the current ratio is declining from 2.35 to 0.93. This declining ratio directly means

that the company is not efficient in terms of making repayment of its short term obligations and

current liabilities.

Causes:

Over-accumulation of current liabilities due to non-payment, shortage of cash, shortage

of funds, non-capacity of the company, following the practice of late payment and various other

are considered as a major reason of the declining percentage of current ratio (Chasanah and

Sucipto, 2019).

Improvement:

However, it can be improved with the adoption of faster conversion cycle in which faster

recovers from debtors may lead to raising of current assets. Likewise, paying off current

liabilities, selling of non-useful assets are all such methods that can improve the current ratio.

Debtor collection period:

It refers to a period that is concerned with the time which is required by the company in

order to collect the due debts from the market (Mithare, 2020). In simple words it is the period

concerning with the collection of due amount of debtors.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Importance:

This is an important ratio for the SKANSKA PLC because through this ratio it can

determine the actual time which is being required in order to collect the due amount from

debtors. It will also enable the company to not have shortage of funds because of the timely

collection of debts.

Comparison:

By having an analysis of the debtor collection period with regard to SKANSKA PLC of

2018 and 2019 it is found that the period is increasing from 68 to 73 days. Though. It is a short

increase but it is an indicator of the poor company’s policy with regard to debtors.

Cause:

Non-payment of debtors on time, carelessness of company with regard to due collection,

poor collection policy. Are all counted as a reason of high debtor collection period. Availing

sales of projects more on credit basis is also a major cause of high ratio.

Improvement:

In order to improve the ratio the company can adopt the policy of giving rewards and

discounts on timely repayment. Likewise, adoption of the policy of flexible repayment, low

focus over the credit sales may also improve the ratio.

Creditors collection period:

It is concerned with the period that is related with the payment of creditors by the

company. Since, no business can survive without the credit, so with the help of this ratio an

analysis of the credit period taken by the company is determined (Kenton, 2019).

Important:

More lower the ratio more brighter the image of the company would be. This is because

if the company will make timely repayment to its creditors then it can anytime avail credit from

the market. Likewise, its image in the market may also improve if the period would be low.

Comparison:

By comparing the creditor collection period of SKANSKA PLC of 2018 and 2019, it is

analysed that the credit period is raised from 77 to 160 days, which is a very high rise. This

raising period clearly denotes that the company’s credit policy in terms of repayment is not good.

Cause:

This is an important ratio for the SKANSKA PLC because through this ratio it can

determine the actual time which is being required in order to collect the due amount from

debtors. It will also enable the company to not have shortage of funds because of the timely

collection of debts.

Comparison:

By having an analysis of the debtor collection period with regard to SKANSKA PLC of

2018 and 2019 it is found that the period is increasing from 68 to 73 days. Though. It is a short

increase but it is an indicator of the poor company’s policy with regard to debtors.

Cause:

Non-payment of debtors on time, carelessness of company with regard to due collection,

poor collection policy. Are all counted as a reason of high debtor collection period. Availing

sales of projects more on credit basis is also a major cause of high ratio.

Improvement:

In order to improve the ratio the company can adopt the policy of giving rewards and

discounts on timely repayment. Likewise, adoption of the policy of flexible repayment, low

focus over the credit sales may also improve the ratio.

Creditors collection period:

It is concerned with the period that is related with the payment of creditors by the

company. Since, no business can survive without the credit, so with the help of this ratio an

analysis of the credit period taken by the company is determined (Kenton, 2019).

Important:

More lower the ratio more brighter the image of the company would be. This is because

if the company will make timely repayment to its creditors then it can anytime avail credit from

the market. Likewise, its image in the market may also improve if the period would be low.

Comparison:

By comparing the creditor collection period of SKANSKA PLC of 2018 and 2019, it is

analysed that the credit period is raised from 77 to 160 days, which is a very high rise. This

raising period clearly denotes that the company’s credit policy in terms of repayment is not good.

Cause:

The main cause of the high credit period includes shortage of funds with the company

with regard to repayment. Poor strategies of the company with regard to credit repayment. Delay

payment policy may also be counted as a cause.

Improvement:

It can be improved if the company will make negotiation with the suppliers at the time of

the assignment so that it can make payment on time. Adoption of automatic credit payment up-

dation policy, timely repayment of creditors, are some of the methods of improvement.

CONCLUSION AND RECOMMENDATION

From the task-1 of above report it is concluded that the management accounting plays an

important role in the functioning of the company including the SKANSKA PLC. It enables the

company to take the adequate decisions along with establishing controlling measures.

Management accounting and its implication of techniques will lead the company towards the

direction of success and growth. From the report it is also understood that management

accounting is solely used and concerned for the purpose of internal use and by the management

of the company. it enables them to take the most suitable and adequate decisions for the

company and for raising the performance of business operation of the company. Likewise, it is

also understood that management accounting also plays an important role in the financial

decision making by the investors because as it is concerned with enhancing the company’s

performance and efficiency will directly attract the investors to take the decision regarding

making of investment in the company.

From the task-2 concerning calculation and the analysis of the above ratio it is concluded

that the financial performance of the company is declining while having a comparison from 2018

to 2019. Major ratios including the profit ratio, return on capital employed ratio, current ratio are

showing a declining stage. This means that the company performance with regard to its efficient

operation of business is not good. Likewise, a raise in the debtors and creditors collection period

also shows that the company is facing a situation of shortage of funds and is not in the condition

of making repayment to its creditors. Thus, it would be recommended that making an investment

in the company is not said to be a right decision from the investor’s perspective because of the

poor and declining financial performance of the SKANSKA PLC.

with regard to repayment. Poor strategies of the company with regard to credit repayment. Delay

payment policy may also be counted as a cause.

Improvement:

It can be improved if the company will make negotiation with the suppliers at the time of

the assignment so that it can make payment on time. Adoption of automatic credit payment up-

dation policy, timely repayment of creditors, are some of the methods of improvement.

CONCLUSION AND RECOMMENDATION

From the task-1 of above report it is concluded that the management accounting plays an

important role in the functioning of the company including the SKANSKA PLC. It enables the

company to take the adequate decisions along with establishing controlling measures.

Management accounting and its implication of techniques will lead the company towards the

direction of success and growth. From the report it is also understood that management

accounting is solely used and concerned for the purpose of internal use and by the management

of the company. it enables them to take the most suitable and adequate decisions for the

company and for raising the performance of business operation of the company. Likewise, it is

also understood that management accounting also plays an important role in the financial

decision making by the investors because as it is concerned with enhancing the company’s

performance and efficiency will directly attract the investors to take the decision regarding

making of investment in the company.

From the task-2 concerning calculation and the analysis of the above ratio it is concluded

that the financial performance of the company is declining while having a comparison from 2018

to 2019. Major ratios including the profit ratio, return on capital employed ratio, current ratio are

showing a declining stage. This means that the company performance with regard to its efficient

operation of business is not good. Likewise, a raise in the debtors and creditors collection period

also shows that the company is facing a situation of shortage of funds and is not in the condition

of making repayment to its creditors. Thus, it would be recommended that making an investment

in the company is not said to be a right decision from the investor’s perspective because of the

poor and declining financial performance of the SKANSKA PLC.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.