Management Accounting: Comparing Costing Systems for Sewing Easy Ltd

VerifiedAdded on 2021/05/31

|8

|1259

|43

Report

AI Summary

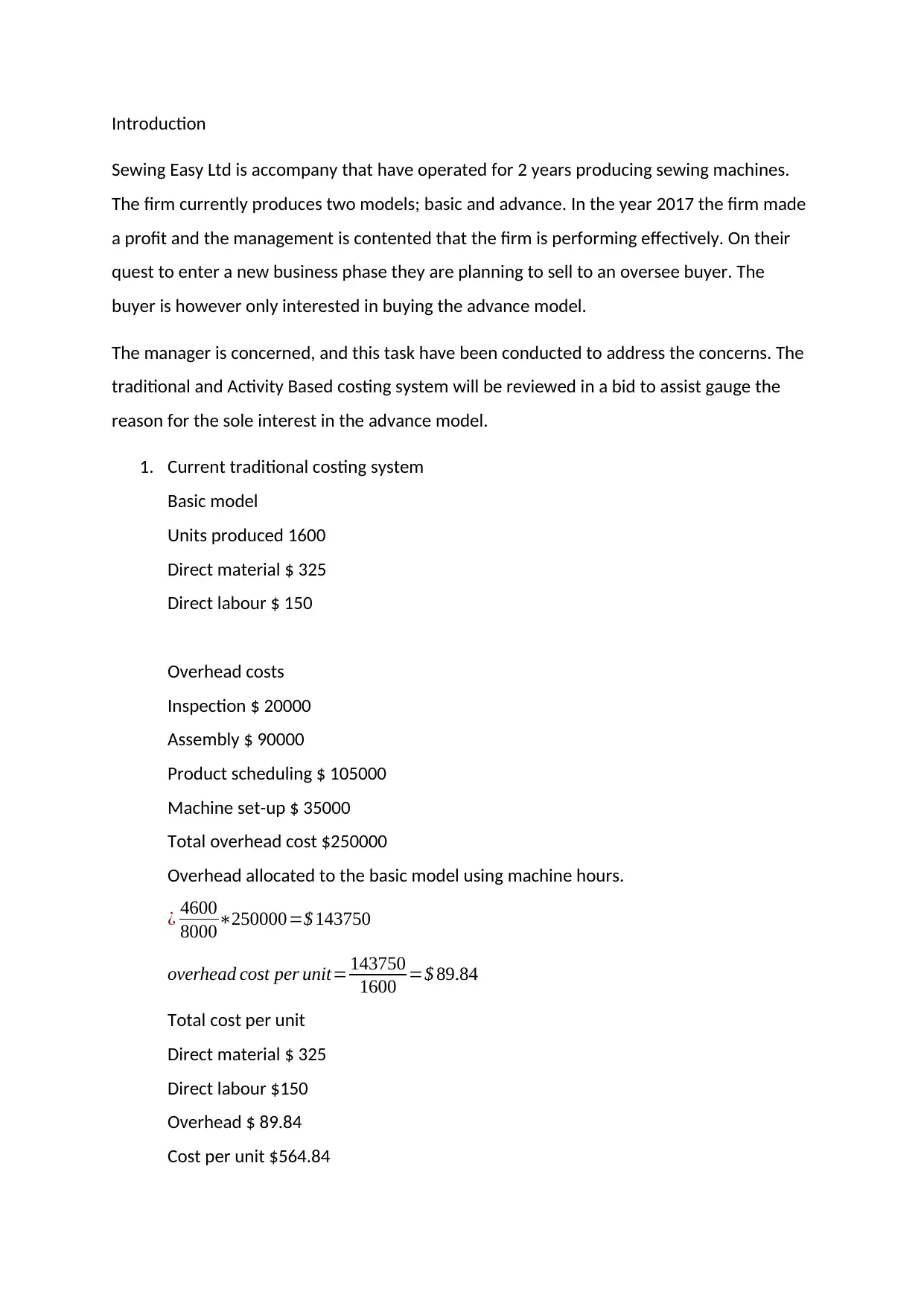

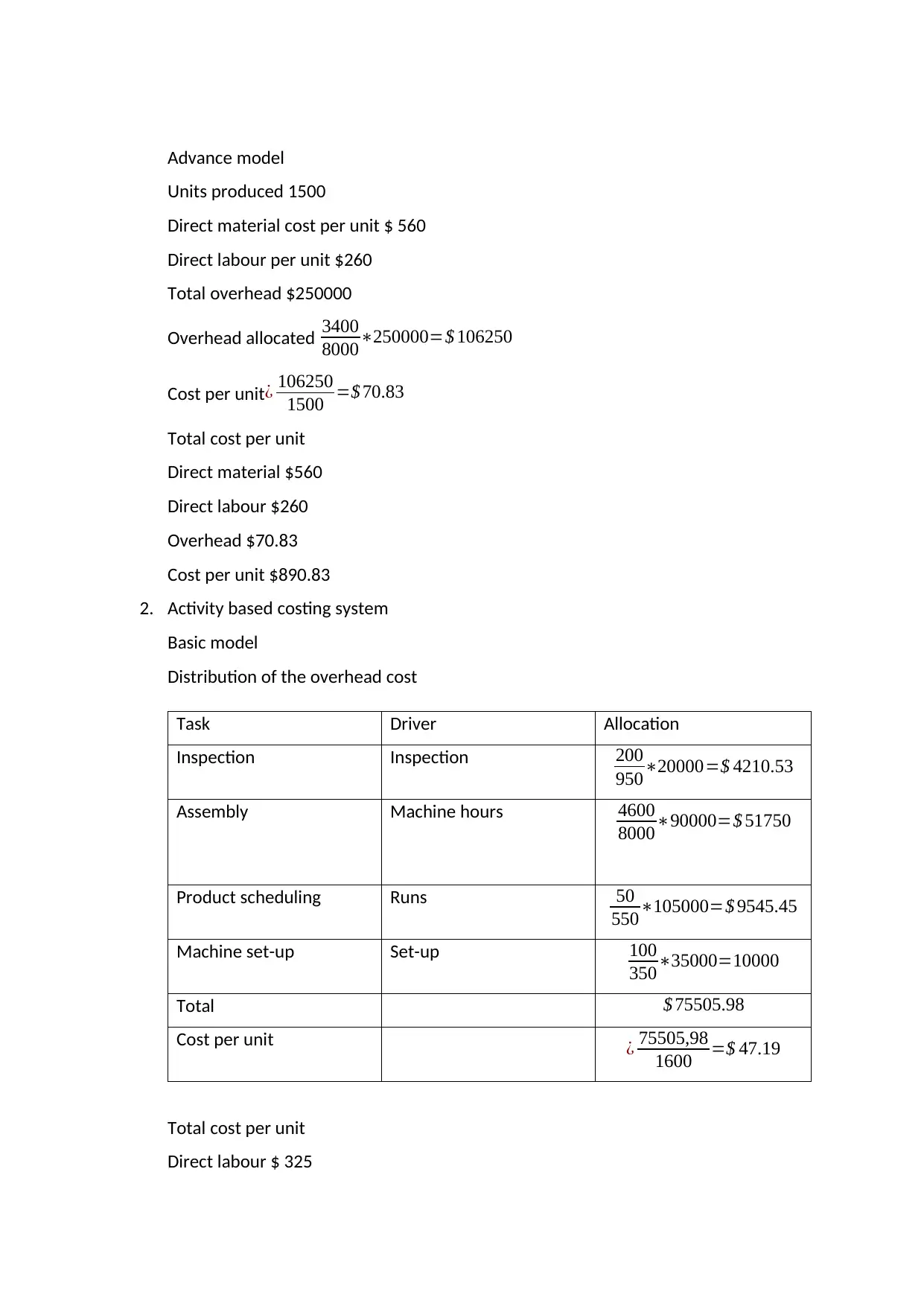

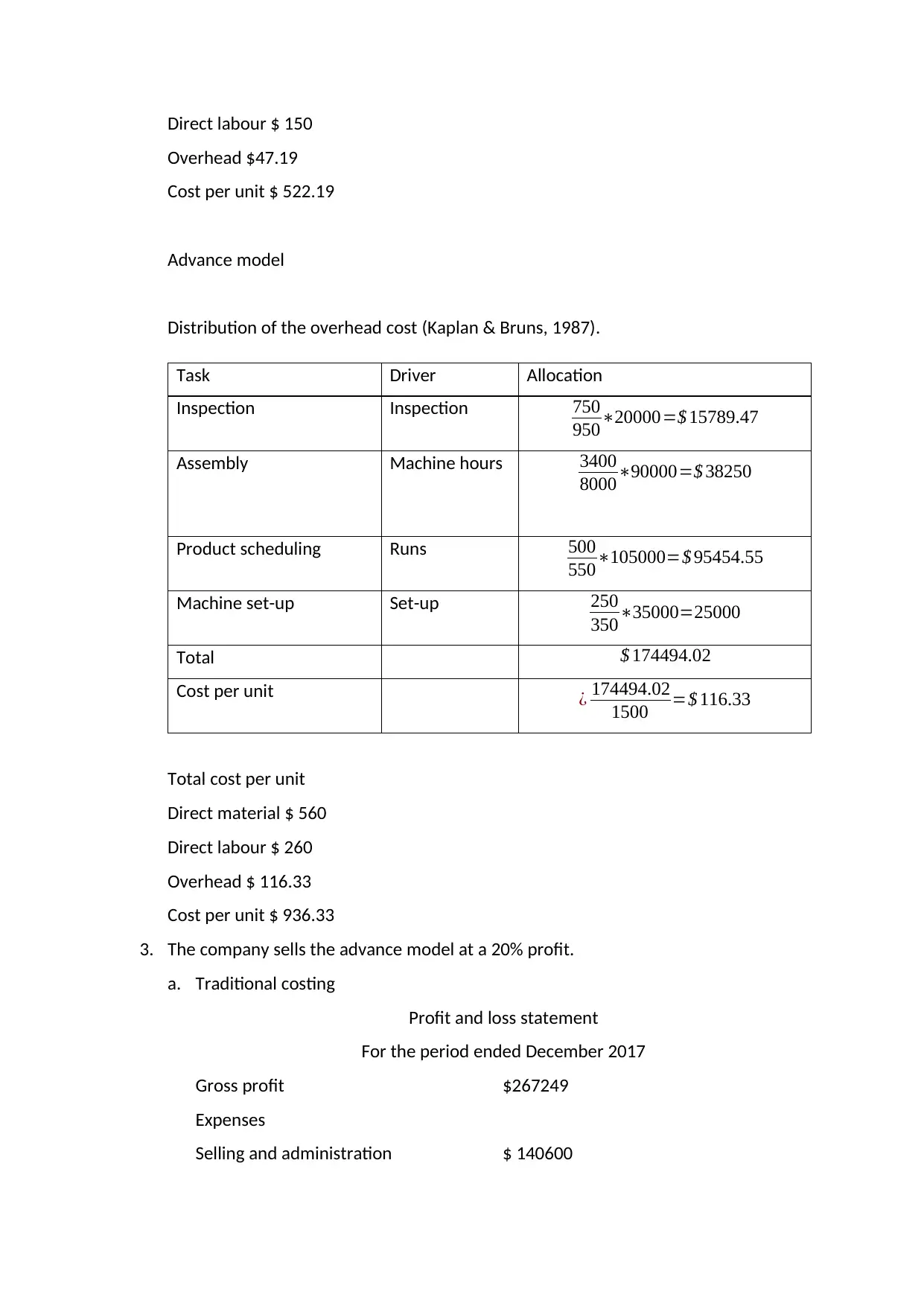

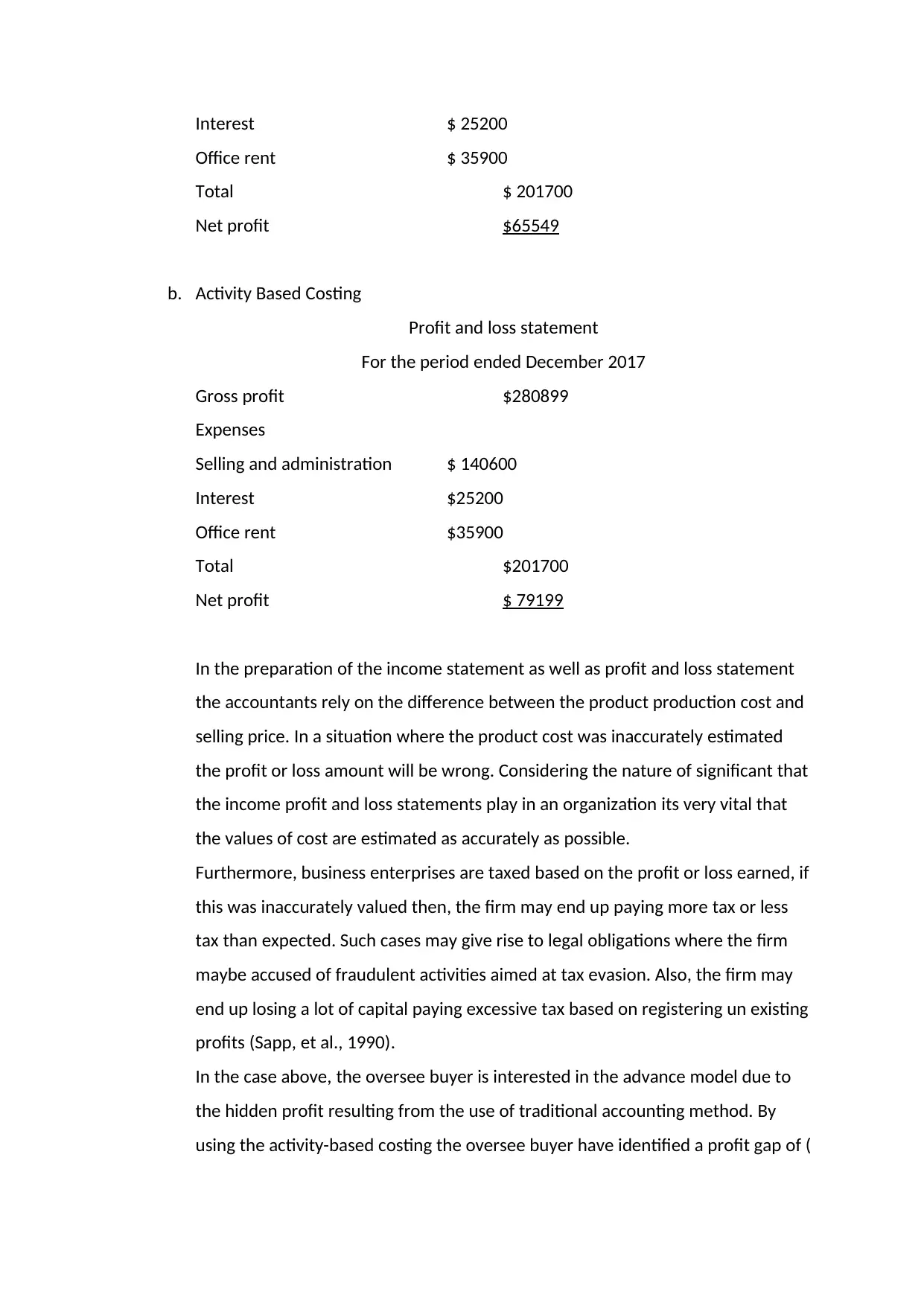

This report analyzes the costing systems of Sewing Easy Ltd, a sewing machine manufacturer, comparing traditional and activity-based costing (ABC) methods. The company, operating for two years, aims to sell its advance model to an overseas buyer. The report highlights the concerns of the management regarding the sole interest in the advance model. It evaluates the firm's current traditional costing system, detailing unit costs for both basic and advance models. The report then presents an ABC system analysis, showcasing overhead allocation and unit costs. A profit and loss statement is provided for both costing methods, revealing discrepancies in net profit. The report emphasizes the importance of accurate cost estimation for financial statements and tax obligations. It explains the buyer's interest in the advance model due to hidden profits from the traditional method. Furthermore, it discusses the benefits and limitations of the ABC system and outlines methods for handling over or under-applied overheads, concluding with a list of relevant references.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.