HA2011 Managerial Accounting Report: ABB Implementation at Wesfarmers

VerifiedAdded on 2023/06/03

|12

|3545

|460

Report

AI Summary

This report analyzes the application of Activity-Based Budgeting (ABB) for Wesfarmers Limited, an Australian retail company. The report begins with an executive summary and introduction, providing an overview of ABB and its features, followed by a detailed description of Wesfarmers. A core component of the report involves a comprehensive comparison of ABB with traditional budgeting methods, highlighting the differences in their approaches, information conveyed, and decision-making processes. The report then assesses the suitability of ABB for Wesfarmers, considering the company's retail operations and cost structure. It emphasizes how ABB can improve cost management by accurately forecasting resources needed for specific activities, enhancing strategic planning, and making the budgeting process more transparent. The report concludes with a summary of findings and recommendations regarding ABB implementation for Wesfarmers, emphasizing the benefits of ABB over traditional methods.

Management accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

The main purpose of this report is to gain an insight into the benefit that firms can

achieve by the use of activity-based budgeting method of budget preparation. This has been done

by providing a description of the activity-based budgeting method and its features. This is

followed by comparison of the method with the traditional method of budgeting. It has been

evaluated with the use of the report that ABB method helps in accurate forecasting of the

resources required to produce a specific output by determination of the activities that are

necessary for achieving that output.

2

The main purpose of this report is to gain an insight into the benefit that firms can

achieve by the use of activity-based budgeting method of budget preparation. This has been done

by providing a description of the activity-based budgeting method and its features. This is

followed by comparison of the method with the traditional method of budgeting. It has been

evaluated with the use of the report that ABB method helps in accurate forecasting of the

resources required to produce a specific output by determination of the activities that are

necessary for achieving that output.

2

Contents

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................4

a)Description of the Selected firm...................................................................................................4

b) Description of Activity-Based Budgeting and Its Features.........................................................4

C: Difference between Activity Based Budgeting and traditional budgeting.................................5

d)Discussion Regarding the Suitability of ABB for Wesfarmers....................................................7

Conclusion.......................................................................................................................................9

References......................................................................................................................................10

3

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................4

a)Description of the Selected firm...................................................................................................4

b) Description of Activity-Based Budgeting and Its Features.........................................................4

C: Difference between Activity Based Budgeting and traditional budgeting.................................5

d)Discussion Regarding the Suitability of ABB for Wesfarmers....................................................7

Conclusion.......................................................................................................................................9

References......................................................................................................................................10

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

This report is developed on the perspective of management accountant assigned the

responsibility of providing recommendation to the CEO of a firm regarding the adoption of

budgeting method of Activity-Based Budgeting (ABB). The selected firm in this context is

Wesfarmers Limited, a retail company of Australia. In this context, it has specifically examined

the suitability of the method to be adopted by the selected firm. The firm selected in this context

is Wesfarmers limited, a recognized retail company of Australia. It is done mainly by developing

an understanding of the ABB by examining its relevant characteristics. Also, a comparison of the

method with the traditional method of budget preparation is also carried out in the report.

a) Description of the selected firm

Wesfarmers Limited is an Australian retail company, having major interests in the

business operations of retail, coal mining, gas processing, chemical, fertilizers, industrial and

safety products. It is listed on the Australian securities Exchange (ASX) have major subsidiaries

of Coles, Supermarkets and Bunning’s warehouse. The company major focus is to provide

higher returns to the shareholders by achieving customer satisfaction. The company is highly

committed to promote the development of the local communities and reducing the environmental

impact of its operations. The company has achieved strong management capability on account of

gaining expertise development and execution of strategy. The strong management of the

company has enabled to achieve a control over its diverse business operations.

b) Description of Activity-Based Budgeting and Its Features

Activity-based budgeting (ABB) can be defined as method of budgeting that is developed

for increasing the transparency in the process of budget development of business entities. It helps

in improving the accountability in the budgeting process of an entity by allocating the revenue

realized in proportion to the unit responsible for that activity. It assists the managers in adequate

management of resources and expenses by having a direct control over them and largely helps in

achieving the overall mission and strategic goals of an entity. The method is largely used by

business nowadays for gaining a competitive advantage over their competitors through adequate

management of their cost structure and reduction of generation of waste resources. The method

4

This report is developed on the perspective of management accountant assigned the

responsibility of providing recommendation to the CEO of a firm regarding the adoption of

budgeting method of Activity-Based Budgeting (ABB). The selected firm in this context is

Wesfarmers Limited, a retail company of Australia. In this context, it has specifically examined

the suitability of the method to be adopted by the selected firm. The firm selected in this context

is Wesfarmers limited, a recognized retail company of Australia. It is done mainly by developing

an understanding of the ABB by examining its relevant characteristics. Also, a comparison of the

method with the traditional method of budget preparation is also carried out in the report.

a) Description of the selected firm

Wesfarmers Limited is an Australian retail company, having major interests in the

business operations of retail, coal mining, gas processing, chemical, fertilizers, industrial and

safety products. It is listed on the Australian securities Exchange (ASX) have major subsidiaries

of Coles, Supermarkets and Bunning’s warehouse. The company major focus is to provide

higher returns to the shareholders by achieving customer satisfaction. The company is highly

committed to promote the development of the local communities and reducing the environmental

impact of its operations. The company has achieved strong management capability on account of

gaining expertise development and execution of strategy. The strong management of the

company has enabled to achieve a control over its diverse business operations.

b) Description of Activity-Based Budgeting and Its Features

Activity-based budgeting (ABB) can be defined as method of budgeting that is developed

for increasing the transparency in the process of budget development of business entities. It helps

in improving the accountability in the budgeting process of an entity by allocating the revenue

realized in proportion to the unit responsible for that activity. It assists the managers in adequate

management of resources and expenses by having a direct control over them and largely helps in

achieving the overall mission and strategic goals of an entity. The method is largely used by

business nowadays for gaining a competitive advantage over their competitors through adequate

management of their cost structure and reduction of generation of waste resources. The method

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

of budgeting primarily involves the identification of the activities followed by analyzing the cost

drivers that are the factors responsible for driving expenses over that activity. It is followed by

forecasting the number of units of cost driver required for completing the activity level. Lastly,

the overall cost is calculated by identifying the cost incurred in completing per unit of activity.

The method is largely effective for gaining an accurate estimate of the overhead costs to be

incurred for completing an activity level. For example, in a scenario of sales office the cost

driver for the number of sales orders can be estimated by calculating the forecasted cost of

processing of a single sales order. It is followed by forecasting the number of sales orders for a

budgeted period and then calculating the overall budget for the total sales. Thus, the method of

ABC would be highly helpful for examining the variable costs such as accommodation that is

incurred by the sale office.

Therefore, it can be said that the major benefit of the use of this type of budgeting system

is that it largely helps the management accountants in gaining a future estimate of the overhead

costs. Thus, it can help in having a direct control over the cost structure of an entity by

identifying the activities that can be eliminated in order to reduce the variable costs incurred

during its overall operational process. The budgeting system enables an entity to forecast the

activities that it will engage for production of a specified volume of products or services. This

will help the management accountants in organizing the number of activities as per its strategic

goals and objectives. The costs of each activity to be incurred is compiled for developing an

accurate budget that enables the managers in taking a right decision regarding its future growth

and development. The major features of the ABB method of budgeting can be stated as follows:

The method of activity-based budgeting should be done mainly by the busies entities that

adopts the use of activity based costing for allocation of operational costs

It is highly useful in achieving Total Quality Managements (TQM) in entities by attaining

cost-effectiveness through elimination of unnecessary activities

It assists in making strategic planning by business managers through establishing a

connection between operational planning and the financial results

It helps in accurate forecasting of the resources required to produce a specific output by

determination of the activities that are necessary for achieving that output and then

allocation of direct resources to each unit of activity

5

drivers that are the factors responsible for driving expenses over that activity. It is followed by

forecasting the number of units of cost driver required for completing the activity level. Lastly,

the overall cost is calculated by identifying the cost incurred in completing per unit of activity.

The method is largely effective for gaining an accurate estimate of the overhead costs to be

incurred for completing an activity level. For example, in a scenario of sales office the cost

driver for the number of sales orders can be estimated by calculating the forecasted cost of

processing of a single sales order. It is followed by forecasting the number of sales orders for a

budgeted period and then calculating the overall budget for the total sales. Thus, the method of

ABC would be highly helpful for examining the variable costs such as accommodation that is

incurred by the sale office.

Therefore, it can be said that the major benefit of the use of this type of budgeting system

is that it largely helps the management accountants in gaining a future estimate of the overhead

costs. Thus, it can help in having a direct control over the cost structure of an entity by

identifying the activities that can be eliminated in order to reduce the variable costs incurred

during its overall operational process. The budgeting system enables an entity to forecast the

activities that it will engage for production of a specified volume of products or services. This

will help the management accountants in organizing the number of activities as per its strategic

goals and objectives. The costs of each activity to be incurred is compiled for developing an

accurate budget that enables the managers in taking a right decision regarding its future growth

and development. The major features of the ABB method of budgeting can be stated as follows:

The method of activity-based budgeting should be done mainly by the busies entities that

adopts the use of activity based costing for allocation of operational costs

It is highly useful in achieving Total Quality Managements (TQM) in entities by attaining

cost-effectiveness through elimination of unnecessary activities

It assists in making strategic planning by business managers through establishing a

connection between operational planning and the financial results

It helps in accurate forecasting of the resources required to produce a specific output by

determination of the activities that are necessary for achieving that output and then

allocation of direct resources to each unit of activity

5

The method of budgeting system is highly useful for the entities in which overhead costs

are a major proportion of the overall cost structure of an entity

It is known to be an output-based approach which involves recognition of the activities at

the initial level that drives the costs and views the overall business operations as a

collection of activities and aligns them with the organizational strategy (Zhang and Isa,

2010)

C: Difference between Activity Based Budgeting and traditional budgeting

It is important to understand the meaning of traditional budgeting and its importance in

management accounting before discussing between traditional budgeting and ABB. In general

traditional budgeting is defined as the management process used to project the business revenue

and expenses for future years through using the budget of previous year. In this context budget is

referred to as management tool that helps to predict and analyze the business earnings and

expenditures. In short it helps in decision making process of management in relation to allocation

of resources. Traditional budgeting process is mainly used by the businesses that are already

established and make use of previous budgets with adjustments to inflation and others changes in

business (Stamenova, 2018). The differences arise between ABB and traditional budgeting due

to difference of process of drafted the budgets, methods used to prepare the budgets, and their

advantages and disadvantages. The budgeting approach used in the preparation of traditional

budgets is referred to as an incremental approach. As per incremental approach of budgeting

company uses past year data to prepare the current budgets but there is need to make correction

in current budgets due to change in output, changes in prices, inflation etc. So it can be said that

this method of budget preparation is very easy and simple to understand.

There are multiple differences in traditional budgeting and activity based budgeting that

has led companies to shift towards the activity based budgeting from traditional budgeting. Some

of major differences between traditional budgeting and activity based budgeting arises due to

manner of preparation, its use, information conveyed, process used, importance, decision making

and many other. While preparing the activity based budgets information from the previous year

budgets are not taken but in this method resource are allocated on the basis of efficiencies of

business operations and available resources with the entity. The role of cost manager in

6

are a major proportion of the overall cost structure of an entity

It is known to be an output-based approach which involves recognition of the activities at

the initial level that drives the costs and views the overall business operations as a

collection of activities and aligns them with the organizational strategy (Zhang and Isa,

2010)

C: Difference between Activity Based Budgeting and traditional budgeting

It is important to understand the meaning of traditional budgeting and its importance in

management accounting before discussing between traditional budgeting and ABB. In general

traditional budgeting is defined as the management process used to project the business revenue

and expenses for future years through using the budget of previous year. In this context budget is

referred to as management tool that helps to predict and analyze the business earnings and

expenditures. In short it helps in decision making process of management in relation to allocation

of resources. Traditional budgeting process is mainly used by the businesses that are already

established and make use of previous budgets with adjustments to inflation and others changes in

business (Stamenova, 2018). The differences arise between ABB and traditional budgeting due

to difference of process of drafted the budgets, methods used to prepare the budgets, and their

advantages and disadvantages. The budgeting approach used in the preparation of traditional

budgets is referred to as an incremental approach. As per incremental approach of budgeting

company uses past year data to prepare the current budgets but there is need to make correction

in current budgets due to change in output, changes in prices, inflation etc. So it can be said that

this method of budget preparation is very easy and simple to understand.

There are multiple differences in traditional budgeting and activity based budgeting that

has led companies to shift towards the activity based budgeting from traditional budgeting. Some

of major differences between traditional budgeting and activity based budgeting arises due to

manner of preparation, its use, information conveyed, process used, importance, decision making

and many other. While preparing the activity based budgets information from the previous year

budgets are not taken but in this method resource are allocated on the basis of efficiencies of

business operations and available resources with the entity. The role of cost manager in

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

preparing the activity based is very strong as he has to analyze each and every activity before

making allocation of resource to each activity. The purpose of analyzing each activity is to

achieve maximum output with optimum utilization of resources. In case of traditional budgeting

no such factors are being considered while performing the task of preparation of budgets. Only

one thing is kept in mind that there is no change in business activities and all activities yield

same output as previous year. This method of budget preparation is very old and does not

support the decision making process. While it has been noted that activity based budgeting plays

a critical role in decision making process. There is orientation difference between both types of

budget methods. Traditional budget is accounting oriented i.e. it follows a process simple

accounting technique without considering a surrounding environment and other factors while

preparing the budgets. ABB is project oriented which means it considers business objectives,

business requirements and requirements of various activities before allocating the resources to

each activity. This way of preparing budgets is very effective and takes in accounts all the factors

that impacts profitability and optimum utilization of resources (Shim, Siegel and Shim, 2011).

In activity based budgeting it is very easy to identify and measure the effect of the unused

capacities while in case of traditional budgeting it is not possible to identify the unused

capacities under each activity, only the effect of unused capacities can be seen. Traditional

budgeting focuses only on cost of departments and completely ignores the total budgeting cost

that is main disadvantage of traditional budgets. On the other hand, activity based budgeting take

into account total volume of work delivered through the budgets together with the total cost

levied. It helps to make suitable changes in budgets that arise due to uncertainties after the

budgets have been prepared. So it can be said that activity based budgets helps in manipulate the

budgets after it has been prepared but it is not possible in case of traditional budgeting. In short it

can be said that activity based budgeting uses more meaningful approach to allocate the

resources while so such approach has been deployed by the traditional budgeting that is its

biggest disadvantage (Lalli, 2011). So it clear that all the shortcoming of the traditional

budgeting has been removed in the activity based budgeting and all the resources are allocated

after evaluating each activity despite of using old budgets. It is important cost manager pay

emphasis on the economic factors while preparing the budgets but due to rigidness of traditional

budgets it is not possible for managers to consider the factors such as economic conditions. In

case of ABB it is important to consider the economic factors before drafting the budgets.

7

making allocation of resource to each activity. The purpose of analyzing each activity is to

achieve maximum output with optimum utilization of resources. In case of traditional budgeting

no such factors are being considered while performing the task of preparation of budgets. Only

one thing is kept in mind that there is no change in business activities and all activities yield

same output as previous year. This method of budget preparation is very old and does not

support the decision making process. While it has been noted that activity based budgeting plays

a critical role in decision making process. There is orientation difference between both types of

budget methods. Traditional budget is accounting oriented i.e. it follows a process simple

accounting technique without considering a surrounding environment and other factors while

preparing the budgets. ABB is project oriented which means it considers business objectives,

business requirements and requirements of various activities before allocating the resources to

each activity. This way of preparing budgets is very effective and takes in accounts all the factors

that impacts profitability and optimum utilization of resources (Shim, Siegel and Shim, 2011).

In activity based budgeting it is very easy to identify and measure the effect of the unused

capacities while in case of traditional budgeting it is not possible to identify the unused

capacities under each activity, only the effect of unused capacities can be seen. Traditional

budgeting focuses only on cost of departments and completely ignores the total budgeting cost

that is main disadvantage of traditional budgets. On the other hand, activity based budgeting take

into account total volume of work delivered through the budgets together with the total cost

levied. It helps to make suitable changes in budgets that arise due to uncertainties after the

budgets have been prepared. So it can be said that activity based budgets helps in manipulate the

budgets after it has been prepared but it is not possible in case of traditional budgeting. In short it

can be said that activity based budgeting uses more meaningful approach to allocate the

resources while so such approach has been deployed by the traditional budgeting that is its

biggest disadvantage (Lalli, 2011). So it clear that all the shortcoming of the traditional

budgeting has been removed in the activity based budgeting and all the resources are allocated

after evaluating each activity despite of using old budgets. It is important cost manager pay

emphasis on the economic factors while preparing the budgets but due to rigidness of traditional

budgets it is not possible for managers to consider the factors such as economic conditions. In

case of ABB it is important to consider the economic factors before drafting the budgets.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

In preparation of activity based budgets cost manager has to follow the procedure of

ranking each activity so that resources can be allocates on optimum basis. Also in case of activity

based budgeting goals and important business functions are considered in preparation of budgets

but traditional budgeting has no provisions to evaluate the business functions and goals (Drury,

2008).

d) Discussion Regarding the Suitability of ABB for Wesfarmers

Wesfarmers is a leading retail company within Australia having a number of subsidiaries

such as Coles, supermarkets, Bunning’s Warehouse and any other. The company as such is

recognized to have interests in various filed such as retail, chemical, fertilizers, coal mining,

industrial and safety products. The company as such is involved in providing various products

and services to the customers and therefore marinating a direct control over its overhead costs is

essential for it to achieve operational efficiency. This can be achieved by the company through

accurate forecasting of cost to be incurred in completing each of its activity by means of budget

preparation. In this context, the company is recommended to adopt the use of method of ABB

(Activity-based Budgeting) that will help in determining the resources required for completing

each unit of activity on the basis of specific output to be achieved.

The retail companies such as Wesfarmers may face increasing difficulties in developing

budgets for its administrative departments. This is because due to lack of clear input-output

relationship as there exists uncertainty on account of labor required as per the volume of

production. Therefore, management can face problem in planning and control for future direction

by having insufficient data relating to the expected expenses to be incurred in administrative

functions. These departments incurs large amount of indirect fixed costs and therefore it is

essential for the retail companies to implementation an accurate method of budgeting that helps

in minimizing the costs in these areas for enabling a company to achieve operational efficiency.

Wesfarmers carries out its business activities in a highly competitive retail environment of

Australia. As such, it is highly essential for the company to utilize an accurate method of

budgeting that enables it to reduce its operational costs for maintaining its competitive position

(Liu and Pan, 2007).

8

ranking each activity so that resources can be allocates on optimum basis. Also in case of activity

based budgeting goals and important business functions are considered in preparation of budgets

but traditional budgeting has no provisions to evaluate the business functions and goals (Drury,

2008).

d) Discussion Regarding the Suitability of ABB for Wesfarmers

Wesfarmers is a leading retail company within Australia having a number of subsidiaries

such as Coles, supermarkets, Bunning’s Warehouse and any other. The company as such is

recognized to have interests in various filed such as retail, chemical, fertilizers, coal mining,

industrial and safety products. The company as such is involved in providing various products

and services to the customers and therefore marinating a direct control over its overhead costs is

essential for it to achieve operational efficiency. This can be achieved by the company through

accurate forecasting of cost to be incurred in completing each of its activity by means of budget

preparation. In this context, the company is recommended to adopt the use of method of ABB

(Activity-based Budgeting) that will help in determining the resources required for completing

each unit of activity on the basis of specific output to be achieved.

The retail companies such as Wesfarmers may face increasing difficulties in developing

budgets for its administrative departments. This is because due to lack of clear input-output

relationship as there exists uncertainty on account of labor required as per the volume of

production. Therefore, management can face problem in planning and control for future direction

by having insufficient data relating to the expected expenses to be incurred in administrative

functions. These departments incurs large amount of indirect fixed costs and therefore it is

essential for the retail companies to implementation an accurate method of budgeting that helps

in minimizing the costs in these areas for enabling a company to achieve operational efficiency.

Wesfarmers carries out its business activities in a highly competitive retail environment of

Australia. As such, it is highly essential for the company to utilize an accurate method of

budgeting that enables it to reduce its operational costs for maintaining its competitive position

(Liu and Pan, 2007).

8

In this context, the method of activity-based budgeting proves to be highly suitable for

assigning the overhead costs as per the volume of products and services. This s can be done by

the management accountants by identifying the number of activities involved in their production

and assigning the overhead costs to each unit of activity as per their resources consumed by them

(Ayers, 2017). As such, the budgets developed with the use of activity-based costing information

can enable the management accountants in retail companies to a large extent by determining the

relation between the quantities of units produced and the activities involved in production of the

specific units. The major benefits that Wesfarmers can realized by the use of ABB method is

identification of the physical resources required for delivering a specific amount of products and

services and also projecting the future costs. It is done by determining the output to be achieved

and the allocating the resources required for completion of that output level. Thus, the

development of a budget with help of ABB method will help the company to achieve its vision

by converting it into a strategy by identification of the various ways through which it can be

realized (Baird, 2007).

The vision of the company is to create value for the customers through providing them

high quality products and services. As such, the development of a forecasted budget predicting

the overall cost to be incurred in delivering a specified dumber of product to the customers will

help the company to determine various ways of creating value for them. This involves taking

important decisions regarding reducing expenses, increasing market share, improving sales rate,

increasing profit margins and minimizing the operational costs. For example, the company can

develop an accurate sales budget with the use of ABB approach (Dunne, 2007). This involves

determination of an estimated demand of goods or services required by carrying out sales

forecasts. This can be done by estimating the demand for the output of each business activity on

the basis of its cost driver. The use of this rate can be done to estimate their resources required

for completing of the activity. As such, it will also enables the management accountants in

developing an insight into each of the business activity and thereby eliminating the unnecessary

activities and reducing the waste generation leading to improved operational efficiency (Huynh,

2013).

As such, Wesfarmers to successfully integrate the method of budget preparation with the

use of ABB for a specific department need to primarily determine the output to be delivered from

9

assigning the overhead costs as per the volume of products and services. This s can be done by

the management accountants by identifying the number of activities involved in their production

and assigning the overhead costs to each unit of activity as per their resources consumed by them

(Ayers, 2017). As such, the budgets developed with the use of activity-based costing information

can enable the management accountants in retail companies to a large extent by determining the

relation between the quantities of units produced and the activities involved in production of the

specific units. The major benefits that Wesfarmers can realized by the use of ABB method is

identification of the physical resources required for delivering a specific amount of products and

services and also projecting the future costs. It is done by determining the output to be achieved

and the allocating the resources required for completion of that output level. Thus, the

development of a budget with help of ABB method will help the company to achieve its vision

by converting it into a strategy by identification of the various ways through which it can be

realized (Baird, 2007).

The vision of the company is to create value for the customers through providing them

high quality products and services. As such, the development of a forecasted budget predicting

the overall cost to be incurred in delivering a specified dumber of product to the customers will

help the company to determine various ways of creating value for them. This involves taking

important decisions regarding reducing expenses, increasing market share, improving sales rate,

increasing profit margins and minimizing the operational costs. For example, the company can

develop an accurate sales budget with the use of ABB approach (Dunne, 2007). This involves

determination of an estimated demand of goods or services required by carrying out sales

forecasts. This can be done by estimating the demand for the output of each business activity on

the basis of its cost driver. The use of this rate can be done to estimate their resources required

for completing of the activity. As such, it will also enables the management accountants in

developing an insight into each of the business activity and thereby eliminating the unnecessary

activities and reducing the waste generation leading to improved operational efficiency (Huynh,

2013).

As such, Wesfarmers to successfully integrate the method of budget preparation with the

use of ABB for a specific department need to primarily determine the output to be delivered from

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

it. This should be followed by developing an estimate of the activities required for delivering the

output and identification of the cost drivers. The demand for each activity should be estimated

followed by determination of the cost of resources required to produce the identified activities. It

can be said from the overall discussion that the use of ABB method of budget preparation will

help the management accountants in achieving the determined cost target effectively. It will

facilitate the business managers in achieving the organizational goals by assisting in taking

accurate decisions (Moustafa, 2005).

In addition to this, the method can be employed by the company in providing an

assessment of the performance of a manager. This can be done by comparing the results obtained

with the use of ABB method with that actually realized. The effectiveness can be assessed by

examining whether the manager has achieved or exceeded the goads described. However, the

company is required to develop an insight into the significant challenges that it can face while

the adoption of ABB method. This involves lack of support from employees, lack of relevant

knowledge and competency in the manager, significant cost to be incurred in implementation and

time required for its successful adoption. As such, the company is required to develop proper

plans for gathering relevant resources and providing training to the business managers and

employees to involve their participation. Also, the perceived benefits to be realized should be

compared with the cost to be incurred in its adoption for taking final decision of its

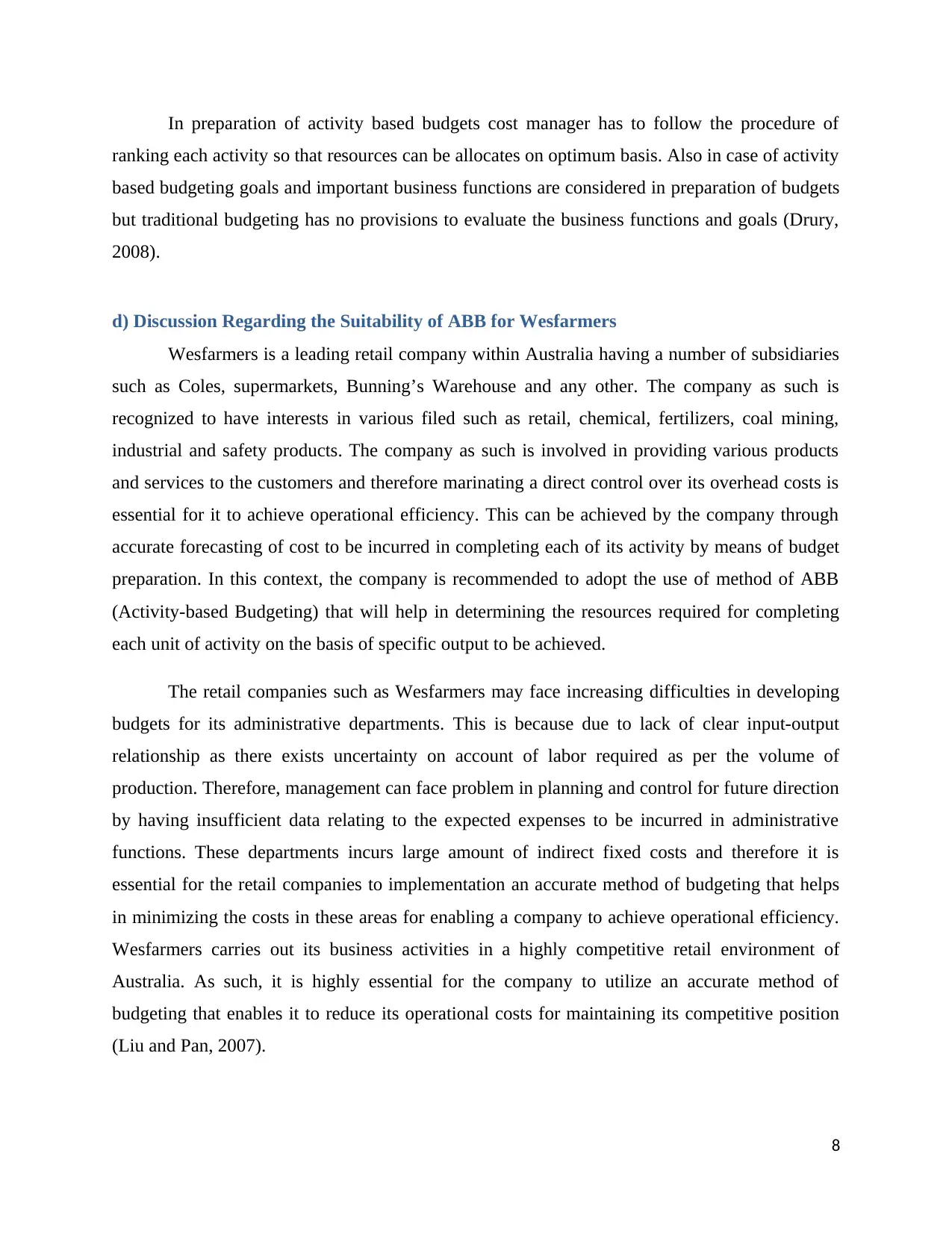

implementation (Oseifuah, 2014). The integration process of ABB within the company can be

illustrated as follows:

10

output and identification of the cost drivers. The demand for each activity should be estimated

followed by determination of the cost of resources required to produce the identified activities. It

can be said from the overall discussion that the use of ABB method of budget preparation will

help the management accountants in achieving the determined cost target effectively. It will

facilitate the business managers in achieving the organizational goals by assisting in taking

accurate decisions (Moustafa, 2005).

In addition to this, the method can be employed by the company in providing an

assessment of the performance of a manager. This can be done by comparing the results obtained

with the use of ABB method with that actually realized. The effectiveness can be assessed by

examining whether the manager has achieved or exceeded the goads described. However, the

company is required to develop an insight into the significant challenges that it can face while

the adoption of ABB method. This involves lack of support from employees, lack of relevant

knowledge and competency in the manager, significant cost to be incurred in implementation and

time required for its successful adoption. As such, the company is required to develop proper

plans for gathering relevant resources and providing training to the business managers and

employees to involve their participation. Also, the perceived benefits to be realized should be

compared with the cost to be incurred in its adoption for taking final decision of its

implementation (Oseifuah, 2014). The integration process of ABB within the company can be

illustrated as follows:

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(Source: http://article.sciencepublishinggroup.com/pdf/10.11648.j.ijefm.20130104.11.pdf)

Conclusion

The report has inferred that the use of ABB method of budget development in

comparison to that of traditional method of budgeting will enable in improving the transparency

in the budget preparation. It also facilitates the managers in taking effective decisions at the time

of strategy formulation by gaining an accurate forecast regarding the overall cost structure of an

entity. It has been recommended to the CEO of Wesfarmers to integrate the method of budget

preparation on the basis of activity costs to gain a realistic view of the firm cost structure and

develop possible ways of maximizing the company’s operational efficiency.

11

Conclusion

The report has inferred that the use of ABB method of budget development in

comparison to that of traditional method of budgeting will enable in improving the transparency

in the budget preparation. It also facilitates the managers in taking effective decisions at the time

of strategy formulation by gaining an accurate forecast regarding the overall cost structure of an

entity. It has been recommended to the CEO of Wesfarmers to integrate the method of budget

preparation on the basis of activity costs to gain a realistic view of the firm cost structure and

develop possible ways of maximizing the company’s operational efficiency.

11

References

Ayers, J. 2017. Retail Supply Chain Management. CRC Press.

Baird, K., 2007. Adoption of activity management practices in public sector organizations.

Accounting and Finance 47, pp. 551-569.

Drury, C. 2008. Management and Cost Accounting. Cengage Learning EMEA.

Dunne, P. 2007. Retailing. Cengage Learning.

Huynh, T. 2013. Integration of activity-based budgeting and activity-based management.

International Journal of Economics, Finance and Management Sciences 1(4), pp. 181-187.

Lalli, W.R. 2011. Handbook of Budgeting. John Wiley & Sons.

Liu, L.Y.J. and Pan, F., 2007. The implementation of Activity-Based Costing in China: An

innovation action research approach. The British Accounting Review 39, pp.249-264.

Moustafa, E. 2005. An Application of Activity-Based-Budgeting in Shared Service Departments

and Its Perceived Benefits and Barriers under Low-IT Environment Conditions. Journal of

Economic & Administrative Sciences 21 (1), pp.42-72.

Oseifuah, E. 2014. Activity based costing (ABC) in the public sector: Benefits and challenges.

Problems and Perspectives in Management 12(4), pp. 581-587.

Shim, J.K., Siegel, J.G. and Shim, A.I. 2011. Budgeting Basics and Beyond. John Wiley & Sons.

Stamenova, S. 2018. Benefits of a budget system. Traditional budgetary Systems versus Rolling

budgets, zero-based budgets and activity-based budgets. GRIN Verlag.

The Wesfarmers Way. 2017. [Online]. Available at: http://www.wesfarmers.com.au/who-we-

are/the-wesfarmers-way [Accessed on: 28 September 2018].

Zhang, Y.F. and Isa, C.R., 2010. Behavioral and organizational variables affecting the success of

ABC success in China. African Journal of Business Management 4(11), pp. 2302-2308.

12

Ayers, J. 2017. Retail Supply Chain Management. CRC Press.

Baird, K., 2007. Adoption of activity management practices in public sector organizations.

Accounting and Finance 47, pp. 551-569.

Drury, C. 2008. Management and Cost Accounting. Cengage Learning EMEA.

Dunne, P. 2007. Retailing. Cengage Learning.

Huynh, T. 2013. Integration of activity-based budgeting and activity-based management.

International Journal of Economics, Finance and Management Sciences 1(4), pp. 181-187.

Lalli, W.R. 2011. Handbook of Budgeting. John Wiley & Sons.

Liu, L.Y.J. and Pan, F., 2007. The implementation of Activity-Based Costing in China: An

innovation action research approach. The British Accounting Review 39, pp.249-264.

Moustafa, E. 2005. An Application of Activity-Based-Budgeting in Shared Service Departments

and Its Perceived Benefits and Barriers under Low-IT Environment Conditions. Journal of

Economic & Administrative Sciences 21 (1), pp.42-72.

Oseifuah, E. 2014. Activity based costing (ABC) in the public sector: Benefits and challenges.

Problems and Perspectives in Management 12(4), pp. 581-587.

Shim, J.K., Siegel, J.G. and Shim, A.I. 2011. Budgeting Basics and Beyond. John Wiley & Sons.

Stamenova, S. 2018. Benefits of a budget system. Traditional budgetary Systems versus Rolling

budgets, zero-based budgets and activity-based budgets. GRIN Verlag.

The Wesfarmers Way. 2017. [Online]. Available at: http://www.wesfarmers.com.au/who-we-

are/the-wesfarmers-way [Accessed on: 28 September 2018].

Zhang, Y.F. and Isa, C.R., 2010. Behavioral and organizational variables affecting the success of

ABC success in China. African Journal of Business Management 4(11), pp. 2302-2308.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.