Unit 5 Management Accounting Report: ABC Co. Ltd Analysis

VerifiedAdded on 2023/01/10

|8

|1855

|33

Report

AI Summary

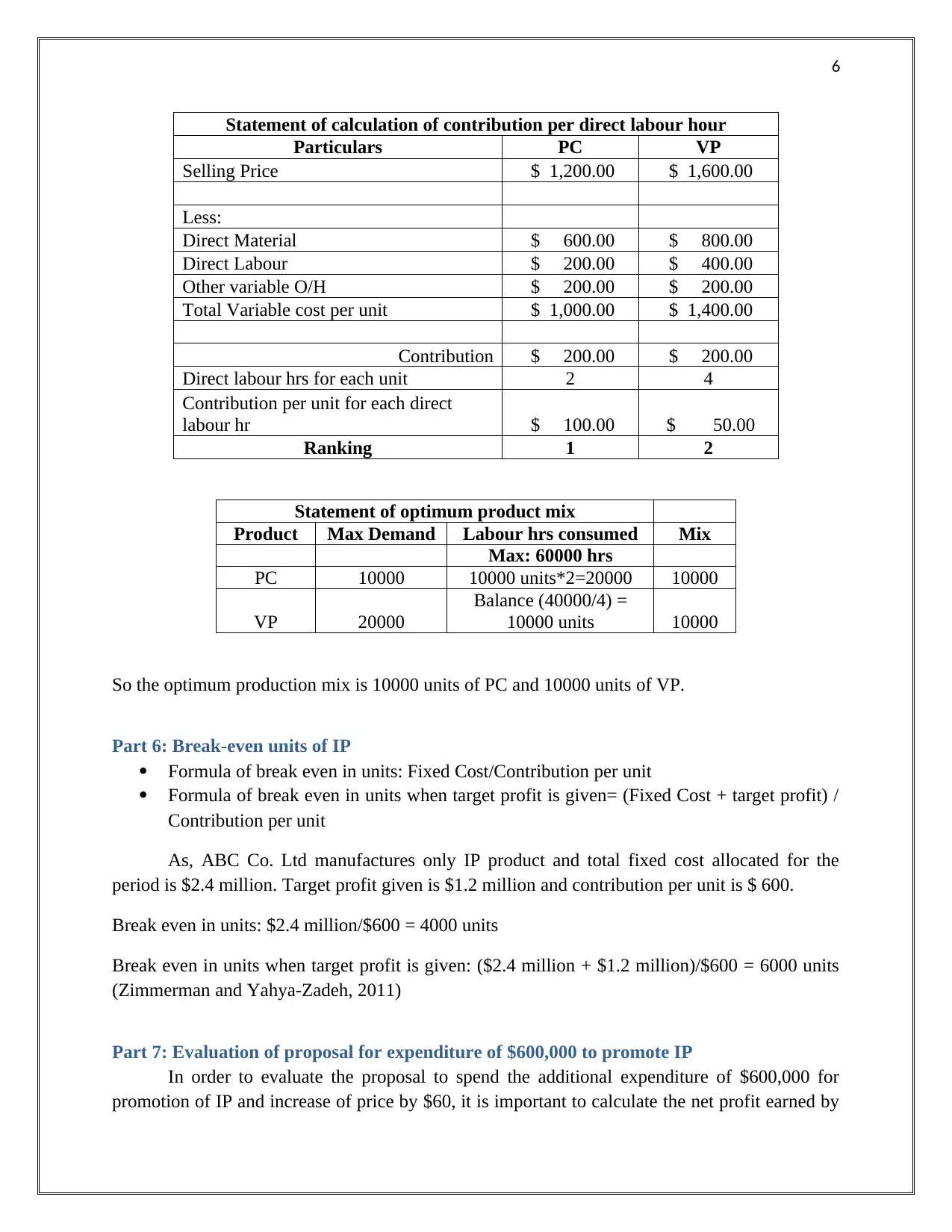

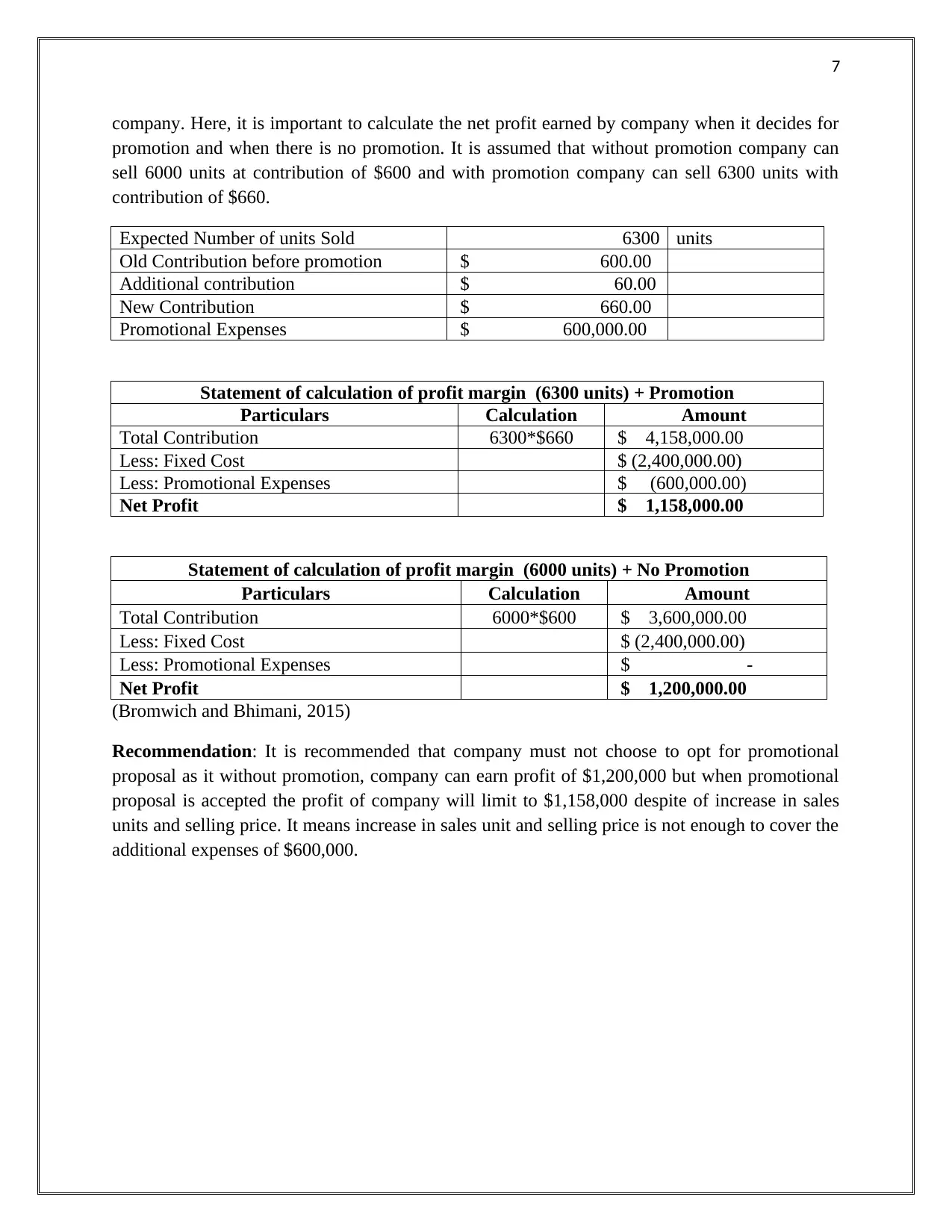

This report provides a detailed analysis of management accounting principles applied to ABC Co. Ltd., a manufacturer of electronic products. It begins by defining management accounting, its types, and the role of management accountants, contrasting it with financial accounting. The report then classifies costs to aid in managerial decision-making, differentiating between fixed, variable, and overhead costs. A significant portion is dedicated to calculating unit costs using absorption and marginal costing methods for two products, PC and VP. The report further explores the job order costing method for special orders, including relevant financial and non-financial considerations. The optimum production mix to maximize profit is determined, along with break-even analysis for a new product, IP. Finally, the report evaluates a proposal to spend $600,000 on promoting IP, assessing the impact on profitability and offering recommendations based on the analysis. The report is supported by references to academic literature.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.