Management Accounting Report: ABC Limited, HNC in Business

VerifiedAdded on 2023/01/13

|17

|4713

|37

Report

AI Summary

This report provides a comprehensive overview of management accounting principles and practices, focusing on the context of ABC Limited, a manufacturing entity. It begins with an introduction to management accounting systems, their essential requirements, and the integration of various systems such as inventory management, cost accounting, and price optimization. The report then explores different types of management accounting reports, including account receivable reports, performance reports, and budget reports, highlighting their benefits and applications. A significant portion of the report is dedicated to calculating net profit using different costing methods, namely marginal and absorption costing, and comparing their advantages and disadvantages. The analysis includes the preparation of budgeted and actual profit and loss statements under both costing methods. Furthermore, the report examines various planning tools and their advantages and disadvantages, and compares how different organizations respond to financial problems, offering insights into the adaptation of management accounting systems and planning tools. Overall, the report aims to provide a solid understanding of management accounting concepts and their practical application in a business environment.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1. Management accounting systems and its essential requirements.....................................3

P2. Different types of management accounting reports .......................................................5

TASK 2............................................................................................................................................6

P3. Calculate net profit by using different costing methods..................................................6

TASK 3..........................................................................................................................................10

P4. Different plaining tools along with advantages or disadvantages..................................10

TASK 4..........................................................................................................................................13

P5. Comparison of organizations that how they respond to any financial problems...........13

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1. Management accounting systems and its essential requirements.....................................3

P2. Different types of management accounting reports .......................................................5

TASK 2............................................................................................................................................6

P3. Calculate net profit by using different costing methods..................................................6

TASK 3..........................................................................................................................................10

P4. Different plaining tools along with advantages or disadvantages..................................10

TASK 4..........................................................................................................................................13

P5. Comparison of organizations that how they respond to any financial problems...........13

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

Every entity in today's competitiveness industry and changing environmental scenario

wants to achieve their defined objectives and targets within scheduled time-frame. Management

in every trade and business enterprise put their efforts towards accomplishment of targets and

other short term goals (Arena and Arnaboldi, 2014). Management accounting is only the crucial

aspect which provide an assistive framework to managerial personnel for attaining goals within

planned time-frame. Management accounting is like full flagged package of all the vital tasks

primarily concerned with both management and accounting aspects.

This study-report emphasises on fundamental and critical aspects of managerial

accounting in context of ABC Limited which is a mid-size entity operating in manufacturing

sector. It also covers necessary requisites of its systems and comprehensive discussion on

different reports used in managerial accounting reporting as well as use of planning-tools in

responding to numerous kind of financial problems. Moreover it consists of comparison of

enterprises in terms of manner of adaption of MA systems and different planning-tools.

TASK 1

P1. Management accounting systems and its essential requirements

Management Accounting: Management or managerial accounting referred as set of

systematic functions which effectively contributes towards detailed tracking and analysis of

internal costs related to multiple business processes which assist a corporation and enterprise in

making of determinations and decisions concerned with productions, core-business operations

and investment & funding in market-place (Azudin and Mansor, 2018)). Enterprises need

managerial accounting and its different aspects to assess efficiency predetermined budgets, costs

of key operations and thereafter efficacious allocation of funds and resources accordingly in

respective departments. Therefore, herein role and function of managerial personnel and

accounting officials is quite significant for business' success.

As per Anglo-American Council of Productivity management accounting is defined as

“Structured presentation of crucial accounting facts and information in structured means with

object to aid in formation of managerial policies and routine operations of business entity.”

Management accounting system: A management-accounting system described as operating

framework which aid in generating crucial information that is ultimately assist in formulation of

Every entity in today's competitiveness industry and changing environmental scenario

wants to achieve their defined objectives and targets within scheduled time-frame. Management

in every trade and business enterprise put their efforts towards accomplishment of targets and

other short term goals (Arena and Arnaboldi, 2014). Management accounting is only the crucial

aspect which provide an assistive framework to managerial personnel for attaining goals within

planned time-frame. Management accounting is like full flagged package of all the vital tasks

primarily concerned with both management and accounting aspects.

This study-report emphasises on fundamental and critical aspects of managerial

accounting in context of ABC Limited which is a mid-size entity operating in manufacturing

sector. It also covers necessary requisites of its systems and comprehensive discussion on

different reports used in managerial accounting reporting as well as use of planning-tools in

responding to numerous kind of financial problems. Moreover it consists of comparison of

enterprises in terms of manner of adaption of MA systems and different planning-tools.

TASK 1

P1. Management accounting systems and its essential requirements

Management Accounting: Management or managerial accounting referred as set of

systematic functions which effectively contributes towards detailed tracking and analysis of

internal costs related to multiple business processes which assist a corporation and enterprise in

making of determinations and decisions concerned with productions, core-business operations

and investment & funding in market-place (Azudin and Mansor, 2018)). Enterprises need

managerial accounting and its different aspects to assess efficiency predetermined budgets, costs

of key operations and thereafter efficacious allocation of funds and resources accordingly in

respective departments. Therefore, herein role and function of managerial personnel and

accounting officials is quite significant for business' success.

As per Anglo-American Council of Productivity management accounting is defined as

“Structured presentation of crucial accounting facts and information in structured means with

object to aid in formation of managerial policies and routine operations of business entity.”

Management accounting system: A management-accounting system described as operating

framework which aid in generating crucial information that is ultimately assist in formulation of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

strategies and decisions. MA involves multiple systems which are employed by managing staff

as per business requirements and organisational structure.

Integration of MA-systems within organisation: Core function of managerial

accounting is to provide critical and meaningful information for management's decision making

tasks, which make it necessary to integrate MA systems within enterprise. Since lack of

integration lead to barrier in generation of such information and eventually affects decision

making. In a organisation like ABC limited, accounting processes and division provides useful

information which is used in one or more MA-systems, thus structured integration here is

needed for quick generation of information/data.

Inventory management system

Inventory management system is a system where the accounts for all inventories and

stock are maintain. It is a combination of both hardware and software. The software helps in

keeping the database- entering, storing and editing the data regarding inventories. Where as

hardware are the tools which reads the barcode labels. This system helps ABC limited in

overseeing its inventories, generates report about stocks, do forecast regarding stock ordering,

and the like. Inventory management system essentially required to maintain records regarding

the flow of its inventories for example amount of stocks are in process, amount of finished and

semi finished products, number of stocks kept in warehouse and so forth.

Cost accounting system

Cost accounting system is a framework adopted by the firm for estimating the cost of

their products. Estimating the true and fare value of cost for products is every essential for

profitability analysis, inventory valuation and cost control. Further, this system helps in

estimating the closing value of finished and work-in progress goods for financial statement

preparation (Chenhall and Moers, 2015). The objective of cost accounting system is to ascertain

the cost, true estimation of selling price, cost reduction & control, ascertaining of profit margin,

making cost decision accordingly.

Price optimization system

Price optimisation is the tool / method used to identify the fluctuation in demand of

every increase or decrease in the price of a product. It also control price that company

determines, which will help to achieve the objectives through maximisation of profits. This

system is used for dynamic pricing strategies for hospitality, e-commerce, etc. It provides

as per business requirements and organisational structure.

Integration of MA-systems within organisation: Core function of managerial

accounting is to provide critical and meaningful information for management's decision making

tasks, which make it necessary to integrate MA systems within enterprise. Since lack of

integration lead to barrier in generation of such information and eventually affects decision

making. In a organisation like ABC limited, accounting processes and division provides useful

information which is used in one or more MA-systems, thus structured integration here is

needed for quick generation of information/data.

Inventory management system

Inventory management system is a system where the accounts for all inventories and

stock are maintain. It is a combination of both hardware and software. The software helps in

keeping the database- entering, storing and editing the data regarding inventories. Where as

hardware are the tools which reads the barcode labels. This system helps ABC limited in

overseeing its inventories, generates report about stocks, do forecast regarding stock ordering,

and the like. Inventory management system essentially required to maintain records regarding

the flow of its inventories for example amount of stocks are in process, amount of finished and

semi finished products, number of stocks kept in warehouse and so forth.

Cost accounting system

Cost accounting system is a framework adopted by the firm for estimating the cost of

their products. Estimating the true and fare value of cost for products is every essential for

profitability analysis, inventory valuation and cost control. Further, this system helps in

estimating the closing value of finished and work-in progress goods for financial statement

preparation (Chenhall and Moers, 2015). The objective of cost accounting system is to ascertain

the cost, true estimation of selling price, cost reduction & control, ascertaining of profit margin,

making cost decision accordingly.

Price optimization system

Price optimisation is the tool / method used to identify the fluctuation in demand of

every increase or decrease in the price of a product. It also control price that company

determines, which will help to achieve the objectives through maximisation of profits. This

system is used for dynamic pricing strategies for hospitality, e-commerce, etc. It provides

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

immediate financial benefits by providing opportunities to focus on variety of goals. It maintain

its consistency with efficiency control. This system essentially required to determine initial

pricing, promotional pricing, and markdown (discount) pricing which influence demand. Initial

Price Optimisation works for most durable products. Promotional price optimisation set

fluctuating prices of sales to meet the desired target of the firm through its promotion.

Markdown optimisation helps ABC limited for short duration products, subject to fashion trends

and seasonable – airlines, hotels, retailers and mass merchants.

P2. Different types of management accounting reports

Account Receivable Report : The Account Receivable Aging Report is also known as

“Schedule of Account Receivable”. This report is a record that shows the result of the firm's

clients/ customers who have not cleared their dues for long time and are bound to pay as soon as

possible. Report inform about unpaid invoice balance along with the duration for which they

have been outstanding. It helps the business to keep them on top as they are the slow paying

clients. Aging report is the primary tool which maintain the collection and contain the contact

information for each customer (Fullerton, Kennedy and Widener, 2014). It is also used by

management of ABC limited, to determine the effectiveness of the credit and collection

function. Variation is schedule may contain a simple listing of receivable by customer, rather

than breaking them down further by age. ABC limited uses this report by collection practices,

credit risk and allowance for bad debts.

Performance Report : It is an statement that measures the results of its success over a

specific time frame. It is report, routinely produced by government, being financed by public

money to justify that money was spent effectively and efficiently. Such reports contain

performance indicators which measure achievements of organisation and its programmes.

Performance report measure individual performance of ABC limited employees. Recipient is

expected to take action when there is an unfavourable variance. Performance report can vary

from company to company, whether they maintain same sort of data. Quality of a good

performance report may contain the specific performance and analyse data which provide

suggestion to improve and move forward. Best performance report focus on the organisation

goals with that outline the employee's strength, success, weakness and opportunities. It's required

by ABC limited to set new targets each time while performing tasks.

its consistency with efficiency control. This system essentially required to determine initial

pricing, promotional pricing, and markdown (discount) pricing which influence demand. Initial

Price Optimisation works for most durable products. Promotional price optimisation set

fluctuating prices of sales to meet the desired target of the firm through its promotion.

Markdown optimisation helps ABC limited for short duration products, subject to fashion trends

and seasonable – airlines, hotels, retailers and mass merchants.

P2. Different types of management accounting reports

Account Receivable Report : The Account Receivable Aging Report is also known as

“Schedule of Account Receivable”. This report is a record that shows the result of the firm's

clients/ customers who have not cleared their dues for long time and are bound to pay as soon as

possible. Report inform about unpaid invoice balance along with the duration for which they

have been outstanding. It helps the business to keep them on top as they are the slow paying

clients. Aging report is the primary tool which maintain the collection and contain the contact

information for each customer (Fullerton, Kennedy and Widener, 2014). It is also used by

management of ABC limited, to determine the effectiveness of the credit and collection

function. Variation is schedule may contain a simple listing of receivable by customer, rather

than breaking them down further by age. ABC limited uses this report by collection practices,

credit risk and allowance for bad debts.

Performance Report : It is an statement that measures the results of its success over a

specific time frame. It is report, routinely produced by government, being financed by public

money to justify that money was spent effectively and efficiently. Such reports contain

performance indicators which measure achievements of organisation and its programmes.

Performance report measure individual performance of ABC limited employees. Recipient is

expected to take action when there is an unfavourable variance. Performance report can vary

from company to company, whether they maintain same sort of data. Quality of a good

performance report may contain the specific performance and analyse data which provide

suggestion to improve and move forward. Best performance report focus on the organisation

goals with that outline the employee's strength, success, weakness and opportunities. It's required

by ABC limited to set new targets each time while performing tasks.

Budget Report : This report used in financial management to evaluate difference

between estimated budget projections with actual budget performance occurred in a specific

duration. Budget is an financial goal, which is targeted by a firm to achieve it, through managers

planning , directing and controlling. Actual output after the performance is to be evaluated with

the estimated output, and the difference are to be controlled with the recommendations and

suggestions (Hitomi, 2017). This report is used by ABC limited to determine which expenditure

level are too high, so that actions may be taken to bring the level back down to the budgeted

amount. A modified income statement can be used as a budget report. Financial data is

documented and recorded in a budget report, often referred to as a Financial Report, which can

be brief and simple.

Above mention all reports are used by ABC limited and make sure that it will help

organization to maintain information and take further decisions accordingly.

Benefits of different management accounting systems:

Management

accounting systems

Benefit and application

Cost accounting

system

It is applied in ABC Ltd as it helps managers to determine cost of

different products that are sold by it in the market.

Inventory

management system

The purpose to utilise in ABC Ltd by managers is to maintain inventory

order level because it is beneficial for prevention of product shortage.

Price optimisation Managers of ABC Ltd, use it to determine consumer response on

fluctuating prices,which helps to analyse margin of sales.

Job order costing ABC Ltd's managers use it to keep record of different jobs that are

performed by it as it is advantageous to allocate funding to different

departments according to their requirements.

TASK 2

P3. Calculate net profit by using different costing methods

Marginal Costing: It can be described as the technique of controlling the relationship

between the profit and volume of output. Here, aggregate cost fluctuates the volume of output

between estimated budget projections with actual budget performance occurred in a specific

duration. Budget is an financial goal, which is targeted by a firm to achieve it, through managers

planning , directing and controlling. Actual output after the performance is to be evaluated with

the estimated output, and the difference are to be controlled with the recommendations and

suggestions (Hitomi, 2017). This report is used by ABC limited to determine which expenditure

level are too high, so that actions may be taken to bring the level back down to the budgeted

amount. A modified income statement can be used as a budget report. Financial data is

documented and recorded in a budget report, often referred to as a Financial Report, which can

be brief and simple.

Above mention all reports are used by ABC limited and make sure that it will help

organization to maintain information and take further decisions accordingly.

Benefits of different management accounting systems:

Management

accounting systems

Benefit and application

Cost accounting

system

It is applied in ABC Ltd as it helps managers to determine cost of

different products that are sold by it in the market.

Inventory

management system

The purpose to utilise in ABC Ltd by managers is to maintain inventory

order level because it is beneficial for prevention of product shortage.

Price optimisation Managers of ABC Ltd, use it to determine consumer response on

fluctuating prices,which helps to analyse margin of sales.

Job order costing ABC Ltd's managers use it to keep record of different jobs that are

performed by it as it is advantageous to allocate funding to different

departments according to their requirements.

TASK 2

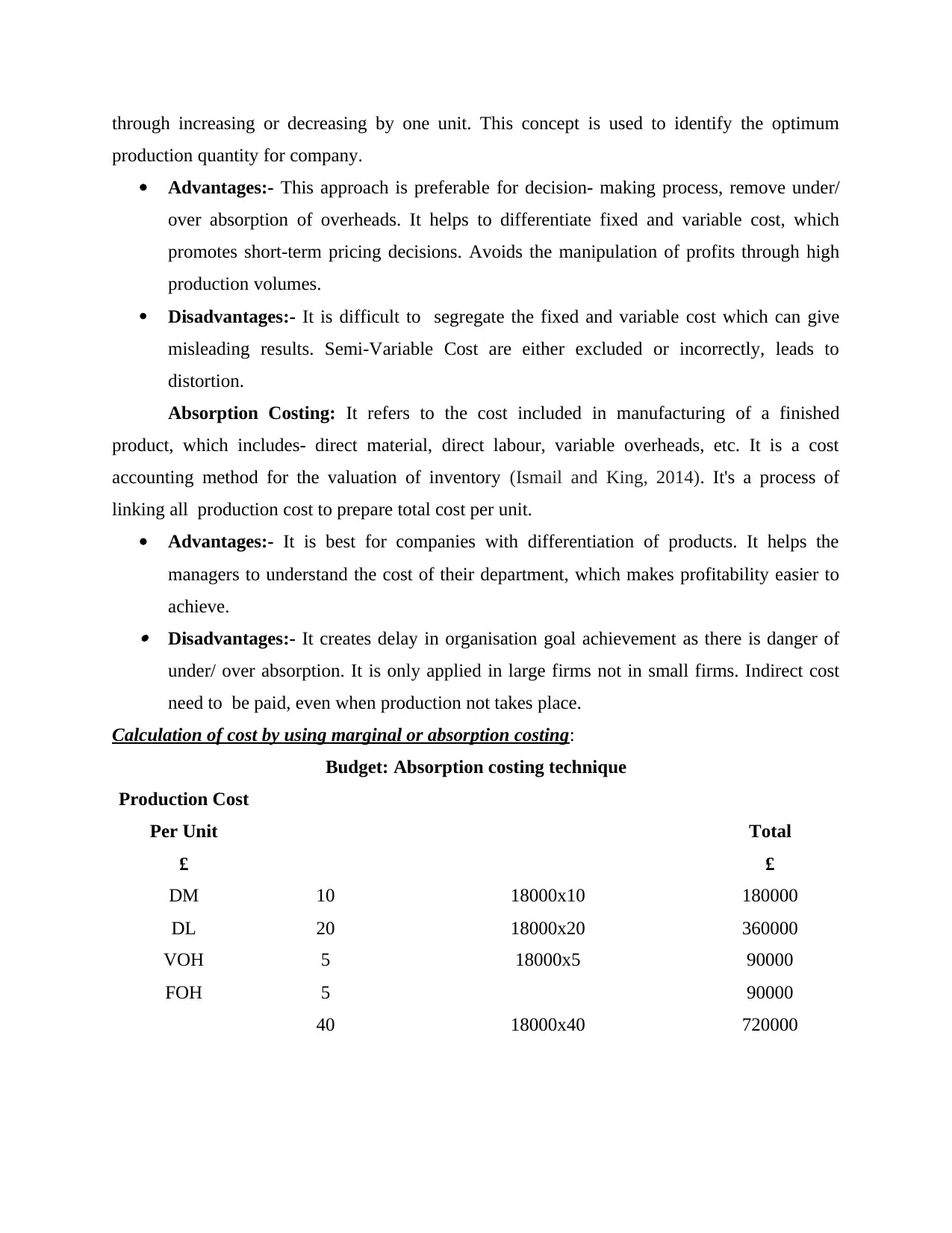

P3. Calculate net profit by using different costing methods

Marginal Costing: It can be described as the technique of controlling the relationship

between the profit and volume of output. Here, aggregate cost fluctuates the volume of output

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

through increasing or decreasing by one unit. This concept is used to identify the optimum

production quantity for company.

Advantages:- This approach is preferable for decision- making process, remove under/

over absorption of overheads. It helps to differentiate fixed and variable cost, which

promotes short-term pricing decisions. Avoids the manipulation of profits through high

production volumes.

Disadvantages:- It is difficult to segregate the fixed and variable cost which can give

misleading results. Semi-Variable Cost are either excluded or incorrectly, leads to

distortion.

Absorption Costing: It refers to the cost included in manufacturing of a finished

product, which includes- direct material, direct labour, variable overheads, etc. It is a cost

accounting method for the valuation of inventory (Ismail and King, 2014). It's a process of

linking all production cost to prepare total cost per unit.

Advantages:- It is best for companies with differentiation of products. It helps the

managers to understand the cost of their department, which makes profitability easier to

achieve. Disadvantages:- It creates delay in organisation goal achievement as there is danger of

under/ over absorption. It is only applied in large firms not in small firms. Indirect cost

need to be paid, even when production not takes place.

Calculation of cost by using marginal or absorption costing:

Budget: Absorption costing technique

Production Cost

Per Unit Total

£ £

DM 10 18000x10 180000

DL 20 18000x20 360000

VOH 5 18000x5 90000

FOH 5 90000

40 18000x40 720000

production quantity for company.

Advantages:- This approach is preferable for decision- making process, remove under/

over absorption of overheads. It helps to differentiate fixed and variable cost, which

promotes short-term pricing decisions. Avoids the manipulation of profits through high

production volumes.

Disadvantages:- It is difficult to segregate the fixed and variable cost which can give

misleading results. Semi-Variable Cost are either excluded or incorrectly, leads to

distortion.

Absorption Costing: It refers to the cost included in manufacturing of a finished

product, which includes- direct material, direct labour, variable overheads, etc. It is a cost

accounting method for the valuation of inventory (Ismail and King, 2014). It's a process of

linking all production cost to prepare total cost per unit.

Advantages:- It is best for companies with differentiation of products. It helps the

managers to understand the cost of their department, which makes profitability easier to

achieve. Disadvantages:- It creates delay in organisation goal achievement as there is danger of

under/ over absorption. It is only applied in large firms not in small firms. Indirect cost

need to be paid, even when production not takes place.

Calculation of cost by using marginal or absorption costing:

Budget: Absorption costing technique

Production Cost

Per Unit Total

£ £

DM 10 18000x10 180000

DL 20 18000x20 360000

VOH 5 18000x5 90000

FOH 5 90000

40 18000x40 720000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

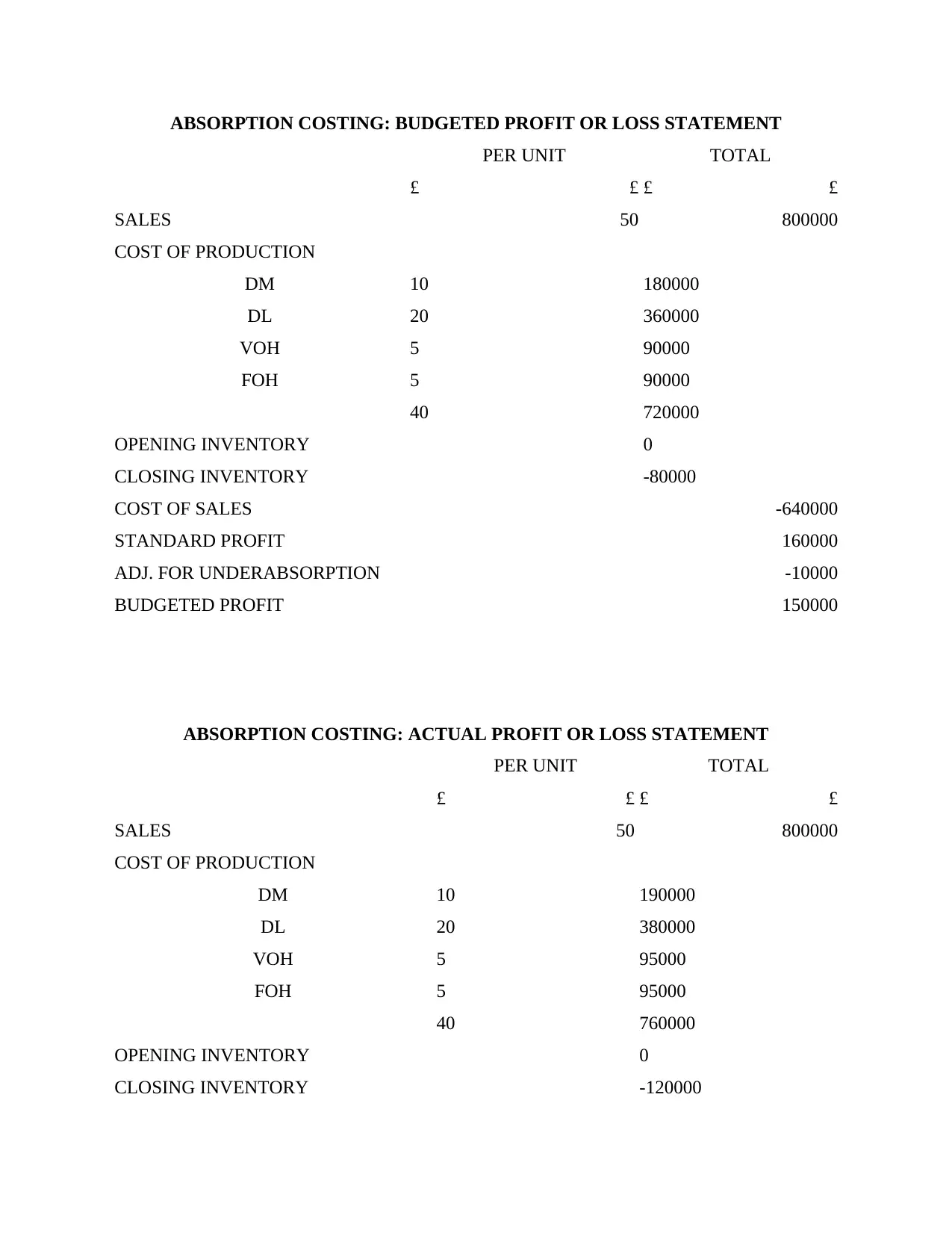

ABSORPTION COSTING: BUDGETED PROFIT OR LOSS STATEMENT

PER UNIT TOTAL

£ £ £ £

SALES 50 800000

COST OF PRODUCTION

DM 10 180000

DL 20 360000

VOH 5 90000

FOH 5 90000

40 720000

OPENING INVENTORY 0

CLOSING INVENTORY -80000

COST OF SALES -640000

STANDARD PROFIT 160000

ADJ. FOR UNDERABSORPTION -10000

BUDGETED PROFIT 150000

ABSORPTION COSTING: ACTUAL PROFIT OR LOSS STATEMENT

PER UNIT TOTAL

£ £ £ £

SALES 50 800000

COST OF PRODUCTION

DM 10 190000

DL 20 380000

VOH 5 95000

FOH 5 95000

40 760000

OPENING INVENTORY 0

CLOSING INVENTORY -120000

PER UNIT TOTAL

£ £ £ £

SALES 50 800000

COST OF PRODUCTION

DM 10 180000

DL 20 360000

VOH 5 90000

FOH 5 90000

40 720000

OPENING INVENTORY 0

CLOSING INVENTORY -80000

COST OF SALES -640000

STANDARD PROFIT 160000

ADJ. FOR UNDERABSORPTION -10000

BUDGETED PROFIT 150000

ABSORPTION COSTING: ACTUAL PROFIT OR LOSS STATEMENT

PER UNIT TOTAL

£ £ £ £

SALES 50 800000

COST OF PRODUCTION

DM 10 190000

DL 20 380000

VOH 5 95000

FOH 5 95000

40 760000

OPENING INVENTORY 0

CLOSING INVENTORY -120000

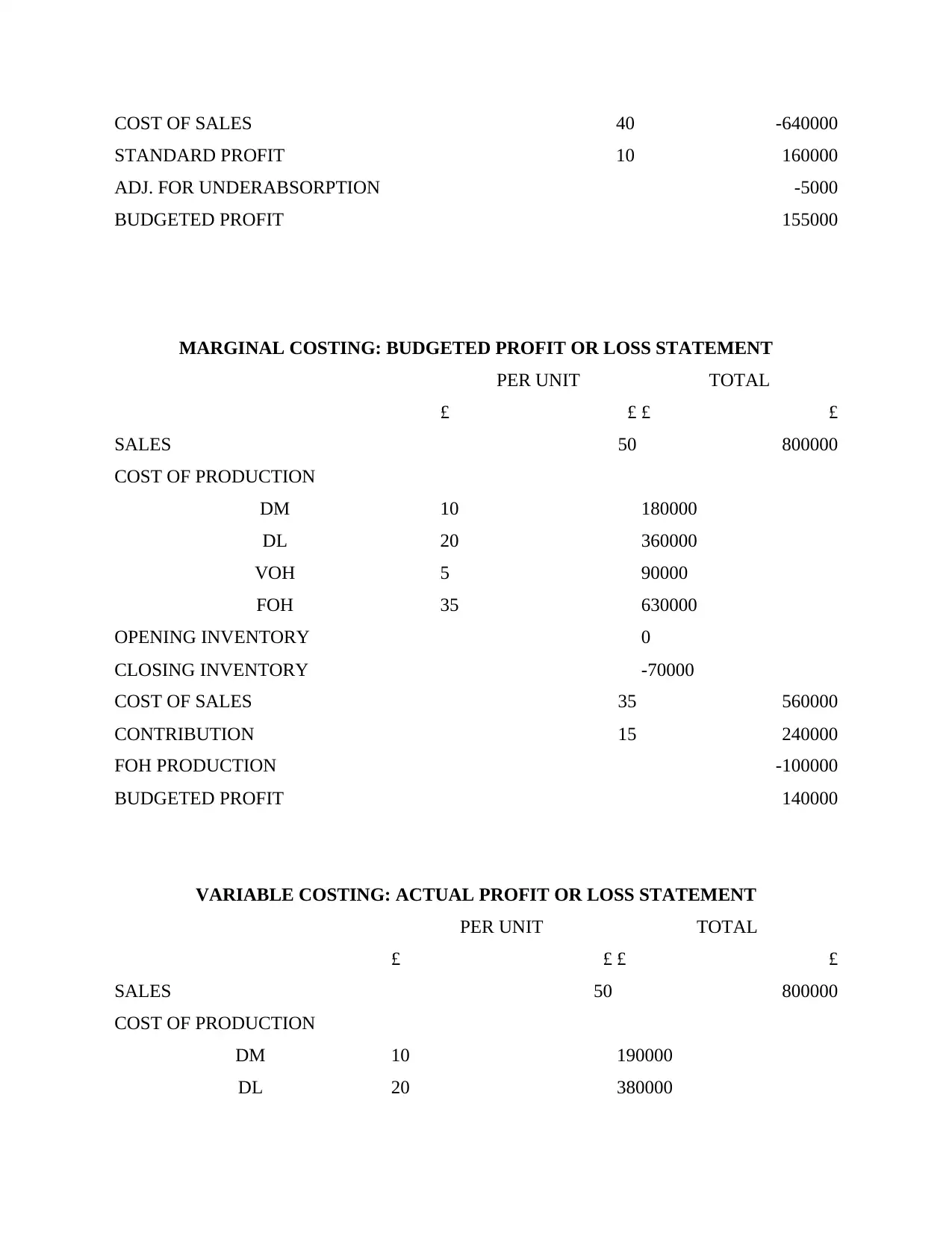

COST OF SALES 40 -640000

STANDARD PROFIT 10 160000

ADJ. FOR UNDERABSORPTION -5000

BUDGETED PROFIT 155000

MARGINAL COSTING: BUDGETED PROFIT OR LOSS STATEMENT

PER UNIT TOTAL

£ £ £ £

SALES 50 800000

COST OF PRODUCTION

DM 10 180000

DL 20 360000

VOH 5 90000

FOH 35 630000

OPENING INVENTORY 0

CLOSING INVENTORY -70000

COST OF SALES 35 560000

CONTRIBUTION 15 240000

FOH PRODUCTION -100000

BUDGETED PROFIT 140000

VARIABLE COSTING: ACTUAL PROFIT OR LOSS STATEMENT

PER UNIT TOTAL

£ £ £ £

SALES 50 800000

COST OF PRODUCTION

DM 10 190000

DL 20 380000

STANDARD PROFIT 10 160000

ADJ. FOR UNDERABSORPTION -5000

BUDGETED PROFIT 155000

MARGINAL COSTING: BUDGETED PROFIT OR LOSS STATEMENT

PER UNIT TOTAL

£ £ £ £

SALES 50 800000

COST OF PRODUCTION

DM 10 180000

DL 20 360000

VOH 5 90000

FOH 35 630000

OPENING INVENTORY 0

CLOSING INVENTORY -70000

COST OF SALES 35 560000

CONTRIBUTION 15 240000

FOH PRODUCTION -100000

BUDGETED PROFIT 140000

VARIABLE COSTING: ACTUAL PROFIT OR LOSS STATEMENT

PER UNIT TOTAL

£ £ £ £

SALES 50 800000

COST OF PRODUCTION

DM 10 190000

DL 20 380000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

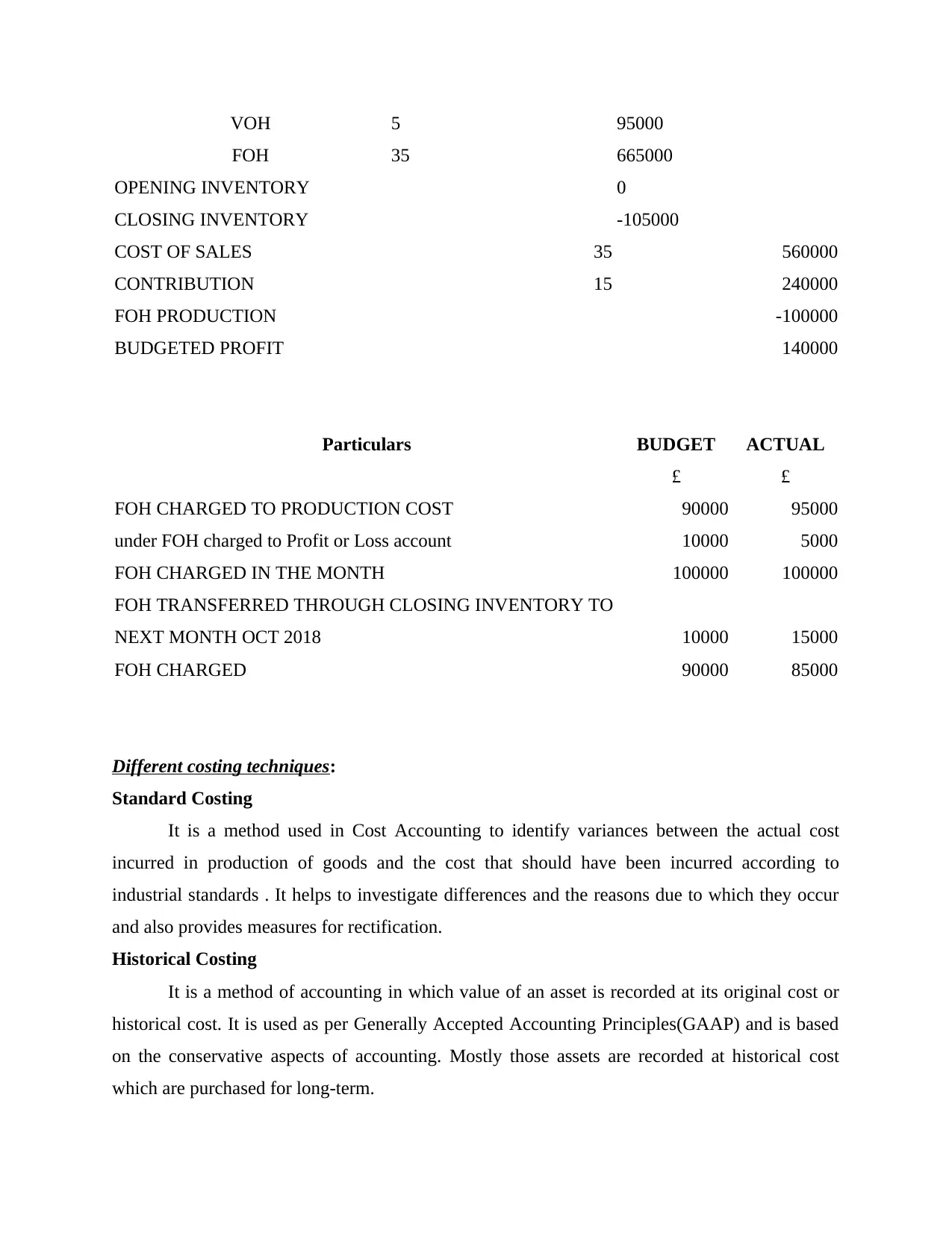

VOH 5 95000

FOH 35 665000

OPENING INVENTORY 0

CLOSING INVENTORY -105000

COST OF SALES 35 560000

CONTRIBUTION 15 240000

FOH PRODUCTION -100000

BUDGETED PROFIT 140000

Particulars BUDGET ACTUAL

£ £

FOH CHARGED TO PRODUCTION COST 90000 95000

under FOH charged to Profit or Loss account 10000 5000

FOH CHARGED IN THE MONTH 100000 100000

FOH TRANSFERRED THROUGH CLOSING INVENTORY TO

NEXT MONTH OCT 2018 10000 15000

FOH CHARGED 90000 85000

Different costing techniques:

Standard Costing

It is a method used in Cost Accounting to identify variances between the actual cost

incurred in production of goods and the cost that should have been incurred according to

industrial standards . It helps to investigate differences and the reasons due to which they occur

and also provides measures for rectification.

Historical Costing

It is a method of accounting in which value of an asset is recorded at its original cost or

historical cost. It is used as per Generally Accepted Accounting Principles(GAAP) and is based

on the conservative aspects of accounting. Mostly those assets are recorded at historical cost

which are purchased for long-term.

FOH 35 665000

OPENING INVENTORY 0

CLOSING INVENTORY -105000

COST OF SALES 35 560000

CONTRIBUTION 15 240000

FOH PRODUCTION -100000

BUDGETED PROFIT 140000

Particulars BUDGET ACTUAL

£ £

FOH CHARGED TO PRODUCTION COST 90000 95000

under FOH charged to Profit or Loss account 10000 5000

FOH CHARGED IN THE MONTH 100000 100000

FOH TRANSFERRED THROUGH CLOSING INVENTORY TO

NEXT MONTH OCT 2018 10000 15000

FOH CHARGED 90000 85000

Different costing techniques:

Standard Costing

It is a method used in Cost Accounting to identify variances between the actual cost

incurred in production of goods and the cost that should have been incurred according to

industrial standards . It helps to investigate differences and the reasons due to which they occur

and also provides measures for rectification.

Historical Costing

It is a method of accounting in which value of an asset is recorded at its original cost or

historical cost. It is used as per Generally Accepted Accounting Principles(GAAP) and is based

on the conservative aspects of accounting. Mostly those assets are recorded at historical cost

which are purchased for long-term.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

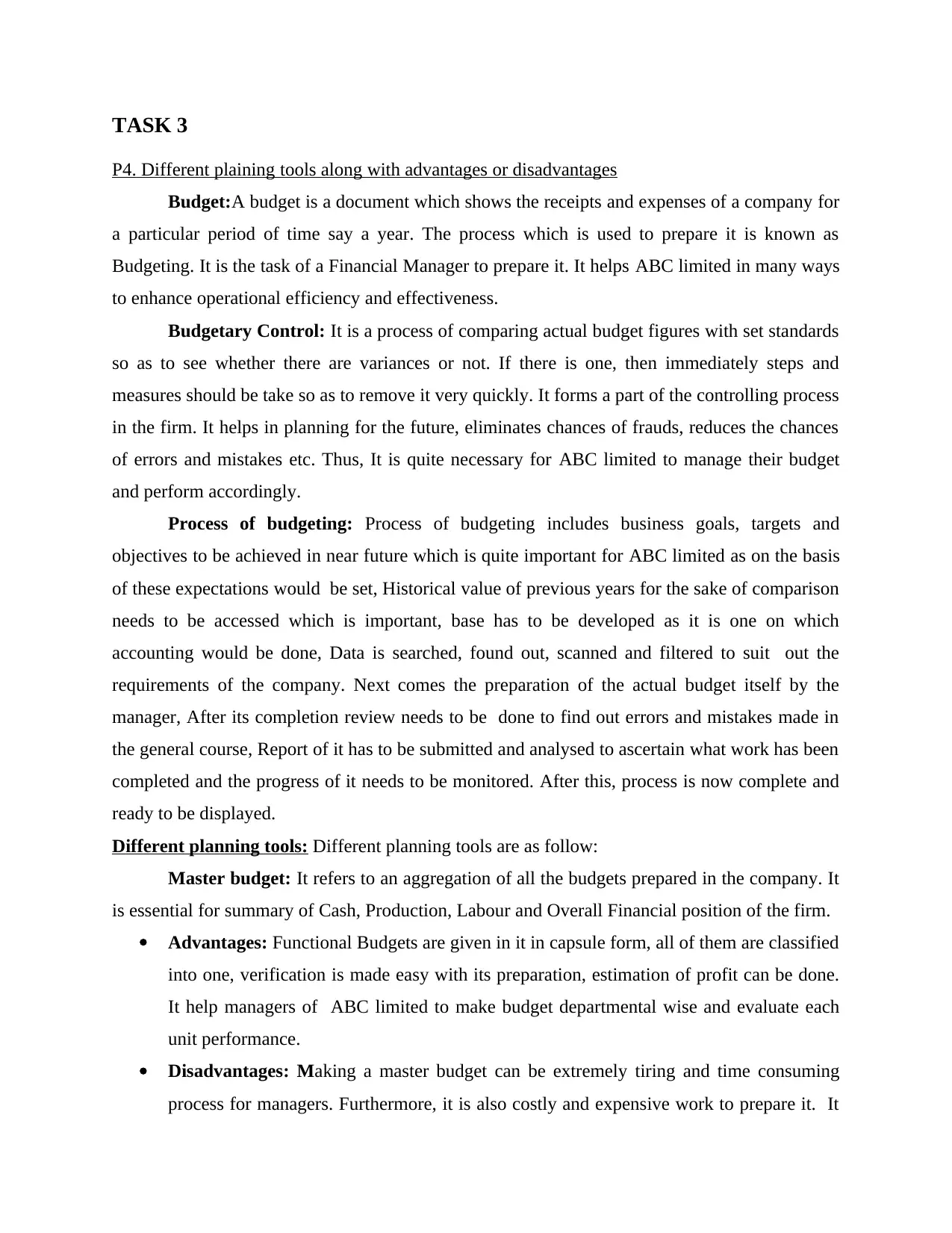

TASK 3

P4. Different plaining tools along with advantages or disadvantages

Budget:A budget is a document which shows the receipts and expenses of a company for

a particular period of time say a year. The process which is used to prepare it is known as

Budgeting. It is the task of a Financial Manager to prepare it. It helps ABC limited in many ways

to enhance operational efficiency and effectiveness.

Budgetary Control: It is a process of comparing actual budget figures with set standards

so as to see whether there are variances or not. If there is one, then immediately steps and

measures should be take so as to remove it very quickly. It forms a part of the controlling process

in the firm. It helps in planning for the future, eliminates chances of frauds, reduces the chances

of errors and mistakes etc. Thus, It is quite necessary for ABC limited to manage their budget

and perform accordingly.

Process of budgeting: Process of budgeting includes business goals, targets and

objectives to be achieved in near future which is quite important for ABC limited as on the basis

of these expectations would be set, Historical value of previous years for the sake of comparison

needs to be accessed which is important, base has to be developed as it is one on which

accounting would be done, Data is searched, found out, scanned and filtered to suit out the

requirements of the company. Next comes the preparation of the actual budget itself by the

manager, After its completion review needs to be done to find out errors and mistakes made in

the general course, Report of it has to be submitted and analysed to ascertain what work has been

completed and the progress of it needs to be monitored. After this, process is now complete and

ready to be displayed.

Different planning tools: Different planning tools are as follow:

Master budget: It refers to an aggregation of all the budgets prepared in the company. It

is essential for summary of Cash, Production, Labour and Overall Financial position of the firm.

Advantages: Functional Budgets are given in it in capsule form, all of them are classified

into one, verification is made easy with its preparation, estimation of profit can be done.

It help managers of ABC limited to make budget departmental wise and evaluate each

unit performance.

Disadvantages: Making a master budget can be extremely tiring and time consuming

process for managers. Furthermore, it is also costly and expensive work to prepare it. It

P4. Different plaining tools along with advantages or disadvantages

Budget:A budget is a document which shows the receipts and expenses of a company for

a particular period of time say a year. The process which is used to prepare it is known as

Budgeting. It is the task of a Financial Manager to prepare it. It helps ABC limited in many ways

to enhance operational efficiency and effectiveness.

Budgetary Control: It is a process of comparing actual budget figures with set standards

so as to see whether there are variances or not. If there is one, then immediately steps and

measures should be take so as to remove it very quickly. It forms a part of the controlling process

in the firm. It helps in planning for the future, eliminates chances of frauds, reduces the chances

of errors and mistakes etc. Thus, It is quite necessary for ABC limited to manage their budget

and perform accordingly.

Process of budgeting: Process of budgeting includes business goals, targets and

objectives to be achieved in near future which is quite important for ABC limited as on the basis

of these expectations would be set, Historical value of previous years for the sake of comparison

needs to be accessed which is important, base has to be developed as it is one on which

accounting would be done, Data is searched, found out, scanned and filtered to suit out the

requirements of the company. Next comes the preparation of the actual budget itself by the

manager, After its completion review needs to be done to find out errors and mistakes made in

the general course, Report of it has to be submitted and analysed to ascertain what work has been

completed and the progress of it needs to be monitored. After this, process is now complete and

ready to be displayed.

Different planning tools: Different planning tools are as follow:

Master budget: It refers to an aggregation of all the budgets prepared in the company. It

is essential for summary of Cash, Production, Labour and Overall Financial position of the firm.

Advantages: Functional Budgets are given in it in capsule form, all of them are classified

into one, verification is made easy with its preparation, estimation of profit can be done.

It help managers of ABC limited to make budget departmental wise and evaluate each

unit performance.

Disadvantages: Making a master budget can be extremely tiring and time consuming

process for managers. Furthermore, it is also costly and expensive work to prepare it. It

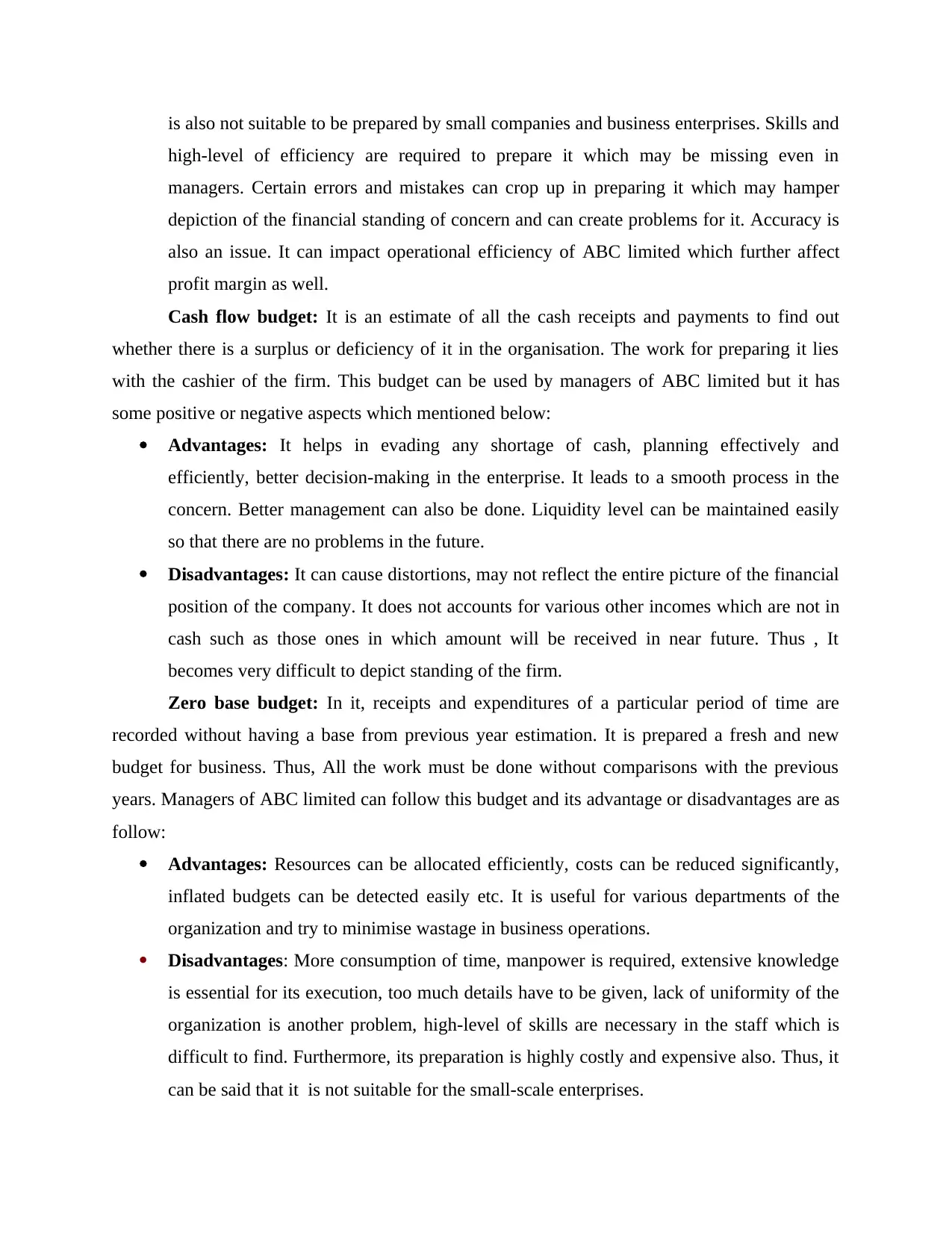

is also not suitable to be prepared by small companies and business enterprises. Skills and

high-level of efficiency are required to prepare it which may be missing even in

managers. Certain errors and mistakes can crop up in preparing it which may hamper

depiction of the financial standing of concern and can create problems for it. Accuracy is

also an issue. It can impact operational efficiency of ABC limited which further affect

profit margin as well.

Cash flow budget: It is an estimate of all the cash receipts and payments to find out

whether there is a surplus or deficiency of it in the organisation. The work for preparing it lies

with the cashier of the firm. This budget can be used by managers of ABC limited but it has

some positive or negative aspects which mentioned below:

Advantages: It helps in evading any shortage of cash, planning effectively and

efficiently, better decision-making in the enterprise. It leads to a smooth process in the

concern. Better management can also be done. Liquidity level can be maintained easily

so that there are no problems in the future.

Disadvantages: It can cause distortions, may not reflect the entire picture of the financial

position of the company. It does not accounts for various other incomes which are not in

cash such as those ones in which amount will be received in near future. Thus , It

becomes very difficult to depict standing of the firm.

Zero base budget: In it, receipts and expenditures of a particular period of time are

recorded without having a base from previous year estimation. It is prepared a fresh and new

budget for business. Thus, All the work must be done without comparisons with the previous

years. Managers of ABC limited can follow this budget and its advantage or disadvantages are as

follow:

Advantages: Resources can be allocated efficiently, costs can be reduced significantly,

inflated budgets can be detected easily etc. It is useful for various departments of the

organization and try to minimise wastage in business operations.

Disadvantages: More consumption of time, manpower is required, extensive knowledge

is essential for its execution, too much details have to be given, lack of uniformity of the

organization is another problem, high-level of skills are necessary in the staff which is

difficult to find. Furthermore, its preparation is highly costly and expensive also. Thus, it

can be said that it is not suitable for the small-scale enterprises.

high-level of efficiency are required to prepare it which may be missing even in

managers. Certain errors and mistakes can crop up in preparing it which may hamper

depiction of the financial standing of concern and can create problems for it. Accuracy is

also an issue. It can impact operational efficiency of ABC limited which further affect

profit margin as well.

Cash flow budget: It is an estimate of all the cash receipts and payments to find out

whether there is a surplus or deficiency of it in the organisation. The work for preparing it lies

with the cashier of the firm. This budget can be used by managers of ABC limited but it has

some positive or negative aspects which mentioned below:

Advantages: It helps in evading any shortage of cash, planning effectively and

efficiently, better decision-making in the enterprise. It leads to a smooth process in the

concern. Better management can also be done. Liquidity level can be maintained easily

so that there are no problems in the future.

Disadvantages: It can cause distortions, may not reflect the entire picture of the financial

position of the company. It does not accounts for various other incomes which are not in

cash such as those ones in which amount will be received in near future. Thus , It

becomes very difficult to depict standing of the firm.

Zero base budget: In it, receipts and expenditures of a particular period of time are

recorded without having a base from previous year estimation. It is prepared a fresh and new

budget for business. Thus, All the work must be done without comparisons with the previous

years. Managers of ABC limited can follow this budget and its advantage or disadvantages are as

follow:

Advantages: Resources can be allocated efficiently, costs can be reduced significantly,

inflated budgets can be detected easily etc. It is useful for various departments of the

organization and try to minimise wastage in business operations.

Disadvantages: More consumption of time, manpower is required, extensive knowledge

is essential for its execution, too much details have to be given, lack of uniformity of the

organization is another problem, high-level of skills are necessary in the staff which is

difficult to find. Furthermore, its preparation is highly costly and expensive also. Thus, it

can be said that it is not suitable for the small-scale enterprises.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.