Management Accounting Report: Planning Tools and Analysis

VerifiedAdded on 2021/01/02

|16

|4489

|59

Report

AI Summary

This report delves into the realm of management accounting, exploring its significance in organizational financial management. It begins with an introduction to management accounting systems, encompassing inventory management, cost accounting, and job costing. The report then examines various management accounting techniques such as marginal and absorption costing, accompanied by budgeted and actual income statements. Furthermore, it analyzes the advantages and disadvantages of planning tools used in budgetary control, like zero-base budgeting and flexible budgeting, highlighting their role in resource allocation and cost control. The report also investigates how management accounting can be utilized to address financial problems, providing insights into the ways organizations, such as ABC Ltd, can leverage these principles to achieve their goals. Finally, the report concludes by emphasizing the importance of effective reporting and accounting functions in driving business success, fostering accountability, and improving overall organizational performance.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

LO 1.................................................................................................................................................1

Management accounting system..................................................................................................1

LO2..................................................................................................................................................4

TASK 3............................................................................................................................................7

Advantages and disadvantages of the planning tools used in budgetary control.........................7

Use of different planning tools and their application...................................................................7

TASK 4............................................................................................................................................9

Using management accounting system to solve financial problems...........................................9

Analysis of how management accounting leads the organization to success............................10

Evaluation of planning tools in solving the financial problems................................................11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

LO 1.................................................................................................................................................1

Management accounting system..................................................................................................1

LO2..................................................................................................................................................4

TASK 3............................................................................................................................................7

Advantages and disadvantages of the planning tools used in budgetary control.........................7

Use of different planning tools and their application...................................................................7

TASK 4............................................................................................................................................9

Using management accounting system to solve financial problems...........................................9

Analysis of how management accounting leads the organization to success............................10

Evaluation of planning tools in solving the financial problems................................................11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

INTRODUCTION

Management accounting is the managing of the accounts any organization. It involves

recording and interpreting the data relating to company. The management accounting is useful to

all levels in organization which includes lower level to the top management staff in company.

Where management accounting involves the recording of data on the daily basis, management

reporting includes presenting of accounting reports to top management. Management report can

include budget report, job-cost report, account receivable reports and inventory management

report.

The report will include management accounting systems. Also, the various management

accounting techniques which are-margin analysis, constraint analysis, capital budgeting,

inventory valuation and product costing (Shahzadi and et.al., 2018).

Further the report includes the use of planning tools which are widely used in

management accounting and the benefits of using management accounting in the course of

business. Also, the report will study about the ways in which organization can use management

accounting to respond to companies financial problem. Also, the management accounting is used

in organization ABC Ltd. In order to achieve its organization goals.

LO 1

Management accounting system

Management accounting-

Management accounting is the process of analysing and evaluating cost of operating any

business. It relates to maintaining of records, report and accounts of business. In the management

accounting process there is management of the affairs of the company. This management of the

accounts by managers help them to take management as well as financial decisions (Bruno and

Lapsley, 2018). The management accounting involves the collection of data through the daily

recording of data, evaluation of the data and preparing reports on the given data. The

management accounting helps in the accumulation of the relevant data to assist the functions of

the company and achieve its organization goals.

Types of management accounting systems-

The management accounting system have many types which are as follows- Inventory management system- this involves the management of the inventory in the

business through the recording of the inflow and outflow of the raw material and finished

1

Management accounting is the managing of the accounts any organization. It involves

recording and interpreting the data relating to company. The management accounting is useful to

all levels in organization which includes lower level to the top management staff in company.

Where management accounting involves the recording of data on the daily basis, management

reporting includes presenting of accounting reports to top management. Management report can

include budget report, job-cost report, account receivable reports and inventory management

report.

The report will include management accounting systems. Also, the various management

accounting techniques which are-margin analysis, constraint analysis, capital budgeting,

inventory valuation and product costing (Shahzadi and et.al., 2018).

Further the report includes the use of planning tools which are widely used in

management accounting and the benefits of using management accounting in the course of

business. Also, the report will study about the ways in which organization can use management

accounting to respond to companies financial problem. Also, the management accounting is used

in organization ABC Ltd. In order to achieve its organization goals.

LO 1

Management accounting system

Management accounting-

Management accounting is the process of analysing and evaluating cost of operating any

business. It relates to maintaining of records, report and accounts of business. In the management

accounting process there is management of the affairs of the company. This management of the

accounts by managers help them to take management as well as financial decisions (Bruno and

Lapsley, 2018). The management accounting involves the collection of data through the daily

recording of data, evaluation of the data and preparing reports on the given data. The

management accounting helps in the accumulation of the relevant data to assist the functions of

the company and achieve its organization goals.

Types of management accounting systems-

The management accounting system have many types which are as follows- Inventory management system- this involves the management of the inventory in the

business through the recording of the inflow and outflow of the raw material and finished

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

goods. This helps in the planning of the production of goods by production department

(Hald and Thrane, 2016). Cost Accounting System- it refers to the recording of the cost of production of any

product. The flow of the goods are to evaluated so that there is proper flow of goods in

the company (Nielsen, Mitchell and Nørreklit, 2015). Job Costing System- the job costing relates to the estimation of cost of every job in the

production process to ascertain the actual cost of producing the product (Akkermans and

Van Oorschot, 2018).

Price optimization system- this relates to the setting of the price at maximum level which

is accepted by the customer and the customer is satisfied (Shahzadi and et.al., 2018).

Also, the price is suitable to company.

Accounting reporting-

The management reporting involves the recording of the data on daily basis by the

operation management, and analysing the recording data (McLean, McGovern and Davie,

2015). After analysing the data is than interpret to the structure is required by the management.

The management usually uses this data in decision making, forming plans and policies. An

owner and manager may request reports on quarterly ,monthly, weekly and daily basis.

Methods used for management accounting reporting-

There are mainly four methods used in the management accounting reporting which are as

follows-11 Budget Report- Budget reports are prepared by mangers to evaluate the cost of incurred

in running of the business and comparing it with the estimated cost (Järvinen, 2016). The

budget reports helps in the determining the cost for the future products to be

manufactured.11 Accounts Receivable ageing reports- the accounts receivable reports shows the cash flow

within the company. With the help of accounts receivables managers can find the

problem in the collection of funds (Bruno and Lapsley, 2018). By the continuous

evaluation of the accounts receivable reports the company can handle its collections

effectively and there can be no overlooking of the debtors.11 Job cost reports- these reports are prepared in relation to a specific projects. This helps in

comparing of the actual cost incurred to estimated cost of that project (Hald and Thrane,

2

(Hald and Thrane, 2016). Cost Accounting System- it refers to the recording of the cost of production of any

product. The flow of the goods are to evaluated so that there is proper flow of goods in

the company (Nielsen, Mitchell and Nørreklit, 2015). Job Costing System- the job costing relates to the estimation of cost of every job in the

production process to ascertain the actual cost of producing the product (Akkermans and

Van Oorschot, 2018).

Price optimization system- this relates to the setting of the price at maximum level which

is accepted by the customer and the customer is satisfied (Shahzadi and et.al., 2018).

Also, the price is suitable to company.

Accounting reporting-

The management reporting involves the recording of the data on daily basis by the

operation management, and analysing the recording data (McLean, McGovern and Davie,

2015). After analysing the data is than interpret to the structure is required by the management.

The management usually uses this data in decision making, forming plans and policies. An

owner and manager may request reports on quarterly ,monthly, weekly and daily basis.

Methods used for management accounting reporting-

There are mainly four methods used in the management accounting reporting which are as

follows-11 Budget Report- Budget reports are prepared by mangers to evaluate the cost of incurred

in running of the business and comparing it with the estimated cost (Järvinen, 2016). The

budget reports helps in the determining the cost for the future products to be

manufactured.11 Accounts Receivable ageing reports- the accounts receivable reports shows the cash flow

within the company. With the help of accounts receivables managers can find the

problem in the collection of funds (Bruno and Lapsley, 2018). By the continuous

evaluation of the accounts receivable reports the company can handle its collections

effectively and there can be no overlooking of the debtors.11 Job cost reports- these reports are prepared in relation to a specific projects. This helps in

comparing of the actual cost incurred to estimated cost of that project (Hald and Thrane,

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2016). By evaluation of the project cost the company can acquire control on the expenses

of the projects.

11 Inventory and manufacturing- companies having physical inventory can use this

accounting reporting. This makes the manufacturing process more effective. These

reports include items such as inventory wastage, hourly labour cost or per-unit overhead

costs (Nielsen, Mitchell and Nørreklit, 2015). From this manager can check the

performances of the various departments and decide whether to give bonus or direct them

to improve. This helps company in accomplishing manufacturing and inventory goals of

company.

Benefits of management accounting

Management accounting is the major function in company which makes working of

company easy and effective. These are the benefits of management accounting- Planning- through the use of management accounting the management can make plans

by using data and execute the plans by checking it regularly (Akkermans and Van

Oorschot, 2018). Controlling- as the management accounting requires the preparation of reports on timely

basis there can be tight control on the operation of the superior staff by management

(McLean, McGovern and Davie, 2015). Service to customers- good and improved services can be acquired by management to

customers by making the accounting system strong (Shahzadi and et.al., 2018). Organizing – as the management accounting involves the division of work between

various authorities it helps the authorities in knowing the responsibility and acting

accordingly (Järvinen, 2016). Coordinating- it is the process of working together in organization. Thus there is perfect

coordination between production, purchase, finance, personnel and sales department. Improvement of efficiency- by the recording and reporting of data on proper time there is

data availability at any time when needed which increases the functionality of task there

by improving efficiency of organization (Bruno and Lapsley, 2018). Motivating- it helps to maintain high degree of motivation in organization. The report of

operation of company is submitted to management periodically which determines the

3

of the projects.

11 Inventory and manufacturing- companies having physical inventory can use this

accounting reporting. This makes the manufacturing process more effective. These

reports include items such as inventory wastage, hourly labour cost or per-unit overhead

costs (Nielsen, Mitchell and Nørreklit, 2015). From this manager can check the

performances of the various departments and decide whether to give bonus or direct them

to improve. This helps company in accomplishing manufacturing and inventory goals of

company.

Benefits of management accounting

Management accounting is the major function in company which makes working of

company easy and effective. These are the benefits of management accounting- Planning- through the use of management accounting the management can make plans

by using data and execute the plans by checking it regularly (Akkermans and Van

Oorschot, 2018). Controlling- as the management accounting requires the preparation of reports on timely

basis there can be tight control on the operation of the superior staff by management

(McLean, McGovern and Davie, 2015). Service to customers- good and improved services can be acquired by management to

customers by making the accounting system strong (Shahzadi and et.al., 2018). Organizing – as the management accounting involves the division of work between

various authorities it helps the authorities in knowing the responsibility and acting

accordingly (Järvinen, 2016). Coordinating- it is the process of working together in organization. Thus there is perfect

coordination between production, purchase, finance, personnel and sales department. Improvement of efficiency- by the recording and reporting of data on proper time there is

data availability at any time when needed which increases the functionality of task there

by improving efficiency of organization (Bruno and Lapsley, 2018). Motivating- it helps to maintain high degree of motivation in organization. The report of

operation of company is submitted to management periodically which determines the

3

working of employee (Hald and Thrane, 2016). Based on this report management

promotes good working staff which motivates them to work. Communication- through the management accounting there is two way communication

system. The top management plans and delegates work to lower staff. Also, lower staff

prepares reports and submit it to top management (Nielsen, Mitchell and Nørreklit,

2015). This two way communication induces sense of responsibility and also improves

work conditions. Regulation of Business activities- proper planning, organizing, coordination and

motivation can bring systematic regularity in business activities (Akkermans and Van

Oorschot, 2018).

Maximization of Profit – there is systematic management of work, improved morale of

employee and proper action by management helps in maximising profit of organization

which is good for its progress and achievement of goals (Shahzadi and et.al., 2018).

Thus the reporting and accounting functions in business are important. There is easy flow

of information through reporting and accounting and there can be achievement of goals by

company. This improves responsibility, accountability and present-ability in organization.

LO2

a) Marginal Costing

Budgeted Income Statement

Particulars Amount

Sales (16000 units @ £50 per unit) £800000

Less- Variable Cost @ £35 per unit (£560000)

Contribution £240000

Less- Fixed Cost (£100000)

Profit £140000

Actual Income Statement

4

promotes good working staff which motivates them to work. Communication- through the management accounting there is two way communication

system. The top management plans and delegates work to lower staff. Also, lower staff

prepares reports and submit it to top management (Nielsen, Mitchell and Nørreklit,

2015). This two way communication induces sense of responsibility and also improves

work conditions. Regulation of Business activities- proper planning, organizing, coordination and

motivation can bring systematic regularity in business activities (Akkermans and Van

Oorschot, 2018).

Maximization of Profit – there is systematic management of work, improved morale of

employee and proper action by management helps in maximising profit of organization

which is good for its progress and achievement of goals (Shahzadi and et.al., 2018).

Thus the reporting and accounting functions in business are important. There is easy flow

of information through reporting and accounting and there can be achievement of goals by

company. This improves responsibility, accountability and present-ability in organization.

LO2

a) Marginal Costing

Budgeted Income Statement

Particulars Amount

Sales (16000 units @ £50 per unit) £800000

Less- Variable Cost @ £35 per unit (£560000)

Contribution £240000

Less- Fixed Cost (£100000)

Profit £140000

Actual Income Statement

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Particulars Amount

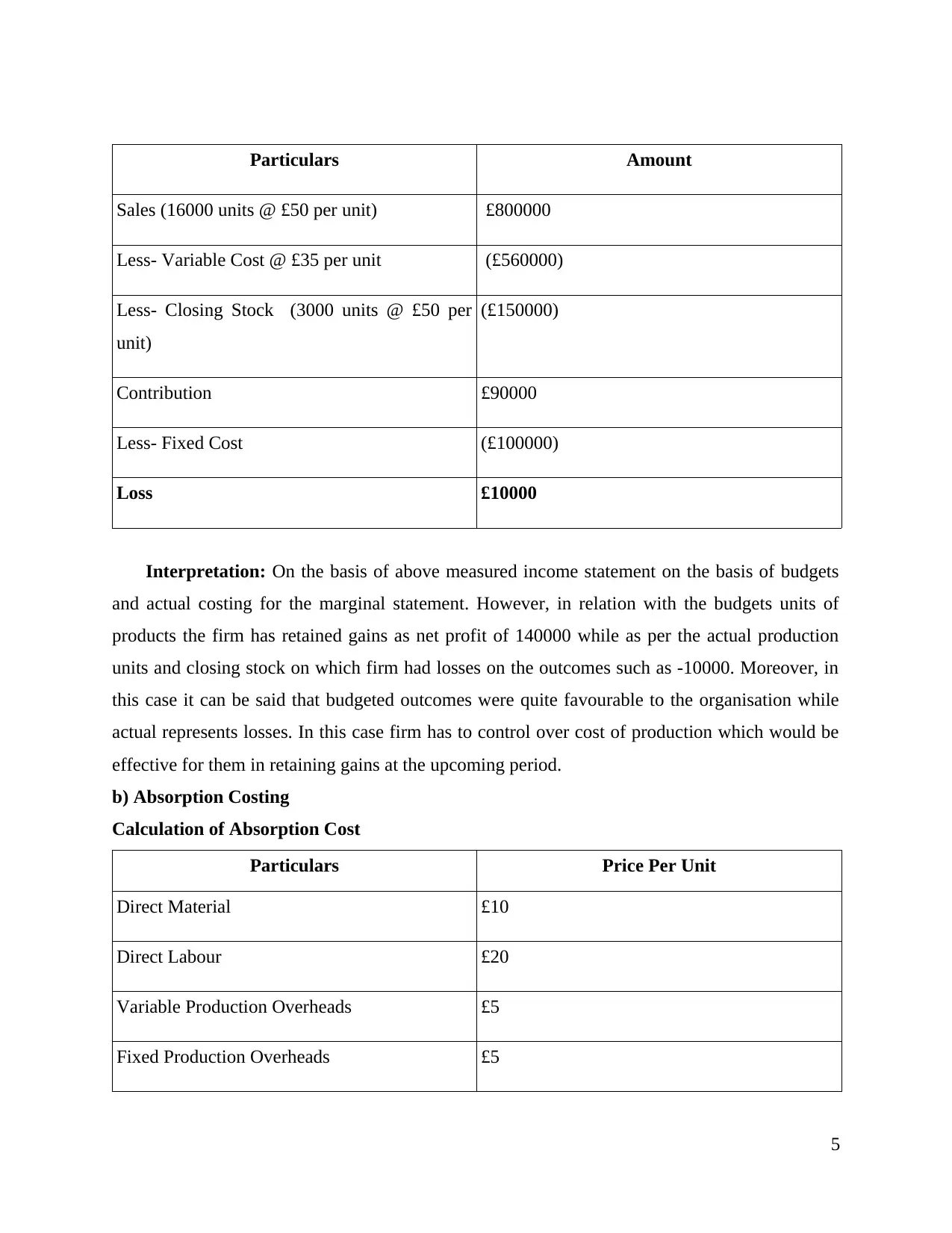

Sales (16000 units @ £50 per unit) £800000

Less- Variable Cost @ £35 per unit (£560000)

Less- Closing Stock (3000 units @ £50 per

unit)

(£150000)

Contribution £90000

Less- Fixed Cost (£100000)

Loss £10000

Interpretation: On the basis of above measured income statement on the basis of budgets

and actual costing for the marginal statement. However, in relation with the budgets units of

products the firm has retained gains as net profit of 140000 while as per the actual production

units and closing stock on which firm had losses on the outcomes such as -10000. Moreover, in

this case it can be said that budgeted outcomes were quite favourable to the organisation while

actual represents losses. In this case firm has to control over cost of production which would be

effective for them in retaining gains at the upcoming period.

b) Absorption Costing

Calculation of Absorption Cost

Particulars Price Per Unit

Direct Material £10

Direct Labour £20

Variable Production Overheads £5

Fixed Production Overheads £5

5

Sales (16000 units @ £50 per unit) £800000

Less- Variable Cost @ £35 per unit (£560000)

Less- Closing Stock (3000 units @ £50 per

unit)

(£150000)

Contribution £90000

Less- Fixed Cost (£100000)

Loss £10000

Interpretation: On the basis of above measured income statement on the basis of budgets

and actual costing for the marginal statement. However, in relation with the budgets units of

products the firm has retained gains as net profit of 140000 while as per the actual production

units and closing stock on which firm had losses on the outcomes such as -10000. Moreover, in

this case it can be said that budgeted outcomes were quite favourable to the organisation while

actual represents losses. In this case firm has to control over cost of production which would be

effective for them in retaining gains at the upcoming period.

b) Absorption Costing

Calculation of Absorption Cost

Particulars Price Per Unit

Direct Material £10

Direct Labour £20

Variable Production Overheads £5

Fixed Production Overheads £5

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Total Cost Per Unit £40 per unit

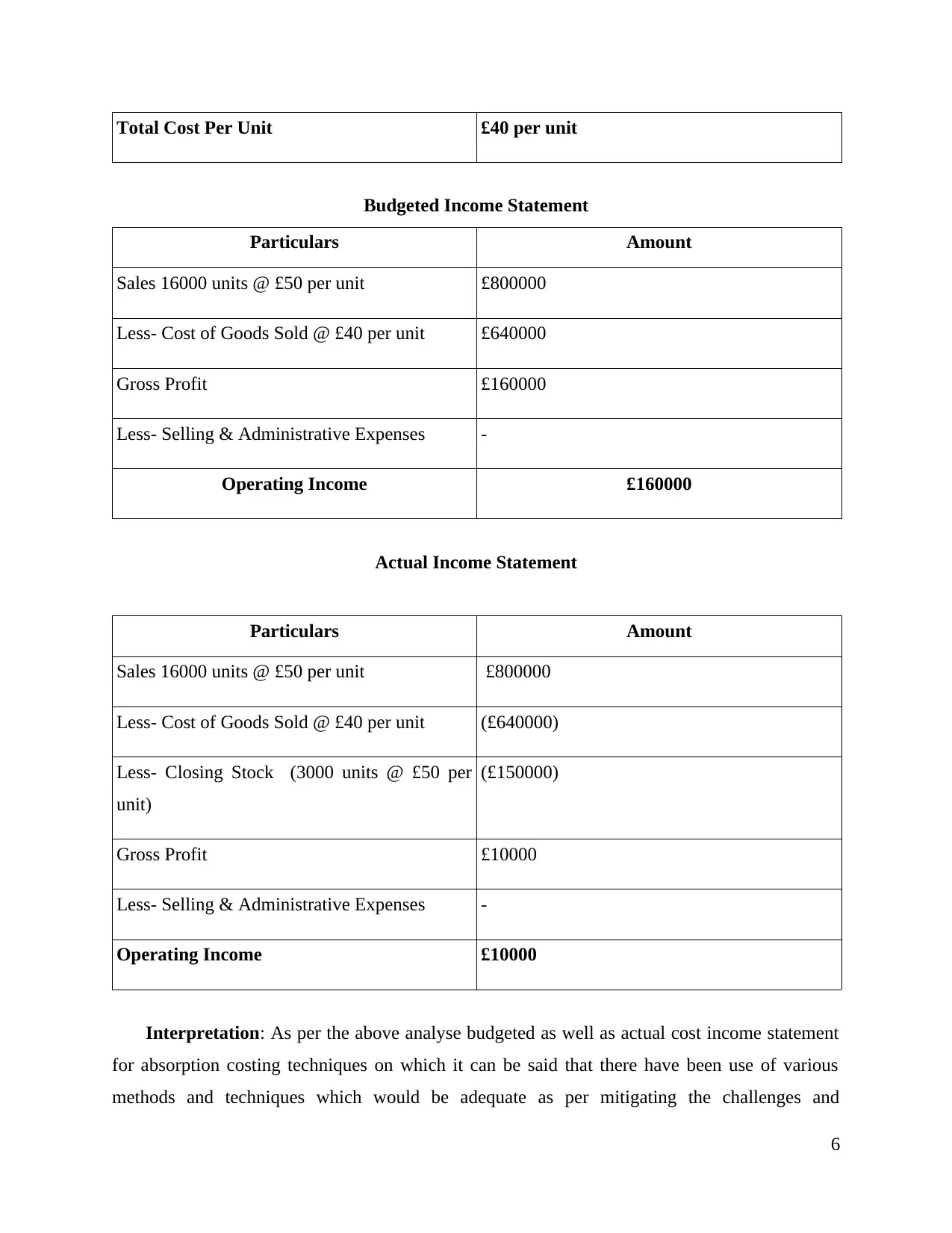

Budgeted Income Statement

Particulars Amount

Sales 16000 units @ £50 per unit £800000

Less- Cost of Goods Sold @ £40 per unit £640000

Gross Profit £160000

Less- Selling & Administrative Expenses -

Operating Income £160000

Actual Income Statement

Particulars Amount

Sales 16000 units @ £50 per unit £800000

Less- Cost of Goods Sold @ £40 per unit (£640000)

Less- Closing Stock (3000 units @ £50 per

unit)

(£150000)

Gross Profit £10000

Less- Selling & Administrative Expenses -

Operating Income £10000

Interpretation: As per the above analyse budgeted as well as actual cost income statement

for absorption costing techniques on which it can be said that there have been use of various

methods and techniques which would be adequate as per mitigating the challenges and

6

Budgeted Income Statement

Particulars Amount

Sales 16000 units @ £50 per unit £800000

Less- Cost of Goods Sold @ £40 per unit £640000

Gross Profit £160000

Less- Selling & Administrative Expenses -

Operating Income £160000

Actual Income Statement

Particulars Amount

Sales 16000 units @ £50 per unit £800000

Less- Cost of Goods Sold @ £40 per unit (£640000)

Less- Closing Stock (3000 units @ £50 per

unit)

(£150000)

Gross Profit £10000

Less- Selling & Administrative Expenses -

Operating Income £10000

Interpretation: As per the above analyse budgeted as well as actual cost income statement

for absorption costing techniques on which it can be said that there have been use of various

methods and techniques which would be adequate as per mitigating the challenges and

6

ascertaining the appropriate gains. Absorption is the technique where all costs have been

considered while analysing outcomes. However, in relation with the budgeted analysis have

represented gains of 160000 while in actual it also has received gains of 10000 GBP. Thus, in

relation with this, on which it can be said that, absorption costing technique is being helpful and

adequate for the firm in retaining appropriate gains in both situation such as budgeted as well as

actual outcomes.

TASK 3

Advantages and disadvantages of the planning tools used in budgetary control

There are a lot many advantages of the planning tools. These tools are more or less

performs same functions only that is zero base budgeting and the flexible budgeting

(Wickramasinghe, 2015). The major advantages of these types of planning tools that is flexible

and zero base budgeting are as follows-

The use of these planning tools helps in the efficient and effective use and allocation of

the available resources and it is based on the needs of the organization and the benefits

which they derive with the help of such tools (McLean, McGovern and Davie, 2015).

Another advantage is that these planning tools helps the top management in identifying

the key areas or departments where earlier there was a wasteful expenses going on.

These tools provide a predefined structure which provides the budgets makers and

planners with different types of features in tracking the expenses, helping the companies

to get the full overview of the budget and the forecasts (Malina, ed., 2018).

Like every coin has two sides, in the same way every topic have advantages and the

disadvantages. The disadvantages of these planning tools are as follows -

The major disadvantage of using these planning tools is that it is very expensive and

costly to install and implement this software and tools in the organization (Järvinen,

2016).

The major disadvantage of using planning tools and software for Unilever is that all these

tools requires highly skilled and knowledgeable persons and this is not possible in a

manufacturing industry that there are much skilled employees (Bruno and Lapsley,

2018).

7

considered while analysing outcomes. However, in relation with the budgeted analysis have

represented gains of 160000 while in actual it also has received gains of 10000 GBP. Thus, in

relation with this, on which it can be said that, absorption costing technique is being helpful and

adequate for the firm in retaining appropriate gains in both situation such as budgeted as well as

actual outcomes.

TASK 3

Advantages and disadvantages of the planning tools used in budgetary control

There are a lot many advantages of the planning tools. These tools are more or less

performs same functions only that is zero base budgeting and the flexible budgeting

(Wickramasinghe, 2015). The major advantages of these types of planning tools that is flexible

and zero base budgeting are as follows-

The use of these planning tools helps in the efficient and effective use and allocation of

the available resources and it is based on the needs of the organization and the benefits

which they derive with the help of such tools (McLean, McGovern and Davie, 2015).

Another advantage is that these planning tools helps the top management in identifying

the key areas or departments where earlier there was a wasteful expenses going on.

These tools provide a predefined structure which provides the budgets makers and

planners with different types of features in tracking the expenses, helping the companies

to get the full overview of the budget and the forecasts (Malina, ed., 2018).

Like every coin has two sides, in the same way every topic have advantages and the

disadvantages. The disadvantages of these planning tools are as follows -

The major disadvantage of using these planning tools is that it is very expensive and

costly to install and implement this software and tools in the organization (Järvinen,

2016).

The major disadvantage of using planning tools and software for Unilever is that all these

tools requires highly skilled and knowledgeable persons and this is not possible in a

manufacturing industry that there are much skilled employees (Bruno and Lapsley,

2018).

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The another disadvantage is that it is difficult to the whole budget because there are many

categories included in the budget and all these activities are linked to each other if thee is

change in any one of the factor then it affects the business as a whole (Hald and Thrane,

2016).

Use of different planning tools and their application

Budgetary control refers to a process with help of which the budgets are made for future

and controls the budgets by comparing the actual performance with planned performance (Grosu,

Almășan and Circa, 2014). Planning tools refers to as some planning tools and instruments which

helps and guides the organization in combining the raw data and converting it into some form of

meaningful and informational budget. The different types of planning tools used by ABC Ltd are

as follows -

Zero base budgeting - it is also known as ZBB. It refers to as a step by step process of

creating a budget from nothing that is without using the past and previous years budgets

and data (Robalo, 2014). It refers to a method or techniques which is used in developing

the budget from a scratch or a zero base by examining each and every expense and cost

which is essential for the company's operations without considering the previous years

activities (Nielsen, Mitchell and Nørreklit, 2015). It helps the top level management in

making strategic goals which are to be implemented into the budgeting process by linking

them to specific functional areas of the organization.

Flexible budgeting - it is also known as variable budget. It is defined as a financial plan

consisting of the expenses and the revenues which are based on the actual current amount

of output (Senftlechner and Hiebl, 2015). In simpler terms flexible budget makes the use

of the current expenses and the revenues by keeping them as base and then estimating

that how these expenses and the revenues will change based on the changes in the output.

This type of budget helps the organization in predicting its performance and the income

levels for a certain level of sales and production.

Activity based budget- this is a type of budget wherein all the activities of the business

which leads to cost involvement are recorded, analysed and evaluated. Using this method

helps in reducing the cost and increase the profits for the company.

Rolling budget- this is type of budget wherein the existing budget is only incremented or

extended and not a new budget is made.

8

categories included in the budget and all these activities are linked to each other if thee is

change in any one of the factor then it affects the business as a whole (Hald and Thrane,

2016).

Use of different planning tools and their application

Budgetary control refers to a process with help of which the budgets are made for future

and controls the budgets by comparing the actual performance with planned performance (Grosu,

Almășan and Circa, 2014). Planning tools refers to as some planning tools and instruments which

helps and guides the organization in combining the raw data and converting it into some form of

meaningful and informational budget. The different types of planning tools used by ABC Ltd are

as follows -

Zero base budgeting - it is also known as ZBB. It refers to as a step by step process of

creating a budget from nothing that is without using the past and previous years budgets

and data (Robalo, 2014). It refers to a method or techniques which is used in developing

the budget from a scratch or a zero base by examining each and every expense and cost

which is essential for the company's operations without considering the previous years

activities (Nielsen, Mitchell and Nørreklit, 2015). It helps the top level management in

making strategic goals which are to be implemented into the budgeting process by linking

them to specific functional areas of the organization.

Flexible budgeting - it is also known as variable budget. It is defined as a financial plan

consisting of the expenses and the revenues which are based on the actual current amount

of output (Senftlechner and Hiebl, 2015). In simpler terms flexible budget makes the use

of the current expenses and the revenues by keeping them as base and then estimating

that how these expenses and the revenues will change based on the changes in the output.

This type of budget helps the organization in predicting its performance and the income

levels for a certain level of sales and production.

Activity based budget- this is a type of budget wherein all the activities of the business

which leads to cost involvement are recorded, analysed and evaluated. Using this method

helps in reducing the cost and increase the profits for the company.

Rolling budget- this is type of budget wherein the existing budget is only incremented or

extended and not a new budget is made.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

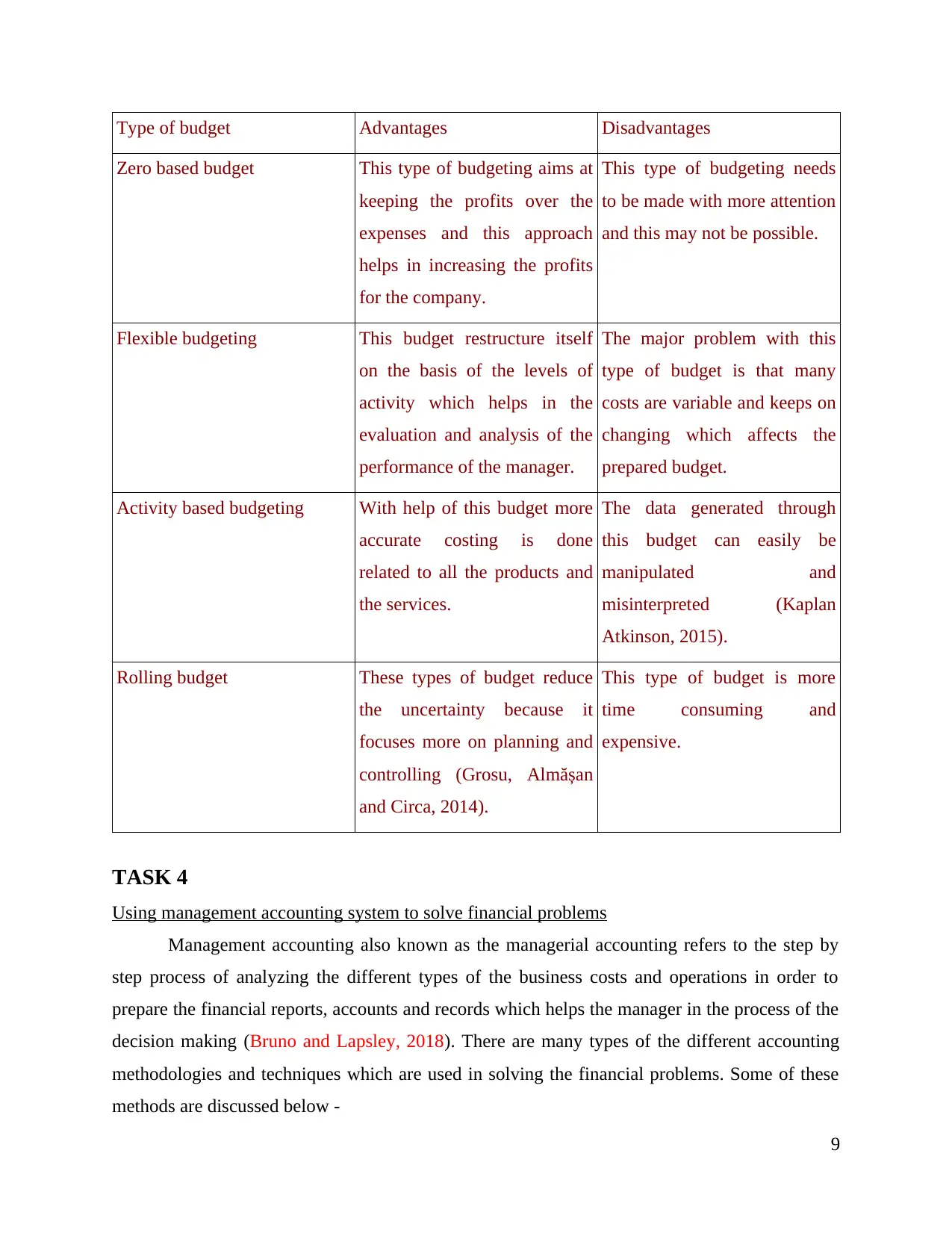

Type of budget Advantages Disadvantages

Zero based budget This type of budgeting aims at

keeping the profits over the

expenses and this approach

helps in increasing the profits

for the company.

This type of budgeting needs

to be made with more attention

and this may not be possible.

Flexible budgeting This budget restructure itself

on the basis of the levels of

activity which helps in the

evaluation and analysis of the

performance of the manager.

The major problem with this

type of budget is that many

costs are variable and keeps on

changing which affects the

prepared budget.

Activity based budgeting With help of this budget more

accurate costing is done

related to all the products and

the services.

The data generated through

this budget can easily be

manipulated and

misinterpreted (Kaplan

Atkinson, 2015).

Rolling budget These types of budget reduce

the uncertainty because it

focuses more on planning and

controlling (Grosu, Almășan

and Circa, 2014).

This type of budget is more

time consuming and

expensive.

TASK 4

Using management accounting system to solve financial problems

Management accounting also known as the managerial accounting refers to the step by

step process of analyzing the different types of the business costs and operations in order to

prepare the financial reports, accounts and records which helps the manager in the process of the

decision making (Bruno and Lapsley, 2018). There are many types of the different accounting

methodologies and techniques which are used in solving the financial problems. Some of these

methods are discussed below -

9

Zero based budget This type of budgeting aims at

keeping the profits over the

expenses and this approach

helps in increasing the profits

for the company.

This type of budgeting needs

to be made with more attention

and this may not be possible.

Flexible budgeting This budget restructure itself

on the basis of the levels of

activity which helps in the

evaluation and analysis of the

performance of the manager.

The major problem with this

type of budget is that many

costs are variable and keeps on

changing which affects the

prepared budget.

Activity based budgeting With help of this budget more

accurate costing is done

related to all the products and

the services.

The data generated through

this budget can easily be

manipulated and

misinterpreted (Kaplan

Atkinson, 2015).

Rolling budget These types of budget reduce

the uncertainty because it

focuses more on planning and

controlling (Grosu, Almășan

and Circa, 2014).

This type of budget is more

time consuming and

expensive.

TASK 4

Using management accounting system to solve financial problems

Management accounting also known as the managerial accounting refers to the step by

step process of analyzing the different types of the business costs and operations in order to

prepare the financial reports, accounts and records which helps the manager in the process of the

decision making (Bruno and Lapsley, 2018). There are many types of the different accounting

methodologies and techniques which are used in solving the financial problems. Some of these

methods are discussed below -

9

Bench marking- it is defined as the process of measuring the performance of the

company's products and services as compared to the another business which is best in the

industry. The main aim of bench marking is to identify the company's own internal

strengths and convert them into opportunities so that it improves the business of the ABC

Ltd by comparing it with the competitors (Morden, 2016). Bench marking helps in

improving the employees understanding about the cost structure and the internal process

because it is compared with the other firm so it can now differentiate between the cost

structure of the ABC Ltd as compared to the other competitors.

Key performance indicators- it refers to a measure or method which demonstrates how

effectively and efficiently the company works in achieving the business objectives and

the goals. This method evaluates the rate of success of the organization or for a particular

activity (Siverbo, 2014). There are basically two types of the KPI that is financial and

non- financial KPI.

Analysis of how management accounting leads the organization to success

Management accounting refers to as the application of the professional skills and

knowledge for preparing the accounting information in such a way that it helps the management

in the process of formulation of the policies and strategies and also helps in the planning and

controlling of all the operations and working of the company (Bruno and Lapsley, 2018).

Advantages of management accounting in achieving success

The following points are the major advantages of the management accounting which helps in

successful accomplishment of goals and objectives of the business-

The use of management accounting helps in increasing the efficiency of the company

because everything is done with help of scientific systems for evaluation and comparison

of the performance of the organization and the employees (Akkermans and Van

Oorschot, 2018).

These methods help the organization in measuring the actual performance of the

organization as compared to the planned performance.

It also helps the business in managing the activities of the business and to maximize the

rate of return on the capital employed (Kaplan and Atkinson, 2015).

It also helps the management in outlining the future requirements and plan of action to

meet the future requirements on the basis of the past performance and results.

10

company's products and services as compared to the another business which is best in the

industry. The main aim of bench marking is to identify the company's own internal

strengths and convert them into opportunities so that it improves the business of the ABC

Ltd by comparing it with the competitors (Morden, 2016). Bench marking helps in

improving the employees understanding about the cost structure and the internal process

because it is compared with the other firm so it can now differentiate between the cost

structure of the ABC Ltd as compared to the other competitors.

Key performance indicators- it refers to a measure or method which demonstrates how

effectively and efficiently the company works in achieving the business objectives and

the goals. This method evaluates the rate of success of the organization or for a particular

activity (Siverbo, 2014). There are basically two types of the KPI that is financial and

non- financial KPI.

Analysis of how management accounting leads the organization to success

Management accounting refers to as the application of the professional skills and

knowledge for preparing the accounting information in such a way that it helps the management

in the process of formulation of the policies and strategies and also helps in the planning and

controlling of all the operations and working of the company (Bruno and Lapsley, 2018).

Advantages of management accounting in achieving success

The following points are the major advantages of the management accounting which helps in

successful accomplishment of goals and objectives of the business-

The use of management accounting helps in increasing the efficiency of the company

because everything is done with help of scientific systems for evaluation and comparison

of the performance of the organization and the employees (Akkermans and Van

Oorschot, 2018).

These methods help the organization in measuring the actual performance of the

organization as compared to the planned performance.

It also helps the business in managing the activities of the business and to maximize the

rate of return on the capital employed (Kaplan and Atkinson, 2015).

It also helps the management in outlining the future requirements and plan of action to

meet the future requirements on the basis of the past performance and results.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.