ACC 202: Management Accounting - Loader Truck Cost Analysis Report

VerifiedAdded on 2020/05/28

|5

|682

|27

Report

AI Summary

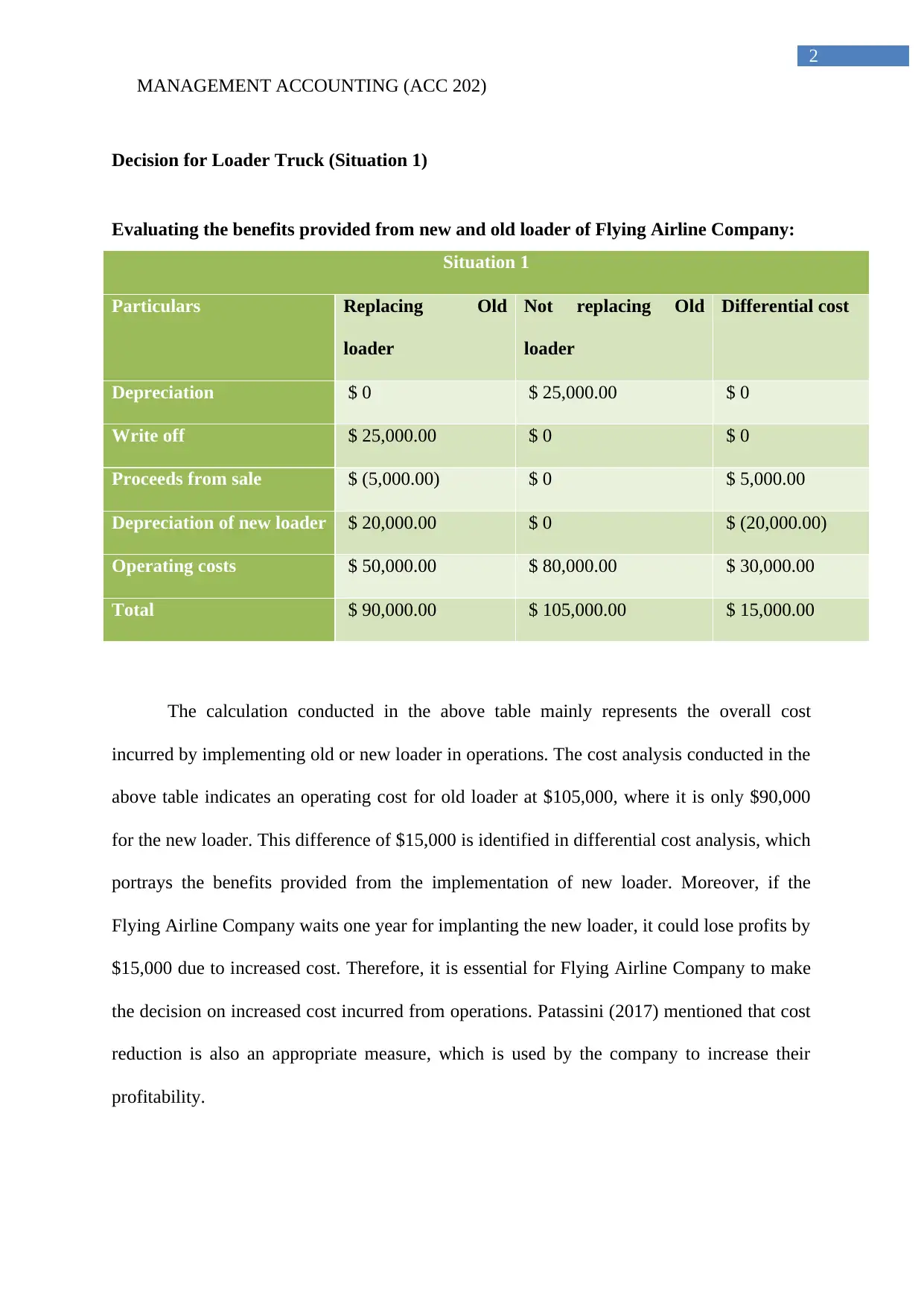

This report, focused on management accounting (ACC 202), analyzes the decision of whether to replace an old loader truck for the Flying Airline Company. It presents a differential cost analysis comparing the costs of operating the old loader versus a new one, considering factors like depreciation, write-offs, proceeds from sales, and operating costs. The analysis reveals that the new loader results in lower operating costs, leading to a potential profit increase of $15,000. The report references academic sources to support the importance of cost reduction and the role of cost analysis in making informed decisions that improve operational capabilities and financial reserves. The conclusion emphasizes the benefits of the new loader for reducing costs and increasing profitability.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.