ACC203 Assignment: Cost Analysis and Journal Entries for Cool Brew Ltd

VerifiedAdded on 2023/05/30

|7

|1241

|475

Homework Assignment

AI Summary

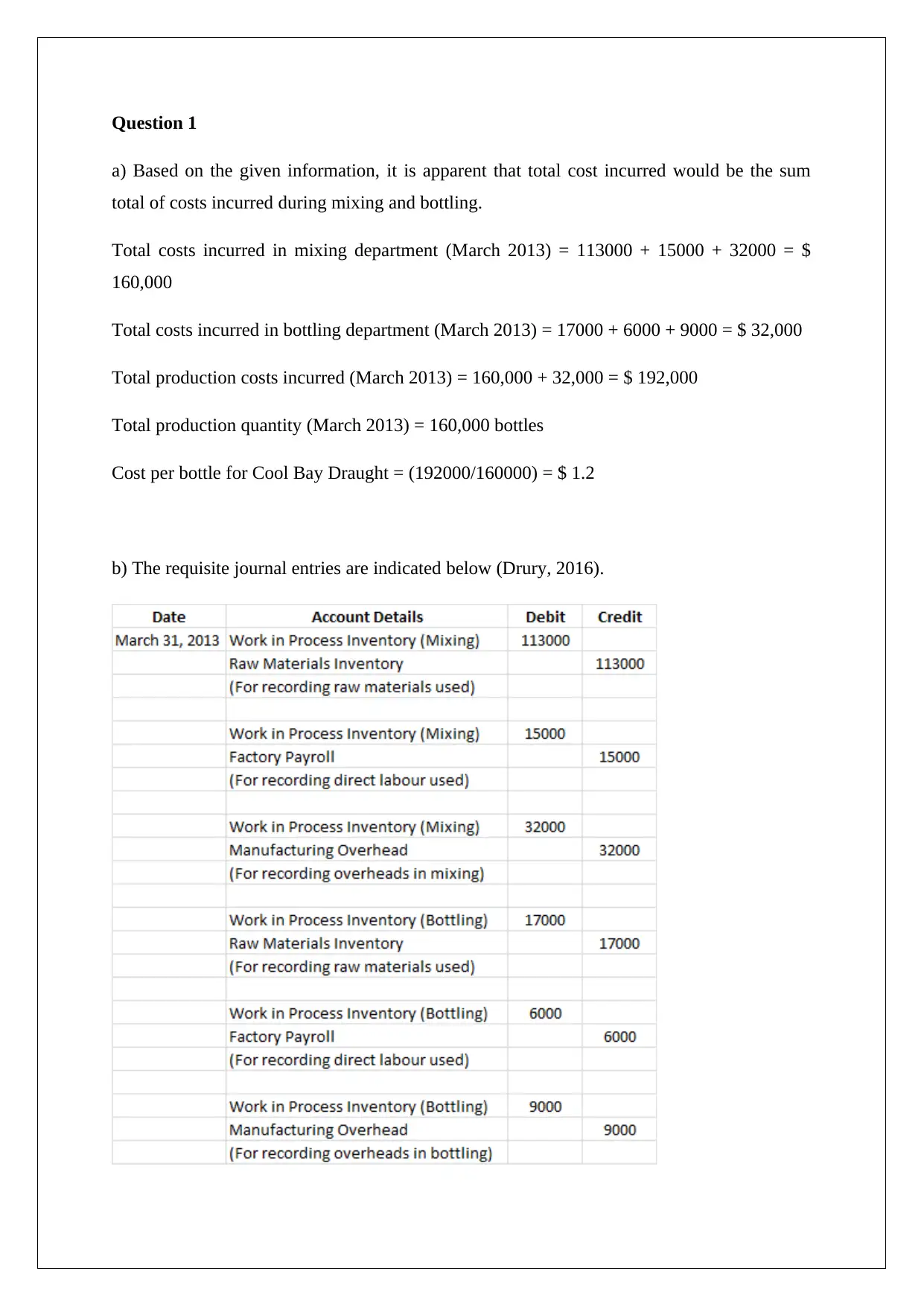

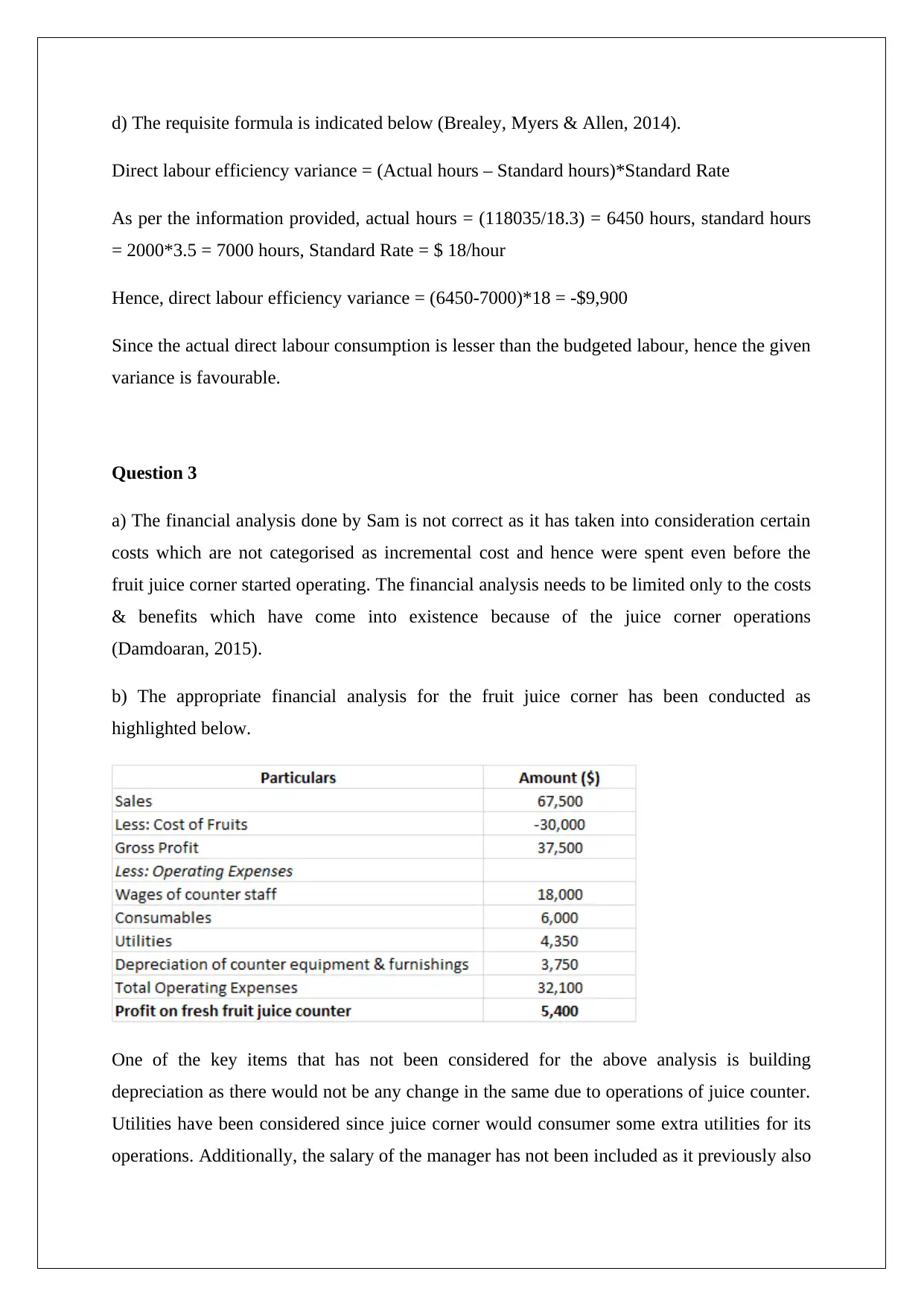

This assignment solution provides a comprehensive analysis of Cool Brew Ltd's production costs, covering key areas such as cost per bottle calculation, journal entries for production costs, and variance analysis. The solution meticulously calculates total production costs, cost per bottle, and prepares the necessary journal entries for the mixing and bottling departments. Furthermore, the solution delves into variance analysis, calculating direct material price and usage variances, direct labor rate and efficiency variances, and provides a financial analysis of a fruit juice corner scenario. The assignment also addresses product profitability, determining the optimal production mix to maximize profit given limited machine hours, comparing contribution margins and recommending production strategies based on machine hour constraints. References to relevant accounting literature are included to support the analysis.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.