Comprehensive Management Accounting Report for Alpha Ltd

VerifiedAdded on 2023/01/18

|21

|5643

|42

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and practices, focusing on the case of Alpha Ltd, a medium-sized UK-based company known for its pizza products. The report begins with an introduction to management accounting, its scope, and its importance in organizational decision-making. It then delves into different types of management accounting systems, including inventory management, cost accounting, job costing, and price optimization systems, highlighting their benefits for Alpha Ltd. The report further explores methods of management accounting reporting, such as budget reports, cost managerial accounting reports, account receivable aging reports, and execution reports. It also examines the integration of management accounting systems and reports within organizational processes. The core of the report involves the calculation of costs using marginal and absorption costing methods, including the preparation of profitability statements and reconciliation statements. Finally, the report addresses break-even point calculations and provides insights into the financial performance and decision-making processes of Alpha Ltd, offering a practical application of management accounting concepts.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION

MA is concerned with the presentation of accounting information in such a manner which

assist organisation in the creation of policy in order to undertake day to day operation in an

effective and efficient manner. Moreover, it enable company to assist managerial activities help

them in ascertaining financial planning for acquiring best position among competitive

marketplace (AlMaryani and Sadik, 2012). Along within this, its contains huge scope as it covers

the areas like financial and cost accounting, budgetary control, usage of statistical methods like

regression analysis and many more for maintaining better business position within an industry.

For this report, Alpha Ltd is considered which is one of the reputed medium sized company in

UK and it is mainly well known by its product i.e. pizzas which covers all age brackets across

the globe. In this study, it covers outline of management accounting along with its types and

methods, formulation of income statement, highlights pros and cons of different budgetary

planning tools. Finally, role of company in managing complex financial problems is also

mentioned here.

P1 Management accounting and different types of management accounting system

It is mandatory for each type of organisation to record financial transaction in order to

monitor their revenue and expenditure that is earned by an organisation in a particular time

period. This functions are done through management accounting and financial department of an

organisation. On other hand this functions are performed by internal departments of organisation

which determines that it is an important part for management. In context of Alpha Ltd financial

or monetary transaction is considered as one crucial decisions for this it is necessary for them to

include new methods and concepts of management accounting (Disney and Gathergood, 2013).

It assist them to control business's actions that is taken by management of Alpha Ltd through

evaluating their performance. Some different types of management accounting are mention as

follow:

Inventory management system- Inventory management works as an effective accounting

management system which is used by organisation to manage their inventory. This system helps

an organisation to deliver their stock within minimum time period. For Alpha Ltd inventory

management system is beneficial because it work as a discipline method that specify needs shape

of goods according to need of customer's. On other hand inventory management is required at all

1

MA is concerned with the presentation of accounting information in such a manner which

assist organisation in the creation of policy in order to undertake day to day operation in an

effective and efficient manner. Moreover, it enable company to assist managerial activities help

them in ascertaining financial planning for acquiring best position among competitive

marketplace (AlMaryani and Sadik, 2012). Along within this, its contains huge scope as it covers

the areas like financial and cost accounting, budgetary control, usage of statistical methods like

regression analysis and many more for maintaining better business position within an industry.

For this report, Alpha Ltd is considered which is one of the reputed medium sized company in

UK and it is mainly well known by its product i.e. pizzas which covers all age brackets across

the globe. In this study, it covers outline of management accounting along with its types and

methods, formulation of income statement, highlights pros and cons of different budgetary

planning tools. Finally, role of company in managing complex financial problems is also

mentioned here.

P1 Management accounting and different types of management accounting system

It is mandatory for each type of organisation to record financial transaction in order to

monitor their revenue and expenditure that is earned by an organisation in a particular time

period. This functions are done through management accounting and financial department of an

organisation. On other hand this functions are performed by internal departments of organisation

which determines that it is an important part for management. In context of Alpha Ltd financial

or monetary transaction is considered as one crucial decisions for this it is necessary for them to

include new methods and concepts of management accounting (Disney and Gathergood, 2013).

It assist them to control business's actions that is taken by management of Alpha Ltd through

evaluating their performance. Some different types of management accounting are mention as

follow:

Inventory management system- Inventory management works as an effective accounting

management system which is used by organisation to manage their inventory. This system helps

an organisation to deliver their stock within minimum time period. For Alpha Ltd inventory

management system is beneficial because it work as a discipline method that specify needs shape

of goods according to need of customer's. On other hand inventory management is required at all

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

locations where organisation operates their business in order to predate their regular stock of

materials.

Cost accounting system- An effective cost accounting system is execute by manufacture

and organisation to record cost of their production activities. This works as a framework that is

used by firms for predicting cost of their products through recording them regularly.

Management of Alpha Ltd uses cost accounting system to decide profit margin on their products

through analysis cost of their operations for making inventory and products. Moreover this

system perform an critical role for operating profitable business's in market through deciding

their profit margin. Another factor assist organisation to analyse price of product and inventory

for manufacturing product. By doing assessment, it has identified that company can determine

price by using cost accounting system. Moreover, it clearly indicates unit price associated with

the operations. Thus, by adding mark-up in unit cost firm can set optimal price for the product or

services.

Price = Unit cost + (cost * mark-up%)

For instance unit cost is £50 then price will be

Price = 50 + (50 * 20%)

= £50 + £10

= £60

Accordingly, by offering products at the price of £60 firm can get desired profit margin.

Job Costing system- This is also known as order costing. This work as a system that is

used to assign and accumulating operational cost of particular unit and batch which is

manufactured by organisation. In context of Alpha Ltd job costing system it is beneficial for

organisation because it helps them to identify cost of various item which is different from each

other. With help of this it is easy for organisation to identify profits for each specific unit of

organisation. On other perspective with order costing organisation decided prices and

manufacture each product unit according to need and demand of customer's (Hawkey, Webb and

Winskel, 2013).

Price optimisation system- Price optimisation accounting system assist an organisation to

formulate an effective framework which helps management for identifying price of their

products and services. Moreover this system is beneficial for organisation as well as customers

because it decided price through mutual concern of all departments. It determines prices which is

2

materials.

Cost accounting system- An effective cost accounting system is execute by manufacture

and organisation to record cost of their production activities. This works as a framework that is

used by firms for predicting cost of their products through recording them regularly.

Management of Alpha Ltd uses cost accounting system to decide profit margin on their products

through analysis cost of their operations for making inventory and products. Moreover this

system perform an critical role for operating profitable business's in market through deciding

their profit margin. Another factor assist organisation to analyse price of product and inventory

for manufacturing product. By doing assessment, it has identified that company can determine

price by using cost accounting system. Moreover, it clearly indicates unit price associated with

the operations. Thus, by adding mark-up in unit cost firm can set optimal price for the product or

services.

Price = Unit cost + (cost * mark-up%)

For instance unit cost is £50 then price will be

Price = 50 + (50 * 20%)

= £50 + £10

= £60

Accordingly, by offering products at the price of £60 firm can get desired profit margin.

Job Costing system- This is also known as order costing. This work as a system that is

used to assign and accumulating operational cost of particular unit and batch which is

manufactured by organisation. In context of Alpha Ltd job costing system it is beneficial for

organisation because it helps them to identify cost of various item which is different from each

other. With help of this it is easy for organisation to identify profits for each specific unit of

organisation. On other perspective with order costing organisation decided prices and

manufacture each product unit according to need and demand of customer's (Hawkey, Webb and

Winskel, 2013).

Price optimisation system- Price optimisation accounting system assist an organisation to

formulate an effective framework which helps management for identifying price of their

products and services. Moreover this system is beneficial for organisation as well as customers

because it decided price through mutual concern of all departments. It determines prices which is

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

decided by organisation is fair and includes marginal profits. So it attracts more number of

customer's through charging minimum prices from them. Within circumstances of Alpha Ltd

price optimisation system leads management to make effective decisions by asserting unbiased

prices from them. In the context of business unit, price optimization system is required with the

motive to setting down appropriate pricing framework. Moreover, when company charges higher

prices for its offerings then it may result into low customer base and lack of competitive

advantage. On the other side, in the case of setting high low prices profitability of the company is

affected negatively. In this way, by undertaking this system business unit can set suitable prices

as per customer’s preferences and thereby would become able to get desired level of outcome or

success.

P2 Methods of management accounting reporting

Management Accounting focuses on information provided by financial accounting for

decision making (Henttu-Aho and Järvinen, 2013). Management Accounting reports facilitate

planning, decision making, regulations etc. these reports are based on financial accounting &

reporting which are prepared throughout the year as all the facts and figures need to be

considered and accuracy requirement is high. Various methods of management accounting

reporting followed by Alpha Ltd are -

Budget Reports- Budget reports are those managerial reports which are used to analyse

the performance of the of the organisation. They can be prepared department wise, activity wise

for a specific period of time. Alpha Ltd prepare a overall budget on the basis of past experiences,

it includes all the possible income and expenditure for the specific time period. These reports

help them to plan for reduction in expenditure and to identify funds requirement. Moreover this

helps an organisation to control prices of all activities that is performed and organised by

management to attain their goals.

Cost Managerial Accounting Reports- In cost report all the cost related to raw material,

labour, overheads are included which gives a clear picture of total cost incurred in production

process. When total cost is divided by total output it gives per unit cost (Kanellou and Spathis,

2013). Alpha Ltd prepare this report as it facilitate them to identify all the cost and profit margins

so that they can optimise the use of resources by reducing the wastage in terms of inventory,

labour hours etc. This types of cost accounting report helps an organisation to estimate price of

their products which is manufactured by them.

3

customer's through charging minimum prices from them. Within circumstances of Alpha Ltd

price optimisation system leads management to make effective decisions by asserting unbiased

prices from them. In the context of business unit, price optimization system is required with the

motive to setting down appropriate pricing framework. Moreover, when company charges higher

prices for its offerings then it may result into low customer base and lack of competitive

advantage. On the other side, in the case of setting high low prices profitability of the company is

affected negatively. In this way, by undertaking this system business unit can set suitable prices

as per customer’s preferences and thereby would become able to get desired level of outcome or

success.

P2 Methods of management accounting reporting

Management Accounting focuses on information provided by financial accounting for

decision making (Henttu-Aho and Järvinen, 2013). Management Accounting reports facilitate

planning, decision making, regulations etc. these reports are based on financial accounting &

reporting which are prepared throughout the year as all the facts and figures need to be

considered and accuracy requirement is high. Various methods of management accounting

reporting followed by Alpha Ltd are -

Budget Reports- Budget reports are those managerial reports which are used to analyse

the performance of the of the organisation. They can be prepared department wise, activity wise

for a specific period of time. Alpha Ltd prepare a overall budget on the basis of past experiences,

it includes all the possible income and expenditure for the specific time period. These reports

help them to plan for reduction in expenditure and to identify funds requirement. Moreover this

helps an organisation to control prices of all activities that is performed and organised by

management to attain their goals.

Cost Managerial Accounting Reports- In cost report all the cost related to raw material,

labour, overheads are included which gives a clear picture of total cost incurred in production

process. When total cost is divided by total output it gives per unit cost (Kanellou and Spathis,

2013). Alpha Ltd prepare this report as it facilitate them to identify all the cost and profit margins

so that they can optimise the use of resources by reducing the wastage in terms of inventory,

labour hours etc. This types of cost accounting report helps an organisation to estimate price of

their products which is manufactured by them.

3

Account Receivable Ageing Reports- These reports are prepared to keep a check on

debtors. When organisation provide frequent & large credit then this becomes so important.

Alpha Ltd prepare this report to identify the debtors who can default in future and to improve the

collection process. Also this helps in planning and creating provisions for bad debts and to

decide the extent for which the credit can be extended to a few parties.

Execution reports- Management account develop and utilize plans for constant and

genuine use of income through including all planned sums. After developing new budget for

organisation all changes are predicted and recorded to make an effective report. Usually this

reports are formulated on annual basis in an organisation (Lavia López and Hiebl, 2014). While

in context of Alpha Ltd they operates their businesses in beverage industry. So it is mandatory

for them to decide price of their products because it enables them to match their product demand

with upcoming future along with cost additions.

M1 Benefits of management accounting system

Management accounting system Benefits

Price optimisation system Accounting system leads an organisation to

analyse prices of their products through

implementing effective decisions. For Alpha

Ltd it helps them to delegate products

effectively.

Cost accounting system Cost accounting system is developed by

organisations for calculating the overall cost of

organisation. Further this system is used by

Alpha Ltd to decide price of products through

analysing its in-depth information (Lovat and

Zhang, Sharp Laboratories of America Inc,

2013).

Job costing system An organisation develops several types of

products in order to offer them in market.

Therefore this is mandatory for Alpha Ltd to

identify prices of products on individual’s basis

4

debtors. When organisation provide frequent & large credit then this becomes so important.

Alpha Ltd prepare this report to identify the debtors who can default in future and to improve the

collection process. Also this helps in planning and creating provisions for bad debts and to

decide the extent for which the credit can be extended to a few parties.

Execution reports- Management account develop and utilize plans for constant and

genuine use of income through including all planned sums. After developing new budget for

organisation all changes are predicted and recorded to make an effective report. Usually this

reports are formulated on annual basis in an organisation (Lavia López and Hiebl, 2014). While

in context of Alpha Ltd they operates their businesses in beverage industry. So it is mandatory

for them to decide price of their products because it enables them to match their product demand

with upcoming future along with cost additions.

M1 Benefits of management accounting system

Management accounting system Benefits

Price optimisation system Accounting system leads an organisation to

analyse prices of their products through

implementing effective decisions. For Alpha

Ltd it helps them to delegate products

effectively.

Cost accounting system Cost accounting system is developed by

organisations for calculating the overall cost of

organisation. Further this system is used by

Alpha Ltd to decide price of products through

analysing its in-depth information (Lovat and

Zhang, Sharp Laboratories of America Inc,

2013).

Job costing system An organisation develops several types of

products in order to offer them in market.

Therefore this is mandatory for Alpha Ltd to

identify prices of products on individual’s basis

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

for evaluating products on each factor.

Inventory management system For an organisation it is essential to manage

inventory according to demand of customer's.

Therefore it is important for them to

manufacture inventories according to upcoming

demands of customer's.

D1 Integration of management accounting system and report within organisational process

Type of reporting & Systems Integration with organisational process

Inventory management report: This report

is prepared through taking base of

information that is gathered from system and

integrate them for benefits of organisation.

This integration is beneficial for organisation

because it helps them to organise raw materials

according to estimated level of purchase orders

that raises in upcoming future (Nganga, 2014).

Performance report: This report is

prepared according to different information

system that is gathers from all departments

of organisation. This includes all actual

performance of Alpha Ltd departments.

Integration of this method in organisational

process helps organisation to make effective juice

by removing deviations and ineffective methods

that increases burden of their cost.

TASK 2

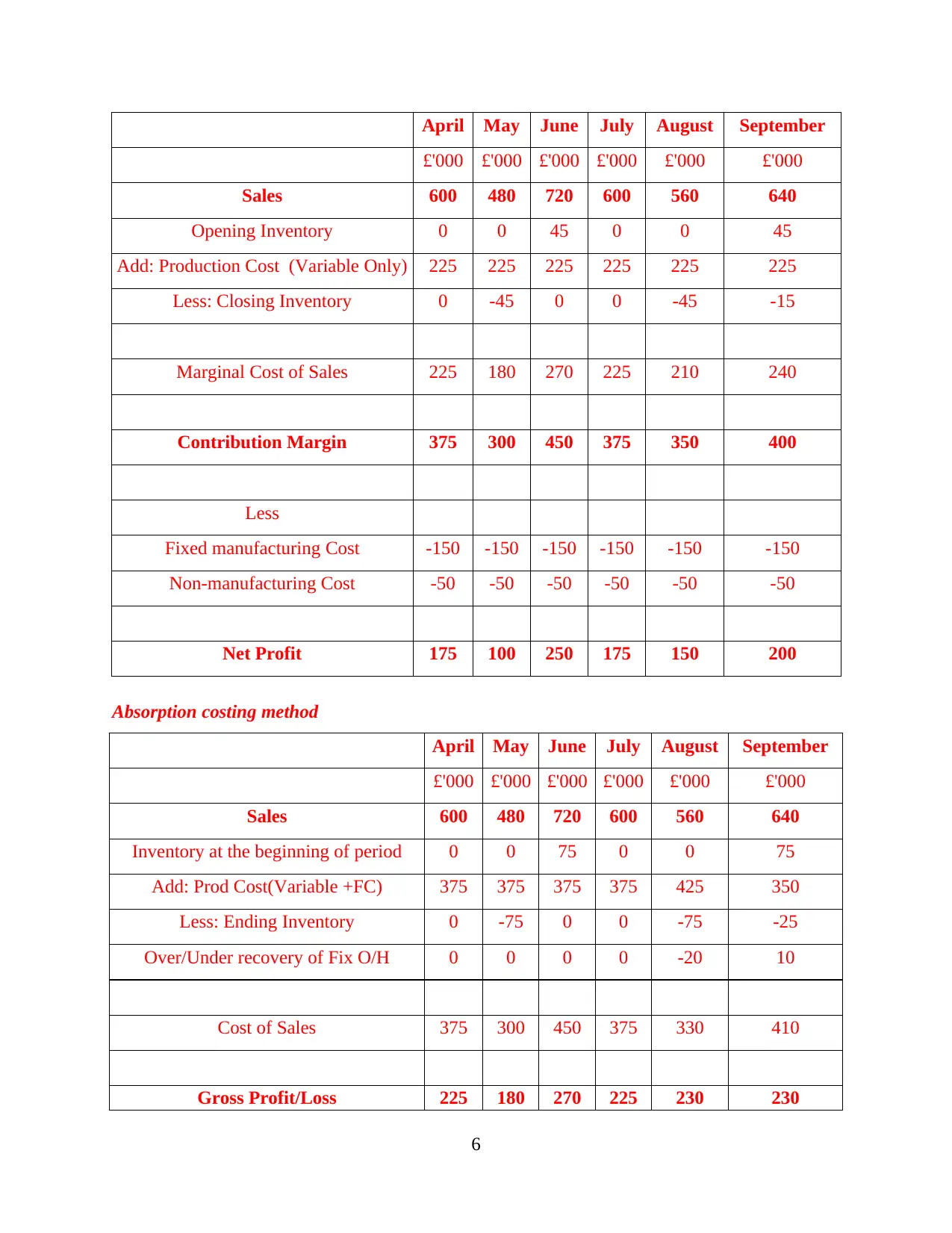

P3 Calculation of cost using marginal and absorption cost

Cost accounting techniques are effective tools which helps organisation like Alpha Ltd.

To identify cost that is incurred by them while going through their production activity. This helps

them to decide profits for each activity. For this task profits for Alpha Ltd is mention through

using marginal and absorption costing.

Marginal Costing: Marginal costing system work as a tool that undertakes only variable

cost for the revenue that is generated from sales (Otley, 2016). While fixed cost is written off

against contribution only for a specific period.

Problem 1

1. calculation product cost unit and income statement as per absorption and marginal costing

Profitability statement as per marginal costing method is enumerated below:

5

Inventory management system For an organisation it is essential to manage

inventory according to demand of customer's.

Therefore it is important for them to

manufacture inventories according to upcoming

demands of customer's.

D1 Integration of management accounting system and report within organisational process

Type of reporting & Systems Integration with organisational process

Inventory management report: This report

is prepared through taking base of

information that is gathered from system and

integrate them for benefits of organisation.

This integration is beneficial for organisation

because it helps them to organise raw materials

according to estimated level of purchase orders

that raises in upcoming future (Nganga, 2014).

Performance report: This report is

prepared according to different information

system that is gathers from all departments

of organisation. This includes all actual

performance of Alpha Ltd departments.

Integration of this method in organisational

process helps organisation to make effective juice

by removing deviations and ineffective methods

that increases burden of their cost.

TASK 2

P3 Calculation of cost using marginal and absorption cost

Cost accounting techniques are effective tools which helps organisation like Alpha Ltd.

To identify cost that is incurred by them while going through their production activity. This helps

them to decide profits for each activity. For this task profits for Alpha Ltd is mention through

using marginal and absorption costing.

Marginal Costing: Marginal costing system work as a tool that undertakes only variable

cost for the revenue that is generated from sales (Otley, 2016). While fixed cost is written off

against contribution only for a specific period.

Problem 1

1. calculation product cost unit and income statement as per absorption and marginal costing

Profitability statement as per marginal costing method is enumerated below:

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

April May June July August September

£'000 £'000 £'000 £'000 £'000 £'000

Sales 600 480 720 600 560 640

Opening Inventory 0 0 45 0 0 45

Add: Production Cost (Variable Only) 225 225 225 225 225 225

Less: Closing Inventory 0 -45 0 0 -45 -15

Marginal Cost of Sales 225 180 270 225 210 240

Contribution Margin 375 300 450 375 350 400

Less

Fixed manufacturing Cost -150 -150 -150 -150 -150 -150

Non-manufacturing Cost -50 -50 -50 -50 -50 -50

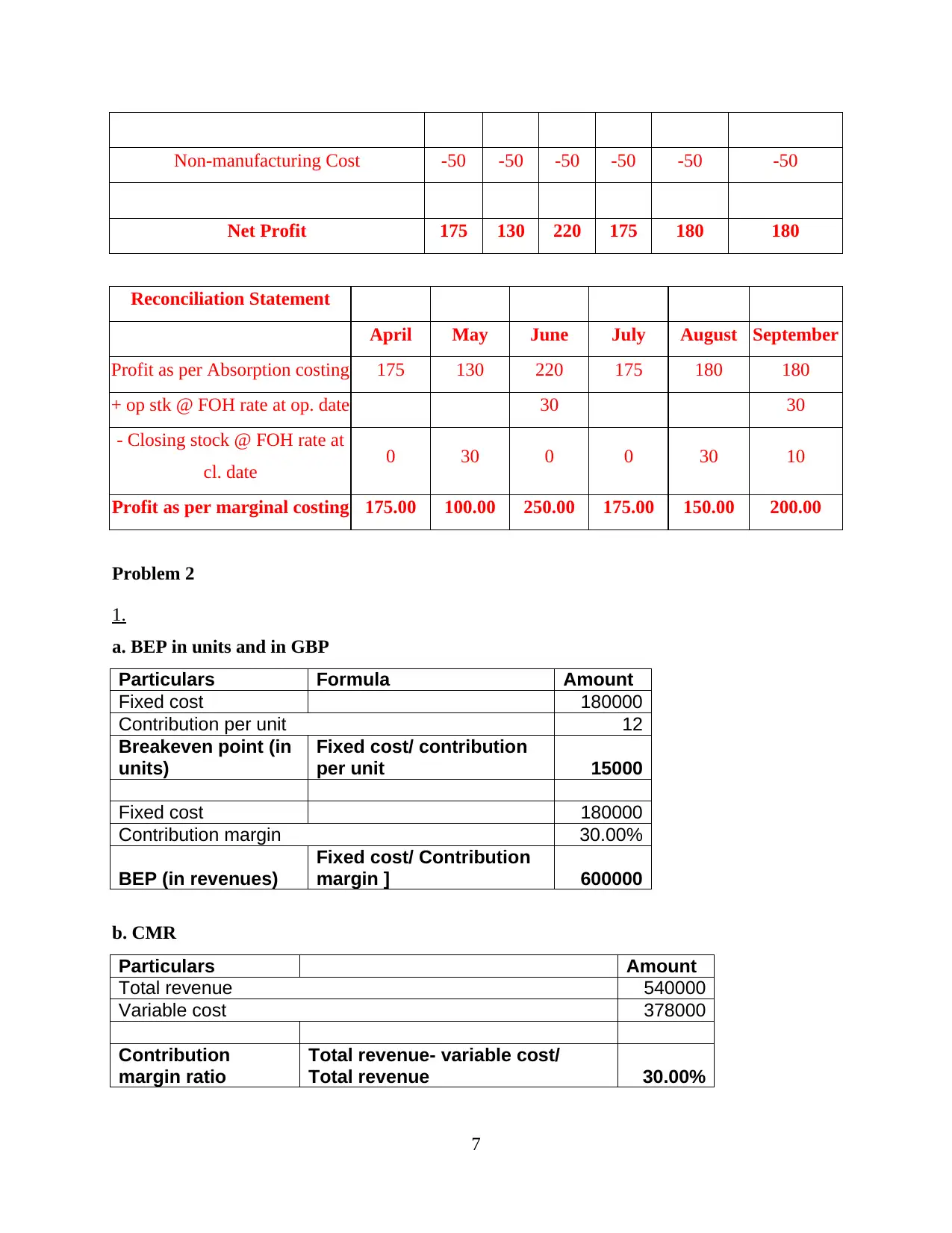

Net Profit 175 100 250 175 150 200

Absorption costing method

April May June July August September

£'000 £'000 £'000 £'000 £'000 £'000

Sales 600 480 720 600 560 640

Inventory at the beginning of period 0 0 75 0 0 75

Add: Prod Cost(Variable +FC) 375 375 375 375 425 350

Less: Ending Inventory 0 -75 0 0 -75 -25

Over/Under recovery of Fix O/H 0 0 0 0 -20 10

Cost of Sales 375 300 450 375 330 410

Gross Profit/Loss 225 180 270 225 230 230

6

£'000 £'000 £'000 £'000 £'000 £'000

Sales 600 480 720 600 560 640

Opening Inventory 0 0 45 0 0 45

Add: Production Cost (Variable Only) 225 225 225 225 225 225

Less: Closing Inventory 0 -45 0 0 -45 -15

Marginal Cost of Sales 225 180 270 225 210 240

Contribution Margin 375 300 450 375 350 400

Less

Fixed manufacturing Cost -150 -150 -150 -150 -150 -150

Non-manufacturing Cost -50 -50 -50 -50 -50 -50

Net Profit 175 100 250 175 150 200

Absorption costing method

April May June July August September

£'000 £'000 £'000 £'000 £'000 £'000

Sales 600 480 720 600 560 640

Inventory at the beginning of period 0 0 75 0 0 75

Add: Prod Cost(Variable +FC) 375 375 375 375 425 350

Less: Ending Inventory 0 -75 0 0 -75 -25

Over/Under recovery of Fix O/H 0 0 0 0 -20 10

Cost of Sales 375 300 450 375 330 410

Gross Profit/Loss 225 180 270 225 230 230

6

Non-manufacturing Cost -50 -50 -50 -50 -50 -50

Net Profit 175 130 220 175 180 180

Reconciliation Statement

April May June July August September

Profit as per Absorption costing 175 130 220 175 180 180

+ op stk @ FOH rate at op. date 30 30

- Closing stock @ FOH rate at

cl. date 0 30 0 0 30 10

Profit as per marginal costing 175.00 100.00 250.00 175.00 150.00 200.00

Problem 2

1.

a. BEP in units and in GBP

Particulars Formula Amount

Fixed cost 180000

Contribution per unit 12

Breakeven point (in

units)

Fixed cost/ contribution

per unit 15000

Fixed cost 180000

Contribution margin 30.00%

BEP (in revenues)

Fixed cost/ Contribution

margin ] 600000

b. CMR

Particulars Amount

Total revenue 540000

Variable cost 378000

Contribution

margin ratio

Total revenue- variable cost/

Total revenue 30.00%

7

Net Profit 175 130 220 175 180 180

Reconciliation Statement

April May June July August September

Profit as per Absorption costing 175 130 220 175 180 180

+ op stk @ FOH rate at op. date 30 30

- Closing stock @ FOH rate at

cl. date 0 30 0 0 30 10

Profit as per marginal costing 175.00 100.00 250.00 175.00 150.00 200.00

Problem 2

1.

a. BEP in units and in GBP

Particulars Formula Amount

Fixed cost 180000

Contribution per unit 12

Breakeven point (in

units)

Fixed cost/ contribution

per unit 15000

Fixed cost 180000

Contribution margin 30.00%

BEP (in revenues)

Fixed cost/ Contribution

margin ] 600000

b. CMR

Particulars Amount

Total revenue 540000

Variable cost 378000

Contribution

margin ratio

Total revenue- variable cost/

Total revenue 30.00%

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

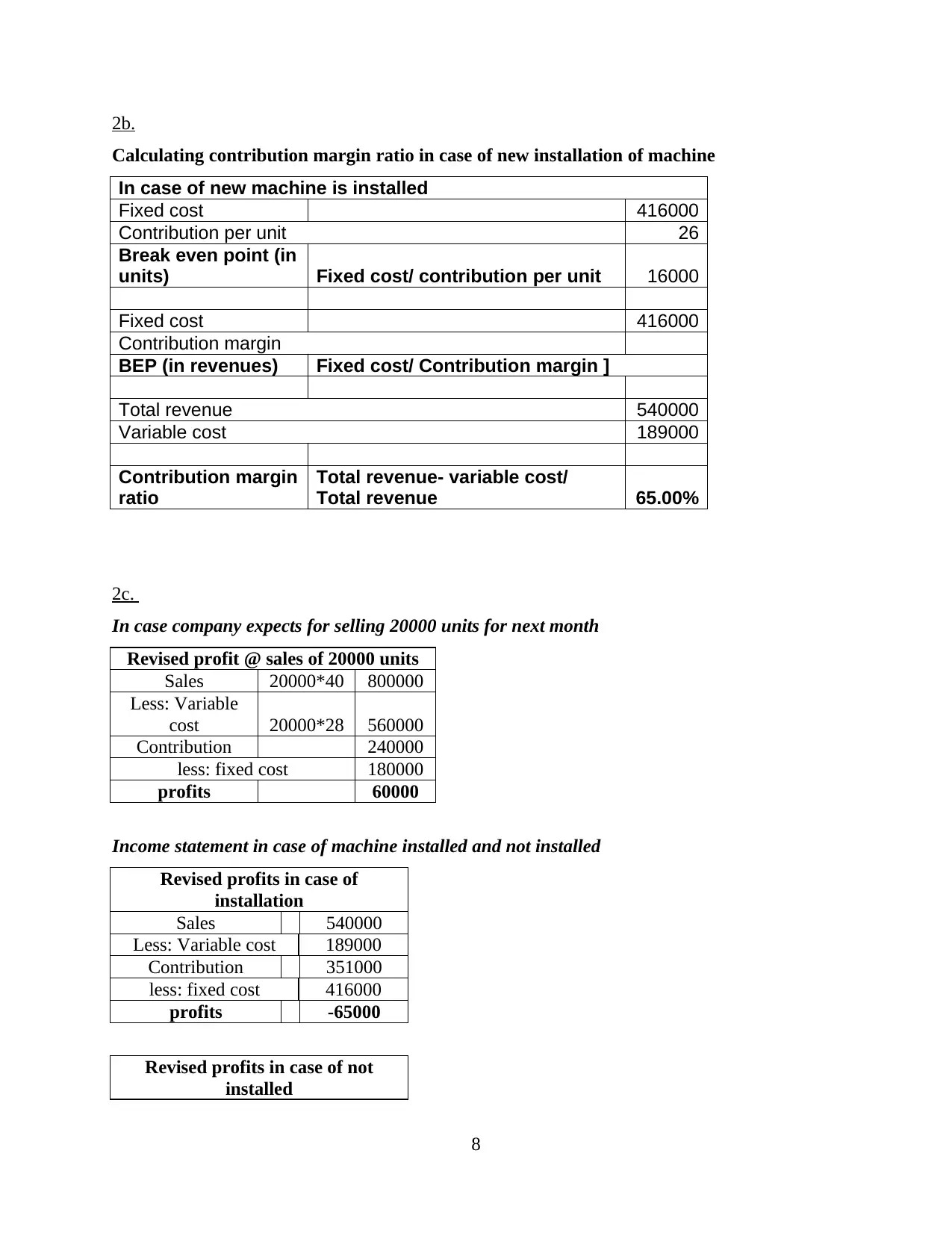

2b.

Calculating contribution margin ratio in case of new installation of machine

In case of new machine is installed

Fixed cost 416000

Contribution per unit 26

Break even point (in

units) Fixed cost/ contribution per unit 16000

Fixed cost 416000

Contribution margin

BEP (in revenues) Fixed cost/ Contribution margin ]

Total revenue 540000

Variable cost 189000

Contribution margin

ratio

Total revenue- variable cost/

Total revenue 65.00%

2c.

In case company expects for selling 20000 units for next month

Revised profit @ sales of 20000 units

Sales 20000*40 800000

Less: Variable

cost 20000*28 560000

Contribution 240000

less: fixed cost 180000

profits 60000

Income statement in case of machine installed and not installed

Revised profits in case of

installation

Sales 540000

Less: Variable cost 189000

Contribution 351000

less: fixed cost 416000

profits -65000

Revised profits in case of not

installed

8

Calculating contribution margin ratio in case of new installation of machine

In case of new machine is installed

Fixed cost 416000

Contribution per unit 26

Break even point (in

units) Fixed cost/ contribution per unit 16000

Fixed cost 416000

Contribution margin

BEP (in revenues) Fixed cost/ Contribution margin ]

Total revenue 540000

Variable cost 189000

Contribution margin

ratio

Total revenue- variable cost/

Total revenue 65.00%

2c.

In case company expects for selling 20000 units for next month

Revised profit @ sales of 20000 units

Sales 20000*40 800000

Less: Variable

cost 20000*28 560000

Contribution 240000

less: fixed cost 180000

profits 60000

Income statement in case of machine installed and not installed

Revised profits in case of

installation

Sales 540000

Less: Variable cost 189000

Contribution 351000

less: fixed cost 416000

profits -65000

Revised profits in case of not

installed

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sales 540000

Less: Variable cost 378000

Contribution 162000

less: fixed cost 180000

profits -18000

Interpretation- the above scenario shows that installation of machinery for the firm is

not profitable as fixed costs are too high and generated a huge loss.

Working notes:

Working note

Particulars Cost per unit

Sales 40

Less: Variable cost 28

Contribution per unit 12

Old fixed cost 180000

Revised fixed cost 18000+236000 416000

Old variable expenses per unit

Revised variable cost per

unit 14 28-50%

Sales 40

Less: Variable cost 14 28

Contribution per unit 26 14

TASK 3.

P4 Advantages and disadvantages of different kind of planning tools of budgetary control.

Budgetary control can be defined as a process in which managers of an organisation set

different standard to complete a task with the help of Budget. It works as an prediction for

organisation after this actual performance of organisation is compared with estimated budget

(RW Hiebl, 2013). This is done is order to know that organisational actual performance is

according to estimated budget or not. Due to this it is easy for them to adopt changes which

increases probability of earning high profits for a longer term period. In present scenario there

are several tools that are related with budgetary control along with their advantages and dis-

advantage are mentions as follow:

9

Less: Variable cost 378000

Contribution 162000

less: fixed cost 180000

profits -18000

Interpretation- the above scenario shows that installation of machinery for the firm is

not profitable as fixed costs are too high and generated a huge loss.

Working notes:

Working note

Particulars Cost per unit

Sales 40

Less: Variable cost 28

Contribution per unit 12

Old fixed cost 180000

Revised fixed cost 18000+236000 416000

Old variable expenses per unit

Revised variable cost per

unit 14 28-50%

Sales 40

Less: Variable cost 14 28

Contribution per unit 26 14

TASK 3.

P4 Advantages and disadvantages of different kind of planning tools of budgetary control.

Budgetary control can be defined as a process in which managers of an organisation set

different standard to complete a task with the help of Budget. It works as an prediction for

organisation after this actual performance of organisation is compared with estimated budget

(RW Hiebl, 2013). This is done is order to know that organisational actual performance is

according to estimated budget or not. Due to this it is easy for them to adopt changes which

increases probability of earning high profits for a longer term period. In present scenario there

are several tools that are related with budgetary control along with their advantages and dis-

advantage are mentions as follow:

9

Static budget- Static budget refers to those budgets that are not flexible. It determines

that they are fixed in nature. This kind of budget are not change because of change in sales of

products. As static budget are complex so they are suitable for those which remain constant for

longer time period. Further this budget is beneficial for Alpha Ltd as it helps to accomplish their

goals within shorter time period. Merits and de-merits of this budget are mention as below:

Merits

This budget remains same for longer time period so there is no need to update them. This

results it helps organisation to save their time and cost. Static budget are easy to monitor because

they are not modified according to need of market and remain same (Soin and Collier, 2013).

De-merits

The major dis-advantage of static budget is lack of flexibility. It results that organisation

is not able to adopt essential changes which increases their sale. Moreover this budget are

inappropriate as they does not provide any effective way to record their expenses.

Zero based budget- Zero based budget is an effective method of budgeting in which all

expenses are identified and justified for new period. This process starts from zero and then each

function of organisation is analysed for its needs and costs. In context of Zero based budget helps

top level management to implement budget into functional areas of organisation (Veprauskait

and Adams, 2013). As in this first cost of organisation are grouped and then it is measured

against previous and current expectations. Advantages and dis-advantage of this are mention as

follow:

Merits

With implement of zero based budget it is easy for organisation to bring efficiency in

their budget results. This helps an organisation to remove those activities that are not justified

within budget.

Demerits

In order to make an effective zero based budget organisation need to invest too much

time and money in organisation. This is not possible for single individual to formulate zero based

budget. More number of team member is required to make this budget.

Flexible budget- This type of budgets are modified and adjust themselves according to

changes in volume and activity. As compare to other budget flexible budget are more beneficial

for organisation and management. Cost of a product or service will change according to volume

10

that they are fixed in nature. This kind of budget are not change because of change in sales of

products. As static budget are complex so they are suitable for those which remain constant for

longer time period. Further this budget is beneficial for Alpha Ltd as it helps to accomplish their

goals within shorter time period. Merits and de-merits of this budget are mention as below:

Merits

This budget remains same for longer time period so there is no need to update them. This

results it helps organisation to save their time and cost. Static budget are easy to monitor because

they are not modified according to need of market and remain same (Soin and Collier, 2013).

De-merits

The major dis-advantage of static budget is lack of flexibility. It results that organisation

is not able to adopt essential changes which increases their sale. Moreover this budget are

inappropriate as they does not provide any effective way to record their expenses.

Zero based budget- Zero based budget is an effective method of budgeting in which all

expenses are identified and justified for new period. This process starts from zero and then each

function of organisation is analysed for its needs and costs. In context of Zero based budget helps

top level management to implement budget into functional areas of organisation (Veprauskait

and Adams, 2013). As in this first cost of organisation are grouped and then it is measured

against previous and current expectations. Advantages and dis-advantage of this are mention as

follow:

Merits

With implement of zero based budget it is easy for organisation to bring efficiency in

their budget results. This helps an organisation to remove those activities that are not justified

within budget.

Demerits

In order to make an effective zero based budget organisation need to invest too much

time and money in organisation. This is not possible for single individual to formulate zero based

budget. More number of team member is required to make this budget.

Flexible budget- This type of budgets are modified and adjust themselves according to

changes in volume and activity. As compare to other budget flexible budget are more beneficial

for organisation and management. Cost of a product or service will change according to volume

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.