Principles & Practice of Management Accounting Report - Alpha Limited

VerifiedAdded on 2023/01/13

|23

|5287

|91

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and practices, focusing on the context of Alpha Limited, a medium-sized manufacturing enterprise. It covers key aspects such as management accounting systems, including inventory management, cost accounting, price optimization, and job costing. The report delves into different methods of management accounting reporting, including inventory reports, performance reports, accounts receivable reports, and budget reports. It further explores the calculation of costs using marginal and absorption costing methods, along with their respective profit and loss accounts. Additionally, the report examines the advantages and disadvantages of various planning tools of budgetary control and discusses the adaptation of management accounting to respond to financial problems. The analysis aims to provide a clear understanding of the application of management accounting techniques for effective financial management and decision-making within a business context.

Principles & Practice of

Management

Accounting

Management

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK...............................................................................................................................................3

P1. Management Accounting and its systems:.......................................................................3

M1 Benefits of management Accounting systems:................................................................5

P2. Different methods of management accounting reporting:................................................6

TASK 2............................................................................................................................................7

P3. Calculation of costs on the basis of marginal and absorption costing method:...............7

M2. Effectively apply a variety of MA techniques and generate correct financial reports: 14

P4. Explanation of advantages and disadvantages of different types of planning tools of

budgetary control:.................................................................................................................15

P5 Adaption of management according to respond financial problem................................17

CONCLUSION..............................................................................................................................21

REFERENCES..............................................................................................................................22

INTRODUCTION...........................................................................................................................3

TASK...............................................................................................................................................3

P1. Management Accounting and its systems:.......................................................................3

M1 Benefits of management Accounting systems:................................................................5

P2. Different methods of management accounting reporting:................................................6

TASK 2............................................................................................................................................7

P3. Calculation of costs on the basis of marginal and absorption costing method:...............7

M2. Effectively apply a variety of MA techniques and generate correct financial reports: 14

P4. Explanation of advantages and disadvantages of different types of planning tools of

budgetary control:.................................................................................................................15

P5 Adaption of management according to respond financial problem................................17

CONCLUSION..............................................................................................................................21

REFERENCES..............................................................................................................................22

INTRODUCTION

Managing business and its numerous kind of operations is difficult as well as essential

task. Management is primary personnel that manage business and for this purpose they require

meaningful and relevant information (Anderson and Sedatole, 2013). Management accounting

key tool which can assist them in managing business. It involve conversion of raw-details and

data into useful information and facts for supporting managerial decisions. It involves systems

and frameworks which provide assistance to managers in adaption of entire system of

management accounting. This covers core areas of accounting and management, which provide a

more detailed information about organisation.

This study-assessment consists of multiple aspects and concepts of management

accounting along with different core systems and key requirements in context of Alpha Limited.

Corporation is a medium sized manufacturing enterprise with just 50 members and medium

turnover of around £ 500000 per year. Study discuss about major reporting methods and other

technique of management accounting. Further it provide explanation about planning tool and

effective comparison of corporations as to how these are adapting systems to efficaciously

responding to different financial problems.

TASK

P1. Management Accounting and its systems:

Management or managerial accounting referring to as collection of structured tasks that

systematically lead to comprehensive monitoring and evaluation of operational costs linked to

various business procedures that assist a company and business in rendering value judgements

and choices related to manufacturing, company's core practices and marketplace development &

financing (Hilton and Platt, 2013). Entities requires managerial accounting as well as its various

factors to evaluate planned budgets for performance, the expenses of key activities and then

effective distribution of funds and capital. For the growth of company, thus, the role and

operation of managerial staff and accounting officers is very crucial here. The corporation uses

different management accounting systems to acquire the requisite financial data from each

division of the organization. These are crucial part of the management accounting procedure, this

system allows the company to document important financial data from its operating operations

on a regular basis. Without the use of such system firms, budget management, risk assessment

Managing business and its numerous kind of operations is difficult as well as essential

task. Management is primary personnel that manage business and for this purpose they require

meaningful and relevant information (Anderson and Sedatole, 2013). Management accounting

key tool which can assist them in managing business. It involve conversion of raw-details and

data into useful information and facts for supporting managerial decisions. It involves systems

and frameworks which provide assistance to managers in adaption of entire system of

management accounting. This covers core areas of accounting and management, which provide a

more detailed information about organisation.

This study-assessment consists of multiple aspects and concepts of management

accounting along with different core systems and key requirements in context of Alpha Limited.

Corporation is a medium sized manufacturing enterprise with just 50 members and medium

turnover of around £ 500000 per year. Study discuss about major reporting methods and other

technique of management accounting. Further it provide explanation about planning tool and

effective comparison of corporations as to how these are adapting systems to efficaciously

responding to different financial problems.

TASK

P1. Management Accounting and its systems:

Management or managerial accounting referring to as collection of structured tasks that

systematically lead to comprehensive monitoring and evaluation of operational costs linked to

various business procedures that assist a company and business in rendering value judgements

and choices related to manufacturing, company's core practices and marketplace development &

financing (Hilton and Platt, 2013). Entities requires managerial accounting as well as its various

factors to evaluate planned budgets for performance, the expenses of key activities and then

effective distribution of funds and capital. For the growth of company, thus, the role and

operation of managerial staff and accounting officers is very crucial here. The corporation uses

different management accounting systems to acquire the requisite financial data from each

division of the organization. These are crucial part of the management accounting procedure, this

system allows the company to document important financial data from its operating operations

on a regular basis. Without the use of such system firms, budget management, risk assessment

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

including investment policy decisions have never been made. Here is the detailed discussion

about MA systems in relation to Alpha limited, as follows:

Management Accounting Systems:

A management accounting systems defined as a functional mechanism that helps to

produce critical information which subsequently helps formulate policies and actions. MA entails

various structures that are utilized by personnel management according to company and

organizational structure specifications (Schaltegger and Csutora, 2012). Alpha is using more than

accounting system as to support management's decisions and boost fiscal performance, as

follows:

Inventory management system: This system involve comprehensive and sequential

information of all kind of inventories and stocks. This is a framework that uses software and

other techniques or tools to manage entity's inventory and stock items. Business uses different

techniques such as LIFO, FIFO approaches to determine the business's inventory related

requirements. For the object of managing stock losses within the enterprise, the supervisor and

managing staff uses this system Inventory management system is valuable to reach optimum

resource efficiency, it helps to improve work capacity, save time and operational expenses,

deliver products to consumers at their prescribed time.

FIFO: Herein this approach very first purchased inventories are assumed to be processed or

sold first for valuing stock/inventories.

LIFO: While here it is normally assumed that most recently purchased items are sold or

processes first for valuing inventories.

Average Cost method: In it simply value of all the inventories are averaged for valuation of

inventories.

Cost Accounting System: Business use that system to assess actual cost of producing goods and

then determine the entity's level of productivity. Costing of jobs and operations is the part of the

cost accounting system. Cost accounting system is quite essential part of management

accounting, manager utilizes such system to make policies that define risks and create policies

for risk analysis, control costs, minimize material wastage. The program also assists in the

process of performance assessment. Company uses this system to assess cost effectiveness of any

key process. In Alpha like manufacturing enterprise this systems enable to determine cost of

each manufactured and processed item as well as to efficaciously control different costs.

about MA systems in relation to Alpha limited, as follows:

Management Accounting Systems:

A management accounting systems defined as a functional mechanism that helps to

produce critical information which subsequently helps formulate policies and actions. MA entails

various structures that are utilized by personnel management according to company and

organizational structure specifications (Schaltegger and Csutora, 2012). Alpha is using more than

accounting system as to support management's decisions and boost fiscal performance, as

follows:

Inventory management system: This system involve comprehensive and sequential

information of all kind of inventories and stocks. This is a framework that uses software and

other techniques or tools to manage entity's inventory and stock items. Business uses different

techniques such as LIFO, FIFO approaches to determine the business's inventory related

requirements. For the object of managing stock losses within the enterprise, the supervisor and

managing staff uses this system Inventory management system is valuable to reach optimum

resource efficiency, it helps to improve work capacity, save time and operational expenses,

deliver products to consumers at their prescribed time.

FIFO: Herein this approach very first purchased inventories are assumed to be processed or

sold first for valuing stock/inventories.

LIFO: While here it is normally assumed that most recently purchased items are sold or

processes first for valuing inventories.

Average Cost method: In it simply value of all the inventories are averaged for valuation of

inventories.

Cost Accounting System: Business use that system to assess actual cost of producing goods and

then determine the entity's level of productivity. Costing of jobs and operations is the part of the

cost accounting system. Cost accounting system is quite essential part of management

accounting, manager utilizes such system to make policies that define risks and create policies

for risk analysis, control costs, minimize material wastage. The program also assists in the

process of performance assessment. Company uses this system to assess cost effectiveness of any

key process. In Alpha like manufacturing enterprise this systems enable to determine cost of

each manufactured and processed item as well as to efficaciously control different costs.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Price optimization system

Price optimization system is the system that uses the mathematical analysis for

determining the price of a product the customers will be willing to pay. It is also used in

determine prices which meet the maximum operating profit for the company (Talley, 2017).

There are many software used by the companies to handle the complex required calculations for

price and cost. Such programs are mathematical program that enables a company to know about

the level of demand incur at different price levels. The data used in price optimization can

includes operating cost, historic prices and sales volume reports, survey data, and inventories.

Job costing system:

This system classify different processes in specific tasks and list all the costs related such

jobs as to assess the cost of job. This system is used to assigning cost to each product of the

company and then calculate and measuring cost of each order company receive free their

customer. Company use this system when their products are identical. Company make products

according to the demand of their customers. This system of managerial accounting helps in

identifying market demand of customers and useful in making and implementing decision of the

company. In Alpha limited this system is used to recognise jobs which are critical for

organisation's performance.

M1 Benefits of management Accounting systems:

System Benefit

Inventories Management System This system is advantageous for Alpha limited

in controlling numerous inventories costs and

identify the root-cause of increasing

inventories costs.

Cost Accounting System In Aplha, managers can use this system to

minimise overall production and operating

cost. It also help in regulating different costs

and optimising operational costs.

Price-optimisation System Price-optimisation is beneficial for enterprise

to control and limit prices. This assist

managers in formulating pricing strategies and

Price optimization system is the system that uses the mathematical analysis for

determining the price of a product the customers will be willing to pay. It is also used in

determine prices which meet the maximum operating profit for the company (Talley, 2017).

There are many software used by the companies to handle the complex required calculations for

price and cost. Such programs are mathematical program that enables a company to know about

the level of demand incur at different price levels. The data used in price optimization can

includes operating cost, historic prices and sales volume reports, survey data, and inventories.

Job costing system:

This system classify different processes in specific tasks and list all the costs related such

jobs as to assess the cost of job. This system is used to assigning cost to each product of the

company and then calculate and measuring cost of each order company receive free their

customer. Company use this system when their products are identical. Company make products

according to the demand of their customers. This system of managerial accounting helps in

identifying market demand of customers and useful in making and implementing decision of the

company. In Alpha limited this system is used to recognise jobs which are critical for

organisation's performance.

M1 Benefits of management Accounting systems:

System Benefit

Inventories Management System This system is advantageous for Alpha limited

in controlling numerous inventories costs and

identify the root-cause of increasing

inventories costs.

Cost Accounting System In Aplha, managers can use this system to

minimise overall production and operating

cost. It also help in regulating different costs

and optimising operational costs.

Price-optimisation System Price-optimisation is beneficial for enterprise

to control and limit prices. This assist

managers in formulating pricing strategies and

policies.

Job costing System This system mainly beneficial in effective

classification of jobs and optimising job costs

and enhance efficiencies of job processes.

P2. Different methods of management accounting reporting:

Managers use several reports from management systems to devise business-level plans,

take decisions and assess their workplace efficiency. Management accounting reporting is

structured task that provides some crucial reports which assist management in taking business

and financial decisions. Entity Aplha plc is also using different reporting tools or approaches that

assist managing staff in effective analysis and evaluation. Here below is a discussion about

multiple reporting methods, as follows:

Inventory report: This report is prepared to keep the organization's inventory level

Inventory report is actually a summery of corporation's average inventory level. It help to asses

the actual re-order stock level, minimum & maximum stock-level. This report segregates all the

inventories and allocate costs. This report all use different techniques like LIFO,FIFO as

discussed above to assess the actual stock level. In Alpha, inventory managers prepare this report

to assess the need of of stock and raw-materials as well as to minimise different costs associated

with stock like storage costs, normal and abnormal inventory costs.

Performance report: This is most essential method of managerial accounting report.

Performance report are made to identify the overall performance of organisation,which included

labour performance employees and employers performance also. Manager use this report for the

purpose of making incentive policies. Company gave rewards and recommendation to their

employees after reviewing their performance. This report is help in identifying low skilled

workforce within the organisation. In Alpha, this report is used to asses the workers/employee

performance as to determine their wages, compensations and allocate works.

Accounts-receivable Report: This report involves list of all the trade debts, accounts

receivables and bills receivables details. This is major report which determines enterprise's actual

collection period. By analysis of this report managers can determine whether debtors are capable

to repay their debts and assess any probability of deb-debts. Alpha's managers apply information

Job costing System This system mainly beneficial in effective

classification of jobs and optimising job costs

and enhance efficiencies of job processes.

P2. Different methods of management accounting reporting:

Managers use several reports from management systems to devise business-level plans,

take decisions and assess their workplace efficiency. Management accounting reporting is

structured task that provides some crucial reports which assist management in taking business

and financial decisions. Entity Aplha plc is also using different reporting tools or approaches that

assist managing staff in effective analysis and evaluation. Here below is a discussion about

multiple reporting methods, as follows:

Inventory report: This report is prepared to keep the organization's inventory level

Inventory report is actually a summery of corporation's average inventory level. It help to asses

the actual re-order stock level, minimum & maximum stock-level. This report segregates all the

inventories and allocate costs. This report all use different techniques like LIFO,FIFO as

discussed above to assess the actual stock level. In Alpha, inventory managers prepare this report

to assess the need of of stock and raw-materials as well as to minimise different costs associated

with stock like storage costs, normal and abnormal inventory costs.

Performance report: This is most essential method of managerial accounting report.

Performance report are made to identify the overall performance of organisation,which included

labour performance employees and employers performance also. Manager use this report for the

purpose of making incentive policies. Company gave rewards and recommendation to their

employees after reviewing their performance. This report is help in identifying low skilled

workforce within the organisation. In Alpha, this report is used to asses the workers/employee

performance as to determine their wages, compensations and allocate works.

Accounts-receivable Report: This report involves list of all the trade debts, accounts

receivables and bills receivables details. This is major report which determines enterprise's actual

collection period. By analysis of this report managers can determine whether debtors are capable

to repay their debts and assess any probability of deb-debts. Alpha's managers apply information

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

of this report to determine the credit policy in relation to debtors. This allow managerial staff to

manage cash-flows by enhancing cash collections.

Budget reports: In this method organisation use to built budget reports in order to

analysis their workforce performance (Fisher and Krumwiede, 2012). Budget report is based on

the collection of provisos data. In this method managers set a target which must be fulfilled in

prescribe time limit. After that managers identifying differences of set target and achieve target

and then make policies to reduce the gap of current and budget target. In Alpha management

apply this approach to assess the actual performance status in different areas by analysis of

variations. This is most critical report which defines the actual efficiency level.

D1. Integration of MA-systems within organisation:

Core function of managerial accounting is to provide critical and meaningful information

for management's decision making tasks, which make it necessary to integrate MA systems

within enterprise. Since lack of integration lead to barrier in generation of such information and

eventually affects decision making. In an enterprise such as Alpha Limited, financial and

accounting reporting functions and processes provide relevant information that is utilized in

more than one MA-systems, thus requiring formal integration for rapid information generation.

TASK 2

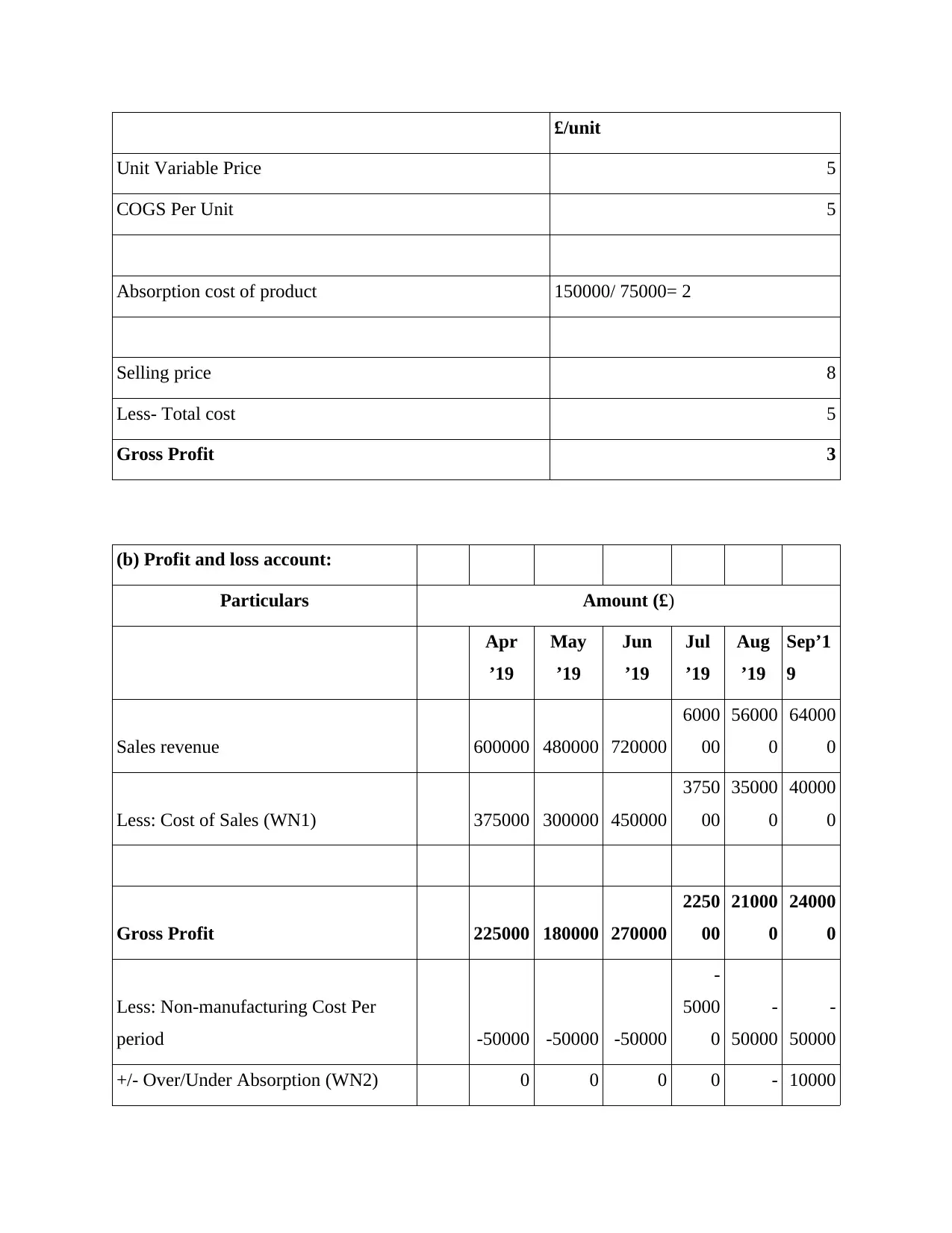

P3. Calculation of costs on the basis of marginal and absorption costing method:

Marginal costing: Marginal costs reflect additional costs generated when incremental units are

generated. It is determined by considering the overall increase in cost of producing additional

goods, as well as dividing this by changing number of goods manufactured. Under marginal

costing, marginal cost is measured to assess the actual profitability level.

Absorption Costing: The phrase "absorption costing" relates to the mechanism by which all the

expenses relating to production process are applied and then assigned separately to the goods.

This costing approach is important as per accounting standards to generate a stock value that is

recorded in an organisation's balance sheet.

Absorption costing:

(a) Cost card

Cost card (Absorption costing)

manage cash-flows by enhancing cash collections.

Budget reports: In this method organisation use to built budget reports in order to

analysis their workforce performance (Fisher and Krumwiede, 2012). Budget report is based on

the collection of provisos data. In this method managers set a target which must be fulfilled in

prescribe time limit. After that managers identifying differences of set target and achieve target

and then make policies to reduce the gap of current and budget target. In Alpha management

apply this approach to assess the actual performance status in different areas by analysis of

variations. This is most critical report which defines the actual efficiency level.

D1. Integration of MA-systems within organisation:

Core function of managerial accounting is to provide critical and meaningful information

for management's decision making tasks, which make it necessary to integrate MA systems

within enterprise. Since lack of integration lead to barrier in generation of such information and

eventually affects decision making. In an enterprise such as Alpha Limited, financial and

accounting reporting functions and processes provide relevant information that is utilized in

more than one MA-systems, thus requiring formal integration for rapid information generation.

TASK 2

P3. Calculation of costs on the basis of marginal and absorption costing method:

Marginal costing: Marginal costs reflect additional costs generated when incremental units are

generated. It is determined by considering the overall increase in cost of producing additional

goods, as well as dividing this by changing number of goods manufactured. Under marginal

costing, marginal cost is measured to assess the actual profitability level.

Absorption Costing: The phrase "absorption costing" relates to the mechanism by which all the

expenses relating to production process are applied and then assigned separately to the goods.

This costing approach is important as per accounting standards to generate a stock value that is

recorded in an organisation's balance sheet.

Absorption costing:

(a) Cost card

Cost card (Absorption costing)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

£/unit

Unit Variable Price 5

COGS Per Unit 5

Absorption cost of product 150000/ 75000= 2

Selling price 8

Less- Total cost 5

Gross Profit 3

(b) Profit and loss account:

Particulars Amount (£)

Apr

’19

May

’19

Jun

’19

Jul

’19

Aug

’19

Sep’1

9

Sales revenue 600000 480000 720000

6000

00

56000

0

64000

0

Less: Cost of Sales (WN1) 375000 300000 450000

3750

00

35000

0

40000

0

Gross Profit 225000 180000 270000

2250

00

21000

0

24000

0

Less: Non-manufacturing Cost Per

period -50000 -50000 -50000

-

5000

0

-

50000

-

50000

+/- Over/Under Absorption (WN2) 0 0 0 0 - 10000

Unit Variable Price 5

COGS Per Unit 5

Absorption cost of product 150000/ 75000= 2

Selling price 8

Less- Total cost 5

Gross Profit 3

(b) Profit and loss account:

Particulars Amount (£)

Apr

’19

May

’19

Jun

’19

Jul

’19

Aug

’19

Sep’1

9

Sales revenue 600000 480000 720000

6000

00

56000

0

64000

0

Less: Cost of Sales (WN1) 375000 300000 450000

3750

00

35000

0

40000

0

Gross Profit 225000 180000 270000

2250

00

21000

0

24000

0

Less: Non-manufacturing Cost Per

period -50000 -50000 -50000

-

5000

0

-

50000

-

50000

+/- Over/Under Absorption (WN2) 0 0 0 0 - 10000

20000

Net Profit/Loss 175000 130000 220000

1750

00

14000

0

20000

0

WNI

Calculation of Variable cost

Apr

’19

May

’19

Jun

’19

Jul

’19

Aug

’19

Sep’1

9

Opening stock 0 0 75000 0 0 75000

Production cost 375000 375000 375000

3750

00

42500

0

35000

0

Less closing stock 0 -75000 0 0

-

75000

-

25000

375000 300000 450000

3750

00

35000

0

40000

0

WN2

Calculation of Over absorption/ Under absorption

Apr

’19

May

’19 Jun ’19

Jul

’19

Aug

’19

Sep’1

9

Fixed Production Overhead with budgeted

production 150000

15000

0 150000

15000

0

15000

0

15000

0

Fixed Production Overhead with actual

production

-

150000

-

15000

0 -150000

-

15000

0

-

17000

0

-

14000

0

Over/ Under absorption 0 0 0 0

-

20000 10000

Net Profit/Loss 175000 130000 220000

1750

00

14000

0

20000

0

WNI

Calculation of Variable cost

Apr

’19

May

’19

Jun

’19

Jul

’19

Aug

’19

Sep’1

9

Opening stock 0 0 75000 0 0 75000

Production cost 375000 375000 375000

3750

00

42500

0

35000

0

Less closing stock 0 -75000 0 0

-

75000

-

25000

375000 300000 450000

3750

00

35000

0

40000

0

WN2

Calculation of Over absorption/ Under absorption

Apr

’19

May

’19 Jun ’19

Jul

’19

Aug

’19

Sep’1

9

Fixed Production Overhead with budgeted

production 150000

15000

0 150000

15000

0

15000

0

15000

0

Fixed Production Overhead with actual

production

-

150000

-

15000

0 -150000

-

15000

0

-

17000

0

-

14000

0

Over/ Under absorption 0 0 0 0

-

20000 10000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Marginal Costing:

(a) Cost card

Cost card (Marginal costing)

£/unit

Unit Variable Price 3

Marginal Cost 3

Selling price 8

Less- Marginal cost 3

Contribution 5

(b) Profit and loss account:

Particulars Amount (£)

Apr

’19

May

’19

Jun

’19 Jul ’19

Aug

’19 Sep’19

Sales revenue

60000

0

48000

0

72000

0

60000

0

56000

0

64000

0

Less: Variable cost

-

22500

0

-

18000

0

-

27000

0

-

22500

0

-

21000

0

-

24000

0

Contribution Margin

37500

0

30000

0

45000

0

37500

0

35000

0

40000

0

Less: Fixed Manufacturing Overheads

15000

0

15000

0

15000

0

15000

0

15000

0

15000

0

(a) Cost card

Cost card (Marginal costing)

£/unit

Unit Variable Price 3

Marginal Cost 3

Selling price 8

Less- Marginal cost 3

Contribution 5

(b) Profit and loss account:

Particulars Amount (£)

Apr

’19

May

’19

Jun

’19 Jul ’19

Aug

’19 Sep’19

Sales revenue

60000

0

48000

0

72000

0

60000

0

56000

0

64000

0

Less: Variable cost

-

22500

0

-

18000

0

-

27000

0

-

22500

0

-

21000

0

-

24000

0

Contribution Margin

37500

0

30000

0

45000

0

37500

0

35000

0

40000

0

Less: Fixed Manufacturing Overheads

15000

0

15000

0

15000

0

15000

0

15000

0

15000

0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Less: Non-manufacturing Cost Per

period 50000 50000 50000 50000 50000 50000

Net Profit/Loss

17500

0

10000

0

25000

0

17500

0

15000

0

20000

0

WN1

Calculation of Variable Cost

Variable cost

Apr

’19

May

’19

Jun

’19 Jul ’19

Aug

’19 Sep’19

Opening stock 0 45000 0 0 45000

Production cost

22500

0

22500

0

22500

0

22500

0

25500

0

21000

0

Less closing stock 0 -45000 0 0 -45000 -15000

22500

0

18000

0

27000

0

22500

0

21000

0

24000

0

Reconciliation of Net Income under Absorption and Marginal Costing

Apr ’19 May ’19 Jun ’19 Jul ’19 Aug ’19 Sep’19

Net Profit as per Absorption

Costing 175000 130000 220000 175000 140000 200000

+Changes in Opening Stock 0 0 30000 0 0 -30000

- Changes in Closing Stock 0 -30000 0 0 30000 20000

under and over absorption rate - - - - -20000 10000

period 50000 50000 50000 50000 50000 50000

Net Profit/Loss

17500

0

10000

0

25000

0

17500

0

15000

0

20000

0

WN1

Calculation of Variable Cost

Variable cost

Apr

’19

May

’19

Jun

’19 Jul ’19

Aug

’19 Sep’19

Opening stock 0 45000 0 0 45000

Production cost

22500

0

22500

0

22500

0

22500

0

25500

0

21000

0

Less closing stock 0 -45000 0 0 -45000 -15000

22500

0

18000

0

27000

0

22500

0

21000

0

24000

0

Reconciliation of Net Income under Absorption and Marginal Costing

Apr ’19 May ’19 Jun ’19 Jul ’19 Aug ’19 Sep’19

Net Profit as per Absorption

Costing 175000 130000 220000 175000 140000 200000

+Changes in Opening Stock 0 0 30000 0 0 -30000

- Changes in Closing Stock 0 -30000 0 0 30000 20000

under and over absorption rate - - - - -20000 10000

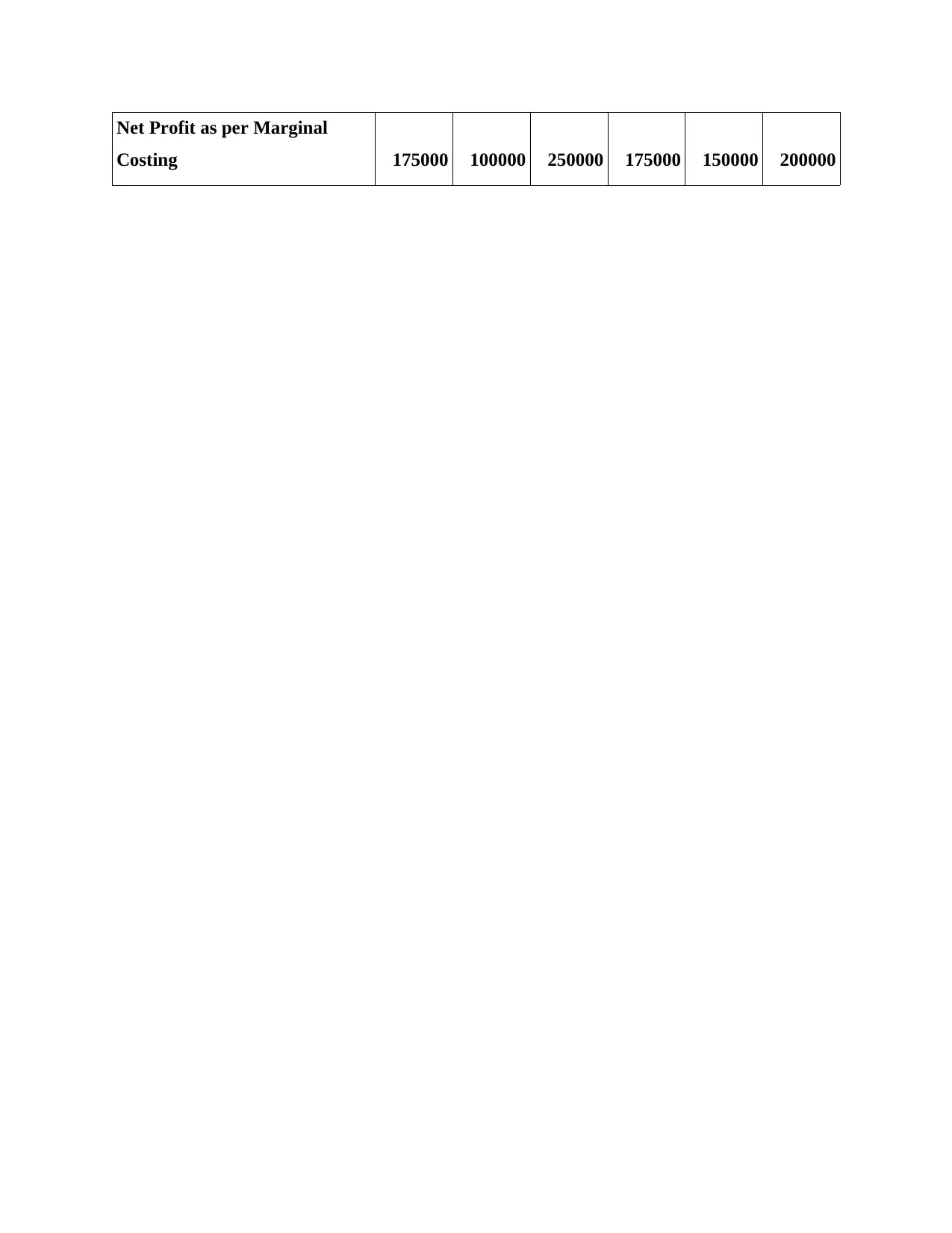

Net Profit as per Marginal

Costing 175000 100000 250000 175000 150000 200000

Costing 175000 100000 250000 175000 150000 200000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.