Management Accounting Report: Principles, Techniques, and Analysis

VerifiedAdded on 2020/12/01

|28

|8475

|118

Report

AI Summary

This report provides a comprehensive overview of management accounting, detailing its principles, processes, and techniques. It explores the management accounting system, its integration within organizations, and its historical origins. The report delves into key concepts such as cost accounting, inventory management, and microeconomic techniques, including cost analysis and cost-volume-profit analysis. It further examines budgeting processes, pricing strategies, and performance measurement tools, including key performance indicators (KPIs). The report also touches upon management's role in areas such as leadership, communication, and knowledge management. It concludes by summarizing the importance of management accounting in decision-making and organizational success. The report is a valuable resource for understanding the multifaceted nature of management accounting and its practical applications.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Management Accounting:...........................................................................................................................5

Management Accounting System:...............................................................................................................6

Integrate in organization:............................................................................................................................6

Origin:..........................................................................................................................................................6

Its role was just informed search (mclany, 2009)........................................................................................6

Management Accounting Principle:............................................................................................................6

Credibility....................................................................................................................................................7

Aggregation.................................................................................................................................................8

Efficient behavior.........................................................................................................................................8

Reporting Focus...................................................................................................................................8

Proven Information.....................................................................................................................................8

Reporting Focus...........................................................................................................................................8

Standards....................................................................................................................................................8

System.........................................................................................................................................................8

Timing..........................................................................................................................................................8

Valuation.....................................................................................................................................................9

Management Accounting Process...............................................................................................................9

Cost accounting System...............................................................................................................................9

Inventory management.............................................................................................................................10

These are the few types of managerial account system............................................................................10

Micro Economics techniques:....................................................................................................................11

Cost :..........................................................................................................................................................11

Cost Analysis..............................................................................................................................................11

Cost Volume profit:...................................................................................................................................11

Price Costing:.............................................................................................................................................13

Fixed costing..............................................................................................................................................13

Variable costing:........................................................................................................................................14

Normal Costing:.........................................................................................................................................14

Standard Costing:......................................................................................................................................14

Inventory Cost:..........................................................................................................................................14

Types of Cost Inventory:............................................................................................................................15

Management Accounting:...........................................................................................................................5

Management Accounting System:...............................................................................................................6

Integrate in organization:............................................................................................................................6

Origin:..........................................................................................................................................................6

Its role was just informed search (mclany, 2009)........................................................................................6

Management Accounting Principle:............................................................................................................6

Credibility....................................................................................................................................................7

Aggregation.................................................................................................................................................8

Efficient behavior.........................................................................................................................................8

Reporting Focus...................................................................................................................................8

Proven Information.....................................................................................................................................8

Reporting Focus...........................................................................................................................................8

Standards....................................................................................................................................................8

System.........................................................................................................................................................8

Timing..........................................................................................................................................................8

Valuation.....................................................................................................................................................9

Management Accounting Process...............................................................................................................9

Cost accounting System...............................................................................................................................9

Inventory management.............................................................................................................................10

These are the few types of managerial account system............................................................................10

Micro Economics techniques:....................................................................................................................11

Cost :..........................................................................................................................................................11

Cost Analysis..............................................................................................................................................11

Cost Volume profit:...................................................................................................................................11

Price Costing:.............................................................................................................................................13

Fixed costing..............................................................................................................................................13

Variable costing:........................................................................................................................................14

Normal Costing:.........................................................................................................................................14

Standard Costing:......................................................................................................................................14

Inventory Cost:..........................................................................................................................................14

Types of Cost Inventory:............................................................................................................................15

Cost inventory:..........................................................................................................................................15

Types of inventory cost System:................................................................................................................15

Benefits of reducing inventory cost...........................................................................................................15

Material cost.............................................................................................................................................15

Material Maintenance:..............................................................................................................................16

Price of competitive:.................................................................................................................................16

Increase profit...........................................................................................................................................16

Budget.......................................................................................................................................................16

Operating Budget:.....................................................................................................................................16

Incremental Budgeting:.............................................................................................................................17

Activity based budgeting:..........................................................................................................................17

Value proposition budgeting:....................................................................................................................17

Zero based budget:....................................................................................................................................17

Flexible Budgeting Method........................................................................................................................17

Pricing:.......................................................................................................................................................18

Pricing Strategy..........................................................................................................................................18

Common Pricing Strategy:.........................................................................................................................18

Plus Cost price...........................................................................................................................................18

Budget controlling process:.......................................................................................................................18

Advantages:...............................................................................................................................................19

Getting Maximum Profit............................................................................................................................19

Coordination:.............................................................................................................................................19

Performance Measurement Tools.............................................................................................................19

Expenses....................................................................................................................................................19

Consciousness...........................................................................................................................................19

Incentives:.................................................................................................................................................19

Limitations in budget controlling:..............................................................................................................19

Future uncertainty.....................................................................................................................................19

Budget revision:.........................................................................................................................................19

Reduce efficiency:......................................................................................................................................20

Problem in coordination:...........................................................................................................................20

Interdepartmental conflicts:......................................................................................................................20

Top Management dependent:...................................................................................................................20

Types of inventory cost System:................................................................................................................15

Benefits of reducing inventory cost...........................................................................................................15

Material cost.............................................................................................................................................15

Material Maintenance:..............................................................................................................................16

Price of competitive:.................................................................................................................................16

Increase profit...........................................................................................................................................16

Budget.......................................................................................................................................................16

Operating Budget:.....................................................................................................................................16

Incremental Budgeting:.............................................................................................................................17

Activity based budgeting:..........................................................................................................................17

Value proposition budgeting:....................................................................................................................17

Zero based budget:....................................................................................................................................17

Flexible Budgeting Method........................................................................................................................17

Pricing:.......................................................................................................................................................18

Pricing Strategy..........................................................................................................................................18

Common Pricing Strategy:.........................................................................................................................18

Plus Cost price...........................................................................................................................................18

Budget controlling process:.......................................................................................................................18

Advantages:...............................................................................................................................................19

Getting Maximum Profit............................................................................................................................19

Coordination:.............................................................................................................................................19

Performance Measurement Tools.............................................................................................................19

Expenses....................................................................................................................................................19

Consciousness...........................................................................................................................................19

Incentives:.................................................................................................................................................19

Limitations in budget controlling:..............................................................................................................19

Future uncertainty.....................................................................................................................................19

Budget revision:.........................................................................................................................................19

Reduce efficiency:......................................................................................................................................20

Problem in coordination:...........................................................................................................................20

Interdepartmental conflicts:......................................................................................................................20

Top Management dependent:...................................................................................................................20

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Costing System:.........................................................................................................................................20

Actual Costing System...............................................................................................................................20

Affinity Diagram.........................................................................................................................................20

Tree Diagram:............................................................................................................................................21

Inter relationship Diagram:.......................................................................................................................21

Matrix Diagram:.........................................................................................................................................21

What is PEST?............................................................................................................................................21

SWOT:........................................................................................................................................................21

Bench Marker:...........................................................................................................................................22

Key Performance indicator:.......................................................................................................................22

Financial key performance:.......................................................................................................................22

Non-Financial Key performance:...............................................................................................................22

Importance of KPI:.....................................................................................................................................23

Budget target:...........................................................................................................................................23

Finance Governess:...................................................................................................................................23

Monitoring strategy...................................................................................................................................24

Accounting Management..........................................................................................................................24

Leadership:................................................................................................................................................24

Experiences:..............................................................................................................................................24

Communicating Skills:................................................................................................................................24

Management of Knowledge:.....................................................................................................................24

Organizations:...........................................................................................................................................24

Managing Time:.........................................................................................................................................24

Reliance:....................................................................................................................................................25

Delegates:..................................................................................................................................................25

Be Confident:.............................................................................................................................................25

Employees respect:...................................................................................................................................25

Conclusion:................................................................................................................................................26

Reference:.................................................................................................................................................26

Actual Costing System...............................................................................................................................20

Affinity Diagram.........................................................................................................................................20

Tree Diagram:............................................................................................................................................21

Inter relationship Diagram:.......................................................................................................................21

Matrix Diagram:.........................................................................................................................................21

What is PEST?............................................................................................................................................21

SWOT:........................................................................................................................................................21

Bench Marker:...........................................................................................................................................22

Key Performance indicator:.......................................................................................................................22

Financial key performance:.......................................................................................................................22

Non-Financial Key performance:...............................................................................................................22

Importance of KPI:.....................................................................................................................................23

Budget target:...........................................................................................................................................23

Finance Governess:...................................................................................................................................23

Monitoring strategy...................................................................................................................................24

Accounting Management..........................................................................................................................24

Leadership:................................................................................................................................................24

Experiences:..............................................................................................................................................24

Communicating Skills:................................................................................................................................24

Management of Knowledge:.....................................................................................................................24

Organizations:...........................................................................................................................................24

Managing Time:.........................................................................................................................................24

Reliance:....................................................................................................................................................25

Delegates:..................................................................................................................................................25

Be Confident:.............................................................................................................................................25

Employees respect:...................................................................................................................................25

Conclusion:................................................................................................................................................26

Reference:.................................................................................................................................................26

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Introduction:

In this project we mainly discuss about management accounting, management accounting

principles and management accounting process. In task 2 we learn about microeconomics

techniques, cost analysis, inventory cost and types of inventory cost system. In task 3 we

discuss we budget, common pricing strategy, and performance management tools. In task 4 we

learn about bench marker importance of KPI communicating strategies, budget targets, and

important techniques of managements

Task 1

Management Accounting

Management accounting is type of establishing activities, evaluating, accessing,

interpreting and transmitting information to managers. Management of accounting

includes all policies aimed at remaining management. It used information relating

at cost of goods or offers that company purchases. Budgets used to calculate

decisions in the well-disciplined form of organization. Management accounting uses

it

efficiently.Reports showing variances in real outcomes from budgets. The key

distinction between management and financial accounting is used for calculating

the finance of statements. Whereas management accounting to keep an eye on

company transactions.

In this project we mainly discuss about management accounting, management accounting

principles and management accounting process. In task 2 we learn about microeconomics

techniques, cost analysis, inventory cost and types of inventory cost system. In task 3 we

discuss we budget, common pricing strategy, and performance management tools. In task 4 we

learn about bench marker importance of KPI communicating strategies, budget targets, and

important techniques of managements

Task 1

Management Accounting

Management accounting is type of establishing activities, evaluating, accessing,

interpreting and transmitting information to managers. Management of accounting

includes all policies aimed at remaining management. It used information relating

at cost of goods or offers that company purchases. Budgets used to calculate

decisions in the well-disciplined form of organization. Management accounting uses

it

efficiently.Reports showing variances in real outcomes from budgets. The key

distinction between management and financial accounting is used for calculating

the finance of statements. Whereas management accounting to keep an eye on

company transactions.

Management Accounting System:

Internal accounting management systems does not used to give

important managing knowledge for the decision-

making of operational business. A company that manufacture use the system

in assist in costing and management of their process. [Peshori, Kishore 2015] The

hospital can use management system to assist Them along with for

insurance other in house billing requirement.

This system different within industries to provide functions

Integrate in organization:

Management accounting

lets administrators within an organization make choices. It is also known as

cost accounting, management accounting that is method of defining

evaluating, interpreting and transmitting facts to administrators in

helping accomplish company objectives. Both accounting areas covering the

administration of corporate activities related to the expense of goods or servi

ces obtained by the organisation shall

be included in the data gathered (Research Report No. R-1428-08-

RR). Accountants use budgets to calculate the corporate spending schedule.

The report on success is used for observing the disparity between current ou

tcomes and the expected results.

Origin:

Its role was just informed search (mclany, 2009)

This website of the institute of management accountant describe management accounting as

“A profession that involves partnering in management decision making, planning and

performance management system”.

Management Accounting Principle:

1. Influence :Communication provides a vital perspective. Communication is beginning and end

of accounting administration. It enhances decision-making by having the necessary insight into all

decision-making processes. Sound exchange of vital knowledge allows management accounting to

intersect silos and facilities an interconnected thinking process process. The effects of steps taken in one

company divide on the other divide can be readily interpreted, accepted or altered.It is also easier to

create and analyses the most important knowledge when addressing the criteria of company decision-

makers. It means that it is necessary for the decision maker to make recommendations and to obtain

influence.

2. Plausibility:For everybody, knowledge is important. Management accounting tests for the best

possible information services, important to the decision made by the people who decide themselves

It needs to achieve a right balance: Present, current and future-related information Foreign and internal

data. Financial and non-financial information, for example environmental and social problems

Internal accounting management systems does not used to give

important managing knowledge for the decision-

making of operational business. A company that manufacture use the system

in assist in costing and management of their process. [Peshori, Kishore 2015] The

hospital can use management system to assist Them along with for

insurance other in house billing requirement.

This system different within industries to provide functions

Integrate in organization:

Management accounting

lets administrators within an organization make choices. It is also known as

cost accounting, management accounting that is method of defining

evaluating, interpreting and transmitting facts to administrators in

helping accomplish company objectives. Both accounting areas covering the

administration of corporate activities related to the expense of goods or servi

ces obtained by the organisation shall

be included in the data gathered (Research Report No. R-1428-08-

RR). Accountants use budgets to calculate the corporate spending schedule.

The report on success is used for observing the disparity between current ou

tcomes and the expected results.

Origin:

Its role was just informed search (mclany, 2009)

This website of the institute of management accountant describe management accounting as

“A profession that involves partnering in management decision making, planning and

performance management system”.

Management Accounting Principle:

1. Influence :Communication provides a vital perspective. Communication is beginning and end

of accounting administration. It enhances decision-making by having the necessary insight into all

decision-making processes. Sound exchange of vital knowledge allows management accounting to

intersect silos and facilities an interconnected thinking process process. The effects of steps taken in one

company divide on the other divide can be readily interpreted, accepted or altered.It is also easier to

create and analyses the most important knowledge when addressing the criteria of company decision-

makers. It means that it is necessary for the decision maker to make recommendations and to obtain

influence.

2. Plausibility:For everybody, knowledge is important. Management accounting tests for the best

possible information services, important to the decision made by the people who decide themselves

It needs to achieve a right balance: Present, current and future-related information Foreign and internal

data. Financial and non-financial information, for example environmental and social problems

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3. Worth Value It is calculated the effect on value. Management accounting

binds the operations of the enterprise to its fundamental corporate model an

d demands a clear awareness of the wider macroeconomic environment. It in

cludes analysing the knowledge along the road of value generation, evaluati

ng the possibility

That could be offered and focusing on risks , costs and opportunities for valu

e generation.

Analysis of circumstances contributes to the review of decision-making.

Thus, companies may determine better to complete or take advantage of

scenario modelling to analyse the effects of particular opportunities and chall

enges.

Furthermore, the models help businesses to measure the potential to achiev

e

or to face risks and the profit to be generated or erode

4. Credibility

Creditworthiness is stewardship. Responsibility and monitoring add even

more to making decision-making. Short term corporate interest for

shareholders against long term increases trust and reliability. [Greenes, K. &

Piktialis, D. (July 2008) ]Experts in management accounting are considered to

be legal, accountable and mindful of values, policy standards and

interpersonal responsibilities of the company. Knowing inconsistent

preferences boosts control of stakeholders and also is an important

consideration in prioritizing stakeholder units. Proactively seeking to collect

input and be open to questions or poor feedback helps employees to track

the overall efficiency of the company. This increases the company 's

credibility, integrity and honesty and tends to enhance systems and forces.

The distinction between management and financial accounting is

Management accounting professionals are considered legal, responsible and

aware of the company's principles, policy norms and interpersonal

obligations. Knowing inconsistent priorities increases stakeholder power and

is also an important factor in giving priority to stakeholder units. Proactively

trying to gain information and to be open to concerns or bad reviews allows

staff to control the company's overall effectiveness. This improves the

prestige, dignity and fairness of the business and helps to strengthen

structures and powers.

binds the operations of the enterprise to its fundamental corporate model an

d demands a clear awareness of the wider macroeconomic environment. It in

cludes analysing the knowledge along the road of value generation, evaluati

ng the possibility

That could be offered and focusing on risks , costs and opportunities for valu

e generation.

Analysis of circumstances contributes to the review of decision-making.

Thus, companies may determine better to complete or take advantage of

scenario modelling to analyse the effects of particular opportunities and chall

enges.

Furthermore, the models help businesses to measure the potential to achiev

e

or to face risks and the profit to be generated or erode

4. Credibility

Creditworthiness is stewardship. Responsibility and monitoring add even

more to making decision-making. Short term corporate interest for

shareholders against long term increases trust and reliability. [Greenes, K. &

Piktialis, D. (July 2008) ]Experts in management accounting are considered to

be legal, accountable and mindful of values, policy standards and

interpersonal responsibilities of the company. Knowing inconsistent

preferences boosts control of stakeholders and also is an important

consideration in prioritizing stakeholder units. Proactively seeking to collect

input and be open to questions or poor feedback helps employees to track

the overall efficiency of the company. This increases the company 's

credibility, integrity and honesty and tends to enhance systems and forces.

The distinction between management and financial accounting is

Management accounting professionals are considered legal, responsible and

aware of the company's principles, policy norms and interpersonal

obligations. Knowing inconsistent priorities increases stakeholder power and

is also an important factor in giving priority to stakeholder units. Proactively

trying to gain information and to be open to concerns or bad reviews allows

staff to control the company's overall effectiveness. This improves the

prestige, dignity and fairness of the business and helps to strengthen

structures and powers.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The disparity between financial accounting and management is as much as

5.Aggregation

Earnings for a whole company are reported in financial accounting. In handlin

g budgets, the income by the product, product line, client and geographical a

rea are almost always more comprehensive.

Efficient behavior

Financial accounting report on performance of a company, while

Reporting Focus

The requirement of functional accounting is on the documents to be held

with significant accuracy to show their correctness. Management accounting

also presents estimates instead of verifiable and confirmed evidence

(Accounting Made Simple –by Mike Piper)

Proven Information

Financial accounting requires the accuracy of documents, which are used to

prove the accuracy of financial statements. Management accounts also work

with estimates instead of verifiable variables that have been confirmed.

Reporting Focus

Financial management is directed at the production of financial records, both

in- and out of-society. Operational accounts, which only distribute within a co

mpany, concern management accounting

Standards

Financial accounting must follow different accounting requirements, while ad

ministrative accounting

must not meet such standards when data is gathered for domestic use.

System

The total method a organisation will earn profit should not pay much attentio

n to financial accounting but for its result. Inversely, administrators tend to s

ee where bottleneck processes take place and how to boost their profits by a

ddressing challenges with a bottleneck.

Timing

Financial accounting demands that at the conclusion of an accounting cycle

the financial reports be published. Managers should report more often and it

offers information that is more valuable to managers because they see it

immediately

Valuation

5.Aggregation

Earnings for a whole company are reported in financial accounting. In handlin

g budgets, the income by the product, product line, client and geographical a

rea are almost always more comprehensive.

Efficient behavior

Financial accounting report on performance of a company, while

Reporting Focus

The requirement of functional accounting is on the documents to be held

with significant accuracy to show their correctness. Management accounting

also presents estimates instead of verifiable and confirmed evidence

(Accounting Made Simple –by Mike Piper)

Proven Information

Financial accounting requires the accuracy of documents, which are used to

prove the accuracy of financial statements. Management accounts also work

with estimates instead of verifiable variables that have been confirmed.

Reporting Focus

Financial management is directed at the production of financial records, both

in- and out of-society. Operational accounts, which only distribute within a co

mpany, concern management accounting

Standards

Financial accounting must follow different accounting requirements, while ad

ministrative accounting

must not meet such standards when data is gathered for domestic use.

System

The total method a organisation will earn profit should not pay much attentio

n to financial accounting but for its result. Inversely, administrators tend to s

ee where bottleneck processes take place and how to boost their profits by a

ddressing challenges with a bottleneck.

Timing

Financial accounting demands that at the conclusion of an accounting cycle

the financial reports be published. Managers should report more often and it

offers information that is more valuable to managers because they see it

immediately

Valuation

Financial management addresses the correct appraisal of properties and

obligations and thereby deficiencies, reassessments, etc. The valuation of

these things, just their productivity, is not associated with management

accounting.

Management Accounting Process

There are two main types of management accounting system namely

Costing system

Inventory Management

Cost accounting System

In order to measure the cost of its goods in terms of inventory assessment, profitability

measurement and cost management, the company applied a costing method or costing system.

Cost distribution is based on both the activity-based costing system and the conventional costing

system in the cost accounting system. For efficient functions, approximating the real prices of

goods is important Cost accounts are the type of accounting system intended to collect

operating costs by weighing the supply costs or production managemental financial problem

assessment The costing system Managers rely on accounting data generally and specifically on c

ost, as their cost can explain any task of the

company. Cost accounting is considered as a core principle of management accounting since it p

rovides the empirical means for ensuring that management successfully performs its reproductiv

ity, such as budgetary regulation, marginal cost, Normal costing, running costs and inventory co

ntrol. (Accounting Made Simple –by Mike Piper)

obligations and thereby deficiencies, reassessments, etc. The valuation of

these things, just their productivity, is not associated with management

accounting.

Management Accounting Process

There are two main types of management accounting system namely

Costing system

Inventory Management

Cost accounting System

In order to measure the cost of its goods in terms of inventory assessment, profitability

measurement and cost management, the company applied a costing method or costing system.

Cost distribution is based on both the activity-based costing system and the conventional costing

system in the cost accounting system. For efficient functions, approximating the real prices of

goods is important Cost accounts are the type of accounting system intended to collect

operating costs by weighing the supply costs or production managemental financial problem

assessment The costing system Managers rely on accounting data generally and specifically on c

ost, as their cost can explain any task of the

company. Cost accounting is considered as a core principle of management accounting since it p

rovides the empirical means for ensuring that management successfully performs its reproductiv

ity, such as budgetary regulation, marginal cost, Normal costing, running costs and inventory co

ntrol. (Accounting Made Simple –by Mike Piper)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Inventory management

The management of stocks relates to the way that materials are managed

and monitored, used and processed by the organization in the manufacturing

of products it offers. Stock control system integrates bar-code inspection,

desktop applications, handheld devices and bar-code printers to improve

inventory management, including consumer products, materials, services

(Drury, 2015). It is also the case that volumes of the final product for sale are

regulated and tracked. The purpose of inventory management is to interpret

the current inventory levels correctly and to reduce overview and

interpretation of circumstances. Managers will have experience and will be

able to make adequate stock choices by the accurate monitoring of amounts

around the stock venue. One of the main investments and accounts for an

investment related to the goods sold is the inventory of a firm.

Inventory management functions: buying orders are made, inventory is

issued, relocated, changed and disposed of. In addition, they sell, collect,

bundle and ship goods (Drury, 2015). (Drury, 2015). Cycle reports and actual

inventory numbers, report creation, management, preparation and

distribution, and bar code labels are printed. The benefits of an

organization’s inventory control scheme include strengthening the

company's basics, improving inventory accuracy and improved business

workflow.

Reporting budget

Receivable account report

Cost managerial report

Report of performance

Other reporting

Cost accounting is managerial technique that aimed to take company total production cost by

assessing variable costs and fixed cost of production as well. i-e lease expenses

It is used internally by management to make business decision that are fully informed

It is flexible to meet needs of management

It consider both variable and fixed cost of production

It has usually following types

1. Standard costing

2. Activity based costing

3. Lean costing

4. Marginal coting

These are the few types of managerial account system

The management of stocks relates to the way that materials are managed

and monitored, used and processed by the organization in the manufacturing

of products it offers. Stock control system integrates bar-code inspection,

desktop applications, handheld devices and bar-code printers to improve

inventory management, including consumer products, materials, services

(Drury, 2015). It is also the case that volumes of the final product for sale are

regulated and tracked. The purpose of inventory management is to interpret

the current inventory levels correctly and to reduce overview and

interpretation of circumstances. Managers will have experience and will be

able to make adequate stock choices by the accurate monitoring of amounts

around the stock venue. One of the main investments and accounts for an

investment related to the goods sold is the inventory of a firm.

Inventory management functions: buying orders are made, inventory is

issued, relocated, changed and disposed of. In addition, they sell, collect,

bundle and ship goods (Drury, 2015). (Drury, 2015). Cycle reports and actual

inventory numbers, report creation, management, preparation and

distribution, and bar code labels are printed. The benefits of an

organization’s inventory control scheme include strengthening the

company's basics, improving inventory accuracy and improved business

workflow.

Reporting budget

Receivable account report

Cost managerial report

Report of performance

Other reporting

Cost accounting is managerial technique that aimed to take company total production cost by

assessing variable costs and fixed cost of production as well. i-e lease expenses

It is used internally by management to make business decision that are fully informed

It is flexible to meet needs of management

It consider both variable and fixed cost of production

It has usually following types

1. Standard costing

2. Activity based costing

3. Lean costing

4. Marginal coting

These are the few types of managerial account system

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Task #2

Micro Economics techniques:

Cost :

Cost accounting is managerial technique that aimed to take company total production cost by

assessing variable costs and fixed cost of production as well. i-e lease expenses

It is used internally by management to make business decision that are fully informed

It is flexible to meet needs of management

It consider both variable and fixed cost of production

It has usually following types

Standard costing

Activity based costing

Lean costing

Marginal coting

Cost Analysis.

Cost analysis is more of difficult because it usually involves more production unit.

By the use of this method review of the items services and related cost

solutions .In the present era many organizations hire purchase managers who

evaluate the value proposition of products by using past history ,general

experience and final decision by product owner.[ Held, J.S. & Posner, D. (1971).]

Cost Analysis has following major considerations

Required personnel

Total per hour work by personnel

Evaluation

Resource costing

Indirect cost of project

The simplest argument about the use of cost analysis is that where market analysis is

not practical, it is used. This is generally because there are no alternative comparative

options or no associated ideas for a work have been submitted. Cost analysis is typically

required for new forms of testing or product creation work or solutions focused on

particular patents or products.[Costing by Kenneth Boyd (2012)] The cost analysis

problem is to attempt to assess equal value without any marketable reference.

Cost Volume profit:

Cost volume analysis profit is simplest argument about the use of cost analysis is that

where market analysis is not practical, it is used. This is generally because there are no

Micro Economics techniques:

Cost :

Cost accounting is managerial technique that aimed to take company total production cost by

assessing variable costs and fixed cost of production as well. i-e lease expenses

It is used internally by management to make business decision that are fully informed

It is flexible to meet needs of management

It consider both variable and fixed cost of production

It has usually following types

Standard costing

Activity based costing

Lean costing

Marginal coting

Cost Analysis.

Cost analysis is more of difficult because it usually involves more production unit.

By the use of this method review of the items services and related cost

solutions .In the present era many organizations hire purchase managers who

evaluate the value proposition of products by using past history ,general

experience and final decision by product owner.[ Held, J.S. & Posner, D. (1971).]

Cost Analysis has following major considerations

Required personnel

Total per hour work by personnel

Evaluation

Resource costing

Indirect cost of project

The simplest argument about the use of cost analysis is that where market analysis is

not practical, it is used. This is generally because there are no alternative comparative

options or no associated ideas for a work have been submitted. Cost analysis is typically

required for new forms of testing or product creation work or solutions focused on

particular patents or products.[Costing by Kenneth Boyd (2012)] The cost analysis

problem is to attempt to assess equal value without any marketable reference.

Cost Volume profit:

Cost volume analysis profit is simplest argument about the use of cost analysis is that

where market analysis is not practical, it is used. This is generally because there are no

alternative comparative options or no associated ideas for a work have been submitted.

Cost analysis is typically required for new forms of testing or product creation work or

solutions focused on particular patents or products. The cost analysis problem is to

attempt to assess equal value without any marketable reference.

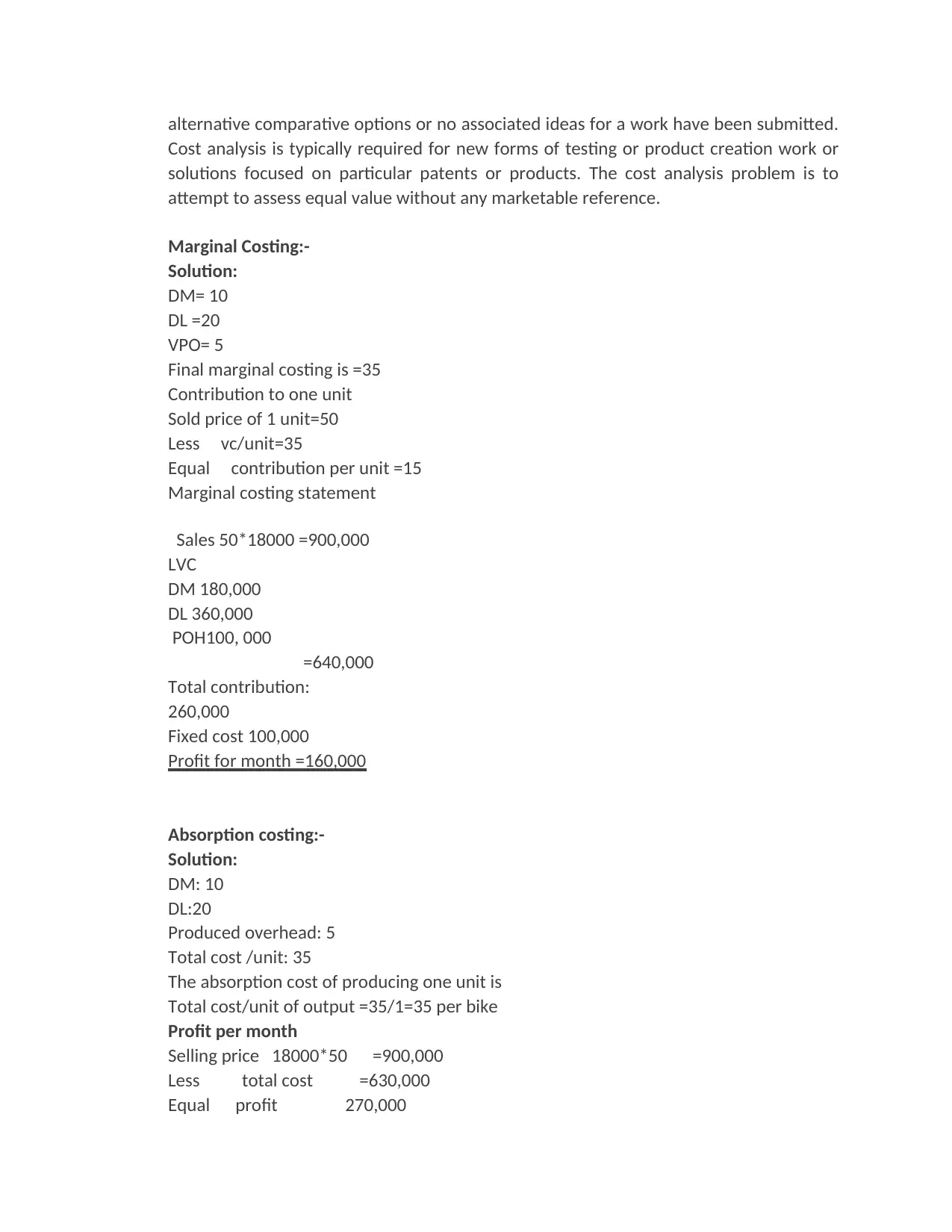

Marginal Costing:-

Solution:

DM= 10

DL =20

VPO= 5

Final marginal costing is =35

Contribution to one unit

Sold price of 1 unit=50

Less vc/unit=35

Equal contribution per unit =15

Marginal costing statement

Sales 50*18000 =900,000

LVC

DM 180,000

DL 360,000

POH100, 000

=640,000

Total contribution:

260,000

Fixed cost 100,000

Profit for month =160,000

Absorption costing:-

Solution:

DM: 10

DL:20

Produced overhead: 5

Total cost /unit: 35

The absorption cost of producing one unit is

Total cost/unit of output =35/1=35 per bike

Profit per month

Selling price 18000*50 =900,000

Less total cost =630,000

Equal profit 270,000

Cost analysis is typically required for new forms of testing or product creation work or

solutions focused on particular patents or products. The cost analysis problem is to

attempt to assess equal value without any marketable reference.

Marginal Costing:-

Solution:

DM= 10

DL =20

VPO= 5

Final marginal costing is =35

Contribution to one unit

Sold price of 1 unit=50

Less vc/unit=35

Equal contribution per unit =15

Marginal costing statement

Sales 50*18000 =900,000

LVC

DM 180,000

DL 360,000

POH100, 000

=640,000

Total contribution:

260,000

Fixed cost 100,000

Profit for month =160,000

Absorption costing:-

Solution:

DM: 10

DL:20

Produced overhead: 5

Total cost /unit: 35

The absorption cost of producing one unit is

Total cost/unit of output =35/1=35 per bike

Profit per month

Selling price 18000*50 =900,000

Less total cost =630,000

Equal profit 270,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 28

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.