Management Accounting Report: System, Methods, and Analysis

VerifiedAdded on 2020/10/22

|21

|5731

|102

Report

AI Summary

This report provides a comprehensive overview of management accounting, covering essential aspects such as inventory management systems, cost accounting systems, and job costing systems. It delves into different reporting methods, including job cost methods, specific order costing, batch costing, and process costing, along with various types of reports like budget reports, cost reports, and variance analysis reports. The report also examines the benefits of management accounting systems and their integration with reporting systems, emphasizing their role in minimizing expenditure and enhancing operational efficiency. Furthermore, it includes calculations of marginal and absorption costing, and explores different budgetary tools, their advantages and disadvantages, and their application in preparing forecasting budgets. Finally, the report addresses the adaptation of management accounting systems to solve financial problems and the use of planning tools in financial analysis, offering a well-rounded understanding of the subject.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

LO 1.................................................................................................................................................1

1 Essential requirements of different types of management accounting system....................1

2. Different methods used for management accounting reporting.........................................3

3. Benefits of management accounting system......................................................................4

4.Integration of management accounting and reporting system.............................................5

LO 2 please don’t change................................................................................................................6

1. Calculation of marginal and absorption costing.................................................................6

LO 3.................................................................................................................................................8

1.Different types of budgetary tools and their advantages and disadvantages......................8

2. Application of different budgetary tools and their application in preparing forecasting

budgets..................................................................................................................................10

LO 4...............................................................................................................................................12

1. Adaption of management accounting system to solve financial problems......................16

Analyzing planning tools in solving financial problems......................................................17

CONCLUSIONS............................................................................................................................17

REFERENCES..............................................................................................................................18

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

LO 1.................................................................................................................................................1

1 Essential requirements of different types of management accounting system....................1

2. Different methods used for management accounting reporting.........................................3

3. Benefits of management accounting system......................................................................4

4.Integration of management accounting and reporting system.............................................5

LO 2 please don’t change................................................................................................................6

1. Calculation of marginal and absorption costing.................................................................6

LO 3.................................................................................................................................................8

1.Different types of budgetary tools and their advantages and disadvantages......................8

2. Application of different budgetary tools and their application in preparing forecasting

budgets..................................................................................................................................10

LO 4...............................................................................................................................................12

1. Adaption of management accounting system to solve financial problems......................16

Analyzing planning tools in solving financial problems......................................................17

CONCLUSIONS............................................................................................................................17

REFERENCES..............................................................................................................................18

INTRODUCTION

Management accounting is advice to the organization and provision of financial data use in

company and development of business. It is the procedure of preparing and developing

management reports and accounts that give timely and accurate statistical and financial

statements. It is used to give data to the internal users and support the company in making

decisions. Management accounting objective is to provide all the essential financial information

to management. For further information on MA, the report explain various requirements of

management accounting systems which includes Cost accounting system, Inventory management

system, and Job costing system. It will focus on various study that is used by company in process

of MA report. It will depict the importance of application of various management system in the

company. It will outline the different methods used for cost calculation which are marginal

costing and absorption costing and will help the company in finding out the better method

between these two. The report will finally show pro and cons of different budgetary control tools

and how the performance indicators are used to resolve financial problems of the organization.

MAIN BODY

LO 1

1 Essential requirements of different types of management accounting system

MA helps internal users in supplying all the applicable information. This system of the

company makes it easy for mangers by assembling information based on trend charts, break even

charts, budgeting, etc which help in forecasting future (Martello, 2016).

Essential requirements of different types of MA system are as follows :

Inventory management system

Company's inventory management system tracks good and raw materials throughout the

business operations. This system helps the manager of the company in making efficient decisions

related to investment and decisions related to manufacturing the raw material in the organization

or purchasing it from outside. The installation cost of this system is high but efficiency of work

gets high. It includes bar coding on the product, tools that are used to report quantity and price of

inventory. It helps the company in forecasting inventory by showing the requirement of raw

materials in the future, by alerting management about inventory in case it gets finished which

help manager in taking decisions (Maas, 2016). It helps in tracking the inventory with serial

1

Management accounting is advice to the organization and provision of financial data use in

company and development of business. It is the procedure of preparing and developing

management reports and accounts that give timely and accurate statistical and financial

statements. It is used to give data to the internal users and support the company in making

decisions. Management accounting objective is to provide all the essential financial information

to management. For further information on MA, the report explain various requirements of

management accounting systems which includes Cost accounting system, Inventory management

system, and Job costing system. It will focus on various study that is used by company in process

of MA report. It will depict the importance of application of various management system in the

company. It will outline the different methods used for cost calculation which are marginal

costing and absorption costing and will help the company in finding out the better method

between these two. The report will finally show pro and cons of different budgetary control tools

and how the performance indicators are used to resolve financial problems of the organization.

MAIN BODY

LO 1

1 Essential requirements of different types of management accounting system

MA helps internal users in supplying all the applicable information. This system of the

company makes it easy for mangers by assembling information based on trend charts, break even

charts, budgeting, etc which help in forecasting future (Martello, 2016).

Essential requirements of different types of MA system are as follows :

Inventory management system

Company's inventory management system tracks good and raw materials throughout the

business operations. This system helps the manager of the company in making efficient decisions

related to investment and decisions related to manufacturing the raw material in the organization

or purchasing it from outside. The installation cost of this system is high but efficiency of work

gets high. It includes bar coding on the product, tools that are used to report quantity and price of

inventory. It helps the company in forecasting inventory by showing the requirement of raw

materials in the future, by alerting management about inventory in case it gets finished which

help manager in taking decisions (Maas, 2016). It helps in tracking the inventory with serial

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

number and tracking batch feature which allow the company to keep record of movement of

items and to control expiry of batch. Valuation of inventory can be done through 2 ways :

LIFO – It stands for last in first out where goods that are bought at last are sold at first

place (Hopper and Bui, 2016.) FIFO – It stands for first in last out in which goods that are bought first are sold at first

place (Bergeron, 2017).

Cost accounting system : It is basically a frame work which is utilized by an organization for

determining the expenditure of goods in order to analyze profit. It is mainly utilized by

manufacturing firm for recording production activities by utilizing a perpetual inventory system

(Cai and et.al, 2018).

Job order costing – It is basically a system of assigning as well as aggregating

manufacturing costs of per unit of output(Hopper, 2016).

Process costing – it is generally technique which includes assignment of costs to units of

production in an organization manufacturing huge amount of consistent products. (Weight,

2015).

Job costing system : It includes accumulation o data related to cost that is related with special

type of production (Weight, 2015). The data provided by job costing system assist in

determining accuracy of estimation (Weight, 2015).

Price Optimization System: It Is a mathematical analysis that helps to determine how

customer respond to different prices for its substitute through variety of channel (Kokubu and

Kitada, 2015). For example, using price optimization software, company will handle complex

situation.

Budget System: It provides a means by which government of the country decides how

much should be spent, how to raise the money it has to spend (Ofori-Kuragu, Baiden and Badu,

2016). For example, when a new product is launch by the firm at that time, government decide

the price and budget needs to be allocated.

2

items and to control expiry of batch. Valuation of inventory can be done through 2 ways :

LIFO – It stands for last in first out where goods that are bought at last are sold at first

place (Hopper and Bui, 2016.) FIFO – It stands for first in last out in which goods that are bought first are sold at first

place (Bergeron, 2017).

Cost accounting system : It is basically a frame work which is utilized by an organization for

determining the expenditure of goods in order to analyze profit. It is mainly utilized by

manufacturing firm for recording production activities by utilizing a perpetual inventory system

(Cai and et.al, 2018).

Job order costing – It is basically a system of assigning as well as aggregating

manufacturing costs of per unit of output(Hopper, 2016).

Process costing – it is generally technique which includes assignment of costs to units of

production in an organization manufacturing huge amount of consistent products. (Weight,

2015).

Job costing system : It includes accumulation o data related to cost that is related with special

type of production (Weight, 2015). The data provided by job costing system assist in

determining accuracy of estimation (Weight, 2015).

Price Optimization System: It Is a mathematical analysis that helps to determine how

customer respond to different prices for its substitute through variety of channel (Kokubu and

Kitada, 2015). For example, using price optimization software, company will handle complex

situation.

Budget System: It provides a means by which government of the country decides how

much should be spent, how to raise the money it has to spend (Ofori-Kuragu, Baiden and Badu,

2016). For example, when a new product is launch by the firm at that time, government decide

the price and budget needs to be allocated.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

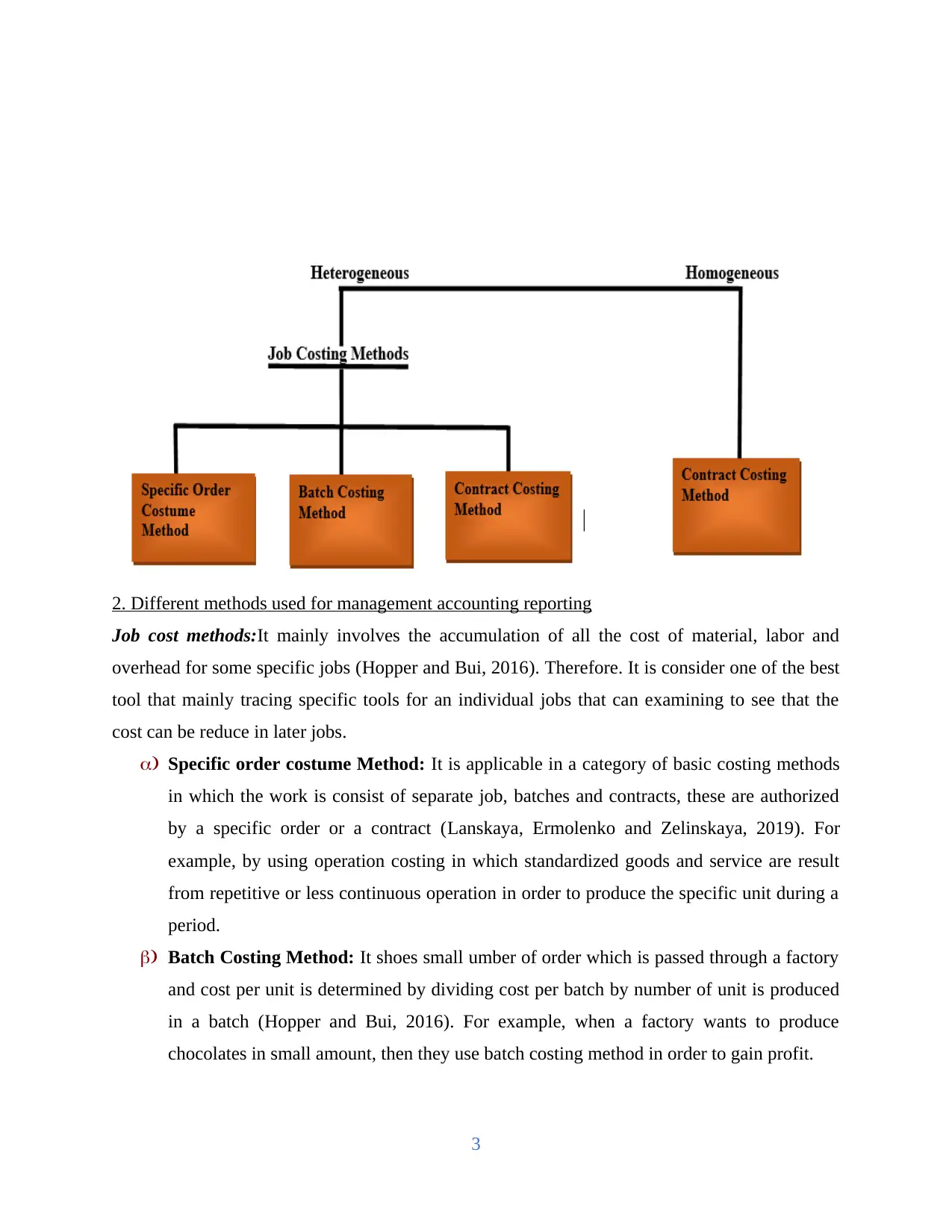

2. Different methods used for management accounting reporting

Job cost methods:It mainly involves the accumulation of all the cost of material, labor and

overhead for some specific jobs (Hopper and Bui, 2016). Therefore. It is consider one of the best

tool that mainly tracing specific tools for an individual jobs that can examining to see that the

cost can be reduce in later jobs.

a) Specific order costume Method: It is applicable in a category of basic costing methods

in which the work is consist of separate job, batches and contracts, these are authorized

by a specific order or a contract (Lanskaya, Ermolenko and Zelinskaya, 2019). For

example, by using operation costing in which standardized goods and service are result

from repetitive or less continuous operation in order to produce the specific unit during a

period.

b) Batch Costing Method: It shoes small umber of order which is passed through a factory

and cost per unit is determined by dividing cost per batch by number of unit is produced

in a batch (Hopper and Bui, 2016). For example, when a factory wants to produce

chocolates in small amount, then they use batch costing method in order to gain profit.

3

Illustration 1: Given by Lecture

Job cost methods:It mainly involves the accumulation of all the cost of material, labor and

overhead for some specific jobs (Hopper and Bui, 2016). Therefore. It is consider one of the best

tool that mainly tracing specific tools for an individual jobs that can examining to see that the

cost can be reduce in later jobs.

a) Specific order costume Method: It is applicable in a category of basic costing methods

in which the work is consist of separate job, batches and contracts, these are authorized

by a specific order or a contract (Lanskaya, Ermolenko and Zelinskaya, 2019). For

example, by using operation costing in which standardized goods and service are result

from repetitive or less continuous operation in order to produce the specific unit during a

period.

b) Batch Costing Method: It shoes small umber of order which is passed through a factory

and cost per unit is determined by dividing cost per batch by number of unit is produced

in a batch (Hopper and Bui, 2016). For example, when a factory wants to produce

chocolates in small amount, then they use batch costing method in order to gain profit.

3

Illustration 1: Given by Lecture

c) Contract costing method: this method is used when a firm is deal at different country

and at that time, there is a need to make separate account which is kept for each

individual contract (Weight, 2015). For example, a construction company uses this

method in order to maintain contract with builders, engineers and labors etc.

d) Process costing method: This is suitable for industries where production is continuous

and well-defined process such that finished products become raw material of subsequent

process and all the products are produced with same process (Martello, 2016). For

example, when a company produces different products with or without by product and

then produces simultaneously at same process and those products are clearly identical.

Different typea of reports are as mention below:

Budget reports – it is basically a internal report which is utilized by management in an

enterprise for comparing estimated costs with budgeted. Budget report assist management in

analyzing the business performance and support in identifying the area which require

improvement. (Chan, 2015).

Cost Report: it is the financial report which determine the cost and also identify charges

related to healthcare services (Jyothi, Vatsala and Gupta, 2019).

Variance Analysis report: It is the quantitative investigation and a difference between

actual and planned behavior, further it is als used to maintain control over a business

(Lanskaya, Ermolenko, and Zelinskaya, 2019).

Account receivable aging report –It is basically a report which consist of detailed information

about unpaid customer invoices as well as underutilized credit memos. Account receivable

aging report is generally utilized by an individual responsible for collecting payment. Those

personnel utilize the Account receivable aging report for determining the invoices which are

due.

Job cost report – It provides clear view of cost incurred by the particular project or job

in the company. It helps in comparing estimated cost with actual revenue the helps the company

in differentiate between the best performance job and least performer project (Cai, and et.al,

2018 ). This report evaluates the profitability of specific projects and optimize their working.

4

and at that time, there is a need to make separate account which is kept for each

individual contract (Weight, 2015). For example, a construction company uses this

method in order to maintain contract with builders, engineers and labors etc.

d) Process costing method: This is suitable for industries where production is continuous

and well-defined process such that finished products become raw material of subsequent

process and all the products are produced with same process (Martello, 2016). For

example, when a company produces different products with or without by product and

then produces simultaneously at same process and those products are clearly identical.

Different typea of reports are as mention below:

Budget reports – it is basically a internal report which is utilized by management in an

enterprise for comparing estimated costs with budgeted. Budget report assist management in

analyzing the business performance and support in identifying the area which require

improvement. (Chan, 2015).

Cost Report: it is the financial report which determine the cost and also identify charges

related to healthcare services (Jyothi, Vatsala and Gupta, 2019).

Variance Analysis report: It is the quantitative investigation and a difference between

actual and planned behavior, further it is als used to maintain control over a business

(Lanskaya, Ermolenko, and Zelinskaya, 2019).

Account receivable aging report –It is basically a report which consist of detailed information

about unpaid customer invoices as well as underutilized credit memos. Account receivable

aging report is generally utilized by an individual responsible for collecting payment. Those

personnel utilize the Account receivable aging report for determining the invoices which are

due.

Job cost report – It provides clear view of cost incurred by the particular project or job

in the company. It helps in comparing estimated cost with actual revenue the helps the company

in differentiate between the best performance job and least performer project (Cai, and et.al,

2018 ). This report evaluates the profitability of specific projects and optimize their working.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

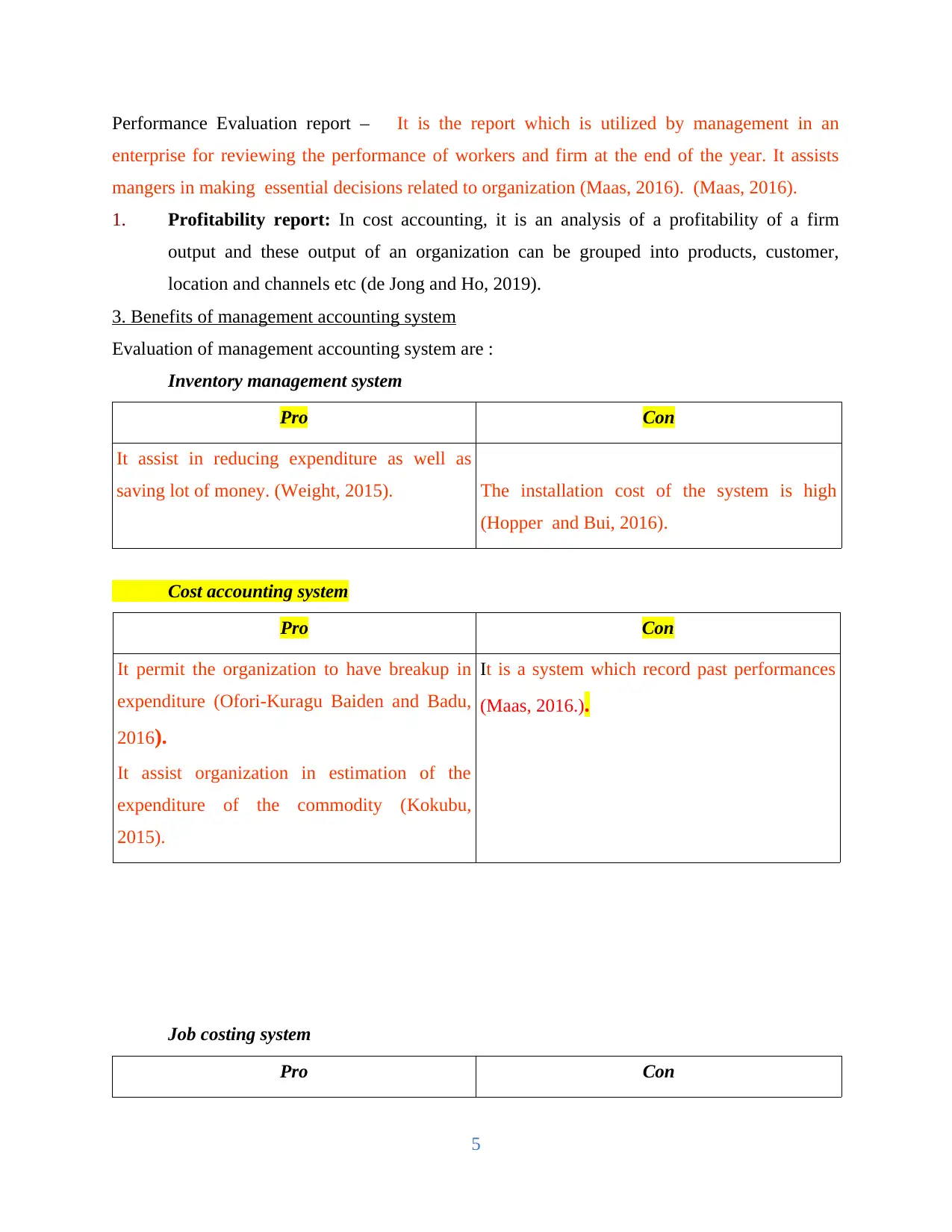

Performance Evaluation report – It is the report which is utilized by management in an

enterprise for reviewing the performance of workers and firm at the end of the year. It assists

mangers in making essential decisions related to organization (Maas, 2016). (Maas, 2016).

1. Profitability report: In cost accounting, it is an analysis of a profitability of a firm

output and these output of an organization can be grouped into products, customer,

location and channels etc (de Jong and Ho, 2019).

3. Benefits of management accounting system

Evaluation of management accounting system are :

Inventory management system

Pro Con

It assist in reducing expenditure as well as

saving lot of money. (Weight, 2015). The installation cost of the system is high

(Hopper and Bui, 2016).

Cost accounting system

Pro Con

It permit the organization to have breakup in

expenditure (Ofori-Kuragu Baiden and Badu,

2016).

It assist organization in estimation of the

expenditure of the commodity (Kokubu,

2015).

It is a system which record past performances

(Maas, 2016.).

Job costing system

Pro Con

5

enterprise for reviewing the performance of workers and firm at the end of the year. It assists

mangers in making essential decisions related to organization (Maas, 2016). (Maas, 2016).

1. Profitability report: In cost accounting, it is an analysis of a profitability of a firm

output and these output of an organization can be grouped into products, customer,

location and channels etc (de Jong and Ho, 2019).

3. Benefits of management accounting system

Evaluation of management accounting system are :

Inventory management system

Pro Con

It assist in reducing expenditure as well as

saving lot of money. (Weight, 2015). The installation cost of the system is high

(Hopper and Bui, 2016).

Cost accounting system

Pro Con

It permit the organization to have breakup in

expenditure (Ofori-Kuragu Baiden and Badu,

2016).

It assist organization in estimation of the

expenditure of the commodity (Kokubu,

2015).

It is a system which record past performances

(Maas, 2016.).

Job costing system

Pro Con

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It assist the organization in figuring out trend

analysis through compilation of real

expenditure. (Nørreklit, 2017).

This system does not provide any

standardization.

When inflation hits, the comparison of jobs

became meaningless (Martello, 2016).

4.Integration of management accounting and reporting system

The integration of management accounting system and reporting system in the

organization works jointly that helps organization in minimizing expenditure and in making

operations more efficient. . The cost accounting system of the organization assist in providing

cost reports to the organization which assist the company in deciding the price of its product

(Bergeron, 2017).

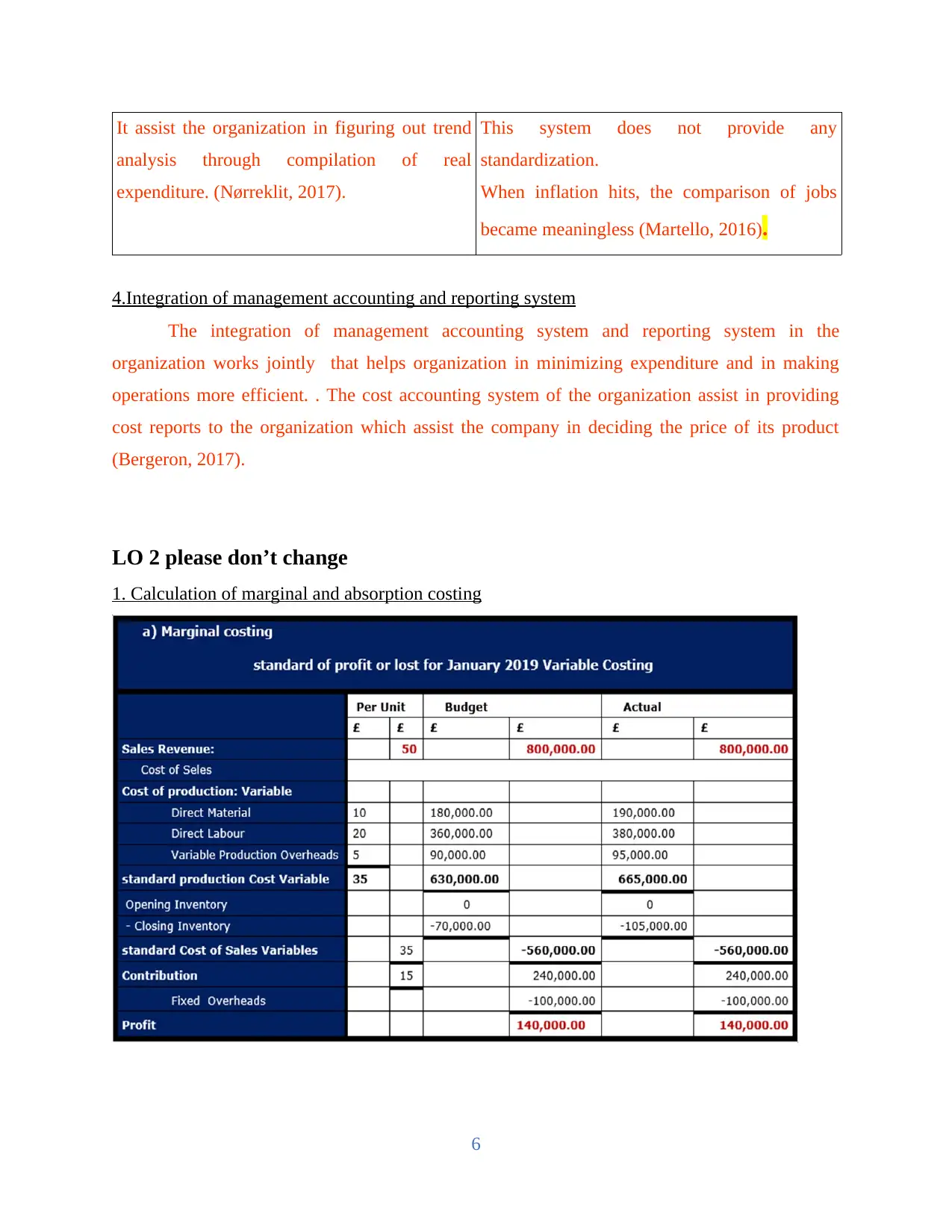

LO 2 please don’t change

1. Calculation of marginal and absorption costing

6

analysis through compilation of real

expenditure. (Nørreklit, 2017).

This system does not provide any

standardization.

When inflation hits, the comparison of jobs

became meaningless (Martello, 2016).

4.Integration of management accounting and reporting system

The integration of management accounting system and reporting system in the

organization works jointly that helps organization in minimizing expenditure and in making

operations more efficient. . The cost accounting system of the organization assist in providing

cost reports to the organization which assist the company in deciding the price of its product

(Bergeron, 2017).

LO 2 please don’t change

1. Calculation of marginal and absorption costing

6

C) Absorption Costing: Reconciliation of Budgeted Profit and Actual Profit

Budget Actual

Number of Units Sold 16,000.00 16,000.00

Standard Profit / Unit 10.00 10.00

Standard Profit 160,000.00 160,000.00

FOH Changed in Cost of Production 90,000.00 95,000.00

Additional FOH Underabsorvition 10,000.00 5,000.00

Total FOH Charged Gross 100,000.00 100,000.00

FOH Transfer for the next month Feb.2019 10,000.00 15,000.00

Net FOH Charged - Absorption Costing 90,000.00 85,000.00

FOH Changed Variable Losting 100,000.00 100,000.00

Reduction in Variable Losting Profit 10,000.00 15,000.00

7

Budget Actual

Number of Units Sold 16,000.00 16,000.00

Standard Profit / Unit 10.00 10.00

Standard Profit 160,000.00 160,000.00

FOH Changed in Cost of Production 90,000.00 95,000.00

Additional FOH Underabsorvition 10,000.00 5,000.00

Total FOH Charged Gross 100,000.00 100,000.00

FOH Transfer for the next month Feb.2019 10,000.00 15,000.00

Net FOH Charged - Absorption Costing 90,000.00 85,000.00

FOH Changed Variable Losting 100,000.00 100,000.00

Reduction in Variable Losting Profit 10,000.00 15,000.00

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

LO 3

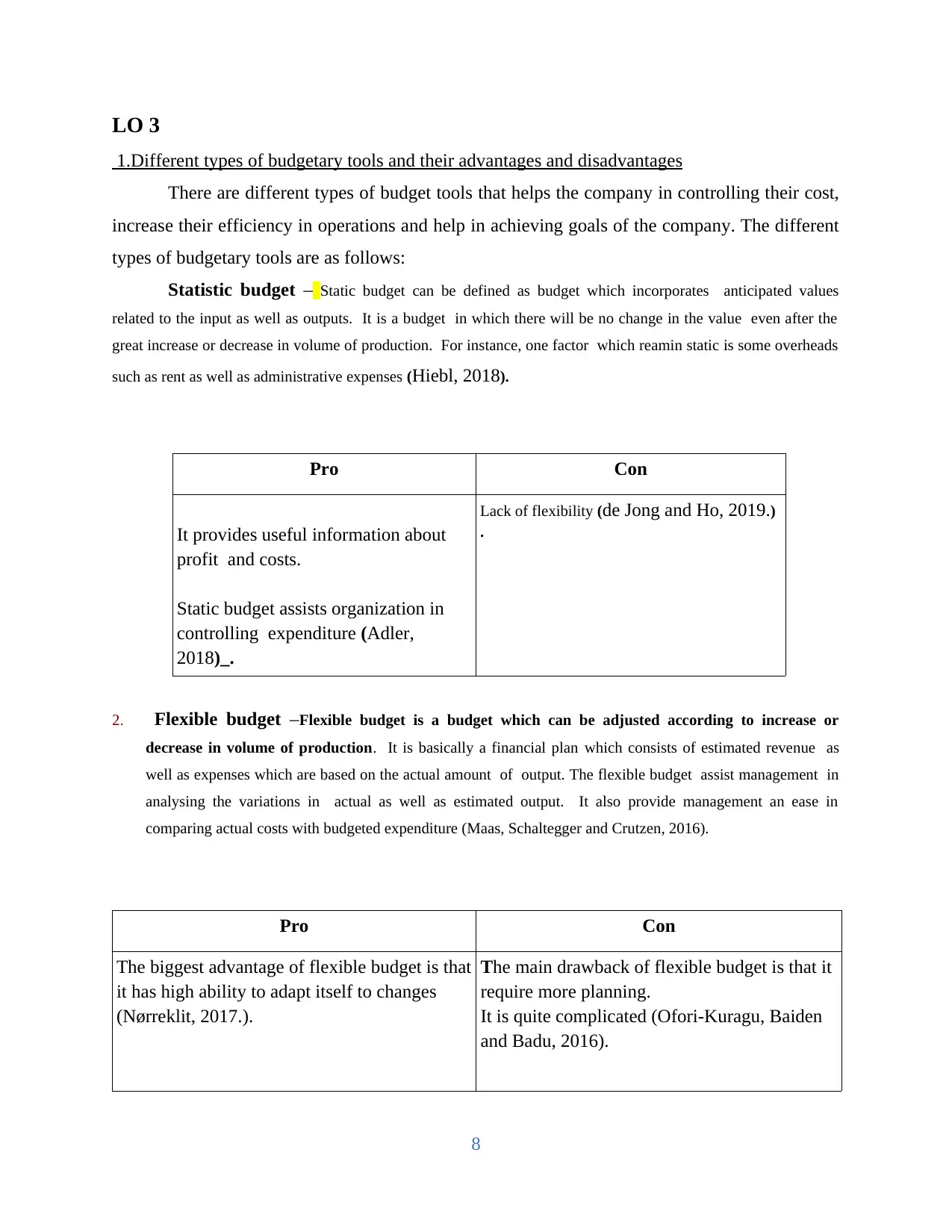

1.Different types of budgetary tools and their advantages and disadvantages

There are different types of budget tools that helps the company in controlling their cost,

increase their efficiency in operations and help in achieving goals of the company. The different

types of budgetary tools are as follows:

Statistic budget – Static budget can be defined as budget which incorporates anticipated values

related to the input as well as outputs. It is a budget in which there will be no change in the value even after the

great increase or decrease in volume of production. For instance, one factor which reamin static is some overheads

such as rent as well as administrative expenses (Hiebl, 2018).

Pro Con

It provides useful information about

profit and costs.

Static budget assists organization in

controlling expenditure (Adler,

2018)_.

Lack of flexibility (de Jong and Ho, 2019.)

.

2. Flexible budget –Flexible budget is a budget which can be adjusted according to increase or

decrease in volume of production. It is basically a financial plan which consists of estimated revenue as

well as expenses which are based on the actual amount of output. The flexible budget assist management in

analysing the variations in actual as well as estimated output. It also provide management an ease in

comparing actual costs with budgeted expenditure (Maas, Schaltegger and Crutzen, 2016).

Pro Con

The biggest advantage of flexible budget is that

it has high ability to adapt itself to changes

(Nørreklit, 2017.).

The main drawback of flexible budget is that it

require more planning.

It is quite complicated (Ofori-Kuragu, Baiden

and Badu, 2016).

8

1.Different types of budgetary tools and their advantages and disadvantages

There are different types of budget tools that helps the company in controlling their cost,

increase their efficiency in operations and help in achieving goals of the company. The different

types of budgetary tools are as follows:

Statistic budget – Static budget can be defined as budget which incorporates anticipated values

related to the input as well as outputs. It is a budget in which there will be no change in the value even after the

great increase or decrease in volume of production. For instance, one factor which reamin static is some overheads

such as rent as well as administrative expenses (Hiebl, 2018).

Pro Con

It provides useful information about

profit and costs.

Static budget assists organization in

controlling expenditure (Adler,

2018)_.

Lack of flexibility (de Jong and Ho, 2019.)

.

2. Flexible budget –Flexible budget is a budget which can be adjusted according to increase or

decrease in volume of production. It is basically a financial plan which consists of estimated revenue as

well as expenses which are based on the actual amount of output. The flexible budget assist management in

analysing the variations in actual as well as estimated output. It also provide management an ease in

comparing actual costs with budgeted expenditure (Maas, Schaltegger and Crutzen, 2016).

Pro Con

The biggest advantage of flexible budget is that

it has high ability to adapt itself to changes

(Nørreklit, 2017.).

The main drawback of flexible budget is that it

require more planning.

It is quite complicated (Ofori-Kuragu, Baiden

and Badu, 2016).

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

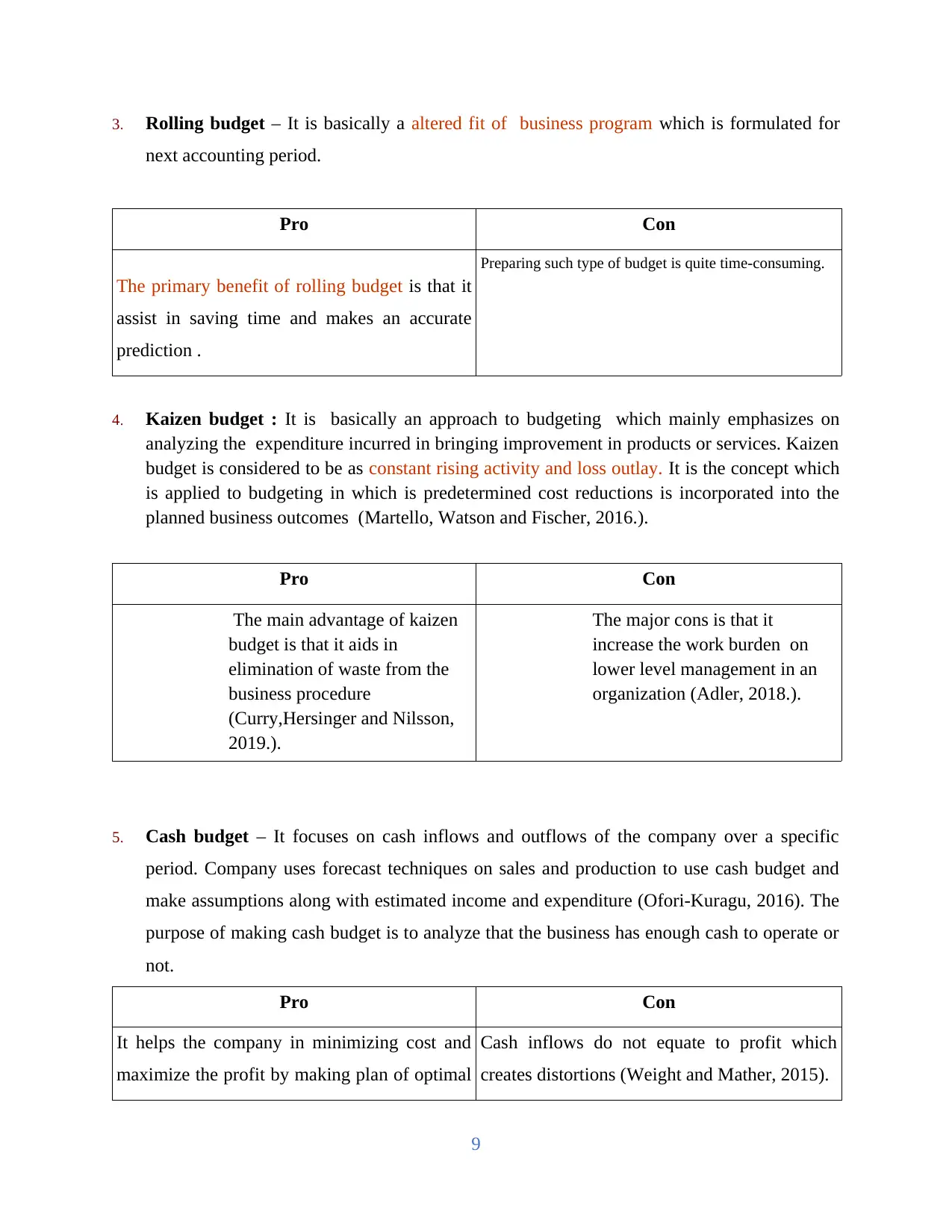

3. Rolling budget – It is basically a altered fit of business program which is formulated for

next accounting period.

Pro Con

The primary benefit of rolling budget is that it

assist in saving time and makes an accurate

prediction .

Preparing such type of budget is quite time-consuming.

4. Kaizen budget : It is basically an approach to budgeting which mainly emphasizes on

analyzing the expenditure incurred in bringing improvement in products or services. Kaizen

budget is considered to be as constant rising activity and loss outlay. It is the concept which

is applied to budgeting in which is predetermined cost reductions is incorporated into the

planned business outcomes (Martello, Watson and Fischer, 2016.).

Pro Con

The main advantage of kaizen

budget is that it aids in

elimination of waste from the

business procedure

(Curry,Hersinger and Nilsson,

2019.).

The major cons is that it

increase the work burden on

lower level management in an

organization (Adler, 2018.).

5. Cash budget – It focuses on cash inflows and outflows of the company over a specific

period. Company uses forecast techniques on sales and production to use cash budget and

make assumptions along with estimated income and expenditure (Ofori-Kuragu, 2016). The

purpose of making cash budget is to analyze that the business has enough cash to operate or

not.

Pro Con

It helps the company in minimizing cost and

maximize the profit by making plan of optimal

Cash inflows do not equate to profit which

creates distortions (Weight and Mather, 2015).

9

next accounting period.

Pro Con

The primary benefit of rolling budget is that it

assist in saving time and makes an accurate

prediction .

Preparing such type of budget is quite time-consuming.

4. Kaizen budget : It is basically an approach to budgeting which mainly emphasizes on

analyzing the expenditure incurred in bringing improvement in products or services. Kaizen

budget is considered to be as constant rising activity and loss outlay. It is the concept which

is applied to budgeting in which is predetermined cost reductions is incorporated into the

planned business outcomes (Martello, Watson and Fischer, 2016.).

Pro Con

The main advantage of kaizen

budget is that it aids in

elimination of waste from the

business procedure

(Curry,Hersinger and Nilsson,

2019.).

The major cons is that it

increase the work burden on

lower level management in an

organization (Adler, 2018.).

5. Cash budget – It focuses on cash inflows and outflows of the company over a specific

period. Company uses forecast techniques on sales and production to use cash budget and

make assumptions along with estimated income and expenditure (Ofori-Kuragu, 2016). The

purpose of making cash budget is to analyze that the business has enough cash to operate or

not.

Pro Con

It helps the company in minimizing cost and

maximize the profit by making plan of optimal

Cash inflows do not equate to profit which

creates distortions (Weight and Mather, 2015).

9

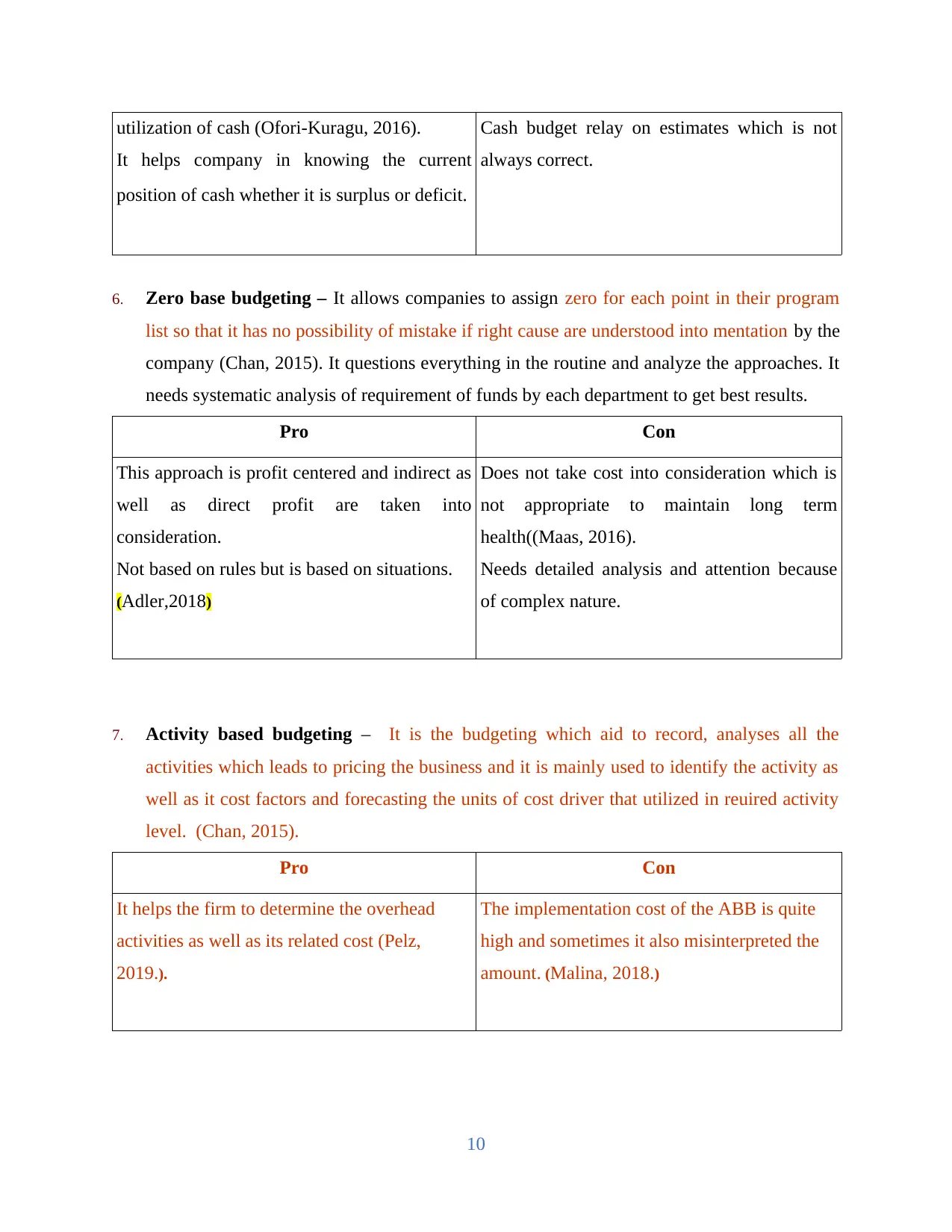

utilization of cash (Ofori-Kuragu, 2016).

It helps company in knowing the current

position of cash whether it is surplus or deficit.

Cash budget relay on estimates which is not

always correct.

6. Zero base budgeting – It allows companies to assign zero for each point in their program

list so that it has no possibility of mistake if right cause are understood into mentation by the

company (Chan, 2015). It questions everything in the routine and analyze the approaches. It

needs systematic analysis of requirement of funds by each department to get best results.

Pro Con

This approach is profit centered and indirect as

well as direct profit are taken into

consideration.

Not based on rules but is based on situations.

(Adler,2018)

Does not take cost into consideration which is

not appropriate to maintain long term

health((Maas, 2016).

Needs detailed analysis and attention because

of complex nature.

7. Activity based budgeting – It is the budgeting which aid to record, analyses all the

activities which leads to pricing the business and it is mainly used to identify the activity as

well as it cost factors and forecasting the units of cost driver that utilized in reuired activity

level. (Chan, 2015).

Pro Con

It helps the firm to determine the overhead

activities as well as its related cost (Pelz,

2019.).

The implementation cost of the ABB is quite

high and sometimes it also misinterpreted the

amount. (Malina, 2018.)

10

It helps company in knowing the current

position of cash whether it is surplus or deficit.

Cash budget relay on estimates which is not

always correct.

6. Zero base budgeting – It allows companies to assign zero for each point in their program

list so that it has no possibility of mistake if right cause are understood into mentation by the

company (Chan, 2015). It questions everything in the routine and analyze the approaches. It

needs systematic analysis of requirement of funds by each department to get best results.

Pro Con

This approach is profit centered and indirect as

well as direct profit are taken into

consideration.

Not based on rules but is based on situations.

(Adler,2018)

Does not take cost into consideration which is

not appropriate to maintain long term

health((Maas, 2016).

Needs detailed analysis and attention because

of complex nature.

7. Activity based budgeting – It is the budgeting which aid to record, analyses all the

activities which leads to pricing the business and it is mainly used to identify the activity as

well as it cost factors and forecasting the units of cost driver that utilized in reuired activity

level. (Chan, 2015).

Pro Con

It helps the firm to determine the overhead

activities as well as its related cost (Pelz,

2019.).

The implementation cost of the ABB is quite

high and sometimes it also misinterpreted the

amount. (Malina, 2018.)

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.