Analysis of Management Accounting Techniques: Woodrock Limited

VerifiedAdded on 2023/01/05

|16

|3945

|25

Homework Assignment

AI Summary

This assignment delves into various management accounting techniques through the analysis of three key questions. The first question focuses on the preparation of a cash budget for Woodrock Limited, evaluating its cash position, and suggesting improvements to enhance cash flow. Additionally, it critically examines behavioral aspects of budgeting that may lead to business problems. The second question explores break-even analysis (BEP), contribution margins, and profit calculations for Plaistead Plc, considering different sales scenarios and pricing strategies. It also discusses the underlying assumptions of the BEP model. The final question involves preparing a columnar statement, calculating variances for direct materials and direct labor, and discussing the purposes, values, and limitations of standard costing and variance analysis. The assignment offers insights into financial planning, cost control, and performance measurement.

Introduction to

Management

Accounting

Management

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

QUESTION 1..................................................................................................................................1

Preparation of the Cash Budget for Woodrock Limited the first six months of trade.................1

Comment on the cash position within the business, analysing what Woodrock Limited could

do to improve cash flow..............................................................................................................3

Critical examination those issues of relevance in behavioural aspects of budgeting which may

lead to problems in a business entity...........................................................................................3

QUESTION 2..................................................................................................................................4

A. Contribution that each electric kettle makes towards covering fixed costs if it is sold for

£13...............................................................................................................................................4

B. Calculation of BEP and margin of safety in revenues and units.............................................4

C. Calculation of profit Plaistead Plc makes if it produces and sells 53,000 electric kettles at

£13 per kettle...............................................................................................................................5

D. Calculation of sales at profit of 90000....................................................................................6

E. Calculation of price of units if 90000 profits is desired by selling 53000 units.....................6

F. Analysis of suitability of strategy to the organisation.............................................................6

G. Brief discussion of the underpinning assumptions attached to the break-even model...........7

QUESTION 4..................................................................................................................................7

A. Prepare a columnar statement showing, by element of cost...................................................7

B Variances for direct material and direct labour........................................................................8

C Discuss the purposes of standard costing, highlighting some of the key values and

limitations associated with the use of variance analysis............................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

QUESTION 1..................................................................................................................................1

Preparation of the Cash Budget for Woodrock Limited the first six months of trade.................1

Comment on the cash position within the business, analysing what Woodrock Limited could

do to improve cash flow..............................................................................................................3

Critical examination those issues of relevance in behavioural aspects of budgeting which may

lead to problems in a business entity...........................................................................................3

QUESTION 2..................................................................................................................................4

A. Contribution that each electric kettle makes towards covering fixed costs if it is sold for

£13...............................................................................................................................................4

B. Calculation of BEP and margin of safety in revenues and units.............................................4

C. Calculation of profit Plaistead Plc makes if it produces and sells 53,000 electric kettles at

£13 per kettle...............................................................................................................................5

D. Calculation of sales at profit of 90000....................................................................................6

E. Calculation of price of units if 90000 profits is desired by selling 53000 units.....................6

F. Analysis of suitability of strategy to the organisation.............................................................6

G. Brief discussion of the underpinning assumptions attached to the break-even model...........7

QUESTION 4..................................................................................................................................7

A. Prepare a columnar statement showing, by element of cost...................................................7

B Variances for direct material and direct labour........................................................................8

C Discuss the purposes of standard costing, highlighting some of the key values and

limitations associated with the use of variance analysis............................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

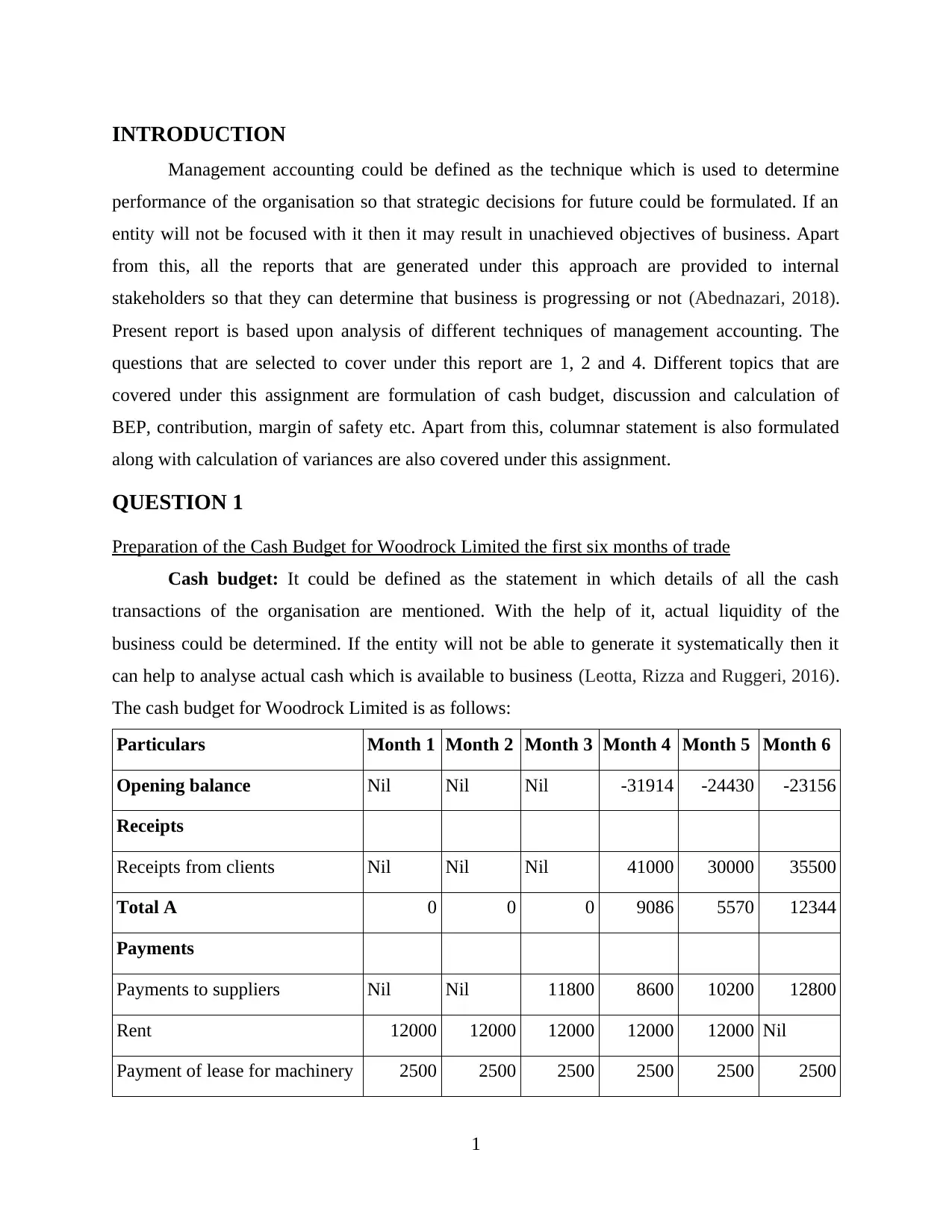

INTRODUCTION

Management accounting could be defined as the technique which is used to determine

performance of the organisation so that strategic decisions for future could be formulated. If an

entity will not be focused with it then it may result in unachieved objectives of business. Apart

from this, all the reports that are generated under this approach are provided to internal

stakeholders so that they can determine that business is progressing or not (Abednazari, 2018).

Present report is based upon analysis of different techniques of management accounting. The

questions that are selected to cover under this report are 1, 2 and 4. Different topics that are

covered under this assignment are formulation of cash budget, discussion and calculation of

BEP, contribution, margin of safety etc. Apart from this, columnar statement is also formulated

along with calculation of variances are also covered under this assignment.

QUESTION 1

Preparation of the Cash Budget for Woodrock Limited the first six months of trade

Cash budget: It could be defined as the statement in which details of all the cash

transactions of the organisation are mentioned. With the help of it, actual liquidity of the

business could be determined. If the entity will not be able to generate it systematically then it

can help to analyse actual cash which is available to business (Leotta, Rizza and Ruggeri, 2016).

The cash budget for Woodrock Limited is as follows:

Particulars Month 1 Month 2 Month 3 Month 4 Month 5 Month 6

Opening balance Nil Nil Nil -31914 -24430 -23156

Receipts

Receipts from clients Nil Nil Nil 41000 30000 35500

Total A 0 0 0 9086 5570 12344

Payments

Payments to suppliers Nil Nil 11800 8600 10200 12800

Rent 12000 12000 12000 12000 12000 Nil

Payment of lease for machinery 2500 2500 2500 2500 2500 2500

1

Management accounting could be defined as the technique which is used to determine

performance of the organisation so that strategic decisions for future could be formulated. If an

entity will not be focused with it then it may result in unachieved objectives of business. Apart

from this, all the reports that are generated under this approach are provided to internal

stakeholders so that they can determine that business is progressing or not (Abednazari, 2018).

Present report is based upon analysis of different techniques of management accounting. The

questions that are selected to cover under this report are 1, 2 and 4. Different topics that are

covered under this assignment are formulation of cash budget, discussion and calculation of

BEP, contribution, margin of safety etc. Apart from this, columnar statement is also formulated

along with calculation of variances are also covered under this assignment.

QUESTION 1

Preparation of the Cash Budget for Woodrock Limited the first six months of trade

Cash budget: It could be defined as the statement in which details of all the cash

transactions of the organisation are mentioned. With the help of it, actual liquidity of the

business could be determined. If the entity will not be able to generate it systematically then it

can help to analyse actual cash which is available to business (Leotta, Rizza and Ruggeri, 2016).

The cash budget for Woodrock Limited is as follows:

Particulars Month 1 Month 2 Month 3 Month 4 Month 5 Month 6

Opening balance Nil Nil Nil -31914 -24430 -23156

Receipts

Receipts from clients Nil Nil Nil 41000 30000 35500

Total A 0 0 0 9086 5570 12344

Payments

Payments to suppliers Nil Nil 11800 8600 10200 12800

Rent 12000 12000 12000 12000 12000 Nil

Payment of lease for machinery 2500 2500 2500 2500 2500 2500

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Marketing and advertising 8000 8000 8000 8000 Nil Nil

Salary to manager 3000 3000 3000 3000 3000 3000

Insurance 4000 Nil Nil Nil Nil Nil

Payment to labour 7416 5412 6414 8016 11226 13032

Total B 36916 30912 31914 33516 28726 18532

Closing balance (A-B) -36916 -30912 -31914 -24430 -23156 -6188

Working notes:

Calculation of receipts from customers

Particulars Month 1 Month 2 Month 3 Month 4 Month 5 Month 6

Desk (30 per

unit) 21000 15000 18000 24000 30000 33000

Cabinet (50 per

unit) 20000 15000 17500 20000 32500 40000

Total receipts 41000 30000 35500 44000 62500 73000

Calculation of payment to supplier

Particulars Month 1 Month 2 Month 3 Month 4 Month 5 Month 6

Desk (10) 7000 5000 6000 8000 10000 11000

Cabinet (12) 4800 3600 4200 4800 7800 9600

Total payments 11800 8600 10200 12800 17800 20600

Calculation of labour hours

Particulars Month 1 Month 2 Month 3 Month 4 Month 5 Month 6

Desk (0.5 hour

per unit) 4200 3000 3600 4800 6000 6600

Cabinet (0.67 3216 2412 2814 3216 5226 6432

2

Salary to manager 3000 3000 3000 3000 3000 3000

Insurance 4000 Nil Nil Nil Nil Nil

Payment to labour 7416 5412 6414 8016 11226 13032

Total B 36916 30912 31914 33516 28726 18532

Closing balance (A-B) -36916 -30912 -31914 -24430 -23156 -6188

Working notes:

Calculation of receipts from customers

Particulars Month 1 Month 2 Month 3 Month 4 Month 5 Month 6

Desk (30 per

unit) 21000 15000 18000 24000 30000 33000

Cabinet (50 per

unit) 20000 15000 17500 20000 32500 40000

Total receipts 41000 30000 35500 44000 62500 73000

Calculation of payment to supplier

Particulars Month 1 Month 2 Month 3 Month 4 Month 5 Month 6

Desk (10) 7000 5000 6000 8000 10000 11000

Cabinet (12) 4800 3600 4200 4800 7800 9600

Total payments 11800 8600 10200 12800 17800 20600

Calculation of labour hours

Particulars Month 1 Month 2 Month 3 Month 4 Month 5 Month 6

Desk (0.5 hour

per unit) 4200 3000 3600 4800 6000 6600

Cabinet (0.67 3216 2412 2814 3216 5226 6432

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

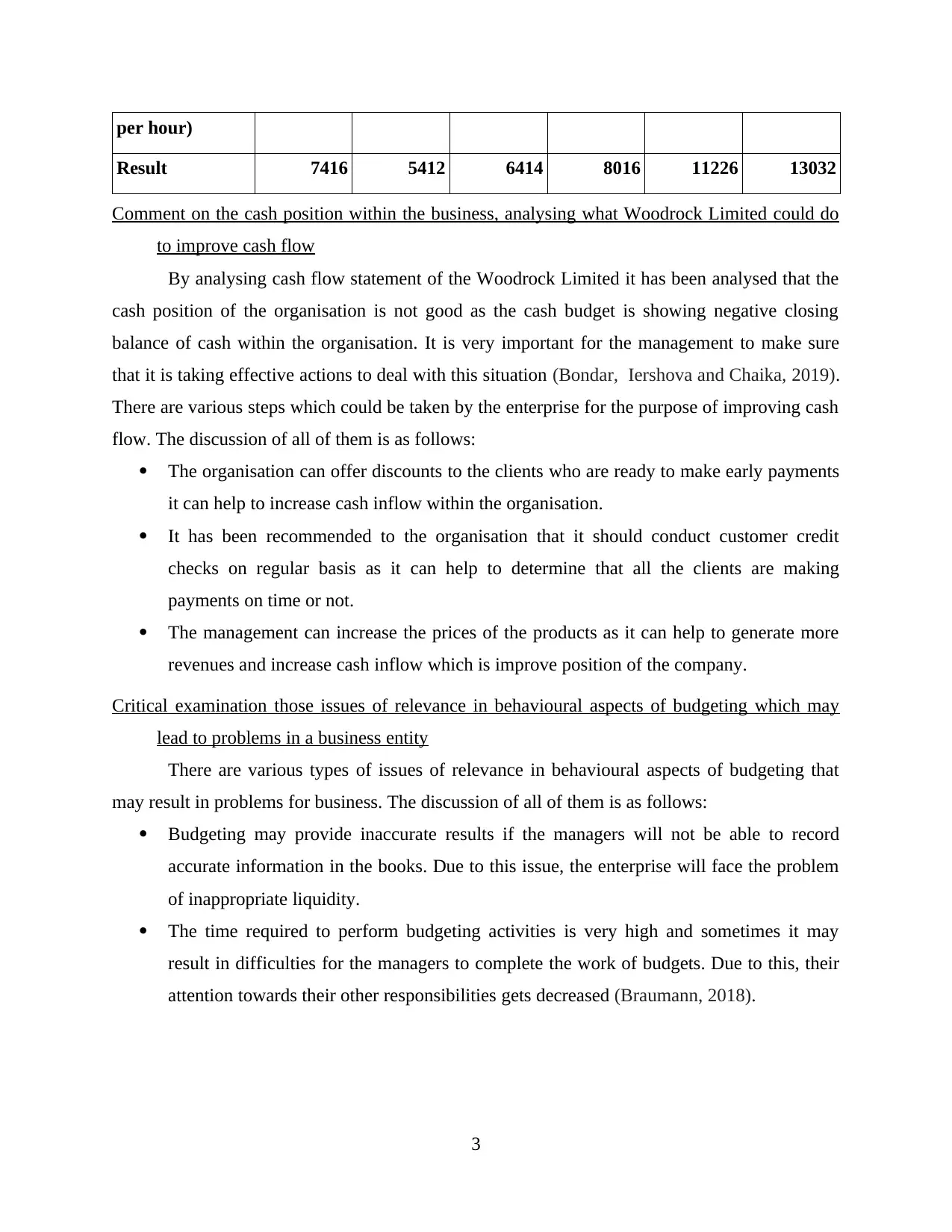

per hour)

Result 7416 5412 6414 8016 11226 13032

Comment on the cash position within the business, analysing what Woodrock Limited could do

to improve cash flow

By analysing cash flow statement of the Woodrock Limited it has been analysed that the

cash position of the organisation is not good as the cash budget is showing negative closing

balance of cash within the organisation. It is very important for the management to make sure

that it is taking effective actions to deal with this situation (Bondar, Iershova and Chaika, 2019).

There are various steps which could be taken by the enterprise for the purpose of improving cash

flow. The discussion of all of them is as follows:

The organisation can offer discounts to the clients who are ready to make early payments

it can help to increase cash inflow within the organisation.

It has been recommended to the organisation that it should conduct customer credit

checks on regular basis as it can help to determine that all the clients are making

payments on time or not.

The management can increase the prices of the products as it can help to generate more

revenues and increase cash inflow which is improve position of the company.

Critical examination those issues of relevance in behavioural aspects of budgeting which may

lead to problems in a business entity

There are various types of issues of relevance in behavioural aspects of budgeting that

may result in problems for business. The discussion of all of them is as follows:

Budgeting may provide inaccurate results if the managers will not be able to record

accurate information in the books. Due to this issue, the enterprise will face the problem

of inappropriate liquidity.

The time required to perform budgeting activities is very high and sometimes it may

result in difficulties for the managers to complete the work of budgets. Due to this, their

attention towards their other responsibilities gets decreased (Braumann, 2018).

3

Result 7416 5412 6414 8016 11226 13032

Comment on the cash position within the business, analysing what Woodrock Limited could do

to improve cash flow

By analysing cash flow statement of the Woodrock Limited it has been analysed that the

cash position of the organisation is not good as the cash budget is showing negative closing

balance of cash within the organisation. It is very important for the management to make sure

that it is taking effective actions to deal with this situation (Bondar, Iershova and Chaika, 2019).

There are various steps which could be taken by the enterprise for the purpose of improving cash

flow. The discussion of all of them is as follows:

The organisation can offer discounts to the clients who are ready to make early payments

it can help to increase cash inflow within the organisation.

It has been recommended to the organisation that it should conduct customer credit

checks on regular basis as it can help to determine that all the clients are making

payments on time or not.

The management can increase the prices of the products as it can help to generate more

revenues and increase cash inflow which is improve position of the company.

Critical examination those issues of relevance in behavioural aspects of budgeting which may

lead to problems in a business entity

There are various types of issues of relevance in behavioural aspects of budgeting that

may result in problems for business. The discussion of all of them is as follows:

Budgeting may provide inaccurate results if the managers will not be able to record

accurate information in the books. Due to this issue, the enterprise will face the problem

of inappropriate liquidity.

The time required to perform budgeting activities is very high and sometimes it may

result in difficulties for the managers to complete the work of budgets. Due to this, their

attention towards their other responsibilities gets decreased (Braumann, 2018).

3

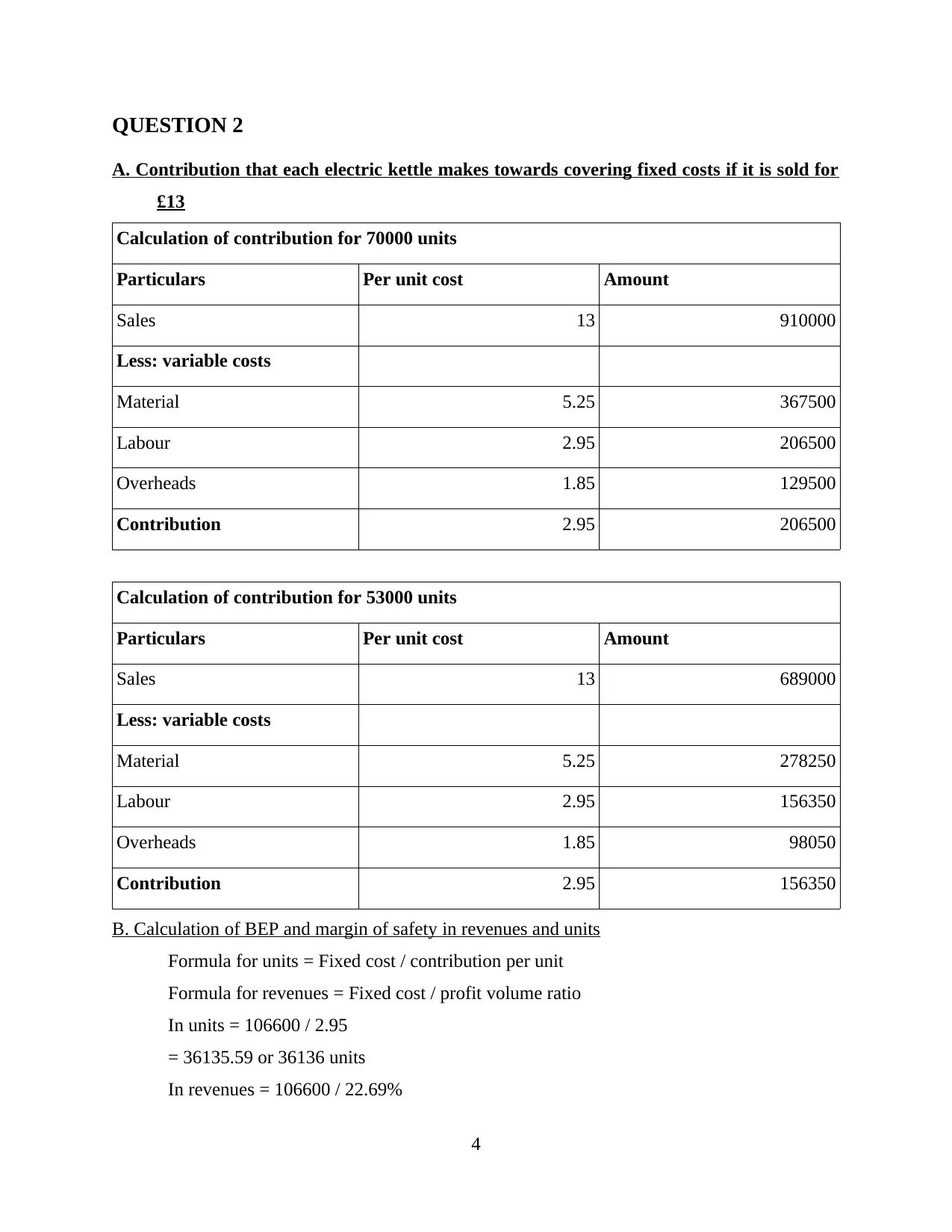

QUESTION 2

A. Contribution that each electric kettle makes towards covering fixed costs if it is sold for

£13

Calculation of contribution for 70000 units

Particulars Per unit cost Amount

Sales 13 910000

Less: variable costs

Material 5.25 367500

Labour 2.95 206500

Overheads 1.85 129500

Contribution 2.95 206500

Calculation of contribution for 53000 units

Particulars Per unit cost Amount

Sales 13 689000

Less: variable costs

Material 5.25 278250

Labour 2.95 156350

Overheads 1.85 98050

Contribution 2.95 156350

B. Calculation of BEP and margin of safety in revenues and units

Formula for units = Fixed cost / contribution per unit

Formula for revenues = Fixed cost / profit volume ratio

In units = 106600 / 2.95

= 36135.59 or 36136 units

In revenues = 106600 / 22.69%

4

A. Contribution that each electric kettle makes towards covering fixed costs if it is sold for

£13

Calculation of contribution for 70000 units

Particulars Per unit cost Amount

Sales 13 910000

Less: variable costs

Material 5.25 367500

Labour 2.95 206500

Overheads 1.85 129500

Contribution 2.95 206500

Calculation of contribution for 53000 units

Particulars Per unit cost Amount

Sales 13 689000

Less: variable costs

Material 5.25 278250

Labour 2.95 156350

Overheads 1.85 98050

Contribution 2.95 156350

B. Calculation of BEP and margin of safety in revenues and units

Formula for units = Fixed cost / contribution per unit

Formula for revenues = Fixed cost / profit volume ratio

In units = 106600 / 2.95

= 36135.59 or 36136 units

In revenues = 106600 / 22.69%

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

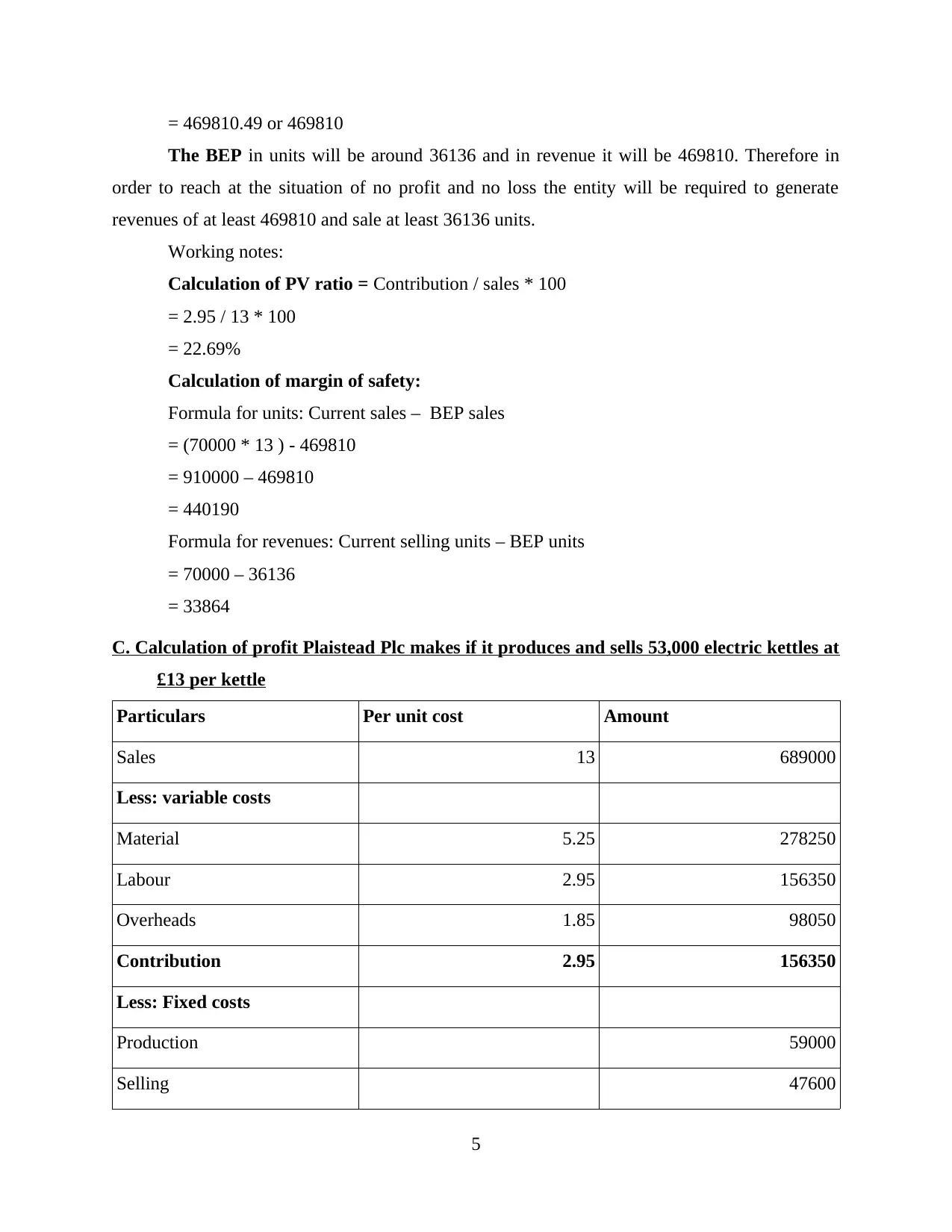

= 469810.49 or 469810

The BEP in units will be around 36136 and in revenue it will be 469810. Therefore in

order to reach at the situation of no profit and no loss the entity will be required to generate

revenues of at least 469810 and sale at least 36136 units.

Working notes:

Calculation of PV ratio = Contribution / sales * 100

= 2.95 / 13 * 100

= 22.69%

Calculation of margin of safety:

Formula for units: Current sales – BEP sales

= (70000 * 13 ) - 469810

= 910000 – 469810

= 440190

Formula for revenues: Current selling units – BEP units

= 70000 – 36136

= 33864

C. Calculation of profit Plaistead Plc makes if it produces and sells 53,000 electric kettles at

£13 per kettle

Particulars Per unit cost Amount

Sales 13 689000

Less: variable costs

Material 5.25 278250

Labour 2.95 156350

Overheads 1.85 98050

Contribution 2.95 156350

Less: Fixed costs

Production 59000

Selling 47600

5

The BEP in units will be around 36136 and in revenue it will be 469810. Therefore in

order to reach at the situation of no profit and no loss the entity will be required to generate

revenues of at least 469810 and sale at least 36136 units.

Working notes:

Calculation of PV ratio = Contribution / sales * 100

= 2.95 / 13 * 100

= 22.69%

Calculation of margin of safety:

Formula for units: Current sales – BEP sales

= (70000 * 13 ) - 469810

= 910000 – 469810

= 440190

Formula for revenues: Current selling units – BEP units

= 70000 – 36136

= 33864

C. Calculation of profit Plaistead Plc makes if it produces and sells 53,000 electric kettles at

£13 per kettle

Particulars Per unit cost Amount

Sales 13 689000

Less: variable costs

Material 5.25 278250

Labour 2.95 156350

Overheads 1.85 98050

Contribution 2.95 156350

Less: Fixed costs

Production 59000

Selling 47600

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

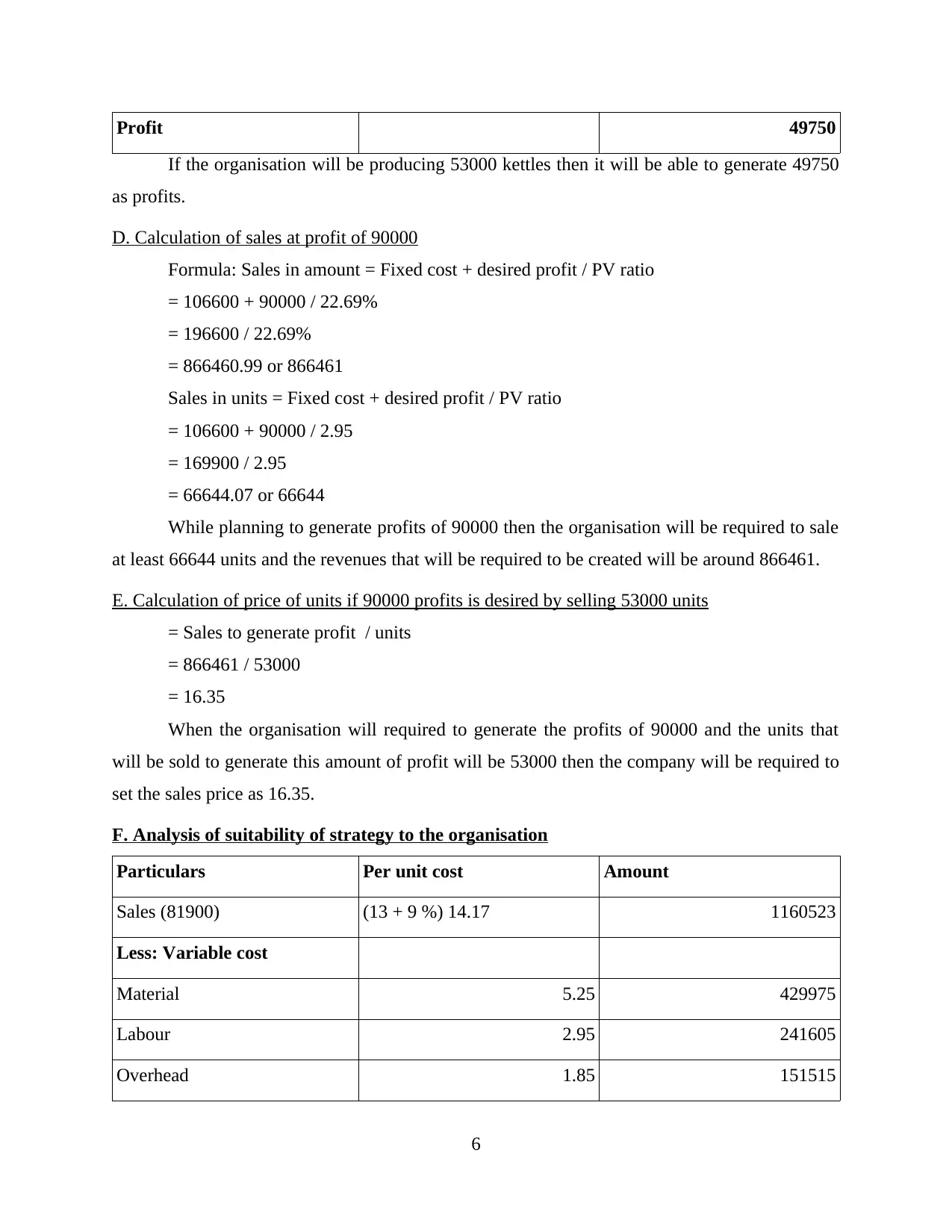

Profit 49750

If the organisation will be producing 53000 kettles then it will be able to generate 49750

as profits.

D. Calculation of sales at profit of 90000

Formula: Sales in amount = Fixed cost + desired profit / PV ratio

= 106600 + 90000 / 22.69%

= 196600 / 22.69%

= 866460.99 or 866461

Sales in units = Fixed cost + desired profit / PV ratio

= 106600 + 90000 / 2.95

= 169900 / 2.95

= 66644.07 or 66644

While planning to generate profits of 90000 then the organisation will be required to sale

at least 66644 units and the revenues that will be required to be created will be around 866461.

E. Calculation of price of units if 90000 profits is desired by selling 53000 units

= Sales to generate profit / units

= 866461 / 53000

= 16.35

When the organisation will required to generate the profits of 90000 and the units that

will be sold to generate this amount of profit will be 53000 then the company will be required to

set the sales price as 16.35.

F. Analysis of suitability of strategy to the organisation

Particulars Per unit cost Amount

Sales (81900) (13 + 9 %) 14.17 1160523

Less: Variable cost

Material 5.25 429975

Labour 2.95 241605

Overhead 1.85 151515

6

If the organisation will be producing 53000 kettles then it will be able to generate 49750

as profits.

D. Calculation of sales at profit of 90000

Formula: Sales in amount = Fixed cost + desired profit / PV ratio

= 106600 + 90000 / 22.69%

= 196600 / 22.69%

= 866460.99 or 866461

Sales in units = Fixed cost + desired profit / PV ratio

= 106600 + 90000 / 2.95

= 169900 / 2.95

= 66644.07 or 66644

While planning to generate profits of 90000 then the organisation will be required to sale

at least 66644 units and the revenues that will be required to be created will be around 866461.

E. Calculation of price of units if 90000 profits is desired by selling 53000 units

= Sales to generate profit / units

= 866461 / 53000

= 16.35

When the organisation will required to generate the profits of 90000 and the units that

will be sold to generate this amount of profit will be 53000 then the company will be required to

set the sales price as 16.35.

F. Analysis of suitability of strategy to the organisation

Particulars Per unit cost Amount

Sales (81900) (13 + 9 %) 14.17 1160523

Less: Variable cost

Material 5.25 429975

Labour 2.95 241605

Overhead 1.85 151515

6

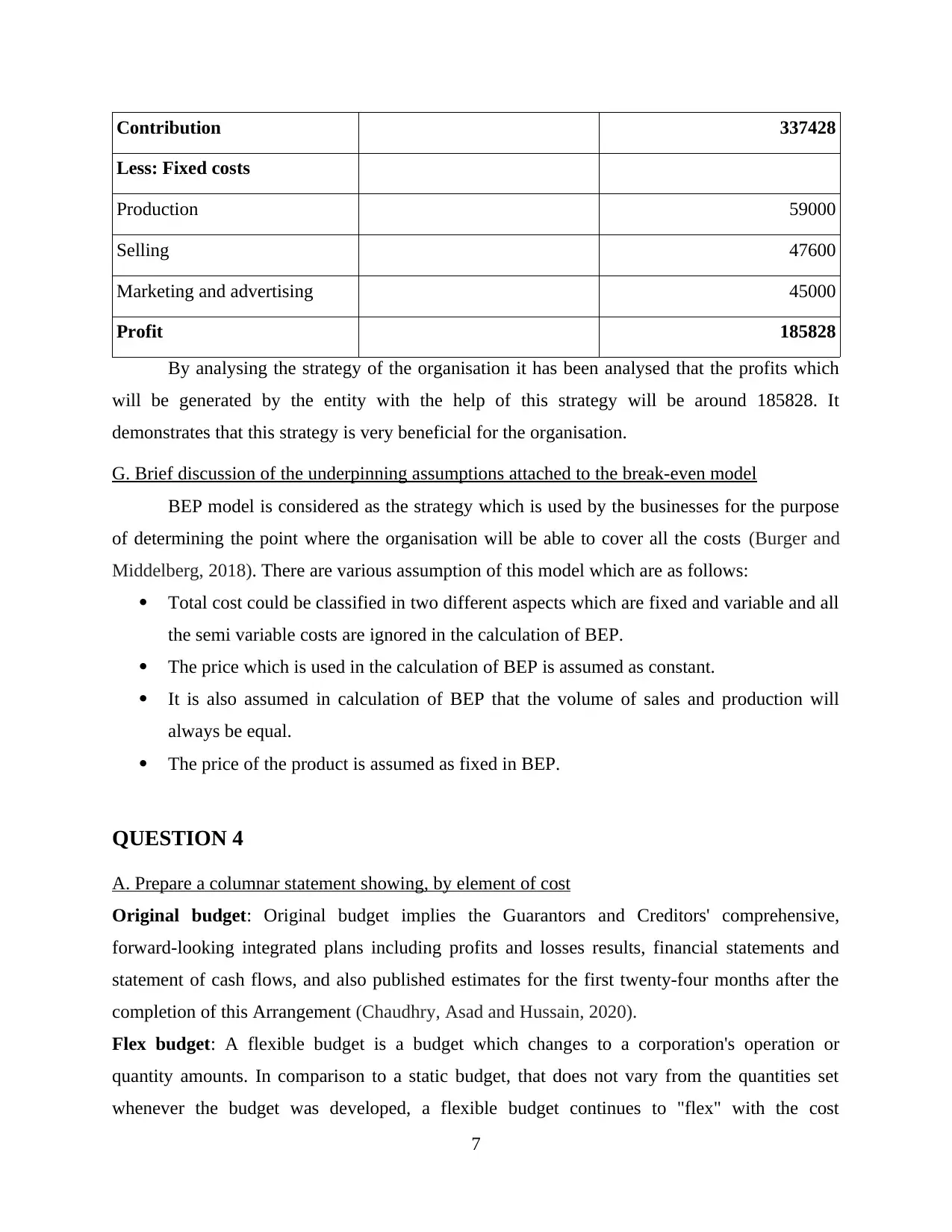

Contribution 337428

Less: Fixed costs

Production 59000

Selling 47600

Marketing and advertising 45000

Profit 185828

By analysing the strategy of the organisation it has been analysed that the profits which

will be generated by the entity with the help of this strategy will be around 185828. It

demonstrates that this strategy is very beneficial for the organisation.

G. Brief discussion of the underpinning assumptions attached to the break-even model

BEP model is considered as the strategy which is used by the businesses for the purpose

of determining the point where the organisation will be able to cover all the costs (Burger and

Middelberg, 2018). There are various assumption of this model which are as follows:

Total cost could be classified in two different aspects which are fixed and variable and all

the semi variable costs are ignored in the calculation of BEP.

The price which is used in the calculation of BEP is assumed as constant.

It is also assumed in calculation of BEP that the volume of sales and production will

always be equal.

The price of the product is assumed as fixed in BEP.

QUESTION 4

A. Prepare a columnar statement showing, by element of cost

Original budget: Original budget implies the Guarantors and Creditors' comprehensive,

forward-looking integrated plans including profits and losses results, financial statements and

statement of cash flows, and also published estimates for the first twenty-four months after the

completion of this Arrangement (Chaudhry, Asad and Hussain, 2020).

Flex budget: A flexible budget is a budget which changes to a corporation's operation or

quantity amounts. In comparison to a static budget, that does not vary from the quantities set

whenever the budget was developed, a flexible budget continues to "flex" with the cost

7

Less: Fixed costs

Production 59000

Selling 47600

Marketing and advertising 45000

Profit 185828

By analysing the strategy of the organisation it has been analysed that the profits which

will be generated by the entity with the help of this strategy will be around 185828. It

demonstrates that this strategy is very beneficial for the organisation.

G. Brief discussion of the underpinning assumptions attached to the break-even model

BEP model is considered as the strategy which is used by the businesses for the purpose

of determining the point where the organisation will be able to cover all the costs (Burger and

Middelberg, 2018). There are various assumption of this model which are as follows:

Total cost could be classified in two different aspects which are fixed and variable and all

the semi variable costs are ignored in the calculation of BEP.

The price which is used in the calculation of BEP is assumed as constant.

It is also assumed in calculation of BEP that the volume of sales and production will

always be equal.

The price of the product is assumed as fixed in BEP.

QUESTION 4

A. Prepare a columnar statement showing, by element of cost

Original budget: Original budget implies the Guarantors and Creditors' comprehensive,

forward-looking integrated plans including profits and losses results, financial statements and

statement of cash flows, and also published estimates for the first twenty-four months after the

completion of this Arrangement (Chaudhry, Asad and Hussain, 2020).

Flex budget: A flexible budget is a budget which changes to a corporation's operation or

quantity amounts. In comparison to a static budget, that does not vary from the quantities set

whenever the budget was developed, a flexible budget continues to "flex" with the cost

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

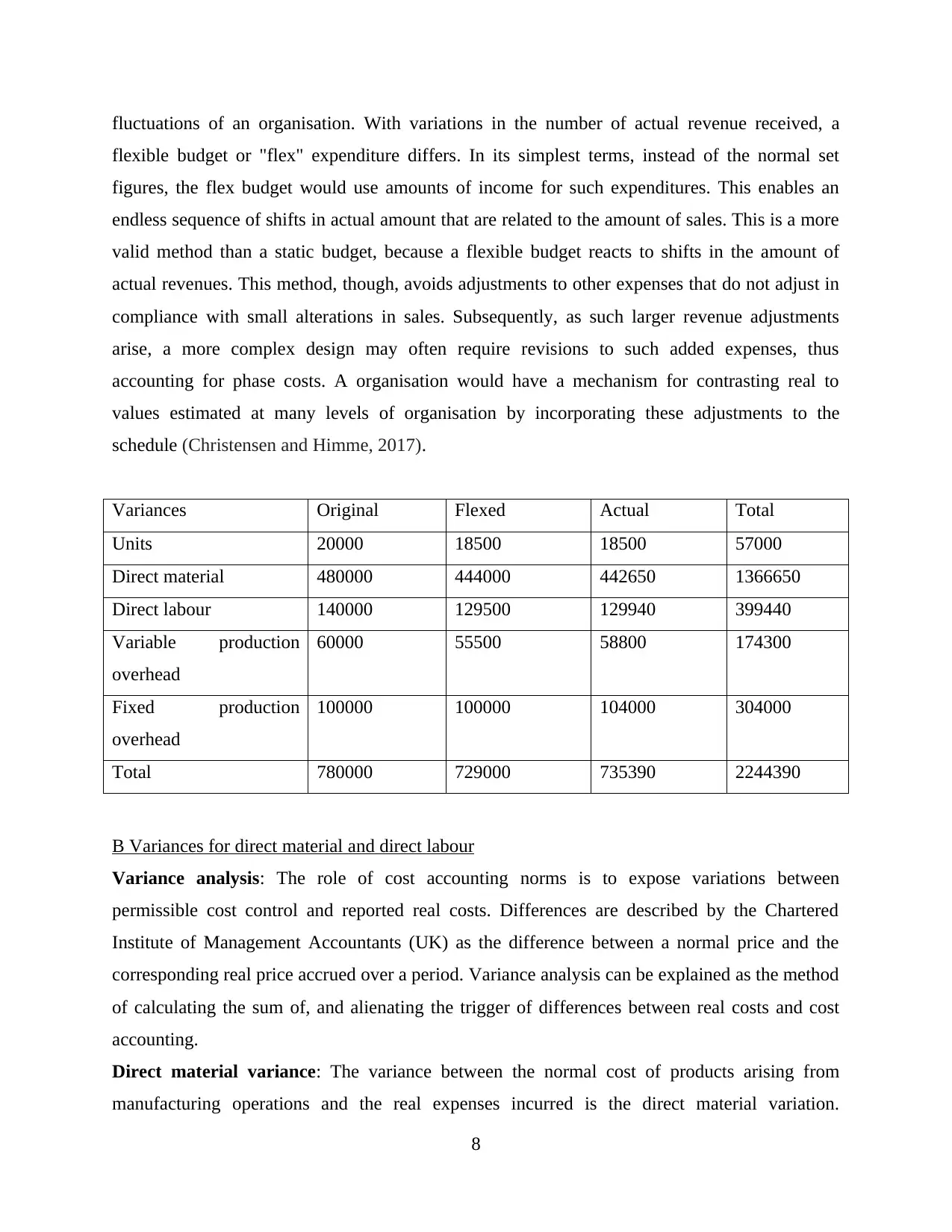

fluctuations of an organisation. With variations in the number of actual revenue received, a

flexible budget or "flex" expenditure differs. In its simplest terms, instead of the normal set

figures, the flex budget would use amounts of income for such expenditures. This enables an

endless sequence of shifts in actual amount that are related to the amount of sales. This is a more

valid method than a static budget, because a flexible budget reacts to shifts in the amount of

actual revenues. This method, though, avoids adjustments to other expenses that do not adjust in

compliance with small alterations in sales. Subsequently, as such larger revenue adjustments

arise, a more complex design may often require revisions to such added expenses, thus

accounting for phase costs. A organisation would have a mechanism for contrasting real to

values estimated at many levels of organisation by incorporating these adjustments to the

schedule (Christensen and Himme, 2017).

Variances Original Flexed Actual Total

Units 20000 18500 18500 57000

Direct material 480000 444000 442650 1366650

Direct labour 140000 129500 129940 399440

Variable production

overhead

60000 55500 58800 174300

Fixed production

overhead

100000 100000 104000 304000

Total 780000 729000 735390 2244390

B Variances for direct material and direct labour

Variance analysis: The role of cost accounting norms is to expose variations between

permissible cost control and reported real costs. Differences are described by the Chartered

Institute of Management Accountants (UK) as the difference between a normal price and the

corresponding real price accrued over a period. Variance analysis can be explained as the method

of calculating the sum of, and alienating the trigger of differences between real costs and cost

accounting.

Direct material variance: The variance between the normal cost of products arising from

manufacturing operations and the real expenses incurred is the direct material variation.

8

flexible budget or "flex" expenditure differs. In its simplest terms, instead of the normal set

figures, the flex budget would use amounts of income for such expenditures. This enables an

endless sequence of shifts in actual amount that are related to the amount of sales. This is a more

valid method than a static budget, because a flexible budget reacts to shifts in the amount of

actual revenues. This method, though, avoids adjustments to other expenses that do not adjust in

compliance with small alterations in sales. Subsequently, as such larger revenue adjustments

arise, a more complex design may often require revisions to such added expenses, thus

accounting for phase costs. A organisation would have a mechanism for contrasting real to

values estimated at many levels of organisation by incorporating these adjustments to the

schedule (Christensen and Himme, 2017).

Variances Original Flexed Actual Total

Units 20000 18500 18500 57000

Direct material 480000 444000 442650 1366650

Direct labour 140000 129500 129940 399440

Variable production

overhead

60000 55500 58800 174300

Fixed production

overhead

100000 100000 104000 304000

Total 780000 729000 735390 2244390

B Variances for direct material and direct labour

Variance analysis: The role of cost accounting norms is to expose variations between

permissible cost control and reported real costs. Differences are described by the Chartered

Institute of Management Accountants (UK) as the difference between a normal price and the

corresponding real price accrued over a period. Variance analysis can be explained as the method

of calculating the sum of, and alienating the trigger of differences between real costs and cost

accounting.

Direct material variance: The variance between the normal cost of products arising from

manufacturing operations and the real expenses incurred is the direct material variation.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Throughout the time sustained, the direct material difference is usually equipped to the cost of

products produced (Datar and Rajan, 2018).

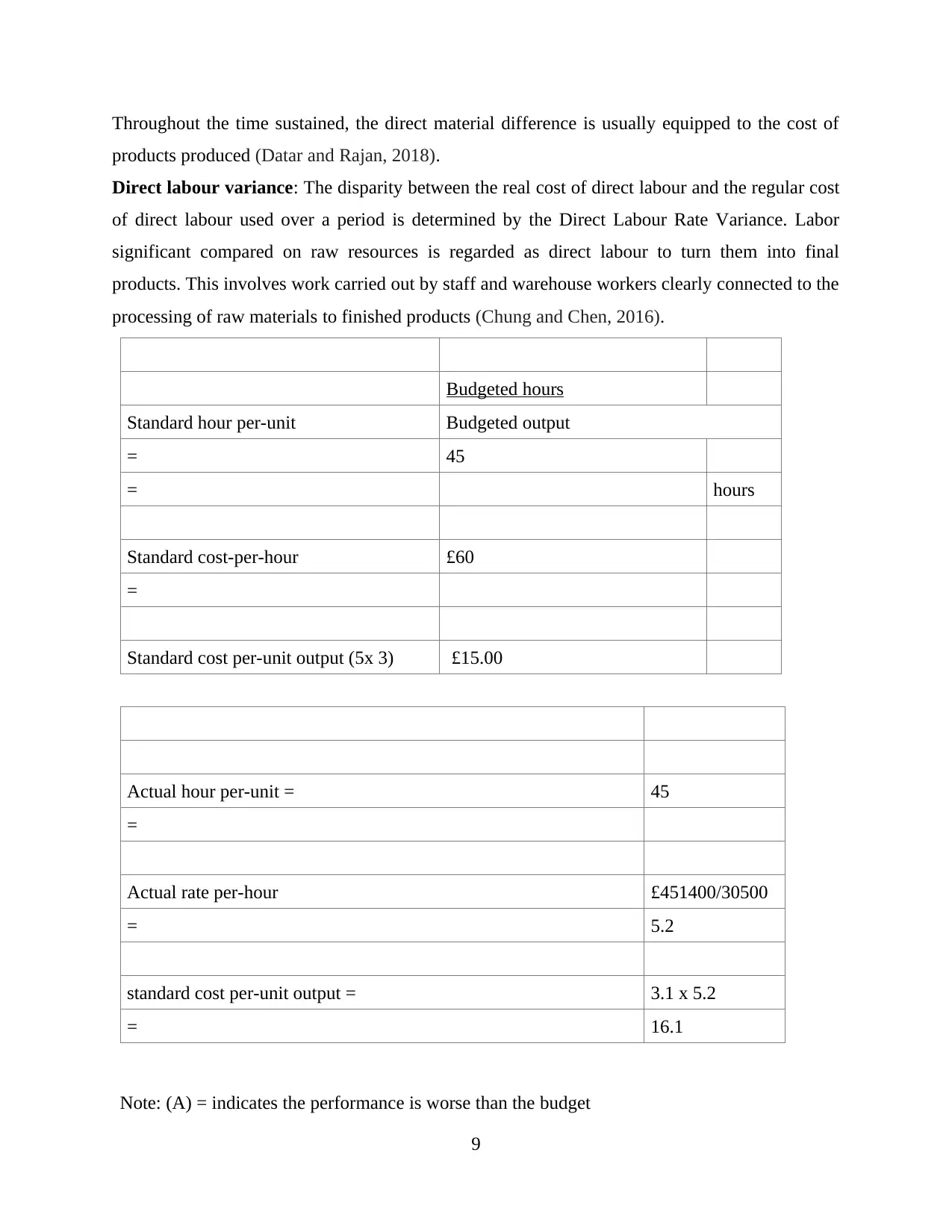

Direct labour variance: The disparity between the real cost of direct labour and the regular cost

of direct labour used over a period is determined by the Direct Labour Rate Variance. Labor

significant compared on raw resources is regarded as direct labour to turn them into final

products. This involves work carried out by staff and warehouse workers clearly connected to the

processing of raw materials to finished products (Chung and Chen, 2016).

Budgeted hours

Standard hour per-unit Budgeted output

= 45

= hours

Standard cost-per-hour £60

=

Standard cost per-unit output (5x 3) £15.00

Actual hour per-unit = 45

=

Actual rate per-hour £451400/30500

= 5.2

standard cost per-unit output = 3.1 x 5.2

= 16.1

Note: (A) = indicates the performance is worse than the budget

9

products produced (Datar and Rajan, 2018).

Direct labour variance: The disparity between the real cost of direct labour and the regular cost

of direct labour used over a period is determined by the Direct Labour Rate Variance. Labor

significant compared on raw resources is regarded as direct labour to turn them into final

products. This involves work carried out by staff and warehouse workers clearly connected to the

processing of raw materials to finished products (Chung and Chen, 2016).

Budgeted hours

Standard hour per-unit Budgeted output

= 45

= hours

Standard cost-per-hour £60

=

Standard cost per-unit output (5x 3) £15.00

Actual hour per-unit = 45

=

Actual rate per-hour £451400/30500

= 5.2

standard cost per-unit output = 3.1 x 5.2

= 16.1

Note: (A) = indicates the performance is worse than the budget

9

(F) = indicated the performance is better than the budget

Total direct wages variance consists of wage/labour rate variance and labour efficiency

variance

Labour total variance:

Labor total variance

= Actual direct labor cost £

15190.00

= Standard direct labor cost £

14110.00

£

1,230.00 (A)

Labor rate variance

= (actual hour x actual rate) - (actual hour x

standard rate)

Actual hours x standard rate £ 16500.00

Actual hours actual rate £ 18120.00

- £

1620.00 (A)

Efficiency variance

Actual unit x standard hour 1900

Actual hour 30500

= labor efficiency hours -3 (A)

Standard rate per-hour 4

Labor efficiency variance - £

450.00 (A)

Material variance

Material total variance

Total material variance

9000 units should have cost £15 £ 1080,000.00

10

Total direct wages variance consists of wage/labour rate variance and labour efficiency

variance

Labour total variance:

Labor total variance

= Actual direct labor cost £

15190.00

= Standard direct labor cost £

14110.00

£

1,230.00 (A)

Labor rate variance

= (actual hour x actual rate) - (actual hour x

standard rate)

Actual hours x standard rate £ 16500.00

Actual hours actual rate £ 18120.00

- £

1620.00 (A)

Efficiency variance

Actual unit x standard hour 1900

Actual hour 30500

= labor efficiency hours -3 (A)

Standard rate per-hour 4

Labor efficiency variance - £

450.00 (A)

Material variance

Material total variance

Total material variance

9000 units should have cost £15 £ 1080,000.00

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.