Management Accounting for Creams Ltd: Systems, Reports and Costing

VerifiedAdded on 2023/01/09

|20

|5070

|71

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on its application within Creams Ltd., a medium-sized ice cream, doughnut, and waffle producer. The report explores various management accounting systems, including cost accounting, inventory management, job costing, and price optimization, highlighting their essential requirements and advantages. It also examines different types of management accounting reports, such as account receivable aging reports, cost accounting reports, performance reports, and budget reports, and their significance in business operations. Furthermore, the report delves into cost calculation techniques like marginal costing and absorption costing, evaluating their benefits and limitations. The integration of management accounting systems and reports is critically evaluated, emphasizing their role in informed decision-making and improved profitability. The report aims to enhance understanding of management accounting principles and their practical application in a business context.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Management Accounting refers to the use of financial data and information in an

organization in such a manner so that the managers are able to take the right decisions which can

lead towards an increase in the overall profitability (Armitage, Webb and Glynn, 2016). When

the management makes use of its provisions it can ensure that right plans are made for the future

time period. The managers should focus on making use of its techniques so that they are able to

analyse and interpret the financial data and information to draw conclusions and

recommendations. This can be very helpful for them to bring the required efficiency and

effectiveness in the level of operations. For this report, Creams Ltd. has been chosen. It is a

medium-sized firm which deals in the production of ice-creams, doughnuts and waffles. In this

report, focus will be made on demonstration of understanding of management accounting

systems, application of a range of its techniques. Additionally, explaining the use of planning

tools and comparison of ways in which organizations can make use of management accounting

to respond to financial problems will be discussed as a part of this assignment.

TASK 1

P1: Management Accounting Systems and their essential requirements

Management Accounting has different types of systems. They are explained as follows-

Cost Accounting System- This system is used widely within the organizations because

its techniques are quite useful for the purpose of calculation of costs (Aureli and et.al., 2019). If

the managers of the organization are able to make use of this system in the right manner then it

will help them a lot in reducing the excessive costs and overheads in the different departments

resulting in maximization of profits. For the managers of Creams Ltd., this system is quite useful

in making of the right decisions effectively and efficiently.

Essential requirements-

This system should be able to identify the different types of departments within the

organization like Finance, HR, Marketing, Sales etc. Thus in this way rectifying

techniques can be used so that these costs are reduced.

1

Management Accounting refers to the use of financial data and information in an

organization in such a manner so that the managers are able to take the right decisions which can

lead towards an increase in the overall profitability (Armitage, Webb and Glynn, 2016). When

the management makes use of its provisions it can ensure that right plans are made for the future

time period. The managers should focus on making use of its techniques so that they are able to

analyse and interpret the financial data and information to draw conclusions and

recommendations. This can be very helpful for them to bring the required efficiency and

effectiveness in the level of operations. For this report, Creams Ltd. has been chosen. It is a

medium-sized firm which deals in the production of ice-creams, doughnuts and waffles. In this

report, focus will be made on demonstration of understanding of management accounting

systems, application of a range of its techniques. Additionally, explaining the use of planning

tools and comparison of ways in which organizations can make use of management accounting

to respond to financial problems will be discussed as a part of this assignment.

TASK 1

P1: Management Accounting Systems and their essential requirements

Management Accounting has different types of systems. They are explained as follows-

Cost Accounting System- This system is used widely within the organizations because

its techniques are quite useful for the purpose of calculation of costs (Aureli and et.al., 2019). If

the managers of the organization are able to make use of this system in the right manner then it

will help them a lot in reducing the excessive costs and overheads in the different departments

resulting in maximization of profits. For the managers of Creams Ltd., this system is quite useful

in making of the right decisions effectively and efficiently.

Essential requirements-

This system should be able to identify the different types of departments within the

organization like Finance, HR, Marketing, Sales etc. Thus in this way rectifying

techniques can be used so that these costs are reduced.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

With the use of this system different types of overheads can be identified as well as

segregated. This ensures that the companies are able to properly allocate them according

to the particular expenses made by these departments.

Advantages-

By making the use of this system, an organization can ensure that costs are controlled in a

proper manner. Therefore for the managers of Creams Ltd. this is an advantage.

When this system is used, an organization is able to use the techniques so that costs can

be reduced. This is beneficial for Creams Ltd.

Inventory Management System- With the use of this system the stock management can

be facilitated by the companies effectively and efficiently (Botes and Sharma, 2017). In this way

they can make sure that they bring the efficiency and effectiveness in their management of

inventory. In this way the managers of Creams Ltd. have an advantage in making use of this

system. This is so because by making the use of this system the managers can make sure that

they are able to track the inflows and outflows of stock without problems and issues.

Essential requirements-

This system should be able to make use of the methods like LIFO, FIFO, Weighted

Average Cost etc. This will help the organizations in tracking the inflows and outflows of

stock.

Inventory Management System should ensure that by making use of right techniques

efficiency and effectiveness can be brought in the management of the stock level.

Advantages-

By using this system, proper maintenance of records of items in the stock can be

maintained. This can help Creams Ltd.

When this system is used it can lead towards reduction in the cost of maintenance of

inventory. For Creams Ltd., it is very much beneficial.

Job Costing System- With the use of this system the companies can make sure that by

using it they can be able to find out the cost of their different job orders (Ghasemi and et.al.,

2016). By using it, the management of Creams Ltd. can identify the inflows and outflows of the

job orders and reduce the costs of its job orders.

Essential requirements-

2

segregated. This ensures that the companies are able to properly allocate them according

to the particular expenses made by these departments.

Advantages-

By making the use of this system, an organization can ensure that costs are controlled in a

proper manner. Therefore for the managers of Creams Ltd. this is an advantage.

When this system is used, an organization is able to use the techniques so that costs can

be reduced. This is beneficial for Creams Ltd.

Inventory Management System- With the use of this system the stock management can

be facilitated by the companies effectively and efficiently (Botes and Sharma, 2017). In this way

they can make sure that they bring the efficiency and effectiveness in their management of

inventory. In this way the managers of Creams Ltd. have an advantage in making use of this

system. This is so because by making the use of this system the managers can make sure that

they are able to track the inflows and outflows of stock without problems and issues.

Essential requirements-

This system should be able to make use of the methods like LIFO, FIFO, Weighted

Average Cost etc. This will help the organizations in tracking the inflows and outflows of

stock.

Inventory Management System should ensure that by making use of right techniques

efficiency and effectiveness can be brought in the management of the stock level.

Advantages-

By using this system, proper maintenance of records of items in the stock can be

maintained. This can help Creams Ltd.

When this system is used it can lead towards reduction in the cost of maintenance of

inventory. For Creams Ltd., it is very much beneficial.

Job Costing System- With the use of this system the companies can make sure that by

using it they can be able to find out the cost of their different job orders (Ghasemi and et.al.,

2016). By using it, the management of Creams Ltd. can identify the inflows and outflows of the

job orders and reduce the costs of its job orders.

Essential requirements-

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It should be able to maintain the records of different types of job orders. This helps in

bringing efficiency and effectiveness in the operations.

Job Costing System must help the organizations in finding out ways to reduce costs of

job orders so as to maximize the profits.

Advantages-

Job Costing System is helpful for the purpose of maintaining efficiency in the

management of job orders. This will help Creams Ltd.

Job Costing System is useful for the managers so that they are able to identify the ways

through which profits can be enhanced by reducing the cost of orders.

Price Optimization System- The use of this system should be able to help the firms in

making sure that they are able to use appropriate techniques for the purpose of setting a right

price within the organization (Gibassier, 2017). This can help the managers of Creams Ltd. In

increasing profits as by setting an appropriate price they will be able to achieve the various goals

and objectives.

Essential requirements-

Price Optimization System should make use of mathematical models and should forecast

the change in prices in the future time period. This can help the firms as they will be able

to make sure that they can effectively forecast the right prices to be used.

Price Optimization System must make sure that by setting the right price profits can be

maximized. This can help the organizations in achieving their goals and objectives in the

long-run.

Advantages-

Price Optimization System is helpful in ensuring that identification of right prices is

made in the organization. For Creams Ltd. this creates an advantage.

Price Optimization System is advantageous for the managers in making sure that forecast

of change in prices can be made. The managers of Creams Ltd. therefore have an

advantage here.

P2: Management Accounting Reports

Reports are the important document of organisation which is prepared by management in

order to run the business and increase the profitability. For running a business and managing

3

bringing efficiency and effectiveness in the operations.

Job Costing System must help the organizations in finding out ways to reduce costs of

job orders so as to maximize the profits.

Advantages-

Job Costing System is helpful for the purpose of maintaining efficiency in the

management of job orders. This will help Creams Ltd.

Job Costing System is useful for the managers so that they are able to identify the ways

through which profits can be enhanced by reducing the cost of orders.

Price Optimization System- The use of this system should be able to help the firms in

making sure that they are able to use appropriate techniques for the purpose of setting a right

price within the organization (Gibassier, 2017). This can help the managers of Creams Ltd. In

increasing profits as by setting an appropriate price they will be able to achieve the various goals

and objectives.

Essential requirements-

Price Optimization System should make use of mathematical models and should forecast

the change in prices in the future time period. This can help the firms as they will be able

to make sure that they can effectively forecast the right prices to be used.

Price Optimization System must make sure that by setting the right price profits can be

maximized. This can help the organizations in achieving their goals and objectives in the

long-run.

Advantages-

Price Optimization System is helpful in ensuring that identification of right prices is

made in the organization. For Creams Ltd. this creates an advantage.

Price Optimization System is advantageous for the managers in making sure that forecast

of change in prices can be made. The managers of Creams Ltd. therefore have an

advantage here.

P2: Management Accounting Reports

Reports are the important document of organisation which is prepared by management in

order to run the business and increase the profitability. For running a business and managing

3

activities there is need to focus on reports and accounting which can help to improve the business

productivity and profitability. Creams Ltd is using different types of management accounting

reports for the purpose of making a profitable business and operating a business by delivering

better quality of products and services.

Account Receivable Aging Reports – This report heavily depend on credit that states

how a business can make profits after receiving the payments (Herschung, Mahlendorf and

Weber, 2018). For businesses it is required to maintain proper records of credits that allows

managers to identify defaulter and receive the payment after a fixed period of time. The

managers of Creams Ltd is required to prepare the account receivable report by keeping proper

records of creditors and get a payment on fixed time. The credit period is 30 days, 60 days and

90 days in which unpaid customers make payment. Moreover, if there is bad debts then it need to

be written off so accurate profits can be calculated.

Cost accounting report – This reports stating the cost of organisation by involving all

income and expenses that are important to run the business and managing the activities properly

(Leotta, Rizza and Ruggeri, 2017). It is important for business industry to manage and run their

business by calculating cost and profitability. In context yo Creams Ltd managers are responsible

to prepare cost accounting reports by estimating cost and expenses which are incurred in

organisation and affected the business. This can help to manage activities as well as performance

in dynamic environment. This also provide an estimation of cost in relation to business that

covers raw material, labour, overhead, cost of inventory and transportation cost that can help to

manage the organisational performance.

Performance report – For reviewing the performance of company performance reports

are prepared by management that can help to evaluate the organisational and management

performance. Whenever organisation wants to expand their business then performance report is

helpful to evaluate the activities and making strategic plans which can help to generate higher

profits. In Creams Ltd, managers are required to prepared the performance report by evaluating

employee's and organisation's performance that can help to understand what need to do and how

it will help to improve the profitability. Moreover, employees are rewarded for their good

performance which shows by such reports that increase the motivation of them and give

confidence to work more.

4

productivity and profitability. Creams Ltd is using different types of management accounting

reports for the purpose of making a profitable business and operating a business by delivering

better quality of products and services.

Account Receivable Aging Reports – This report heavily depend on credit that states

how a business can make profits after receiving the payments (Herschung, Mahlendorf and

Weber, 2018). For businesses it is required to maintain proper records of credits that allows

managers to identify defaulter and receive the payment after a fixed period of time. The

managers of Creams Ltd is required to prepare the account receivable report by keeping proper

records of creditors and get a payment on fixed time. The credit period is 30 days, 60 days and

90 days in which unpaid customers make payment. Moreover, if there is bad debts then it need to

be written off so accurate profits can be calculated.

Cost accounting report – This reports stating the cost of organisation by involving all

income and expenses that are important to run the business and managing the activities properly

(Leotta, Rizza and Ruggeri, 2017). It is important for business industry to manage and run their

business by calculating cost and profitability. In context yo Creams Ltd managers are responsible

to prepare cost accounting reports by estimating cost and expenses which are incurred in

organisation and affected the business. This can help to manage activities as well as performance

in dynamic environment. This also provide an estimation of cost in relation to business that

covers raw material, labour, overhead, cost of inventory and transportation cost that can help to

manage the organisational performance.

Performance report – For reviewing the performance of company performance reports

are prepared by management that can help to evaluate the organisational and management

performance. Whenever organisation wants to expand their business then performance report is

helpful to evaluate the activities and making strategic plans which can help to generate higher

profits. In Creams Ltd, managers are required to prepared the performance report by evaluating

employee's and organisation's performance that can help to understand what need to do and how

it will help to improve the profitability. Moreover, employees are rewarded for their good

performance which shows by such reports that increase the motivation of them and give

confidence to work more.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Budget reports – This is defined as accounting reports in relation to a management that

needed to perform well by setting the budget properly (Hiebl and Richter, 2018). It is defined as

estimation of previous information and experiences that can help to make the right business

decisions. Creams Ltd can use budget report by involving all income and expenses which are

incurred in a business and helps to operate the business successfully. This can be uses to make

further plans of investment and completing the task in challenging situation by identifying cost

and make plans accordingly.

M1: Benefits of Management Accounting Systems

Cost Accounting System helps the organizations in segregating costs. Also it can be

helpful for them in reducing the costs effectively. Inventory Management System is helpful for

the firms in management of stock level. Also it can help them in tracking the inflows and

outflows of stock. Job Costing System helps the firms in managing the job orders in a proper

manner. Also it helps them in reducing the costs of job orders. Price Optimization System is

helpful for the firms in optimizing the price. Also it can be useful in maximization of profits.

Thus in this way it is beneficial for the management of Creams Ltd.

D1: Critical evaluation of integration of management accounting systems and management

accounting reports

These can be easily integrated within the organizational processes by making the right

use of correct accounting system and reports. This can lead towards effective decision-making

helping in bringing the required improvements easily. In this way the managers of Creams Ltd.

Can make sure that they are able to realize their goals as well as objectives and thus realize their

chance of maximization of the profits in the future time period helping them in achieving

sustainable success.

TASK 2

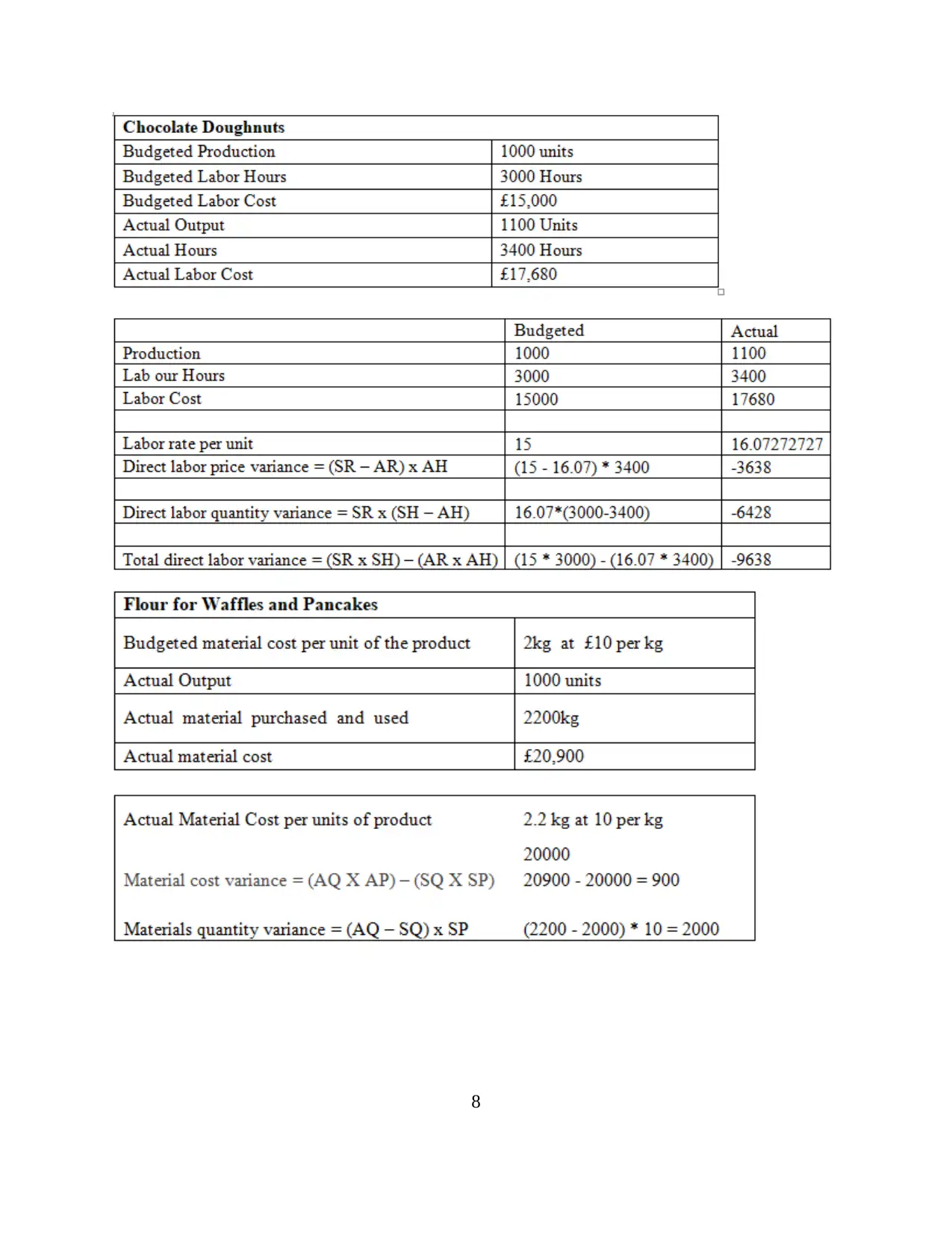

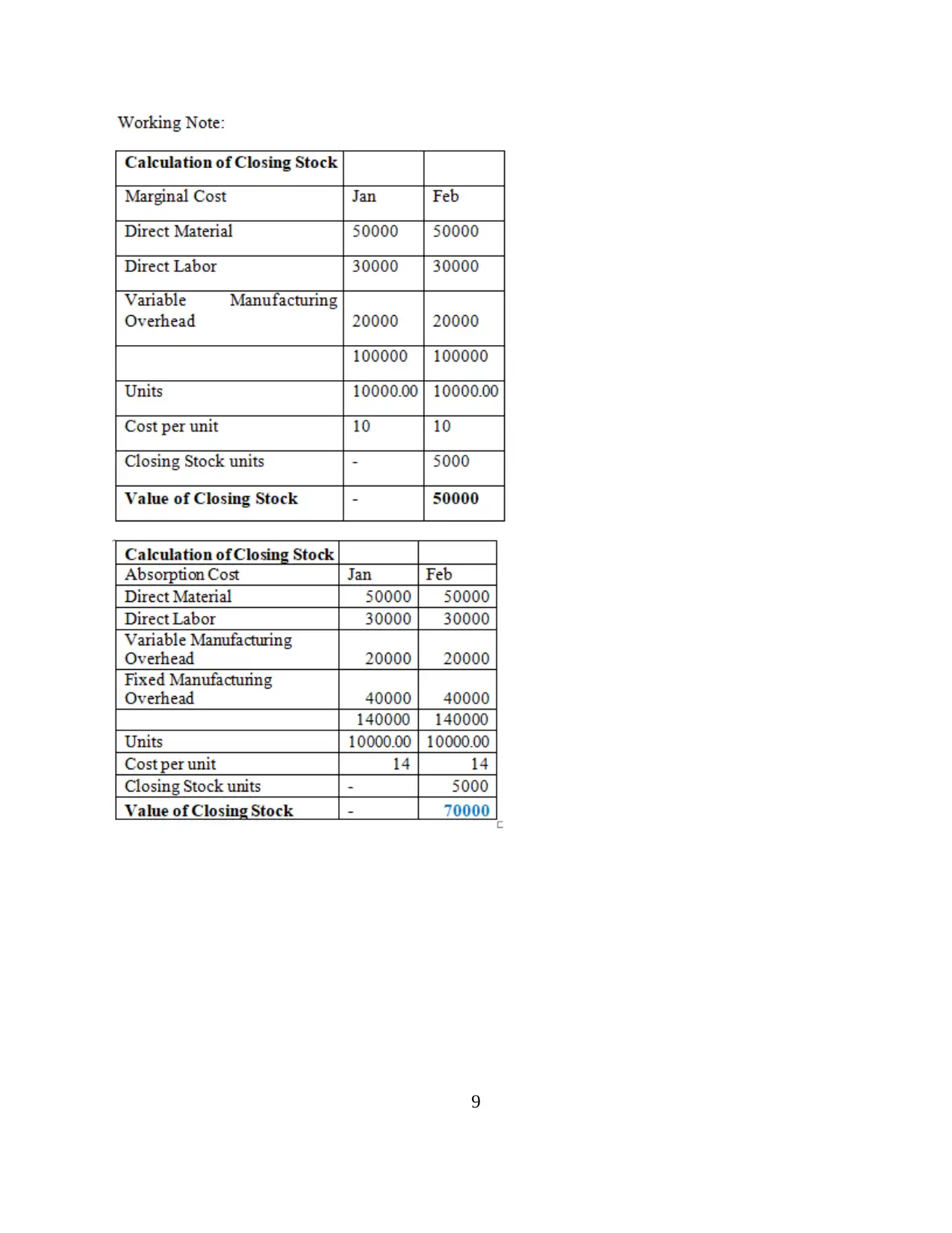

P3: Calculation of costs by making use of appropriate techniques

Profitability level can be identified with the use of various types of techniques. This can

be quite helpful in the context of the organizations. These techniques are-

Marginal costing-

5

needed to perform well by setting the budget properly (Hiebl and Richter, 2018). It is defined as

estimation of previous information and experiences that can help to make the right business

decisions. Creams Ltd can use budget report by involving all income and expenses which are

incurred in a business and helps to operate the business successfully. This can be uses to make

further plans of investment and completing the task in challenging situation by identifying cost

and make plans accordingly.

M1: Benefits of Management Accounting Systems

Cost Accounting System helps the organizations in segregating costs. Also it can be

helpful for them in reducing the costs effectively. Inventory Management System is helpful for

the firms in management of stock level. Also it can help them in tracking the inflows and

outflows of stock. Job Costing System helps the firms in managing the job orders in a proper

manner. Also it helps them in reducing the costs of job orders. Price Optimization System is

helpful for the firms in optimizing the price. Also it can be useful in maximization of profits.

Thus in this way it is beneficial for the management of Creams Ltd.

D1: Critical evaluation of integration of management accounting systems and management

accounting reports

These can be easily integrated within the organizational processes by making the right

use of correct accounting system and reports. This can lead towards effective decision-making

helping in bringing the required improvements easily. In this way the managers of Creams Ltd.

Can make sure that they are able to realize their goals as well as objectives and thus realize their

chance of maximization of the profits in the future time period helping them in achieving

sustainable success.

TASK 2

P3: Calculation of costs by making use of appropriate techniques

Profitability level can be identified with the use of various types of techniques. This can

be quite helpful in the context of the organizations. These techniques are-

Marginal costing-

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

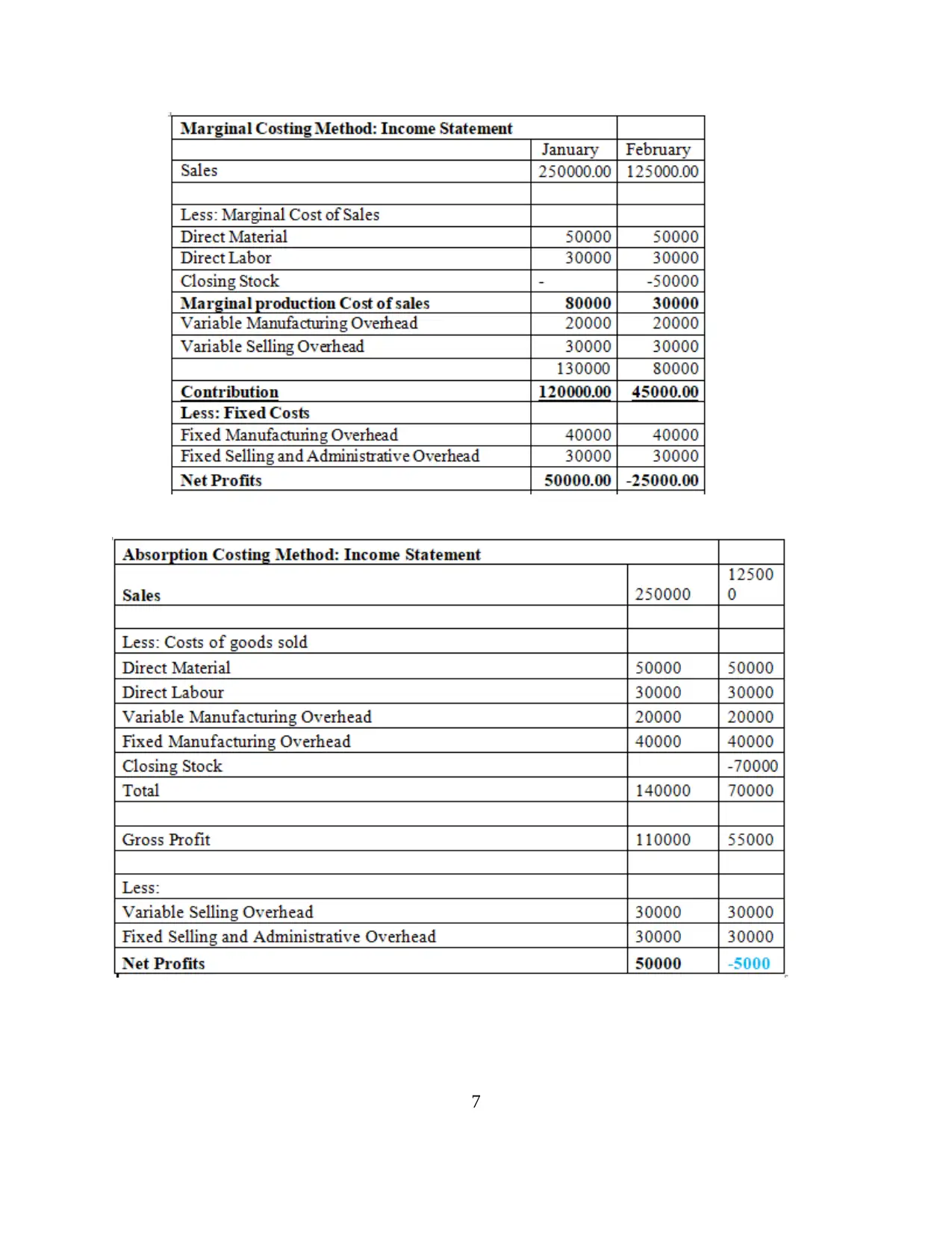

It is a technique which is used quite commonly so that the organizations are able to find

out the break-even point (Honggowati and et.al., 2017). It is a point where it earns neither profits

nor does it incurs losses. This is useful for facilitation of comparison with other companies. In it,

the variable cost is charged to the units of production and fixed cost is written off against it.

Creams Ltd. can make use of this technique so that it is able to effectively find out its profits

easily.

Advantages-

The use of Marginal Costing technique is helpful for the managers in determining the

break-even point. Thus in this way it is advantageous for the management of Creams Ltd.

This technique is very useful for the managers because it is very simple to use and

understand. This is beneficial for Creams Ltd.'s management.

Disadvantages-

It is not useful in the computation of overheads within the organization which is quite

crucial. This creates disadvantage for the managers of Creams Ltd.

Marginal Costing technique can be disadvantageous because it is not comprehensive in

nature. This is a disadvantage for the management of Creams Ltd.

Absorption Costing-

It is a technique in which the comprehensive computation of overall costs within an organization

is made. The managers of Creams Ltd. can make sure that by making use of this technique they

are able to evaluate the total costs in the company.

Advantages-

Absorption Costing technique facilitates the treatment of overheads incurring within the

organization. This is an advantage for the management of Creams Ltd.

This technique helps in the segregation of the different types of costs which are incurred

in the departments. In this way an advantage is created for the managers of Creams Ltd.

Disadvantages-

This technique is not helpful for the managers in comparing and controlling the costs in

the organization. This is a disadvantage for Creams Ltd.

Absorption Costing technique does not helps the managers to take decisions. For the

managers of Creams Ltd., this is a disadvantage.

6

out the break-even point (Honggowati and et.al., 2017). It is a point where it earns neither profits

nor does it incurs losses. This is useful for facilitation of comparison with other companies. In it,

the variable cost is charged to the units of production and fixed cost is written off against it.

Creams Ltd. can make use of this technique so that it is able to effectively find out its profits

easily.

Advantages-

The use of Marginal Costing technique is helpful for the managers in determining the

break-even point. Thus in this way it is advantageous for the management of Creams Ltd.

This technique is very useful for the managers because it is very simple to use and

understand. This is beneficial for Creams Ltd.'s management.

Disadvantages-

It is not useful in the computation of overheads within the organization which is quite

crucial. This creates disadvantage for the managers of Creams Ltd.

Marginal Costing technique can be disadvantageous because it is not comprehensive in

nature. This is a disadvantage for the management of Creams Ltd.

Absorption Costing-

It is a technique in which the comprehensive computation of overall costs within an organization

is made. The managers of Creams Ltd. can make sure that by making use of this technique they

are able to evaluate the total costs in the company.

Advantages-

Absorption Costing technique facilitates the treatment of overheads incurring within the

organization. This is an advantage for the management of Creams Ltd.

This technique helps in the segregation of the different types of costs which are incurred

in the departments. In this way an advantage is created for the managers of Creams Ltd.

Disadvantages-

This technique is not helpful for the managers in comparing and controlling the costs in

the organization. This is a disadvantage for Creams Ltd.

Absorption Costing technique does not helps the managers to take decisions. For the

managers of Creams Ltd., this is a disadvantage.

6

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

9

M2: Application of management accounting techniques

Both of these costing techniques can be used by the companies for the facilitation of the

calculation of costs and profits. This helps in producing financial statements in the organization.

Thus the managers of Creams Ltd. are required to ensure that they can make use of these

techniques effectively and efficiently and provide good financial statements which reflect the

financial position of the company so that appropriate comparison can be made with other firms

and the necessary improvements can be made with the use of rectifying techniques.

D2: Producing of financial reports

Cash Flow Statement, Trading A/c, Profit and Loss A/c and Balance Sheet are financial

reports which are very helpful for the managers because they not only reflect the profitability and

financial position but also help in analysis and interpretation. Using them, the management of

Creams Ltd. can find out the problems and issues which they are facing and thus in this way can

use techniques to find solutions to them.

10

Both of these costing techniques can be used by the companies for the facilitation of the

calculation of costs and profits. This helps in producing financial statements in the organization.

Thus the managers of Creams Ltd. are required to ensure that they can make use of these

techniques effectively and efficiently and provide good financial statements which reflect the

financial position of the company so that appropriate comparison can be made with other firms

and the necessary improvements can be made with the use of rectifying techniques.

D2: Producing of financial reports

Cash Flow Statement, Trading A/c, Profit and Loss A/c and Balance Sheet are financial

reports which are very helpful for the managers because they not only reflect the profitability and

financial position but also help in analysis and interpretation. Using them, the management of

Creams Ltd. can find out the problems and issues which they are facing and thus in this way can

use techniques to find solutions to them.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.