Management Accounting Report: Techniques and Planning Tools Analysis

VerifiedAdded on 2020/10/22

|19

|6020

|335

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles, focusing on their application within a retail clothing company, Rowlinson Knitwear. The report begins by defining management accounting and its distinctions from financial accounting, emphasizing the importance of various accounting systems such as price optimization, activity-based costing, inventory management, and cost accounting. It then details the different types of management accounting reports, including financial reports, cash flow reports, sales reports, performance reports, and job cost reports, highlighting their significance in providing a clear picture of an organization's financial position. The report further explores the benefits and applications of these systems, followed by a critical analysis of accounting reporting systems. The core of the report delves into costing techniques, specifically marginal and absorption costing, and their application in calculating costs and net income. It also examines planning tools used for budgetary control, including their advantages and disadvantages. Finally, the report compares how organizations adapt management accounting systems to address financial problems and evaluates the effectiveness of various planning tools.

Unit 5

Management Accounting

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Management accounting and need of various types of accounting systems..........................3

P2 Methods used for management accounting reporting............................................................5

M1 Benefits and applications of management accounting systems............................................7

D1 Critical analyses of accounting reporting system..................................................................7

TASK 2............................................................................................................................................8

P3 Calculation of costs and net income using marginal and absorption costing........................8

M2 Types of management accounting techniques....................................................................10

D2 Interpretation of data...........................................................................................................10

TASK 3..........................................................................................................................................11

P4 Advantages and disadvantages of various planning tools used for budgetary control .......11

M3 Applications of planning tools of budgetary control .........................................................12

TASK 4..........................................................................................................................................13

P5 Comparison on how organisations are adapting management accounting systems............13

M4 Analyses of financial problems..........................................................................................14

D3 Evaluation of planning tools...............................................................................................15

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Management accounting and need of various types of accounting systems..........................3

P2 Methods used for management accounting reporting............................................................5

M1 Benefits and applications of management accounting systems............................................7

D1 Critical analyses of accounting reporting system..................................................................7

TASK 2............................................................................................................................................8

P3 Calculation of costs and net income using marginal and absorption costing........................8

M2 Types of management accounting techniques....................................................................10

D2 Interpretation of data...........................................................................................................10

TASK 3..........................................................................................................................................11

P4 Advantages and disadvantages of various planning tools used for budgetary control .......11

M3 Applications of planning tools of budgetary control .........................................................12

TASK 4..........................................................................................................................................13

P5 Comparison on how organisations are adapting management accounting systems............13

M4 Analyses of financial problems..........................................................................................14

D3 Evaluation of planning tools...............................................................................................15

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

Management accounting is a core function while managing an organisation, which

includes various systems and techniques to prepare managerial reports and other documents so

that it can reflect a true and fair managerial and financial position of an organisation which helps

investors and other related parties to access accurate management reports and records.

Rowlinson Knitwear is a retail clothing company which deals in personalised knitwear, which

uses cost analyses techniques like marginal and absorption costing to prepare their income

statement and uses planning tools for the preparation of the budgets which are the future

estimates of their expenses and profits (Banerjee, 2012).

This project focuses on management accounting and its tools and techniques which helps

an organisation like Rowlinson Knitwear in the preparation of their managerial accounts and

reports for efficient decision-making process. Accounting techniques like marginal and

absorption costing used to determine net income and profitability by charging various expenses

including variable or fixed.

TASK 1

P1 Management accounting and need of various types of accounting systems

Management accounting refers to the process of preparing management accounting

documents and reports and extract the information from those reports to analyse, interpret and

represent the information in an understandable form. Management accounting is different from

financial accounting as it has a wider scope, it controls all management issues including financial

issues.

Rowlinson knitwear is a clothing retailer company based in United Kingdom which deals

in personalised knitwear, Rowlinson is the leading manufacturer in United Kingdom which uses

management accounting systems to improve their decision-making process. For an effective

management organisation uses various management accounting systems and they are:

Types of various management accounting systems and their requirements in an

organisation

Management accounting systems are the methods of recording and analysing which an

organisational manager to understand true and fair position of the organisation, these systems

are:

Management accounting is a core function while managing an organisation, which

includes various systems and techniques to prepare managerial reports and other documents so

that it can reflect a true and fair managerial and financial position of an organisation which helps

investors and other related parties to access accurate management reports and records.

Rowlinson Knitwear is a retail clothing company which deals in personalised knitwear, which

uses cost analyses techniques like marginal and absorption costing to prepare their income

statement and uses planning tools for the preparation of the budgets which are the future

estimates of their expenses and profits (Banerjee, 2012).

This project focuses on management accounting and its tools and techniques which helps

an organisation like Rowlinson Knitwear in the preparation of their managerial accounts and

reports for efficient decision-making process. Accounting techniques like marginal and

absorption costing used to determine net income and profitability by charging various expenses

including variable or fixed.

TASK 1

P1 Management accounting and need of various types of accounting systems

Management accounting refers to the process of preparing management accounting

documents and reports and extract the information from those reports to analyse, interpret and

represent the information in an understandable form. Management accounting is different from

financial accounting as it has a wider scope, it controls all management issues including financial

issues.

Rowlinson knitwear is a clothing retailer company based in United Kingdom which deals

in personalised knitwear, Rowlinson is the leading manufacturer in United Kingdom which uses

management accounting systems to improve their decision-making process. For an effective

management organisation uses various management accounting systems and they are:

Types of various management accounting systems and their requirements in an

organisation

Management accounting systems are the methods of recording and analysing which an

organisational manager to understand true and fair position of the organisation, these systems

are:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Price optimisation systems – Price optimisation system is a management accounting

technique which helps an organisation to allocate different prices to their different

produced products and analyse the reaction of the customers, so that effective pricing

strategy can be developed. Rowlinson Knitwear delivers personalised school wear due to

which they have different prices for their various products due to which they uses price

optimisation system to satisfy all their customers and at the same time can earn

reasonable profits (Burritt, 2011).

Activity based costing – Activity based costing or system is a process of determination

of costs involved in an activity performed by the organisation. For example, in case of

Rowlinson knitwear they determine the costs of their various activities like

manufacturing, packaging etc. by activity-based costing as it delivers accurate and

reliable results which can be trusted for preparing of financial and managerial reports.

Inventory management system – Inventory management system is a process of

managing and controlling the issues related to inventory stocked in an organisation.

Rowlinson Knitwear is a retail store in United Kingdom and delivers number of clothes

every year due to which they requires an efficient inventory management system and this

management accounting system provides a framework to manage and control their

inventories including raw material and goods engaged in work in progress so that their

organisational objectives like customer satisfaction and profit maximisation can be

achieved.

Cost accounting system – Cost accounting system is a method which helps an

organisation to determine all their costs involved in an organisation so that they can

estimate their profitability, here Rowlinson Knitwear also uses cost accounting system to

estimate all the costs which can be included in their processes so that a clear profit can be

ascertained.

Job costing – Job costing system is a process of determining the cost involved in an

specific job, job costing helps an organisation to determine costs for various job this

system is appropriate for the organisations where there is production of customised

products like Rowlinson Knitwear which deals in personalised products (Christ, 2013).

Product costing – Product costing system is a method of determining all the costs

involved in a product which is manufactured by an organisation including all direct and

technique which helps an organisation to allocate different prices to their different

produced products and analyse the reaction of the customers, so that effective pricing

strategy can be developed. Rowlinson Knitwear delivers personalised school wear due to

which they have different prices for their various products due to which they uses price

optimisation system to satisfy all their customers and at the same time can earn

reasonable profits (Burritt, 2011).

Activity based costing – Activity based costing or system is a process of determination

of costs involved in an activity performed by the organisation. For example, in case of

Rowlinson knitwear they determine the costs of their various activities like

manufacturing, packaging etc. by activity-based costing as it delivers accurate and

reliable results which can be trusted for preparing of financial and managerial reports.

Inventory management system – Inventory management system is a process of

managing and controlling the issues related to inventory stocked in an organisation.

Rowlinson Knitwear is a retail store in United Kingdom and delivers number of clothes

every year due to which they requires an efficient inventory management system and this

management accounting system provides a framework to manage and control their

inventories including raw material and goods engaged in work in progress so that their

organisational objectives like customer satisfaction and profit maximisation can be

achieved.

Cost accounting system – Cost accounting system is a method which helps an

organisation to determine all their costs involved in an organisation so that they can

estimate their profitability, here Rowlinson Knitwear also uses cost accounting system to

estimate all the costs which can be included in their processes so that a clear profit can be

ascertained.

Job costing – Job costing system is a process of determining the cost involved in an

specific job, job costing helps an organisation to determine costs for various job this

system is appropriate for the organisations where there is production of customised

products like Rowlinson Knitwear which deals in personalised products (Christ, 2013).

Product costing – Product costing system is a method of determining all the costs

involved in a product which is manufactured by an organisation including all direct and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

indirect costs like direct material, direct labour, other variable and fixed manufacturing

expenses. Here, Rowlinson Knitwear has also adapted cost accounting system to

determine costs of their products so that they can allocate the prices and ascertain the

profitability.

P2 Methods used for management accounting reporting

Management accounting reports are the managerial documents which reflect the true and

fair picture of an organisation's financial position, preparation of these management accounting

reports are a crucial task to perform as it requires high skills. There are many reports which can

be prepared like financial and costing reports but unlike management accounting report they

can’t present an exact reflection of the organisation's financial and managerial position.

Rowlinson knitwear has hired a team of professionals who look after their managerial

accounts and reports to make sure that investors and other parties can access accurate reports and

other managerial documents ( Contrafatto, 2013).

Types of management accounting reports

Management accounting report is an organisational management document which is

prepared by the managers for the third parties so that they can access a true and fair picture of the

organisation, few of those management accounting reports are:

Financial reports – Usually financial reports are included in financial accounting but to

acknowledge an accurate management position of an organisation it’s important for the

managers to include financial report while preparing managerial accounting report as it

reflect figures and exact numbers of the organisation's profitability, costs etc. Financial

reports of an organisation mainly includes trading account, profit and loss statement and

balance sheet. Rowlinson Knitwear prepares their financial report by including their

profit and loss statement which shows all revenues and expenditures of the organisation

and balance sheet which the evidence of the assets and liabilities is.

Cash flow report – Cash flow statement or report includes all cash transactions of the

organisation which affects an organisation's performance. It includes all inflow and

outflow cash transaction occurred from operating, investing and financing activities,

Rowlinson Knitwear prepares cash flow statement for short periods which can be

beneficial for them to access monthly estimates of expenses and which can update easily.

expenses. Here, Rowlinson Knitwear has also adapted cost accounting system to

determine costs of their products so that they can allocate the prices and ascertain the

profitability.

P2 Methods used for management accounting reporting

Management accounting reports are the managerial documents which reflect the true and

fair picture of an organisation's financial position, preparation of these management accounting

reports are a crucial task to perform as it requires high skills. There are many reports which can

be prepared like financial and costing reports but unlike management accounting report they

can’t present an exact reflection of the organisation's financial and managerial position.

Rowlinson knitwear has hired a team of professionals who look after their managerial

accounts and reports to make sure that investors and other parties can access accurate reports and

other managerial documents ( Contrafatto, 2013).

Types of management accounting reports

Management accounting report is an organisational management document which is

prepared by the managers for the third parties so that they can access a true and fair picture of the

organisation, few of those management accounting reports are:

Financial reports – Usually financial reports are included in financial accounting but to

acknowledge an accurate management position of an organisation it’s important for the

managers to include financial report while preparing managerial accounting report as it

reflect figures and exact numbers of the organisation's profitability, costs etc. Financial

reports of an organisation mainly includes trading account, profit and loss statement and

balance sheet. Rowlinson Knitwear prepares their financial report by including their

profit and loss statement which shows all revenues and expenditures of the organisation

and balance sheet which the evidence of the assets and liabilities is.

Cash flow report – Cash flow statement or report includes all cash transactions of the

organisation which affects an organisation's performance. It includes all inflow and

outflow cash transaction occurred from operating, investing and financing activities,

Rowlinson Knitwear prepares cash flow statement for short periods which can be

beneficial for them to access monthly estimates of expenses and which can update easily.

Sales report – Sales report includes sales done in a financial year which can help an

organisation analysing what sources are more profitable and identifies those salespeople

who generates most income. Rowlinson Knitwear prepare their sales report by

determining all sales made in an year, and analyses which distribution channel is

generating more revenue that is retail distribution channel or wholesale distribution

channel (Fullerton, 2014).

Performance report – Performance report are prepared to check overall performance of

an organisation including every employee of every department, managers of an

organisation analyse and evaluates performances of employees and compare it from

various pre-fixed standards and benchmarks. Rowlinson Knitwear prepares their

performance report to have accurate results for development of their strategies which can

lead them towards achievement of their goals.

Job cost report – Job cost report is a type of management accounting report which

determines the costs involved in various jobs performed in an organisation. Job cost

report helps organisations like Rowlinson knitwear to evaluates and identify the profit-

making ability of various job activities, so that manager can focus on most profitable job

activity.

Account receivable report – Account receivable report is a document which contains

lists of all unpaid customer along with their amounts, dates and accounting periods.

Accounting receivable report is prepared to account the records of all unpaid buyers to

make sure that all amount is received duly, if any unpaid buyer fails to pay the amount

than it will be recorded in bad debts report separately or in the section of bad debts in

account receivable report only.

Inventory management report – Inventory management report is an accounting

document where all inventories of an organisation are recorded regardless of its nature

like raw material, goods engaged in work in progress or final products. This accounting

report is important as organisations like Rowlinson Knitwear which diversity in their

products and inventories are in much need of an effective inventory management report

system, so that all stocked inventories can be used efficiently ( Giovannoni, 2011).

organisation analysing what sources are more profitable and identifies those salespeople

who generates most income. Rowlinson Knitwear prepare their sales report by

determining all sales made in an year, and analyses which distribution channel is

generating more revenue that is retail distribution channel or wholesale distribution

channel (Fullerton, 2014).

Performance report – Performance report are prepared to check overall performance of

an organisation including every employee of every department, managers of an

organisation analyse and evaluates performances of employees and compare it from

various pre-fixed standards and benchmarks. Rowlinson Knitwear prepares their

performance report to have accurate results for development of their strategies which can

lead them towards achievement of their goals.

Job cost report – Job cost report is a type of management accounting report which

determines the costs involved in various jobs performed in an organisation. Job cost

report helps organisations like Rowlinson knitwear to evaluates and identify the profit-

making ability of various job activities, so that manager can focus on most profitable job

activity.

Account receivable report – Account receivable report is a document which contains

lists of all unpaid customer along with their amounts, dates and accounting periods.

Accounting receivable report is prepared to account the records of all unpaid buyers to

make sure that all amount is received duly, if any unpaid buyer fails to pay the amount

than it will be recorded in bad debts report separately or in the section of bad debts in

account receivable report only.

Inventory management report – Inventory management report is an accounting

document where all inventories of an organisation are recorded regardless of its nature

like raw material, goods engaged in work in progress or final products. This accounting

report is important as organisations like Rowlinson Knitwear which diversity in their

products and inventories are in much need of an effective inventory management report

system, so that all stocked inventories can be used efficiently ( Giovannoni, 2011).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

M1 Benefits and applications of management accounting systems

Management accounting systems are developed for the ease of organisations and these

systems are universal applicable, different systems are appropriate for different type of

organisations depending on its size, scope and nature. Application and benefits of these

management accounting systems are described below:

Price optimisation system This system is appropriate for those

organisations which has diversity in their

products, due to which this system is

applicable where there is need of allocate the

prices to different produced goods.

Activity based cost system Activity based system is applicable on

organisations where there are different

departments and complexity in activities like

Rowlinson Knitwear

Inventory management system This management system benefits those

organisations which has a lot of stocked

inventories like grocery stores.

Cost accounting system Cost accounting system is beneficial for every

organisation as it helps in determining the costs

involved in every activity and product of the

organisation.

D1 Critical analyses of accounting reporting system

Management accounting is a process of preparing management accounting documents to

serve valuable and reliable information in an understandable way, management accounting

documents or reports are prepared by the help of management accounting systems. Cost

accounting system is used to prepare performance report, similarly inventory management report

is prepared with the help of inventory management system which shows the integrated

mechanism of management accounting systems and management accounting reporting ( Hilton,

2013).

Management accounting systems are developed for the ease of organisations and these

systems are universal applicable, different systems are appropriate for different type of

organisations depending on its size, scope and nature. Application and benefits of these

management accounting systems are described below:

Price optimisation system This system is appropriate for those

organisations which has diversity in their

products, due to which this system is

applicable where there is need of allocate the

prices to different produced goods.

Activity based cost system Activity based system is applicable on

organisations where there are different

departments and complexity in activities like

Rowlinson Knitwear

Inventory management system This management system benefits those

organisations which has a lot of stocked

inventories like grocery stores.

Cost accounting system Cost accounting system is beneficial for every

organisation as it helps in determining the costs

involved in every activity and product of the

organisation.

D1 Critical analyses of accounting reporting system

Management accounting is a process of preparing management accounting documents to

serve valuable and reliable information in an understandable way, management accounting

documents or reports are prepared by the help of management accounting systems. Cost

accounting system is used to prepare performance report, similarly inventory management report

is prepared with the help of inventory management system which shows the integrated

mechanism of management accounting systems and management accounting reporting ( Hilton,

2013).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Rowlinson Knitwear integrates management systems to management reporting for

effective decision making, manager of Rowlinson Knitwear has appointed a team of professional

which prepares management accounting reports using management accounting systems.

TASK 2

P3 Calculation of costs and net income using marginal and absorption costing

Marginal costing – Marginal costing is the costing technique where all variable costs are

charged against sales to calculate contribution and all fixed costs are charged against

contribution to ascertain net income or profit of the organisation. Variable costs are the sum of

all marginal costs including direct material costs, direct labour costs and other variable

manufacturing costs ( Lambert, 2012).

Marginal costs are used by organisations so that they can ascertain their profit-making

ability after charging all costs by using below mentioned formula:

Sales revenue – Marginal costs (Direct material+Direct labour+Direct expenses+Variable

overheads) = Contribution – Fixed costs = Net income or profit

Particulars Amount

Sales revenue = (selling price * no. of goods sold = 55 * 600) 33000

Marginal Cost of goods sold: 9600

Production = (units produced * marginal cost per unit = 800 * 16) 12800

closing stock = (closing stock units * marginal cost per unit = 200 *

16) 3200

Contribution 23400

Fixed cost ( 3200+1200+1500 ) 5900

Net profit 17500

Absorption costing – Absorption costing is a cost accounting technique where all costs

of goods sold or manufacturing costs are absorbed by sales revenue to ascertain gross profit,

costs of goods sold includes all manufacturing costs including direct material, direct labour and

effective decision making, manager of Rowlinson Knitwear has appointed a team of professional

which prepares management accounting reports using management accounting systems.

TASK 2

P3 Calculation of costs and net income using marginal and absorption costing

Marginal costing – Marginal costing is the costing technique where all variable costs are

charged against sales to calculate contribution and all fixed costs are charged against

contribution to ascertain net income or profit of the organisation. Variable costs are the sum of

all marginal costs including direct material costs, direct labour costs and other variable

manufacturing costs ( Lambert, 2012).

Marginal costs are used by organisations so that they can ascertain their profit-making

ability after charging all costs by using below mentioned formula:

Sales revenue – Marginal costs (Direct material+Direct labour+Direct expenses+Variable

overheads) = Contribution – Fixed costs = Net income or profit

Particulars Amount

Sales revenue = (selling price * no. of goods sold = 55 * 600) 33000

Marginal Cost of goods sold: 9600

Production = (units produced * marginal cost per unit = 800 * 16) 12800

closing stock = (closing stock units * marginal cost per unit = 200 *

16) 3200

Contribution 23400

Fixed cost ( 3200+1200+1500 ) 5900

Net profit 17500

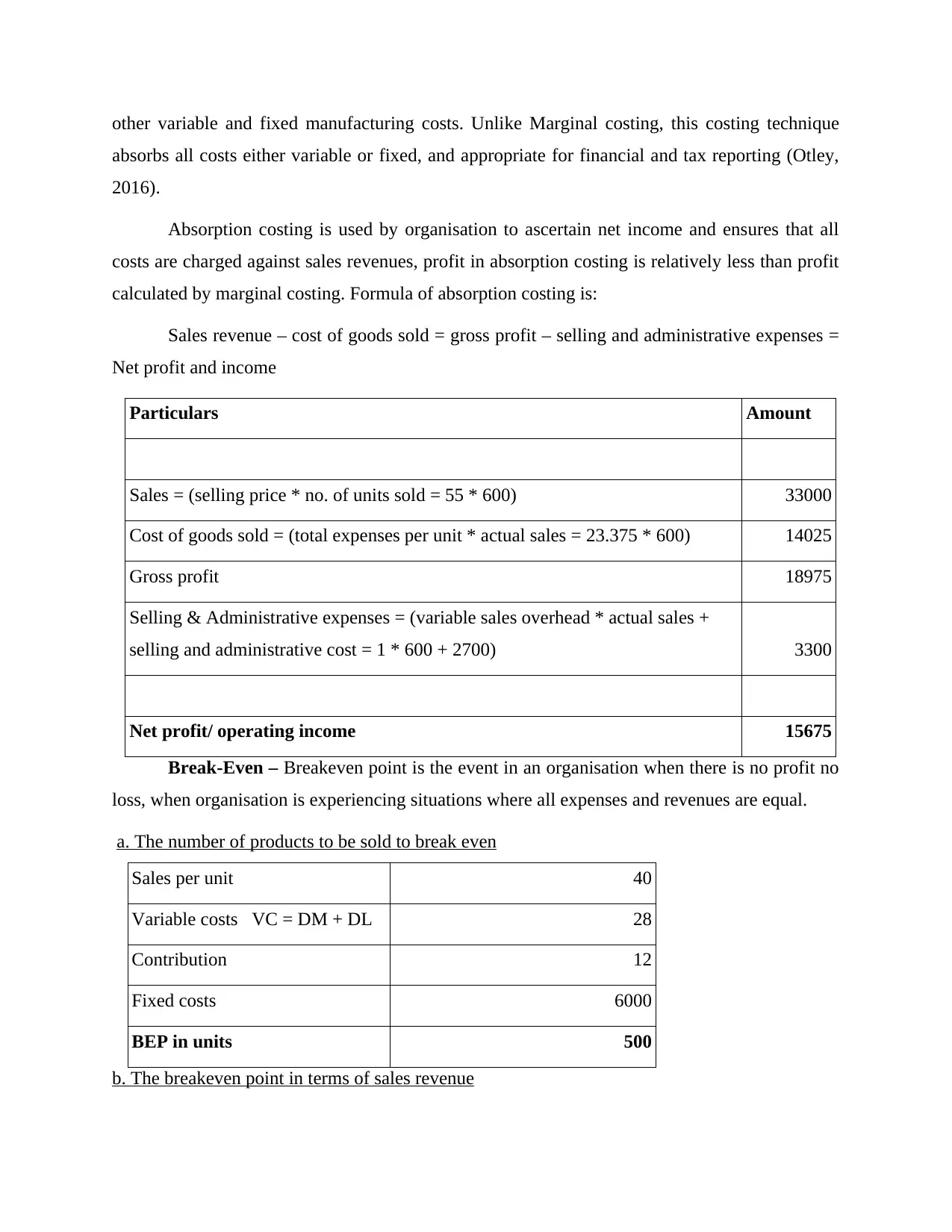

Absorption costing – Absorption costing is a cost accounting technique where all costs

of goods sold or manufacturing costs are absorbed by sales revenue to ascertain gross profit,

costs of goods sold includes all manufacturing costs including direct material, direct labour and

other variable and fixed manufacturing costs. Unlike Marginal costing, this costing technique

absorbs all costs either variable or fixed, and appropriate for financial and tax reporting (Otley,

2016).

Absorption costing is used by organisation to ascertain net income and ensures that all

costs are charged against sales revenues, profit in absorption costing is relatively less than profit

calculated by marginal costing. Formula of absorption costing is:

Sales revenue – cost of goods sold = gross profit – selling and administrative expenses =

Net profit and income

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales +

selling and administrative cost = 1 * 600 + 2700) 3300

Net profit/ operating income 15675

Break-Even – Breakeven point is the event in an organisation when there is no profit no

loss, when organisation is experiencing situations where all expenses and revenues are equal.

a. The number of products to be sold to break even

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

BEP in units 500

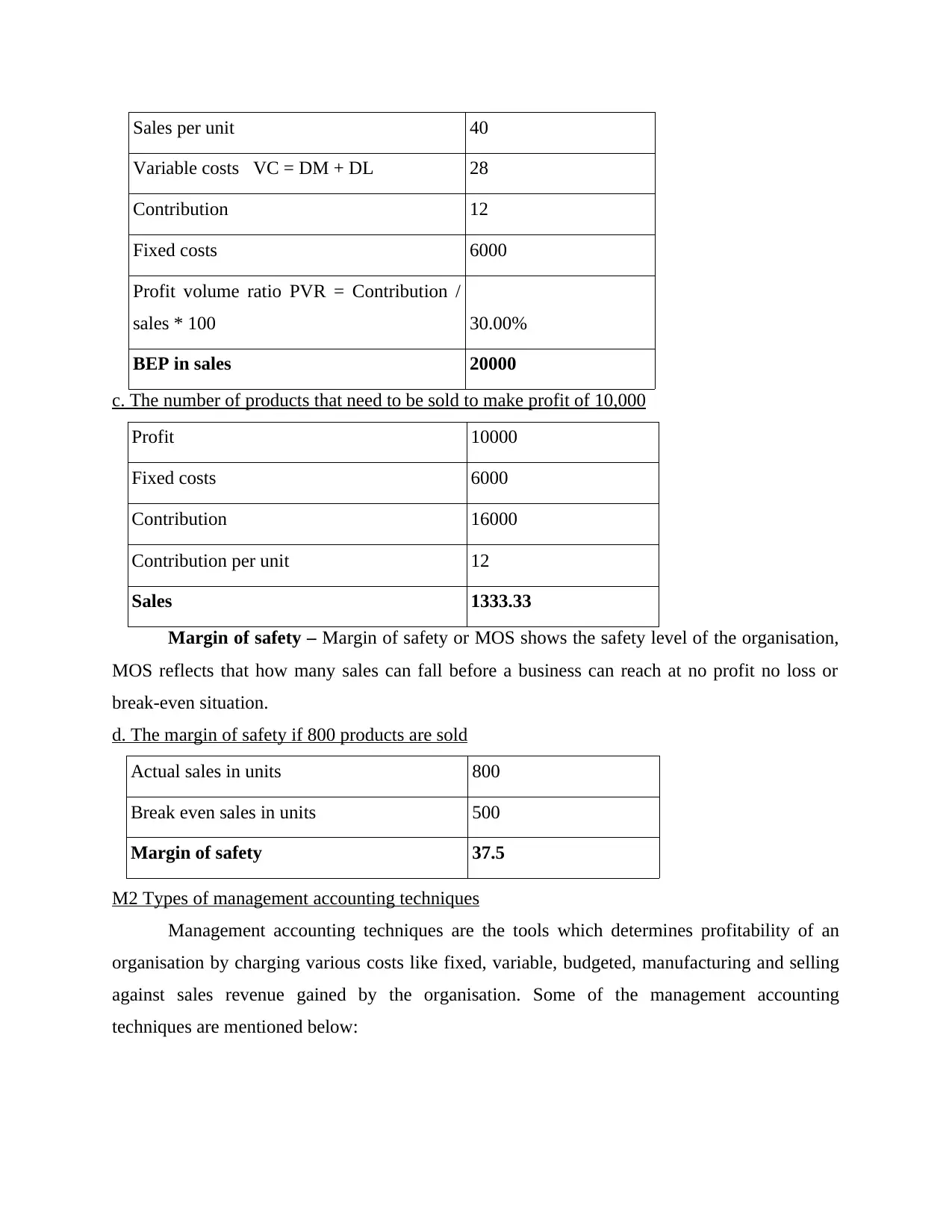

b. The breakeven point in terms of sales revenue

absorbs all costs either variable or fixed, and appropriate for financial and tax reporting (Otley,

2016).

Absorption costing is used by organisation to ascertain net income and ensures that all

costs are charged against sales revenues, profit in absorption costing is relatively less than profit

calculated by marginal costing. Formula of absorption costing is:

Sales revenue – cost of goods sold = gross profit – selling and administrative expenses =

Net profit and income

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales +

selling and administrative cost = 1 * 600 + 2700) 3300

Net profit/ operating income 15675

Break-Even – Breakeven point is the event in an organisation when there is no profit no

loss, when organisation is experiencing situations where all expenses and revenues are equal.

a. The number of products to be sold to break even

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

BEP in units 500

b. The breakeven point in terms of sales revenue

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

Profit volume ratio PVR = Contribution /

sales * 100 30.00%

BEP in sales 20000

c. The number of products that need to be sold to make profit of 10,000

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

Margin of safety – Margin of safety or MOS shows the safety level of the organisation,

MOS reflects that how many sales can fall before a business can reach at no profit no loss or

break-even situation.

d. The margin of safety if 800 products are sold

Actual sales in units 800

Break even sales in units 500

Margin of safety 37.5

M2 Types of management accounting techniques

Management accounting techniques are the tools which determines profitability of an

organisation by charging various costs like fixed, variable, budgeted, manufacturing and selling

against sales revenue gained by the organisation. Some of the management accounting

techniques are mentioned below:

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

Profit volume ratio PVR = Contribution /

sales * 100 30.00%

BEP in sales 20000

c. The number of products that need to be sold to make profit of 10,000

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

Margin of safety – Margin of safety or MOS shows the safety level of the organisation,

MOS reflects that how many sales can fall before a business can reach at no profit no loss or

break-even situation.

d. The margin of safety if 800 products are sold

Actual sales in units 800

Break even sales in units 500

Margin of safety 37.5

M2 Types of management accounting techniques

Management accounting techniques are the tools which determines profitability of an

organisation by charging various costs like fixed, variable, budgeted, manufacturing and selling

against sales revenue gained by the organisation. Some of the management accounting

techniques are mentioned below:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Standard costing – Standard costing is a process of estimating future profitability; all

pre-determined predicted costs are charged against estimated sales. This process of

determining net profit compares the budgeted or standard profits from actual outcomes.

Marginal costing – Marginal costing is an management accounting technique which

helps an organisation in determination of net incomes of an organisation by charging all

variable costs against sales revenue to ascertain amount contributed by an organisation

and then charging all fixed costs against that contributed amount to determine profits or

net incomes ( P. Tucker, B. 2014).

D2 Interpretation of data

Profit calculated under marginal costing that is 17500 is higher than the profit calculated

under absorption costing that is 15675, this difference is caused as marginal costing only

includes variable manufacturing costs, but absorption costing includes all manufacturing costs

either variable or fixed. Similarity contributed amount in marginal costing is higher than the

gross profit calculated from absorption costing.

From the data, it can be interpreted that if this organisation at least produces 500 units than it can

face situation of no loss no profit, margin of safety is calculated to identify the safety level of an

organisation, in this case margin of safety is 37.5.

TASK 3

P4 Advantages and disadvantages of various planning tools used for budgetary control

Budgetary control is a technique of management control which compares budgeted

estimates from actual outcomes, budgetary control involves preparation of various budgets like

sales budget, cash budget, fixed budget, flexible budget etc., which helps an organisation to

make profit.

Cash budget – Cash budget is the estimation of cash position of the organisation, where

all expenses are revenues are recorded which are likely to be incurred or gained in future( Ward,

2012).

Sales budget – Sales budget is the primary budget which is prepared before any budget

to estimate all future sales according to the demand and trend analyses of past few years.

Planning tools used in budgetary control are the techniques which are kept in mind while

preparation of any budget, these tools are forecasting, scenario and contingency tools which

pre-determined predicted costs are charged against estimated sales. This process of

determining net profit compares the budgeted or standard profits from actual outcomes.

Marginal costing – Marginal costing is an management accounting technique which

helps an organisation in determination of net incomes of an organisation by charging all

variable costs against sales revenue to ascertain amount contributed by an organisation

and then charging all fixed costs against that contributed amount to determine profits or

net incomes ( P. Tucker, B. 2014).

D2 Interpretation of data

Profit calculated under marginal costing that is 17500 is higher than the profit calculated

under absorption costing that is 15675, this difference is caused as marginal costing only

includes variable manufacturing costs, but absorption costing includes all manufacturing costs

either variable or fixed. Similarity contributed amount in marginal costing is higher than the

gross profit calculated from absorption costing.

From the data, it can be interpreted that if this organisation at least produces 500 units than it can

face situation of no loss no profit, margin of safety is calculated to identify the safety level of an

organisation, in this case margin of safety is 37.5.

TASK 3

P4 Advantages and disadvantages of various planning tools used for budgetary control

Budgetary control is a technique of management control which compares budgeted

estimates from actual outcomes, budgetary control involves preparation of various budgets like

sales budget, cash budget, fixed budget, flexible budget etc., which helps an organisation to

make profit.

Cash budget – Cash budget is the estimation of cash position of the organisation, where

all expenses are revenues are recorded which are likely to be incurred or gained in future( Ward,

2012).

Sales budget – Sales budget is the primary budget which is prepared before any budget

to estimate all future sales according to the demand and trend analyses of past few years.

Planning tools used in budgetary control are the techniques which are kept in mind while

preparation of any budget, these tools are forecasting, scenario and contingency tools which

helps an organisation to make more reliable and accurate budgets. Planning tools has its own

advantages and disadvantages which are listed below:

Forecasting - Forecasting is a planning tool that projects future events and conditions, it

helps management to ascertain the uncertainties of the future by considering past experiences

and trend analysis.

Advantages: Forecasting is the process of ascertaining future events which helps an

organisation to achieve their objective of customer satisfaction as they predict customers'

requirements and demands, forecasting also helps in reducing staffing costs by predicting

how many employees are needed to do a specific job.

Disadvantages: Forecasting is based on past events, which cannot give an accurate true

and fair projection of future events, forecasting involves trend analyses which is not a

proof or evidence of reliable projections (Van, 2011).

Contingency – Contingency is a planning tool which enables an organisation to be

prepared for future uncertainties and emergencies, contingency planning includes advance

decision making about the financial resources and inventory management. Contingency planning

includes answering the questions about what is going to happen, how management is going to

deal with it and what steps should be taken to deal with such emergencies.

Advantages: Contingency plan acts as a backup plan which is activated when there is

any emergency situations which reduces loss. Contingency plan activates when there is a

disaster situation and prevents panic of managers and helps in getting clear plan to

follow, it allows managers to focus on recovery instead of panicking. Contingency plan

includes steps for prevention which minimises the damages likely to occur in

emergencies.

Disadvantages: Contingency plan is a backup plan for future emergencies, but if none

of the emergency situations occur than all the money and resources used in preparation

of contingency plan is resultant to be wasted.

Scenario – Scenario is a planning tool where manager develops all possible scenarios

which may can occur in near future, this plan captures all possibilities by identifying trends and

possible uncertainties.

Advantages: Scenario is a planning tool which improves the quality of decision-making

process, due to scenario planning organisation can efficiently use available resources. It

advantages and disadvantages which are listed below:

Forecasting - Forecasting is a planning tool that projects future events and conditions, it

helps management to ascertain the uncertainties of the future by considering past experiences

and trend analysis.

Advantages: Forecasting is the process of ascertaining future events which helps an

organisation to achieve their objective of customer satisfaction as they predict customers'

requirements and demands, forecasting also helps in reducing staffing costs by predicting

how many employees are needed to do a specific job.

Disadvantages: Forecasting is based on past events, which cannot give an accurate true

and fair projection of future events, forecasting involves trend analyses which is not a

proof or evidence of reliable projections (Van, 2011).

Contingency – Contingency is a planning tool which enables an organisation to be

prepared for future uncertainties and emergencies, contingency planning includes advance

decision making about the financial resources and inventory management. Contingency planning

includes answering the questions about what is going to happen, how management is going to

deal with it and what steps should be taken to deal with such emergencies.

Advantages: Contingency plan acts as a backup plan which is activated when there is

any emergency situations which reduces loss. Contingency plan activates when there is a

disaster situation and prevents panic of managers and helps in getting clear plan to

follow, it allows managers to focus on recovery instead of panicking. Contingency plan

includes steps for prevention which minimises the damages likely to occur in

emergencies.

Disadvantages: Contingency plan is a backup plan for future emergencies, but if none

of the emergency situations occur than all the money and resources used in preparation

of contingency plan is resultant to be wasted.

Scenario – Scenario is a planning tool where manager develops all possible scenarios

which may can occur in near future, this plan captures all possibilities by identifying trends and

possible uncertainties.

Advantages: Scenario is a planning tool which improves the quality of decision-making

process, due to scenario planning organisation can efficiently use available resources. It

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.