Management Accounting Activities Report - HND Business (2020/2021)

VerifiedAdded on 2022/12/26

|10

|3254

|99

Report

AI Summary

This report delves into various aspects of management accounting, beginning with an introduction to the field and its significance in organizational decision-making. It explores different management accounting systems, including cost management, price optimization, inventory management, and job order costing. The report then examines management accounting reporting techniques, such as management reports, budget reports, and performance reports. It proceeds to demonstrate the preparation of income statements using marginal and absorption costing methods, as well as a cash flow statement. Furthermore, the report analyzes the advantages and limitations of various planning tools under budgetary control, including the balanced scorecard, variance analysis, responsibility accounting, and zero-base budgeting. Finally, it discusses how organizations utilize management accounting systems to address financial issues, such as benchmarking. The report aims to provide a comprehensive overview of management accounting principles and their practical applications within a business context.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Management accounting and essential requirement of various kinds of MA systems..........3

P2 Different techniques used in regard to management accounting reporting...........................4

TASK 2............................................................................................................................................4

P3 Preparation of income statements under cost analysis...........................................................4

TASK 3............................................................................................................................................6

P4 Advantages and limitations of various planning tools under budgetary control...................6

P5 Usage of management accounting systems by various organisations as well as their way of

responding to financial issues.....................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Management accounting and essential requirement of various kinds of MA systems..........3

P2 Different techniques used in regard to management accounting reporting...........................4

TASK 2............................................................................................................................................4

P3 Preparation of income statements under cost analysis...........................................................4

TASK 3............................................................................................................................................6

P4 Advantages and limitations of various planning tools under budgetary control...................6

P5 Usage of management accounting systems by various organisations as well as their way of

responding to financial issues.....................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION

Management accounting is said to be determination, analysis, evaluation of various

management data which actually helps managerial personnel to produce sound financial

decisions for ultimate organisational success. It is considerably significant branch of accounting

which provides assistance in decision-making in regard to an organisation. In this respective

study, various essential management accounting techniques will be discussed in detailed manner.

Significance of different financial reporting techniques will be considered in ultimate

organisational success. As well as correlation between management accounting and its respective

systems has also been analysed in order to identify organisational efficiency in operations. Also

with the use of different cost analysis techniques, income statements will be formulated for

identification of prevailing profits in an organisation.

TASK 1

P1 Management accounting and essential requirement of various kinds of MA systems

Management accounting is a vital technique which make use of scattered data into

systematic manner so that ultimate decisions can be provided. It includes both financial as well

as non financial data in form of quantitative and qualitative in order to help businesses to reach

their respective short term as well as long term goals. This form of accounting takes place by

management team to facilitate managers for better utilization of such data in reference to

organisational success (Krishnan, 2020).

Management accounting being a significant activity, includes various elements and

techniques which ultimately helpful for generation of efficient statements which will assist in

judgement for operations being going on for ultimate profitability. Various management

accounting system relevant features can be discussed as following:

Cost management accounting: In this system different costs occurring in operations of

an organisation are being managed in an appropriate manner so that maximum profits can be

generated through such practices. It also helps in data formulation by management specialist in

order to form adequate strategies which will provide basis of growth, market sustainability and

so on (Jiang, 2020). Therefore, cost management accounting is said to be effective for making

cost based decision through managers of an organisation. In this system maximum emphasis is

given to cost effectiveness which will help an organisation to generate maximum profits through

increased productivity and efficiency in operations of an organisation.

Price-optimization: In this approach various techniques such as market survey, customer

behaviour analysis, demographic information, operating expenditure, etc. has been evaluated in

order balance respective supply and demand of a product in an market. This procedure is adopted

in order to formulate dynamic pricing policies which will assist in reach practical demand of a

respective goods and services. It is said to be beneficial from company's as well as customer's

point of view as it satisfies both of their respective needs in the marketplace. It is used by various

large and medium sized organisations in order to identify respective position or demand of a

product in order to rectify errors if any for long term profitability.

Inventory management system: This is a procedure which helps in creating

transparency within inventory based activities through effective management of such operations.

Through this process stock of an organisation is managed in more effective manner without any

inherent errors or misconceptions in quality, quantity, etc. It benefits an organisation in a way

which reflects optimum system of inventory starting from initial form till its sale (Anshori,

2020). This system is very beneficial for organisations which has production based operations in

Management accounting is said to be determination, analysis, evaluation of various

management data which actually helps managerial personnel to produce sound financial

decisions for ultimate organisational success. It is considerably significant branch of accounting

which provides assistance in decision-making in regard to an organisation. In this respective

study, various essential management accounting techniques will be discussed in detailed manner.

Significance of different financial reporting techniques will be considered in ultimate

organisational success. As well as correlation between management accounting and its respective

systems has also been analysed in order to identify organisational efficiency in operations. Also

with the use of different cost analysis techniques, income statements will be formulated for

identification of prevailing profits in an organisation.

TASK 1

P1 Management accounting and essential requirement of various kinds of MA systems

Management accounting is a vital technique which make use of scattered data into

systematic manner so that ultimate decisions can be provided. It includes both financial as well

as non financial data in form of quantitative and qualitative in order to help businesses to reach

their respective short term as well as long term goals. This form of accounting takes place by

management team to facilitate managers for better utilization of such data in reference to

organisational success (Krishnan, 2020).

Management accounting being a significant activity, includes various elements and

techniques which ultimately helpful for generation of efficient statements which will assist in

judgement for operations being going on for ultimate profitability. Various management

accounting system relevant features can be discussed as following:

Cost management accounting: In this system different costs occurring in operations of

an organisation are being managed in an appropriate manner so that maximum profits can be

generated through such practices. It also helps in data formulation by management specialist in

order to form adequate strategies which will provide basis of growth, market sustainability and

so on (Jiang, 2020). Therefore, cost management accounting is said to be effective for making

cost based decision through managers of an organisation. In this system maximum emphasis is

given to cost effectiveness which will help an organisation to generate maximum profits through

increased productivity and efficiency in operations of an organisation.

Price-optimization: In this approach various techniques such as market survey, customer

behaviour analysis, demographic information, operating expenditure, etc. has been evaluated in

order balance respective supply and demand of a product in an market. This procedure is adopted

in order to formulate dynamic pricing policies which will assist in reach practical demand of a

respective goods and services. It is said to be beneficial from company's as well as customer's

point of view as it satisfies both of their respective needs in the marketplace. It is used by various

large and medium sized organisations in order to identify respective position or demand of a

product in order to rectify errors if any for long term profitability.

Inventory management system: This is a procedure which helps in creating

transparency within inventory based activities through effective management of such operations.

Through this process stock of an organisation is managed in more effective manner without any

inherent errors or misconceptions in quality, quantity, etc. It benefits an organisation in a way

which reflects optimum system of inventory starting from initial form till its sale (Anshori,

2020). This system is very beneficial for organisations which has production based operations in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

order to maintain effectiveness and efficiency in over all structure. This way more profits and

less wastages can be promoted for longer period.

Job order Costing: In this system, different costs are assembled in a specific batch or

order. This system is used when there are different kinds of goods being produced. Management

is required to keep separate record for each job cost including respective direct and indirect

costing. This is widely used by manufacturing units which are producing various products having

distinctions and similarities. Products having similarities will be kept under one job head so that

it would become easier to assign cost to each unit without any lower profit-margins in the long

term. Job costing is important task to be adopted by organisations in term of profitability and

sustainability by managing their costs in effective manner in the respective industry

(Suranatthakul and et. al., 2020).

P2 Different techniques used in regard to management accounting reporting

Management report: These reports are mainly used to make appropriate decisions,

identify progress as well as adhering to respective business goals in effective manner. The

adequate manner of management report preparation starts from setting particular goal or target

and also develop understanding of relevant results which are desirable. After target is being set,

it is required to identify key performance indicators which are perfect suitable for analysing

organisational performance in the long term. Also make valid comparisons of past and present

data for analysing relevant progress in company's overall performance. Through the use of charts

and graphs such data is being visualized to assist managers for appropriate decision-making.

Budget report: It is said to be respective cost and revenue of an organisation for a

relevant period. A budget report measures organisational objectives and also baseline for

measuring actual results from projected data. It also helps an organisation to keep up with the

changing circumstances in order to keep any sort of contingencies at future date (Tatake, 2020).

This technique is very beneficial for organisational growth by increasing productivity and profit-

margins over the period. It is presentation of expected expenditure in order to eliminate any kind

of unnecessary expenses from company's hand to increase overall profitability of an

organisation.

Performance report: This approach is used to identify actual performance of an

organisation with the use of appropriate strategies and policies. It is useful in various aspects like

to increase profit earning capacity of a company, to eliminate extra costing, to increase sales

volume and so on. Therefore, performance is a key factor which is responsible for growth of a

company by increasing performance levels for a long term performing organisations.

Performance is mainly analysed through comparisons of actual data from budgeted report so that

a conclusion can be formed in regard to rectification which are required to be made. Performance

is a basic requirement an organisation looks up to in order to increase its profit-margins and

sustainability in intense competition.

TASK 2

P3 Preparation of income statements under cost analysis

Income statement under marginal costing

Particulars Amount(£)

Total sales 2000000

less wastages can be promoted for longer period.

Job order Costing: In this system, different costs are assembled in a specific batch or

order. This system is used when there are different kinds of goods being produced. Management

is required to keep separate record for each job cost including respective direct and indirect

costing. This is widely used by manufacturing units which are producing various products having

distinctions and similarities. Products having similarities will be kept under one job head so that

it would become easier to assign cost to each unit without any lower profit-margins in the long

term. Job costing is important task to be adopted by organisations in term of profitability and

sustainability by managing their costs in effective manner in the respective industry

(Suranatthakul and et. al., 2020).

P2 Different techniques used in regard to management accounting reporting

Management report: These reports are mainly used to make appropriate decisions,

identify progress as well as adhering to respective business goals in effective manner. The

adequate manner of management report preparation starts from setting particular goal or target

and also develop understanding of relevant results which are desirable. After target is being set,

it is required to identify key performance indicators which are perfect suitable for analysing

organisational performance in the long term. Also make valid comparisons of past and present

data for analysing relevant progress in company's overall performance. Through the use of charts

and graphs such data is being visualized to assist managers for appropriate decision-making.

Budget report: It is said to be respective cost and revenue of an organisation for a

relevant period. A budget report measures organisational objectives and also baseline for

measuring actual results from projected data. It also helps an organisation to keep up with the

changing circumstances in order to keep any sort of contingencies at future date (Tatake, 2020).

This technique is very beneficial for organisational growth by increasing productivity and profit-

margins over the period. It is presentation of expected expenditure in order to eliminate any kind

of unnecessary expenses from company's hand to increase overall profitability of an

organisation.

Performance report: This approach is used to identify actual performance of an

organisation with the use of appropriate strategies and policies. It is useful in various aspects like

to increase profit earning capacity of a company, to eliminate extra costing, to increase sales

volume and so on. Therefore, performance is a key factor which is responsible for growth of a

company by increasing performance levels for a long term performing organisations.

Performance is mainly analysed through comparisons of actual data from budgeted report so that

a conclusion can be formed in regard to rectification which are required to be made. Performance

is a basic requirement an organisation looks up to in order to increase its profit-margins and

sustainability in intense competition.

TASK 2

P3 Preparation of income statements under cost analysis

Income statement under marginal costing

Particulars Amount(£)

Total sales 2000000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

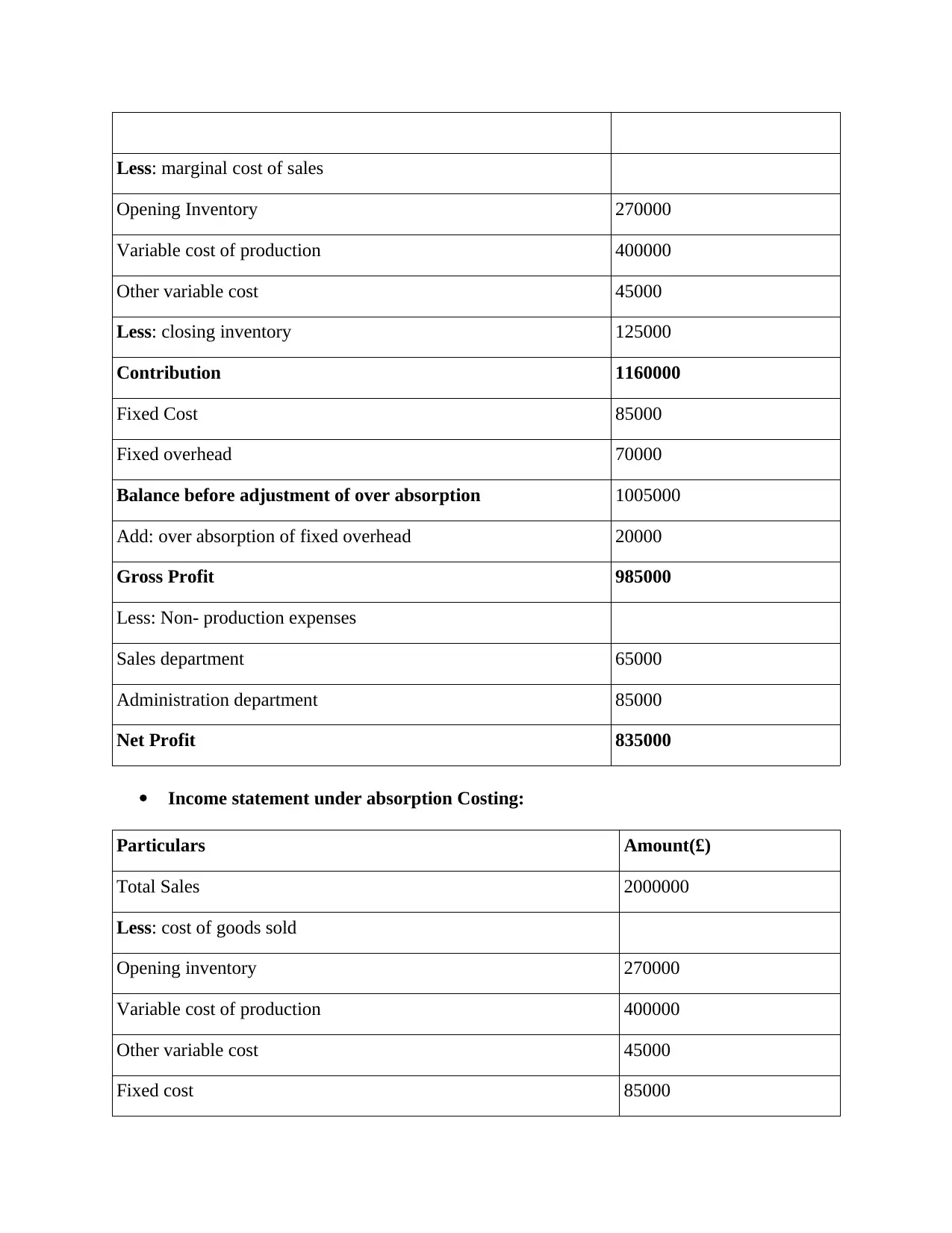

Less: marginal cost of sales

Opening Inventory 270000

Variable cost of production 400000

Other variable cost 45000

Less: closing inventory 125000

Contribution 1160000

Fixed Cost 85000

Fixed overhead 70000

Balance before adjustment of over absorption 1005000

Add: over absorption of fixed overhead 20000

Gross Profit 985000

Less: Non- production expenses

Sales department 65000

Administration department 85000

Net Profit 835000

Income statement under absorption Costing:

Particulars Amount(£)

Total Sales 2000000

Less: cost of goods sold

Opening inventory 270000

Variable cost of production 400000

Other variable cost 45000

Fixed cost 85000

Opening Inventory 270000

Variable cost of production 400000

Other variable cost 45000

Less: closing inventory 125000

Contribution 1160000

Fixed Cost 85000

Fixed overhead 70000

Balance before adjustment of over absorption 1005000

Add: over absorption of fixed overhead 20000

Gross Profit 985000

Less: Non- production expenses

Sales department 65000

Administration department 85000

Net Profit 835000

Income statement under absorption Costing:

Particulars Amount(£)

Total Sales 2000000

Less: cost of goods sold

Opening inventory 270000

Variable cost of production 400000

Other variable cost 45000

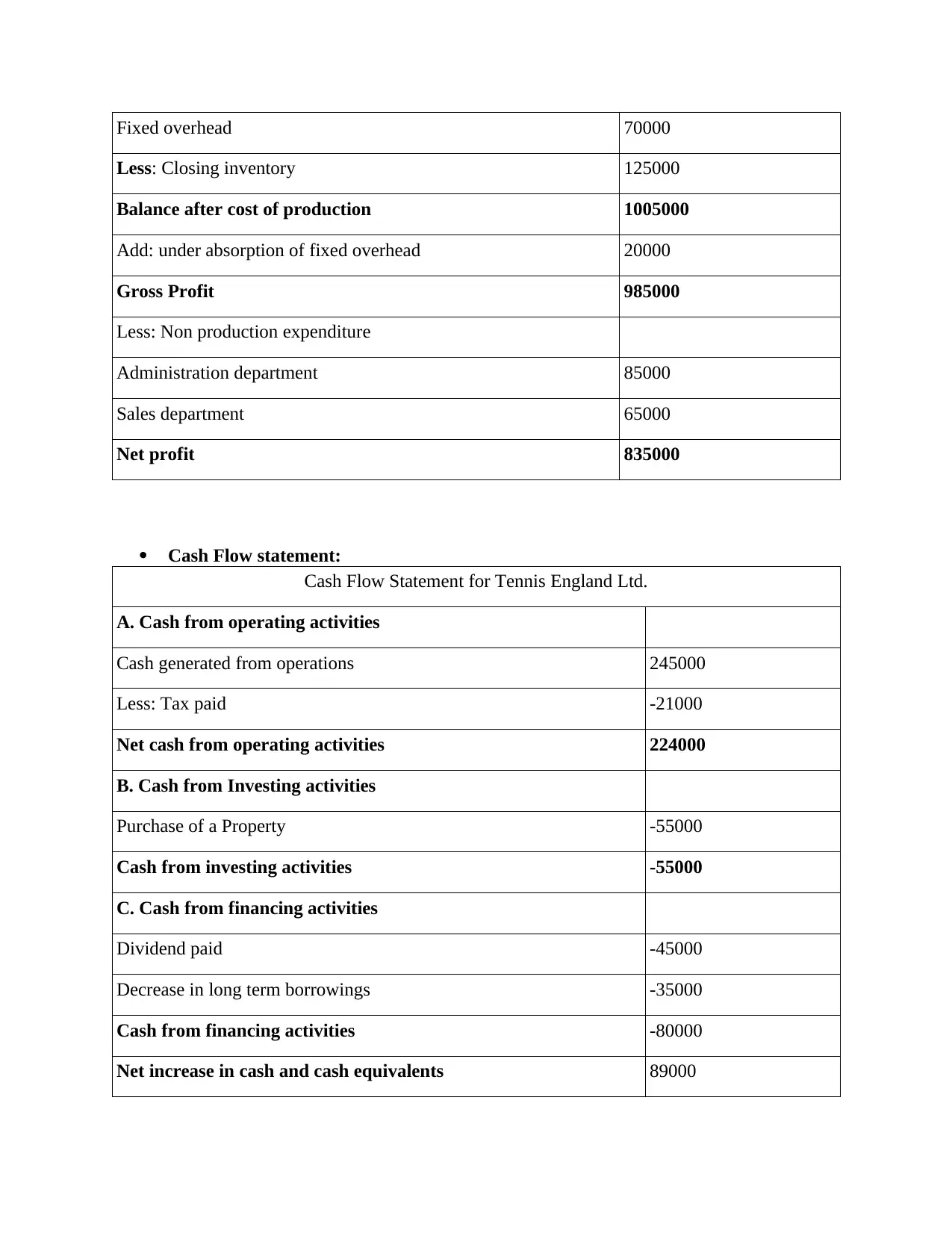

Fixed cost 85000

Fixed overhead 70000

Less: Closing inventory 125000

Balance after cost of production 1005000

Add: under absorption of fixed overhead 20000

Gross Profit 985000

Less: Non production expenditure

Administration department 85000

Sales department 65000

Net profit 835000

Cash Flow statement:

Cash Flow Statement for Tennis England Ltd.

A. Cash from operating activities

Cash generated from operations 245000

Less: Tax paid -21000

Net cash from operating activities 224000

B. Cash from Investing activities

Purchase of a Property -55000

Cash from investing activities -55000

C. Cash from financing activities

Dividend paid -45000

Decrease in long term borrowings -35000

Cash from financing activities -80000

Net increase in cash and cash equivalents 89000

Less: Closing inventory 125000

Balance after cost of production 1005000

Add: under absorption of fixed overhead 20000

Gross Profit 985000

Less: Non production expenditure

Administration department 85000

Sales department 65000

Net profit 835000

Cash Flow statement:

Cash Flow Statement for Tennis England Ltd.

A. Cash from operating activities

Cash generated from operations 245000

Less: Tax paid -21000

Net cash from operating activities 224000

B. Cash from Investing activities

Purchase of a Property -55000

Cash from investing activities -55000

C. Cash from financing activities

Dividend paid -45000

Decrease in long term borrowings -35000

Cash from financing activities -80000

Net increase in cash and cash equivalents 89000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 3

P4 Advantages and limitations of various planning tools under budgetary control

Balanced Scorecard: It is significant performance measurement technique which helps

in identification, rectification and controlling of a particular business functions in reference to the

resulting outcomes. This system helps in providing information of an organisational objectives

so that proper strategies can be implemented in order to rectify internal structures in order to

conclude optimum outcomes (Abou Taleb and Al Farooque, 2021).

Advantages: This technique of budgeting control provides adequate structure to policies which

needs to be implemented in an organisation as well as it eases to communicate a particular state

of mind with help of visual format. Also various departments and divisions of an organisations

works in a systematic manner by providing optimum results.

Disadvantages: It is gets complicated some times to make proper understanding of a data and at

times it goes in wrong direction as no focus has been provided to external forces such as

competitors which affects organisation as a whole.

Variance analysis: It is a method where difference between forecasted budgets and

actual figures is being assessed in order to each any kind of deviation in the performance of a

company. It is quantitative technique which reflect scope where corrective actions are taken in

reference to actual results in order to modify outcomes (Malik and et. al., 2021).

Advantages: It is considered as essential element of budgetary control which helps in

identification of deviations between actual and forecasted statements so that ultimate outcomes

can be achieved by the company.

Disadvantages: Respective disadvantage of such theory is that is requires lots of time to find out

any differences in such statements as it is complex process which needs to be followed in order

to identify such deviations.

Responsibility accounting: It includes preparation of budgets for ultimate responsible

centre. This system also considers preparation of various budgets in this regard. It also considers

relevant cost as well as revenue of an organisation. It maintains monthly, quarterly, weekly or

yearly reports which are used by superiors in order provide adequate report of further decisions.

Advantages: This is approach encourages organisational staff to reflect costs to their specified

responsibility centre so that actual accountable person will be held responsible for such act. Also

it is cost effective technique of an organisation where cost has been given ultimate preference

above other factors (Soriya and Rastogi, 2021).

Disadvantages: This systems requires adhering to the essentials of a successful responsibility

system which makes it difficult to comply with whole system by turning it into inaccurate

outcome.

Zero base Budgeting: It is a system where budget needs to be prepared from scratch in

order to promote more accuracy and reliability in forecasted expenditure. Proper justification

needs to be given for every expenditure being presented in the respective budget on the expenses

of an organisational activities. This method is said to be very important in modern terms. It is

now used by mostly of the companies in order produce more specific and accurate budgets.

Advantages: This system is developed over cost benefit analysis which is estimated through

formulation of accurate formulas. This method mostly prioritize allocation efficiency of certain

resources in order to generate maximum return over investments.

P4 Advantages and limitations of various planning tools under budgetary control

Balanced Scorecard: It is significant performance measurement technique which helps

in identification, rectification and controlling of a particular business functions in reference to the

resulting outcomes. This system helps in providing information of an organisational objectives

so that proper strategies can be implemented in order to rectify internal structures in order to

conclude optimum outcomes (Abou Taleb and Al Farooque, 2021).

Advantages: This technique of budgeting control provides adequate structure to policies which

needs to be implemented in an organisation as well as it eases to communicate a particular state

of mind with help of visual format. Also various departments and divisions of an organisations

works in a systematic manner by providing optimum results.

Disadvantages: It is gets complicated some times to make proper understanding of a data and at

times it goes in wrong direction as no focus has been provided to external forces such as

competitors which affects organisation as a whole.

Variance analysis: It is a method where difference between forecasted budgets and

actual figures is being assessed in order to each any kind of deviation in the performance of a

company. It is quantitative technique which reflect scope where corrective actions are taken in

reference to actual results in order to modify outcomes (Malik and et. al., 2021).

Advantages: It is considered as essential element of budgetary control which helps in

identification of deviations between actual and forecasted statements so that ultimate outcomes

can be achieved by the company.

Disadvantages: Respective disadvantage of such theory is that is requires lots of time to find out

any differences in such statements as it is complex process which needs to be followed in order

to identify such deviations.

Responsibility accounting: It includes preparation of budgets for ultimate responsible

centre. This system also considers preparation of various budgets in this regard. It also considers

relevant cost as well as revenue of an organisation. It maintains monthly, quarterly, weekly or

yearly reports which are used by superiors in order provide adequate report of further decisions.

Advantages: This is approach encourages organisational staff to reflect costs to their specified

responsibility centre so that actual accountable person will be held responsible for such act. Also

it is cost effective technique of an organisation where cost has been given ultimate preference

above other factors (Soriya and Rastogi, 2021).

Disadvantages: This systems requires adhering to the essentials of a successful responsibility

system which makes it difficult to comply with whole system by turning it into inaccurate

outcome.

Zero base Budgeting: It is a system where budget needs to be prepared from scratch in

order to promote more accuracy and reliability in forecasted expenditure. Proper justification

needs to be given for every expenditure being presented in the respective budget on the expenses

of an organisational activities. This method is said to be very important in modern terms. It is

now used by mostly of the companies in order produce more specific and accurate budgets.

Advantages: This system is developed over cost benefit analysis which is estimated through

formulation of accurate formulas. This method mostly prioritize allocation efficiency of certain

resources in order to generate maximum return over investments.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Disadvantages: It is considerably much expensive system with lots of complexities which makes

it less approachable technique by the companies in order to advance their profit-margins in the

long term (Bhaskar and Flower, 2021).

TASK 4

P5 Usage of management accounting systems by various organisations as well as their way of

responding to financial issues

There are situations when organisation face extreme financial issues which needs to be

sorted out through use of effective management accounting techniques. Such methods are helpful

in utilisation of companies resources in much effective manner by reflecting adequate

profitability in the long term. These problem solving techniques can be discussed as follows:

Benchmarking: This is a technique used by organisation in order to use standard to

promote systematic follow of operations in an organisation. Through this approach more

adequate and effective results can be drawn. Tennis England Ltd. Has been using such approach

in order to modify its operations in respect to prevailing competitions in the relevant industry. It

is one of the most effective tool which is less time consuming, more cost effective and promotes

reliability of activities which will ultimately increase organisational productivity (Balios, 2021).

KPIs: Also known as Key performance indicators is a technique used to identify the

performance of an organisation in regard to its operations. This technique is widely used by

companies in order to improvise performance by applying such method in order to determine

organisational growth and efficiency in the long term (Asiri, Khan and Kend, 2020). This

method helps measure an organisational success in respect of its current operations. It is

considered as most reliable approach which shows whether an organisation can achieve ultimate

or forecasted success or need to make more improvisations.

Balanced Scorecard: It is said to be performance measurement tool which is mainly

used by managerial team in order to keep track of its respective operations being executed by

management within their controlling scope as well as monitor various consequences coming up

from such actions. It is widely used by organisation in order to facilitate managers in decision-

making which will help it in future for long term sustainability. This strategy is aimed at

managing operating activities on an organisation which needs to be performed in balanced

manner so that maximum profits can be drawn (Kajüter and Schröder, 2017).

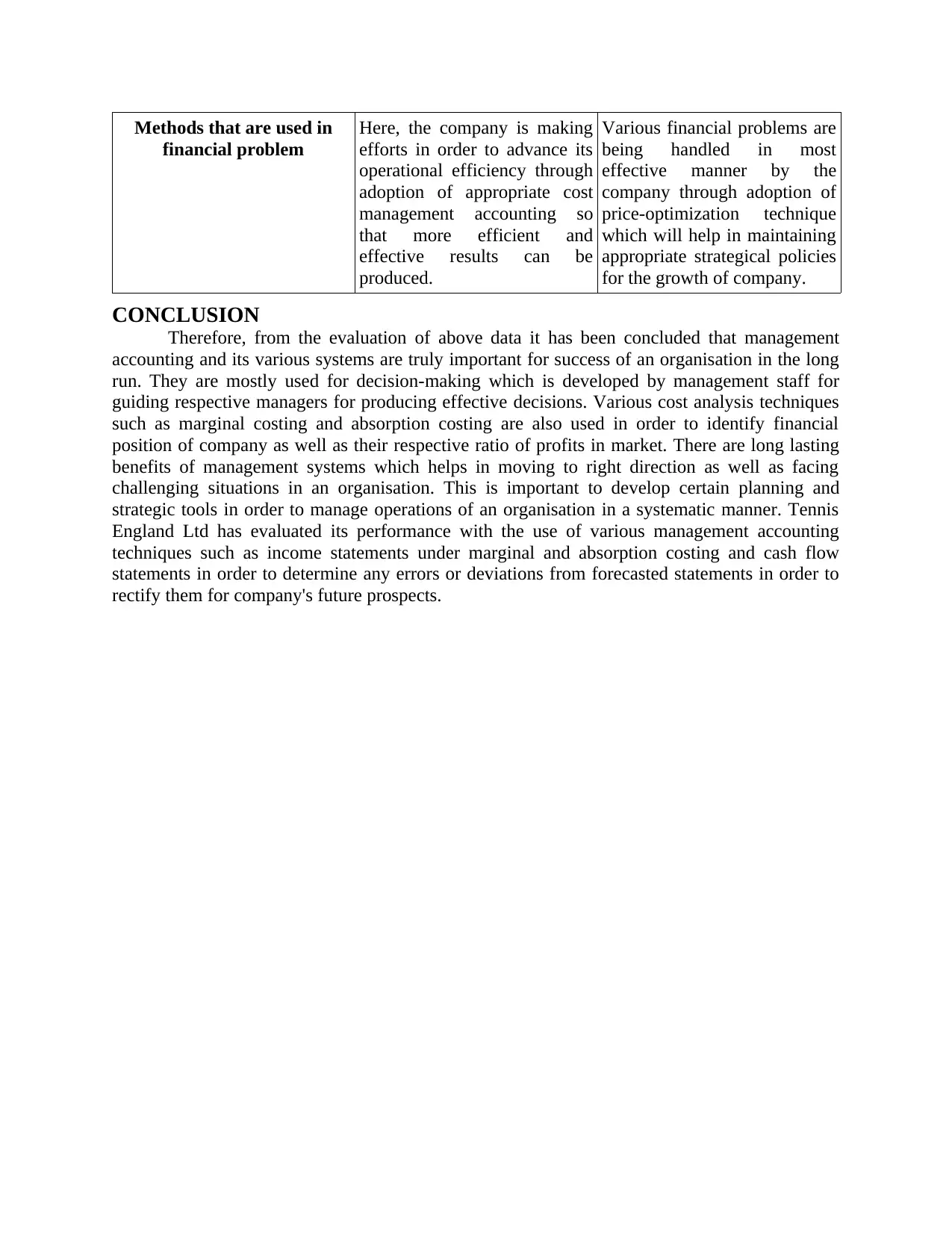

Basis of Comparison Tennis England Ltd. Northern Vision

Financial Problem The company has been lacking

in cash inflows which could be

a problem for such

organisation to survive in the

long term.

Here financial issue is relevant

to mismanagement of cost

which is making difficult for

the company to advance its

profit-margins.

Approach adopted The above company is focused

over benchmarking system in

order to promote maximum

level of stability in its

operations which will be

beneficial in long term aspects.

Northern vision is emphasising

over Key performance

indicators(KPIs) which helps

to increase efficiency of an

organisation which will

ultimately results in

modification in profitability.

it less approachable technique by the companies in order to advance their profit-margins in the

long term (Bhaskar and Flower, 2021).

TASK 4

P5 Usage of management accounting systems by various organisations as well as their way of

responding to financial issues

There are situations when organisation face extreme financial issues which needs to be

sorted out through use of effective management accounting techniques. Such methods are helpful

in utilisation of companies resources in much effective manner by reflecting adequate

profitability in the long term. These problem solving techniques can be discussed as follows:

Benchmarking: This is a technique used by organisation in order to use standard to

promote systematic follow of operations in an organisation. Through this approach more

adequate and effective results can be drawn. Tennis England Ltd. Has been using such approach

in order to modify its operations in respect to prevailing competitions in the relevant industry. It

is one of the most effective tool which is less time consuming, more cost effective and promotes

reliability of activities which will ultimately increase organisational productivity (Balios, 2021).

KPIs: Also known as Key performance indicators is a technique used to identify the

performance of an organisation in regard to its operations. This technique is widely used by

companies in order to improvise performance by applying such method in order to determine

organisational growth and efficiency in the long term (Asiri, Khan and Kend, 2020). This

method helps measure an organisational success in respect of its current operations. It is

considered as most reliable approach which shows whether an organisation can achieve ultimate

or forecasted success or need to make more improvisations.

Balanced Scorecard: It is said to be performance measurement tool which is mainly

used by managerial team in order to keep track of its respective operations being executed by

management within their controlling scope as well as monitor various consequences coming up

from such actions. It is widely used by organisation in order to facilitate managers in decision-

making which will help it in future for long term sustainability. This strategy is aimed at

managing operating activities on an organisation which needs to be performed in balanced

manner so that maximum profits can be drawn (Kajüter and Schröder, 2017).

Basis of Comparison Tennis England Ltd. Northern Vision

Financial Problem The company has been lacking

in cash inflows which could be

a problem for such

organisation to survive in the

long term.

Here financial issue is relevant

to mismanagement of cost

which is making difficult for

the company to advance its

profit-margins.

Approach adopted The above company is focused

over benchmarking system in

order to promote maximum

level of stability in its

operations which will be

beneficial in long term aspects.

Northern vision is emphasising

over Key performance

indicators(KPIs) which helps

to increase efficiency of an

organisation which will

ultimately results in

modification in profitability.

Methods that are used in

financial problem

Here, the company is making

efforts in order to advance its

operational efficiency through

adoption of appropriate cost

management accounting so

that more efficient and

effective results can be

produced.

Various financial problems are

being handled in most

effective manner by the

company through adoption of

price-optimization technique

which will help in maintaining

appropriate strategical policies

for the growth of company.

CONCLUSION

Therefore, from the evaluation of above data it has been concluded that management

accounting and its various systems are truly important for success of an organisation in the long

run. They are mostly used for decision-making which is developed by management staff for

guiding respective managers for producing effective decisions. Various cost analysis techniques

such as marginal costing and absorption costing are also used in order to identify financial

position of company as well as their respective ratio of profits in market. There are long lasting

benefits of management systems which helps in moving to right direction as well as facing

challenging situations in an organisation. This is important to develop certain planning and

strategic tools in order to manage operations of an organisation in a systematic manner. Tennis

England Ltd has evaluated its performance with the use of various management accounting

techniques such as income statements under marginal and absorption costing and cash flow

statements in order to determine any errors or deviations from forecasted statements in order to

rectify them for company's future prospects.

financial problem

Here, the company is making

efforts in order to advance its

operational efficiency through

adoption of appropriate cost

management accounting so

that more efficient and

effective results can be

produced.

Various financial problems are

being handled in most

effective manner by the

company through adoption of

price-optimization technique

which will help in maintaining

appropriate strategical policies

for the growth of company.

CONCLUSION

Therefore, from the evaluation of above data it has been concluded that management

accounting and its various systems are truly important for success of an organisation in the long

run. They are mostly used for decision-making which is developed by management staff for

guiding respective managers for producing effective decisions. Various cost analysis techniques

such as marginal costing and absorption costing are also used in order to identify financial

position of company as well as their respective ratio of profits in market. There are long lasting

benefits of management systems which helps in moving to right direction as well as facing

challenging situations in an organisation. This is important to develop certain planning and

strategic tools in order to manage operations of an organisation in a systematic manner. Tennis

England Ltd has evaluated its performance with the use of various management accounting

techniques such as income statements under marginal and absorption costing and cash flow

statements in order to determine any errors or deviations from forecasted statements in order to

rectify them for company's future prospects.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and journals

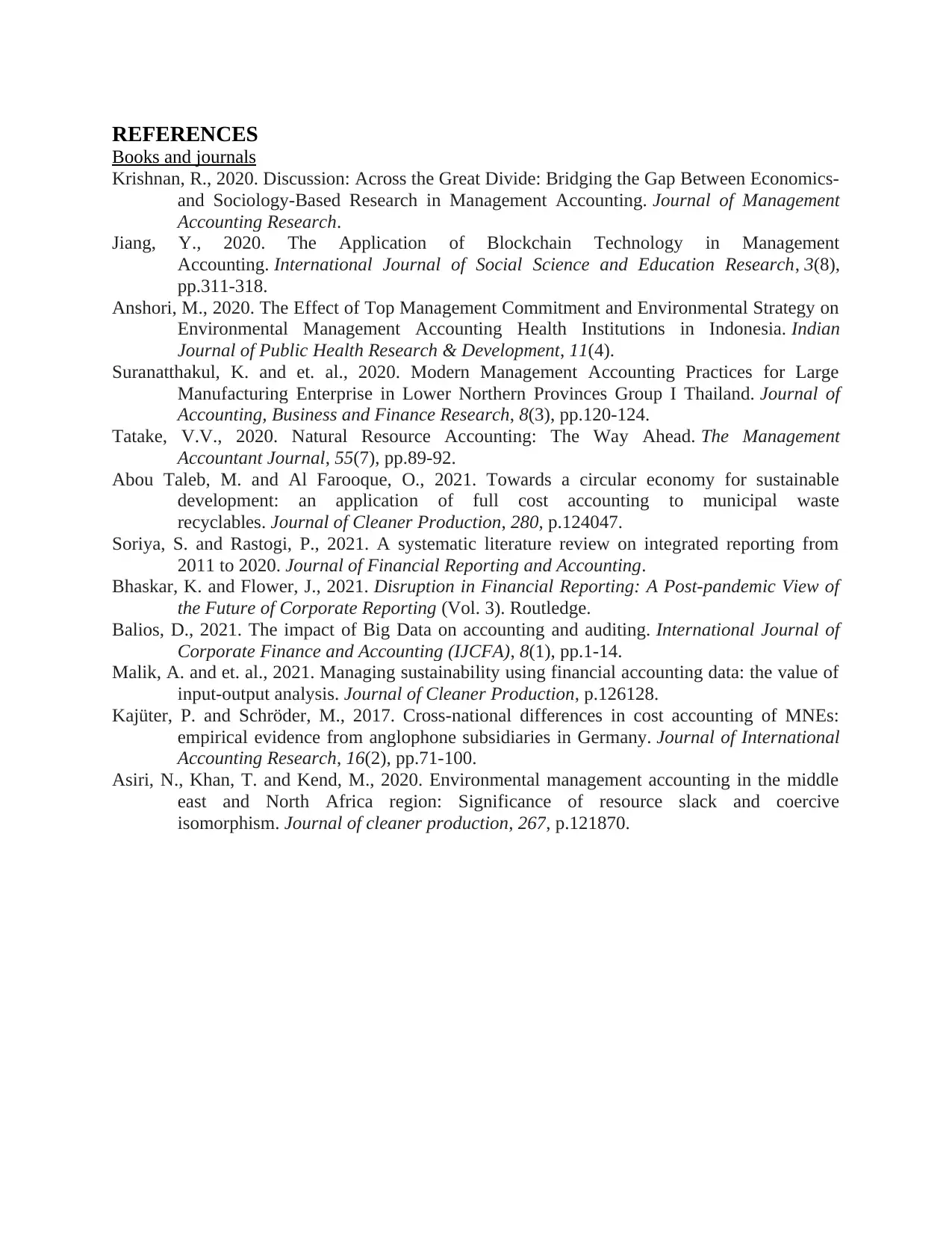

Krishnan, R., 2020. Discussion: Across the Great Divide: Bridging the Gap Between Economics-

and Sociology-Based Research in Management Accounting. Journal of Management

Accounting Research.

Jiang, Y., 2020. The Application of Blockchain Technology in Management

Accounting. International Journal of Social Science and Education Research, 3(8),

pp.311-318.

Anshori, M., 2020. The Effect of Top Management Commitment and Environmental Strategy on

Environmental Management Accounting Health Institutions in Indonesia. Indian

Journal of Public Health Research & Development, 11(4).

Suranatthakul, K. and et. al., 2020. Modern Management Accounting Practices for Large

Manufacturing Enterprise in Lower Northern Provinces Group I Thailand. Journal of

Accounting, Business and Finance Research, 8(3), pp.120-124.

Tatake, V.V., 2020. Natural Resource Accounting: The Way Ahead. The Management

Accountant Journal, 55(7), pp.89-92.

Abou Taleb, M. and Al Farooque, O., 2021. Towards a circular economy for sustainable

development: an application of full cost accounting to municipal waste

recyclables. Journal of Cleaner Production, 280, p.124047.

Soriya, S. and Rastogi, P., 2021. A systematic literature review on integrated reporting from

2011 to 2020. Journal of Financial Reporting and Accounting.

Bhaskar, K. and Flower, J., 2021. Disruption in Financial Reporting: A Post-pandemic View of

the Future of Corporate Reporting (Vol. 3). Routledge.

Balios, D., 2021. The impact of Big Data on accounting and auditing. International Journal of

Corporate Finance and Accounting (IJCFA), 8(1), pp.1-14.

Malik, A. and et. al., 2021. Managing sustainability using financial accounting data: the value of

input-output analysis. Journal of Cleaner Production, p.126128.

Kajüter, P. and Schröder, M., 2017. Cross-national differences in cost accounting of MNEs:

empirical evidence from anglophone subsidiaries in Germany. Journal of International

Accounting Research, 16(2), pp.71-100.

Asiri, N., Khan, T. and Kend, M., 2020. Environmental management accounting in the middle

east and North Africa region: Significance of resource slack and coercive

isomorphism. Journal of cleaner production, 267, p.121870.

Books and journals

Krishnan, R., 2020. Discussion: Across the Great Divide: Bridging the Gap Between Economics-

and Sociology-Based Research in Management Accounting. Journal of Management

Accounting Research.

Jiang, Y., 2020. The Application of Blockchain Technology in Management

Accounting. International Journal of Social Science and Education Research, 3(8),

pp.311-318.

Anshori, M., 2020. The Effect of Top Management Commitment and Environmental Strategy on

Environmental Management Accounting Health Institutions in Indonesia. Indian

Journal of Public Health Research & Development, 11(4).

Suranatthakul, K. and et. al., 2020. Modern Management Accounting Practices for Large

Manufacturing Enterprise in Lower Northern Provinces Group I Thailand. Journal of

Accounting, Business and Finance Research, 8(3), pp.120-124.

Tatake, V.V., 2020. Natural Resource Accounting: The Way Ahead. The Management

Accountant Journal, 55(7), pp.89-92.

Abou Taleb, M. and Al Farooque, O., 2021. Towards a circular economy for sustainable

development: an application of full cost accounting to municipal waste

recyclables. Journal of Cleaner Production, 280, p.124047.

Soriya, S. and Rastogi, P., 2021. A systematic literature review on integrated reporting from

2011 to 2020. Journal of Financial Reporting and Accounting.

Bhaskar, K. and Flower, J., 2021. Disruption in Financial Reporting: A Post-pandemic View of

the Future of Corporate Reporting (Vol. 3). Routledge.

Balios, D., 2021. The impact of Big Data on accounting and auditing. International Journal of

Corporate Finance and Accounting (IJCFA), 8(1), pp.1-14.

Malik, A. and et. al., 2021. Managing sustainability using financial accounting data: the value of

input-output analysis. Journal of Cleaner Production, p.126128.

Kajüter, P. and Schröder, M., 2017. Cross-national differences in cost accounting of MNEs:

empirical evidence from anglophone subsidiaries in Germany. Journal of International

Accounting Research, 16(2), pp.71-100.

Asiri, N., Khan, T. and Kend, M., 2020. Environmental management accounting in the middle

east and North Africa region: Significance of resource slack and coercive

isomorphism. Journal of cleaner production, 267, p.121870.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.