Comprehensive Management Accounting Report: ABC Ltd Financial Analysis

VerifiedAdded on 2023/01/05

|16

|4734

|88

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and their application within ABC Ltd, a manufacturing business. It begins with an introduction to management accounting, its systems, and essential requirements, including inventory management, cost accounting, and price optimization. The report then delves into various reporting methods, such as account receivable and performance reports, and evaluates the benefits of these systems within the organization. Task 2 focuses on costing methods, calculating production costs using both marginal and absorption costing techniques, and producing budgeted profit and loss statements. The report also examines planning tools, including their advantages and disadvantages, and their role in budgeting and forecasting. Finally, it explores how organizations adapt management accounting systems to address financial problems and achieve sustainable success, evaluating the role of planning tools in solving financial issues.

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1. Explanation of management accounting and essential requirements of its systems...............1

2. Different methods that are used for management accounting reporting..................................2

3. Evaluation of benefits of management accounting systems and their application within the

organisation..................................................................................................................................3

4. Critical evaluation of the way in which different systems and reports of management

accounting reports are integrated with organisational processes.................................................3

TASK 2............................................................................................................................................4

1. Calculation of production cost per unit, total production cost and total cost of sales for

January.........................................................................................................................................4

2. Application of techniques and production of budgeted profit and loss statement for January7

TASK 3............................................................................................................................................7

1. Explanation of different planning tools along with their advantages and disadvantages........7

2. Analyse the use of different planning tools and their applications for preparing and

forecasting budgets......................................................................................................................9

TASK 4............................................................................................................................................9

Compare how organisations are adapting management accounting systems to respond to

financial problems.......................................................................................................................9

Analyse how, in responding to financial problems, management accounting can lead

organisations to sustainable success..........................................................................................11

Evaluate how planning tools for management accounting respond appropriately for solving

financial problems to lead organisations to sustainable success...............................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1. Explanation of management accounting and essential requirements of its systems...............1

2. Different methods that are used for management accounting reporting..................................2

3. Evaluation of benefits of management accounting systems and their application within the

organisation..................................................................................................................................3

4. Critical evaluation of the way in which different systems and reports of management

accounting reports are integrated with organisational processes.................................................3

TASK 2............................................................................................................................................4

1. Calculation of production cost per unit, total production cost and total cost of sales for

January.........................................................................................................................................4

2. Application of techniques and production of budgeted profit and loss statement for January7

TASK 3............................................................................................................................................7

1. Explanation of different planning tools along with their advantages and disadvantages........7

2. Analyse the use of different planning tools and their applications for preparing and

forecasting budgets......................................................................................................................9

TASK 4............................................................................................................................................9

Compare how organisations are adapting management accounting systems to respond to

financial problems.......................................................................................................................9

Analyse how, in responding to financial problems, management accounting can lead

organisations to sustainable success..........................................................................................11

Evaluate how planning tools for management accounting respond appropriately for solving

financial problems to lead organisations to sustainable success...............................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Management accounting is a technique which is used in businesses for assessing business

performance with the help of internal reports. If the managers will not be able to generate them

in systematic manner, then it may result in unattained objectives of business. For all the

managers it is very important to be focused with it as it can help them to reach to long as well as

short term business goals as it facilitates the process of strategy formulation (Alsharari and

Abougamos, 2017). While planning to improve organisational performance it is very important

for all the managers to make sure that they are focused with it. Present report is based upon ABC

Ltd which is operating business under manufacturing industry and it is a medium sized entity.

This report covers various topics that includes management accounting, its systems, approaches

and techniques. Apart from this, different types of planning tools along with the way in which

businesses can use management accounting to respond financial problems are also discussed in

this report.

TASK 1

1. Explanation of management accounting and essential requirements of its systems

Management accounting could be defined as the technique which is used by businesses

for the purpose of generating internal reports and determine performance of the company. It is

very important for the businesses to make sure that they are focused with use of it as it will help

the management teams to make sure that they are formulating effective strategies. ABC Ltd

which is a medium sized enterprise also uses it as it helps the internal stakeholders to get aware

of actual situation of business. There are various types of management accounting systems that

are used within the organisation. Discussion of all of them is as follows:

Inventory management system: It is used by businesses for keeping track record of the

inventory which is used for carrying out operational activities in systematic manner. In ABC it is

used by managers for assuring that it is having sufficient goods to perform the manufacturing

activities of business. It is essentially required for the entity as by using it the management of the

company will be aware of that they are having enough inventory or not (Atmoko and Hapsoro,

2017).

Cost accounting system: It is a system which is used by businesses for the purpose of

analysing costs of all the items that are produced within the year. In ABC Ltd it is used for the

1

Management accounting is a technique which is used in businesses for assessing business

performance with the help of internal reports. If the managers will not be able to generate them

in systematic manner, then it may result in unattained objectives of business. For all the

managers it is very important to be focused with it as it can help them to reach to long as well as

short term business goals as it facilitates the process of strategy formulation (Alsharari and

Abougamos, 2017). While planning to improve organisational performance it is very important

for all the managers to make sure that they are focused with it. Present report is based upon ABC

Ltd which is operating business under manufacturing industry and it is a medium sized entity.

This report covers various topics that includes management accounting, its systems, approaches

and techniques. Apart from this, different types of planning tools along with the way in which

businesses can use management accounting to respond financial problems are also discussed in

this report.

TASK 1

1. Explanation of management accounting and essential requirements of its systems

Management accounting could be defined as the technique which is used by businesses

for the purpose of generating internal reports and determine performance of the company. It is

very important for the businesses to make sure that they are focused with use of it as it will help

the management teams to make sure that they are formulating effective strategies. ABC Ltd

which is a medium sized enterprise also uses it as it helps the internal stakeholders to get aware

of actual situation of business. There are various types of management accounting systems that

are used within the organisation. Discussion of all of them is as follows:

Inventory management system: It is used by businesses for keeping track record of the

inventory which is used for carrying out operational activities in systematic manner. In ABC it is

used by managers for assuring that it is having sufficient goods to perform the manufacturing

activities of business. It is essentially required for the entity as by using it the management of the

company will be aware of that they are having enough inventory or not (Atmoko and Hapsoro,

2017).

Cost accounting system: It is a system which is used by businesses for the purpose of

analysing costs of all the items that are produced within the year. In ABC Ltd it is used for the

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

purpose of making sure that it gets details of all the manufacturing related costs so that funds

could be arranged according to them. The essential requirement of it for the organisation is that it

facilitate the business to get information of the cost which may take place in future (Baños

Sánchez-Matamoros, 2020).

Price optimisation system: Under this type of system optimum price for all the products

that are sold by the entities are analysed so that the satisfaction level of all the customers could

be met. The managers in ABC are using it for setting appropriate price for all the items that are

manufactured by it so that it can attract large number of customers. The main requirement of it

for the business is that it can help to determine the best suitable price for the products that can

met expectation level of clients.

Job costing system: It is used by businesses for the purpose of analysing the cost of each

and every job which is performed for the purpose of meeting expectations of clients. In ABC Ltd

it is used by managers for making sure that they keep record of all the jobs that are performed on

the basis of specifications of clients. The main requirement of it for the business is that it can

help the managers to analyse cost of each job which is performed by the entity separately (Boyd

and Pitre, 2020).

2. Different methods that are used for management accounting reporting

Management accounting reporting is the process of recording internal information in

different reports so that the internal stakeholders can determine the position of business. In ABC

Ltd the managers are paying attention towards it as it can help to generate detailed reports for the

organisation. There are various reports that are generated by the organisation which are described

below:

Account receivable report: It is used by businesses for recording information of the

payment which is due by customers. In ABC Ltd it is used for the purpose of analysing total

outstanding amount which will be recovered from the customers in future. It is beneficial for

managers as it can help them to determine actual owed amount by the debtors (Daniyar and

Ruzanov, 2019).

Performance report: This report is used in businesses to record information of

performance of employees and business so that strategic decisions for future could be

formulated. In ABC Ltd it is used by the managers to analyse that business is able to meet the

desired level of success or not. The main benefit of it for the entity is that it can help to

2

could be arranged according to them. The essential requirement of it for the organisation is that it

facilitate the business to get information of the cost which may take place in future (Baños

Sánchez-Matamoros, 2020).

Price optimisation system: Under this type of system optimum price for all the products

that are sold by the entities are analysed so that the satisfaction level of all the customers could

be met. The managers in ABC are using it for setting appropriate price for all the items that are

manufactured by it so that it can attract large number of customers. The main requirement of it

for the business is that it can help to determine the best suitable price for the products that can

met expectation level of clients.

Job costing system: It is used by businesses for the purpose of analysing the cost of each

and every job which is performed for the purpose of meeting expectations of clients. In ABC Ltd

it is used by managers for making sure that they keep record of all the jobs that are performed on

the basis of specifications of clients. The main requirement of it for the business is that it can

help the managers to analyse cost of each job which is performed by the entity separately (Boyd

and Pitre, 2020).

2. Different methods that are used for management accounting reporting

Management accounting reporting is the process of recording internal information in

different reports so that the internal stakeholders can determine the position of business. In ABC

Ltd the managers are paying attention towards it as it can help to generate detailed reports for the

organisation. There are various reports that are generated by the organisation which are described

below:

Account receivable report: It is used by businesses for recording information of the

payment which is due by customers. In ABC Ltd it is used for the purpose of analysing total

outstanding amount which will be recovered from the customers in future. It is beneficial for

managers as it can help them to determine actual owed amount by the debtors (Daniyar and

Ruzanov, 2019).

Performance report: This report is used in businesses to record information of

performance of employees and business so that strategic decisions for future could be

formulated. In ABC Ltd it is used by the managers to analyse that business is able to meet the

desired level of success or not. The main benefit of it for the entity is that it can help to

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

determine that the employees are performing appropriately so that bonus could be offered to

them accordingly.

Budget report: It is used in businesses for assigning funding to all the operations for the

purpose of proper execution of all of them. With the help of it, managers in ABC try to analyse

that the managers are assigning sufficient funds to all the departments according to their

requirements or not. It is beneficial for the enterprises because with the help of it the companies

will be able to perform operational activities in monetary resources that are assigned to them.

3. Evaluation of benefits of management accounting systems and their application within the

organisation

There are various types management accounting systems that are used by the managers of

ABC Ltd. Discussion of benefits of them along with application are discussed below:

Inventory management system: It is used in ABC Ltd by the managers for making sure

that they have detailed information of the inventory which is used for performing operations as it

is beneficial for execution of all the activities systematically (Datar and Rajan, 2018).

Cost accounting system: In ABC Ltd it is used by management team because it is

beneficial in determining cost of each and every activity performed by the enterprise.

Price optimisation system: Managers of ABC Ltd are using it for assuring that best

suitable price for all the products are determined as it is beneficial for meeting expectations of

customers.

Job order costing system: It is applied in ABC Ltd because it facilitates managers to

analyse cost of each and every job performed according to specifications of customers.

4. Critical evaluation of the way in which different systems and reports of management

accounting reports are integrated with organisational processes

In ABC Ltd the managers are using different types of management accounting reports and

systems. All of them are integrated with organisations processes. For example, inventory

management system is used by the managers for analysing that the entity is able to keep

sufficient goods for performing all the operations in systematic manner. On the other hand,

account receivable system is used for analysing the owed amount of different customers. For

example, if the managers of the organisation will not be able to analyse actual outstanding

amount then this report could be used by them to determine it (Feng and Ho, 2016).

3

them accordingly.

Budget report: It is used in businesses for assigning funding to all the operations for the

purpose of proper execution of all of them. With the help of it, managers in ABC try to analyse

that the managers are assigning sufficient funds to all the departments according to their

requirements or not. It is beneficial for the enterprises because with the help of it the companies

will be able to perform operational activities in monetary resources that are assigned to them.

3. Evaluation of benefits of management accounting systems and their application within the

organisation

There are various types management accounting systems that are used by the managers of

ABC Ltd. Discussion of benefits of them along with application are discussed below:

Inventory management system: It is used in ABC Ltd by the managers for making sure

that they have detailed information of the inventory which is used for performing operations as it

is beneficial for execution of all the activities systematically (Datar and Rajan, 2018).

Cost accounting system: In ABC Ltd it is used by management team because it is

beneficial in determining cost of each and every activity performed by the enterprise.

Price optimisation system: Managers of ABC Ltd are using it for assuring that best

suitable price for all the products are determined as it is beneficial for meeting expectations of

customers.

Job order costing system: It is applied in ABC Ltd because it facilitates managers to

analyse cost of each and every job performed according to specifications of customers.

4. Critical evaluation of the way in which different systems and reports of management

accounting reports are integrated with organisational processes

In ABC Ltd the managers are using different types of management accounting reports and

systems. All of them are integrated with organisations processes. For example, inventory

management system is used by the managers for analysing that the entity is able to keep

sufficient goods for performing all the operations in systematic manner. On the other hand,

account receivable system is used for analysing the owed amount of different customers. For

example, if the managers of the organisation will not be able to analyse actual outstanding

amount then this report could be used by them to determine it (Feng and Ho, 2016).

3

TASK 2

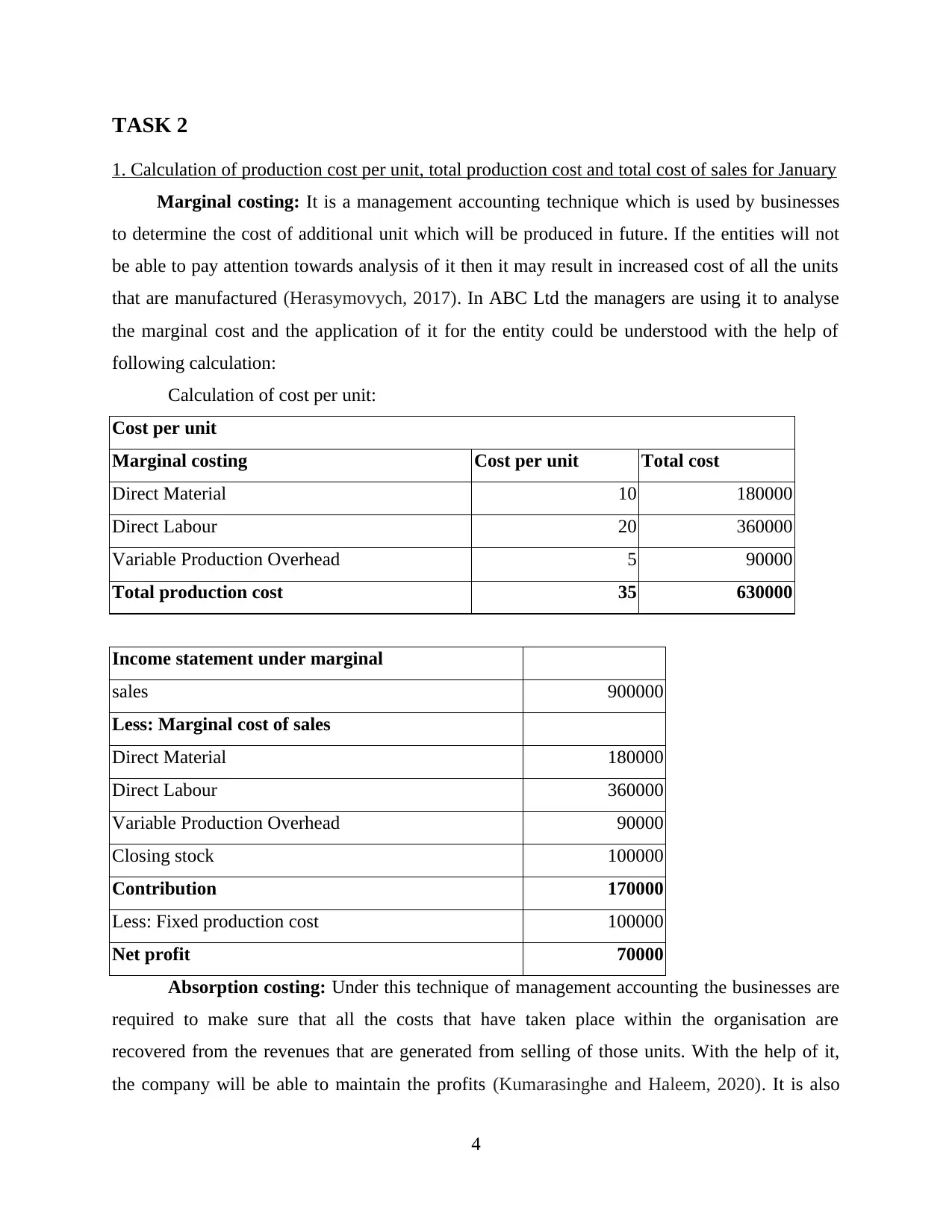

1. Calculation of production cost per unit, total production cost and total cost of sales for January

Marginal costing: It is a management accounting technique which is used by businesses

to determine the cost of additional unit which will be produced in future. If the entities will not

be able to pay attention towards analysis of it then it may result in increased cost of all the units

that are manufactured (Herasymovych, 2017). In ABC Ltd the managers are using it to analyse

the marginal cost and the application of it for the entity could be understood with the help of

following calculation:

Calculation of cost per unit:

Cost per unit

Marginal costing Cost per unit Total cost

Direct Material 10 180000

Direct Labour 20 360000

Variable Production Overhead 5 90000

Total production cost 35 630000

Income statement under marginal

sales 900000

Less: Marginal cost of sales

Direct Material 180000

Direct Labour 360000

Variable Production Overhead 90000

Closing stock 100000

Contribution 170000

Less: Fixed production cost 100000

Net profit 70000

Absorption costing: Under this technique of management accounting the businesses are

required to make sure that all the costs that have taken place within the organisation are

recovered from the revenues that are generated from selling of those units. With the help of it,

the company will be able to maintain the profits (Kumarasinghe and Haleem, 2020). It is also

4

1. Calculation of production cost per unit, total production cost and total cost of sales for January

Marginal costing: It is a management accounting technique which is used by businesses

to determine the cost of additional unit which will be produced in future. If the entities will not

be able to pay attention towards analysis of it then it may result in increased cost of all the units

that are manufactured (Herasymovych, 2017). In ABC Ltd the managers are using it to analyse

the marginal cost and the application of it for the entity could be understood with the help of

following calculation:

Calculation of cost per unit:

Cost per unit

Marginal costing Cost per unit Total cost

Direct Material 10 180000

Direct Labour 20 360000

Variable Production Overhead 5 90000

Total production cost 35 630000

Income statement under marginal

sales 900000

Less: Marginal cost of sales

Direct Material 180000

Direct Labour 360000

Variable Production Overhead 90000

Closing stock 100000

Contribution 170000

Less: Fixed production cost 100000

Net profit 70000

Absorption costing: Under this technique of management accounting the businesses are

required to make sure that all the costs that have taken place within the organisation are

recovered from the revenues that are generated from selling of those units. With the help of it,

the company will be able to maintain the profits (Kumarasinghe and Haleem, 2020). It is also

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

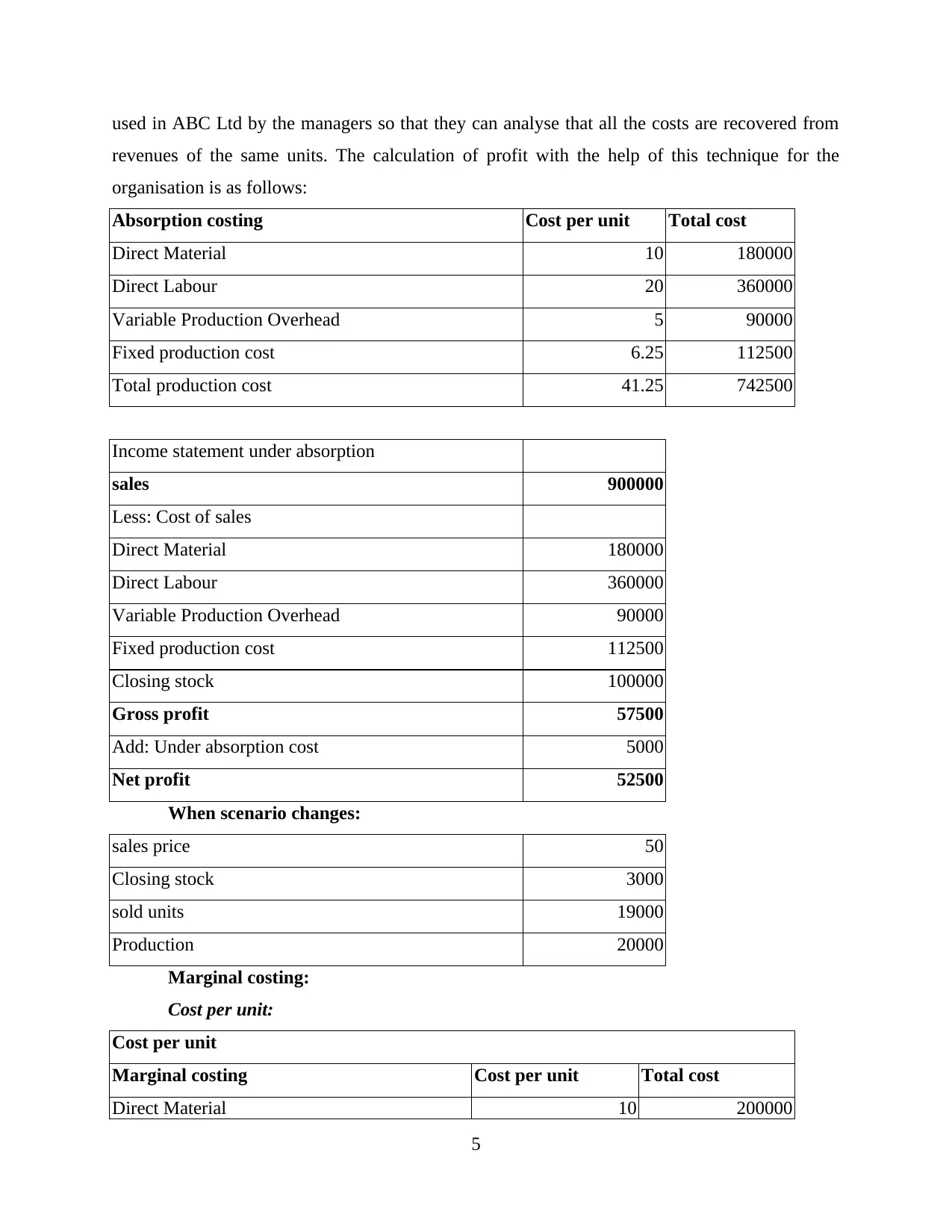

used in ABC Ltd by the managers so that they can analyse that all the costs are recovered from

revenues of the same units. The calculation of profit with the help of this technique for the

organisation is as follows:

Absorption costing Cost per unit Total cost

Direct Material 10 180000

Direct Labour 20 360000

Variable Production Overhead 5 90000

Fixed production cost 6.25 112500

Total production cost 41.25 742500

Income statement under absorption

sales 900000

Less: Cost of sales

Direct Material 180000

Direct Labour 360000

Variable Production Overhead 90000

Fixed production cost 112500

Closing stock 100000

Gross profit 57500

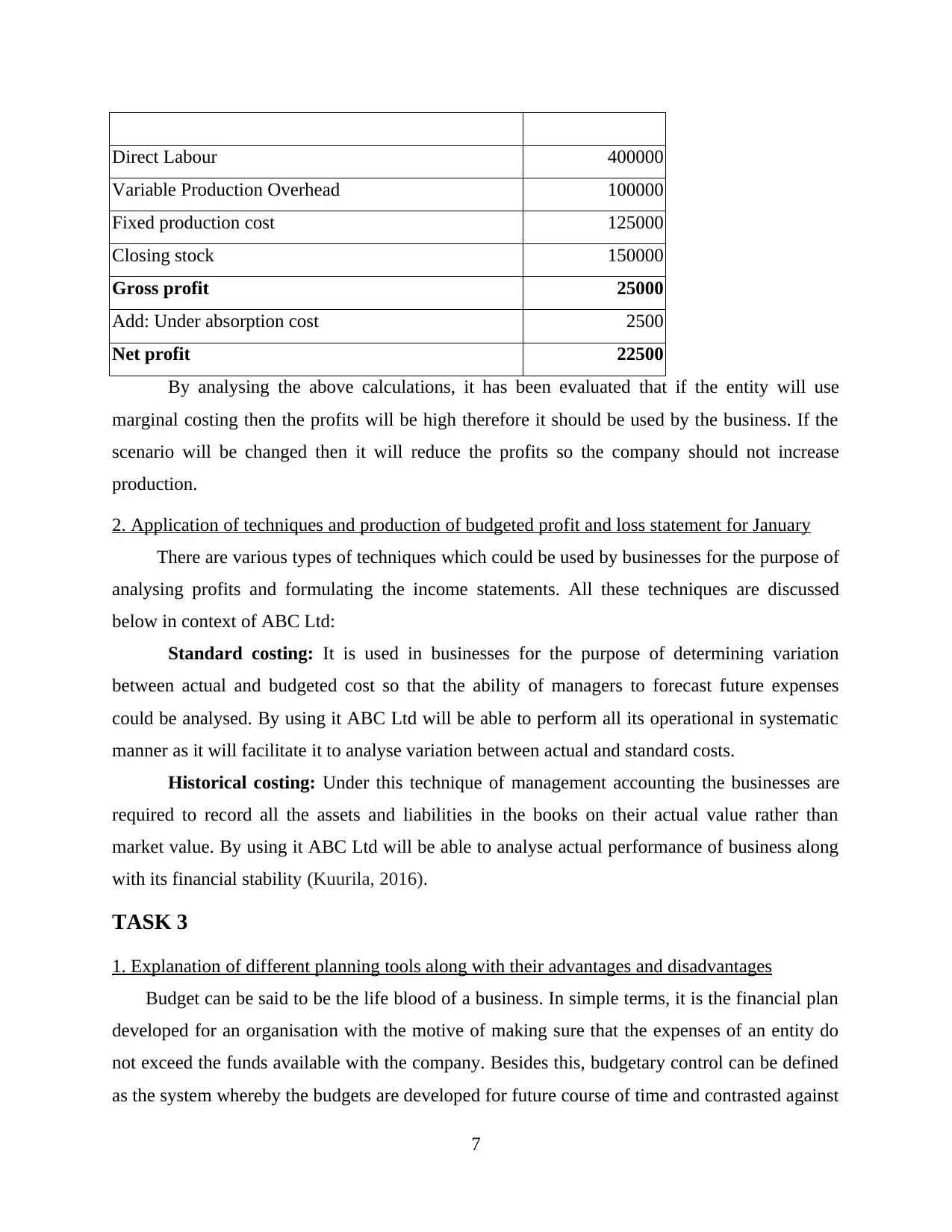

Add: Under absorption cost 5000

Net profit 52500

When scenario changes:

sales price 50

Closing stock 3000

sold units 19000

Production 20000

Marginal costing:

Cost per unit:

Cost per unit

Marginal costing Cost per unit Total cost

Direct Material 10 200000

5

revenues of the same units. The calculation of profit with the help of this technique for the

organisation is as follows:

Absorption costing Cost per unit Total cost

Direct Material 10 180000

Direct Labour 20 360000

Variable Production Overhead 5 90000

Fixed production cost 6.25 112500

Total production cost 41.25 742500

Income statement under absorption

sales 900000

Less: Cost of sales

Direct Material 180000

Direct Labour 360000

Variable Production Overhead 90000

Fixed production cost 112500

Closing stock 100000

Gross profit 57500

Add: Under absorption cost 5000

Net profit 52500

When scenario changes:

sales price 50

Closing stock 3000

sold units 19000

Production 20000

Marginal costing:

Cost per unit:

Cost per unit

Marginal costing Cost per unit Total cost

Direct Material 10 200000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

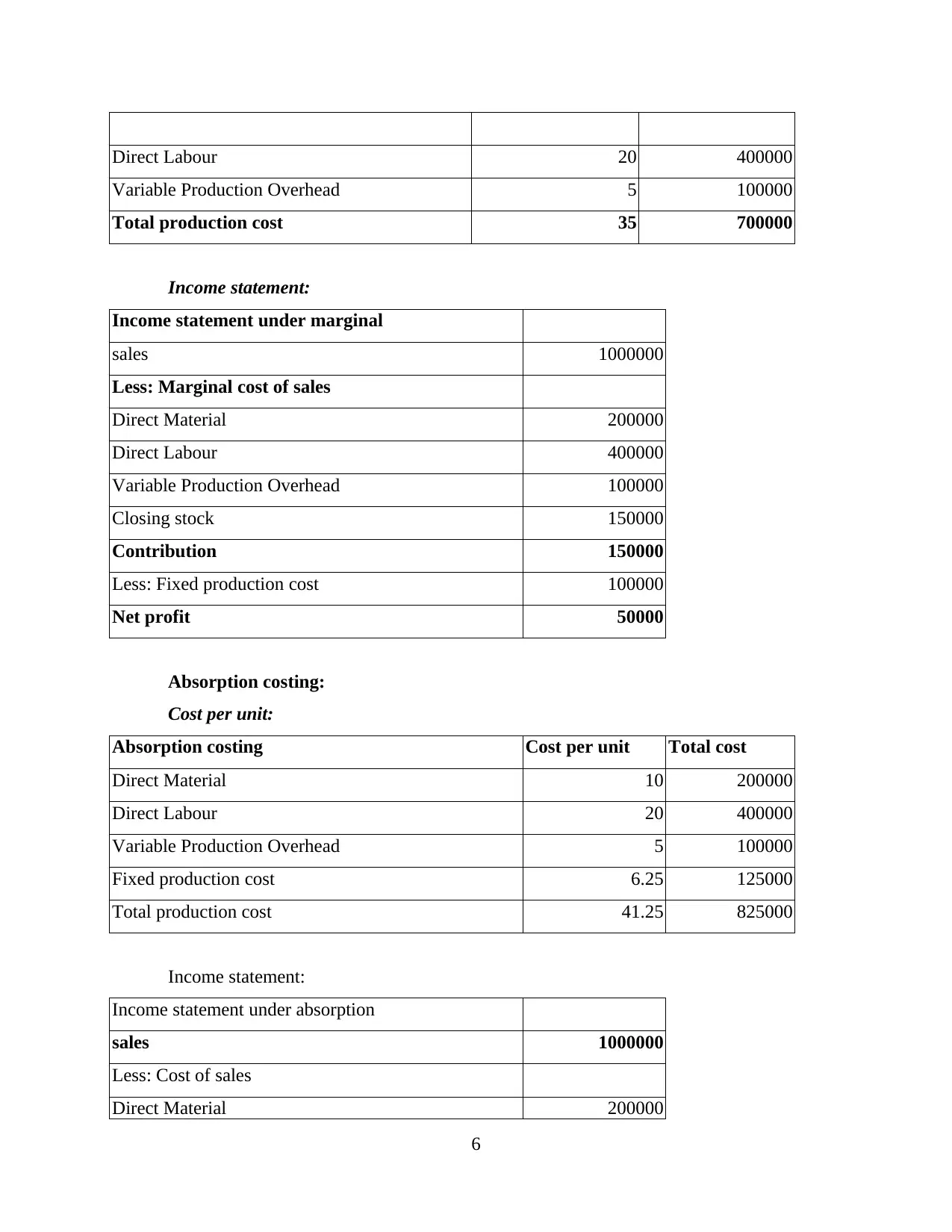

Direct Labour 20 400000

Variable Production Overhead 5 100000

Total production cost 35 700000

Income statement:

Income statement under marginal

sales 1000000

Less: Marginal cost of sales

Direct Material 200000

Direct Labour 400000

Variable Production Overhead 100000

Closing stock 150000

Contribution 150000

Less: Fixed production cost 100000

Net profit 50000

Absorption costing:

Cost per unit:

Absorption costing Cost per unit Total cost

Direct Material 10 200000

Direct Labour 20 400000

Variable Production Overhead 5 100000

Fixed production cost 6.25 125000

Total production cost 41.25 825000

Income statement:

Income statement under absorption

sales 1000000

Less: Cost of sales

Direct Material 200000

6

Variable Production Overhead 5 100000

Total production cost 35 700000

Income statement:

Income statement under marginal

sales 1000000

Less: Marginal cost of sales

Direct Material 200000

Direct Labour 400000

Variable Production Overhead 100000

Closing stock 150000

Contribution 150000

Less: Fixed production cost 100000

Net profit 50000

Absorption costing:

Cost per unit:

Absorption costing Cost per unit Total cost

Direct Material 10 200000

Direct Labour 20 400000

Variable Production Overhead 5 100000

Fixed production cost 6.25 125000

Total production cost 41.25 825000

Income statement:

Income statement under absorption

sales 1000000

Less: Cost of sales

Direct Material 200000

6

Direct Labour 400000

Variable Production Overhead 100000

Fixed production cost 125000

Closing stock 150000

Gross profit 25000

Add: Under absorption cost 2500

Net profit 22500

By analysing the above calculations, it has been evaluated that if the entity will use

marginal costing then the profits will be high therefore it should be used by the business. If the

scenario will be changed then it will reduce the profits so the company should not increase

production.

2. Application of techniques and production of budgeted profit and loss statement for January

There are various types of techniques which could be used by businesses for the purpose of

analysing profits and formulating the income statements. All these techniques are discussed

below in context of ABC Ltd:

Standard costing: It is used in businesses for the purpose of determining variation

between actual and budgeted cost so that the ability of managers to forecast future expenses

could be analysed. By using it ABC Ltd will be able to perform all its operational in systematic

manner as it will facilitate it to analyse variation between actual and standard costs.

Historical costing: Under this technique of management accounting the businesses are

required to record all the assets and liabilities in the books on their actual value rather than

market value. By using it ABC Ltd will be able to analyse actual performance of business along

with its financial stability (Kuurila, 2016).

TASK 3

1. Explanation of different planning tools along with their advantages and disadvantages

Budget can be said to be the life blood of a business. In simple terms, it is the financial plan

developed for an organisation with the motive of making sure that the expenses of an entity do

not exceed the funds available with the company. Besides this, budgetary control can be defined

as the system whereby the budgets are developed for future course of time and contrasted against

7

Variable Production Overhead 100000

Fixed production cost 125000

Closing stock 150000

Gross profit 25000

Add: Under absorption cost 2500

Net profit 22500

By analysing the above calculations, it has been evaluated that if the entity will use

marginal costing then the profits will be high therefore it should be used by the business. If the

scenario will be changed then it will reduce the profits so the company should not increase

production.

2. Application of techniques and production of budgeted profit and loss statement for January

There are various types of techniques which could be used by businesses for the purpose of

analysing profits and formulating the income statements. All these techniques are discussed

below in context of ABC Ltd:

Standard costing: It is used in businesses for the purpose of determining variation

between actual and budgeted cost so that the ability of managers to forecast future expenses

could be analysed. By using it ABC Ltd will be able to perform all its operational in systematic

manner as it will facilitate it to analyse variation between actual and standard costs.

Historical costing: Under this technique of management accounting the businesses are

required to record all the assets and liabilities in the books on their actual value rather than

market value. By using it ABC Ltd will be able to analyse actual performance of business along

with its financial stability (Kuurila, 2016).

TASK 3

1. Explanation of different planning tools along with their advantages and disadvantages

Budget can be said to be the life blood of a business. In simple terms, it is the financial plan

developed for an organisation with the motive of making sure that the expenses of an entity do

not exceed the funds available with the company. Besides this, budgetary control can be defined

as the system whereby the budgets are developed for future course of time and contrasted against

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the actual performance given by the firm to reach at the variances. Now, it has been recognised

that there are several planning tools which are used by ABC Ltd. for carrying out budgetary

control (Li, 2018). These are critically discussed and evaluated as follows:

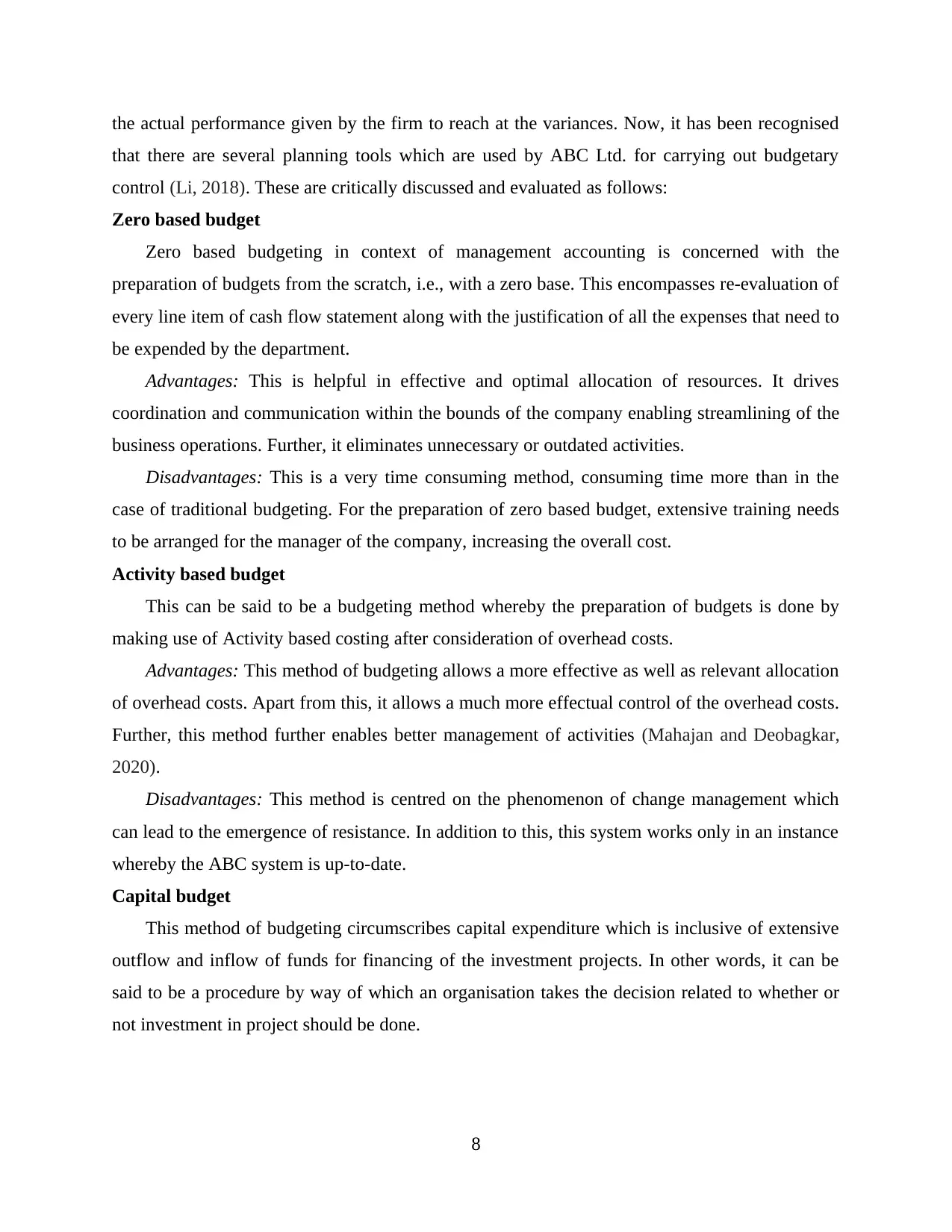

Zero based budget

Zero based budgeting in context of management accounting is concerned with the

preparation of budgets from the scratch, i.e., with a zero base. This encompasses re-evaluation of

every line item of cash flow statement along with the justification of all the expenses that need to

be expended by the department.

Advantages: This is helpful in effective and optimal allocation of resources. It drives

coordination and communication within the bounds of the company enabling streamlining of the

business operations. Further, it eliminates unnecessary or outdated activities.

Disadvantages: This is a very time consuming method, consuming time more than in the

case of traditional budgeting. For the preparation of zero based budget, extensive training needs

to be arranged for the manager of the company, increasing the overall cost.

Activity based budget

This can be said to be a budgeting method whereby the preparation of budgets is done by

making use of Activity based costing after consideration of overhead costs.

Advantages: This method of budgeting allows a more effective as well as relevant allocation

of overhead costs. Apart from this, it allows a much more effectual control of the overhead costs.

Further, this method further enables better management of activities (Mahajan and Deobagkar,

2020).

Disadvantages: This method is centred on the phenomenon of change management which

can lead to the emergence of resistance. In addition to this, this system works only in an instance

whereby the ABC system is up-to-date.

Capital budget

This method of budgeting circumscribes capital expenditure which is inclusive of extensive

outflow and inflow of funds for financing of the investment projects. In other words, it can be

said to be a procedure by way of which an organisation takes the decision related to whether or

not investment in project should be done.

8

that there are several planning tools which are used by ABC Ltd. for carrying out budgetary

control (Li, 2018). These are critically discussed and evaluated as follows:

Zero based budget

Zero based budgeting in context of management accounting is concerned with the

preparation of budgets from the scratch, i.e., with a zero base. This encompasses re-evaluation of

every line item of cash flow statement along with the justification of all the expenses that need to

be expended by the department.

Advantages: This is helpful in effective and optimal allocation of resources. It drives

coordination and communication within the bounds of the company enabling streamlining of the

business operations. Further, it eliminates unnecessary or outdated activities.

Disadvantages: This is a very time consuming method, consuming time more than in the

case of traditional budgeting. For the preparation of zero based budget, extensive training needs

to be arranged for the manager of the company, increasing the overall cost.

Activity based budget

This can be said to be a budgeting method whereby the preparation of budgets is done by

making use of Activity based costing after consideration of overhead costs.

Advantages: This method of budgeting allows a more effective as well as relevant allocation

of overhead costs. Apart from this, it allows a much more effectual control of the overhead costs.

Further, this method further enables better management of activities (Mahajan and Deobagkar,

2020).

Disadvantages: This method is centred on the phenomenon of change management which

can lead to the emergence of resistance. In addition to this, this system works only in an instance

whereby the ABC system is up-to-date.

Capital budget

This method of budgeting circumscribes capital expenditure which is inclusive of extensive

outflow and inflow of funds for financing of the investment projects. In other words, it can be

said to be a procedure by way of which an organisation takes the decision related to whether or

not investment in project should be done.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Advantages: This system provides due assistance in gaining knowledge of the risks and its

outcomes. In addition to this, this method enables to take decisions related to investment within a

project by taking into due consideration all the essential and necessary factors.

Disadvantages: The decisions taken by virtue of this method of budgeting is in long term

and thus cannot be reversed in any way. Apart from this, the techniques used to carry out capital

budget are assumed and not exist in reality (Nik, Abdullah and Said, 2016).

2. Analyse the use of different planning tools and their applications for preparing and forecasting

budgets

There are various types of planning tools that are used in ABC Ltd. these are zero based,

activity based and capital budget. All of them facilitate the organisation to forecast and prepare

budget so that success in future could be attained. With the help of them, managers try to analyse

the future incomes and expenses and then formulate decisions to assign budgets to different

departments (Shareia, 2016).

TASK 4

Compare how organisations are adapting management accounting systems to respond to

financial problems

In the business environment, management accounting systems are defined as important aspects

which should be consider while running a business as it supports to make the right business

decision. While running a business many financial problems arises, where it is important for

management to solve them by using best alternatives (Renz, 2016). ABC company is facing

different types of financial problem in their business that are as explained:

Improper cash flow management: For organisation it is important that prepare the cash

flow statement and manage them properly. If organisation is not able to arrange and organise

the financial records then a challenge will be occurred as low profitability. ABC Ltd is

facing the financial problem due to lack of cash flow management and not recording

financial information that needs to be solve.

Late payment by clients: The business mainly depends on creditors and debtors who

manages the activities by payment and receiving the money. In case if clients has deny and

make the payment late then financial problem arises in business. ABC Ltd can face the

challenge as customers are making late payment for buying the products.

9

outcomes. In addition to this, this method enables to take decisions related to investment within a

project by taking into due consideration all the essential and necessary factors.

Disadvantages: The decisions taken by virtue of this method of budgeting is in long term

and thus cannot be reversed in any way. Apart from this, the techniques used to carry out capital

budget are assumed and not exist in reality (Nik, Abdullah and Said, 2016).

2. Analyse the use of different planning tools and their applications for preparing and forecasting

budgets

There are various types of planning tools that are used in ABC Ltd. these are zero based,

activity based and capital budget. All of them facilitate the organisation to forecast and prepare

budget so that success in future could be attained. With the help of them, managers try to analyse

the future incomes and expenses and then formulate decisions to assign budgets to different

departments (Shareia, 2016).

TASK 4

Compare how organisations are adapting management accounting systems to respond to

financial problems

In the business environment, management accounting systems are defined as important aspects

which should be consider while running a business as it supports to make the right business

decision. While running a business many financial problems arises, where it is important for

management to solve them by using best alternatives (Renz, 2016). ABC company is facing

different types of financial problem in their business that are as explained:

Improper cash flow management: For organisation it is important that prepare the cash

flow statement and manage them properly. If organisation is not able to arrange and organise

the financial records then a challenge will be occurred as low profitability. ABC Ltd is

facing the financial problem due to lack of cash flow management and not recording

financial information that needs to be solve.

Late payment by clients: The business mainly depends on creditors and debtors who

manages the activities by payment and receiving the money. In case if clients has deny and

make the payment late then financial problem arises in business. ABC Ltd can face the

challenge as customers are making late payment for buying the products.

9

Financial governance: This stating as governmental authority who formulates different

regulations and laws that helps to run a business. This is the way of collecting, managing,

monitoring and controlling the financial information which helps to run a business

effectively in challenging environment.

Tools which are used to identify the financial problem

KPI: This means key performance indicator which is key measurable value uses to know

the financial and non-financial performance. This can be used by ABC Ltd company to

identify the gap between different activities and make the right business decision by

managing and organising all information.

Benchmarking: This tool is related to operation and management which can help to

complete the task and attain competitive benefits by comparing with other company. ABC

Ltd can use this tool for comparing with other company and formulate planning accordingly

that helps to solve the problems (Sekerez, 2017).

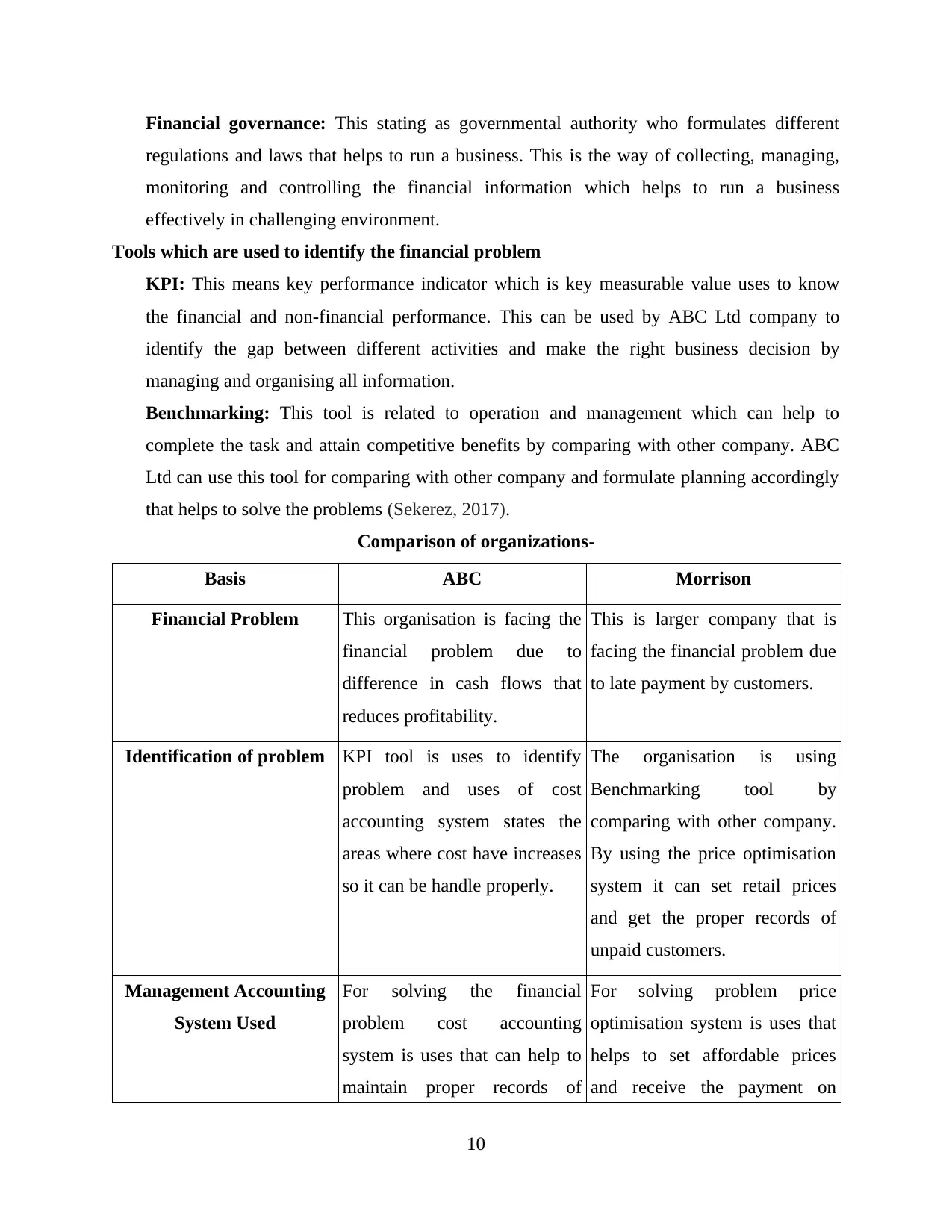

Comparison of organizations-

Basis ABC Morrison

Financial Problem This organisation is facing the

financial problem due to

difference in cash flows that

reduces profitability.

This is larger company that is

facing the financial problem due

to late payment by customers.

Identification of problem KPI tool is uses to identify

problem and uses of cost

accounting system states the

areas where cost have increases

so it can be handle properly.

The organisation is using

Benchmarking tool by

comparing with other company.

By using the price optimisation

system it can set retail prices

and get the proper records of

unpaid customers.

Management Accounting

System Used

For solving the financial

problem cost accounting

system is uses that can help to

maintain proper records of

For solving problem price

optimisation system is uses that

helps to set affordable prices

and receive the payment on

10

regulations and laws that helps to run a business. This is the way of collecting, managing,

monitoring and controlling the financial information which helps to run a business

effectively in challenging environment.

Tools which are used to identify the financial problem

KPI: This means key performance indicator which is key measurable value uses to know

the financial and non-financial performance. This can be used by ABC Ltd company to

identify the gap between different activities and make the right business decision by

managing and organising all information.

Benchmarking: This tool is related to operation and management which can help to

complete the task and attain competitive benefits by comparing with other company. ABC

Ltd can use this tool for comparing with other company and formulate planning accordingly

that helps to solve the problems (Sekerez, 2017).

Comparison of organizations-

Basis ABC Morrison

Financial Problem This organisation is facing the

financial problem due to

difference in cash flows that

reduces profitability.

This is larger company that is

facing the financial problem due

to late payment by customers.

Identification of problem KPI tool is uses to identify

problem and uses of cost

accounting system states the

areas where cost have increases

so it can be handle properly.

The organisation is using

Benchmarking tool by

comparing with other company.

By using the price optimisation

system it can set retail prices

and get the proper records of

unpaid customers.

Management Accounting

System Used

For solving the financial

problem cost accounting

system is uses that can help to

maintain proper records of

For solving problem price

optimisation system is uses that

helps to set affordable prices

and receive the payment on

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.