Management Accounting Report: Performance and Decision Making

VerifiedAdded on 2022/12/19

|13

|2628

|238

Report

AI Summary

This report analyzes management accounting techniques, including activity-based costing, budgeting, and balanced scorecards, to evaluate organizational performance and financial feasibility. The report begins with an introduction to management accounting and its role in decision-making, followed by an analysis of activity-based costing, calculations of activity costs, and recommendations for capacity utilization. The second section presents an income statement analysis, calculations of contribution margins, break-even points, and sales levels. The report then explores sales, production, and component usage budgets, offering recommendations for financial feasibility. Finally, the report discusses the balanced scorecard as a performance management tool, outlining its perspectives, objectives, and measures for the University of Malaysia. The report emphasizes the importance of cost management, strategic planning, and effective decision-making for improved organizational outcomes.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Management Accounting.................................................................................................................1

Introduction......................................................................................................................................3

Main Body.......................................................................................................................................3

Question 1........................................................................................................................................3

Question 2........................................................................................................................................4

Question 3........................................................................................................................................7

a) Various budget preparation................................................................................................7

b) Recommendations to organisation in regard to their financial feasibility.........................9

Question 4........................................................................................................................................9

Conclusion.....................................................................................................................................11

REFERENCES..............................................................................................................................13

INTRODUCTION.........................................................................................................................14

Management Accounting.................................................................................................................1

Introduction......................................................................................................................................3

Main Body.......................................................................................................................................3

Question 1........................................................................................................................................3

Question 2........................................................................................................................................4

Question 3........................................................................................................................................7

a) Various budget preparation................................................................................................7

b) Recommendations to organisation in regard to their financial feasibility.........................9

Question 4........................................................................................................................................9

Conclusion.....................................................................................................................................11

REFERENCES..............................................................................................................................13

INTRODUCTION.........................................................................................................................14

Introduction

Management accounting is a broad term which includes various forms of techniques that are

helpful in decision making by supervisors or managers in an organisation. It includes

different types of management techniques such as Activity based costing, marginal costing,

budget preparation, balanced scorecard and other factors which hamper decisions in an

organisation. There is considerably huge importance of cost accounting in an organisation in

order to determine wide range of factors connected with organisational decisions. In this

report, impact of cost accounting techniques will be analysed in order to evaluate

performance of an organisation and respective decision which needs to be taken in such

regard. It is believed that cost accounting plays vital role in management of organisational

operations in more effective and efficient manner.

Main Body

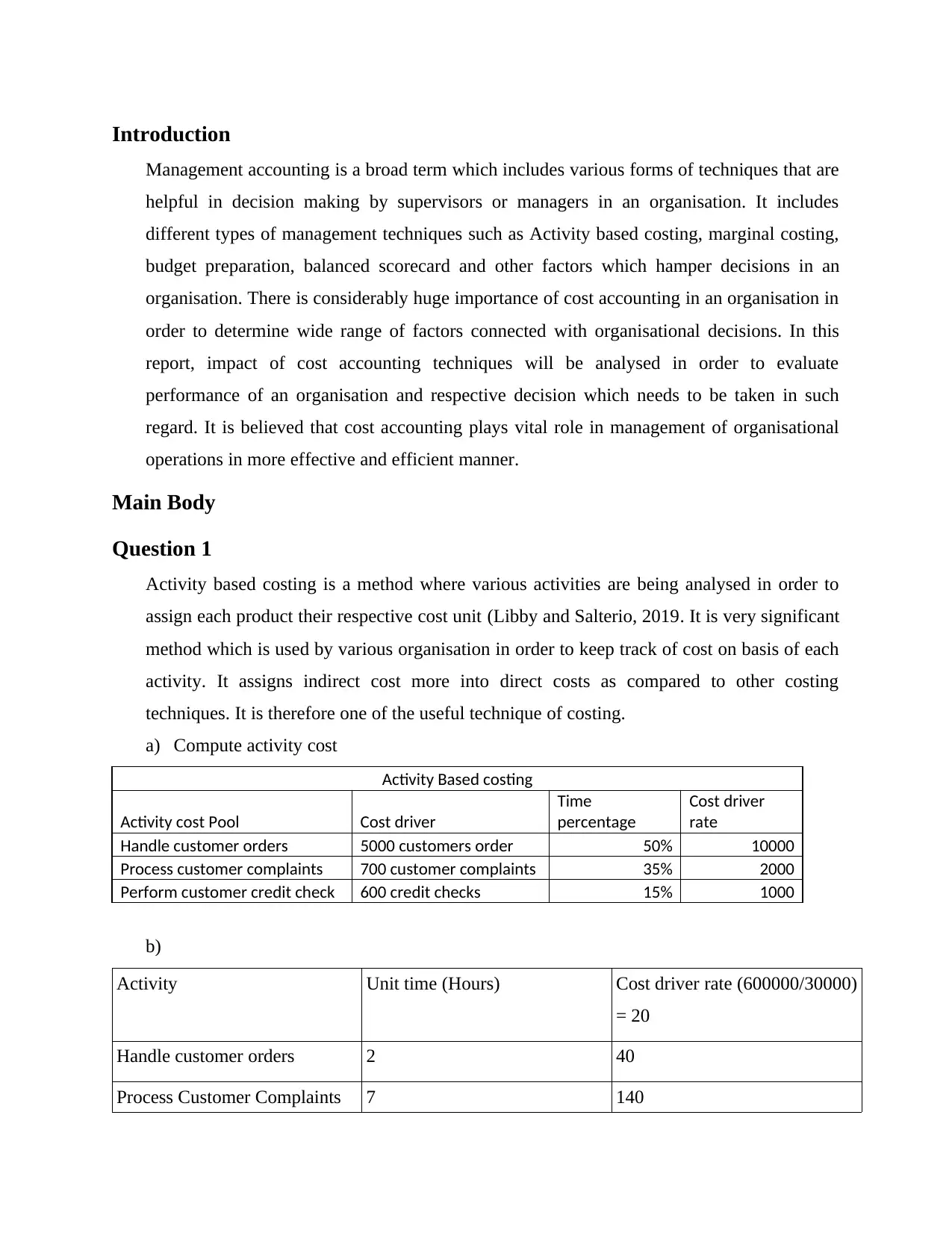

Question 1

Activity based costing is a method where various activities are being analysed in order to

assign each product their respective cost unit (Libby and Salterio, 2019. It is very significant

method which is used by various organisation in order to keep track of cost on basis of each

activity. It assigns indirect cost more into direct costs as compared to other costing

techniques. It is therefore one of the useful technique of costing.

a) Compute activity cost

Activity Based costing

Activity cost Pool Cost driver

Time

percentage

Cost driver

rate

Handle customer orders 5000 customers order 50% 10000

Process customer complaints 700 customer complaints 35% 2000

Perform customer credit check 600 credit checks 15% 1000

b)

Activity Unit time (Hours) Cost driver rate (600000/30000)

= 20

Handle customer orders 2 40

Process Customer Complaints 7 140

Management accounting is a broad term which includes various forms of techniques that are

helpful in decision making by supervisors or managers in an organisation. It includes

different types of management techniques such as Activity based costing, marginal costing,

budget preparation, balanced scorecard and other factors which hamper decisions in an

organisation. There is considerably huge importance of cost accounting in an organisation in

order to determine wide range of factors connected with organisational decisions. In this

report, impact of cost accounting techniques will be analysed in order to evaluate

performance of an organisation and respective decision which needs to be taken in such

regard. It is believed that cost accounting plays vital role in management of organisational

operations in more effective and efficient manner.

Main Body

Question 1

Activity based costing is a method where various activities are being analysed in order to

assign each product their respective cost unit (Libby and Salterio, 2019. It is very significant

method which is used by various organisation in order to keep track of cost on basis of each

activity. It assigns indirect cost more into direct costs as compared to other costing

techniques. It is therefore one of the useful technique of costing.

a) Compute activity cost

Activity Based costing

Activity cost Pool Cost driver

Time

percentage

Cost driver

rate

Handle customer orders 5000 customers order 50% 10000

Process customer complaints 700 customer complaints 35% 2000

Perform customer credit check 600 credit checks 15% 1000

b)

Activity Unit time (Hours) Cost driver rate (600000/30000)

= 20

Handle customer orders 2 40

Process Customer Complaints 7 140

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Perform customer credit check 5 100

280

c)

Activity cost Pool

Cost driver

rates

Cost

assigned

5,000 customer orders 40 200000

600 customer complaints 140 84000

400 credit checks 100 40000

d) By analysing above activity based costing, it is assumed that organisation needs to

emphasize over utilization of unused capacity in order to eliminate wastage in operations

of an organisation (Wegmann, 2019. Such practices promote healthy flow of operations

in an organisation.

Question 2

Question 2

Working Notes:

January

Sales price per unit 300 RM

Sales level of single shift 4000 capacitor

Production capacity single shift 5500 capacitor

Variable production cost 150

RM per

capacitor

Fixed production cost 300000 RM per month

Variable selling and distribution cost 30

RM per

capacitor

Fixed selling and distribution cost 60000 RM per month

280

c)

Activity cost Pool

Cost driver

rates

Cost

assigned

5,000 customer orders 40 200000

600 customer complaints 140 84000

400 credit checks 100 40000

d) By analysing above activity based costing, it is assumed that organisation needs to

emphasize over utilization of unused capacity in order to eliminate wastage in operations

of an organisation (Wegmann, 2019. Such practices promote healthy flow of operations

in an organisation.

Question 2

Question 2

Working Notes:

January

Sales price per unit 300 RM

Sales level of single shift 4000 capacitor

Production capacity single shift 5500 capacitor

Variable production cost 150

RM per

capacitor

Fixed production cost 300000 RM per month

Variable selling and distribution cost 30

RM per

capacitor

Fixed selling and distribution cost 60000 RM per month

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

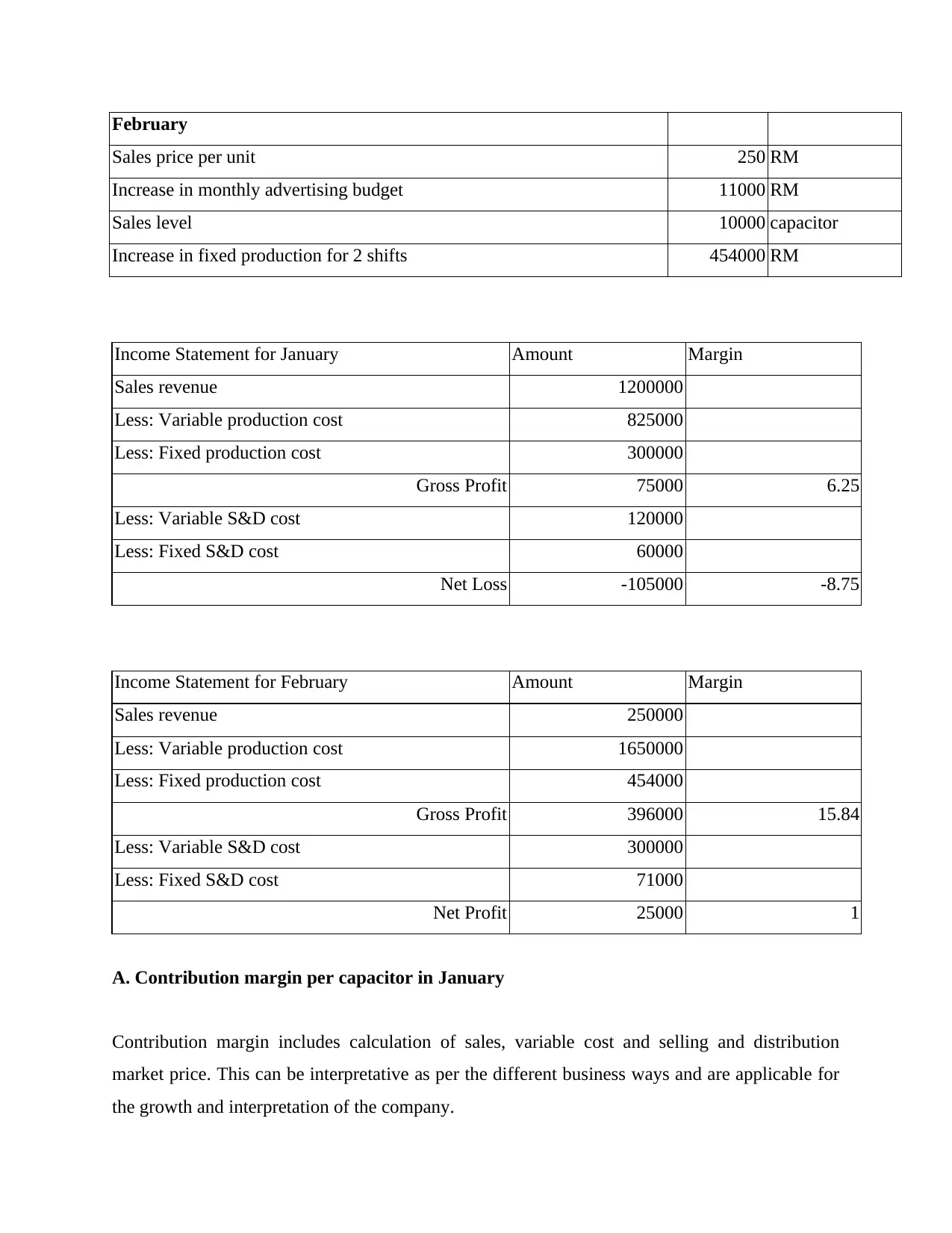

February

Sales price per unit 250 RM

Increase in monthly advertising budget 11000 RM

Sales level 10000 capacitor

Increase in fixed production for 2 shifts 454000 RM

Income Statement for January Amount Margin

Sales revenue 1200000

Less: Variable production cost 825000

Less: Fixed production cost 300000

Gross Profit 75000 6.25

Less: Variable S&D cost 120000

Less: Fixed S&D cost 60000

Net Loss -105000 -8.75

Income Statement for February Amount Margin

Sales revenue 250000

Less: Variable production cost 1650000

Less: Fixed production cost 454000

Gross Profit 396000 15.84

Less: Variable S&D cost 300000

Less: Fixed S&D cost 71000

Net Profit 25000 1

A. Contribution margin per capacitor in January

Contribution margin includes calculation of sales, variable cost and selling and distribution

market price. This can be interpretative as per the different business ways and are applicable for

the growth and interpretation of the company.

Sales price per unit 250 RM

Increase in monthly advertising budget 11000 RM

Sales level 10000 capacitor

Increase in fixed production for 2 shifts 454000 RM

Income Statement for January Amount Margin

Sales revenue 1200000

Less: Variable production cost 825000

Less: Fixed production cost 300000

Gross Profit 75000 6.25

Less: Variable S&D cost 120000

Less: Fixed S&D cost 60000

Net Loss -105000 -8.75

Income Statement for February Amount Margin

Sales revenue 250000

Less: Variable production cost 1650000

Less: Fixed production cost 454000

Gross Profit 396000 15.84

Less: Variable S&D cost 300000

Less: Fixed S&D cost 71000

Net Profit 25000 1

A. Contribution margin per capacitor in January

Contribution margin includes calculation of sales, variable cost and selling and distribution

market price. This can be interpretative as per the different business ways and are applicable for

the growth and interpretation of the company.

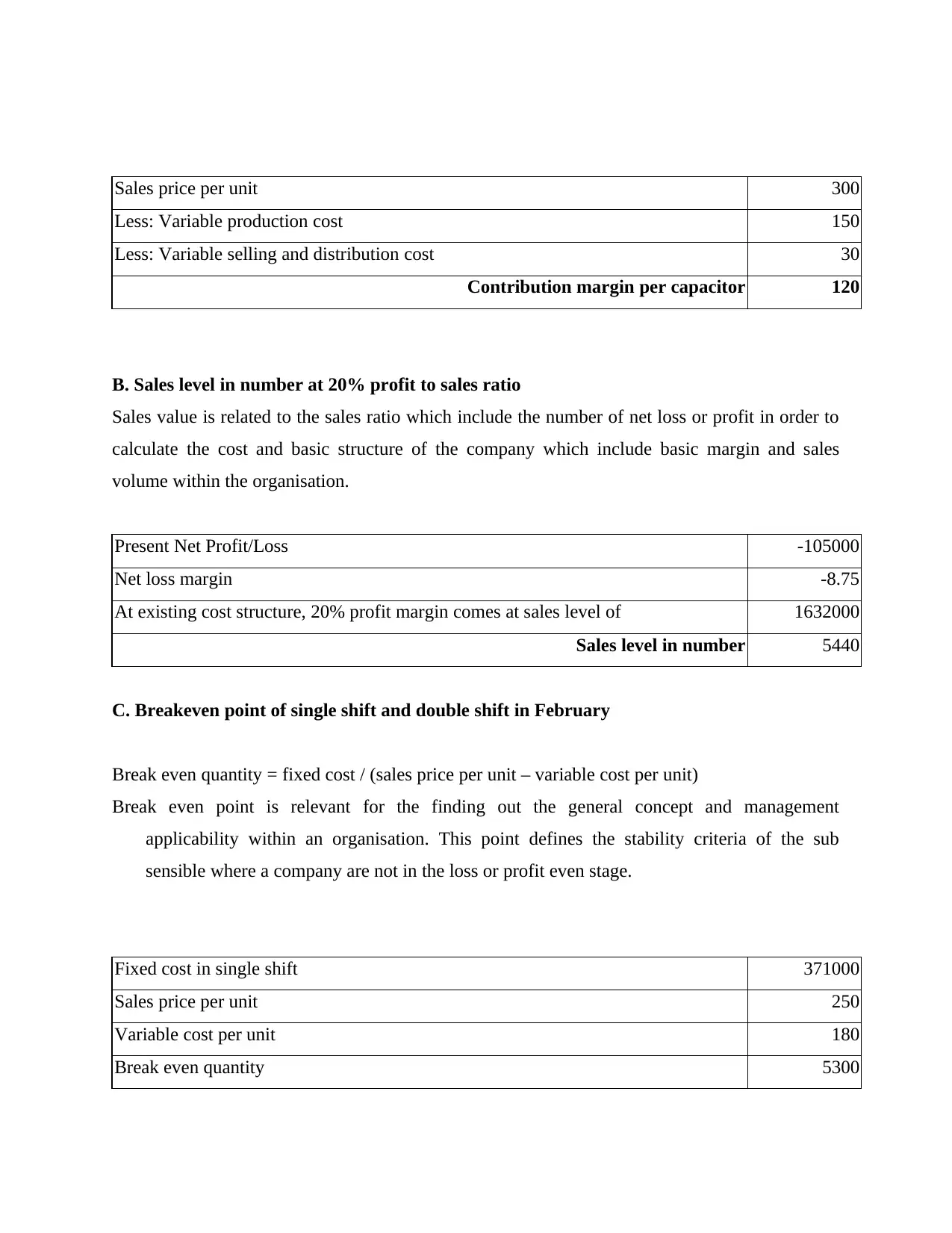

Sales price per unit 300

Less: Variable production cost 150

Less: Variable selling and distribution cost 30

Contribution margin per capacitor 120

B. Sales level in number at 20% profit to sales ratio

Sales value is related to the sales ratio which include the number of net loss or profit in order to

calculate the cost and basic structure of the company which include basic margin and sales

volume within the organisation.

Present Net Profit/Loss -105000

Net loss margin -8.75

At existing cost structure, 20% profit margin comes at sales level of 1632000

Sales level in number 5440

C. Breakeven point of single shift and double shift in February

Break even quantity = fixed cost / (sales price per unit – variable cost per unit)

Break even point is relevant for the finding out the general concept and management

applicability within an organisation. This point defines the stability criteria of the sub

sensible where a company are not in the loss or profit even stage.

Fixed cost in single shift 371000

Sales price per unit 250

Variable cost per unit 180

Break even quantity 5300

Less: Variable production cost 150

Less: Variable selling and distribution cost 30

Contribution margin per capacitor 120

B. Sales level in number at 20% profit to sales ratio

Sales value is related to the sales ratio which include the number of net loss or profit in order to

calculate the cost and basic structure of the company which include basic margin and sales

volume within the organisation.

Present Net Profit/Loss -105000

Net loss margin -8.75

At existing cost structure, 20% profit margin comes at sales level of 1632000

Sales level in number 5440

C. Breakeven point of single shift and double shift in February

Break even quantity = fixed cost / (sales price per unit – variable cost per unit)

Break even point is relevant for the finding out the general concept and management

applicability within an organisation. This point defines the stability criteria of the sub

sensible where a company are not in the loss or profit even stage.

Fixed cost in single shift 371000

Sales price per unit 250

Variable cost per unit 180

Break even quantity 5300

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

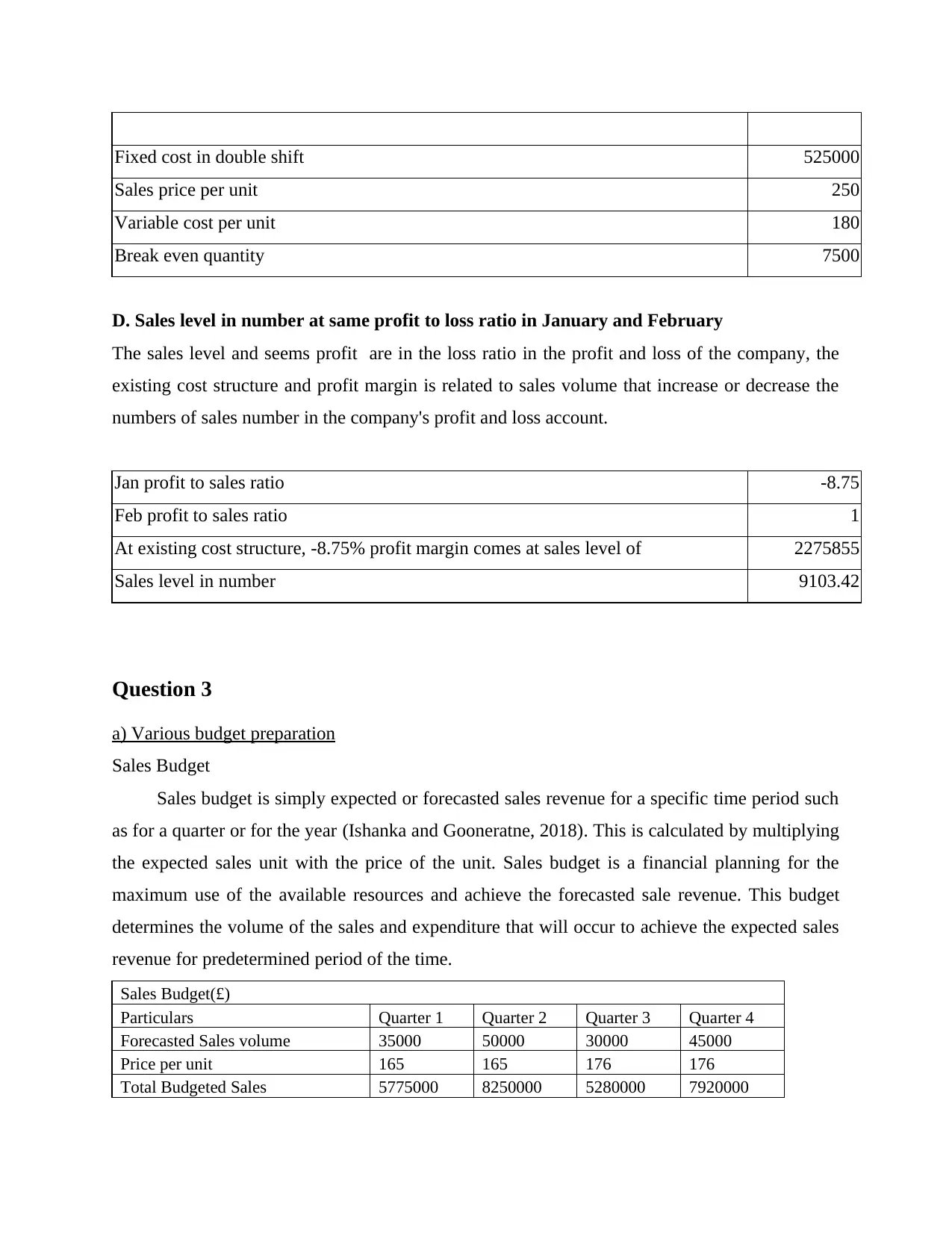

Fixed cost in double shift 525000

Sales price per unit 250

Variable cost per unit 180

Break even quantity 7500

D. Sales level in number at same profit to loss ratio in January and February

The sales level and seems profit are in the loss ratio in the profit and loss of the company, the

existing cost structure and profit margin is related to sales volume that increase or decrease the

numbers of sales number in the company's profit and loss account.

Jan profit to sales ratio -8.75

Feb profit to sales ratio 1

At existing cost structure, -8.75% profit margin comes at sales level of 2275855

Sales level in number 9103.42

Question 3

a) Various budget preparation

Sales Budget

Sales budget is simply expected or forecasted sales revenue for a specific time period such

as for a quarter or for the year (Ishanka and Gooneratne, 2018). This is calculated by multiplying

the expected sales unit with the price of the unit. Sales budget is a financial planning for the

maximum use of the available resources and achieve the forecasted sale revenue. This budget

determines the volume of the sales and expenditure that will occur to achieve the expected sales

revenue for predetermined period of the time.

Sales Budget(£)

Particulars Quarter 1 Quarter 2 Quarter 3 Quarter 4

Forecasted Sales volume 35000 50000 30000 45000

Price per unit 165 165 176 176

Total Budgeted Sales 5775000 8250000 5280000 7920000

Sales price per unit 250

Variable cost per unit 180

Break even quantity 7500

D. Sales level in number at same profit to loss ratio in January and February

The sales level and seems profit are in the loss ratio in the profit and loss of the company, the

existing cost structure and profit margin is related to sales volume that increase or decrease the

numbers of sales number in the company's profit and loss account.

Jan profit to sales ratio -8.75

Feb profit to sales ratio 1

At existing cost structure, -8.75% profit margin comes at sales level of 2275855

Sales level in number 9103.42

Question 3

a) Various budget preparation

Sales Budget

Sales budget is simply expected or forecasted sales revenue for a specific time period such

as for a quarter or for the year (Ishanka and Gooneratne, 2018). This is calculated by multiplying

the expected sales unit with the price of the unit. Sales budget is a financial planning for the

maximum use of the available resources and achieve the forecasted sale revenue. This budget

determines the volume of the sales and expenditure that will occur to achieve the expected sales

revenue for predetermined period of the time.

Sales Budget(£)

Particulars Quarter 1 Quarter 2 Quarter 3 Quarter 4

Forecasted Sales volume 35000 50000 30000 45000

Price per unit 165 165 176 176

Total Budgeted Sales 5775000 8250000 5280000 7920000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

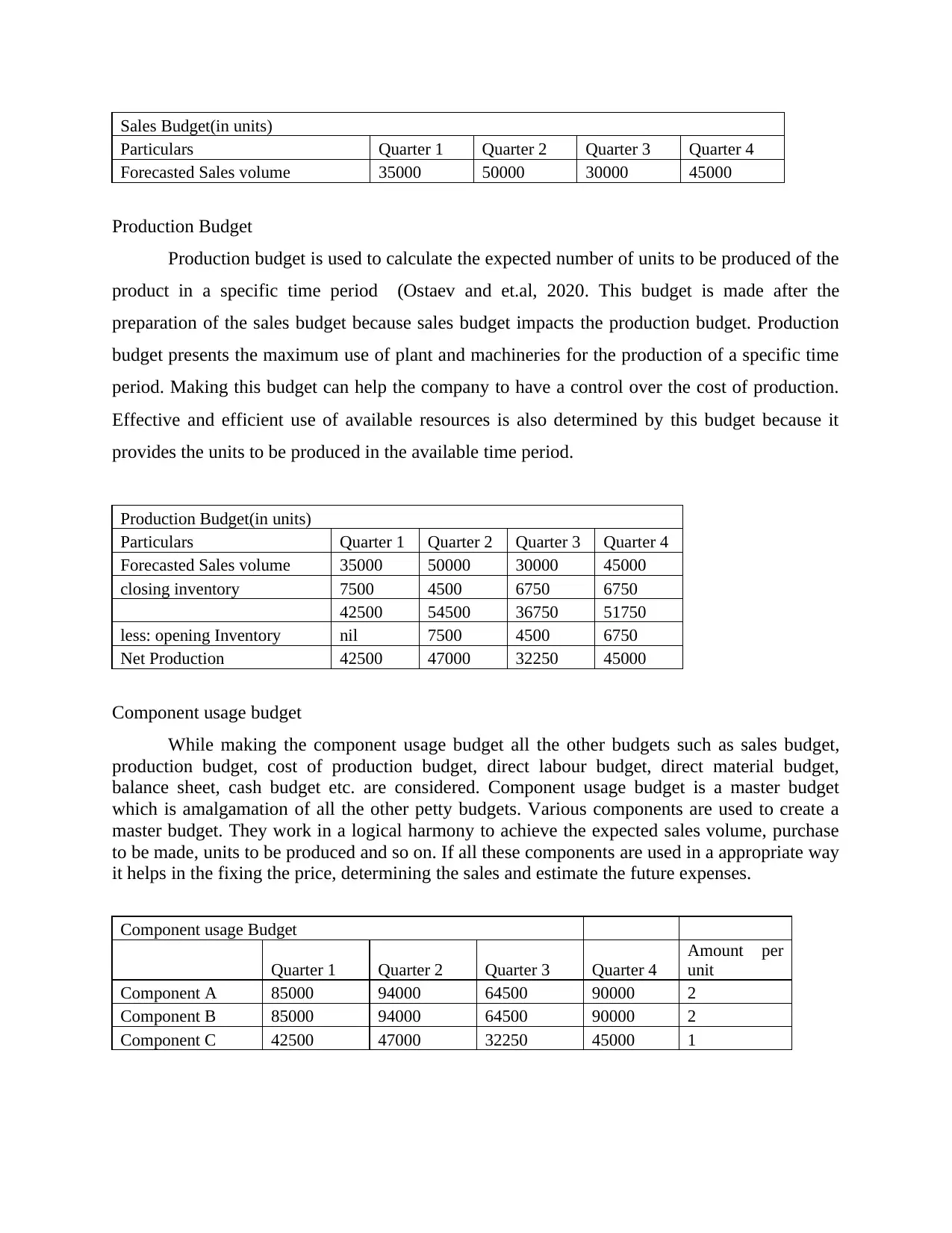

Sales Budget(in units)

Particulars Quarter 1 Quarter 2 Quarter 3 Quarter 4

Forecasted Sales volume 35000 50000 30000 45000

Production Budget

Production budget is used to calculate the expected number of units to be produced of the

product in a specific time period (Ostaev and et.al, 2020. This budget is made after the

preparation of the sales budget because sales budget impacts the production budget. Production

budget presents the maximum use of plant and machineries for the production of a specific time

period. Making this budget can help the company to have a control over the cost of production.

Effective and efficient use of available resources is also determined by this budget because it

provides the units to be produced in the available time period.

Production Budget(in units)

Particulars Quarter 1 Quarter 2 Quarter 3 Quarter 4

Forecasted Sales volume 35000 50000 30000 45000

closing inventory 7500 4500 6750 6750

42500 54500 36750 51750

less: opening Inventory nil 7500 4500 6750

Net Production 42500 47000 32250 45000

Component usage budget

While making the component usage budget all the other budgets such as sales budget,

production budget, cost of production budget, direct labour budget, direct material budget,

balance sheet, cash budget etc. are considered. Component usage budget is a master budget

which is amalgamation of all the other petty budgets. Various components are used to create a

master budget. They work in a logical harmony to achieve the expected sales volume, purchase

to be made, units to be produced and so on. If all these components are used in a appropriate way

it helps in the fixing the price, determining the sales and estimate the future expenses.

Component usage Budget

Quarter 1 Quarter 2 Quarter 3 Quarter 4

Amount per

unit

Component A 85000 94000 64500 90000 2

Component B 85000 94000 64500 90000 2

Component C 42500 47000 32250 45000 1

Particulars Quarter 1 Quarter 2 Quarter 3 Quarter 4

Forecasted Sales volume 35000 50000 30000 45000

Production Budget

Production budget is used to calculate the expected number of units to be produced of the

product in a specific time period (Ostaev and et.al, 2020. This budget is made after the

preparation of the sales budget because sales budget impacts the production budget. Production

budget presents the maximum use of plant and machineries for the production of a specific time

period. Making this budget can help the company to have a control over the cost of production.

Effective and efficient use of available resources is also determined by this budget because it

provides the units to be produced in the available time period.

Production Budget(in units)

Particulars Quarter 1 Quarter 2 Quarter 3 Quarter 4

Forecasted Sales volume 35000 50000 30000 45000

closing inventory 7500 4500 6750 6750

42500 54500 36750 51750

less: opening Inventory nil 7500 4500 6750

Net Production 42500 47000 32250 45000

Component usage budget

While making the component usage budget all the other budgets such as sales budget,

production budget, cost of production budget, direct labour budget, direct material budget,

balance sheet, cash budget etc. are considered. Component usage budget is a master budget

which is amalgamation of all the other petty budgets. Various components are used to create a

master budget. They work in a logical harmony to achieve the expected sales volume, purchase

to be made, units to be produced and so on. If all these components are used in a appropriate way

it helps in the fixing the price, determining the sales and estimate the future expenses.

Component usage Budget

Quarter 1 Quarter 2 Quarter 3 Quarter 4

Amount per

unit

Component A 85000 94000 64500 90000 2

Component B 85000 94000 64500 90000 2

Component C 42500 47000 32250 45000 1

Production cost budget

This budget is made to estimate the cost which is going to be used in the production of

the product. Production cost budget helps in meeting the needs of keeping inventory/stock handy

for the company. Cost that will occur to produce the forecasted sales units is calculated with the

help of production cost budget. This budget is also called the manufacturing budget. Sales units

to be produced in the specific time period are also estimated with the help of production cost

budget. Demand of the product can rise in the market at any time and this budget keeps the

production in the check.

b) Recommendations to organisation in regard to their financial feasibility

As per above analysis, it is concluded that organisation needs to emphasize over its

components wise cost in order to increase profit- margins in long term. For production based

companies, it is significant to manage their respective costing structure in much effective

and efficient manner so that proper operations can be initiated by the company. Also

organisation needs to focus over production of material so that less wastages and more

efficiency can be promoted by the company. It is necessary for an organisation to manage its

costs in effective manner as cost plays significant role in profit generation and reduction in

unnecessary costs. Therefore, it is required by the company to adopt adequate structure of

cost valuation and cost reduction in order to promote healthy business environment and

sustainability for long lasting term.

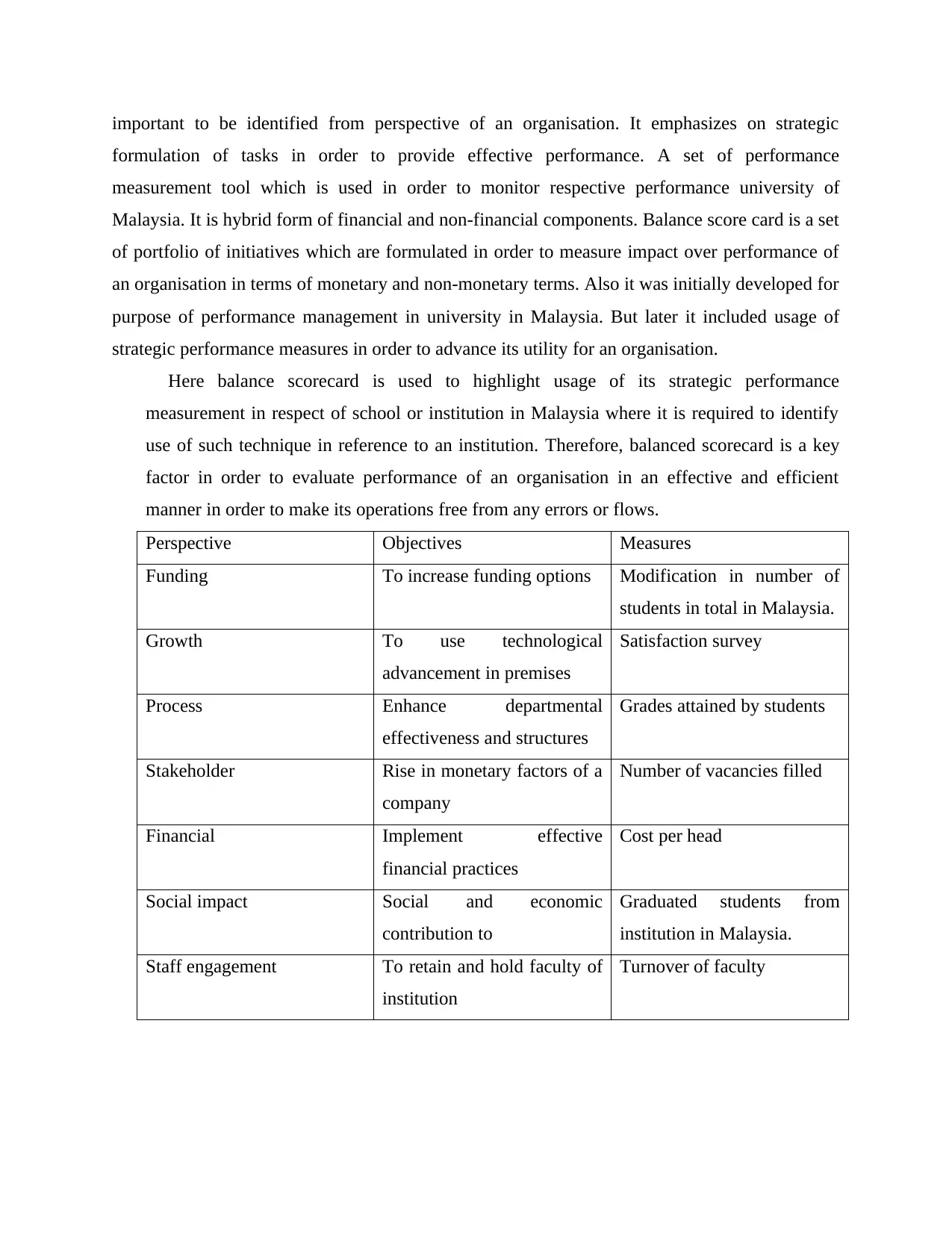

Question 4

Balanced score card is key strategy used by various institutions in regard to manage

performance of an organisation in a structured manner. It is used by managers to track various

tasks and activities in an organisation which is being executed by staff of the company so that

controlling and monitoring can be done adequately. It is primary tool of performance

management used by report in order to focus on errors or deviations which are required to rectify

so that smooth flow of operations can be maintained. It has various characteristics which are

This budget is made to estimate the cost which is going to be used in the production of

the product. Production cost budget helps in meeting the needs of keeping inventory/stock handy

for the company. Cost that will occur to produce the forecasted sales units is calculated with the

help of production cost budget. This budget is also called the manufacturing budget. Sales units

to be produced in the specific time period are also estimated with the help of production cost

budget. Demand of the product can rise in the market at any time and this budget keeps the

production in the check.

b) Recommendations to organisation in regard to their financial feasibility

As per above analysis, it is concluded that organisation needs to emphasize over its

components wise cost in order to increase profit- margins in long term. For production based

companies, it is significant to manage their respective costing structure in much effective

and efficient manner so that proper operations can be initiated by the company. Also

organisation needs to focus over production of material so that less wastages and more

efficiency can be promoted by the company. It is necessary for an organisation to manage its

costs in effective manner as cost plays significant role in profit generation and reduction in

unnecessary costs. Therefore, it is required by the company to adopt adequate structure of

cost valuation and cost reduction in order to promote healthy business environment and

sustainability for long lasting term.

Question 4

Balanced score card is key strategy used by various institutions in regard to manage

performance of an organisation in a structured manner. It is used by managers to track various

tasks and activities in an organisation which is being executed by staff of the company so that

controlling and monitoring can be done adequately. It is primary tool of performance

management used by report in order to focus on errors or deviations which are required to rectify

so that smooth flow of operations can be maintained. It has various characteristics which are

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

important to be identified from perspective of an organisation. It emphasizes on strategic

formulation of tasks in order to provide effective performance. A set of performance

measurement tool which is used in order to monitor respective performance university of

Malaysia. It is hybrid form of financial and non-financial components. Balance score card is a set

of portfolio of initiatives which are formulated in order to measure impact over performance of

an organisation in terms of monetary and non-monetary terms. Also it was initially developed for

purpose of performance management in university in Malaysia. But later it included usage of

strategic performance measures in order to advance its utility for an organisation.

Here balance scorecard is used to highlight usage of its strategic performance

measurement in respect of school or institution in Malaysia where it is required to identify

use of such technique in reference to an institution. Therefore, balanced scorecard is a key

factor in order to evaluate performance of an organisation in an effective and efficient

manner in order to make its operations free from any errors or flows.

Perspective Objectives Measures

Funding To increase funding options Modification in number of

students in total in Malaysia.

Growth To use technological

advancement in premises

Satisfaction survey

Process Enhance departmental

effectiveness and structures

Grades attained by students

Stakeholder Rise in monetary factors of a

company

Number of vacancies filled

Financial Implement effective

financial practices

Cost per head

Social impact Social and economic

contribution to

Graduated students from

institution in Malaysia.

Staff engagement To retain and hold faculty of

institution

Turnover of faculty

formulation of tasks in order to provide effective performance. A set of performance

measurement tool which is used in order to monitor respective performance university of

Malaysia. It is hybrid form of financial and non-financial components. Balance score card is a set

of portfolio of initiatives which are formulated in order to measure impact over performance of

an organisation in terms of monetary and non-monetary terms. Also it was initially developed for

purpose of performance management in university in Malaysia. But later it included usage of

strategic performance measures in order to advance its utility for an organisation.

Here balance scorecard is used to highlight usage of its strategic performance

measurement in respect of school or institution in Malaysia where it is required to identify

use of such technique in reference to an institution. Therefore, balanced scorecard is a key

factor in order to evaluate performance of an organisation in an effective and efficient

manner in order to make its operations free from any errors or flows.

Perspective Objectives Measures

Funding To increase funding options Modification in number of

students in total in Malaysia.

Growth To use technological

advancement in premises

Satisfaction survey

Process Enhance departmental

effectiveness and structures

Grades attained by students

Stakeholder Rise in monetary factors of a

company

Number of vacancies filled

Financial Implement effective

financial practices

Cost per head

Social impact Social and economic

contribution to

Graduated students from

institution in Malaysia.

Staff engagement To retain and hold faculty of

institution

Turnover of faculty

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Conclusion

It was observed in this report that management accounting techniques such as activity based

costing, marginal costing, balanced scorecard and budgeting plays significant role in

identification of financial performance of an organisation in order to make optimum

decision making in order to rectify errors or modifications required in operations of an

organisation. Decision making is important task in organisation, therefore it must be

addressed in proper manner with help of relevant financial statements and cost results which

will help an organisation to reach at feasible outcome.

It was observed in this report that management accounting techniques such as activity based

costing, marginal costing, balanced scorecard and budgeting plays significant role in

identification of financial performance of an organisation in order to make optimum

decision making in order to rectify errors or modifications required in operations of an

organisation. Decision making is important task in organisation, therefore it must be

addressed in proper manner with help of relevant financial statements and cost results which

will help an organisation to reach at feasible outcome.

REFERENCES

Books and Journals

Libby, T. and Salterio, S. E., 2019. Deception in management accounting experimental

research:“A tricky issue” revisited. Journal of Management Accounting Research.

31(2). pp.143-158.

Wegmann, G., 2019. A typology of cost accounting practices based on Activity-Based Costing-a

strategic cost management approach. Asia-Pacific Management Accounting Journal. 14.

pp.161-184.

Ishanka, S. and Gooneratne, T., 2018. Total quality management and changes in management

accounting systems in a manufacturing firm: A case study. Asia-Pacific Management

Accounting Journal. 13(1). pp.45-75.

Ostaev, G. Y. and et.al, 2020. Accounting agricultural business from scratch: management

accounting, decision making, analysis and monitoring of business processes. Amazonia

Investiga. 9(27). pp.319-332.

Tucker, B. P. and Leach, M., 2017. Learning from the experience of others: Lessons on the

research–practice gap in management accounting–A nursing perspective. In Advances

in Management Accounting. Emerald Publishing Limited.

Godil, D. I. and Shabib-ul-Hasan, S., 2018. An investigation of a contingency framework of

management accounting practices in manufacturing companies of Pakistan. GMJACS.

8(1). pp.12-12.

Burritt, R. L. and Christ, K. L., 2017. The need for monetary information within corporate water

accounting. Journal of environmental management. 201. pp.72-81.

GOVDYA, V. and KHROMOVA, I., 2018. Methodical Aspects of the Decomposition Approach

to the Formation of the Managerial Cost Accounting System in the Organizations of the

Russian Agroindustrial Complex. Journal of Applied Economic Sciences. 13(3).

Dahlan, M., 2019. Analysis of interrelationship between usefulness of management accounting

systems, interactive budget use and job performance. Management Science Letters.

9(7). pp.967-972.

Vetrov, Y. P., Vandina, O. G. and Galustov, A. R., 2017. Strategic management accounting in

organizations’ cash flow control. Journal of History Culture and Art Research. 6(4).

pp.425-435.

Christensen, J., 2018. Accounting in 2036: A Learned Profession: Part II: A Learned Research

and Education Environment. The Accounting Review. 93(6). pp.387-390.

Rikhardsson, P. and Yigitbasioglu, O., 2017, May. Business Intelligence in management

accounting research: current status and future focus. In 40th Annual Congress European

Accounting Association.

Galustov, 2017) (Christensen, 2018) (Rikhardsson and Yigitbasioglu, 2017)

Books and Journals

Libby, T. and Salterio, S. E., 2019. Deception in management accounting experimental

research:“A tricky issue” revisited. Journal of Management Accounting Research.

31(2). pp.143-158.

Wegmann, G., 2019. A typology of cost accounting practices based on Activity-Based Costing-a

strategic cost management approach. Asia-Pacific Management Accounting Journal. 14.

pp.161-184.

Ishanka, S. and Gooneratne, T., 2018. Total quality management and changes in management

accounting systems in a manufacturing firm: A case study. Asia-Pacific Management

Accounting Journal. 13(1). pp.45-75.

Ostaev, G. Y. and et.al, 2020. Accounting agricultural business from scratch: management

accounting, decision making, analysis and monitoring of business processes. Amazonia

Investiga. 9(27). pp.319-332.

Tucker, B. P. and Leach, M., 2017. Learning from the experience of others: Lessons on the

research–practice gap in management accounting–A nursing perspective. In Advances

in Management Accounting. Emerald Publishing Limited.

Godil, D. I. and Shabib-ul-Hasan, S., 2018. An investigation of a contingency framework of

management accounting practices in manufacturing companies of Pakistan. GMJACS.

8(1). pp.12-12.

Burritt, R. L. and Christ, K. L., 2017. The need for monetary information within corporate water

accounting. Journal of environmental management. 201. pp.72-81.

GOVDYA, V. and KHROMOVA, I., 2018. Methodical Aspects of the Decomposition Approach

to the Formation of the Managerial Cost Accounting System in the Organizations of the

Russian Agroindustrial Complex. Journal of Applied Economic Sciences. 13(3).

Dahlan, M., 2019. Analysis of interrelationship between usefulness of management accounting

systems, interactive budget use and job performance. Management Science Letters.

9(7). pp.967-972.

Vetrov, Y. P., Vandina, O. G. and Galustov, A. R., 2017. Strategic management accounting in

organizations’ cash flow control. Journal of History Culture and Art Research. 6(4).

pp.425-435.

Christensen, J., 2018. Accounting in 2036: A Learned Profession: Part II: A Learned Research

and Education Environment. The Accounting Review. 93(6). pp.387-390.

Rikhardsson, P. and Yigitbasioglu, O., 2017, May. Business Intelligence in management

accounting research: current status and future focus. In 40th Annual Congress European

Accounting Association.

Galustov, 2017) (Christensen, 2018) (Rikhardsson and Yigitbasioglu, 2017)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.