Management Accounting: Costing, Budgeting, and Financial Analysis

VerifiedAdded on 2023/01/13

|11

|2428

|76

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles, focusing on their application within Rowlinson Knitwear. It begins with an introduction to management accounting, detailing its role in managerial decision-making and the essential requirements of various management accounting systems, such as job costing and inventory management. The report then explores different methods of management accounting reporting, including budget reports, account receivable ageing reports, and performance reports. A significant portion is dedicated to the calculation of costs using marginal and absorption costing methods, providing income statements for each method. Furthermore, the report examines the advantages and disadvantages of different planning tools for budgetary control, such as fixed, flexible, and zero budgets. Finally, it uses specific examples to compare organizations in the context of management accounting systems, discussing financial problems and solutions like benchmarking and key performance indicators to reduce financial problems. The report concludes by emphasizing the importance of management accounting in aiding organizational decision-making and cost control.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

P1. Explanation of management accounting together with essential requirements of different

types........................................................................................................................................1

P2. Different methods of management accounting reporting.................................................2

P3. Calculation of costs on the basis of marginal and absorption costing method................3

P4. Explanation of advantages and disadvantages of different types of planning tools of

budgetary control....................................................................................................................5

P5. Use specific examples for a comparison of organisations in the context with management

accounting systems.................................................................................................................5

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

INTRODUCTION...........................................................................................................................1

P1. Explanation of management accounting together with essential requirements of different

types........................................................................................................................................1

P2. Different methods of management accounting reporting.................................................2

P3. Calculation of costs on the basis of marginal and absorption costing method................3

P4. Explanation of advantages and disadvantages of different types of planning tools of

budgetary control....................................................................................................................5

P5. Use specific examples for a comparison of organisations in the context with management

accounting systems.................................................................................................................5

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

INTRODUCTION

Management accounting is a branch of accounting which deals with managerial activities.

It is directly related to financial transactions but may have major impact in decision-making

related to such transactions (Commerford and et.al, 2016). Furthermore, it is used by the internal

management to take major decisions which can be implemented in the entity. The main purpose

of this is to help with proper administration of activities in a company. In this report, Rowlinson

Knitwear has been chosen which has its headquarter in United Kingdom. The assignment covers

explanation of management accounting along with essential requirements of different types,

different methods, application of marginal and absorption costing to calculate the costs,

advantages and disadvantages of types of planning tools for budgetary control and use of specific

examples for conducting comparison of management accounting systems.

P1. Explanation of management accounting together with essential requirements of different

types

Management accounting: It is a technique used by manager for the purpose of taking

decision by identifying, analysing, measuring and communicating essential financial

information. In other words it is a process of collecting essential financial information in order to

make plans and policies for the organisation. Management accounting also known as

“managerial accounting”. It is used by internal department of an organisation. The company use

various management accounting system in order to collecting necessary financial information of

each department of the company. These are the vital part of managerial accounting process,

theses system helps the organisation to record essential financial data of their daily basis

operational activities. Without using these system company never took decision regarding budget

policy risk assessment policy and investment policy. Essential requirements of management

accounting system are mention below:

Job costing system: This system is used to assigning cost to each product of the

company and then calculate and measuring cost of each order company receive free their

customer. Company use this system when their products are identical. Company make products

according to the demand of their customers (Cools, Stouthuysen and Van den Abbeele, 2017).

This system of managerial accounting helps in identifying market demand of customers and

useful in making and implementing decision of the company.

1

Management accounting is a branch of accounting which deals with managerial activities.

It is directly related to financial transactions but may have major impact in decision-making

related to such transactions (Commerford and et.al, 2016). Furthermore, it is used by the internal

management to take major decisions which can be implemented in the entity. The main purpose

of this is to help with proper administration of activities in a company. In this report, Rowlinson

Knitwear has been chosen which has its headquarter in United Kingdom. The assignment covers

explanation of management accounting along with essential requirements of different types,

different methods, application of marginal and absorption costing to calculate the costs,

advantages and disadvantages of types of planning tools for budgetary control and use of specific

examples for conducting comparison of management accounting systems.

P1. Explanation of management accounting together with essential requirements of different

types

Management accounting: It is a technique used by manager for the purpose of taking

decision by identifying, analysing, measuring and communicating essential financial

information. In other words it is a process of collecting essential financial information in order to

make plans and policies for the organisation. Management accounting also known as

“managerial accounting”. It is used by internal department of an organisation. The company use

various management accounting system in order to collecting necessary financial information of

each department of the company. These are the vital part of managerial accounting process,

theses system helps the organisation to record essential financial data of their daily basis

operational activities. Without using these system company never took decision regarding budget

policy risk assessment policy and investment policy. Essential requirements of management

accounting system are mention below:

Job costing system: This system is used to assigning cost to each product of the

company and then calculate and measuring cost of each order company receive free their

customer. Company use this system when their products are identical. Company make products

according to the demand of their customers (Cools, Stouthuysen and Van den Abbeele, 2017).

This system of managerial accounting helps in identifying market demand of customers and

useful in making and implementing decision of the company.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Price optimizing system:It is an essential system of management accounting. Manager

use this this system for analysing pricing policies of their rivalry industries and then make price

policies according to the stage of life cycle of an product. At initial stage they use penetration

pricing policy,company offer discount at initial stage. At boom stage they use skimming price

policy. Company use this system for the purpose of optimum utilization of their resource prices.

Cost accounting system: Company use this system for measuring cost of manufacturing

products and then calculating profitability rate of the entity. Job and process costing are the part

of cost accounting system. Cost accounting system is the essential part of managerial accounting

system,manager uses this system in making policies identifying risk and built risk assessment

policies,controlling cost, reduce wastage of products (Kastberg and Siverbo, 2016). This system

also helps in performance appraisal method. Company use this system for analysing capabilities

of their workforce.

Inventory management system: It is a tool which use software and hardware devices

for the purpose of maintaining stock level of the organisation. Company uses various technique

like EOQ ,LIFO,FIFO methods for identifying requirements of the company. The manager use

ABC analysis,JIT analysis,for the purpose of controlling wastage of stock within the

organisation. Inventory management system are useful in order to achieve optimum utilization of

resources, it helps in enhancing capabilities of works, save time and cost of

organisation ,provides goods to customer at their prescribe time.

P2. Different methods of management accounting reporting

Manager use management accounting reports for the purpose of making business level

strategies, taking decision and measuring performance of their workforce. Following are the

methods manager uses for making management accounting reports:

Budget reports: In this method organisation use to built budget reports in order to

analysis their workforce performance. Budget report is based on the collection of provisos data.

In this method managers set a target which must be fulfilled in prescribe time limit. After that

managers identifying differences of set target and achieve target and then make policies to

reduce the gap of current and budget target.

Account receivable ageing report: This is the most vital method of management

accounting policies. Management department made rigid credit policies to their customers. This

report is made to maintain cash flow and liquidity of the business entity. Management

2

use this this system for analysing pricing policies of their rivalry industries and then make price

policies according to the stage of life cycle of an product. At initial stage they use penetration

pricing policy,company offer discount at initial stage. At boom stage they use skimming price

policy. Company use this system for the purpose of optimum utilization of their resource prices.

Cost accounting system: Company use this system for measuring cost of manufacturing

products and then calculating profitability rate of the entity. Job and process costing are the part

of cost accounting system. Cost accounting system is the essential part of managerial accounting

system,manager uses this system in making policies identifying risk and built risk assessment

policies,controlling cost, reduce wastage of products (Kastberg and Siverbo, 2016). This system

also helps in performance appraisal method. Company use this system for analysing capabilities

of their workforce.

Inventory management system: It is a tool which use software and hardware devices

for the purpose of maintaining stock level of the organisation. Company uses various technique

like EOQ ,LIFO,FIFO methods for identifying requirements of the company. The manager use

ABC analysis,JIT analysis,for the purpose of controlling wastage of stock within the

organisation. Inventory management system are useful in order to achieve optimum utilization of

resources, it helps in enhancing capabilities of works, save time and cost of

organisation ,provides goods to customer at their prescribe time.

P2. Different methods of management accounting reporting

Manager use management accounting reports for the purpose of making business level

strategies, taking decision and measuring performance of their workforce. Following are the

methods manager uses for making management accounting reports:

Budget reports: In this method organisation use to built budget reports in order to

analysis their workforce performance. Budget report is based on the collection of provisos data.

In this method managers set a target which must be fulfilled in prescribe time limit. After that

managers identifying differences of set target and achieve target and then make policies to

reduce the gap of current and budget target.

Account receivable ageing report: This is the most vital method of management

accounting policies. Management department made rigid credit policies to their customers. This

report is made to maintain cash flow and liquidity of the business entity. Management

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

department made policies for those customers who did not give back payment of the company.

They should make those polices which charges fines and penalties to default customers. Only

after that an organisation can maintain their liquidity level (Qian, Hörisch and Schaltegger,

2018).

Job cost report:Organisation make job reports to calculate cost of overall process of

manufacturing each product within the entity. Job report is a summery of overall expense

incurred by an organisation. Managers use this report in analysing expenses of product and

making price policies regarding cost of product. Company uses this report in identifying their

profits.

Performance report:This is most essential method of managerial accounting report.

Performance report are made to identify the overall performance of organisation,which included

labour performance employees and employers performance also. Manager use this report for the

purpose of making incentive policies. Company gave rewards and recommendation to their

employees after reviewing their performance. This report is help in identifying low skilled

workforce within the organisation.

Inventory report: This report is prepair to maintain stock level of the organisation.

Inventory report is the summery of overall stock level of entity. It describes minimum,maximum

and dangerous level of products. Manager use this report to maintain stock of raw materiel and

finished goods of the company,so that organisation can provides good at prescribe time to their

customers.

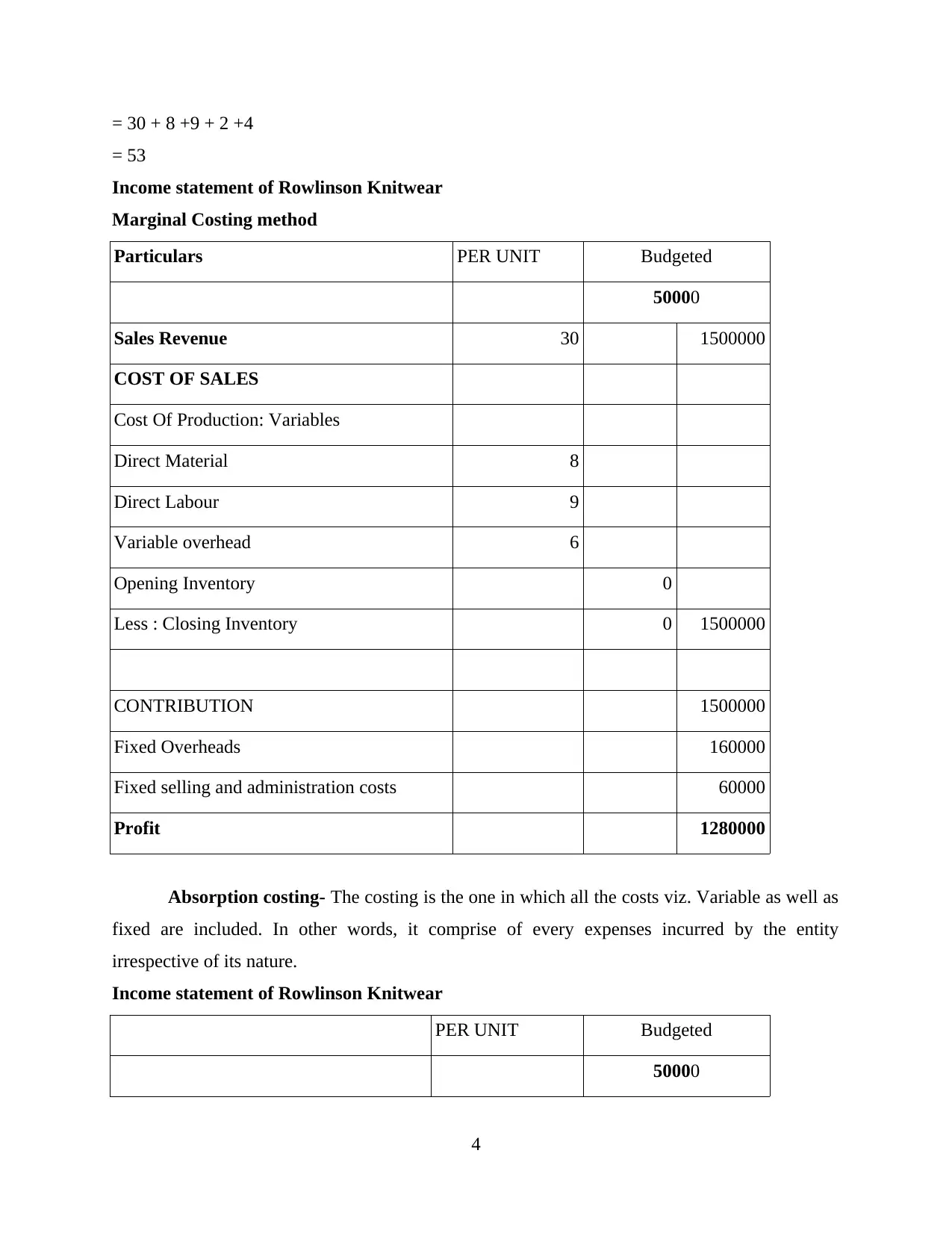

P3. Calculation of costs on the basis of marginal and absorption costing method

Marginal costing- This technique involves only the variable costs and fixed costs are

completely ignored. The cost is calculated by taking into account direct material, labour,

expenses and variable overheads (Saleem Salem Alzoubi, 2016).

Cost per unit:

Direct Material = 8

Direct Labour = 9

Variable overhead = 2

Variable expenses = 4

Total cost = Selling price + Direct material + Direct labour + Variable overhead + Variable

expenses

3

They should make those polices which charges fines and penalties to default customers. Only

after that an organisation can maintain their liquidity level (Qian, Hörisch and Schaltegger,

2018).

Job cost report:Organisation make job reports to calculate cost of overall process of

manufacturing each product within the entity. Job report is a summery of overall expense

incurred by an organisation. Managers use this report in analysing expenses of product and

making price policies regarding cost of product. Company uses this report in identifying their

profits.

Performance report:This is most essential method of managerial accounting report.

Performance report are made to identify the overall performance of organisation,which included

labour performance employees and employers performance also. Manager use this report for the

purpose of making incentive policies. Company gave rewards and recommendation to their

employees after reviewing their performance. This report is help in identifying low skilled

workforce within the organisation.

Inventory report: This report is prepair to maintain stock level of the organisation.

Inventory report is the summery of overall stock level of entity. It describes minimum,maximum

and dangerous level of products. Manager use this report to maintain stock of raw materiel and

finished goods of the company,so that organisation can provides good at prescribe time to their

customers.

P3. Calculation of costs on the basis of marginal and absorption costing method

Marginal costing- This technique involves only the variable costs and fixed costs are

completely ignored. The cost is calculated by taking into account direct material, labour,

expenses and variable overheads (Saleem Salem Alzoubi, 2016).

Cost per unit:

Direct Material = 8

Direct Labour = 9

Variable overhead = 2

Variable expenses = 4

Total cost = Selling price + Direct material + Direct labour + Variable overhead + Variable

expenses

3

= 30 + 8 +9 + 2 +4

= 53

Income statement of Rowlinson Knitwear

Marginal Costing method

Particulars PER UNIT Budgeted

50000

Sales Revenue 30 1500000

COST OF SALES

Cost Of Production: Variables

Direct Material 8

Direct Labour 9

Variable overhead 6

Opening Inventory 0

Less : Closing Inventory 0 1500000

CONTRIBUTION 1500000

Fixed Overheads 160000

Fixed selling and administration costs 60000

Profit 1280000

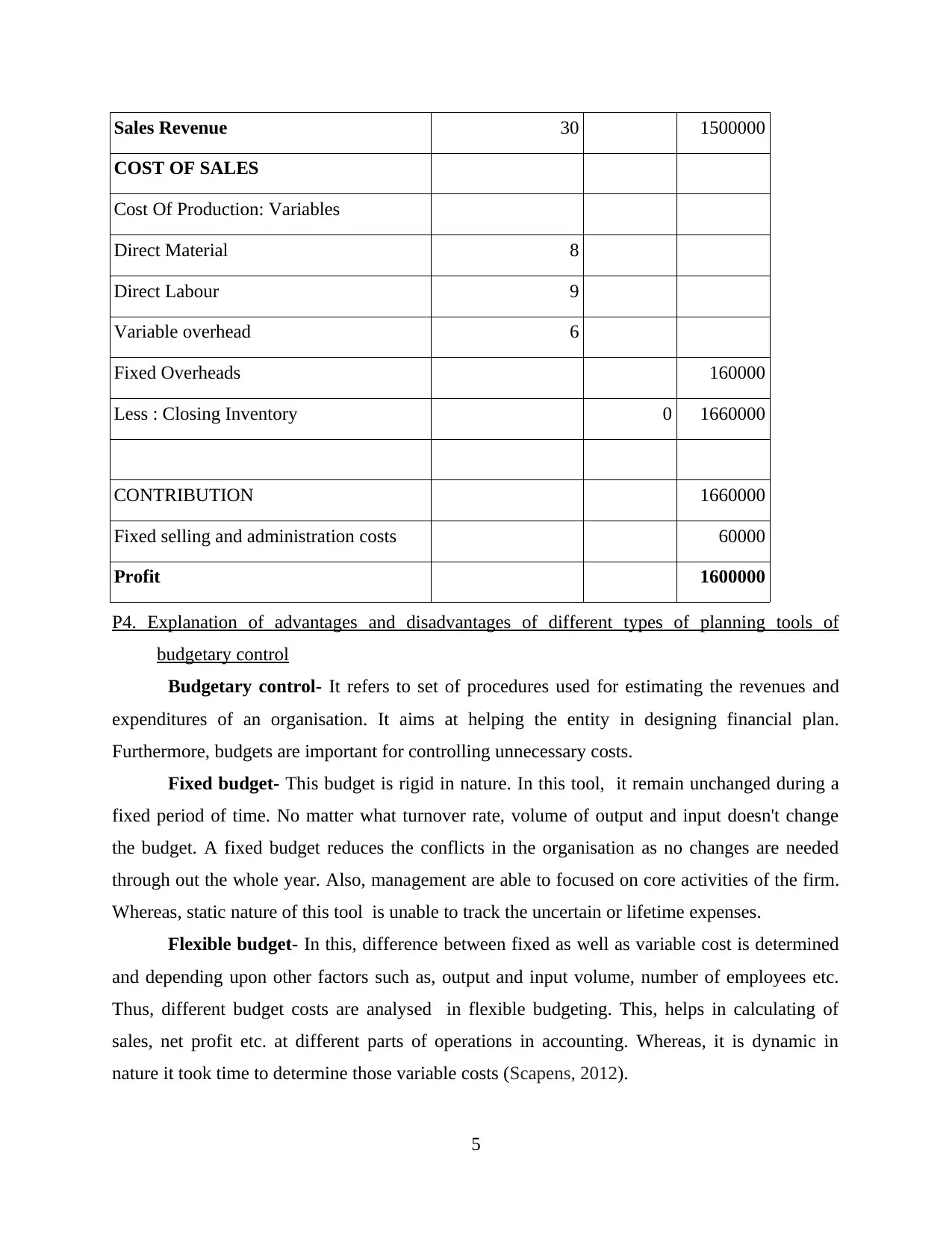

Absorption costing- The costing is the one in which all the costs viz. Variable as well as

fixed are included. In other words, it comprise of every expenses incurred by the entity

irrespective of its nature.

Income statement of Rowlinson Knitwear

PER UNIT Budgeted

50000

4

= 53

Income statement of Rowlinson Knitwear

Marginal Costing method

Particulars PER UNIT Budgeted

50000

Sales Revenue 30 1500000

COST OF SALES

Cost Of Production: Variables

Direct Material 8

Direct Labour 9

Variable overhead 6

Opening Inventory 0

Less : Closing Inventory 0 1500000

CONTRIBUTION 1500000

Fixed Overheads 160000

Fixed selling and administration costs 60000

Profit 1280000

Absorption costing- The costing is the one in which all the costs viz. Variable as well as

fixed are included. In other words, it comprise of every expenses incurred by the entity

irrespective of its nature.

Income statement of Rowlinson Knitwear

PER UNIT Budgeted

50000

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Sales Revenue 30 1500000

COST OF SALES

Cost Of Production: Variables

Direct Material 8

Direct Labour 9

Variable overhead 6

Fixed Overheads 160000

Less : Closing Inventory 0 1660000

CONTRIBUTION 1660000

Fixed selling and administration costs 60000

Profit 1600000

P4. Explanation of advantages and disadvantages of different types of planning tools of

budgetary control

Budgetary control- It refers to set of procedures used for estimating the revenues and

expenditures of an organisation. It aims at helping the entity in designing financial plan.

Furthermore, budgets are important for controlling unnecessary costs.

Fixed budget- This budget is rigid in nature. In this tool, it remain unchanged during a

fixed period of time. No matter what turnover rate, volume of output and input doesn't change

the budget. A fixed budget reduces the conflicts in the organisation as no changes are needed

through out the whole year. Also, management are able to focused on core activities of the firm.

Whereas, static nature of this tool is unable to track the uncertain or lifetime expenses.

Flexible budget- In this, difference between fixed as well as variable cost is determined

and depending upon other factors such as, output and input volume, number of employees etc.

Thus, different budget costs are analysed in flexible budgeting. This, helps in calculating of

sales, net profit etc. at different parts of operations in accounting. Whereas, it is dynamic in

nature it took time to determine those variable costs (Scapens, 2012).

5

COST OF SALES

Cost Of Production: Variables

Direct Material 8

Direct Labour 9

Variable overhead 6

Fixed Overheads 160000

Less : Closing Inventory 0 1660000

CONTRIBUTION 1660000

Fixed selling and administration costs 60000

Profit 1600000

P4. Explanation of advantages and disadvantages of different types of planning tools of

budgetary control

Budgetary control- It refers to set of procedures used for estimating the revenues and

expenditures of an organisation. It aims at helping the entity in designing financial plan.

Furthermore, budgets are important for controlling unnecessary costs.

Fixed budget- This budget is rigid in nature. In this tool, it remain unchanged during a

fixed period of time. No matter what turnover rate, volume of output and input doesn't change

the budget. A fixed budget reduces the conflicts in the organisation as no changes are needed

through out the whole year. Also, management are able to focused on core activities of the firm.

Whereas, static nature of this tool is unable to track the uncertain or lifetime expenses.

Flexible budget- In this, difference between fixed as well as variable cost is determined

and depending upon other factors such as, output and input volume, number of employees etc.

Thus, different budget costs are analysed in flexible budgeting. This, helps in calculating of

sales, net profit etc. at different parts of operations in accounting. Whereas, it is dynamic in

nature it took time to determine those variable costs (Scapens, 2012).

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Zero budget- It is the budgetary control in which the expenses for a new period should

be zero. In other words, the functions are carried from nil base which are take to a stage from

which an organisation can achieve the target. Also, there must be justification for every costs

which are being utilised in the company. In the context to Rowlinson Knitwear, it can use this

for starting a new project which may require all the costs to be zero.

P5. Use specific examples for a comparison of organisations in the context with management

accounting systems

Financial problem:It is a situation when companies are unable are unable to fulfil their

organisation needs due to lack of capital. Financial problem arise due to uncertainty in monetary

transaction (Youssef, 2013). Bad debts and high account payable ratio are main reason of

financial crises arises in company. Customers are not take initiatives to pay their money,thus

organisation could not collect money and this effect the account payable ration of the entity,due

to lack of capital and high interest rate policy of creditors. organisation cannot fulfil

requirements of their creditors and company suffers from financial problems. At present time

Rowlinson Knitwear is suffers from financial problem. Following are the methods to reduce their

financial problem:

Benchmarking : It is a technique of evaluation of performance appraisal. Benchmarking

is a process in which organisation compare their business practices and performance with their

rivalry industries. Management department compare quality, price,customer

satisfaction,performance level of their employees with other ones. Benchmarking is essential

technique of reducing financial problem of the company by setting target to achieve within fix

period of time.

Key performance indicator: It is method which are used managers to analysis how

effectively workforce of the entity performance in order to achieve organisation goals. This

technique helps in removing financial problem of the entity by reducing cost and other expensive

activities of organisation.

These problems can be resolved with the use of any of the above-mentioned technique so

that the issues can be resolved within the limited period. However, if key performance indicator

is being used, then there should be a company which has set the example (Windolph and

Moeller, 2012). The strategies of that company be set as standard for measuring the results of

Rowlinson Knitwear.

6

be zero. In other words, the functions are carried from nil base which are take to a stage from

which an organisation can achieve the target. Also, there must be justification for every costs

which are being utilised in the company. In the context to Rowlinson Knitwear, it can use this

for starting a new project which may require all the costs to be zero.

P5. Use specific examples for a comparison of organisations in the context with management

accounting systems

Financial problem:It is a situation when companies are unable are unable to fulfil their

organisation needs due to lack of capital. Financial problem arise due to uncertainty in monetary

transaction (Youssef, 2013). Bad debts and high account payable ratio are main reason of

financial crises arises in company. Customers are not take initiatives to pay their money,thus

organisation could not collect money and this effect the account payable ration of the entity,due

to lack of capital and high interest rate policy of creditors. organisation cannot fulfil

requirements of their creditors and company suffers from financial problems. At present time

Rowlinson Knitwear is suffers from financial problem. Following are the methods to reduce their

financial problem:

Benchmarking : It is a technique of evaluation of performance appraisal. Benchmarking

is a process in which organisation compare their business practices and performance with their

rivalry industries. Management department compare quality, price,customer

satisfaction,performance level of their employees with other ones. Benchmarking is essential

technique of reducing financial problem of the company by setting target to achieve within fix

period of time.

Key performance indicator: It is method which are used managers to analysis how

effectively workforce of the entity performance in order to achieve organisation goals. This

technique helps in removing financial problem of the entity by reducing cost and other expensive

activities of organisation.

These problems can be resolved with the use of any of the above-mentioned technique so

that the issues can be resolved within the limited period. However, if key performance indicator

is being used, then there should be a company which has set the example (Windolph and

Moeller, 2012). The strategies of that company be set as standard for measuring the results of

Rowlinson Knitwear.

6

CONCLUSION

From the above report, it has been concluded that management accounting is important

for the organisation for helping the management to make decisions which can be create positive

outcomes in the form of growth. Also, there are various methods in budgetary control which

should be used in controlling the unnecessary costs. Furthermore, management accounting

provides principles and reporting system which can be take into account.

7

From the above report, it has been concluded that management accounting is important

for the organisation for helping the management to make decisions which can be create positive

outcomes in the form of growth. Also, there are various methods in budgetary control which

should be used in controlling the unnecessary costs. Furthermore, management accounting

provides principles and reporting system which can be take into account.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books & Journals:

Commerford, B. P. and et.al, 2016. Real earnings management: A threat to auditor

comfort?. Auditing: A Journal of Practice & Theory. 35(4). pp.39-56.

Cools, M., Stouthuysen, K. and Van den Abbeele, A., 2017. Management control for stimulating

different types of creativity: The role of budgets. Journal of Management Accounting

Research. 29(3). pp.1-21.

Kastberg, G. and Siverbo, S., 2016. The role of management accounting and control in making

professional organizations horizontal. Accounting, Auditing & Accountability Journal.

Qian, W., Hörisch, J. and Schaltegger, S., 2018. Environmental management accounting and its

effects on carbon management and disclosure quality. Journal of cleaner production.

174. pp.1608-1619.

Saleem Salem Alzoubi, E., 2016. Ownership structure and earnings management: evidence from

Jordan. International Journal of Accounting & Information Management. 24(2). pp.135-

161.

Scapens, R. W., 2012. How important is practice-relevant management accounting

research?. Qualitative Research in Accounting & Management.

Windolph, M. and Moeller, K., 2012. Open-book accounting: Reason for failure of inter-firm

cooperation?. Management Accounting Research. 23(1). pp.47-60.

Youssef, M. A., 2013. Management accounting change in an Egyptian organization: an

institutional analysis. Journal of Accounting & Organizational Change.

8

Books & Journals:

Commerford, B. P. and et.al, 2016. Real earnings management: A threat to auditor

comfort?. Auditing: A Journal of Practice & Theory. 35(4). pp.39-56.

Cools, M., Stouthuysen, K. and Van den Abbeele, A., 2017. Management control for stimulating

different types of creativity: The role of budgets. Journal of Management Accounting

Research. 29(3). pp.1-21.

Kastberg, G. and Siverbo, S., 2016. The role of management accounting and control in making

professional organizations horizontal. Accounting, Auditing & Accountability Journal.

Qian, W., Hörisch, J. and Schaltegger, S., 2018. Environmental management accounting and its

effects on carbon management and disclosure quality. Journal of cleaner production.

174. pp.1608-1619.

Saleem Salem Alzoubi, E., 2016. Ownership structure and earnings management: evidence from

Jordan. International Journal of Accounting & Information Management. 24(2). pp.135-

161.

Scapens, R. W., 2012. How important is practice-relevant management accounting

research?. Qualitative Research in Accounting & Management.

Windolph, M. and Moeller, K., 2012. Open-book accounting: Reason for failure of inter-firm

cooperation?. Management Accounting Research. 23(1). pp.47-60.

Youssef, M. A., 2013. Management accounting change in an Egyptian organization: an

institutional analysis. Journal of Accounting & Organizational Change.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

9

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.