HNC Business: Management Accounting Report - Costing and Planning

VerifiedAdded on 2022/08/14

|12

|3658

|20

Report

AI Summary

This report provides a detailed analysis of management accounting principles and their application within a business context. It begins with an introduction to management accounting systems, their requirements, and the benefits they offer, including inventory management, cost accounting, and job costing systems. The report then explores various management accounting reporting methods, such as cost reports, performance reports, and variance reports, along with their integration. A significant portion of the report is dedicated to the calculation of costs using absorption and marginal costing methods, including the preparation of income statements and the determination of breakeven units. Variance analysis is also discussed, highlighting the importance of identifying and addressing deviations from the budget. Furthermore, the report examines different planning tools and their application in budgetary control, emphasizing the advantages of a well-structured budget. Finally, it addresses the use of management accounting systems to respond to financial problems, providing a comprehensive understanding of the subject matter. The report concludes with a summary of the key findings and includes a list of references for further study.

1

Management accounting

Management accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Table of Contents

Introduction................................................................................................................................3

Task 1.........................................................................................................................................3

Requirement of Management accounting systems and their benefits....................................3

Various Management accounting reporting...........................................................................4

Integration of management accounting system and reports...................................................5

Task 2.........................................................................................................................................5

Calculation of cost using absorption and marginal costing...................................................5

Calculation of breakeven units...............................................................................................7

Variance analysis...................................................................................................................7

Task 3.........................................................................................................................................8

Different planning tools and their application in budgetary control......................................8

Task 4.........................................................................................................................................9

Use of management accounting systems to respond to financial problems...........................9

Conclusion................................................................................................................................10

References................................................................................................................................11

Table of Contents

Introduction................................................................................................................................3

Task 1.........................................................................................................................................3

Requirement of Management accounting systems and their benefits....................................3

Various Management accounting reporting...........................................................................4

Integration of management accounting system and reports...................................................5

Task 2.........................................................................................................................................5

Calculation of cost using absorption and marginal costing...................................................5

Calculation of breakeven units...............................................................................................7

Variance analysis...................................................................................................................7

Task 3.........................................................................................................................................8

Different planning tools and their application in budgetary control......................................8

Task 4.........................................................................................................................................9

Use of management accounting systems to respond to financial problems...........................9

Conclusion................................................................................................................................10

References................................................................................................................................11

3

Introduction

In the business there is requirement for proper accounting and in that there will be a recording

of all the events which are taking place. Management accounting is a tool which includes

collection, recording, and interpretation of the information will be made possible. In this,

there are various aspects that need to be understood and they will be considered in the report

below. There are various types of management accounting systems that are involved in this

process and they will be discussed with the importance of the same. The reports are made in

the process and various types of reports will be identified in the report. The calculation will

be made by using marginal and absorption costing and the total cost which is involved will be

ascertained. There will be the determination of the breakeven point and the variance analysis

is to be discussed. There are several planning tools that are involved in the budgetary control

process and they will be taken into consideration. The manner in which management

accounting systems help in dealing with the financial tools will also be discussed by which

the required understanding will be gained.

Task 1

A requirement of Management accounting systems and its benefits

The operations are required to be performed in a business and this will be done in manner

that all the business objectives are fulfilled. In addition to the financial accounting, there will

be carrying out of the management accounting in which all the financial and non-financial

elements will be considered (Arroyo, 2012). There will be the use of all the information

which is involved in relation to the business. In this process there are various systems that are

involved and an understanding of them shall be obtained by which the benefits which are

gained with them can be identified.

Inventory management system: There is a need for the business to manage the inventory in an

adequate manner and for that this system is used. There is the stock maintenance and it

should be appropriate otherwise the funds will be blocked. The level of inventory that shall

be maintained will be considered and then the final decisions will be made accordingly. The

balance of the inventory will be valued with the help of the appropriate method and that

decision about the FIFO and other available methods will be made (Chenhall, 2012). This is

beneficial as the inventory management will be improved and cost will be controlled.

Introduction

In the business there is requirement for proper accounting and in that there will be a recording

of all the events which are taking place. Management accounting is a tool which includes

collection, recording, and interpretation of the information will be made possible. In this,

there are various aspects that need to be understood and they will be considered in the report

below. There are various types of management accounting systems that are involved in this

process and they will be discussed with the importance of the same. The reports are made in

the process and various types of reports will be identified in the report. The calculation will

be made by using marginal and absorption costing and the total cost which is involved will be

ascertained. There will be the determination of the breakeven point and the variance analysis

is to be discussed. There are several planning tools that are involved in the budgetary control

process and they will be taken into consideration. The manner in which management

accounting systems help in dealing with the financial tools will also be discussed by which

the required understanding will be gained.

Task 1

A requirement of Management accounting systems and its benefits

The operations are required to be performed in a business and this will be done in manner

that all the business objectives are fulfilled. In addition to the financial accounting, there will

be carrying out of the management accounting in which all the financial and non-financial

elements will be considered (Arroyo, 2012). There will be the use of all the information

which is involved in relation to the business. In this process there are various systems that are

involved and an understanding of them shall be obtained by which the benefits which are

gained with them can be identified.

Inventory management system: There is a need for the business to manage the inventory in an

adequate manner and for that this system is used. There is the stock maintenance and it

should be appropriate otherwise the funds will be blocked. The level of inventory that shall

be maintained will be considered and then the final decisions will be made accordingly. The

balance of the inventory will be valued with the help of the appropriate method and that

decision about the FIFO and other available methods will be made (Chenhall, 2012). This is

beneficial as the inventory management will be improved and cost will be controlled.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

Cost accounting system: The cost which is involved in the business shall be identified so that

proper recording in that respect can be made. There will be cost ascertainment and then that

will be classified in a proper manner. There are fixed and variable costs that are involved and

it is required that proper classification shall be made among them. The cost will be

ascertained and in that proper method will be used which will be involving the standard

costing, normal costing and actual costing (Maas, Schaltegger and Crutzen, 2016). This will

be helping in taking further decisions such as pricing decisions that are based on cost.

Job costing system: In the manufacturing business various jobs are involved which are

carried and there is the need to identify them (Drury, 2015). The cost which is associated with

them will be ascertained and that will help in managing the cost appropriately and also the

allocation will be made in the required manner.

Various Management accounting reporting

The information that is present in the company shall be taken into account for the reporting

purpose in an adequate manner and for that various reports are prescribed which are used.

With the help of this, the collected information will be reported adequately and will be used

by all the parties for several processes (Edmonds and Olds, 2013). The explanation of various

reports is provided by which the required knowledge will be gained.

Cost report: The cost-related data which is collected will be considered in preparing this

report. The information will be available in one place with this report and that will be used in

making the required decisions (Hiebl, 2014). The proper evaluation of cost will be made and

with that, the control will be established on the same. The benefit of the reduced cost will be

attained in the form of increased profits.

Performance reports: It is necessary that the performance shall be maintained in the business

and for that, there are various performance metrics that will be used. They all will be

specified in this report by which all the staff members will be having an idea about the targets

which are to be met by them (Seal et al., 2014). This will be improving their efficiency as the

motivation will be involved and every employee will try to perform better.

Variance report: The budget is made and it is required that they are followed in an adequate

manner. In actual the performance which is made deviates from the budgeted values and for

that variance report is prepared. In that, all the deviations which are involved will be

Cost accounting system: The cost which is involved in the business shall be identified so that

proper recording in that respect can be made. There will be cost ascertainment and then that

will be classified in a proper manner. There are fixed and variable costs that are involved and

it is required that proper classification shall be made among them. The cost will be

ascertained and in that proper method will be used which will be involving the standard

costing, normal costing and actual costing (Maas, Schaltegger and Crutzen, 2016). This will

be helping in taking further decisions such as pricing decisions that are based on cost.

Job costing system: In the manufacturing business various jobs are involved which are

carried and there is the need to identify them (Drury, 2015). The cost which is associated with

them will be ascertained and that will help in managing the cost appropriately and also the

allocation will be made in the required manner.

Various Management accounting reporting

The information that is present in the company shall be taken into account for the reporting

purpose in an adequate manner and for that various reports are prescribed which are used.

With the help of this, the collected information will be reported adequately and will be used

by all the parties for several processes (Edmonds and Olds, 2013). The explanation of various

reports is provided by which the required knowledge will be gained.

Cost report: The cost-related data which is collected will be considered in preparing this

report. The information will be available in one place with this report and that will be used in

making the required decisions (Hiebl, 2014). The proper evaluation of cost will be made and

with that, the control will be established on the same. The benefit of the reduced cost will be

attained in the form of increased profits.

Performance reports: It is necessary that the performance shall be maintained in the business

and for that, there are various performance metrics that will be used. They all will be

specified in this report by which all the staff members will be having an idea about the targets

which are to be met by them (Seal et al., 2014). This will be improving their efficiency as the

motivation will be involved and every employee will try to perform better.

Variance report: The budget is made and it is required that they are followed in an adequate

manner. In actual the performance which is made deviates from the budgeted values and for

that variance report is prepared. In that, all the deviations which are involved will be

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

identified and with that, the reason for the same will also be determined (Fullerton, Kennedy

and Widener, 2013). This will help the business in dealing with the situation as the changes

will be incorporated in the plans which will be made further.

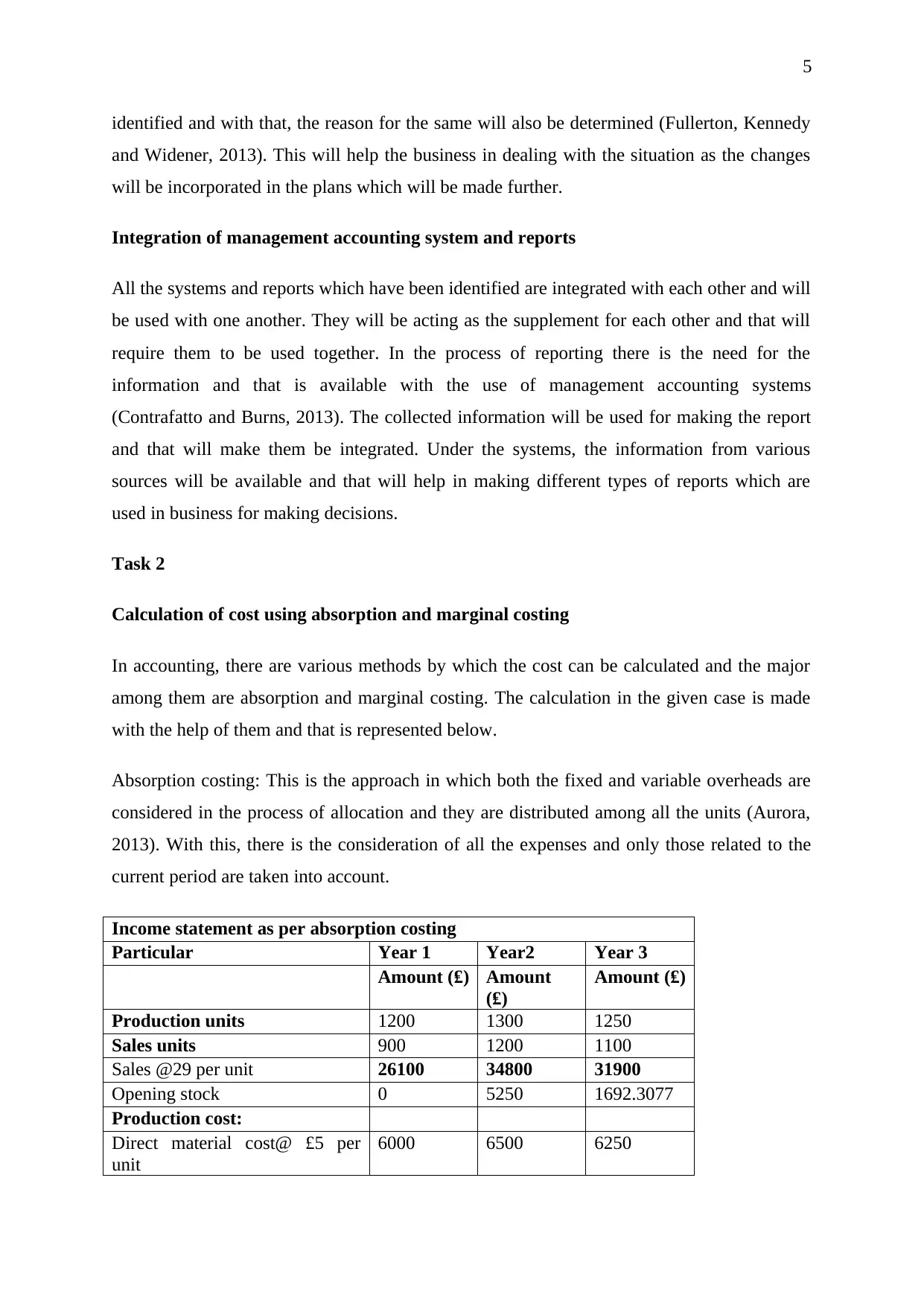

Integration of management accounting system and reports

All the systems and reports which have been identified are integrated with each other and will

be used with one another. They will be acting as the supplement for each other and that will

require them to be used together. In the process of reporting there is the need for the

information and that is available with the use of management accounting systems

(Contrafatto and Burns, 2013). The collected information will be used for making the report

and that will make them be integrated. Under the systems, the information from various

sources will be available and that will help in making different types of reports which are

used in business for making decisions.

Task 2

Calculation of cost using absorption and marginal costing

In accounting, there are various methods by which the cost can be calculated and the major

among them are absorption and marginal costing. The calculation in the given case is made

with the help of them and that is represented below.

Absorption costing: This is the approach in which both the fixed and variable overheads are

considered in the process of allocation and they are distributed among all the units (Aurora,

2013). With this, there is the consideration of all the expenses and only those related to the

current period are taken into account.

Income statement as per absorption costing

Particular Year 1 Year2 Year 3

Amount (₤) Amount

(₤)

Amount (₤)

Production units 1200 1300 1250

Sales units 900 1200 1100

Sales @29 per unit 26100 34800 31900

Opening stock 0 5250 1692.3077

Production cost:

Direct material cost@ £5 per

unit

6000 6500 6250

identified and with that, the reason for the same will also be determined (Fullerton, Kennedy

and Widener, 2013). This will help the business in dealing with the situation as the changes

will be incorporated in the plans which will be made further.

Integration of management accounting system and reports

All the systems and reports which have been identified are integrated with each other and will

be used with one another. They will be acting as the supplement for each other and that will

require them to be used together. In the process of reporting there is the need for the

information and that is available with the use of management accounting systems

(Contrafatto and Burns, 2013). The collected information will be used for making the report

and that will make them be integrated. Under the systems, the information from various

sources will be available and that will help in making different types of reports which are

used in business for making decisions.

Task 2

Calculation of cost using absorption and marginal costing

In accounting, there are various methods by which the cost can be calculated and the major

among them are absorption and marginal costing. The calculation in the given case is made

with the help of them and that is represented below.

Absorption costing: This is the approach in which both the fixed and variable overheads are

considered in the process of allocation and they are distributed among all the units (Aurora,

2013). With this, there is the consideration of all the expenses and only those related to the

current period are taken into account.

Income statement as per absorption costing

Particular Year 1 Year2 Year 3

Amount (₤) Amount

(₤)

Amount (₤)

Production units 1200 1300 1250

Sales units 900 1200 1100

Sales @29 per unit 26100 34800 31900

Opening stock 0 5250 1692.3077

Production cost:

Direct material cost@ £5 per

unit

6000 6500 6250

6

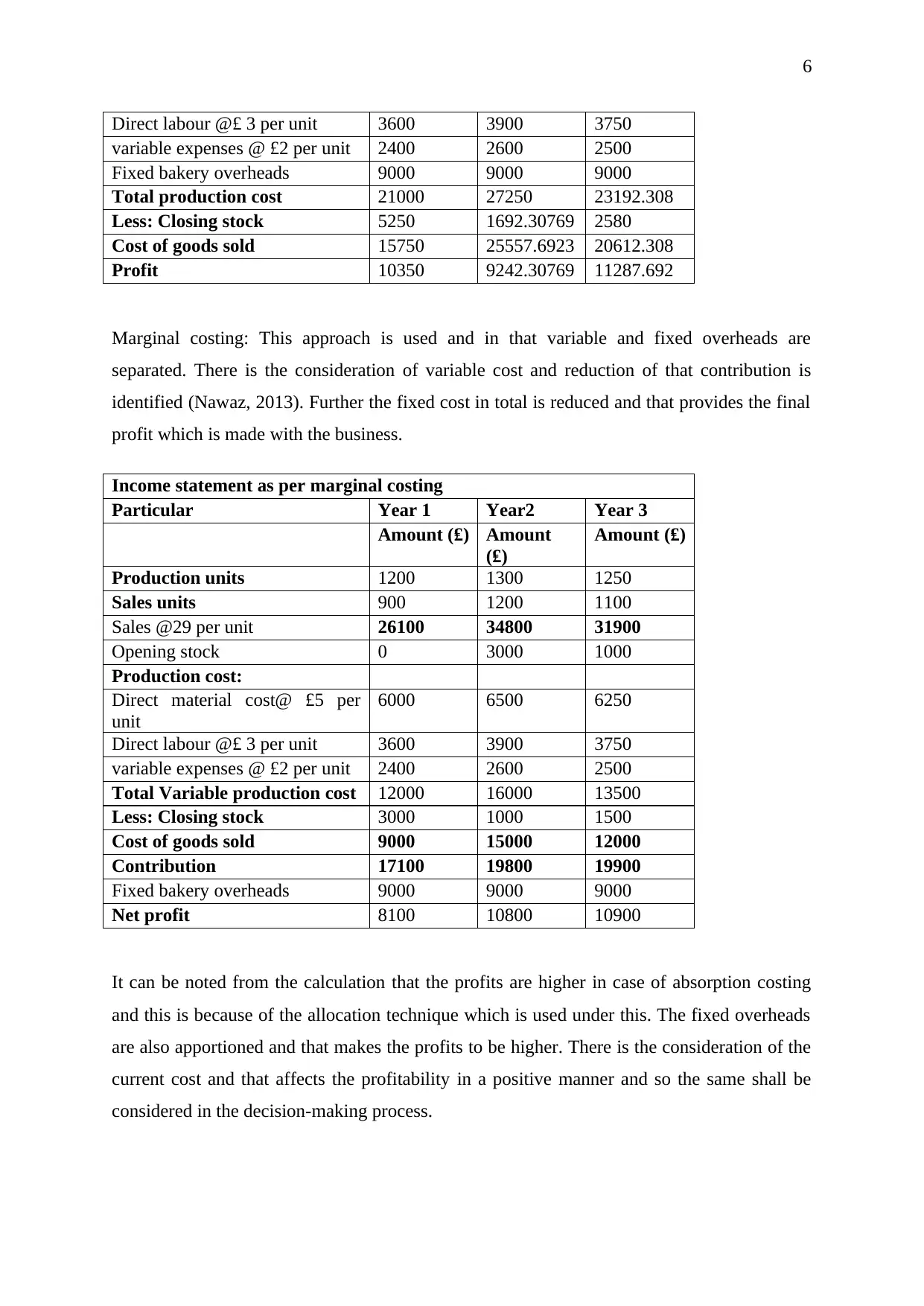

Direct labour @£ 3 per unit 3600 3900 3750

variable expenses @ £2 per unit 2400 2600 2500

Fixed bakery overheads 9000 9000 9000

Total production cost 21000 27250 23192.308

Less: Closing stock 5250 1692.30769 2580

Cost of goods sold 15750 25557.6923 20612.308

Profit 10350 9242.30769 11287.692

Marginal costing: This approach is used and in that variable and fixed overheads are

separated. There is the consideration of variable cost and reduction of that contribution is

identified (Nawaz, 2013). Further the fixed cost in total is reduced and that provides the final

profit which is made with the business.

Income statement as per marginal costing

Particular Year 1 Year2 Year 3

Amount (₤) Amount

(₤)

Amount (₤)

Production units 1200 1300 1250

Sales units 900 1200 1100

Sales @29 per unit 26100 34800 31900

Opening stock 0 3000 1000

Production cost:

Direct material cost@ £5 per

unit

6000 6500 6250

Direct labour @£ 3 per unit 3600 3900 3750

variable expenses @ £2 per unit 2400 2600 2500

Total Variable production cost 12000 16000 13500

Less: Closing stock 3000 1000 1500

Cost of goods sold 9000 15000 12000

Contribution 17100 19800 19900

Fixed bakery overheads 9000 9000 9000

Net profit 8100 10800 10900

It can be noted from the calculation that the profits are higher in case of absorption costing

and this is because of the allocation technique which is used under this. The fixed overheads

are also apportioned and that makes the profits to be higher. There is the consideration of the

current cost and that affects the profitability in a positive manner and so the same shall be

considered in the decision-making process.

Direct labour @£ 3 per unit 3600 3900 3750

variable expenses @ £2 per unit 2400 2600 2500

Fixed bakery overheads 9000 9000 9000

Total production cost 21000 27250 23192.308

Less: Closing stock 5250 1692.30769 2580

Cost of goods sold 15750 25557.6923 20612.308

Profit 10350 9242.30769 11287.692

Marginal costing: This approach is used and in that variable and fixed overheads are

separated. There is the consideration of variable cost and reduction of that contribution is

identified (Nawaz, 2013). Further the fixed cost in total is reduced and that provides the final

profit which is made with the business.

Income statement as per marginal costing

Particular Year 1 Year2 Year 3

Amount (₤) Amount

(₤)

Amount (₤)

Production units 1200 1300 1250

Sales units 900 1200 1100

Sales @29 per unit 26100 34800 31900

Opening stock 0 3000 1000

Production cost:

Direct material cost@ £5 per

unit

6000 6500 6250

Direct labour @£ 3 per unit 3600 3900 3750

variable expenses @ £2 per unit 2400 2600 2500

Total Variable production cost 12000 16000 13500

Less: Closing stock 3000 1000 1500

Cost of goods sold 9000 15000 12000

Contribution 17100 19800 19900

Fixed bakery overheads 9000 9000 9000

Net profit 8100 10800 10900

It can be noted from the calculation that the profits are higher in case of absorption costing

and this is because of the allocation technique which is used under this. The fixed overheads

are also apportioned and that makes the profits to be higher. There is the consideration of the

current cost and that affects the profitability in a positive manner and so the same shall be

considered in the decision-making process.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

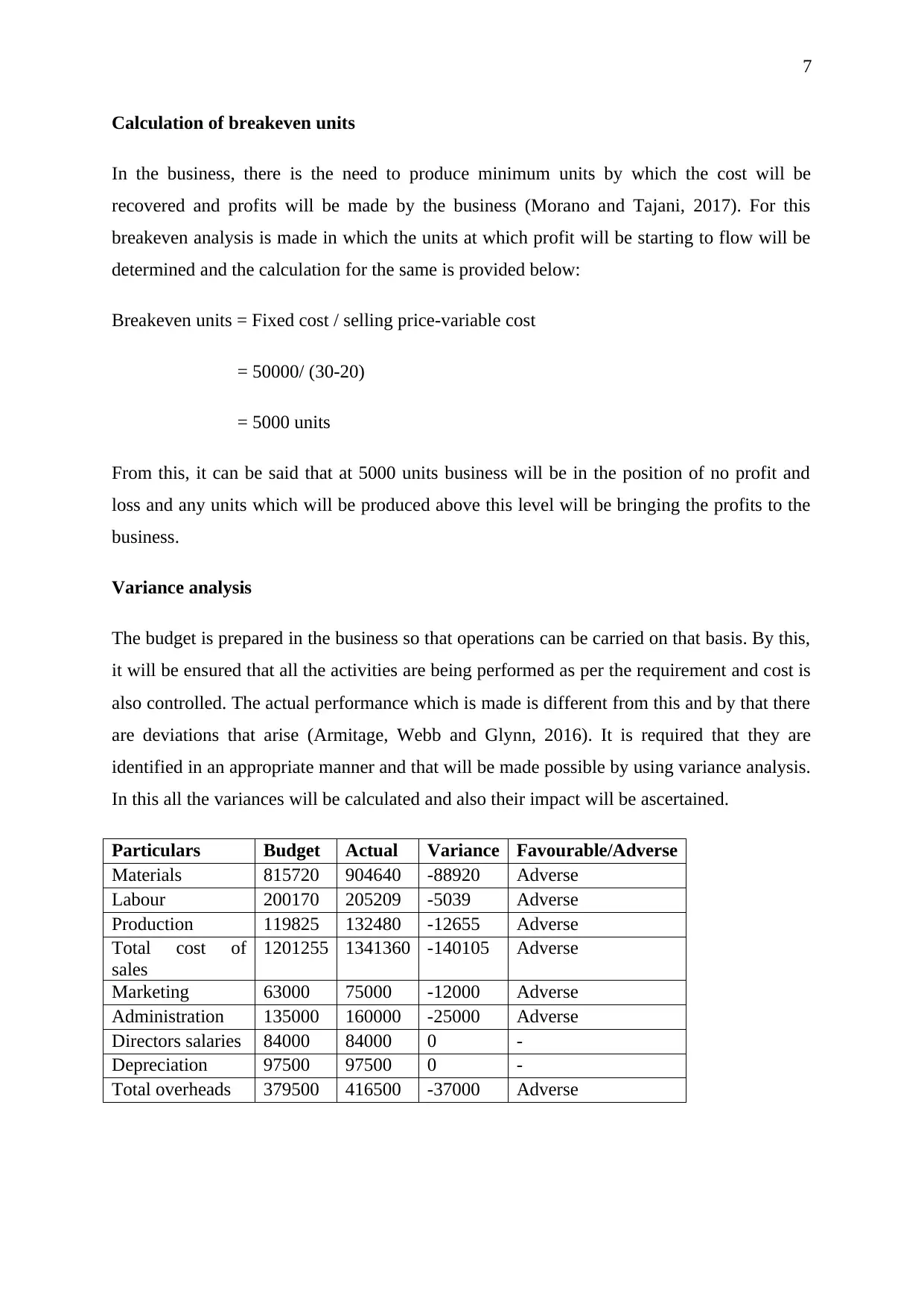

Calculation of breakeven units

In the business, there is the need to produce minimum units by which the cost will be

recovered and profits will be made by the business (Morano and Tajani, 2017). For this

breakeven analysis is made in which the units at which profit will be starting to flow will be

determined and the calculation for the same is provided below:

Breakeven units = Fixed cost / selling price-variable cost

= 50000/ (30-20)

= 5000 units

From this, it can be said that at 5000 units business will be in the position of no profit and

loss and any units which will be produced above this level will be bringing the profits to the

business.

Variance analysis

The budget is prepared in the business so that operations can be carried on that basis. By this,

it will be ensured that all the activities are being performed as per the requirement and cost is

also controlled. The actual performance which is made is different from this and by that there

are deviations that arise (Armitage, Webb and Glynn, 2016). It is required that they are

identified in an appropriate manner and that will be made possible by using variance analysis.

In this all the variances will be calculated and also their impact will be ascertained.

Particulars Budget Actual Variance Favourable/Adverse

Materials 815720 904640 -88920 Adverse

Labour 200170 205209 -5039 Adverse

Production 119825 132480 -12655 Adverse

Total cost of

sales

1201255 1341360 -140105 Adverse

Marketing 63000 75000 -12000 Adverse

Administration 135000 160000 -25000 Adverse

Directors salaries 84000 84000 0 -

Depreciation 97500 97500 0 -

Total overheads 379500 416500 -37000 Adverse

Calculation of breakeven units

In the business, there is the need to produce minimum units by which the cost will be

recovered and profits will be made by the business (Morano and Tajani, 2017). For this

breakeven analysis is made in which the units at which profit will be starting to flow will be

determined and the calculation for the same is provided below:

Breakeven units = Fixed cost / selling price-variable cost

= 50000/ (30-20)

= 5000 units

From this, it can be said that at 5000 units business will be in the position of no profit and

loss and any units which will be produced above this level will be bringing the profits to the

business.

Variance analysis

The budget is prepared in the business so that operations can be carried on that basis. By this,

it will be ensured that all the activities are being performed as per the requirement and cost is

also controlled. The actual performance which is made is different from this and by that there

are deviations that arise (Armitage, Webb and Glynn, 2016). It is required that they are

identified in an appropriate manner and that will be made possible by using variance analysis.

In this all the variances will be calculated and also their impact will be ascertained.

Particulars Budget Actual Variance Favourable/Adverse

Materials 815720 904640 -88920 Adverse

Labour 200170 205209 -5039 Adverse

Production 119825 132480 -12655 Adverse

Total cost of

sales

1201255 1341360 -140105 Adverse

Marketing 63000 75000 -12000 Adverse

Administration 135000 160000 -25000 Adverse

Directors salaries 84000 84000 0 -

Depreciation 97500 97500 0 -

Total overheads 379500 416500 -37000 Adverse

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

Task 3

Different planning tools and their application in budgetary control

In the budget-making, there are various aspects that need to be considered and with that

several tools are used. The budgets set the target which is to be achieved by the company and

by that performance improvement is made (Adongo and Jagongo, 2013). All the costs which

will be incurred are identified and this helps in controlling them as all the irrelevant activities

will be eliminated. There are various advantage and disadvantages which will be involved

with this and they are described below:

Advantages:

There will be proper work allocation which will be made under budget and that helps in

making the appropriate delegation of all the responsibilities.

There will be a proper cost plan which will be made and the waste which is made will be

eliminated. By this cost reduction will be made possible which is highly required in any

business.

The undertaking of the operations will be made in such manner that the effectiveness and

efficiency will be increased. This will improve the quality and a higher level of

satisfaction will be maintained.

The communication process will be improved as the making of the budget will involve

various departments and communication among them will be established.

Disadvantages:

The budget requires timely updates to deal with all the changes and this is not possible for

the business to update the budget on a frequent basis.

There are various assumptions and estimates which are involved in the making of the

budget and so complete reliance cannot be placed on them.

There is a high cost which is involved in making the budget as research is to be carried

and by that overall expenses of the business are raised.

The budgets are prepared in various forms and they are as follows:

Zero-based budgeting: This is the budget in which no historical data is used and all the

information is collected from the starting point. In this complete research is made and by that

Task 3

Different planning tools and their application in budgetary control

In the budget-making, there are various aspects that need to be considered and with that

several tools are used. The budgets set the target which is to be achieved by the company and

by that performance improvement is made (Adongo and Jagongo, 2013). All the costs which

will be incurred are identified and this helps in controlling them as all the irrelevant activities

will be eliminated. There are various advantage and disadvantages which will be involved

with this and they are described below:

Advantages:

There will be proper work allocation which will be made under budget and that helps in

making the appropriate delegation of all the responsibilities.

There will be a proper cost plan which will be made and the waste which is made will be

eliminated. By this cost reduction will be made possible which is highly required in any

business.

The undertaking of the operations will be made in such manner that the effectiveness and

efficiency will be increased. This will improve the quality and a higher level of

satisfaction will be maintained.

The communication process will be improved as the making of the budget will involve

various departments and communication among them will be established.

Disadvantages:

The budget requires timely updates to deal with all the changes and this is not possible for

the business to update the budget on a frequent basis.

There are various assumptions and estimates which are involved in the making of the

budget and so complete reliance cannot be placed on them.

There is a high cost which is involved in making the budget as research is to be carried

and by that overall expenses of the business are raised.

The budgets are prepared in various forms and they are as follows:

Zero-based budgeting: This is the budget in which no historical data is used and all the

information is collected from the starting point. In this complete research is made and by that

9

the workload is increased together with the cost (Glass, Stefanova and Prinzivalli, 2014). As

there will be new data so the chances of using wrong information are not involved and there

is a proper budget that is formulated. There will be the use of the relevant information and by

that better results will be attained.

Master budget: This is also an important tool in making a budget as under this all the aspects

and areas of the business are considered. There is the incorporation of all the elements in

making this budget and by that proper control on all the transactions is made which will help

in improving the overall of the business.

Variance analysis budget: Under the variances which are involved in the budget are identified

and then the budget is prepared accordingly. This is made in order to reduce the cost which is

involved as all the deviations will be identified and also the main cause of the same will be

ascertained. There will be proper corrective actions that will be designed and by that the

situation will be improved by the elimination of deviations.

Task 4

Use of management accounting systems to respond to financial problems

In the carrying of all the activities and operations in business, there are several issues that are

faced and it is required that they are eliminated effectively. Several management accounting

systems that are used and they also help in resolving the problems which are faced. There is a

proper collection of information that helps in taking the action to remove the problem. The

various aspects are involved and they will be resolved in the manner prescribed below.

Key-performance indicators: There is a need to maintain the performance in the business so

that all the problems can be resolved. This will be done with the help of setting parameters

that will be used to perform the task. Key performance indicators are such elements that are

set and on that basis, the performance is evaluated (Neiger et al., 2012). The employees will

be performing the task in a manner that they are able to accomplish the indicator and can

prove themselves. This will increase the success rate and problems will be resolved.

Benchmarking: There are various standards that are required to be met and they are identified

as the benchmarks. In this other company or industry is taken as the benchmark and standards

are set accordingly. All the employees are informed about the same and the will be

the workload is increased together with the cost (Glass, Stefanova and Prinzivalli, 2014). As

there will be new data so the chances of using wrong information are not involved and there

is a proper budget that is formulated. There will be the use of the relevant information and by

that better results will be attained.

Master budget: This is also an important tool in making a budget as under this all the aspects

and areas of the business are considered. There is the incorporation of all the elements in

making this budget and by that proper control on all the transactions is made which will help

in improving the overall of the business.

Variance analysis budget: Under the variances which are involved in the budget are identified

and then the budget is prepared accordingly. This is made in order to reduce the cost which is

involved as all the deviations will be identified and also the main cause of the same will be

ascertained. There will be proper corrective actions that will be designed and by that the

situation will be improved by the elimination of deviations.

Task 4

Use of management accounting systems to respond to financial problems

In the carrying of all the activities and operations in business, there are several issues that are

faced and it is required that they are eliminated effectively. Several management accounting

systems that are used and they also help in resolving the problems which are faced. There is a

proper collection of information that helps in taking the action to remove the problem. The

various aspects are involved and they will be resolved in the manner prescribed below.

Key-performance indicators: There is a need to maintain the performance in the business so

that all the problems can be resolved. This will be done with the help of setting parameters

that will be used to perform the task. Key performance indicators are such elements that are

set and on that basis, the performance is evaluated (Neiger et al., 2012). The employees will

be performing the task in a manner that they are able to accomplish the indicator and can

prove themselves. This will increase the success rate and problems will be resolved.

Benchmarking: There are various standards that are required to be met and they are identified

as the benchmarks. In this other company or industry is taken as the benchmark and standards

are set accordingly. All the employees are informed about the same and the will be

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

performing to make the position better than those standards (Hatem et al., 2013). The

performance will be evaluated against those benchmarks and the shortcomings which are

involved will be eliminated.

Variance analysis: The deviations which are involved in the actual and budgeted performance

are identified under this. By this corrective measures are taken and that helps in removing the

deviations in the coming period. The budget is made by incorporating all the correction

elements and by that it is ensured that the current problem will not arise again.

Conclusion

The report that is presented above elucidates that there is a need for the business to consider

management accounting. It is an important process which shall be followed and various

aspects and methods which are involved with this shall also be considered. With the help of

this, the position is improved and there is the attainment of sustainable success which is

necessary for business. The various management accounting systems and reports which are

involved in the business have been identified and the manner in which they are integrated has

also been taken into account. There are various calculations that are made under the

absorption and marginal costing by which the concept involved is understood. The cost is

identified and also the profitability which is involved is ascertained. There is the

determination of breakeven point and variance analysis has also been used. With them, the

results are obtained that help management in taking the required actions. The different

planning tools which are involved in budgetary control have been considered and proper

explanation in relation to them has been provided. In that, all the advantages and

disadvantages associated with them have been involved. The resolution of financial problems

with the management accounting systems has been determined in the report in an appropriate

manner.

performing to make the position better than those standards (Hatem et al., 2013). The

performance will be evaluated against those benchmarks and the shortcomings which are

involved will be eliminated.

Variance analysis: The deviations which are involved in the actual and budgeted performance

are identified under this. By this corrective measures are taken and that helps in removing the

deviations in the coming period. The budget is made by incorporating all the correction

elements and by that it is ensured that the current problem will not arise again.

Conclusion

The report that is presented above elucidates that there is a need for the business to consider

management accounting. It is an important process which shall be followed and various

aspects and methods which are involved with this shall also be considered. With the help of

this, the position is improved and there is the attainment of sustainable success which is

necessary for business. The various management accounting systems and reports which are

involved in the business have been identified and the manner in which they are integrated has

also been taken into account. There are various calculations that are made under the

absorption and marginal costing by which the concept involved is understood. The cost is

identified and also the profitability which is involved is ascertained. There is the

determination of breakeven point and variance analysis has also been used. With them, the

results are obtained that help management in taking the required actions. The different

planning tools which are involved in budgetary control have been considered and proper

explanation in relation to them has been provided. In that, all the advantages and

disadvantages associated with them have been involved. The resolution of financial problems

with the management accounting systems has been determined in the report in an appropriate

manner.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

References

Adongo, K.O. and Jagongo, A. (2013) Budgetary control as a measure of the financial

performance of state corporations in Kenya. International Journal of Accounting and

Taxation, 1(1), pp.38-57.

Armitage, H.M., Webb, A. and Glynn, J. (2016) The use of management accounting

techniques by small and medium‐sized enterprises: a field study of Canadian and Australian

practice. Accounting Perspectives, 15(1), pp.31-69.

Arroyo, P. (2012) Management accounting change and sustainability: an institutional

approach. Journal of Accounting & Organizational Change, 8(3), pp.286-309.

Aurora, B.B.C. (2013) The Cost of Production Under Direct Costing And Absorption

Costing–A Comparative Approach. Annals-Economy Series, 2, pp.123-129.

Chenhall, R. H. (2012) Developing an organizational perspective to management

accounting. Journal of Management Accounting Research. 24(1). pp.65-76.

Contrafatto, M. and Burns, J. (2013) Social and environmental accounting, organisational

change and management accounting: A processual view. Management Accounting

Research, 24(4), pp.349-365.

Drury, C. (2015) Management and Cost Accounting. 9th Ed. Cengage Learning.

Edmonds, T. and Olds, P. (2013) Fundamental Managerial Accounting Concepts. 7th Ed.

Maidenhead: McGraw-Hill.

Fullerton, R.R., Kennedy, F.A. and Widener, S.K. (2013) Management accounting and

control practices in a lean manufacturing environment. Accounting, Organizations and

Society, 38(1), pp.50-71.

Glass, V., Stefanova, S. and Prinzivalli, J. (2014) Zero-based budgeting: Does it make sense

for universal service reform?. Government Information Quarterly, 31(1), pp.84-89.

Hatem, A., Bozdağ, D., Toland, A.E. and Çatalyürek, Ü.V. (2013) Benchmarking short

sequence mapping tools. BMC bioinformatics, 14(1), p.184.

References

Adongo, K.O. and Jagongo, A. (2013) Budgetary control as a measure of the financial

performance of state corporations in Kenya. International Journal of Accounting and

Taxation, 1(1), pp.38-57.

Armitage, H.M., Webb, A. and Glynn, J. (2016) The use of management accounting

techniques by small and medium‐sized enterprises: a field study of Canadian and Australian

practice. Accounting Perspectives, 15(1), pp.31-69.

Arroyo, P. (2012) Management accounting change and sustainability: an institutional

approach. Journal of Accounting & Organizational Change, 8(3), pp.286-309.

Aurora, B.B.C. (2013) The Cost of Production Under Direct Costing And Absorption

Costing–A Comparative Approach. Annals-Economy Series, 2, pp.123-129.

Chenhall, R. H. (2012) Developing an organizational perspective to management

accounting. Journal of Management Accounting Research. 24(1). pp.65-76.

Contrafatto, M. and Burns, J. (2013) Social and environmental accounting, organisational

change and management accounting: A processual view. Management Accounting

Research, 24(4), pp.349-365.

Drury, C. (2015) Management and Cost Accounting. 9th Ed. Cengage Learning.

Edmonds, T. and Olds, P. (2013) Fundamental Managerial Accounting Concepts. 7th Ed.

Maidenhead: McGraw-Hill.

Fullerton, R.R., Kennedy, F.A. and Widener, S.K. (2013) Management accounting and

control practices in a lean manufacturing environment. Accounting, Organizations and

Society, 38(1), pp.50-71.

Glass, V., Stefanova, S. and Prinzivalli, J. (2014) Zero-based budgeting: Does it make sense

for universal service reform?. Government Information Quarterly, 31(1), pp.84-89.

Hatem, A., Bozdağ, D., Toland, A.E. and Çatalyürek, Ü.V. (2013) Benchmarking short

sequence mapping tools. BMC bioinformatics, 14(1), p.184.

12

Hiebl, M. R. (2014) Upper echelons theory in management accounting and control

research. Journal of Management Control. 24(3). pp.223-240.

Maas, K., Schaltegger, S. and Crutzen, N. (2016) Integrating corporate sustainability

assessment, management accounting, control, and reporting. Journal of Cleaner

Production, 136, pp.237-248.

Morano, P. and Tajani, F. (2017) The break-even analysis applied to urban renewal

investments: a model to evaluate the share of social housing financially sustainable for

private investors. Habitat International, 59, pp.10-20.

Nawaz, M. (2013) An Insight Into the Two Costing Technique: Absorption Costing and

Marginal Costing. BRAND. Broad Research in Accounting, Negotiation, and

Distribution, 4(1), pp.48-61.

Neiger, B.L., Thackeray, R., Van Wagenen, S.A., Hanson, C.L., West, J.H., Barnes, M.D.

and Fagen, M.C. (2012) Use of social media in health promotion: purposes, key performance

indicators, and evaluation metrics. Health promotion practice, 13(2), pp.159-164.

Seal, W. et al (2014) Management Accounting. 5th Ed. Maidenhead: McGraw-Hill.

Hiebl, M. R. (2014) Upper echelons theory in management accounting and control

research. Journal of Management Control. 24(3). pp.223-240.

Maas, K., Schaltegger, S. and Crutzen, N. (2016) Integrating corporate sustainability

assessment, management accounting, control, and reporting. Journal of Cleaner

Production, 136, pp.237-248.

Morano, P. and Tajani, F. (2017) The break-even analysis applied to urban renewal

investments: a model to evaluate the share of social housing financially sustainable for

private investors. Habitat International, 59, pp.10-20.

Nawaz, M. (2013) An Insight Into the Two Costing Technique: Absorption Costing and

Marginal Costing. BRAND. Broad Research in Accounting, Negotiation, and

Distribution, 4(1), pp.48-61.

Neiger, B.L., Thackeray, R., Van Wagenen, S.A., Hanson, C.L., West, J.H., Barnes, M.D.

and Fagen, M.C. (2012) Use of social media in health promotion: purposes, key performance

indicators, and evaluation metrics. Health promotion practice, 13(2), pp.159-164.

Seal, W. et al (2014) Management Accounting. 5th Ed. Maidenhead: McGraw-Hill.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.