Comparative Analysis of Management Accounting Systems: Two Firms

VerifiedAdded on 2022/03/21

|29

|7983

|11

Report

AI Summary

This report provides a comprehensive analysis of the management accounting systems of Coffeegreen Ltd. and Galaxy, exploring how these firms utilize various planning tools to address financial challenges and achieve sustainable success. The analysis begins with an examination of planning tools, including standard costs, budgets, and the balanced scorecard (BSC), outlining their advantages and disadvantages. The report then delves into specific calculations, such as determining the cost of a contract and the standard cost for processed coffee, along with the optimal selling price to maximize revenue. Furthermore, the report includes the preparation of monthly budgets for sales revenue and production resources. It also evaluates how planning tools contribute to Coffeegreen's long-term success and applies PEST, SWOT, and BSC analyses. The report then compares the management accounting systems of both firms, highlighting the characteristics of efficient management accountants and analyzing how management accounting can lead to sustainable success for both Coffeegreen and Galaxy. The report concludes with a discussion of the practical suggestions for improving the accounting system.

10200517_NGUYEN THI NHAT UYEN_MA_A2.1

Management accounting systems of two firms, Coffeegreen Ltd. and Galaxy

0

Management accounting systems of two firms, Coffeegreen Ltd. and Galaxy

0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION........................................................................................................2

SCENARIO 1...............................................................................................................3

1. Advantages and disadvantages of planning tools.............................................3

1.1. Standard costs and standard price.............................................................4

1.2. Budgets.....................................................................................................5

1.3. Balanced Scorecard (BSC)........................................................................5

2. Calculate the cost of the contract No. 348. Calculate the standard cost for 1 kg

of processed coffee and determine the selling price that helps Coffeegreen Ltd.

maximize its revenue in 2021....................................................................................6

2.1. Standard cost for 1 kg of processed coffee are as follows:........................7

2.2. Cost of the contract No. 348:....................................................................7

2.3. Determine the selling price that helps Coffeegreen Ltd. maximize its

revenue in 2021.....................................................................................................9

3. With the sales specified from the requirement 2, prepare the monthly budgets

for sales revenue, production volume, each production resource (raw materials,

labor, variable overheads).........................................................................................9

4. Evaluate how planning tools respond appropriately to solving financial

problems to lead Coffeegreen to sustainable success..............................................14

5. Apply PEST, SWOT and balanced scorecard analysis for Coffeegreen Ltd..16

5.1. PEST analysis.........................................................................................16

5.2. SWOT analysis.......................................................................................19

5.3. Balanced scorecard (BSC) analysis.........................................................21

SCENARIO 2.............................................................................................................. 21

1. Compare how Coffeegreen and Galaxy are adapting management accounting

systems to respond to financial problems................................................................21

2. Characteristics of efficient management accountants....................................23

3. Analyse and evaluate how in responding to financial problems, management

accounting can lead Coffeegreen and Galaxy to sustainable success......................23

3.1. Coffeegreen.............................................................................................23

3.2. Galaxy.....................................................................................................24

REFERENCES...........................................................................................................25

APPENDIX................................................................................................................. 27

1

INTRODUCTION........................................................................................................2

SCENARIO 1...............................................................................................................3

1. Advantages and disadvantages of planning tools.............................................3

1.1. Standard costs and standard price.............................................................4

1.2. Budgets.....................................................................................................5

1.3. Balanced Scorecard (BSC)........................................................................5

2. Calculate the cost of the contract No. 348. Calculate the standard cost for 1 kg

of processed coffee and determine the selling price that helps Coffeegreen Ltd.

maximize its revenue in 2021....................................................................................6

2.1. Standard cost for 1 kg of processed coffee are as follows:........................7

2.2. Cost of the contract No. 348:....................................................................7

2.3. Determine the selling price that helps Coffeegreen Ltd. maximize its

revenue in 2021.....................................................................................................9

3. With the sales specified from the requirement 2, prepare the monthly budgets

for sales revenue, production volume, each production resource (raw materials,

labor, variable overheads).........................................................................................9

4. Evaluate how planning tools respond appropriately to solving financial

problems to lead Coffeegreen to sustainable success..............................................14

5. Apply PEST, SWOT and balanced scorecard analysis for Coffeegreen Ltd..16

5.1. PEST analysis.........................................................................................16

5.2. SWOT analysis.......................................................................................19

5.3. Balanced scorecard (BSC) analysis.........................................................21

SCENARIO 2.............................................................................................................. 21

1. Compare how Coffeegreen and Galaxy are adapting management accounting

systems to respond to financial problems................................................................21

2. Characteristics of efficient management accountants....................................23

3. Analyse and evaluate how in responding to financial problems, management

accounting can lead Coffeegreen and Galaxy to sustainable success......................23

3.1. Coffeegreen.............................................................................................23

3.2. Galaxy.....................................................................................................24

REFERENCES...........................................................................................................25

APPENDIX................................................................................................................. 27

1

INTRODUCTION

I analyze and evaluate two management accounting systems of two firms, Coffeegreen Ltd.

and Galaxy, in this report. After that, I give some practical suggestions for improving their

accounting system to ensure long-term success.

2

I analyze and evaluate two management accounting systems of two firms, Coffeegreen Ltd.

and Galaxy, in this report. After that, I give some practical suggestions for improving their

accounting system to ensure long-term success.

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

SCENARIO 1

1. Advantages and disadvantages of planning tools.

Coffeegreen Ltd. is organized by Gia Lai Coffee Processing Company Ltd. and German

Drink Ltd. as a joint venture. Coffeegreen specializes in high-quality Arabica coffee mainly

for export to Germany. To maximize the profit, there are 4 planning tools applied namely

budgets, standard price, standard costs and balanced scorecard (BSC). Each planning tool has

its benefits and drawbacks for the company and its management accounting system, which

are analyzed below.

1.1. Standard costs and standard price.

Standards costing is a management accounting method that compares standard costs and

revenue to actual results to determine variances that can be used to motivate better efficiency.

By using standard costing system, the company can evaluate and make decision in the best

material and methods to maximize its profit. Furthermore, standard costs, prices, and budgets

are used as a benchmark for evaluating a company's actual costs, prices, and efficiency. As a

result, it is clear that by establishing standards, Coffeegreen will be able to manage potential

challenges, minimize total both production and non-production costs, and set more accurate

budgets.

According to Horngren et al (2015), the standard cost of a product or service needed for one

unit of input is a planned unit cost, which is calculated using the standard quantity of each

input and the standard price per input unit (standard price per kg of raw coffee bean or

standard price per labor hour). To set standard costs, the accountants have to set standard

prices which is carefully calculated prices that a company plans to pay for a unit of input in

production. Using standard costs supports Coffeegreen simplify the process of bookkeeping

in cost accounting management rather than FIFO, LIFO, etc. This planning tool – standard

costs have many advantages. Firstly, the company would gain better cost management by

setting standards for each form of expenses and each cost item (materials, labor, overhead)

incurred very complete and detailed, then identify challenges presented or variances which

are unexpected or unplanned things. Moreover, future actual costs could be close to standard

costs if Coffeegreen’s management sets acceptable cost standards and succeeds in controlling

manufacturing costs. As a result, managers can prepare more reliable budgets, estimate

expenses for bidding on work, and reduce unfavorable variances using standard costs. Top

management may benefit from a standard cost method when planning and making decisions.

The third benefit of using standard costs method is that the company can easily measure

3

1. Advantages and disadvantages of planning tools.

Coffeegreen Ltd. is organized by Gia Lai Coffee Processing Company Ltd. and German

Drink Ltd. as a joint venture. Coffeegreen specializes in high-quality Arabica coffee mainly

for export to Germany. To maximize the profit, there are 4 planning tools applied namely

budgets, standard price, standard costs and balanced scorecard (BSC). Each planning tool has

its benefits and drawbacks for the company and its management accounting system, which

are analyzed below.

1.1. Standard costs and standard price.

Standards costing is a management accounting method that compares standard costs and

revenue to actual results to determine variances that can be used to motivate better efficiency.

By using standard costing system, the company can evaluate and make decision in the best

material and methods to maximize its profit. Furthermore, standard costs, prices, and budgets

are used as a benchmark for evaluating a company's actual costs, prices, and efficiency. As a

result, it is clear that by establishing standards, Coffeegreen will be able to manage potential

challenges, minimize total both production and non-production costs, and set more accurate

budgets.

According to Horngren et al (2015), the standard cost of a product or service needed for one

unit of input is a planned unit cost, which is calculated using the standard quantity of each

input and the standard price per input unit (standard price per kg of raw coffee bean or

standard price per labor hour). To set standard costs, the accountants have to set standard

prices which is carefully calculated prices that a company plans to pay for a unit of input in

production. Using standard costs supports Coffeegreen simplify the process of bookkeeping

in cost accounting management rather than FIFO, LIFO, etc. This planning tool – standard

costs have many advantages. Firstly, the company would gain better cost management by

setting standards for each form of expenses and each cost item (materials, labor, overhead)

incurred very complete and detailed, then identify challenges presented or variances which

are unexpected or unplanned things. Moreover, future actual costs could be close to standard

costs if Coffeegreen’s management sets acceptable cost standards and succeeds in controlling

manufacturing costs. As a result, managers can prepare more reliable budgets, estimate

expenses for bidding on work, and reduce unfavorable variances using standard costs. Top

management may benefit from a standard cost method when planning and making decisions.

The third benefit of using standard costs method is that the company can easily measure

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

inventory value because Coffeegreen produces tons of coffee. Therefore, Coffeegreen can

save time and costs in production process and inventory system, then minimize cost of

potential risks of inventories. Besides, standard costs also help to reduce manufacturing costs

including both direct material and labor costs. However, the weakness of applying standard

costs is that it is limited for the director to figure out what constitutes a material or irregular

variance. Additionally, it is also difficult to analyze and resolve negatively unexpected

variances. It may lead to inefficiencies hidden or low morale performance because workers

are not reported or disbuse between director and workers (Lumen Learning, 2021). As a

result, the budgetary slack could increase. Furthermore, the standard prices could negatively

influence on management accounting if the price of production input sharply changes in term

of season especially raw coffee bean. The final drawback of standard cost system is time-

consuming and costly. In general, it needs a lot of time and incurs many costs to set and

maintaining for establishing the standard costs and standard prices.

1.2. Budgets.

According to Horngren et al (2015), budget is (a) a quantitative representation of

management's proposed plan of action for a certain period of time, and (b) a tool for

coordinating what needs to be done to put the plan into action. A budget includes planned

revenue, expenses, assets, liabilities and cash flows. A major advantage of budget is the

ability to evaluate different options and carry out ‘what if’ analysis. By changing the value of

certain variables, management are able to assess the effect of potential changes in their

environment. Budgets could also be able to assist Coffeegreen in achieving its objectives in

the future and compel planning. During setting budgets, it is likely to be easier for the

accountants of Coffeegreen to communicate ideas with plans. After that, activities and

functional departments should coordinate to follow the budgets. In addition to budgets’

advantages, a budget provides a framework for responsibility accounting to necessary

reduction and efficiency improvement to maximize profit of Coffeegreen. The accountants

set budgets for the purpose to establish a system of control to manage all expenses in

production. Besides, the manager can motivate workers to improve their performance to

boost the profit of the company by reporting budgets to them. Nevertheless, budget tool also

has some drawbacks. Firstly, it seems to be very difficult to identity budgeted numbers as it

needs expert to predict those numbers. Therefore, it could be time-consuming and money-

consuming for this process. In addition, the coordination between functional departments

could be considered as an advantage but it is actually difficult to require that. Finally, budgets

4

save time and costs in production process and inventory system, then minimize cost of

potential risks of inventories. Besides, standard costs also help to reduce manufacturing costs

including both direct material and labor costs. However, the weakness of applying standard

costs is that it is limited for the director to figure out what constitutes a material or irregular

variance. Additionally, it is also difficult to analyze and resolve negatively unexpected

variances. It may lead to inefficiencies hidden or low morale performance because workers

are not reported or disbuse between director and workers (Lumen Learning, 2021). As a

result, the budgetary slack could increase. Furthermore, the standard prices could negatively

influence on management accounting if the price of production input sharply changes in term

of season especially raw coffee bean. The final drawback of standard cost system is time-

consuming and costly. In general, it needs a lot of time and incurs many costs to set and

maintaining for establishing the standard costs and standard prices.

1.2. Budgets.

According to Horngren et al (2015), budget is (a) a quantitative representation of

management's proposed plan of action for a certain period of time, and (b) a tool for

coordinating what needs to be done to put the plan into action. A budget includes planned

revenue, expenses, assets, liabilities and cash flows. A major advantage of budget is the

ability to evaluate different options and carry out ‘what if’ analysis. By changing the value of

certain variables, management are able to assess the effect of potential changes in their

environment. Budgets could also be able to assist Coffeegreen in achieving its objectives in

the future and compel planning. During setting budgets, it is likely to be easier for the

accountants of Coffeegreen to communicate ideas with plans. After that, activities and

functional departments should coordinate to follow the budgets. In addition to budgets’

advantages, a budget provides a framework for responsibility accounting to necessary

reduction and efficiency improvement to maximize profit of Coffeegreen. The accountants

set budgets for the purpose to establish a system of control to manage all expenses in

production. Besides, the manager can motivate workers to improve their performance to

boost the profit of the company by reporting budgets to them. Nevertheless, budget tool also

has some drawbacks. Firstly, it seems to be very difficult to identity budgeted numbers as it

needs expert to predict those numbers. Therefore, it could be time-consuming and money-

consuming for this process. In addition, the coordination between functional departments

could be considered as an advantage but it is actually difficult to require that. Finally, budgets

4

are set to always compare with actual costs so it sometimes lowers moral performance of

workers (Thakur, 2021).

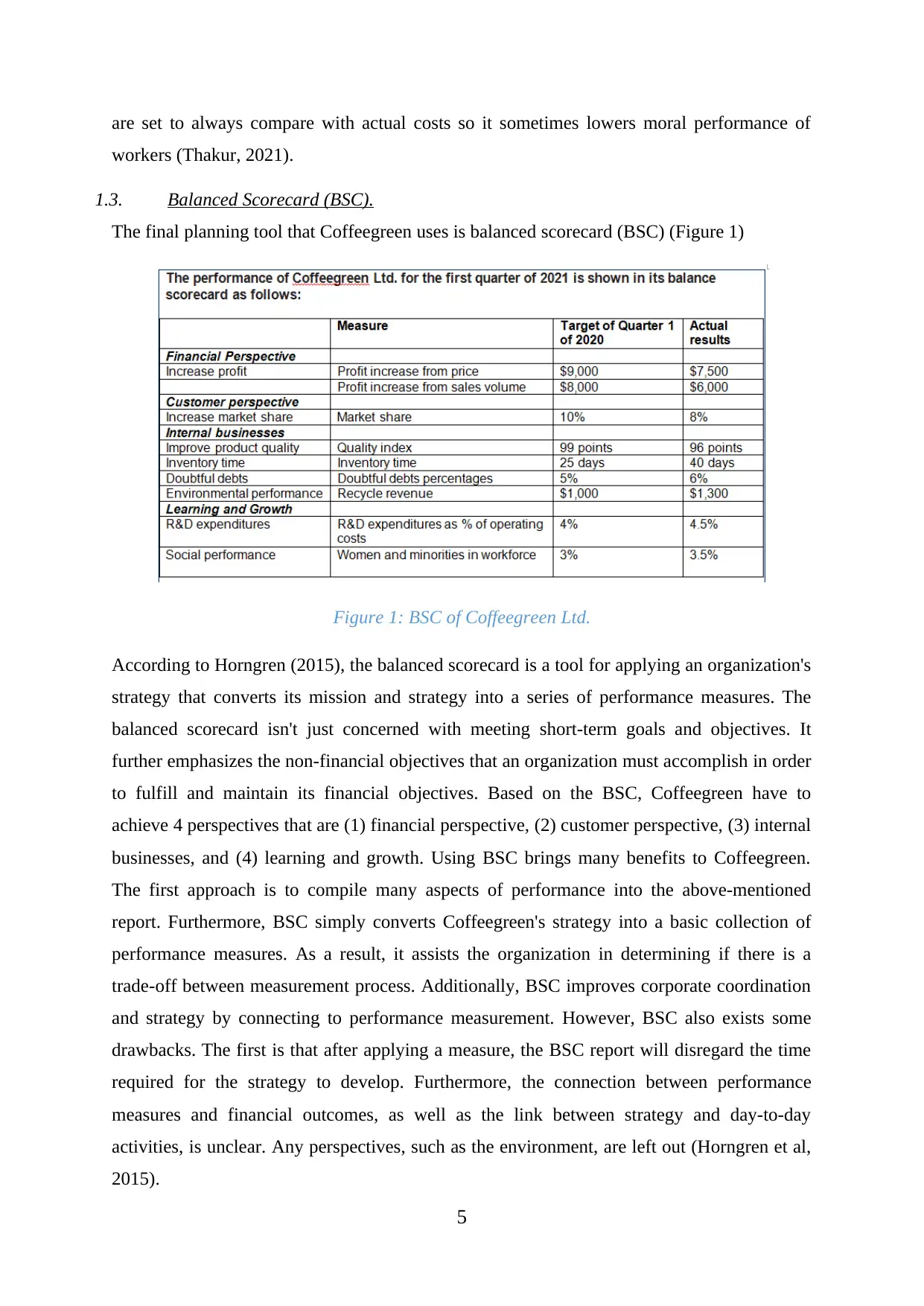

1.3. Balanced Scorecard (BSC).

The final planning tool that Coffeegreen uses is balanced scorecard (BSC) (Figure 1)

Figure 1: BSC of Coffeegreen Ltd.

According to Horngren (2015), the balanced scorecard is a tool for applying an organization's

strategy that converts its mission and strategy into a series of performance measures. The

balanced scorecard isn't just concerned with meeting short-term goals and objectives. It

further emphasizes the non-financial objectives that an organization must accomplish in order

to fulfill and maintain its financial objectives. Based on the BSC, Coffeegreen have to

achieve 4 perspectives that are (1) financial perspective, (2) customer perspective, (3) internal

businesses, and (4) learning and growth. Using BSC brings many benefits to Coffeegreen.

The first approach is to compile many aspects of performance into the above-mentioned

report. Furthermore, BSC simply converts Coffeegreen's strategy into a basic collection of

performance measures. As a result, it assists the organization in determining if there is a

trade-off between measurement process. Additionally, BSC improves corporate coordination

and strategy by connecting to performance measurement. However, BSC also exists some

drawbacks. The first is that after applying a measure, the BSC report will disregard the time

required for the strategy to develop. Furthermore, the connection between performance

measures and financial outcomes, as well as the link between strategy and day-to-day

activities, is unclear. Any perspectives, such as the environment, are left out (Horngren et al,

2015).

5

workers (Thakur, 2021).

1.3. Balanced Scorecard (BSC).

The final planning tool that Coffeegreen uses is balanced scorecard (BSC) (Figure 1)

Figure 1: BSC of Coffeegreen Ltd.

According to Horngren (2015), the balanced scorecard is a tool for applying an organization's

strategy that converts its mission and strategy into a series of performance measures. The

balanced scorecard isn't just concerned with meeting short-term goals and objectives. It

further emphasizes the non-financial objectives that an organization must accomplish in order

to fulfill and maintain its financial objectives. Based on the BSC, Coffeegreen have to

achieve 4 perspectives that are (1) financial perspective, (2) customer perspective, (3) internal

businesses, and (4) learning and growth. Using BSC brings many benefits to Coffeegreen.

The first approach is to compile many aspects of performance into the above-mentioned

report. Furthermore, BSC simply converts Coffeegreen's strategy into a basic collection of

performance measures. As a result, it assists the organization in determining if there is a

trade-off between measurement process. Additionally, BSC improves corporate coordination

and strategy by connecting to performance measurement. However, BSC also exists some

drawbacks. The first is that after applying a measure, the BSC report will disregard the time

required for the strategy to develop. Furthermore, the connection between performance

measures and financial outcomes, as well as the link between strategy and day-to-day

activities, is unclear. Any perspectives, such as the environment, are left out (Horngren et al,

2015).

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2. Calculate the cost of the contract No. 348. Calculate the standard cost for 1 kg of processed

coffee and determine the selling price that helps Coffeegreen Ltd. maximize its revenue in

2021.

- Standard costs of Coffeegreen for 1 kg of coffee are as follows:

Coffee bean costs: 1.4 kg * $2/kg = $2.8

Direct labor costs: 0.6 labor hours * $5 per hour = $3

Predetermined overhead rate: 100% of labor costs

- In March 2021:

Production volume 24 tons

Exported/ sales volume for the contract No. 348 15 tons

Ending inventory 4 tons

Actual overhead $70,000.

- The policy of Coffeegreen is that the over/under-allocation of overhead should be counted in

the cost of goods sold.

- Estimates for the market possibility of coffee in 2021 of Coffeegreen are below:

Quantity demanded (kg) Selling price ($/kg)

300,000 10

280,000 11

250,000 12

240,000 13

200,000 14

- Sales volume in the high season (Nov-Apr) = 150% x Sales volume in the low season (May-

Oct).

- Monthly production volume = 40% x Sales volume of next month + 60% x Sales volume of

current month.

- One kg of processed coffee requires 1.4 kg of raw coffee bean.

2.1. Standard cost for 1 kg of processed coffee are as follows:

Standard cost for 1 kg of processed coffee:

Materials: Coffee bean costs $2.8

Direct labor costs $3

Overhead cost = 100% of labor cost $3

Standard cost for 1 kg of processed coffee = $2.8 + $3 + $3 $8.8

6

coffee and determine the selling price that helps Coffeegreen Ltd. maximize its revenue in

2021.

- Standard costs of Coffeegreen for 1 kg of coffee are as follows:

Coffee bean costs: 1.4 kg * $2/kg = $2.8

Direct labor costs: 0.6 labor hours * $5 per hour = $3

Predetermined overhead rate: 100% of labor costs

- In March 2021:

Production volume 24 tons

Exported/ sales volume for the contract No. 348 15 tons

Ending inventory 4 tons

Actual overhead $70,000.

- The policy of Coffeegreen is that the over/under-allocation of overhead should be counted in

the cost of goods sold.

- Estimates for the market possibility of coffee in 2021 of Coffeegreen are below:

Quantity demanded (kg) Selling price ($/kg)

300,000 10

280,000 11

250,000 12

240,000 13

200,000 14

- Sales volume in the high season (Nov-Apr) = 150% x Sales volume in the low season (May-

Oct).

- Monthly production volume = 40% x Sales volume of next month + 60% x Sales volume of

current month.

- One kg of processed coffee requires 1.4 kg of raw coffee bean.

2.1. Standard cost for 1 kg of processed coffee are as follows:

Standard cost for 1 kg of processed coffee:

Materials: Coffee bean costs $2.8

Direct labor costs $3

Overhead cost = 100% of labor cost $3

Standard cost for 1 kg of processed coffee = $2.8 + $3 + $3 $8.8

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2.2. Cost of the contract No. 348:

Notes:

- Sales volume in March 2021 = Production volume - Ending inventory volume

- Overallocated overhead = Applied overhead – Actual overhead (>0)

- Total applied overhead = Overhead cost for 1 kg of processed coffee x Production volume

- Since the over allocation of overhead should be counted in the costs of goods sold,

overallocated overhead is counted for total sale volume in March 2021 that is 20,000 kg of

coffee.

- Sales volume of the contract No. 348 = 15 tons = 15,000 kg.

- Total production costs for 1 kg of coffee of the contract No. 348 = Direct materials costs +

Direct labor costs + Overhead cost.

- The over-allocated overhead is counted Cost of No. 348 sold = over-allocated overhead for

1 kg of coffee sold x Sale volume of the contract No. 348

- Total production costs for the contract No. 348 = Total production costs for 1 kg of coffee x

Sale volume of the contract No. 348.

- Total cost of goods sold for the contract No. 348 = Total production costs for the contract No.

348 - The over-allocated overhead is counted Cost of No. 348 sold

Sales volume in March 2021

Production volume = 24 tons 24,000 kg

Ending inventory volume = 4 tons 4,000 kg

Total sales volume in March 2021 = 24 tons – 4 tons 20,000 kg

The over-allocated overhead is counted in the Cost of goods sold

(= $72,000 - $70,000)

$2,000

Actual overhead $70,000

Applied overhead = $3 x 24,000 $72,000

The over-allocated overhead for 1 kg of coffee sold =

$2,000/20,000

$0.1

Compute COST OF GOODS SOLD of the contract No. 348

Production costs for 1 kg of coffee of the contract No. 348

7

Notes:

- Sales volume in March 2021 = Production volume - Ending inventory volume

- Overallocated overhead = Applied overhead – Actual overhead (>0)

- Total applied overhead = Overhead cost for 1 kg of processed coffee x Production volume

- Since the over allocation of overhead should be counted in the costs of goods sold,

overallocated overhead is counted for total sale volume in March 2021 that is 20,000 kg of

coffee.

- Sales volume of the contract No. 348 = 15 tons = 15,000 kg.

- Total production costs for 1 kg of coffee of the contract No. 348 = Direct materials costs +

Direct labor costs + Overhead cost.

- The over-allocated overhead is counted Cost of No. 348 sold = over-allocated overhead for

1 kg of coffee sold x Sale volume of the contract No. 348

- Total production costs for the contract No. 348 = Total production costs for 1 kg of coffee x

Sale volume of the contract No. 348.

- Total cost of goods sold for the contract No. 348 = Total production costs for the contract No.

348 - The over-allocated overhead is counted Cost of No. 348 sold

Sales volume in March 2021

Production volume = 24 tons 24,000 kg

Ending inventory volume = 4 tons 4,000 kg

Total sales volume in March 2021 = 24 tons – 4 tons 20,000 kg

The over-allocated overhead is counted in the Cost of goods sold

(= $72,000 - $70,000)

$2,000

Actual overhead $70,000

Applied overhead = $3 x 24,000 $72,000

The over-allocated overhead for 1 kg of coffee sold =

$2,000/20,000

$0.1

Compute COST OF GOODS SOLD of the contract No. 348

Production costs for 1 kg of coffee of the contract No. 348

7

Direct materials costs : Coffee bean costs $2.8

Direct labor costs $3

Overhead cost = 100% of labor cost $3

Total production costs for 1 kg of coffee of the contract No.

348 = $2.8 + 3 + 3

$8.8

Sale volume of the contract No. 348 = 15 tons 15,000 kg

The over-allocated overhead is counted Cost of No. 348 sold =

$0.1 x 15,000

$1,500

Total production costs for the contract No. 348 = $8.8 x 15,000 $132,000

Total cost of goods sold for the contract No. 348 = $132,000 –

$1,500

$130,500

2.3. Determine the selling price that helps Coffeegreen Ltd. maximize its revenue in 2021.

Estimates for the market possibility of coffee in 2021 of Coffeegreen are below:

Quantity demanded (kg) Selling price ($/kg) Revenue ($)

300,000 10 3,000,000

280,000 11 3,080,000

250,000 12 3,000,000

240,000 13 (MAX) 3,120,000

200,000 14 2,800,000

Note: Revenue = Quantity demanded x Selling price

In conclusion, as can be seen from the table above, if Coffeegreen Ltd. wants to maximize its

revenue in 2021, the selling price for 1 kg of coffee should be $13/kg along with 240,000 kg

of coffee for quantity demanded. At this selling price, the sales revenue would maximize and

equal to $3,120,000.

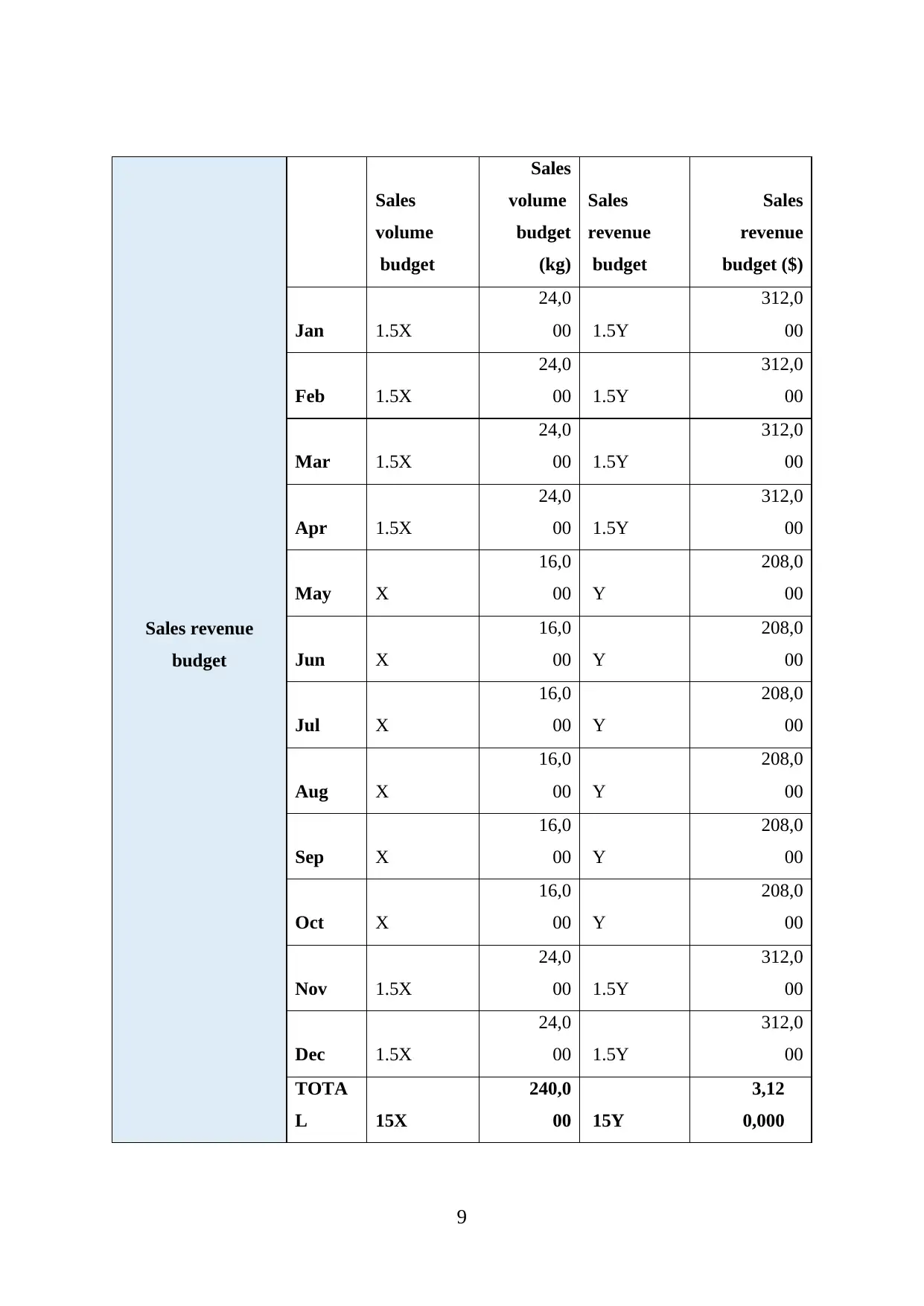

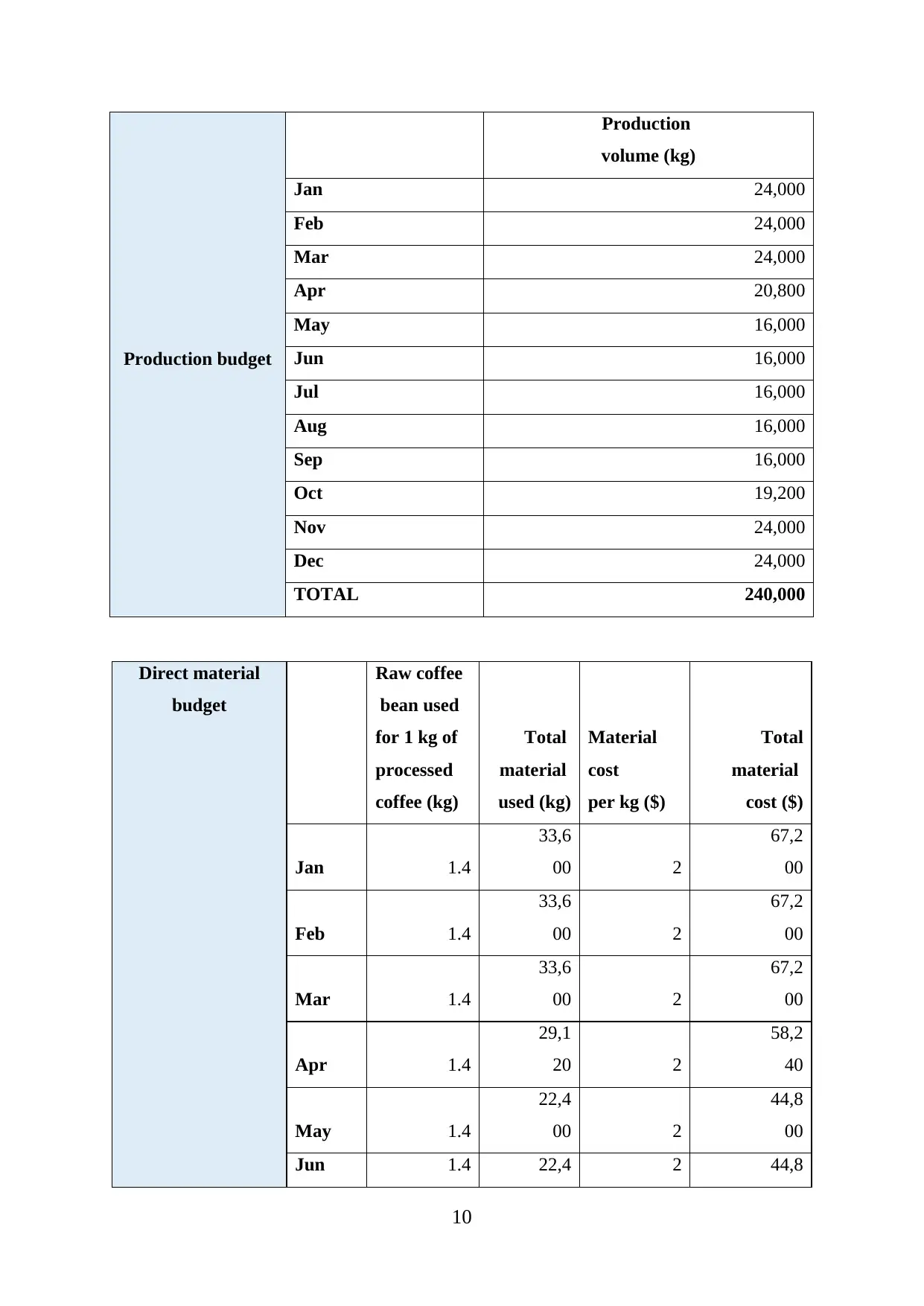

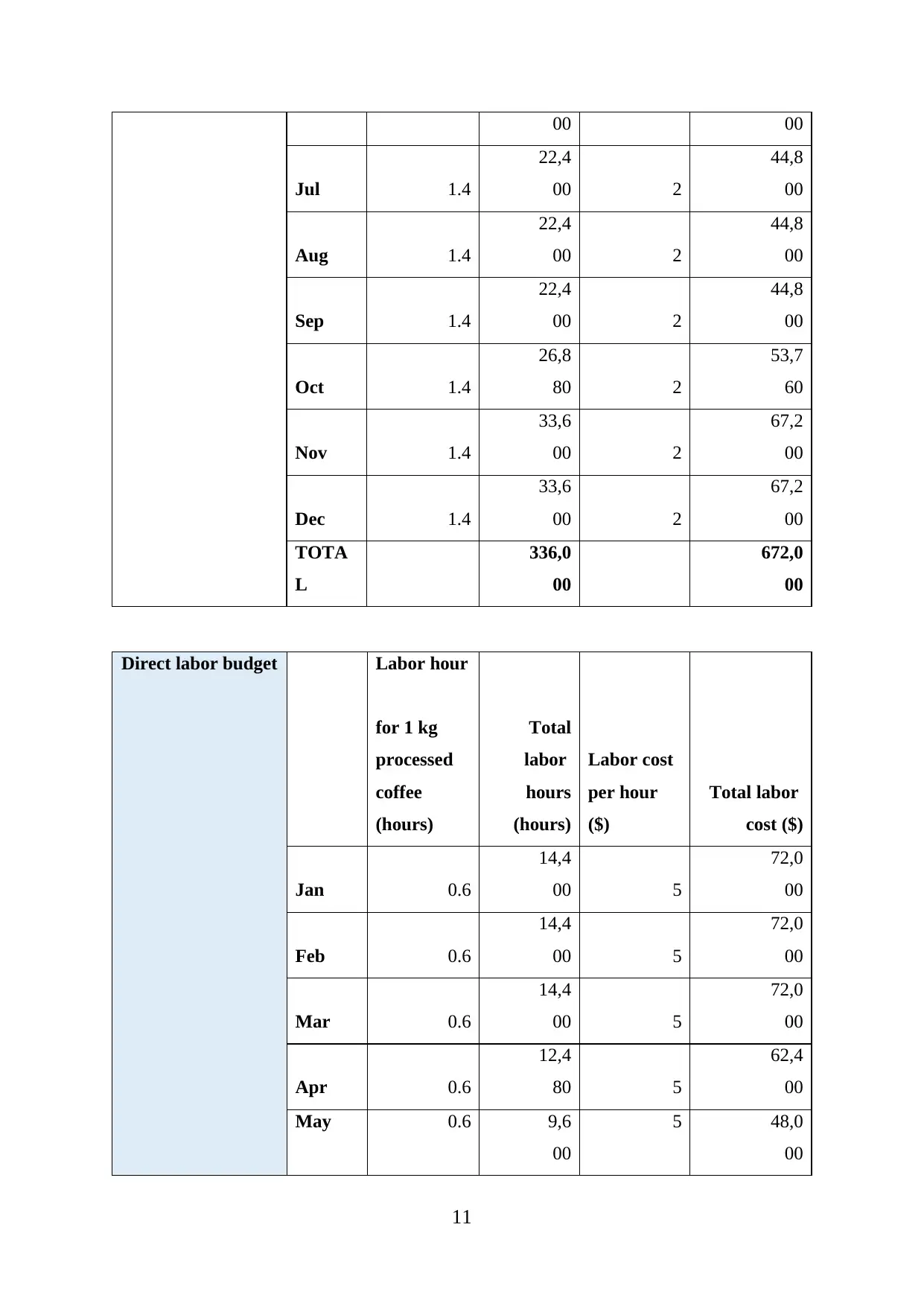

3. With the sales specified from the requirement 2, prepare the monthly budgets for sales

revenue, production volume, each production resource (raw materials, labor, variable

overheads).

Monthly budget in 2021

8

Direct labor costs $3

Overhead cost = 100% of labor cost $3

Total production costs for 1 kg of coffee of the contract No.

348 = $2.8 + 3 + 3

$8.8

Sale volume of the contract No. 348 = 15 tons 15,000 kg

The over-allocated overhead is counted Cost of No. 348 sold =

$0.1 x 15,000

$1,500

Total production costs for the contract No. 348 = $8.8 x 15,000 $132,000

Total cost of goods sold for the contract No. 348 = $132,000 –

$1,500

$130,500

2.3. Determine the selling price that helps Coffeegreen Ltd. maximize its revenue in 2021.

Estimates for the market possibility of coffee in 2021 of Coffeegreen are below:

Quantity demanded (kg) Selling price ($/kg) Revenue ($)

300,000 10 3,000,000

280,000 11 3,080,000

250,000 12 3,000,000

240,000 13 (MAX) 3,120,000

200,000 14 2,800,000

Note: Revenue = Quantity demanded x Selling price

In conclusion, as can be seen from the table above, if Coffeegreen Ltd. wants to maximize its

revenue in 2021, the selling price for 1 kg of coffee should be $13/kg along with 240,000 kg

of coffee for quantity demanded. At this selling price, the sales revenue would maximize and

equal to $3,120,000.

3. With the sales specified from the requirement 2, prepare the monthly budgets for sales

revenue, production volume, each production resource (raw materials, labor, variable

overheads).

Monthly budget in 2021

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Sales revenue

budget

Sales

volume

budget

Sales

volume

budget

(kg)

Sales

revenue

budget

Sales

revenue

budget ($)

Jan 1.5X

24,0

00 1.5Y

312,0

00

Feb 1.5X

24,0

00 1.5Y

312,0

00

Mar 1.5X

24,0

00 1.5Y

312,0

00

Apr 1.5X

24,0

00 1.5Y

312,0

00

May X

16,0

00 Y

208,0

00

Jun X

16,0

00 Y

208,0

00

Jul X

16,0

00 Y

208,0

00

Aug X

16,0

00 Y

208,0

00

Sep X

16,0

00 Y

208,0

00

Oct X

16,0

00 Y

208,0

00

Nov 1.5X

24,0

00 1.5Y

312,0

00

Dec 1.5X

24,0

00 1.5Y

312,0

00

TOTA

L 15X

240,0

00 15Y

3,12

0,000

9

budget

Sales

volume

budget

Sales

volume

budget

(kg)

Sales

revenue

budget

Sales

revenue

budget ($)

Jan 1.5X

24,0

00 1.5Y

312,0

00

Feb 1.5X

24,0

00 1.5Y

312,0

00

Mar 1.5X

24,0

00 1.5Y

312,0

00

Apr 1.5X

24,0

00 1.5Y

312,0

00

May X

16,0

00 Y

208,0

00

Jun X

16,0

00 Y

208,0

00

Jul X

16,0

00 Y

208,0

00

Aug X

16,0

00 Y

208,0

00

Sep X

16,0

00 Y

208,0

00

Oct X

16,0

00 Y

208,0

00

Nov 1.5X

24,0

00 1.5Y

312,0

00

Dec 1.5X

24,0

00 1.5Y

312,0

00

TOTA

L 15X

240,0

00 15Y

3,12

0,000

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Production budget

Production

volume (kg)

Jan 24,000

Feb 24,000

Mar 24,000

Apr 20,800

May 16,000

Jun 16,000

Jul 16,000

Aug 16,000

Sep 16,000

Oct 19,200

Nov 24,000

Dec 24,000

TOTAL 240,000

Direct material

budget

Raw coffee

bean used

for 1 kg of

processed

coffee (kg)

Total

material

used (kg)

Material

cost

per kg ($)

Total

material

cost ($)

Jan 1.4

33,6

00 2

67,2

00

Feb 1.4

33,6

00 2

67,2

00

Mar 1.4

33,6

00 2

67,2

00

Apr 1.4

29,1

20 2

58,2

40

May 1.4

22,4

00 2

44,8

00

Jun 1.4 22,4 2 44,8

10

Production

volume (kg)

Jan 24,000

Feb 24,000

Mar 24,000

Apr 20,800

May 16,000

Jun 16,000

Jul 16,000

Aug 16,000

Sep 16,000

Oct 19,200

Nov 24,000

Dec 24,000

TOTAL 240,000

Direct material

budget

Raw coffee

bean used

for 1 kg of

processed

coffee (kg)

Total

material

used (kg)

Material

cost

per kg ($)

Total

material

cost ($)

Jan 1.4

33,6

00 2

67,2

00

Feb 1.4

33,6

00 2

67,2

00

Mar 1.4

33,6

00 2

67,2

00

Apr 1.4

29,1

20 2

58,2

40

May 1.4

22,4

00 2

44,8

00

Jun 1.4 22,4 2 44,8

10

00 00

Jul 1.4

22,4

00 2

44,8

00

Aug 1.4

22,4

00 2

44,8

00

Sep 1.4

22,4

00 2

44,8

00

Oct 1.4

26,8

80 2

53,7

60

Nov 1.4

33,6

00 2

67,2

00

Dec 1.4

33,6

00 2

67,2

00

TOTA

L

336,0

00

672,0

00

Direct labor budget Labor hour

for 1 kg

processed

coffee

(hours)

Total

labor

hours

(hours)

Labor cost

per hour

($)

Total labor

cost ($)

Jan 0.6

14,4

00 5

72,0

00

Feb 0.6

14,4

00 5

72,0

00

Mar 0.6

14,4

00 5

72,0

00

Apr 0.6

12,4

80 5

62,4

00

May 0.6 9,6

00

5 48,0

00

11

Jul 1.4

22,4

00 2

44,8

00

Aug 1.4

22,4

00 2

44,8

00

Sep 1.4

22,4

00 2

44,8

00

Oct 1.4

26,8

80 2

53,7

60

Nov 1.4

33,6

00 2

67,2

00

Dec 1.4

33,6

00 2

67,2

00

TOTA

L

336,0

00

672,0

00

Direct labor budget Labor hour

for 1 kg

processed

coffee

(hours)

Total

labor

hours

(hours)

Labor cost

per hour

($)

Total labor

cost ($)

Jan 0.6

14,4

00 5

72,0

00

Feb 0.6

14,4

00 5

72,0

00

Mar 0.6

14,4

00 5

72,0

00

Apr 0.6

12,4

80 5

62,4

00

May 0.6 9,6

00

5 48,0

00

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 29

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.