Management Accounting Report: Cost Analysis, Planning, and Adaptation

VerifiedAdded on 2022/12/28

|17

|3941

|39

Report

AI Summary

This report provides a comprehensive overview of management accounting principles and their practical application within the context of Western Food Limited, a UK-based food manufacturing company. It delves into various aspects of management accounting, including explaining management accounting systems, methods of reporting, and calculating costs using marginal and absorption costing to prepare income statements. The report also examines different planning tools used for budgetary control, analyzing their advantages and disadvantages, and compares how organizations adapt management accounting systems to respond to financial problems. The analysis includes practical examples such as break-even analysis, variance analysis, and the identification of fixed and variable costs, offering a detailed understanding of cost behavior and its impact on profitability and decision-making. The report uses real-world scenarios to illustrate the importance of accurate financial data for strategic planning and organizational success. Finally, the report concludes with a concise summary of key findings and recommendations.

Management

accounting

Table of Contents

accounting

Table of Contents

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Explain management accounting and give the essential requirements of different types of

management accounting systems.................................................................................................3

P2 Explain different methods used for management accounting reporting.................................6

TASK 2............................................................................................................................................7

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs...........................................................................7

TASK 3..........................................................................................................................................12

P4 Explain the advantages and disadvantages of different types of planning tools used for

budgetary control.......................................................................................................................12

TASK 4..........................................................................................................................................14

P5 Compare how organizations are adapting management accounting systems to respond to

financial problems.....................................................................................................................14

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

Books and Journals:...................................................................................................................17

TASK 1............................................................................................................................................3

P1 Explain management accounting and give the essential requirements of different types of

management accounting systems.................................................................................................3

P2 Explain different methods used for management accounting reporting.................................6

TASK 2............................................................................................................................................7

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs...........................................................................7

TASK 3..........................................................................................................................................12

P4 Explain the advantages and disadvantages of different types of planning tools used for

budgetary control.......................................................................................................................12

TASK 4..........................................................................................................................................14

P5 Compare how organizations are adapting management accounting systems to respond to

financial problems.....................................................................................................................14

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

Books and Journals:...................................................................................................................17

INTRODUCTION

Management accounting is the procedure of accounting system that provided detail

structure and documents of accounting information using through various tools and techniques.

Management require the operation's of planning functions and in accordance with that collection

of resources and makes its fuller utilisation. However, accounting system consist the same role as

a part of management function. It plans the cost, expenditure, incomes and reserves into

systematic manner. Involving appropriates accounting standard helps in retention of employees

and attracting shareholders towards organisation profitability and accuracy. It helps in

identification of financial and non financial data of the organisation that provide assistance to the

managers in making decisions regarding finance sources, keeping records, data entry and

comparison between past and present growth (Ravenda and et.al., 2019). According to the

provisions of CMA cost management accounting system, country like London involves

accounting as a term of making policies and strategies top look at organisation glow of monetary

elements and at which source. This report is going to consist role of management in accounting

standard in the context of western food limited, it is a medium scale enterprise in London UK.

The company has manufacturing concern into food products. It has taken into consideration all

the counting measures for the enterprise to attract shareholders and enhance expansion.

TASK 1

P1 Explain management accounting and give the essential requirements of different types of

management accounting systems.

Management accounting is a appropriate system of identifying, analysing, recording and

deciding the financial outcome of the company. In involves managers decision making regarding

needs of financial funding and capital investment into the organization. Management accounting

provides an initial structure of techniques to record transactions on daily basis, prepare

statements and take decisions regarding buying investments. In carries out the activity of

preparing statements and records to gather wide data into one single documents, these data are

collected for stakeholders preferences as it work as a proof of companies profitability into

market. The documents show organisations potential in order to stand against competitive

market.

Management accounting is the procedure of accounting system that provided detail

structure and documents of accounting information using through various tools and techniques.

Management require the operation's of planning functions and in accordance with that collection

of resources and makes its fuller utilisation. However, accounting system consist the same role as

a part of management function. It plans the cost, expenditure, incomes and reserves into

systematic manner. Involving appropriates accounting standard helps in retention of employees

and attracting shareholders towards organisation profitability and accuracy. It helps in

identification of financial and non financial data of the organisation that provide assistance to the

managers in making decisions regarding finance sources, keeping records, data entry and

comparison between past and present growth (Ravenda and et.al., 2019). According to the

provisions of CMA cost management accounting system, country like London involves

accounting as a term of making policies and strategies top look at organisation glow of monetary

elements and at which source. This report is going to consist role of management in accounting

standard in the context of western food limited, it is a medium scale enterprise in London UK.

The company has manufacturing concern into food products. It has taken into consideration all

the counting measures for the enterprise to attract shareholders and enhance expansion.

TASK 1

P1 Explain management accounting and give the essential requirements of different types of

management accounting systems.

Management accounting is a appropriate system of identifying, analysing, recording and

deciding the financial outcome of the company. In involves managers decision making regarding

needs of financial funding and capital investment into the organization. Management accounting

provides an initial structure of techniques to record transactions on daily basis, prepare

statements and take decisions regarding buying investments. In carries out the activity of

preparing statements and records to gather wide data into one single documents, these data are

collected for stakeholders preferences as it work as a proof of companies profitability into

market. The documents show organisations potential in order to stand against competitive

market.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

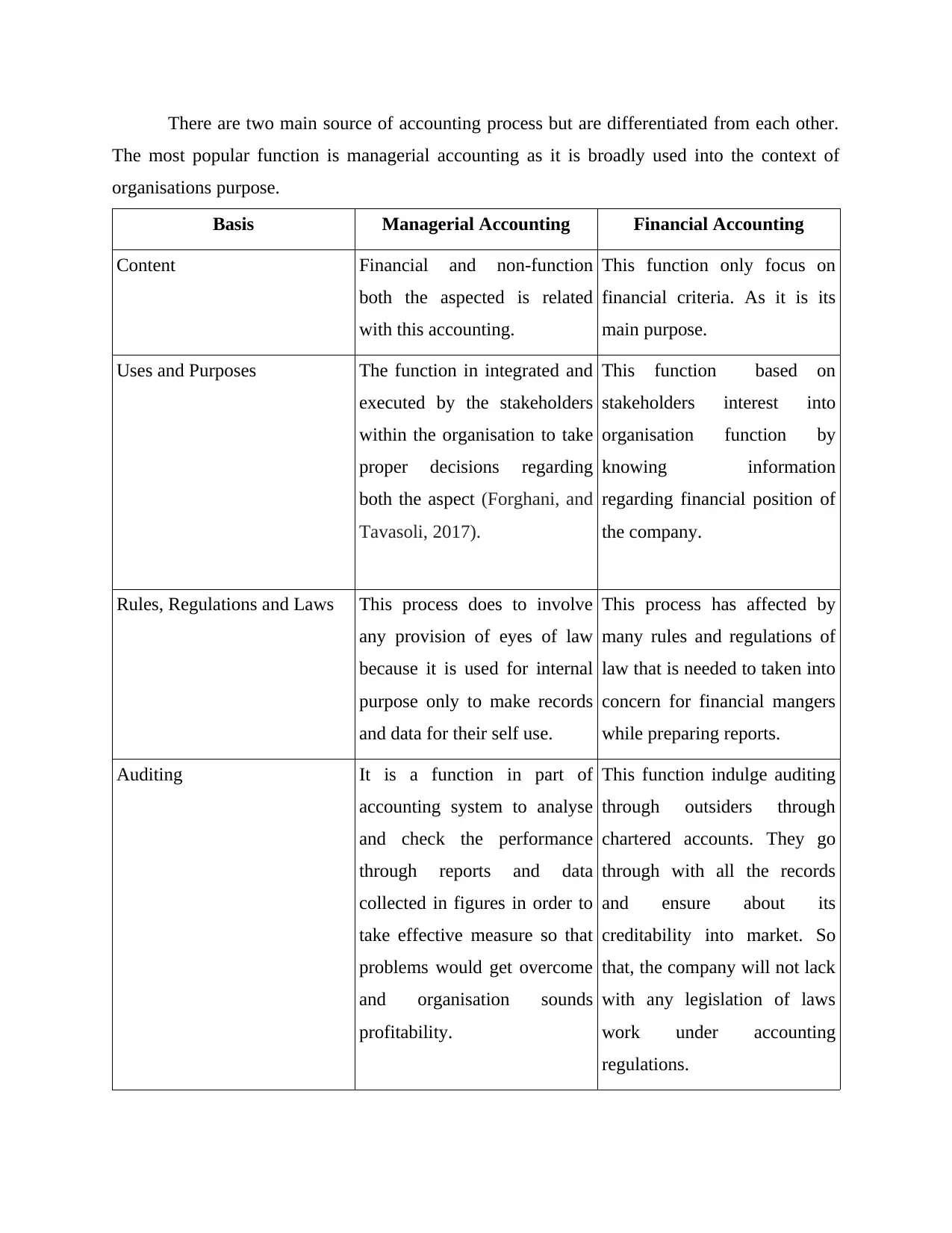

There are two main source of accounting process but are differentiated from each other.

The most popular function is managerial accounting as it is broadly used into the context of

organisations purpose.

Basis Managerial Accounting Financial Accounting

Content Financial and non-function

both the aspected is related

with this accounting.

This function only focus on

financial criteria. As it is its

main purpose.

Uses and Purposes The function in integrated and

executed by the stakeholders

within the organisation to take

proper decisions regarding

both the aspect (Forghani, and

Tavasoli, 2017).

This function based on

stakeholders interest into

organisation function by

knowing information

regarding financial position of

the company.

Rules, Regulations and Laws This process does to involve

any provision of eyes of law

because it is used for internal

purpose only to make records

and data for their self use.

This process has affected by

many rules and regulations of

law that is needed to taken into

concern for financial mangers

while preparing reports.

Auditing It is a function in part of

accounting system to analyse

and check the performance

through reports and data

collected in figures in order to

take effective measure so that

problems would get overcome

and organisation sounds

profitability.

This function indulge auditing

through outsiders through

chartered accounts. They go

through with all the records

and ensure about its

creditability into market. So

that, the company will not lack

with any legislation of laws

work under accounting

regulations.

The most popular function is managerial accounting as it is broadly used into the context of

organisations purpose.

Basis Managerial Accounting Financial Accounting

Content Financial and non-function

both the aspected is related

with this accounting.

This function only focus on

financial criteria. As it is its

main purpose.

Uses and Purposes The function in integrated and

executed by the stakeholders

within the organisation to take

proper decisions regarding

both the aspect (Forghani, and

Tavasoli, 2017).

This function based on

stakeholders interest into

organisation function by

knowing information

regarding financial position of

the company.

Rules, Regulations and Laws This process does to involve

any provision of eyes of law

because it is used for internal

purpose only to make records

and data for their self use.

This process has affected by

many rules and regulations of

law that is needed to taken into

concern for financial mangers

while preparing reports.

Auditing It is a function in part of

accounting system to analyse

and check the performance

through reports and data

collected in figures in order to

take effective measure so that

problems would get overcome

and organisation sounds

profitability.

This function indulge auditing

through outsiders through

chartered accounts. They go

through with all the records

and ensure about its

creditability into market. So

that, the company will not lack

with any legislation of laws

work under accounting

regulations.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

There are further different accounting systems which are mentioned below:

Cost Accounting System: this system consist the data and facts of cost related facts of the

organization. These cost could be any of like variable, fixed, accumulated or semi-variable that

an organisation incurred while running organisation functions. This system provide an assistance

regarding lowering down all these costs by taken corrective measure and cost effective

techniques where he organisation lack of efficiency. Organisation existence is based on its

profitability which will be provided by analysing and minimizing cost and maximizing the

profit.

Inventory Management System: this accounting and management is all based upon the

inventory and stock which company maintains for manufacturing and selling. It does include all

the unfurnished products like raw materials, semi-finished and fully finished products in order to

make them available for resale. This stock in due and maintain for specific time period that cost

extra to the company. To reduce these extra cost companies use this system of accounting and

clear unsold stock first (NGUYEN, 2020) (Talebi, and Bahri Sales, 2018).

Job Costing System: this cost is basically incurred on working on special and specific

product as per customers requirement. As western food limited provides product with customer

demand it incur cost of production process. It is needed to analyse these cost in order to attain

profits over expenditure. It consist all the expenditure incurring relation to production,

promotion and selling aspect.

Price Optimizing System: this process is all based on evaluation prices and cost of

products. By indulging this process, The western food Ltd will be identify what should be the

minimum price for their product which ill cover the profit over costs. Price optimization is an

essential function to facilitate process as per customer creditability for purchasing.

These are the major accounting systems which are followed by the organisation to the

most of extent and provide accurate assistance in leveraging profits and minimizing cost. Some

of the methods are cost effective and some are to take decision for future purpose (Das, and

Singh, 2018).

Cost Accounting System: this system consist the data and facts of cost related facts of the

organization. These cost could be any of like variable, fixed, accumulated or semi-variable that

an organisation incurred while running organisation functions. This system provide an assistance

regarding lowering down all these costs by taken corrective measure and cost effective

techniques where he organisation lack of efficiency. Organisation existence is based on its

profitability which will be provided by analysing and minimizing cost and maximizing the

profit.

Inventory Management System: this accounting and management is all based upon the

inventory and stock which company maintains for manufacturing and selling. It does include all

the unfurnished products like raw materials, semi-finished and fully finished products in order to

make them available for resale. This stock in due and maintain for specific time period that cost

extra to the company. To reduce these extra cost companies use this system of accounting and

clear unsold stock first (NGUYEN, 2020) (Talebi, and Bahri Sales, 2018).

Job Costing System: this cost is basically incurred on working on special and specific

product as per customers requirement. As western food limited provides product with customer

demand it incur cost of production process. It is needed to analyse these cost in order to attain

profits over expenditure. It consist all the expenditure incurring relation to production,

promotion and selling aspect.

Price Optimizing System: this process is all based on evaluation prices and cost of

products. By indulging this process, The western food Ltd will be identify what should be the

minimum price for their product which ill cover the profit over costs. Price optimization is an

essential function to facilitate process as per customer creditability for purchasing.

These are the major accounting systems which are followed by the organisation to the

most of extent and provide accurate assistance in leveraging profits and minimizing cost. Some

of the methods are cost effective and some are to take decision for future purpose (Das, and

Singh, 2018).

P2 Explain different methods used for management accounting reporting.

Reports are the major part of accounting system theta specifically shows the data, facts

and figures drives from the organizational performance. These reports are significant to optimize

company potential over their cost and expenditure that will make them reliable to take

competitive advantage. The main purpose of preparing report is to make differentiation among

past performance with the current trends and money worth This includes all the cost and incomes

regarding operations, working capital, sales and purchase also other fixed and variable costs.

Managers will get assistance through these data in decision making purpose to decide where to

cover the cost and make it convert in6to profits. A business organization will only look forwards

to the factor where they get maximum profits and make all these scenario of this purpose only.

The report must be prepared in accurate and relevant way by building correct data and facts.

Any up down in figures will lead to cause a hurdle into whole organisation performance. So that

it is all are in the hands of accounting manager to be authentic and reliable with reports

formation. There are many reports that are essential to prepare for mangers are described below:

Budget Report: this cost is initial that needs to be prepare for the foremost aspect as it

contains budget for the company performance. The budget has been prepare on the bass of past

performance and must considers to eliminate all the expense which are not feasible for the

organization (Kim, And Matsumura, 2017).

Job Cost Report: this report is based on the special cost occurred in the special events

and production. The purposed report consist all information regarding expense labors,

transportation and accumulated cost of machinery.

Inventory and Manufacturing Budget: the report includes all the information regarding

goods, inventory whether it is opening or closing, sold or unsold. Each details will be covering

into structure of report and managers make final conclusion on which elements needs to move

out from the process on inventory flow.

Order Information Report: under this process, the management of organization prepare

reports for all the orders received an enormous numbers through different location. That needs to

be record so that no order will be left out from its delivery and information containing its price

and invoice that will show actual profit company has earned.

Reports are the major part of accounting system theta specifically shows the data, facts

and figures drives from the organizational performance. These reports are significant to optimize

company potential over their cost and expenditure that will make them reliable to take

competitive advantage. The main purpose of preparing report is to make differentiation among

past performance with the current trends and money worth This includes all the cost and incomes

regarding operations, working capital, sales and purchase also other fixed and variable costs.

Managers will get assistance through these data in decision making purpose to decide where to

cover the cost and make it convert in6to profits. A business organization will only look forwards

to the factor where they get maximum profits and make all these scenario of this purpose only.

The report must be prepared in accurate and relevant way by building correct data and facts.

Any up down in figures will lead to cause a hurdle into whole organisation performance. So that

it is all are in the hands of accounting manager to be authentic and reliable with reports

formation. There are many reports that are essential to prepare for mangers are described below:

Budget Report: this cost is initial that needs to be prepare for the foremost aspect as it

contains budget for the company performance. The budget has been prepare on the bass of past

performance and must considers to eliminate all the expense which are not feasible for the

organization (Kim, And Matsumura, 2017).

Job Cost Report: this report is based on the special cost occurred in the special events

and production. The purposed report consist all information regarding expense labors,

transportation and accumulated cost of machinery.

Inventory and Manufacturing Budget: the report includes all the information regarding

goods, inventory whether it is opening or closing, sold or unsold. Each details will be covering

into structure of report and managers make final conclusion on which elements needs to move

out from the process on inventory flow.

Order Information Report: under this process, the management of organization prepare

reports for all the orders received an enormous numbers through different location. That needs to

be record so that no order will be left out from its delivery and information containing its price

and invoice that will show actual profit company has earned.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounts Receivable Aging Report: under this report, organization keep records of

receivables data I.e. whom goods have provided them on credit basis and money is about to be

revived. It is required to keep their information so that no amount will convert into bad debts.

Performance Report: this report consider performance of organization function through overall

companies working in terms of employees, stakeholders. It sets appropriation standard to be

effective and profitable into all the management criteria (Altukhov, Predeus, and Predeus,

2019).

TASK 2

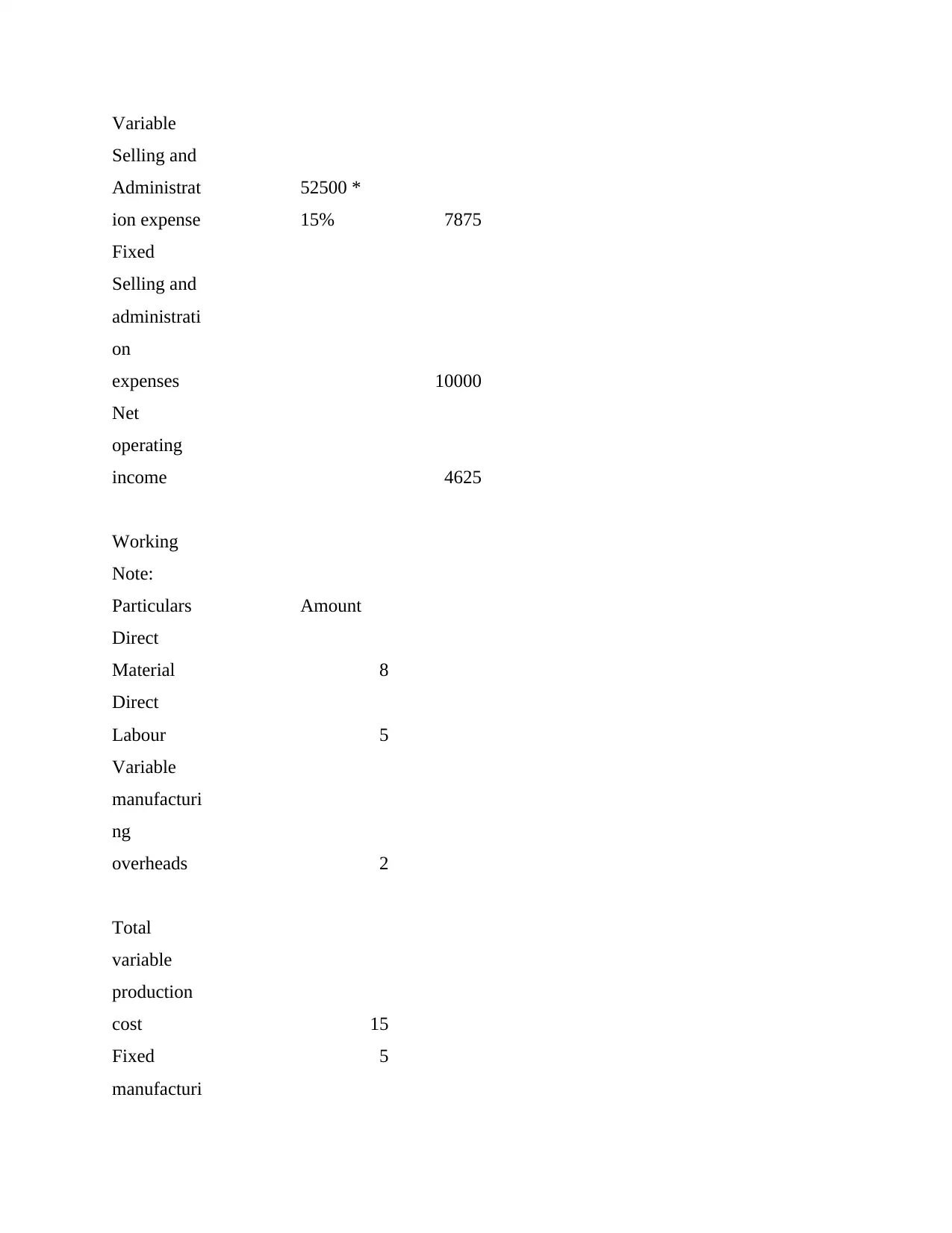

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income statement

using marginal and absorption costs.

Income

Statement

as per

Absorption

costing

Particulars Working Amount

Sales 1500*35 52500

Less: Cost

of goods

sold 1500*20 30000

Gross

Margin 22500

Less:

Selling and

administrati

on

expenses

receivables data I.e. whom goods have provided them on credit basis and money is about to be

revived. It is required to keep their information so that no amount will convert into bad debts.

Performance Report: this report consider performance of organization function through overall

companies working in terms of employees, stakeholders. It sets appropriation standard to be

effective and profitable into all the management criteria (Altukhov, Predeus, and Predeus,

2019).

TASK 2

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income statement

using marginal and absorption costs.

Income

Statement

as per

Absorption

costing

Particulars Working Amount

Sales 1500*35 52500

Less: Cost

of goods

sold 1500*20 30000

Gross

Margin 22500

Less:

Selling and

administrati

on

expenses

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

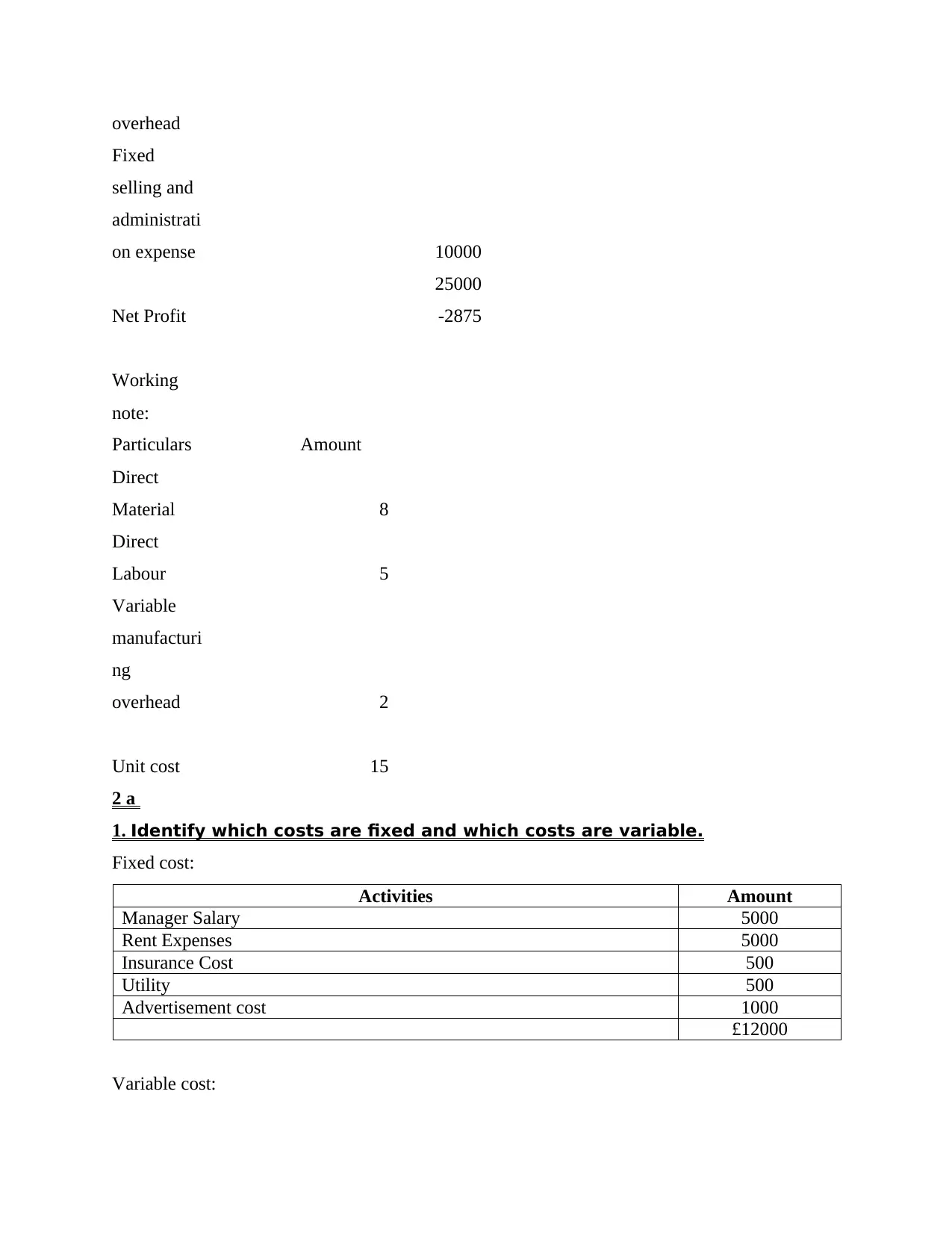

Variable

Selling and

Administrat

ion expense

52500 *

15% 7875

Fixed

Selling and

administrati

on

expenses 10000

Net

operating

income 4625

Working

Note:

Particulars Amount

Direct

Material 8

Direct

Labour 5

Variable

manufacturi

ng

overheads 2

Total

variable

production

cost 15

Fixed

manufacturi

5

Selling and

Administrat

ion expense

52500 *

15% 7875

Fixed

Selling and

administrati

on

expenses 10000

Net

operating

income 4625

Working

Note:

Particulars Amount

Direct

Material 8

Direct

Labour 5

Variable

manufacturi

ng

overheads 2

Total

variable

production

cost 15

Fixed

manufacturi

5

ng

overheads

Unit cost 20

Income

statement

as per

marginal

costing

method

Particulars Working Amount

Sales 1500*35 52500

Less:

Variable

Expenses

Variable

production

cost 1500*15 22500

Variable

Selling and

Administrat

ion expense

52500 *

15% 7875

30375

Margin

Contributio

n 22125

Fixed

Expenses

Fixed

production

15000

overheads

Unit cost 20

Income

statement

as per

marginal

costing

method

Particulars Working Amount

Sales 1500*35 52500

Less:

Variable

Expenses

Variable

production

cost 1500*15 22500

Variable

Selling and

Administrat

ion expense

52500 *

15% 7875

30375

Margin

Contributio

n 22125

Fixed

Expenses

Fixed

production

15000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

overhead

Fixed

selling and

administrati

on expense 10000

25000

Net Profit -2875

Working

note:

Particulars Amount

Direct

Material 8

Direct

Labour 5

Variable

manufacturi

ng

overhead 2

Unit cost 15

2 a

1. Identify which costs are fixed and which costs are variable.

Fixed cost:

Activities Amount

Manager Salary 5000

Rent Expenses 5000

Insurance Cost 500

Utility 500

Advertisement cost 1000

£12000

Variable cost:

Fixed

selling and

administrati

on expense 10000

25000

Net Profit -2875

Working

note:

Particulars Amount

Direct

Material 8

Direct

Labour 5

Variable

manufacturi

ng

overhead 2

Unit cost 15

2 a

1. Identify which costs are fixed and which costs are variable.

Fixed cost:

Activities Amount

Manager Salary 5000

Rent Expenses 5000

Insurance Cost 500

Utility 500

Advertisement cost 1000

£12000

Variable cost:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

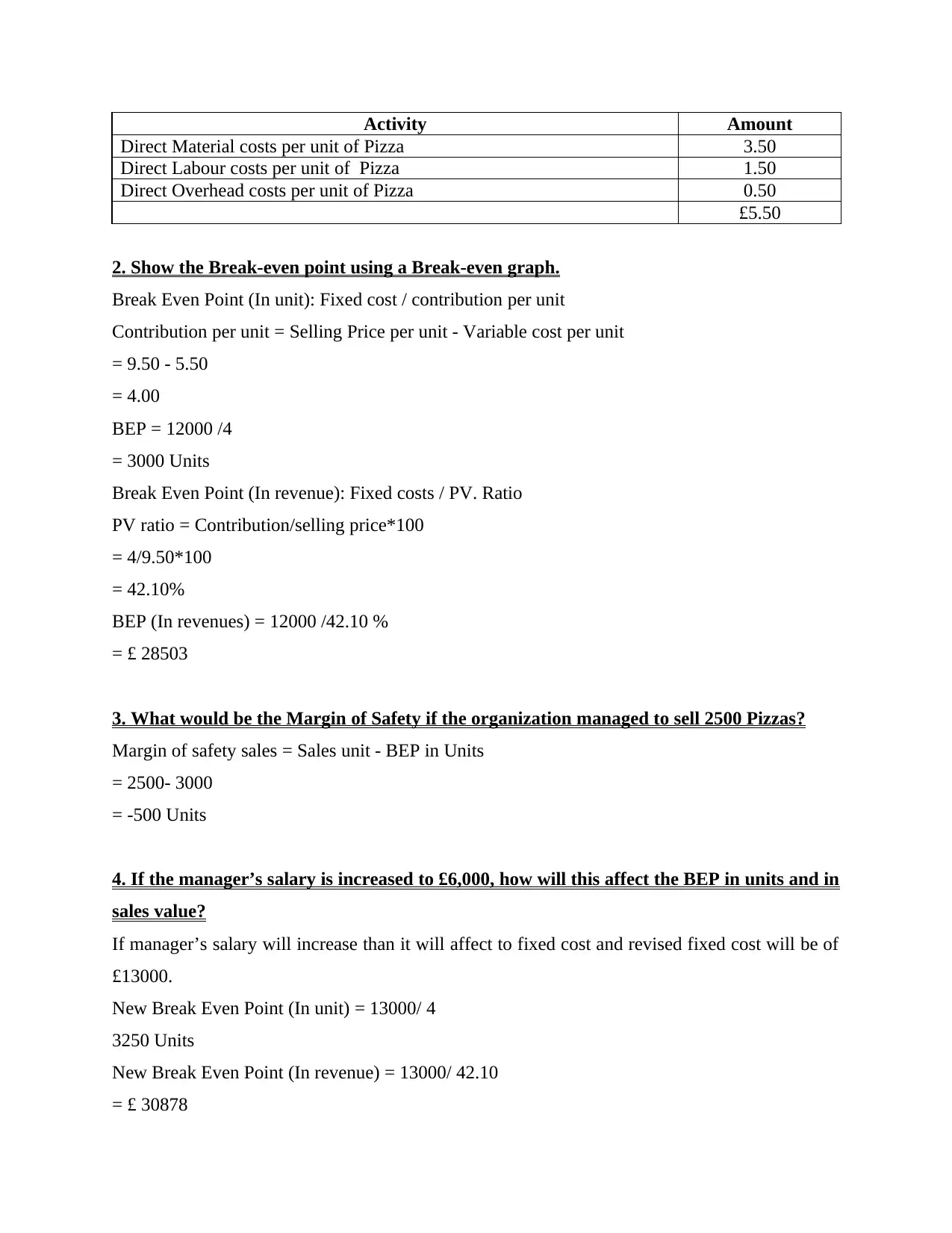

Activity Amount

Direct Material costs per unit of Pizza 3.50

Direct Labour costs per unit of Pizza 1.50

Direct Overhead costs per unit of Pizza 0.50

£5.50

2. Show the Break-even point using a Break-even graph.

Break Even Point (In unit): Fixed cost / contribution per unit

Contribution per unit = Selling Price per unit - Variable cost per unit

= 9.50 - 5.50

= 4.00

BEP = 12000 /4

= 3000 Units

Break Even Point (In revenue): Fixed costs / PV. Ratio

PV ratio = Contribution/selling price*100

= 4/9.50*100

= 42.10%

BEP (In revenues) = 12000 /42.10 %

= £ 28503

3. What would be the Margin of Safety if the organization managed to sell 2500 Pizzas?

Margin of safety sales = Sales unit - BEP in Units

= 2500- 3000

= -500 Units

4. If the manager’s salary is increased to £6,000, how will this affect the BEP in units and in

sales value?

If manager’s salary will increase than it will affect to fixed cost and revised fixed cost will be of

£13000.

New Break Even Point (In unit) = 13000/ 4

3250 Units

New Break Even Point (In revenue) = 13000/ 42.10

= £ 30878

Direct Material costs per unit of Pizza 3.50

Direct Labour costs per unit of Pizza 1.50

Direct Overhead costs per unit of Pizza 0.50

£5.50

2. Show the Break-even point using a Break-even graph.

Break Even Point (In unit): Fixed cost / contribution per unit

Contribution per unit = Selling Price per unit - Variable cost per unit

= 9.50 - 5.50

= 4.00

BEP = 12000 /4

= 3000 Units

Break Even Point (In revenue): Fixed costs / PV. Ratio

PV ratio = Contribution/selling price*100

= 4/9.50*100

= 42.10%

BEP (In revenues) = 12000 /42.10 %

= £ 28503

3. What would be the Margin of Safety if the organization managed to sell 2500 Pizzas?

Margin of safety sales = Sales unit - BEP in Units

= 2500- 3000

= -500 Units

4. If the manager’s salary is increased to £6,000, how will this affect the BEP in units and in

sales value?

If manager’s salary will increase than it will affect to fixed cost and revised fixed cost will be of

£13000.

New Break Even Point (In unit) = 13000/ 4

3250 Units

New Break Even Point (In revenue) = 13000/ 42.10

= £ 30878

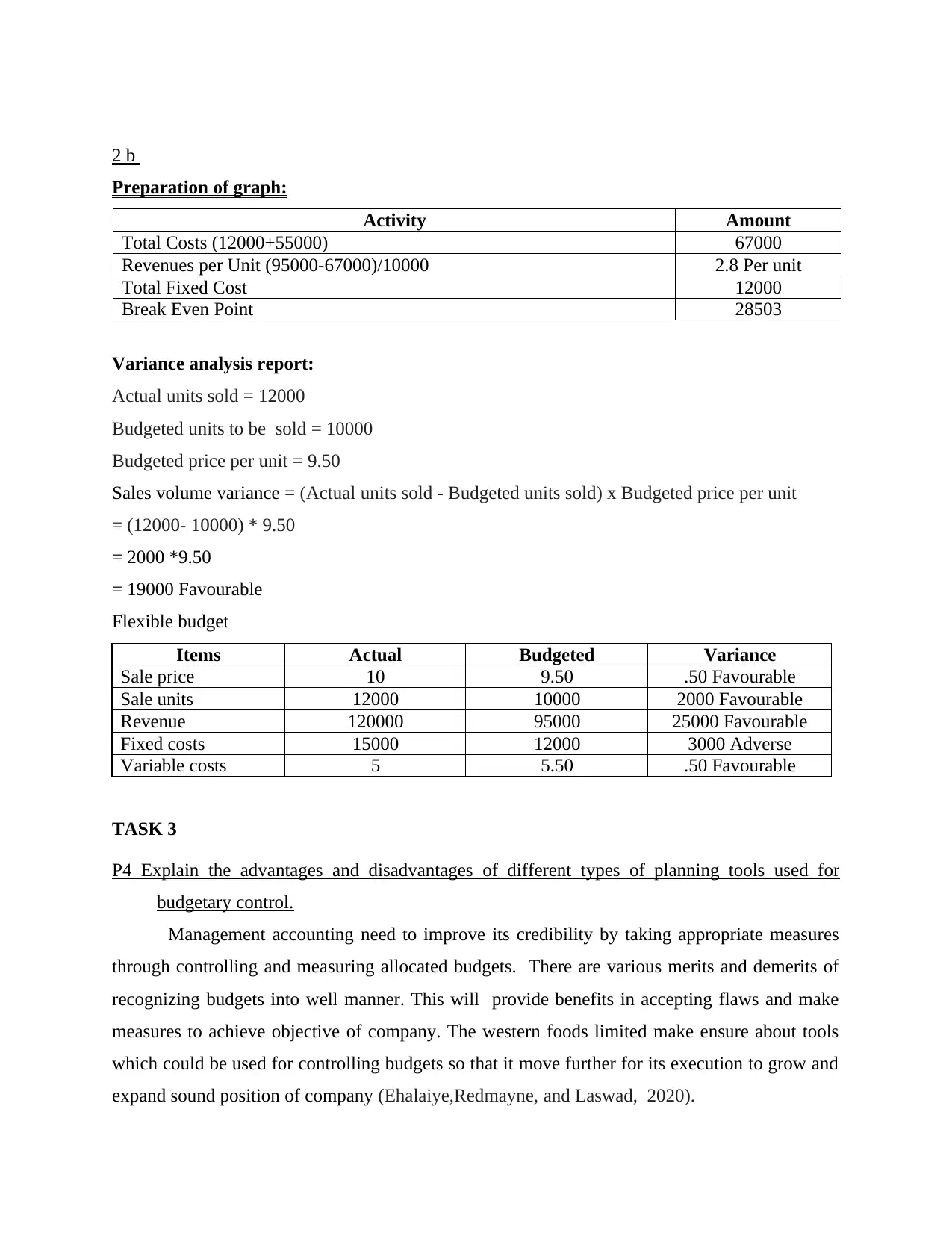

2 b

Preparation of graph:

Activity Amount

Total Costs (12000+55000) 67000

Revenues per Unit (95000-67000)/10000 2.8 Per unit

Total Fixed Cost 12000

Break Even Point 28503

Variance analysis report:

Actual units sold = 12000

Budgeted units to be sold = 10000

Budgeted price per unit = 9.50

Sales volume variance = (Actual units sold - Budgeted units sold) x Budgeted price per unit

= (12000- 10000) * 9.50

= 2000 *9.50

= 19000 Favourable

Flexible budget

Items Actual Budgeted Variance

Sale price 10 9.50 .50 Favourable

Sale units 12000 10000 2000 Favourable

Revenue 120000 95000 25000 Favourable

Fixed costs 15000 12000 3000 Adverse

Variable costs 5 5.50 .50 Favourable

TASK 3

P4 Explain the advantages and disadvantages of different types of planning tools used for

budgetary control.

Management accounting need to improve its credibility by taking appropriate measures

through controlling and measuring allocated budgets. There are various merits and demerits of

recognizing budgets into well manner. This will provide benefits in accepting flaws and make

measures to achieve objective of company. The western foods limited make ensure about tools

which could be used for controlling budgets so that it move further for its execution to grow and

expand sound position of company (Ehalaiye,Redmayne, and Laswad, 2020).

Preparation of graph:

Activity Amount

Total Costs (12000+55000) 67000

Revenues per Unit (95000-67000)/10000 2.8 Per unit

Total Fixed Cost 12000

Break Even Point 28503

Variance analysis report:

Actual units sold = 12000

Budgeted units to be sold = 10000

Budgeted price per unit = 9.50

Sales volume variance = (Actual units sold - Budgeted units sold) x Budgeted price per unit

= (12000- 10000) * 9.50

= 2000 *9.50

= 19000 Favourable

Flexible budget

Items Actual Budgeted Variance

Sale price 10 9.50 .50 Favourable

Sale units 12000 10000 2000 Favourable

Revenue 120000 95000 25000 Favourable

Fixed costs 15000 12000 3000 Adverse

Variable costs 5 5.50 .50 Favourable

TASK 3

P4 Explain the advantages and disadvantages of different types of planning tools used for

budgetary control.

Management accounting need to improve its credibility by taking appropriate measures

through controlling and measuring allocated budgets. There are various merits and demerits of

recognizing budgets into well manner. This will provide benefits in accepting flaws and make

measures to achieve objective of company. The western foods limited make ensure about tools

which could be used for controlling budgets so that it move further for its execution to grow and

expand sound position of company (Ehalaiye,Redmayne, and Laswad, 2020).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.