Report on Management Accounting: Principles, Systems, and Analysis

VerifiedAdded on 2021/01/01

|17

|4595

|275

Report

AI Summary

This report provides a comprehensive overview of management accounting, its principles, and its application in business decision-making. It begins by defining management accounting and distinguishing it from financial accounting, highlighting its role in internal management and operational strategies. The report then explores key concepts such as ABC costing, relevant costing analysis, and various cost accounting systems, including actual costing, standard costing, and normal costing. It further delves into inventory management systems, including FIFO, LIFO, and AVCO methods, as well as job costing systems like batch costing, contract costing, and service costing. The report also covers the presentation of financial information through various reports, such as exception reports, schedule reports, and performance reports. A practical example of preparing an income statement using marginal costing is also included, demonstrating the application of these concepts in a real-world scenario. The report concludes by emphasizing the importance of management accounting in addressing financial problems and supporting effective business management. This report is a valuable resource for students studying finance and accounting, providing insights into the tools and techniques used to manage and analyze financial information for better decision-making.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

\Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

a) Explain the management accounting and the essential requirement of management

accounting...................................................................................................................................1

b) Presenting financial information.............................................................................................5

TASK 2............................................................................................................................................6

Preparing income statement........................................................................................................6

TASK 3............................................................................................................................................7

Budgetary control process, types of budgeting tools and importance........................................7

TASK 4..........................................................................................................................................10

Importance of management accounting to respond financial problems....................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

a) Explain the management accounting and the essential requirement of management

accounting...................................................................................................................................1

b) Presenting financial information.............................................................................................5

TASK 2............................................................................................................................................6

Preparing income statement........................................................................................................6

TASK 3............................................................................................................................................7

Budgetary control process, types of budgeting tools and importance........................................7

TASK 4..........................................................................................................................................10

Importance of management accounting to respond financial problems....................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Effective management and operations are the essential requirement of organisation in

order to attain desired aim and objective of business (Bovens, Goodin and Schillemans, 2014).

Management accounting is an internal part of organisation which helps to manage and operate

the functions and operations of business in particular format. This report is prepared to analyse

the essential aspect of management accounting. Management accounting system provides a

structure to record the transactions and events in better way. Types of management accounting

systems and reporting methods are defined in this context. Types of reports are provided in terms

of helping and recording the data in effective and reliable manner. Tech UK Ltd is chosen

organisation in which the role of management accounting is defined.

TASK 1

a) Explain the management accounting and the essential requirement of management accounting

Management accounting

Management accounting is a considered as a management tool which assists to prepare

and manage in terms of day to day business transactions and short term managerial decision.

There are types of information and tools are analysed in terms of making effective plans and

management strategies in business. Management accounting is a concept which analyse the

overall transactions and events happened during the year and summarise the information subject

to determining the performance of organisation. Periodic reports and information are produced to

managers and the accountants which helps to manage the operations and departments of

organisation (Brewer, Sorensen and Stout, 2014).

AS per IMA (Institute of Management Accountants), Management accounting is a

profession which remains involves in management decision making and developing plans and

performance management system. It provides expertise in financial reporting and control to help

the management in the formulation and implementation of an organisation's strategy. This is one

of the essential aspect and important thing for determining the effectiveness of organisation. This

basically helps managers and accountants to make business plans, effective management and

operational strategies with effective management and operations. This is mainly associated with

taking crucial decision and management (What is management accounting system, 2018.).

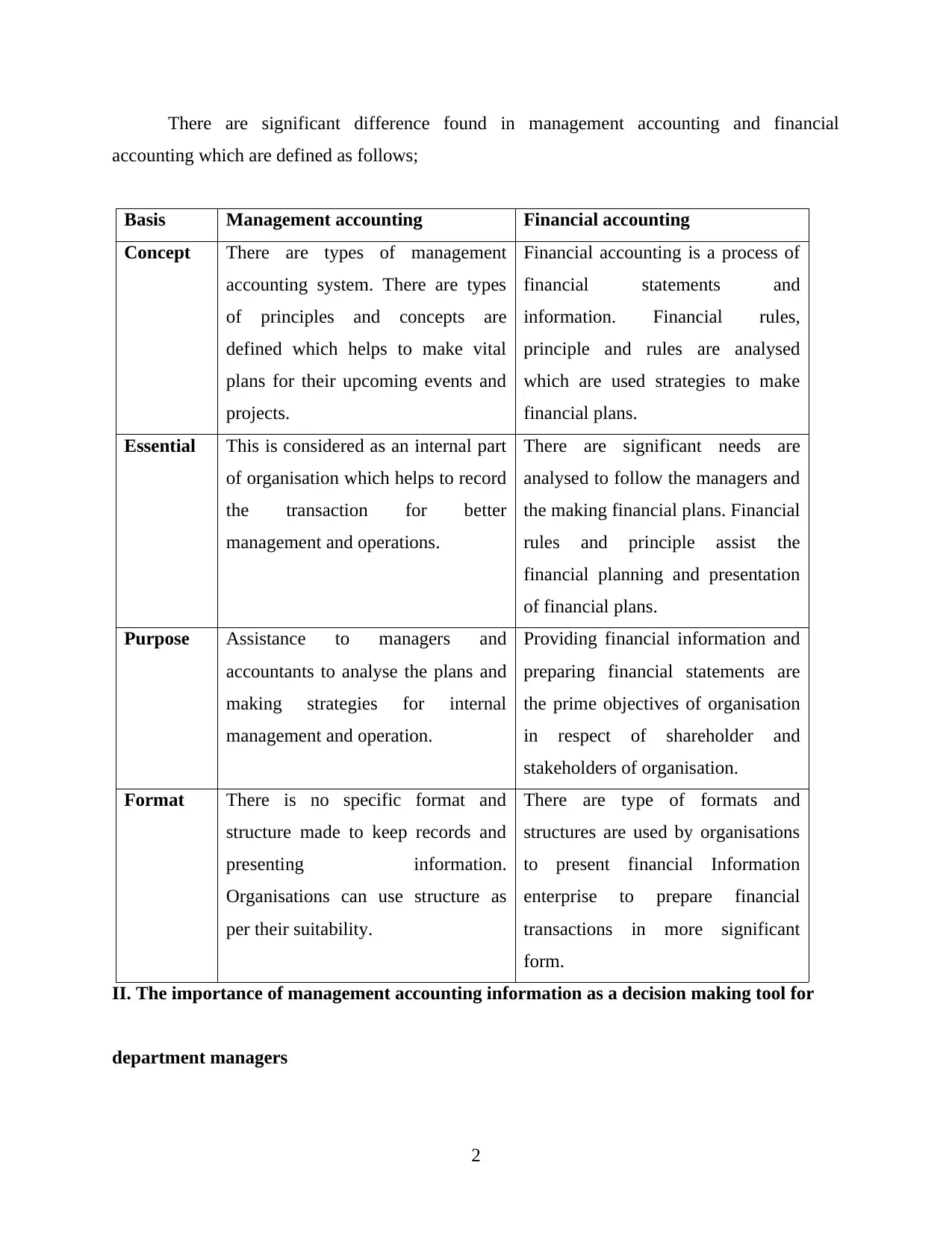

I. Distinguishing Management Accounting from Financial Accounting

1

Effective management and operations are the essential requirement of organisation in

order to attain desired aim and objective of business (Bovens, Goodin and Schillemans, 2014).

Management accounting is an internal part of organisation which helps to manage and operate

the functions and operations of business in particular format. This report is prepared to analyse

the essential aspect of management accounting. Management accounting system provides a

structure to record the transactions and events in better way. Types of management accounting

systems and reporting methods are defined in this context. Types of reports are provided in terms

of helping and recording the data in effective and reliable manner. Tech UK Ltd is chosen

organisation in which the role of management accounting is defined.

TASK 1

a) Explain the management accounting and the essential requirement of management accounting

Management accounting

Management accounting is a considered as a management tool which assists to prepare

and manage in terms of day to day business transactions and short term managerial decision.

There are types of information and tools are analysed in terms of making effective plans and

management strategies in business. Management accounting is a concept which analyse the

overall transactions and events happened during the year and summarise the information subject

to determining the performance of organisation. Periodic reports and information are produced to

managers and the accountants which helps to manage the operations and departments of

organisation (Brewer, Sorensen and Stout, 2014).

AS per IMA (Institute of Management Accountants), Management accounting is a

profession which remains involves in management decision making and developing plans and

performance management system. It provides expertise in financial reporting and control to help

the management in the formulation and implementation of an organisation's strategy. This is one

of the essential aspect and important thing for determining the effectiveness of organisation. This

basically helps managers and accountants to make business plans, effective management and

operational strategies with effective management and operations. This is mainly associated with

taking crucial decision and management (What is management accounting system, 2018.).

I. Distinguishing Management Accounting from Financial Accounting

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

There are significant difference found in management accounting and financial

accounting which are defined as follows;

Basis Management accounting Financial accounting

Concept There are types of management

accounting system. There are types

of principles and concepts are

defined which helps to make vital

plans for their upcoming events and

projects.

Financial accounting is a process of

financial statements and

information. Financial rules,

principle and rules are analysed

which are used strategies to make

financial plans.

Essential This is considered as an internal part

of organisation which helps to record

the transaction for better

management and operations.

There are significant needs are

analysed to follow the managers and

the making financial plans. Financial

rules and principle assist the

financial planning and presentation

of financial plans.

Purpose Assistance to managers and

accountants to analyse the plans and

making strategies for internal

management and operation.

Providing financial information and

preparing financial statements are

the prime objectives of organisation

in respect of shareholder and

stakeholders of organisation.

Format There is no specific format and

structure made to keep records and

presenting information.

Organisations can use structure as

per their suitability.

There are type of formats and

structures are used by organisations

to present financial Information

enterprise to prepare financial

transactions in more significant

form.

II. The importance of management accounting information as a decision making tool for

department managers

2

accounting which are defined as follows;

Basis Management accounting Financial accounting

Concept There are types of management

accounting system. There are types

of principles and concepts are

defined which helps to make vital

plans for their upcoming events and

projects.

Financial accounting is a process of

financial statements and

information. Financial rules,

principle and rules are analysed

which are used strategies to make

financial plans.

Essential This is considered as an internal part

of organisation which helps to record

the transaction for better

management and operations.

There are significant needs are

analysed to follow the managers and

the making financial plans. Financial

rules and principle assist the

financial planning and presentation

of financial plans.

Purpose Assistance to managers and

accountants to analyse the plans and

making strategies for internal

management and operation.

Providing financial information and

preparing financial statements are

the prime objectives of organisation

in respect of shareholder and

stakeholders of organisation.

Format There is no specific format and

structure made to keep records and

presenting information.

Organisations can use structure as

per their suitability.

There are type of formats and

structures are used by organisations

to present financial Information

enterprise to prepare financial

transactions in more significant

form.

II. The importance of management accounting information as a decision making tool for

department managers

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Managers and accountants adopt management accounting system with in organisation in

order to maintain the records and information in effective manner. Information and data which

are produced under management accounting system are used in decision making process and

managerial decisions. There are type of management accounting information are used in decision

making which are defined as follows;

ABC costing: this is one of the effective accounting system which helps to determine the

activities that a company perform and allocate direct and indirect cost with in operations. This

system helps to prioritise the activities and functions on the basis of priorities. There are

production overheads and costs are allocated in such an manner so that traditional methods of

allocating cost would not affect (Chiwamit Modell and Yang, 2014).

Evaluation of effective information: there is a proper analysis and evaluation done in

respect of produced information and data. These information are used to affect the decision

making process and strategic planning. There are types of information which need to determine

the implication affecting the profitability of an organisation.

Relevant costing analysis: cost analysis is also determined and analyse the important

factors which remain associated with reducing cost and enhancing profitability of organisation.

Relevant information are used to make decision and strategies.

III. Cost accounting systems

cost accounting system is mainly helps to determine the overall cost of production,

manufacturing and functional cost. Minimise the cost and maximise profitability is one of the

prime objective of cost accounting system. All the cost related to indirect cost and direct cost are

considered in this context.

Actual costing: the real cost incurred in operations are considered in this cost accounting

format. Direct expenses, indirect expenses, overheads which are connected directly with

production process are considered in this costing system. There are actual cost of material cost,

actual overheads, actual quantity of the allocation base experienced during the reporting period.

Actual cost is mainly based upon direct costing and measurable cost. It is calculated as per

following formula;

Actual direct cost = Actual cost rates * Actual quantities used

Actual indirect cost = Allocated indirect cost rates * Actual quantities of the cost of

allocation bases

3

order to maintain the records and information in effective manner. Information and data which

are produced under management accounting system are used in decision making process and

managerial decisions. There are type of management accounting information are used in decision

making which are defined as follows;

ABC costing: this is one of the effective accounting system which helps to determine the

activities that a company perform and allocate direct and indirect cost with in operations. This

system helps to prioritise the activities and functions on the basis of priorities. There are

production overheads and costs are allocated in such an manner so that traditional methods of

allocating cost would not affect (Chiwamit Modell and Yang, 2014).

Evaluation of effective information: there is a proper analysis and evaluation done in

respect of produced information and data. These information are used to affect the decision

making process and strategic planning. There are types of information which need to determine

the implication affecting the profitability of an organisation.

Relevant costing analysis: cost analysis is also determined and analyse the important

factors which remain associated with reducing cost and enhancing profitability of organisation.

Relevant information are used to make decision and strategies.

III. Cost accounting systems

cost accounting system is mainly helps to determine the overall cost of production,

manufacturing and functional cost. Minimise the cost and maximise profitability is one of the

prime objective of cost accounting system. All the cost related to indirect cost and direct cost are

considered in this context.

Actual costing: the real cost incurred in operations are considered in this cost accounting

format. Direct expenses, indirect expenses, overheads which are connected directly with

production process are considered in this costing system. There are actual cost of material cost,

actual overheads, actual quantity of the allocation base experienced during the reporting period.

Actual cost is mainly based upon direct costing and measurable cost. It is calculated as per

following formula;

Actual direct cost = Actual cost rates * Actual quantities used

Actual indirect cost = Allocated indirect cost rates * Actual quantities of the cost of

allocation bases

3

Standard costing:this is one of the accounting technique which helps to analyse and

construct the accounting structure in effective manner (EBRAHIMI and MOGHADASPOUR,

2015). Reduction of cost is based upon standards and actual cost. Difference between actual and

standard cost are analysed by variance analysis approach. This mainly remains associated with

manufacturing budgets, planning of profit, making master budgets and the accounting year.

There are types of accounts made for maintain the records and data related to inventories and the

cost of hoods are sold to the standard cost by direct material, direct labour and the cost of goods

sold.

Normal costing: this is a system which helps to determined the cost of manufactured

products, direct cost and manufacturing based upon predetermined rate. It is mainly associated

with analysing the actual direct and labour cost with estimating the overheads cost.

IV. Inventory management systems

this is the system which helps to mange the level of inventories and the management.

There are type of inventory valuation methods are analysed in this context which. Inventory

management system helps to determine the cost of stock and inventories are defined in this

context. This basically assist the managers and accountants to manage the level of economic

order quantity (Klychova, Faskhutdinova and Sadrieva, 2014). Effective use of management

accounting techniques used in inventory management which are defined as follows;

FIFO: this is the method which helps to determined the essential aspect in terms of

analysing the cost of inventories on the basis of first introduced with in production process and

evaluate the profitability. This is the method which is approved by GAAP restrictions on the use

of FIFO at the reporting financial outcomes.

LIFO: this method is basically helps to determined the cost of inventories on the basis of

inventories and stock incurred last and sold first. There are certain business analysed in terms of

new items are sold out at priority basis. This method is used in organisation which deals in

seasonable inventories.

AVCO: this is also one of the method which helps to determine the cost of inventories by

consolidating all the cost and average cost method. There are type of similar as average cost

method which are analysing the total value of ending stock and cost of sales (Lavia López and

Hiebl, 2014).

4

construct the accounting structure in effective manner (EBRAHIMI and MOGHADASPOUR,

2015). Reduction of cost is based upon standards and actual cost. Difference between actual and

standard cost are analysed by variance analysis approach. This mainly remains associated with

manufacturing budgets, planning of profit, making master budgets and the accounting year.

There are types of accounts made for maintain the records and data related to inventories and the

cost of hoods are sold to the standard cost by direct material, direct labour and the cost of goods

sold.

Normal costing: this is a system which helps to determined the cost of manufactured

products, direct cost and manufacturing based upon predetermined rate. It is mainly associated

with analysing the actual direct and labour cost with estimating the overheads cost.

IV. Inventory management systems

this is the system which helps to mange the level of inventories and the management.

There are type of inventory valuation methods are analysed in this context which. Inventory

management system helps to determine the cost of stock and inventories are defined in this

context. This basically assist the managers and accountants to manage the level of economic

order quantity (Klychova, Faskhutdinova and Sadrieva, 2014). Effective use of management

accounting techniques used in inventory management which are defined as follows;

FIFO: this is the method which helps to determined the essential aspect in terms of

analysing the cost of inventories on the basis of first introduced with in production process and

evaluate the profitability. This is the method which is approved by GAAP restrictions on the use

of FIFO at the reporting financial outcomes.

LIFO: this method is basically helps to determined the cost of inventories on the basis of

inventories and stock incurred last and sold first. There are certain business analysed in terms of

new items are sold out at priority basis. This method is used in organisation which deals in

seasonable inventories.

AVCO: this is also one of the method which helps to determine the cost of inventories by

consolidating all the cost and average cost method. There are type of similar as average cost

method which are analysing the total value of ending stock and cost of sales (Lavia López and

Hiebl, 2014).

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

V. Job costing systems

This is one of the essential aspect in respect of determining the cost of products instead of

measure the total assign products and cost. Basically this method helps to record the group of

products. There are type of accounting systems are used by organisations in terms of providing

information related to particular department and section. This costing system helps to bifurcate

the level of cost among different department of organisation.

Batch costing: this is also the costing system which helps to determine the cost of per

order and analyse the cost of particular job. Organisations which deals in multiple

products are utilised in terms of determine the cost of operations in terms of determining

the produces.

Contract costing: there are type of contracts are analysed in terms of determining the

related prospective associated with projects and tasks. This also helps to examine the cost

of projects and related to specific contract.

Service costing: this method helps to bifurcate the level of operations and management

of various services in accordance of producing products during the time.

Process costing: this costing helps to analyse the cost of production which remain

bifurcated in various stages. These process mainly associated with analysing the cost of

operations at particular process.

b) Presenting financial information

There are types of management information and data are produced under management

accounting system which are used in decision making strategies and making plans. These reports

are produced as follows;

Exception reports: reports which remain associated with analysing the structure of

business at particular range. These reports can not be produced in without prior approval of

senior authorities and management authorities. This kind of reports basically helps to manage the

reports are analysed with different department.

Schedule reports: these are the reports which are produce the reports related to plan

structure and deadline strategies. There is a particular dashboard is prepared in terms of

managing the operations and business in effective manner (Nørreklit, 2014).

Performance report: it is reported that various type of management accounting systems

are analysed in respect of determining the essential aspects related to suitability of organisation.

5

This is one of the essential aspect in respect of determining the cost of products instead of

measure the total assign products and cost. Basically this method helps to record the group of

products. There are type of accounting systems are used by organisations in terms of providing

information related to particular department and section. This costing system helps to bifurcate

the level of cost among different department of organisation.

Batch costing: this is also the costing system which helps to determine the cost of per

order and analyse the cost of particular job. Organisations which deals in multiple

products are utilised in terms of determine the cost of operations in terms of determining

the produces.

Contract costing: there are type of contracts are analysed in terms of determining the

related prospective associated with projects and tasks. This also helps to examine the cost

of projects and related to specific contract.

Service costing: this method helps to bifurcate the level of operations and management

of various services in accordance of producing products during the time.

Process costing: this costing helps to analyse the cost of production which remain

bifurcated in various stages. These process mainly associated with analysing the cost of

operations at particular process.

b) Presenting financial information

There are types of management information and data are produced under management

accounting system which are used in decision making strategies and making plans. These reports

are produced as follows;

Exception reports: reports which remain associated with analysing the structure of

business at particular range. These reports can not be produced in without prior approval of

senior authorities and management authorities. This kind of reports basically helps to manage the

reports are analysed with different department.

Schedule reports: these are the reports which are produce the reports related to plan

structure and deadline strategies. There is a particular dashboard is prepared in terms of

managing the operations and business in effective manner (Nørreklit, 2014).

Performance report: it is reported that various type of management accounting systems

are analysed in respect of determining the essential aspects related to suitability of organisation.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

There are type of management information and related to define the real situation and apsetcs are

considered in this context.

Inventory management report: this is one of the essential system which helps to

determine the cost of operations and management in effective manner. This majorly helps to

bifurcate the cost of operations and analyse the essential aspects related to determine preliminary

and secondary aspects related to growth and efficiency of organisation (Quinn2014).

Accounting receivable reports: these are the reports helps to determine the amount of

business in terms of determining the amount to be received from debtors of organisation. There

are type of information and reporting systems are used in respect of recovery which is mainly

associated with overdue and bed debts accounts. These reports helps managers and accountant to

make effective payment policies and strategies for effective management and operations.

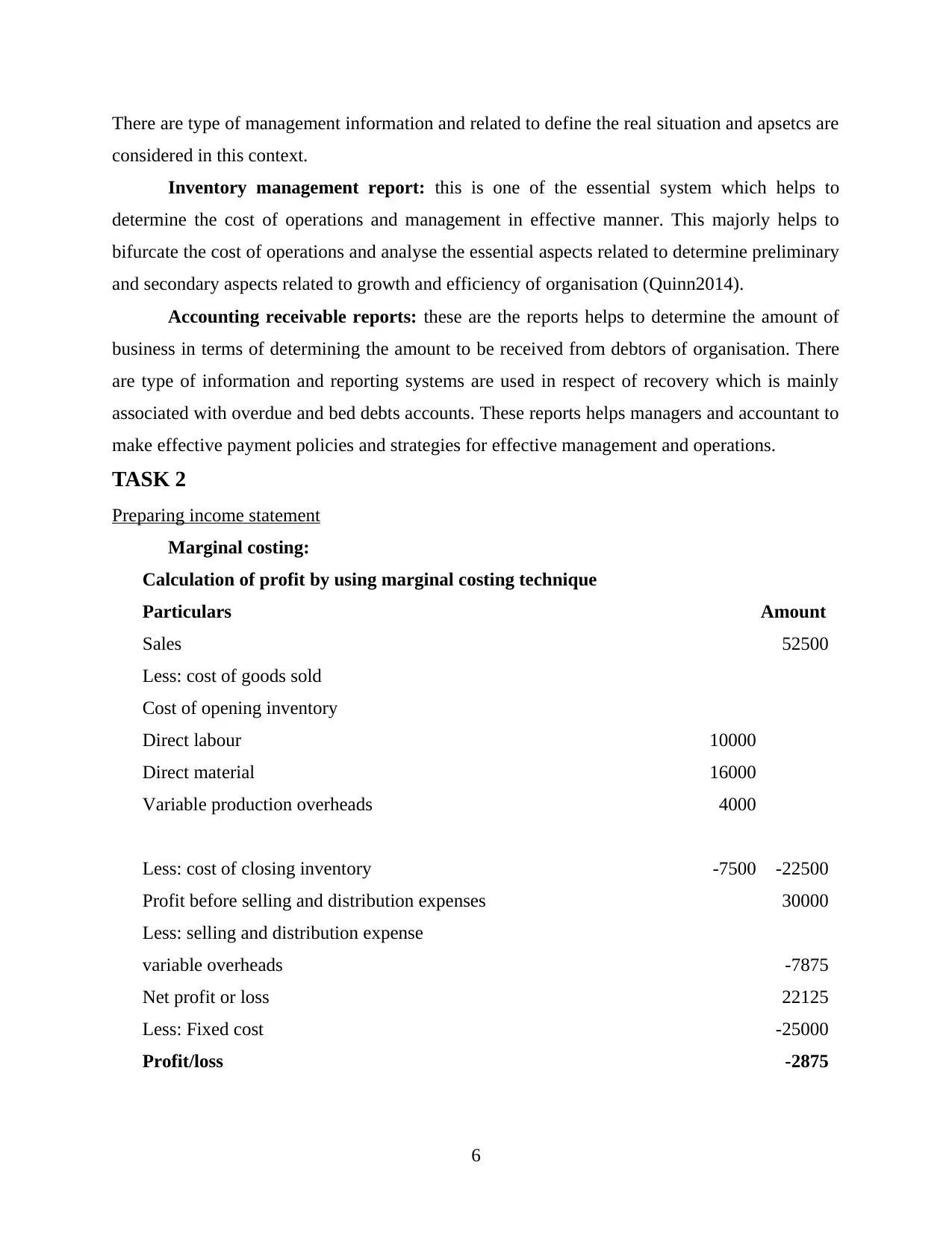

TASK 2

Preparing income statement

Marginal costing:

Calculation of profit by using marginal costing technique

Particulars Amount

Sales 52500

Less: cost of goods sold

Cost of opening inventory

Direct labour 10000

Direct material 16000

Variable production overheads 4000

Less: cost of closing inventory -7500 -22500

Profit before selling and distribution expenses 30000

Less: selling and distribution expense

variable overheads -7875

Net profit or loss 22125

Less: Fixed cost -25000

Profit/loss -2875

6

considered in this context.

Inventory management report: this is one of the essential system which helps to

determine the cost of operations and management in effective manner. This majorly helps to

bifurcate the cost of operations and analyse the essential aspects related to determine preliminary

and secondary aspects related to growth and efficiency of organisation (Quinn2014).

Accounting receivable reports: these are the reports helps to determine the amount of

business in terms of determining the amount to be received from debtors of organisation. There

are type of information and reporting systems are used in respect of recovery which is mainly

associated with overdue and bed debts accounts. These reports helps managers and accountant to

make effective payment policies and strategies for effective management and operations.

TASK 2

Preparing income statement

Marginal costing:

Calculation of profit by using marginal costing technique

Particulars Amount

Sales 52500

Less: cost of goods sold

Cost of opening inventory

Direct labour 10000

Direct material 16000

Variable production overheads 4000

Less: cost of closing inventory -7500 -22500

Profit before selling and distribution expenses 30000

Less: selling and distribution expense

variable overheads -7875

Net profit or loss 22125

Less: Fixed cost -25000

Profit/loss -2875

6

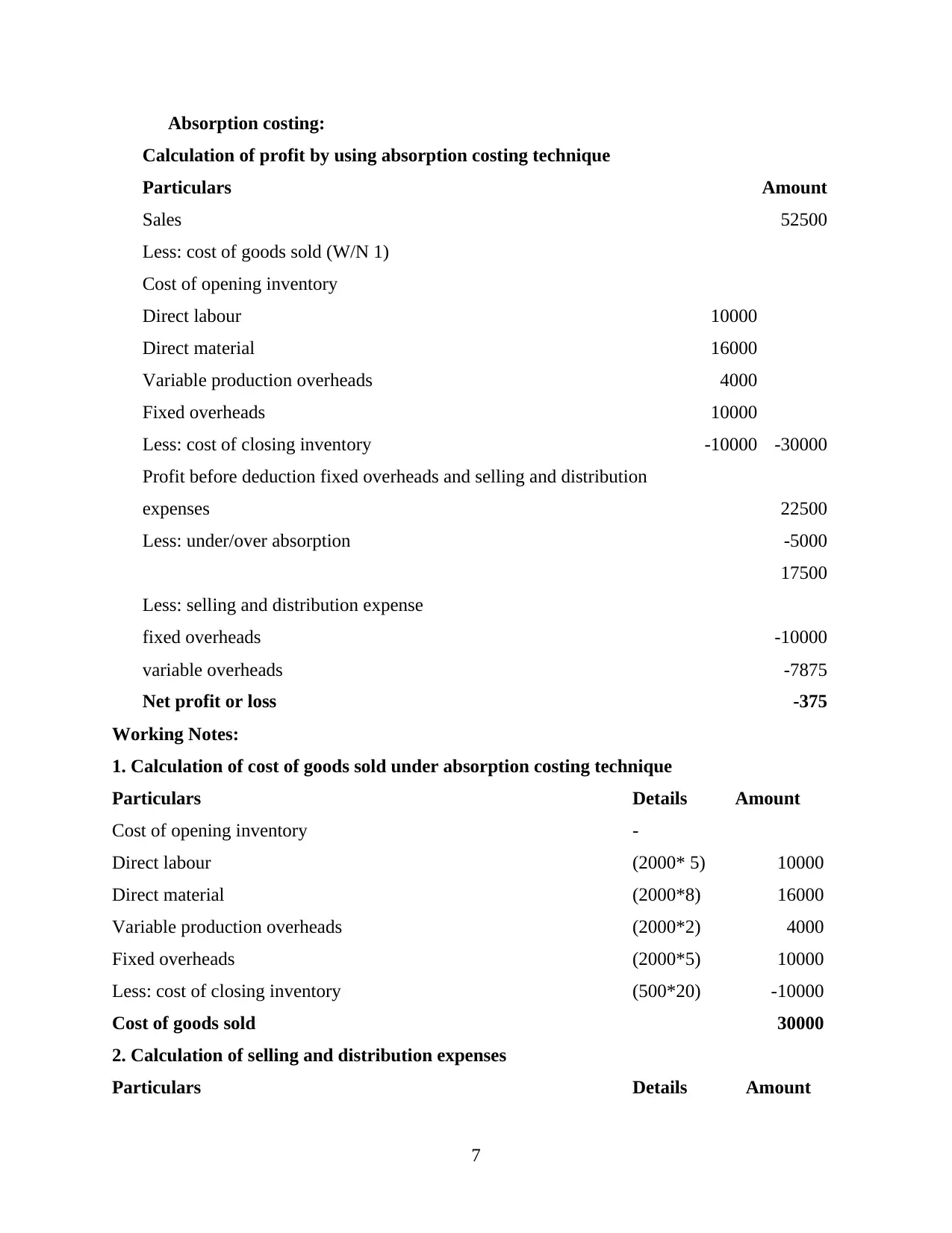

Absorption costing:

Calculation of profit by using absorption costing technique

Particulars Amount

Sales 52500

Less: cost of goods sold (W/N 1)

Cost of opening inventory

Direct labour 10000

Direct material 16000

Variable production overheads 4000

Fixed overheads 10000

Less: cost of closing inventory -10000 -30000

Profit before deduction fixed overheads and selling and distribution

expenses 22500

Less: under/over absorption -5000

17500

Less: selling and distribution expense

fixed overheads -10000

variable overheads -7875

Net profit or loss -375

Working Notes:

1. Calculation of cost of goods sold under absorption costing technique

Particulars Details Amount

Cost of opening inventory -

Direct labour (2000* 5) 10000

Direct material (2000*8) 16000

Variable production overheads (2000*2) 4000

Fixed overheads (2000*5) 10000

Less: cost of closing inventory (500*20) -10000

Cost of goods sold 30000

2. Calculation of selling and distribution expenses

Particulars Details Amount

7

Calculation of profit by using absorption costing technique

Particulars Amount

Sales 52500

Less: cost of goods sold (W/N 1)

Cost of opening inventory

Direct labour 10000

Direct material 16000

Variable production overheads 4000

Fixed overheads 10000

Less: cost of closing inventory -10000 -30000

Profit before deduction fixed overheads and selling and distribution

expenses 22500

Less: under/over absorption -5000

17500

Less: selling and distribution expense

fixed overheads -10000

variable overheads -7875

Net profit or loss -375

Working Notes:

1. Calculation of cost of goods sold under absorption costing technique

Particulars Details Amount

Cost of opening inventory -

Direct labour (2000* 5) 10000

Direct material (2000*8) 16000

Variable production overheads (2000*2) 4000

Fixed overheads (2000*5) 10000

Less: cost of closing inventory (500*20) -10000

Cost of goods sold 30000

2. Calculation of selling and distribution expenses

Particulars Details Amount

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

fixed overheads 10000

variable overheads (52500*15%) 7875

Total selling and distribution expenses 17875

3. Calculation of cost of goods sold under marginal costing technique

Particulars Details Amount

Cost of opening inventory -

Direct labour (2000* 5) 10000

Direct material (2000*8) 16000

Variable production overheads (2000*2) 4000

Less: cost of closing inventory (500*15) 7500

Cost of goods sold 22500

TASK 3

Budgetary control process, types of budgeting tools and importance

Incremental planning

An Incremental spending plan is a spending which is shaped by executing a last year

spending plan or genuine execution as frame on the premise with the incremental sum which

have been included for the new spending time frame (Renz and Herman, 2016).

Designation of assets is depended upon allotment from the prior period.

This approach does not alluded as it neglects to shape into account dynamic conditions.

Besides, this invigorates "spending up to the monetary allowance" to help a reasonable

designation in the following time frame. This develop to a "spend it or lose" mindset.

Focal points of incremental planning:

The monetary allowance is steady and dynamic is progressive. Points of interest could work their

specialties on a settled premise. Framework is helpfully easy to work and straightforward

(Schaltegger and Burritt, 2017).

Clashes must be maintained a strategic distance from if the offices could be viewed as

same.

Co-appointment between spending plans is more straightforward to accomplish.

The impact of progress could be outlined quick.

Detriments of incremental planning

8

variable overheads (52500*15%) 7875

Total selling and distribution expenses 17875

3. Calculation of cost of goods sold under marginal costing technique

Particulars Details Amount

Cost of opening inventory -

Direct labour (2000* 5) 10000

Direct material (2000*8) 16000

Variable production overheads (2000*2) 4000

Less: cost of closing inventory (500*15) 7500

Cost of goods sold 22500

TASK 3

Budgetary control process, types of budgeting tools and importance

Incremental planning

An Incremental spending plan is a spending which is shaped by executing a last year

spending plan or genuine execution as frame on the premise with the incremental sum which

have been included for the new spending time frame (Renz and Herman, 2016).

Designation of assets is depended upon allotment from the prior period.

This approach does not alluded as it neglects to shape into account dynamic conditions.

Besides, this invigorates "spending up to the monetary allowance" to help a reasonable

designation in the following time frame. This develop to a "spend it or lose" mindset.

Focal points of incremental planning:

The monetary allowance is steady and dynamic is progressive. Points of interest could work their

specialties on a settled premise. Framework is helpfully easy to work and straightforward

(Schaltegger and Burritt, 2017).

Clashes must be maintained a strategic distance from if the offices could be viewed as

same.

Co-appointment between spending plans is more straightforward to accomplish.

The impact of progress could be outlined quick.

Detriments of incremental planning

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accept undertakings and devices of working would be consistent in the comparative way.

No motivation for developing new thoughts.

No motivation to restrain costs.

Elevate spending up to the monetary allowance from this time forward spending plan is

kept up one year from now.

The monetary allowance may wind up obsolete and never again associated with the level

of action or sorts of work being presented.

The significance for assets may have fluctuated as the monetary allowance is made

successfully.

There may be a budgetary slack into the financial plan, which isn't looked into

administrators that may have overestimated their required.

Zero Based Planning

ZBB is a planning methodology which designates finance that are depended upon the

program effectively and significance rather than spending history. Rather than conventional

planning, no item is naturally contains in the following spending plan. In ZBB, budgeters survey

each program and consumptions amid of each spending cycle and that must sensible every item

to attain financing (Robalo, 2014). Spending producer could execute ZBB to any sorts of costs:

capital uses; operational costs; deals, general and regulatory costs; showcasing expenses; or cost

of offers. At the pinnacle time, ZBB produces radical investment funds and frees firms from the

entranched offices and devices. Whenever unsuccessful, company's expenses could be received.

Points of interest:

Rise spending plan is very supported and identified with methodology.

Catalyzes more extensive converge all through the association.

Help cost restricting by dismissal programmed spending improves, for the most part rise

in investment funds.

Upgrades tasks efficiencies by testing of estimation.

Impediments:

Exorbitant, complex and tedious as spending plan is improved without any preparation

yearly, while advantageously and snappy customary planning needs support just for incremental

changes. ZBB is hazardous at the season of potential reserve funds are not settled.

9

No motivation for developing new thoughts.

No motivation to restrain costs.

Elevate spending up to the monetary allowance from this time forward spending plan is

kept up one year from now.

The monetary allowance may wind up obsolete and never again associated with the level

of action or sorts of work being presented.

The significance for assets may have fluctuated as the monetary allowance is made

successfully.

There may be a budgetary slack into the financial plan, which isn't looked into

administrators that may have overestimated their required.

Zero Based Planning

ZBB is a planning methodology which designates finance that are depended upon the

program effectively and significance rather than spending history. Rather than conventional

planning, no item is naturally contains in the following spending plan. In ZBB, budgeters survey

each program and consumptions amid of each spending cycle and that must sensible every item

to attain financing (Robalo, 2014). Spending producer could execute ZBB to any sorts of costs:

capital uses; operational costs; deals, general and regulatory costs; showcasing expenses; or cost

of offers. At the pinnacle time, ZBB produces radical investment funds and frees firms from the

entranched offices and devices. Whenever unsuccessful, company's expenses could be received.

Points of interest:

Rise spending plan is very supported and identified with methodology.

Catalyzes more extensive converge all through the association.

Help cost restricting by dismissal programmed spending improves, for the most part rise

in investment funds.

Upgrades tasks efficiencies by testing of estimation.

Impediments:

Exorbitant, complex and tedious as spending plan is improved without any preparation

yearly, while advantageously and snappy customary planning needs support just for incremental

changes. ZBB is hazardous at the season of potential reserve funds are not settled.

9

Action Based Planned

Action Based planning is an instrument of planning under which the errands which

happen costs in each practical region of an organization which are recorded and their

associations which are explained and evaluated (Schaltegger and Burritt, 2017). Movement

Based Costing does not just alter prior to the record for the development of the association.

Aside from ABB found for efficiencies in business activities and development spending plans

depended on these errands.

Focal points of ABB

ABB frameworks empowers for higher level of control over the planning procedure.

There are some of focal points of ABC which are as per the following:

Precise Item Expenses.

Data about Cost Conduct.

Following of exercises for the cost protest.

Better Basic leadership

Cost administration

Actualize of greater limit and cost restricting

Favorable position to benefit industry.

Negative marks of Action Based Costing:

There are such a significant number of downsides which are utilized as under:

Costly and Complex: ABC has different costs pools and assorted cost drivers and from

now on,

Choice of Drivers: Couple of crises are rise in the utilization of ABC framework, similar

to determination of costs drivers, task of basic costs, fluctuating cost driver rates

TASK 4

Importance of management accounting to respond financial problems

It is vital for an association which breaks down the cost of task in regard of upgrading

benefit of association. To accomplish center ability and manage monetary issues associations are

adjusting administration furnishing framework to support the level of task and administration.

There are numerous budgetary issues are looked by the association (Suomala, Lyly-

Yrjänäinen and Lukka, 2014). Fund is the one of the essential source which helps in powerful

10

Action Based planning is an instrument of planning under which the errands which

happen costs in each practical region of an organization which are recorded and their

associations which are explained and evaluated (Schaltegger and Burritt, 2017). Movement

Based Costing does not just alter prior to the record for the development of the association.

Aside from ABB found for efficiencies in business activities and development spending plans

depended on these errands.

Focal points of ABB

ABB frameworks empowers for higher level of control over the planning procedure.

There are some of focal points of ABC which are as per the following:

Precise Item Expenses.

Data about Cost Conduct.

Following of exercises for the cost protest.

Better Basic leadership

Cost administration

Actualize of greater limit and cost restricting

Favorable position to benefit industry.

Negative marks of Action Based Costing:

There are such a significant number of downsides which are utilized as under:

Costly and Complex: ABC has different costs pools and assorted cost drivers and from

now on,

Choice of Drivers: Couple of crises are rise in the utilization of ABC framework, similar

to determination of costs drivers, task of basic costs, fluctuating cost driver rates

TASK 4

Importance of management accounting to respond financial problems

It is vital for an association which breaks down the cost of task in regard of upgrading

benefit of association. To accomplish center ability and manage monetary issues associations are

adjusting administration furnishing framework to support the level of task and administration.

There are numerous budgetary issues are looked by the association (Suomala, Lyly-

Yrjänäinen and Lukka, 2014). Fund is the one of the essential source which helps in powerful

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.