Applied Management Accounting: Analysis and Decision Making Process

VerifiedAdded on 2023/06/18

|13

|3794

|128

Report

AI Summary

This report provides a detailed overview of applied management accounting, starting with its historical roots in cost accounting and tracing its evolution through various stages. It discusses early management accounting techniques like marginal and absorption costing, illustrating their application with examples from the Legal and General Group Plc and British Associated Food. The report then transitions to modern developments in production environments, highlighting innovative techniques such as performance measurement, balanced scorecards, activity-based costing, just-in-time inventory management, and total quality management. It also explores the relationship between management accounting and other organizational functions, emphasizing the importance of coordination for achieving organizational objectives. Finally, the report delves into Michael Porter's generic management functions, value chain analysis, and the decision-making process, providing a comprehensive understanding of how management accounting contributes to strategic decision-making and competitive advantage.

APPLIED MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION..........................................................................................................................2

MAIN BODY..................................................................................................................................2

Explaining the history of MA from cost accounting regime......................................................2

Discussing early management accounting techniques................................................................3

Discussing modern development in production environment and innovative MA techniques. .6

Describing relationship with other function of organization......................................................7

Explaining Michael Porter generic management function..........................................................8

Explaining value chain analysis..................................................................................................9

Analysing decision Making process.........................................................................................10

CONCLUSION.............................................................................................................................11

REFERENCES..............................................................................................................................12

1

INTRODUCTION..........................................................................................................................2

MAIN BODY..................................................................................................................................2

Explaining the history of MA from cost accounting regime......................................................2

Discussing early management accounting techniques................................................................3

Discussing modern development in production environment and innovative MA techniques. .6

Describing relationship with other function of organization......................................................7

Explaining Michael Porter generic management function..........................................................8

Explaining value chain analysis..................................................................................................9

Analysing decision Making process.........................................................................................10

CONCLUSION.............................................................................................................................11

REFERENCES..............................................................................................................................12

1

INTRODUCTION

Management Accounting (MA) is the procedure of obtaining, analysing and managing

financial resources of organization. in the currents scenario it is important for the company to

have effective management accounting procedure to get competitive advantages in terms of

monitoring and optimizing monetary resources. The present report is based on providing

information about management accounting practical exposure to get deeper knowledge. Current

case study is involving various aspects of MA of both production and service sector. The case

study will give emphasis on management accounting techniques to provide accurate information

for analysing, interpreting and communicating crucial data. In addition to this, present report

will largely give emphasis on modern development factors affecting organizational performance

and relationship with other functions of company. It will comprise Michael Porter generic

management function, value chain analysis and decision making process.

MAIN BODY

Explaining the history of MA from cost accounting regime

MA is one of the crucial part of modern business environmental s it provides variety of

benefits that ensures smooth functioning. Cost accounting (CA) has been formulated from the

industrial revolution for creation of recording and summarizing system of financial transaction of

company. CA contribute largely in obtaining success through identifying important aspect of

business so that better decision making can be exerted to achieve competitive advantages.

Management counting’s root is found in 19th century of industrial revolution which was initially

controlled by few number of managers for its smooth functioning and evolving better practical

implementation (Caglio and Ditillo, 2021). Management and cost accounting techniques both

appeared in the US in nineteen centuries which wider scope and can be utilized in organization in

all types of industry.

MA has evolved in four stages that makes easily under stable that at what extent changes

are obtained. In prior 1959 focus was on cost assessment & financial control via taking

budgeting & costa accounting technologies. In the 1965 the concentration has shifted to provision

of data for management planning & controlling through utilization of tolls for the decision

analysis and responsibility accounting. Stage 3 has been occurred in 1985 in which attention as

given to declination of waste of resources. The last phase that is focused to enabling firm to get

2

Management Accounting (MA) is the procedure of obtaining, analysing and managing

financial resources of organization. in the currents scenario it is important for the company to

have effective management accounting procedure to get competitive advantages in terms of

monitoring and optimizing monetary resources. The present report is based on providing

information about management accounting practical exposure to get deeper knowledge. Current

case study is involving various aspects of MA of both production and service sector. The case

study will give emphasis on management accounting techniques to provide accurate information

for analysing, interpreting and communicating crucial data. In addition to this, present report

will largely give emphasis on modern development factors affecting organizational performance

and relationship with other functions of company. It will comprise Michael Porter generic

management function, value chain analysis and decision making process.

MAIN BODY

Explaining the history of MA from cost accounting regime

MA is one of the crucial part of modern business environmental s it provides variety of

benefits that ensures smooth functioning. Cost accounting (CA) has been formulated from the

industrial revolution for creation of recording and summarizing system of financial transaction of

company. CA contribute largely in obtaining success through identifying important aspect of

business so that better decision making can be exerted to achieve competitive advantages.

Management counting’s root is found in 19th century of industrial revolution which was initially

controlled by few number of managers for its smooth functioning and evolving better practical

implementation (Caglio and Ditillo, 2021). Management and cost accounting techniques both

appeared in the US in nineteen centuries which wider scope and can be utilized in organization in

all types of industry.

MA has evolved in four stages that makes easily under stable that at what extent changes

are obtained. In prior 1959 focus was on cost assessment & financial control via taking

budgeting & costa accounting technologies. In the 1965 the concentration has shifted to provision

of data for management planning & controlling through utilization of tolls for the decision

analysis and responsibility accounting. Stage 3 has been occurred in 1985 in which attention as

given to declination of waste of resources. The last phase that is focused to enabling firm to get

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

efficiency to optimize resources through suing tools in order to obtain better understanding of

customer & shareholder value and organizational creativeness. The mentioned changes have

obtained by 1995. In the initial stage it was seen as technical activity to pursuit organizational

objective then performing staff role to support line management via provision of data for

palnni9ng and monitoring. In last two phase it has taken as integral part of management

processing for getting higher efficiency.

In present time it is important for all companies irrespective of their scale of operation to

know deeper and basic knowledge about MA and CA so that proper coordination between all

areas can be established (Hadid and Al-Sayed, 2021.). These both were in extreme criticism for

their manipulation to investigate change and inability to support the management accounting

innovation. There are various changes has occurred due to remove inappropriate characteristic

and make MA more efficient and bring capability to present the comprehensive to data in

systematic manner so that over the past year more effectual decision making can become possible

for the frim. Focus of management accounting has shifted to provision of planning and

controlling information of commercial transactions by utilizing technologies such as decision

analysis. While utilizing management accounting in current scenario as compared to previous

there are various factors that are achieved to make internal processing more effective.

Discussing early management accounting techniques

It is referred as traditional accounting methods which comprises costing, budgeting,

performance evaluation, etc. the current report will emphasis on marginal and absorption costing

for getting practical exposure.

Marginal technique of cost analysis is procedure of taking expenditure incurred for an

additional unit of output. The particular method is taken into consideration for determining cost

associated with production function. In this specific traditional technique prices are determined

on the basis of marginal contribution & cost. Expenditures are classified on the basis of fixed

and variable & profitability is dependent on contribution margin (Adu-Gyamfi and Chipwere,

2020). In this type of traditional approach of costing net profitability per unit is obtained as end

outcome. This mainly concentrates on variable cost while valuing finished & WIP goods. There

are various benefits that production service sector obtains from implementing these in

organizational procedure for the purpose of costing. Firm become able to take appropriate

decision as it provides opportunity to get information regarding under and over absorption of

3

customer & shareholder value and organizational creativeness. The mentioned changes have

obtained by 1995. In the initial stage it was seen as technical activity to pursuit organizational

objective then performing staff role to support line management via provision of data for

palnni9ng and monitoring. In last two phase it has taken as integral part of management

processing for getting higher efficiency.

In present time it is important for all companies irrespective of their scale of operation to

know deeper and basic knowledge about MA and CA so that proper coordination between all

areas can be established (Hadid and Al-Sayed, 2021.). These both were in extreme criticism for

their manipulation to investigate change and inability to support the management accounting

innovation. There are various changes has occurred due to remove inappropriate characteristic

and make MA more efficient and bring capability to present the comprehensive to data in

systematic manner so that over the past year more effectual decision making can become possible

for the frim. Focus of management accounting has shifted to provision of planning and

controlling information of commercial transactions by utilizing technologies such as decision

analysis. While utilizing management accounting in current scenario as compared to previous

there are various factors that are achieved to make internal processing more effective.

Discussing early management accounting techniques

It is referred as traditional accounting methods which comprises costing, budgeting,

performance evaluation, etc. the current report will emphasis on marginal and absorption costing

for getting practical exposure.

Marginal technique of cost analysis is procedure of taking expenditure incurred for an

additional unit of output. The particular method is taken into consideration for determining cost

associated with production function. In this specific traditional technique prices are determined

on the basis of marginal contribution & cost. Expenditures are classified on the basis of fixed

and variable & profitability is dependent on contribution margin (Adu-Gyamfi and Chipwere,

2020). In this type of traditional approach of costing net profitability per unit is obtained as end

outcome. This mainly concentrates on variable cost while valuing finished & WIP goods. There

are various benefits that production service sector obtains from implementing these in

organizational procedure for the purpose of costing. Firm become able to take appropriate

decision as it provides opportunity to get information regarding under and over absorption of

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

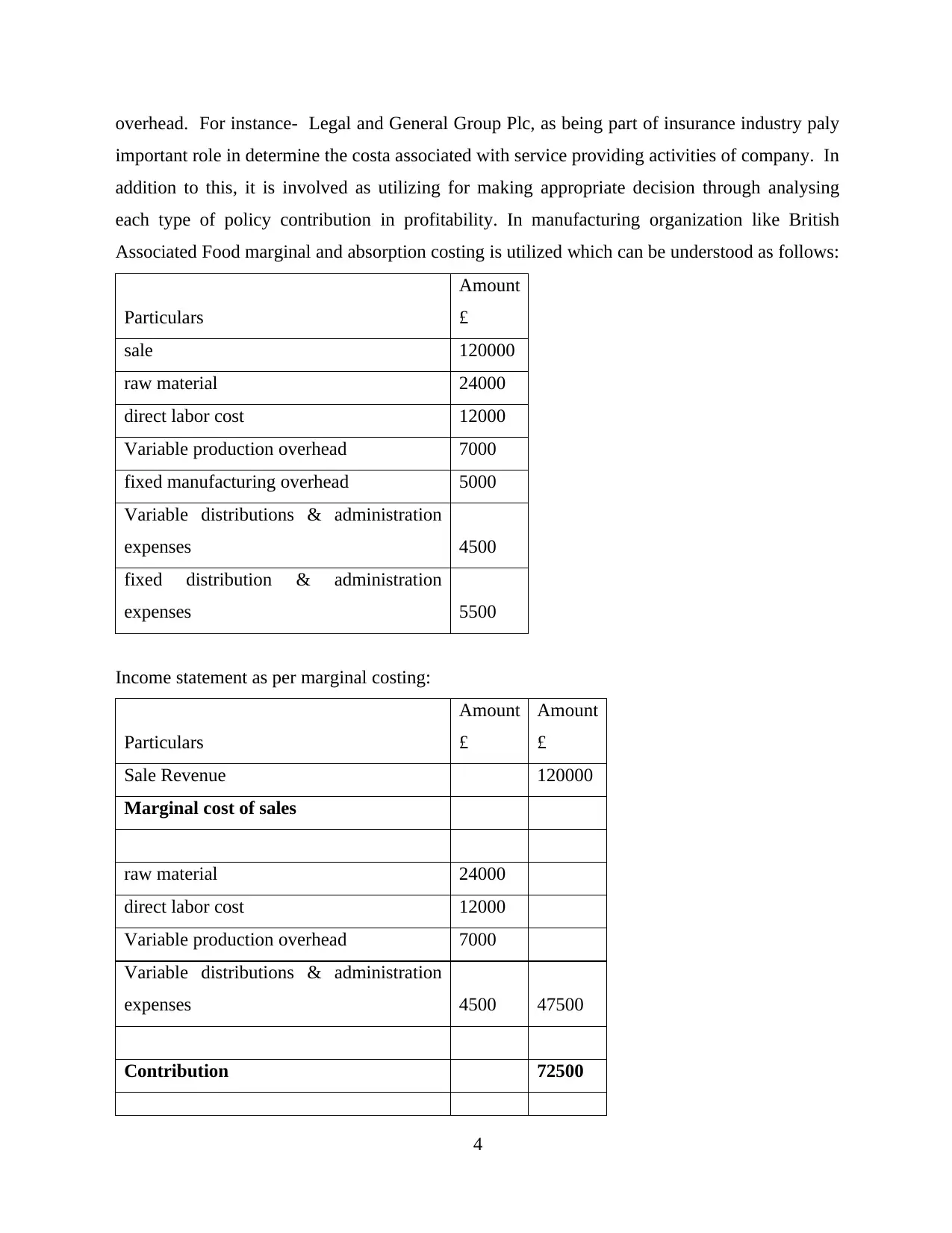

overhead. For instance- Legal and General Group Plc, as being part of insurance industry paly

important role in determine the costa associated with service providing activities of company. In

addition to this, it is involved as utilizing for making appropriate decision through analysing

each type of policy contribution in profitability. In manufacturing organization like British

Associated Food marginal and absorption costing is utilized which can be understood as follows:

Particulars

Amount

£

sale 120000

raw material 24000

direct labor cost 12000

Variable production overhead 7000

fixed manufacturing overhead 5000

Variable distributions & administration

expenses 4500

fixed distribution & administration

expenses 5500

Income statement as per marginal costing:

Particulars

Amount

£

Amount

£

Sale Revenue 120000

Marginal cost of sales

raw material 24000

direct labor cost 12000

Variable production overhead 7000

Variable distributions & administration

expenses 4500 47500

Contribution 72500

4

important role in determine the costa associated with service providing activities of company. In

addition to this, it is involved as utilizing for making appropriate decision through analysing

each type of policy contribution in profitability. In manufacturing organization like British

Associated Food marginal and absorption costing is utilized which can be understood as follows:

Particulars

Amount

£

sale 120000

raw material 24000

direct labor cost 12000

Variable production overhead 7000

fixed manufacturing overhead 5000

Variable distributions & administration

expenses 4500

fixed distribution & administration

expenses 5500

Income statement as per marginal costing:

Particulars

Amount

£

Amount

£

Sale Revenue 120000

Marginal cost of sales

raw material 24000

direct labor cost 12000

Variable production overhead 7000

Variable distributions & administration

expenses 4500 47500

Contribution 72500

4

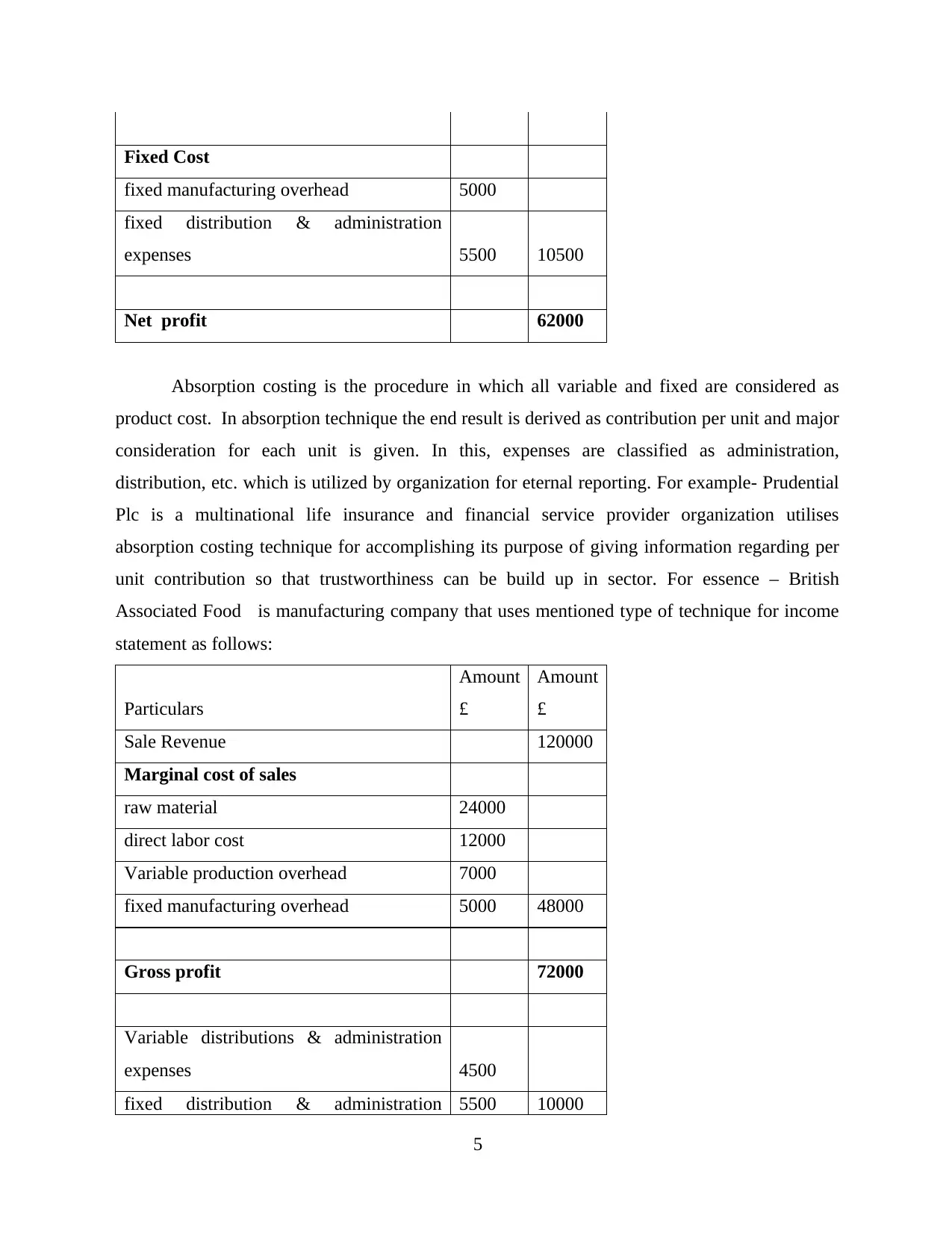

Fixed Cost

fixed manufacturing overhead 5000

fixed distribution & administration

expenses 5500 10500

Net profit 62000

Absorption costing is the procedure in which all variable and fixed are considered as

product cost. In absorption technique the end result is derived as contribution per unit and major

consideration for each unit is given. In this, expenses are classified as administration,

distribution, etc. which is utilized by organization for eternal reporting. For example- Prudential

Plc is a multinational life insurance and financial service provider organization utilises

absorption costing technique for accomplishing its purpose of giving information regarding per

unit contribution so that trustworthiness can be build up in sector. For essence – British

Associated Food is manufacturing company that uses mentioned type of technique for income

statement as follows:

Particulars

Amount

£

Amount

£

Sale Revenue 120000

Marginal cost of sales

raw material 24000

direct labor cost 12000

Variable production overhead 7000

fixed manufacturing overhead 5000 48000

Gross profit 72000

Variable distributions & administration

expenses 4500

fixed distribution & administration 5500 10000

5

fixed manufacturing overhead 5000

fixed distribution & administration

expenses 5500 10500

Net profit 62000

Absorption costing is the procedure in which all variable and fixed are considered as

product cost. In absorption technique the end result is derived as contribution per unit and major

consideration for each unit is given. In this, expenses are classified as administration,

distribution, etc. which is utilized by organization for eternal reporting. For example- Prudential

Plc is a multinational life insurance and financial service provider organization utilises

absorption costing technique for accomplishing its purpose of giving information regarding per

unit contribution so that trustworthiness can be build up in sector. For essence – British

Associated Food is manufacturing company that uses mentioned type of technique for income

statement as follows:

Particulars

Amount

£

Amount

£

Sale Revenue 120000

Marginal cost of sales

raw material 24000

direct labor cost 12000

Variable production overhead 7000

fixed manufacturing overhead 5000 48000

Gross profit 72000

Variable distributions & administration

expenses 4500

fixed distribution & administration 5500 10000

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

expenses

Net profit 62000

From the above example the difference can be understood that there how the expenses are

treated differently to obtain net profitability. On the basis of this it can be interpreted that using

absorption technique is more beneficial as it provides clear view of costing.

Discussing modern development in production environment and innovative MA techniques

In the present environment, it has become crucial for the organization to have effective

implementation of modern techniques so that better productivity to cope up with changing

scenario can be derived (Bhimani, 2020). Customer taste and preferences re changing on

frequent basis which require firm to have better production procedure in turn ability to meet

market forces can be attained. For this purpose, frim can give emphasis on following

techniques:

Performance Measurement

In manufacturing organization, it becomes essential for the firm to take look of actual

outcome derived. Firm establishes predestined goals to lead organization towards success for

this measuring performance is important (Abdusalomova, 2019). Company set the target for end

outcome in terms produced units, efficiency of employees, etc. By comparing achieved result

with set standard lacking areas and causes behind this can be identify. In order to coordinate

with changing trend of customer preferences efficiently meeting client demand become possible.

Removing lack performing aspect become possible by implementing it.

Balance scorecard

This is used to recognize, evaluate, analyze and make control in end outcome for

deriving efficiency to adapt changing circumstances. Balance score card provide assistance in

measuring growth, development, customers satisfaction, etc. These are widely used in

manufacturing companies so that better focus on financial, customer, internal and learning

aspect can be exerted for executing proper execution of operational activities (Balance

scorecard, 2021). In respect to these mentioned areas it become possible to identify factor that

do not contribute in achieving success so that suitable course of action can be taken.

Activity based Costing

6

Net profit 62000

From the above example the difference can be understood that there how the expenses are

treated differently to obtain net profitability. On the basis of this it can be interpreted that using

absorption technique is more beneficial as it provides clear view of costing.

Discussing modern development in production environment and innovative MA techniques

In the present environment, it has become crucial for the organization to have effective

implementation of modern techniques so that better productivity to cope up with changing

scenario can be derived (Bhimani, 2020). Customer taste and preferences re changing on

frequent basis which require firm to have better production procedure in turn ability to meet

market forces can be attained. For this purpose, frim can give emphasis on following

techniques:

Performance Measurement

In manufacturing organization, it becomes essential for the firm to take look of actual

outcome derived. Firm establishes predestined goals to lead organization towards success for

this measuring performance is important (Abdusalomova, 2019). Company set the target for end

outcome in terms produced units, efficiency of employees, etc. By comparing achieved result

with set standard lacking areas and causes behind this can be identify. In order to coordinate

with changing trend of customer preferences efficiently meeting client demand become possible.

Removing lack performing aspect become possible by implementing it.

Balance scorecard

This is used to recognize, evaluate, analyze and make control in end outcome for

deriving efficiency to adapt changing circumstances. Balance score card provide assistance in

measuring growth, development, customers satisfaction, etc. These are widely used in

manufacturing companies so that better focus on financial, customer, internal and learning

aspect can be exerted for executing proper execution of operational activities (Balance

scorecard, 2021). In respect to these mentioned areas it become possible to identify factor that

do not contribute in achieving success so that suitable course of action can be taken.

Activity based Costing

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Production activity highly need to adopt innovative procedures to obtain better approach

for making manufacturing function efficient & effective. In modern business environment there

is requirement of identifying and executing trending practices to get higher conversion rate

(Weetman, 2019). Activity based costing is the procedure of assigning indirect overheads to

products. It aids in having proper pricing strategy to attain large market share to lead in industry.

It aids in identifying activities essential for smooth operational procedure. It helps in getting

efficient manufacturing process to meet with customer demand.

Just in Time

It is one of the most important management strategy for monitory inventory to increase

efficiency. In addition to this, JIT procedure is most important to manage stock of firm to ensure

better productivity and efficiency (Azudin and Mansor, 2018). It aids in reducing cost

concerned with storage of stock so that better profit margin can be maintained. This tool

assures that better success with efficient processing by marinating high quality of products is

available. There is possibility of obtaining distribution in supply chain so it is crucial for firm to

use this in effective manner.

Total quality management

It is continuous procedure that assist in detecting and declining errors & mistakes

arriving in manufacturing practices. It ensures better customer experience and employees speed

up tactics that enhances revenue of firm. This modern approach is largely considered with

evaluating each step of production function in order to get standard qualitative products. TQM

helps in gaining competitive advantages in terms higher quality so that having loyal and

committed employees can be achieved.

Describing relationship with other function of organization

There variety of functions in company that are all integrated with each other and helps in

achieving organizational objectives to get higher productivity and sustainability. It can be

identified that re there are different types of model that pays attention on deriving successful

processing of business practices. Functional areas are sales, marketing, production research &

development, etc. and among all requires better coordination to build significant position in

industry. It is important for the ales department to get information from production through

having effectual management accounting technique so that available products for promoting and

targeted customer can be decided (Hiebl and Richter, 2018). Research and development paly

7

for making manufacturing function efficient & effective. In modern business environment there

is requirement of identifying and executing trending practices to get higher conversion rate

(Weetman, 2019). Activity based costing is the procedure of assigning indirect overheads to

products. It aids in having proper pricing strategy to attain large market share to lead in industry.

It aids in identifying activities essential for smooth operational procedure. It helps in getting

efficient manufacturing process to meet with customer demand.

Just in Time

It is one of the most important management strategy for monitory inventory to increase

efficiency. In addition to this, JIT procedure is most important to manage stock of firm to ensure

better productivity and efficiency (Azudin and Mansor, 2018). It aids in reducing cost

concerned with storage of stock so that better profit margin can be maintained. This tool

assures that better success with efficient processing by marinating high quality of products is

available. There is possibility of obtaining distribution in supply chain so it is crucial for firm to

use this in effective manner.

Total quality management

It is continuous procedure that assist in detecting and declining errors & mistakes

arriving in manufacturing practices. It ensures better customer experience and employees speed

up tactics that enhances revenue of firm. This modern approach is largely considered with

evaluating each step of production function in order to get standard qualitative products. TQM

helps in gaining competitive advantages in terms higher quality so that having loyal and

committed employees can be achieved.

Describing relationship with other function of organization

There variety of functions in company that are all integrated with each other and helps in

achieving organizational objectives to get higher productivity and sustainability. It can be

identified that re there are different types of model that pays attention on deriving successful

processing of business practices. Functional areas are sales, marketing, production research &

development, etc. and among all requires better coordination to build significant position in

industry. It is important for the ales department to get information from production through

having effectual management accounting technique so that available products for promoting and

targeted customer can be decided (Hiebl and Richter, 2018). Research and development paly

7

role of analysing market and giving relevant data for launching new products according to

prevailing trend in turn higher customers’ satisfaction can be obtained. Planning, allocating,

directing, controlling is some of the functions that assist in optimum utilization of resources.

This gives convenience in building effectual pattern of working in firm via getting relevant and

sufficient information from implementing management accounting. MA equally focus on all

segment that require cost and resources to meet set gaols of firm so that desirable profitability

can be obtained by properly allocating and monitoring resources. The relationship can be

understood by focusing on management accounting practices that gives insights to other

functions regarding available resources, funds, etc. to manage their roles and responsibility.

With help of these it become possible to determine production capacity, budget of marketing &

promotion, etc.

Describing the functions can be derived from following:

Explaining Michael Porter generic management function

It is one of the strategy that provide assistance in identifying suitable strategy for smooth

functioning. This focuses on getting competitive advantages in company so that profitability

and sustainability in industry can become possible. There is involvement of matrix that specifies

company can get competitive benefit by targeting narrow or broad segment via lowering cost or

offering differentiating characteristics. It involves cost leadership, differentiation and focus

strategy.

Cost leadership strategy

It is one of the part of Michael Porters generic management function that targets

customers who are price sensitive (Porter's Generic Competitive Strategies, 2021). Cost

leadership strategy is effective for those firm who has ability to offer lower price to attract

customer by marinating desirable level of profitability and sustainability in industry. It is exerted

by adopting three approaches such as high utilization of resources, lower direct & indirect

operating cost and controlling value chain containing all functions like marketing, sales,

production, etc. each approach is adopted according to suitability to so better cost leadership

strategy can effectively have implemented. It has limitation as well such as there is no assurance

of getting loyal customers as they can switch to lower priced substitute.

Differentiation strategy

8

prevailing trend in turn higher customers’ satisfaction can be obtained. Planning, allocating,

directing, controlling is some of the functions that assist in optimum utilization of resources.

This gives convenience in building effectual pattern of working in firm via getting relevant and

sufficient information from implementing management accounting. MA equally focus on all

segment that require cost and resources to meet set gaols of firm so that desirable profitability

can be obtained by properly allocating and monitoring resources. The relationship can be

understood by focusing on management accounting practices that gives insights to other

functions regarding available resources, funds, etc. to manage their roles and responsibility.

With help of these it become possible to determine production capacity, budget of marketing &

promotion, etc.

Describing the functions can be derived from following:

Explaining Michael Porter generic management function

It is one of the strategy that provide assistance in identifying suitable strategy for smooth

functioning. This focuses on getting competitive advantages in company so that profitability

and sustainability in industry can become possible. There is involvement of matrix that specifies

company can get competitive benefit by targeting narrow or broad segment via lowering cost or

offering differentiating characteristics. It involves cost leadership, differentiation and focus

strategy.

Cost leadership strategy

It is one of the part of Michael Porters generic management function that targets

customers who are price sensitive (Porter's Generic Competitive Strategies, 2021). Cost

leadership strategy is effective for those firm who has ability to offer lower price to attract

customer by marinating desirable level of profitability and sustainability in industry. It is exerted

by adopting three approaches such as high utilization of resources, lower direct & indirect

operating cost and controlling value chain containing all functions like marketing, sales,

production, etc. each approach is adopted according to suitability to so better cost leadership

strategy can effectively have implemented. It has limitation as well such as there is no assurance

of getting loyal customers as they can switch to lower priced substitute.

Differentiation strategy

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Competitive advantage can be attained by setting proper features in firm’s products and

services. It suitable for this organization who targeted audience is not price sensitivity so that

attracting towards differentiating characteristics can become possible. This strategy is concerned

with obtaining competitive advantages through accurate utilization of available resources to

meet changing demand of clients in respect to get ability to charge premium prices for the

products.

Focus strategy

It is associated with offering specialised product or services to customer of niche

market. In this, strategy there is market segregation to provide good stop customer those who

are actually interested in buying so that all kept efforts can provide higher profitability and

stability in organization (Rikhardsson and Yigitbasioglu, 2018). this is widely suitable for those

frim who has appropriate segmenting technique so that customer can pay attention on firm. It is

focused that either lower prices or differentiating characteristics are offered to niche market.

These three strategy are sued by firm according to their need and suitability to obtain

better approach of processing in organization.

Explaining value chain analysis

It is exerted in company by concentrating on two types of activities such as primary and

supportive. The segregation is helps in undertraining the proper processing mong the functional

areas of organization

Primary Activities

It includes inbound, operations, outbound, marketing & sales and services which are

considered to be more important than supporting practices. Inbound practices are related to

material procurement activities such as receiving, warehousing and managing inventory (Jones,

Demirkaya and Bethmann, 2019). There is involvement of focusing on operational practices

such as turning raw material into finished goods. Distribution, packaging, shipping all function

are included into out bounding. Promotional, marketing & strategy regarding pricing are part

of marketing & sales function. Value chain analysis has given focus on functional area of after

sales service in competitive environment it plays important role in providing quality assurance to

get higher customer satisfaction.

Secondary Activities

9

services. It suitable for this organization who targeted audience is not price sensitivity so that

attracting towards differentiating characteristics can become possible. This strategy is concerned

with obtaining competitive advantages through accurate utilization of available resources to

meet changing demand of clients in respect to get ability to charge premium prices for the

products.

Focus strategy

It is associated with offering specialised product or services to customer of niche

market. In this, strategy there is market segregation to provide good stop customer those who

are actually interested in buying so that all kept efforts can provide higher profitability and

stability in organization (Rikhardsson and Yigitbasioglu, 2018). this is widely suitable for those

frim who has appropriate segmenting technique so that customer can pay attention on firm. It is

focused that either lower prices or differentiating characteristics are offered to niche market.

These three strategy are sued by firm according to their need and suitability to obtain

better approach of processing in organization.

Explaining value chain analysis

It is exerted in company by concentrating on two types of activities such as primary and

supportive. The segregation is helps in undertraining the proper processing mong the functional

areas of organization

Primary Activities

It includes inbound, operations, outbound, marketing & sales and services which are

considered to be more important than supporting practices. Inbound practices are related to

material procurement activities such as receiving, warehousing and managing inventory (Jones,

Demirkaya and Bethmann, 2019). There is involvement of focusing on operational practices

such as turning raw material into finished goods. Distribution, packaging, shipping all function

are included into out bounding. Promotional, marketing & strategy regarding pricing are part

of marketing & sales function. Value chain analysis has given focus on functional area of after

sales service in competitive environment it plays important role in providing quality assurance to

get higher customer satisfaction.

Secondary Activities

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

These are important in present workings scenario to help firm to have competitive

advantages which contribute in making all function more efficient. It comprises procurement,

technological development, human resource management and infrastructure. Value chain

analysis provide assistance in paying attention on all supporting practices that influences growth

of enterprise (Salayo and et.al., 2021.). Activities of procuring highly influences production and

supply of products. Technological development need to be given greater consideration as it is

main external factor affecting efficiency of product design, research, etc. in addition to this, it

aids in achieving ability to meet market trends. HRM play role of recruitment, hiring, training,

retention, etc. that ensures higher potential sharing of employees’ potential to reach desirable

position. Infrastructure activities regarding overhead and management involving financial

planning, etc.

Value chain analysis is utilized to get clarity regarding part of activities prevailing in

firm which enable its management accounting processing in proper way.

Analysing decision Making process

Ever organization irrespective of their type of industry makes certain crucial decisions on

daily basis that impact the functional processing of firm. There are various types challenges that

company faces and affect its growth and profitability. It becomes crucial for the company to have

proper understanding of prevailing lacking areas so that suitable course of action can be

determined.

Decision making is systematic procedure that helps company in eliminating irrelevant

factors which are irrelevant in achieving organizational objectives (Stankevich, 2017). In order

to make strategic decision company require to recognise the problem existing in its organization.

To make sure about its impact and causes firm require to collect all related information so that

deeper emphasis on this can be exerted. Identifying alternative that can resolve the issue as it

may be affecting various functions of company like planning, organizing, coordinating,

controlling, etc. which can decline growth rate of firm. In the next phase after collecting

information regarding gathered method of resolving issue. Selecting best alternative among the

chosen methods for achieving the target outcome in most efficient pattern. Taking corrective and

suitable course of practice play important role in influencing the irrelevant aspects to move

organization towards failure. The last step in formulation of particular decision is evaluate the

10

advantages which contribute in making all function more efficient. It comprises procurement,

technological development, human resource management and infrastructure. Value chain

analysis provide assistance in paying attention on all supporting practices that influences growth

of enterprise (Salayo and et.al., 2021.). Activities of procuring highly influences production and

supply of products. Technological development need to be given greater consideration as it is

main external factor affecting efficiency of product design, research, etc. in addition to this, it

aids in achieving ability to meet market trends. HRM play role of recruitment, hiring, training,

retention, etc. that ensures higher potential sharing of employees’ potential to reach desirable

position. Infrastructure activities regarding overhead and management involving financial

planning, etc.

Value chain analysis is utilized to get clarity regarding part of activities prevailing in

firm which enable its management accounting processing in proper way.

Analysing decision Making process

Ever organization irrespective of their type of industry makes certain crucial decisions on

daily basis that impact the functional processing of firm. There are various types challenges that

company faces and affect its growth and profitability. It becomes crucial for the company to have

proper understanding of prevailing lacking areas so that suitable course of action can be

determined.

Decision making is systematic procedure that helps company in eliminating irrelevant

factors which are irrelevant in achieving organizational objectives (Stankevich, 2017). In order

to make strategic decision company require to recognise the problem existing in its organization.

To make sure about its impact and causes firm require to collect all related information so that

deeper emphasis on this can be exerted. Identifying alternative that can resolve the issue as it

may be affecting various functions of company like planning, organizing, coordinating,

controlling, etc. which can decline growth rate of firm. In the next phase after collecting

information regarding gathered method of resolving issue. Selecting best alternative among the

chosen methods for achieving the target outcome in most efficient pattern. Taking corrective and

suitable course of practice play important role in influencing the irrelevant aspects to move

organization towards failure. The last step in formulation of particular decision is evaluate the

10

result with predetermined standard so that variation can be assessed to take appropriate plan to

improve it.

In order to move towards success, it is crucial to make strategic decision in all functional

areas as there is coordination among them to obtain organizational overall objective. There are

several situations which require firm to make important decision so that higher efficiency,

productivity, declining cost, etc. can be derived. This become important for the firm to focus on

all areas with proper focus to get appropriate processing in company. These mentioned

techniques are contributing in deciding important functional part to give more focus to remove

lacking performance via effective management.

CONCLUSION

From the above report it can be concluded that management accounting is crucial part of

modern business process to get competitive advantages. The current case study ha involved

revolution of management accounting from cost regime. Present report has comprised traditional

MA techniques such as marginal and absorption costing via providing practical example in the

required context. In addition to this, it has involved modern development in management

accounting techniques such as performance measurement, balance scorecard, TQM, JIT and

activity based costing. Report has given emphasis on describing relationship ith other

organization function. Present case study has focused on Michael Porter generic management

function, value chain analysis and decision making process.

11

improve it.

In order to move towards success, it is crucial to make strategic decision in all functional

areas as there is coordination among them to obtain organizational overall objective. There are

several situations which require firm to make important decision so that higher efficiency,

productivity, declining cost, etc. can be derived. This become important for the firm to focus on

all areas with proper focus to get appropriate processing in company. These mentioned

techniques are contributing in deciding important functional part to give more focus to remove

lacking performance via effective management.

CONCLUSION

From the above report it can be concluded that management accounting is crucial part of

modern business process to get competitive advantages. The current case study ha involved

revolution of management accounting from cost regime. Present report has comprised traditional

MA techniques such as marginal and absorption costing via providing practical example in the

required context. In addition to this, it has involved modern development in management

accounting techniques such as performance measurement, balance scorecard, TQM, JIT and

activity based costing. Report has given emphasis on describing relationship ith other

organization function. Present case study has focused on Michael Porter generic management

function, value chain analysis and decision making process.

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.