Analyzing Costing Methods and Planning Tools in Management Accounting

VerifiedAdded on 2023/02/02

|20

|4271

|61

Report

AI Summary

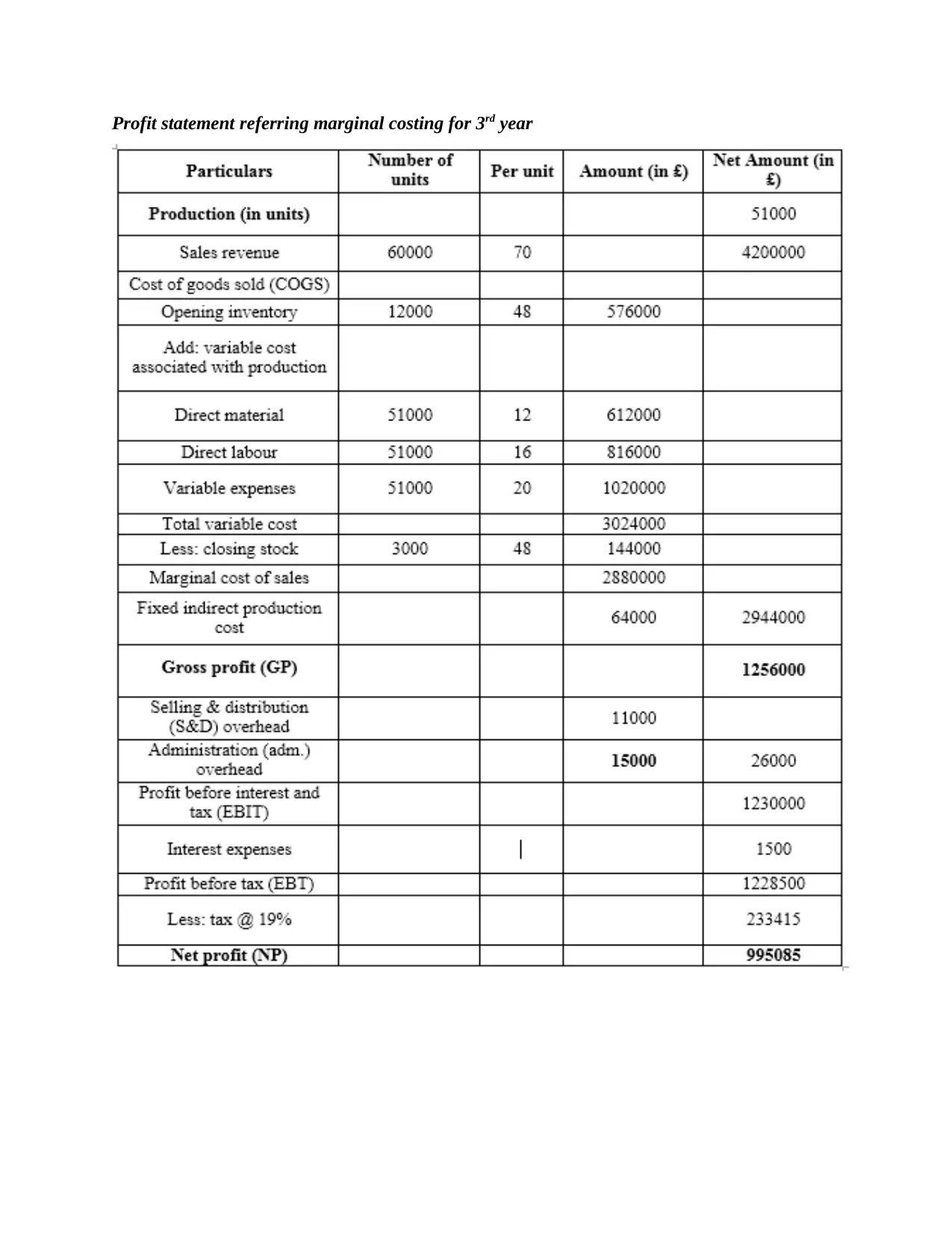

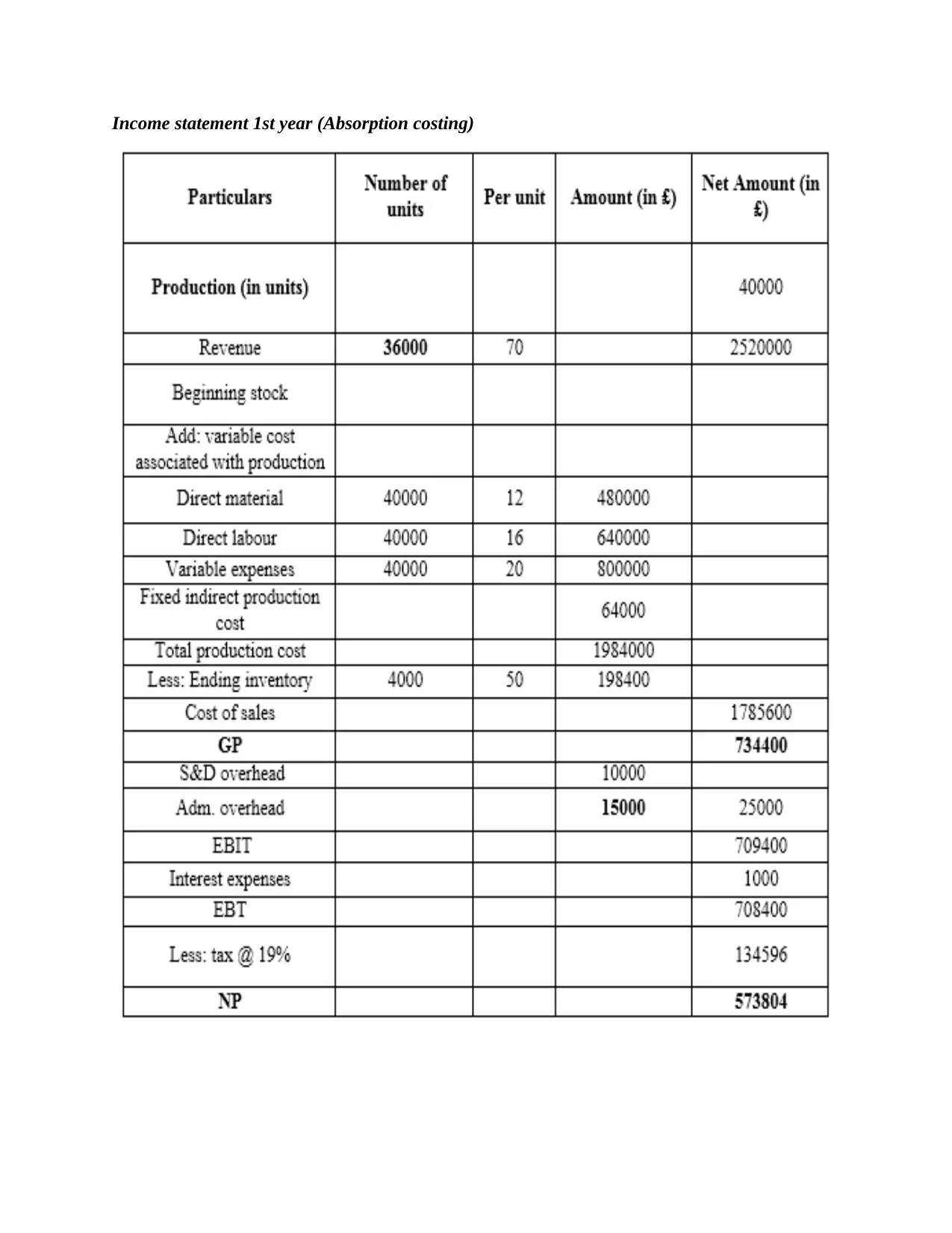

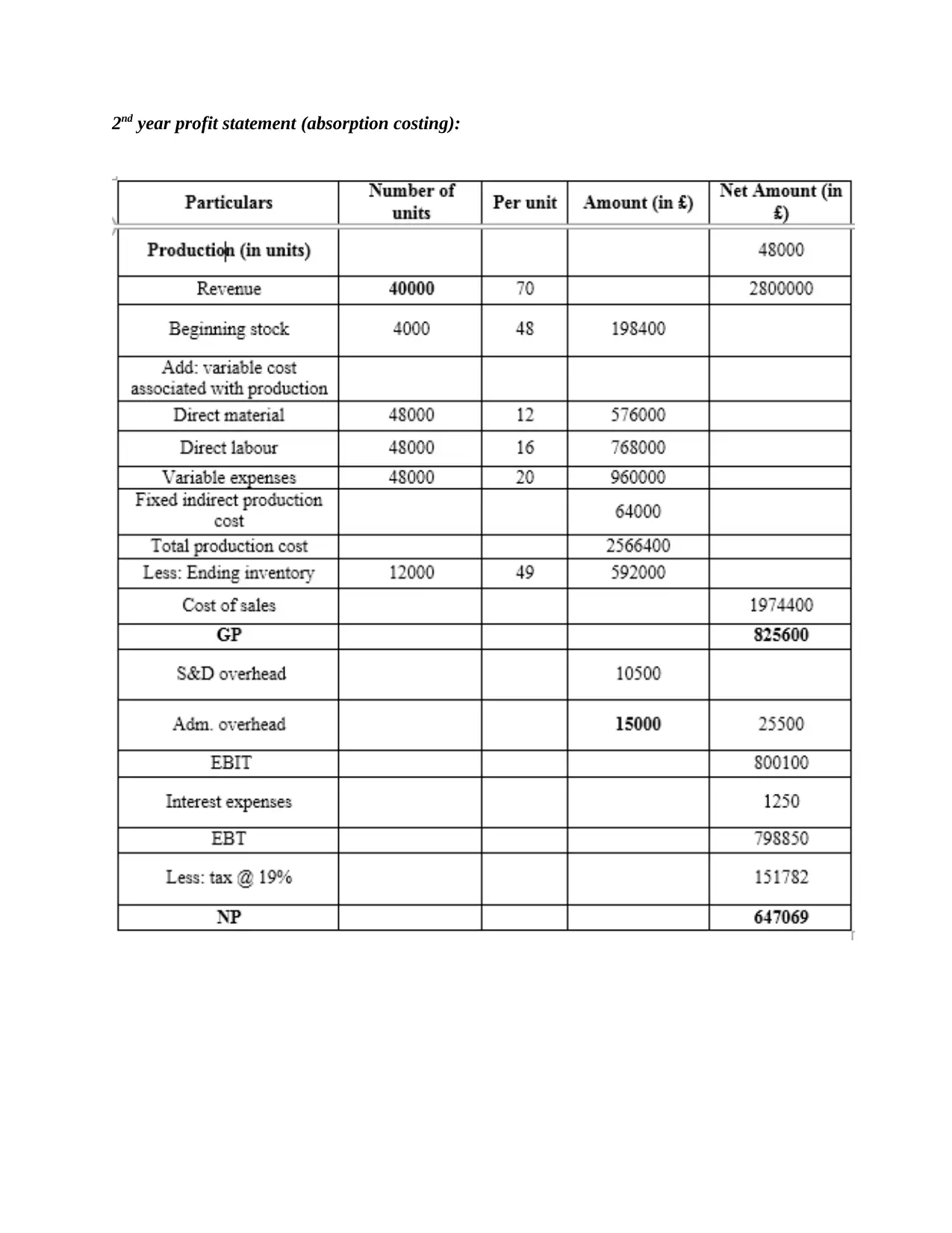

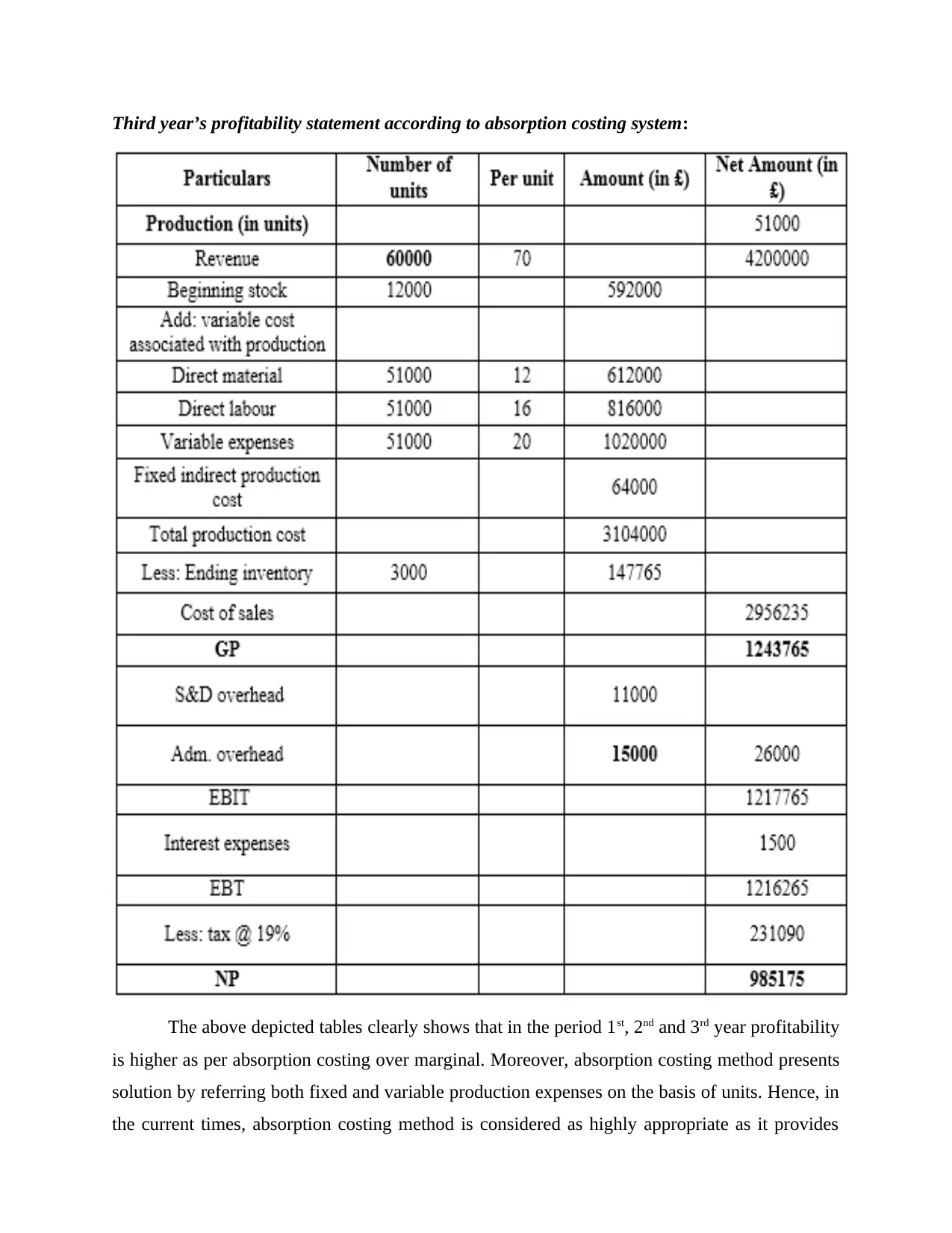

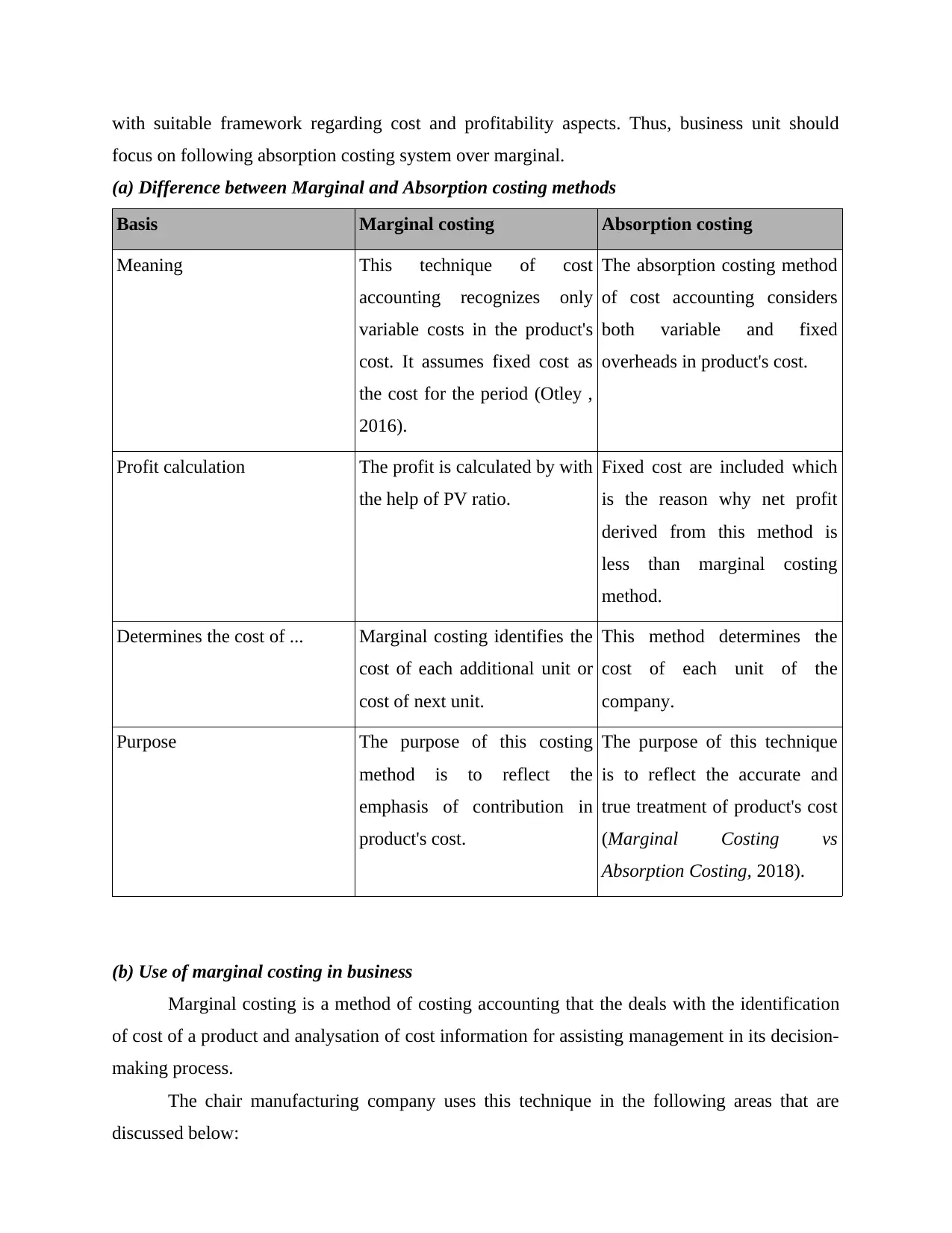

This report provides a detailed analysis of management accounting, beginning with a comparison of marginal and absorption costing methods, highlighting the differences in profit calculation and the suitability of absorption costing for providing a comprehensive view of cost and profitability. It explores the use of marginal costing in cost control, product costing, and decision-making, while also explaining the reasons for profit variances under different costing methods. Furthermore, the report discusses various planning tools used in management accounting, including fixed, flexible, and incremental budgets, outlining their advantages and disadvantages. It evaluates how organizations adapt management accounting to respond to financial problems and how management accounting contributes to sustainable success, concluding with an assessment of how planning tools aid in solving financial issues.

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.