Comprehensive Analysis of Cost and Control in Management Accounting

VerifiedAdded on 2023/06/14

|16

|3200

|184

Homework Assignment

AI Summary

This assignment solution delves into various aspects of management accounting for cost and control. It begins by explaining Michel Foucault's theory of Panopticism and its application in preventing corruption through strong auditing programs and transparency. The functions of management accounting, including planning, organizing, and decision-making, are discussed in detail. The assignment highlights the use of checklists for maintaining consistency and control, using the rock band Van Halen as an example. It provides a comprehensive manufacturing statement and income statement for Tendulkar Manufacturing Co., both in normal and formula views. Further, it explains the perpetual inventory system and the accounting treatment of overtime payments. Journal entries for material control and accrued payroll are presented, along with a detailed analysis of accrued payroll and related journal entries. Finally, the document differentiates between activity-based costing (ABC) and traditional costing methods, emphasizing the accuracy of ABC costing. Desklib offers a wide array of similar solved assignments and study resources for students.

Running head: MANAGEMENT ACCOUNTING FOR COST AND CONTROL

Management Accounting for Cost and Control

Name of the Student

Name of the University

Name of the Author

Course ID

Management Accounting for Cost and Control

Name of the Student

Name of the University

Name of the Author

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGEMENT ACCOUNTING FOR COST AND CONTROL

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................2

Answer to question 3:.................................................................................................................3

Answer to question 4:.................................................................................................................4

Answer to question 5:.................................................................................................................7

Answer to 5 A:...........................................................................................................................7

Answer to 5 B:...........................................................................................................................8

Answer to question 6:.................................................................................................................8

Answer to question 7:.................................................................................................................8

Answer to question 8:.................................................................................................................8

Part A.........................................................................................................................................8

Part B:.........................................................................................................................................9

Part C:.........................................................................................................................................9

Answer to question 9:...............................................................................................................10

Answer to question 10:.............................................................................................................12

Reference List:.........................................................................................................................14

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................2

Answer to question 3:.................................................................................................................3

Answer to question 4:.................................................................................................................4

Answer to question 5:.................................................................................................................7

Answer to 5 A:...........................................................................................................................7

Answer to 5 B:...........................................................................................................................8

Answer to question 6:.................................................................................................................8

Answer to question 7:.................................................................................................................8

Answer to question 8:.................................................................................................................8

Part A.........................................................................................................................................8

Part B:.........................................................................................................................................9

Part C:.........................................................................................................................................9

Answer to question 9:...............................................................................................................10

Answer to question 10:.............................................................................................................12

Reference List:.........................................................................................................................14

2MANAGEMENT ACCOUNTING FOR COST AND CONTROL

Answer to question 1:

Panopticism that was originally developed by the French philosopher named Michel

Foucault is referred as the social theory. Michel Foucault developed the theory of

Panopticism in his book named Discipline and Punish (Munro, 2015). The theory Panopticon

refers to the experimental laboratory of power where according to Michel Foucault the

behaviour an individual can be modified. Michel Foucault considered the theory of

Panopticon as the mark of disciplinary culture of investigation.

The theory of Panopticism under the concept of management accounting demands

attention in the specific areas of management and bookkeeping fundamentals of anti-

corruption. The theory of Panopticism helps in providing a detailed description of

impressions of inspecting and book-keeping to detect and avoid any corruption activity

(Romele et al., 2017). Panopticism is viewed as the instrument of enforcing control on the

bookkeeping records and serving as the element of reformation by reducing the stress on

financial accounting and avoiding corruption activities. The particular objective of this theory

is to eliminate the conflict of interest among the management and executives and

implementing control through strong auditing programs. Panoticism also helps in promoting

transparency of data with durable application of control on the activities of the firm.

Answer to question 2:

The functions of management accounting plays a vital role in the managerial

functions that are performed by the managers. The functions are as follows.

a. Planning: The functions of management accounting is closely related to planning as

it offers the managers with the decision making functions (Weygandt et al., 2015).

Since the entire process of budgeting is associated with the accounting related reports,

the management accounting helps in providing the managers with the estimated

Answer to question 1:

Panopticism that was originally developed by the French philosopher named Michel

Foucault is referred as the social theory. Michel Foucault developed the theory of

Panopticism in his book named Discipline and Punish (Munro, 2015). The theory Panopticon

refers to the experimental laboratory of power where according to Michel Foucault the

behaviour an individual can be modified. Michel Foucault considered the theory of

Panopticon as the mark of disciplinary culture of investigation.

The theory of Panopticism under the concept of management accounting demands

attention in the specific areas of management and bookkeeping fundamentals of anti-

corruption. The theory of Panopticism helps in providing a detailed description of

impressions of inspecting and book-keeping to detect and avoid any corruption activity

(Romele et al., 2017). Panopticism is viewed as the instrument of enforcing control on the

bookkeeping records and serving as the element of reformation by reducing the stress on

financial accounting and avoiding corruption activities. The particular objective of this theory

is to eliminate the conflict of interest among the management and executives and

implementing control through strong auditing programs. Panoticism also helps in promoting

transparency of data with durable application of control on the activities of the firm.

Answer to question 2:

The functions of management accounting plays a vital role in the managerial

functions that are performed by the managers. The functions are as follows.

a. Planning: The functions of management accounting is closely related to planning as

it offers the managers with the decision making functions (Weygandt et al., 2015).

Since the entire process of budgeting is associated with the accounting related reports,

the management accounting helps in providing the managers with the estimated

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGEMENT ACCOUNTING FOR COST AND CONTROL

impact of alternative course of actions. Therefore, planning facilitates both long and

short run business actions.

b. Organizing: Organizing demands clarity of approach regarding each of the

manager’s accountability and lines of authority. In an organization there are numerous

departments are interested as hierarchy and requires formal communication structure

to pass down the information from lower level to higher level and vice versa.

Therefore, organizing creates organizational functions and assigns the responsibility

to the people in an organization.

c. Decision making: A manager would not be able to plan without taking any decision

and is under obligation of selecting from the competing objectives (Warren & Jones,

2018). Decision making as the management functions helps in selecting from the

competing alternatives and it is an inherent functions of planning and organizing.

Answer to question 3:

A checklist is defined as the form of job that is put into the use to eliminate the

possibilities of failure by compensating for the potential limits of the human memory and

attention (Wiffen, 2016). Checklist helps in making sure that consistency is maintained and

completeness in executing the task. For the rock band Van Helen checklist assisted in

eliminating the probabilities of failure or missing out something very important. The rock

band of Van Helen asserted that checklist helped in assuring that steadiness is maintained in

completing the particular activity. Additionally, Van Helen regarded checklist as the element

of implementing control and making sure that each person that are engaged in the work able

to understand their goals and objectives.

Van Helen bought forward that checklist helped in assuring the consistency of rock

band supply of inventory and often termed that checklist was very time saving as it helped

them in keeping accounting of the required records amid the other list of objects. Van Helen

impact of alternative course of actions. Therefore, planning facilitates both long and

short run business actions.

b. Organizing: Organizing demands clarity of approach regarding each of the

manager’s accountability and lines of authority. In an organization there are numerous

departments are interested as hierarchy and requires formal communication structure

to pass down the information from lower level to higher level and vice versa.

Therefore, organizing creates organizational functions and assigns the responsibility

to the people in an organization.

c. Decision making: A manager would not be able to plan without taking any decision

and is under obligation of selecting from the competing objectives (Warren & Jones,

2018). Decision making as the management functions helps in selecting from the

competing alternatives and it is an inherent functions of planning and organizing.

Answer to question 3:

A checklist is defined as the form of job that is put into the use to eliminate the

possibilities of failure by compensating for the potential limits of the human memory and

attention (Wiffen, 2016). Checklist helps in making sure that consistency is maintained and

completeness in executing the task. For the rock band Van Helen checklist assisted in

eliminating the probabilities of failure or missing out something very important. The rock

band of Van Helen asserted that checklist helped in assuring that steadiness is maintained in

completing the particular activity. Additionally, Van Helen regarded checklist as the element

of implementing control and making sure that each person that are engaged in the work able

to understand their goals and objectives.

Van Helen bought forward that checklist helped in assuring the consistency of rock

band supply of inventory and often termed that checklist was very time saving as it helped

them in keeping accounting of the required records amid the other list of objects. Van Helen

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGEMENT ACCOUNTING FOR COST AND CONTROL

stated that using the checklist also enabled to ensure that they do not forget any form of

important steps.

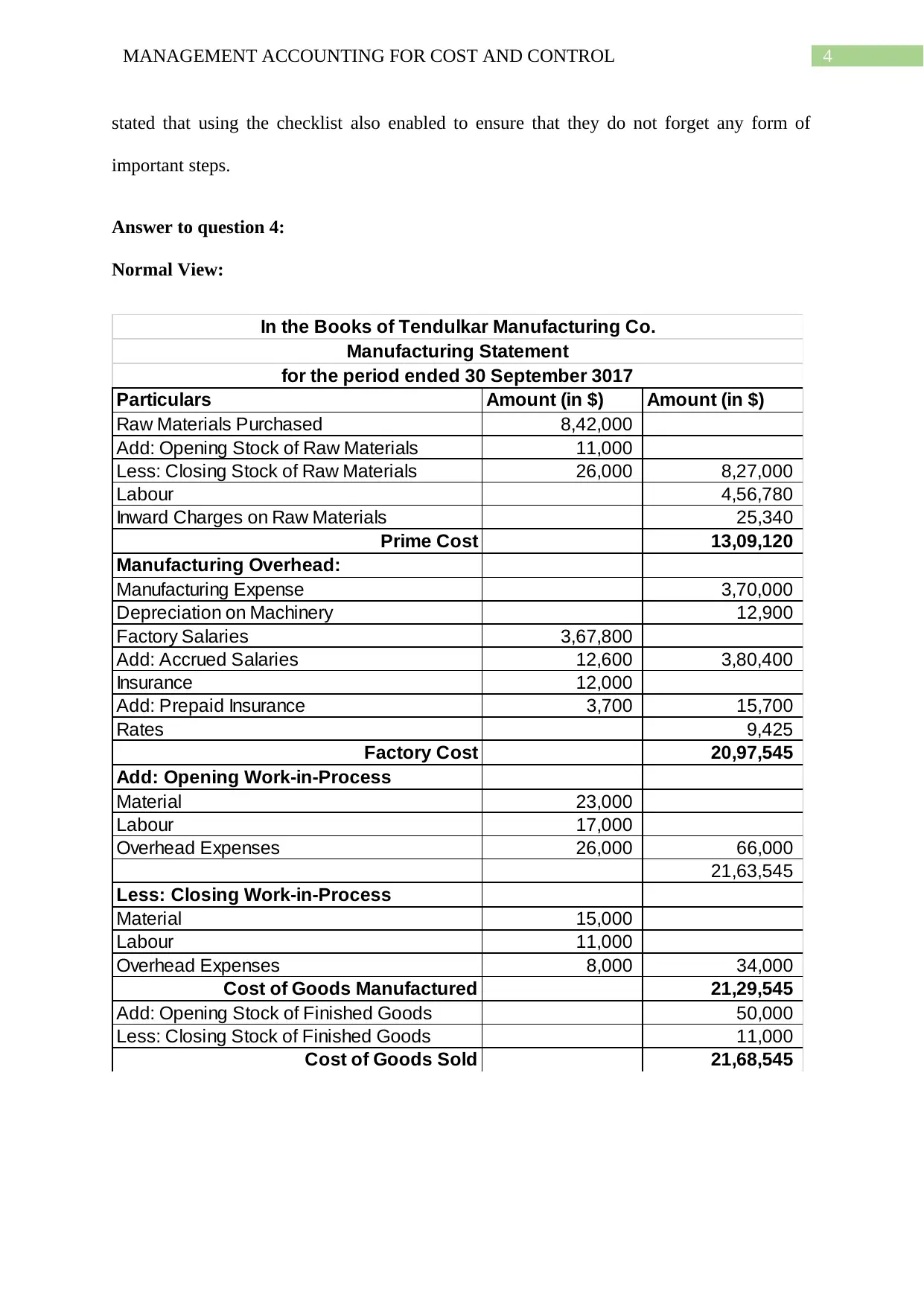

Answer to question 4:

Normal View:

Particulars Amount (in $) Amount (in $)

Raw Materials Purchased 8,42,000

Add: Opening Stock of Raw Materials 11,000

Less: Closing Stock of Raw Materials 26,000 8,27,000

Labour 4,56,780

Inward Charges on Raw Materials 25,340

Prime Cost 13,09,120

Manufacturing Overhead:

Manufacturing Expense 3,70,000

Depreciation on Machinery 12,900

Factory Salaries 3,67,800

Add: Accrued Salaries 12,600 3,80,400

Insurance 12,000

Add: Prepaid Insurance 3,700 15,700

Rates 9,425

Factory Cost 20,97,545

Add: Opening Work-in-Process

Material 23,000

Labour 17,000

Overhead Expenses 26,000 66,000

21,63,545

Less: Closing Work-in-Process

Material 15,000

Labour 11,000

Overhead Expenses 8,000 34,000

Cost of Goods Manufactured 21,29,545

Add: Opening Stock of Finished Goods 50,000

Less: Closing Stock of Finished Goods 11,000

Cost of Goods Sold 21,68,545

In the Books of Tendulkar Manufacturing Co.

Manufacturing Statement

for the period ended 30 September 3017

stated that using the checklist also enabled to ensure that they do not forget any form of

important steps.

Answer to question 4:

Normal View:

Particulars Amount (in $) Amount (in $)

Raw Materials Purchased 8,42,000

Add: Opening Stock of Raw Materials 11,000

Less: Closing Stock of Raw Materials 26,000 8,27,000

Labour 4,56,780

Inward Charges on Raw Materials 25,340

Prime Cost 13,09,120

Manufacturing Overhead:

Manufacturing Expense 3,70,000

Depreciation on Machinery 12,900

Factory Salaries 3,67,800

Add: Accrued Salaries 12,600 3,80,400

Insurance 12,000

Add: Prepaid Insurance 3,700 15,700

Rates 9,425

Factory Cost 20,97,545

Add: Opening Work-in-Process

Material 23,000

Labour 17,000

Overhead Expenses 26,000 66,000

21,63,545

Less: Closing Work-in-Process

Material 15,000

Labour 11,000

Overhead Expenses 8,000 34,000

Cost of Goods Manufactured 21,29,545

Add: Opening Stock of Finished Goods 50,000

Less: Closing Stock of Finished Goods 11,000

Cost of Goods Sold 21,68,545

In the Books of Tendulkar Manufacturing Co.

Manufacturing Statement

for the period ended 30 September 3017

5MANAGEMENT ACCOUNTING FOR COST AND CONTROL

Particulars Amount (in $) Amount (in $)

Sales of Finished Goods 38,56,000

Cost of Goods Sold 21,68,545

Gross Profit 16,87,455

Operating Expenses:

Advertising 24,000

Audit Fee 12,000

Discount Expense 3,450

Discount Revenue (5,320)

Freight Outwards 6,543

Insurance 4,000

Less: Prepaid Insurance 925 3,075

Light and Power 23,000

General Expenses 54,320

Rates 3,142

Office Salaries 35,000

Add: Accrued Office Salaries 2,340 37,340

Sales Commission 47,600

Total Operating Expenses 2,09,150

Operating Income 14,78,305

Tax Expense 56,740

Net Profit 14,21,565

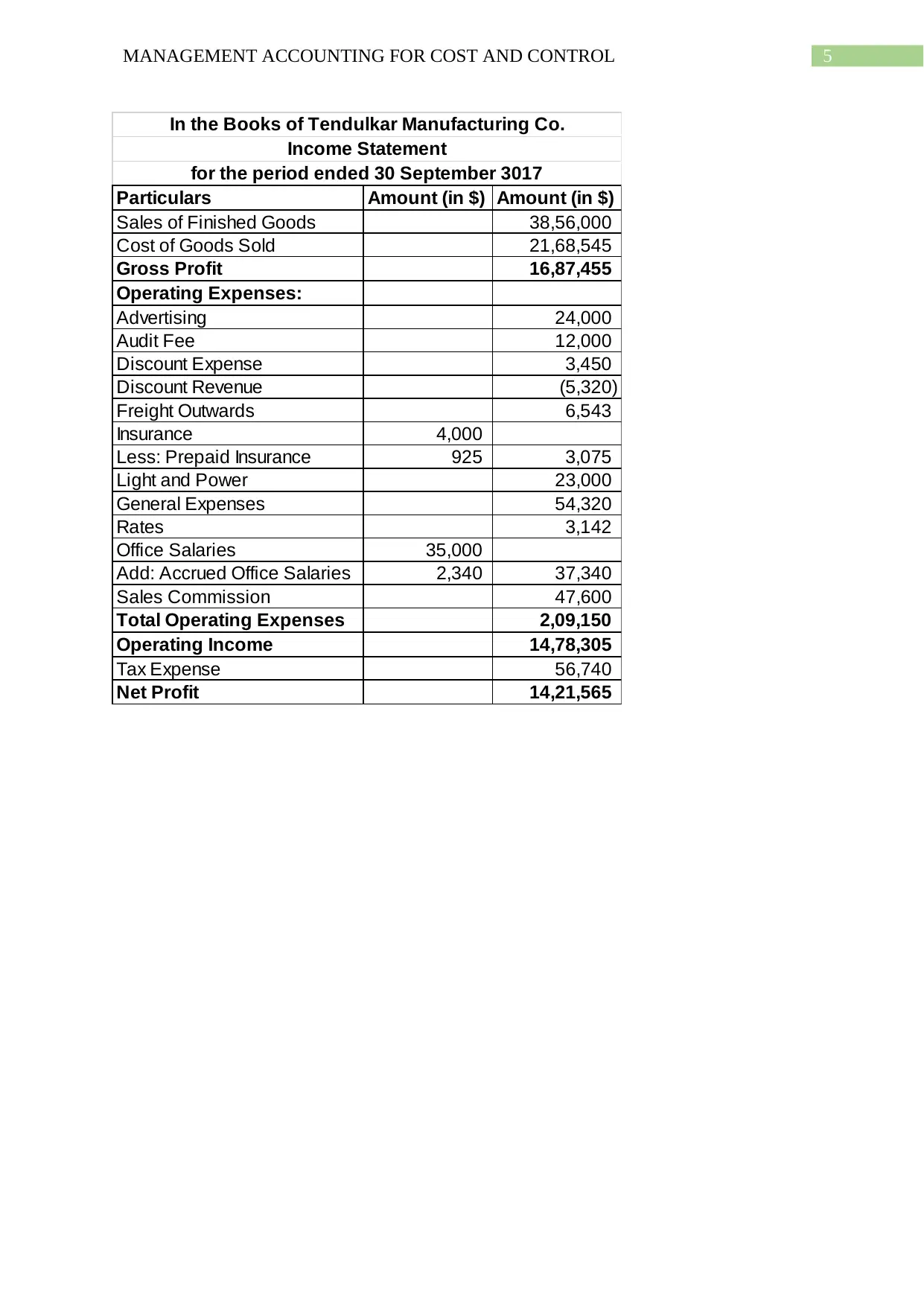

In the Books of Tendulkar Manufacturing Co.

Income Statement

for the period ended 30 September 3017

Particulars Amount (in $) Amount (in $)

Sales of Finished Goods 38,56,000

Cost of Goods Sold 21,68,545

Gross Profit 16,87,455

Operating Expenses:

Advertising 24,000

Audit Fee 12,000

Discount Expense 3,450

Discount Revenue (5,320)

Freight Outwards 6,543

Insurance 4,000

Less: Prepaid Insurance 925 3,075

Light and Power 23,000

General Expenses 54,320

Rates 3,142

Office Salaries 35,000

Add: Accrued Office Salaries 2,340 37,340

Sales Commission 47,600

Total Operating Expenses 2,09,150

Operating Income 14,78,305

Tax Expense 56,740

Net Profit 14,21,565

In the Books of Tendulkar Manufacturing Co.

Income Statement

for the period ended 30 September 3017

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGEMENT ACCOUNTING FOR COST AND CONTROL

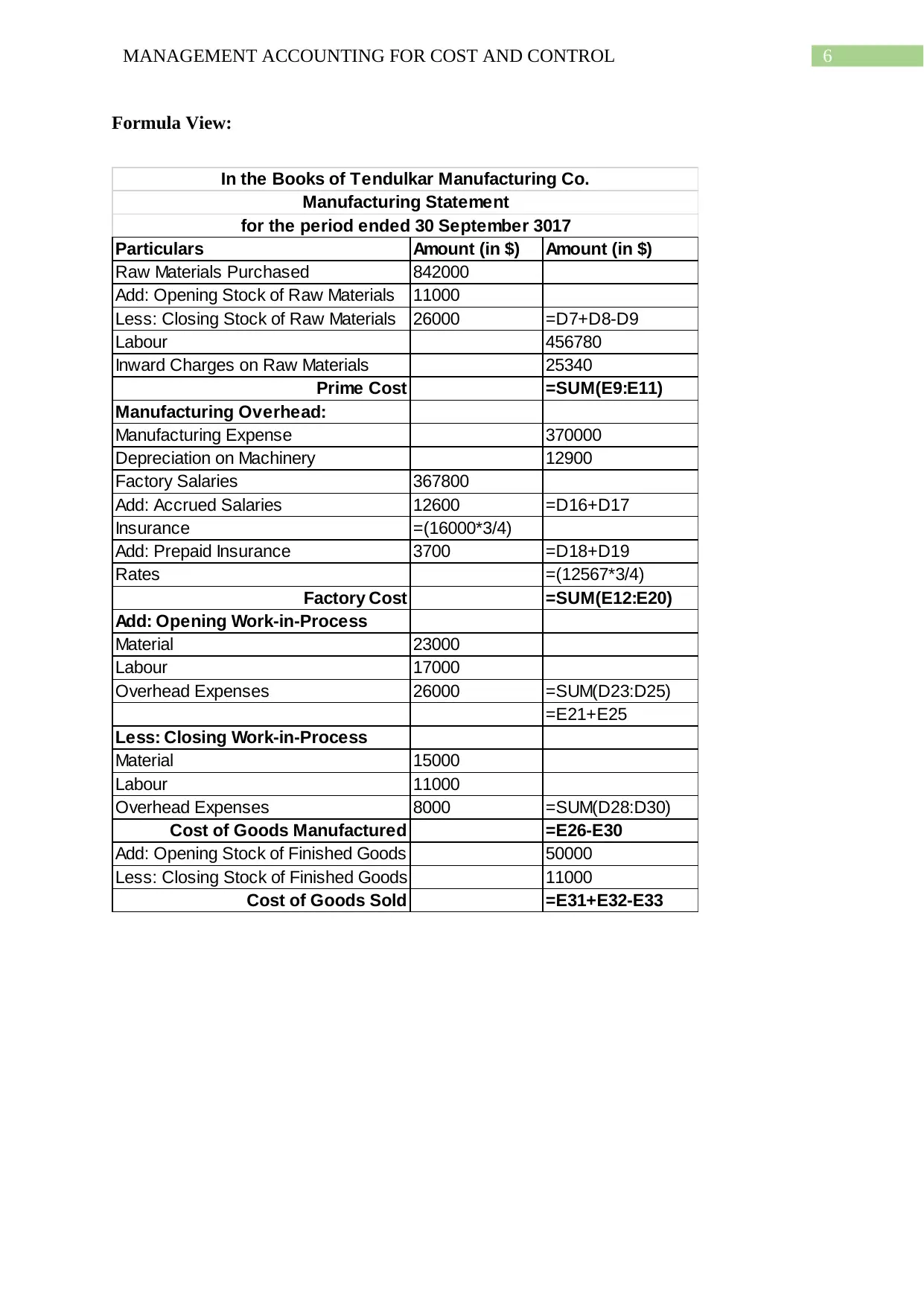

Formula View:

Particulars Amount (in $) Amount (in $)

Raw Materials Purchased 842000

Add: Opening Stock of Raw Materials 11000

Less: Closing Stock of Raw Materials 26000 =D7+D8-D9

Labour 456780

Inward Charges on Raw Materials 25340

Prime Cost =SUM(E9:E11)

Manufacturing Overhead:

Manufacturing Expense 370000

Depreciation on Machinery 12900

Factory Salaries 367800

Add: Accrued Salaries 12600 =D16+D17

Insurance =(16000*3/4)

Add: Prepaid Insurance 3700 =D18+D19

Rates =(12567*3/4)

Factory Cost =SUM(E12:E20)

Add: Opening Work-in-Process

Material 23000

Labour 17000

Overhead Expenses 26000 =SUM(D23:D25)

=E21+E25

Less: Closing Work-in-Process

Material 15000

Labour 11000

Overhead Expenses 8000 =SUM(D28:D30)

Cost of Goods Manufactured =E26-E30

Add: Opening Stock of Finished Goods 50000

Less: Closing Stock of Finished Goods 11000

Cost of Goods Sold =E31+E32-E33

In the Books of Tendulkar Manufacturing Co.

Manufacturing Statement

for the period ended 30 September 3017

Formula View:

Particulars Amount (in $) Amount (in $)

Raw Materials Purchased 842000

Add: Opening Stock of Raw Materials 11000

Less: Closing Stock of Raw Materials 26000 =D7+D8-D9

Labour 456780

Inward Charges on Raw Materials 25340

Prime Cost =SUM(E9:E11)

Manufacturing Overhead:

Manufacturing Expense 370000

Depreciation on Machinery 12900

Factory Salaries 367800

Add: Accrued Salaries 12600 =D16+D17

Insurance =(16000*3/4)

Add: Prepaid Insurance 3700 =D18+D19

Rates =(12567*3/4)

Factory Cost =SUM(E12:E20)

Add: Opening Work-in-Process

Material 23000

Labour 17000

Overhead Expenses 26000 =SUM(D23:D25)

=E21+E25

Less: Closing Work-in-Process

Material 15000

Labour 11000

Overhead Expenses 8000 =SUM(D28:D30)

Cost of Goods Manufactured =E26-E30

Add: Opening Stock of Finished Goods 50000

Less: Closing Stock of Finished Goods 11000

Cost of Goods Sold =E31+E32-E33

In the Books of Tendulkar Manufacturing Co.

Manufacturing Statement

for the period ended 30 September 3017

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGEMENT ACCOUNTING FOR COST AND CONTROL

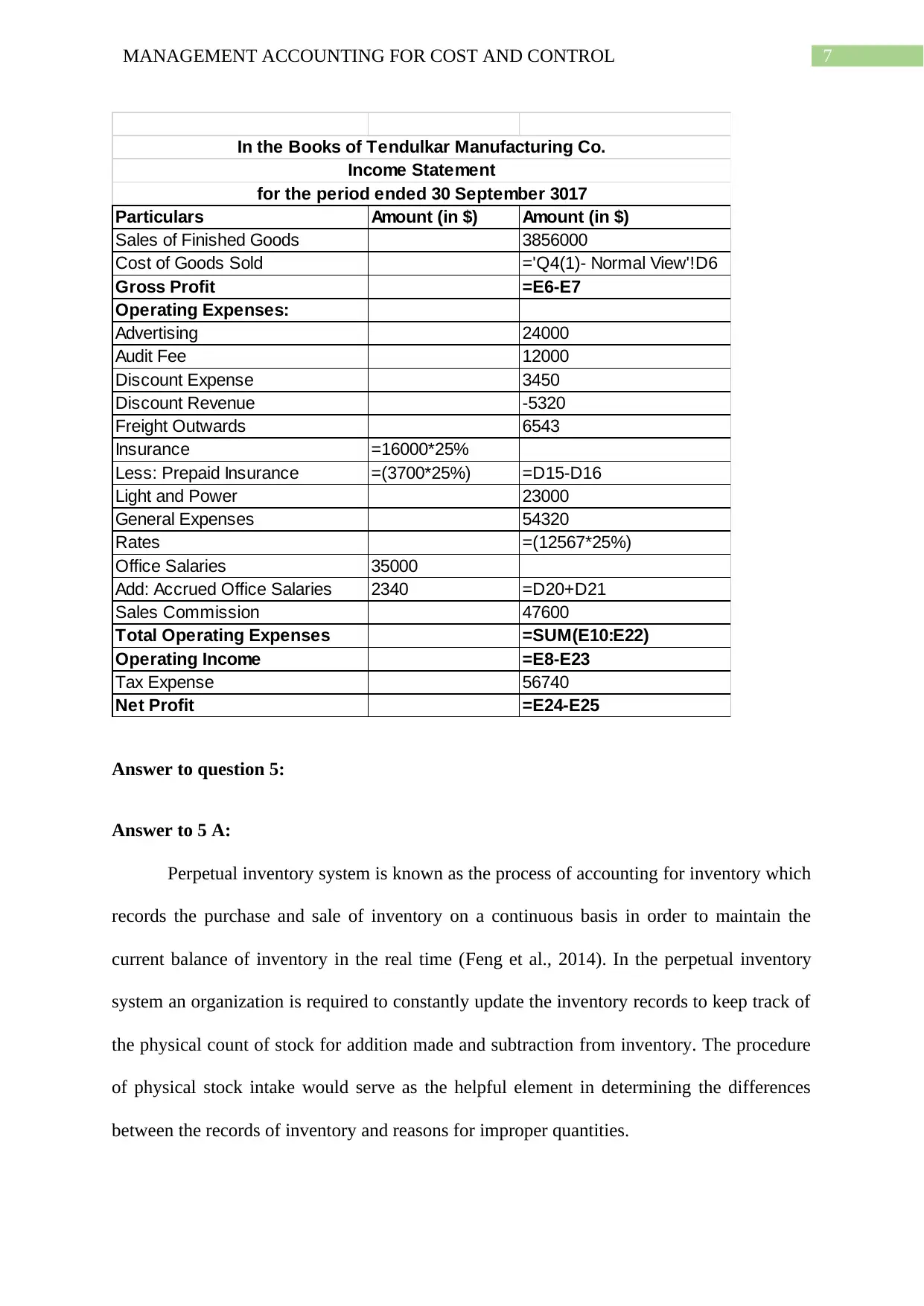

Particulars Amount (in $) Amount (in $)

Sales of Finished Goods 3856000

Cost of Goods Sold ='Q4(1)- Normal View'!D6

Gross Profit =E6-E7

Operating Expenses:

Advertising 24000

Audit Fee 12000

Discount Expense 3450

Discount Revenue -5320

Freight Outwards 6543

Insurance =16000*25%

Less: Prepaid Insurance =(3700*25%) =D15-D16

Light and Power 23000

General Expenses 54320

Rates =(12567*25%)

Office Salaries 35000

Add: Accrued Office Salaries 2340 =D20+D21

Sales Commission 47600

Total Operating Expenses =SUM(E10:E22)

Operating Income =E8-E23

Tax Expense 56740

Net Profit =E24-E25

In the Books of Tendulkar Manufacturing Co.

Income Statement

for the period ended 30 September 3017

Answer to question 5:

Answer to 5 A:

Perpetual inventory system is known as the process of accounting for inventory which

records the purchase and sale of inventory on a continuous basis in order to maintain the

current balance of inventory in the real time (Feng et al., 2014). In the perpetual inventory

system an organization is required to constantly update the inventory records to keep track of

the physical count of stock for addition made and subtraction from inventory. The procedure

of physical stock intake would serve as the helpful element in determining the differences

between the records of inventory and reasons for improper quantities.

Particulars Amount (in $) Amount (in $)

Sales of Finished Goods 3856000

Cost of Goods Sold ='Q4(1)- Normal View'!D6

Gross Profit =E6-E7

Operating Expenses:

Advertising 24000

Audit Fee 12000

Discount Expense 3450

Discount Revenue -5320

Freight Outwards 6543

Insurance =16000*25%

Less: Prepaid Insurance =(3700*25%) =D15-D16

Light and Power 23000

General Expenses 54320

Rates =(12567*25%)

Office Salaries 35000

Add: Accrued Office Salaries 2340 =D20+D21

Sales Commission 47600

Total Operating Expenses =SUM(E10:E22)

Operating Income =E8-E23

Tax Expense 56740

Net Profit =E24-E25

In the Books of Tendulkar Manufacturing Co.

Income Statement

for the period ended 30 September 3017

Answer to question 5:

Answer to 5 A:

Perpetual inventory system is known as the process of accounting for inventory which

records the purchase and sale of inventory on a continuous basis in order to maintain the

current balance of inventory in the real time (Feng et al., 2014). In the perpetual inventory

system an organization is required to constantly update the inventory records to keep track of

the physical count of stock for addition made and subtraction from inventory. The procedure

of physical stock intake would serve as the helpful element in determining the differences

between the records of inventory and reasons for improper quantities.

8MANAGEMENT ACCOUNTING FOR COST AND CONTROL

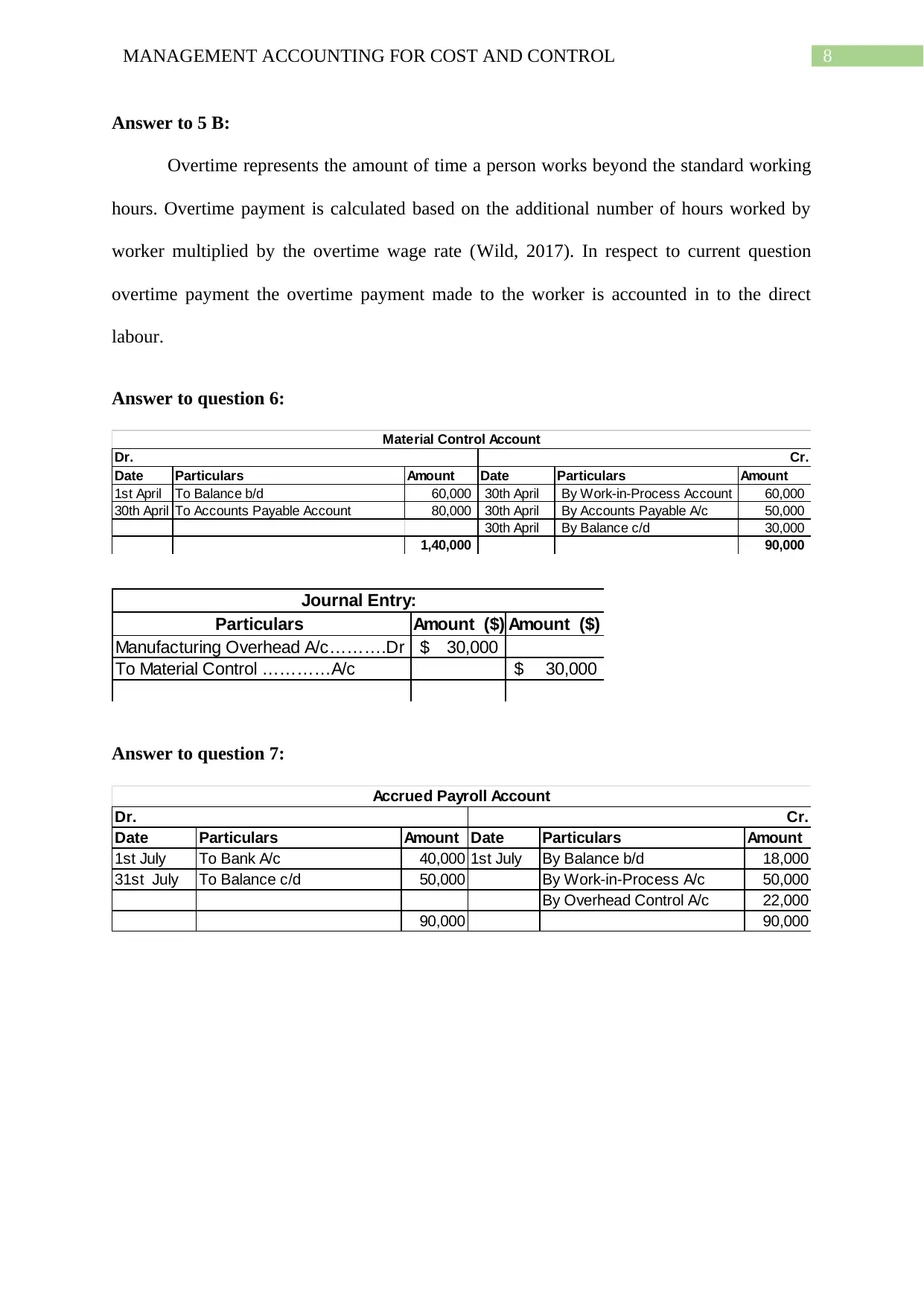

Answer to 5 B:

Overtime represents the amount of time a person works beyond the standard working

hours. Overtime payment is calculated based on the additional number of hours worked by

worker multiplied by the overtime wage rate (Wild, 2017). In respect to current question

overtime payment the overtime payment made to the worker is accounted in to the direct

labour.

Answer to question 6:

Date Particulars Amount Date Particulars Amount

1st April To Balance b/d 60,000 30th April By Work-in-Process Account 60,000

30th April To Accounts Payable Account 80,000 30th April By Accounts Payable A/c 50,000

30th April By Balance c/d 30,000

1,40,000 90,000

Material Control Account

Cr.Dr.

Particulars Amount ($) Amount ($)

Manufacturing Overhead A/c……….Dr 30,000$

To Material Control …………A/c 30,000$

Journal Entry:

Answer to question 7:

Date Particulars Amount Date Particulars Amount

1st July To Bank A/c 40,000 1st July By Balance b/d 18,000

31st July To Balance c/d 50,000 By Work-in-Process A/c 50,000

By Overhead Control A/c 22,000

90,000 90,000

Accrued Payroll Account

Dr. Cr.

Answer to 5 B:

Overtime represents the amount of time a person works beyond the standard working

hours. Overtime payment is calculated based on the additional number of hours worked by

worker multiplied by the overtime wage rate (Wild, 2017). In respect to current question

overtime payment the overtime payment made to the worker is accounted in to the direct

labour.

Answer to question 6:

Date Particulars Amount Date Particulars Amount

1st April To Balance b/d 60,000 30th April By Work-in-Process Account 60,000

30th April To Accounts Payable Account 80,000 30th April By Accounts Payable A/c 50,000

30th April By Balance c/d 30,000

1,40,000 90,000

Material Control Account

Cr.Dr.

Particulars Amount ($) Amount ($)

Manufacturing Overhead A/c……….Dr 30,000$

To Material Control …………A/c 30,000$

Journal Entry:

Answer to question 7:

Date Particulars Amount Date Particulars Amount

1st July To Bank A/c 40,000 1st July By Balance b/d 18,000

31st July To Balance c/d 50,000 By Work-in-Process A/c 50,000

By Overhead Control A/c 22,000

90,000 90,000

Accrued Payroll Account

Dr. Cr.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGEMENT ACCOUNTING FOR COST AND CONTROL

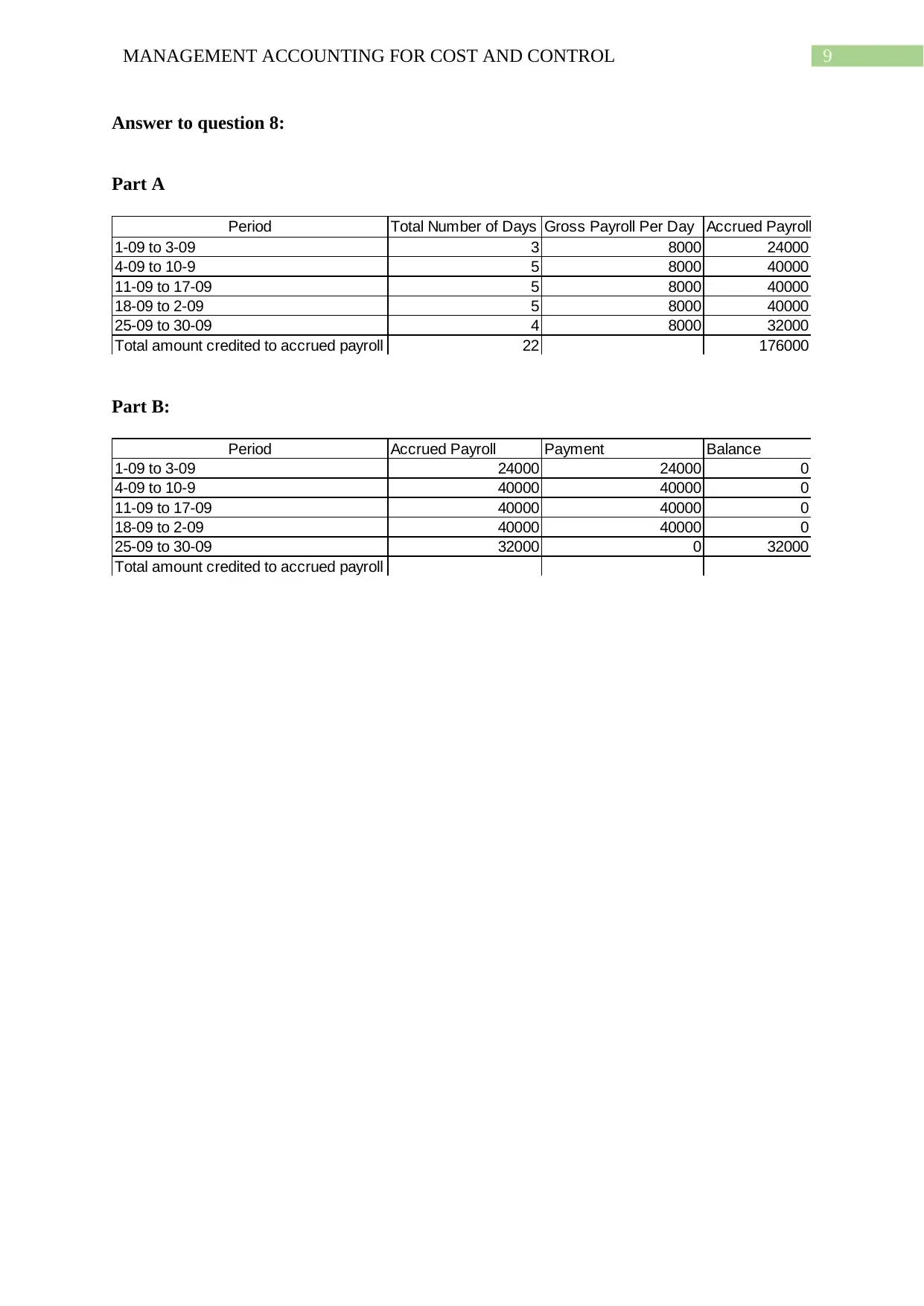

Answer to question 8:

Part A

Period Total Number of Days Gross Payroll Per Day Accrued Payroll

1-09 to 3-09 3 8000 24000

4-09 to 10-9 5 8000 40000

11-09 to 17-09 5 8000 40000

18-09 to 2-09 5 8000 40000

25-09 to 30-09 4 8000 32000

Total amount credited to accrued payroll 22 176000

Part B:

Period Accrued Payroll Payment Balance

1-09 to 3-09 24000 24000 0

4-09 to 10-9 40000 40000 0

11-09 to 17-09 40000 40000 0

18-09 to 2-09 40000 40000 0

25-09 to 30-09 32000 0 32000

Total amount credited to accrued payroll

Answer to question 8:

Part A

Period Total Number of Days Gross Payroll Per Day Accrued Payroll

1-09 to 3-09 3 8000 24000

4-09 to 10-9 5 8000 40000

11-09 to 17-09 5 8000 40000

18-09 to 2-09 5 8000 40000

25-09 to 30-09 4 8000 32000

Total amount credited to accrued payroll 22 176000

Part B:

Period Accrued Payroll Payment Balance

1-09 to 3-09 24000 24000 0

4-09 to 10-9 40000 40000 0

11-09 to 17-09 40000 40000 0

18-09 to 2-09 40000 40000 0

25-09 to 30-09 32000 0 32000

Total amount credited to accrued payroll

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGEMENT ACCOUNTING FOR COST AND CONTROL

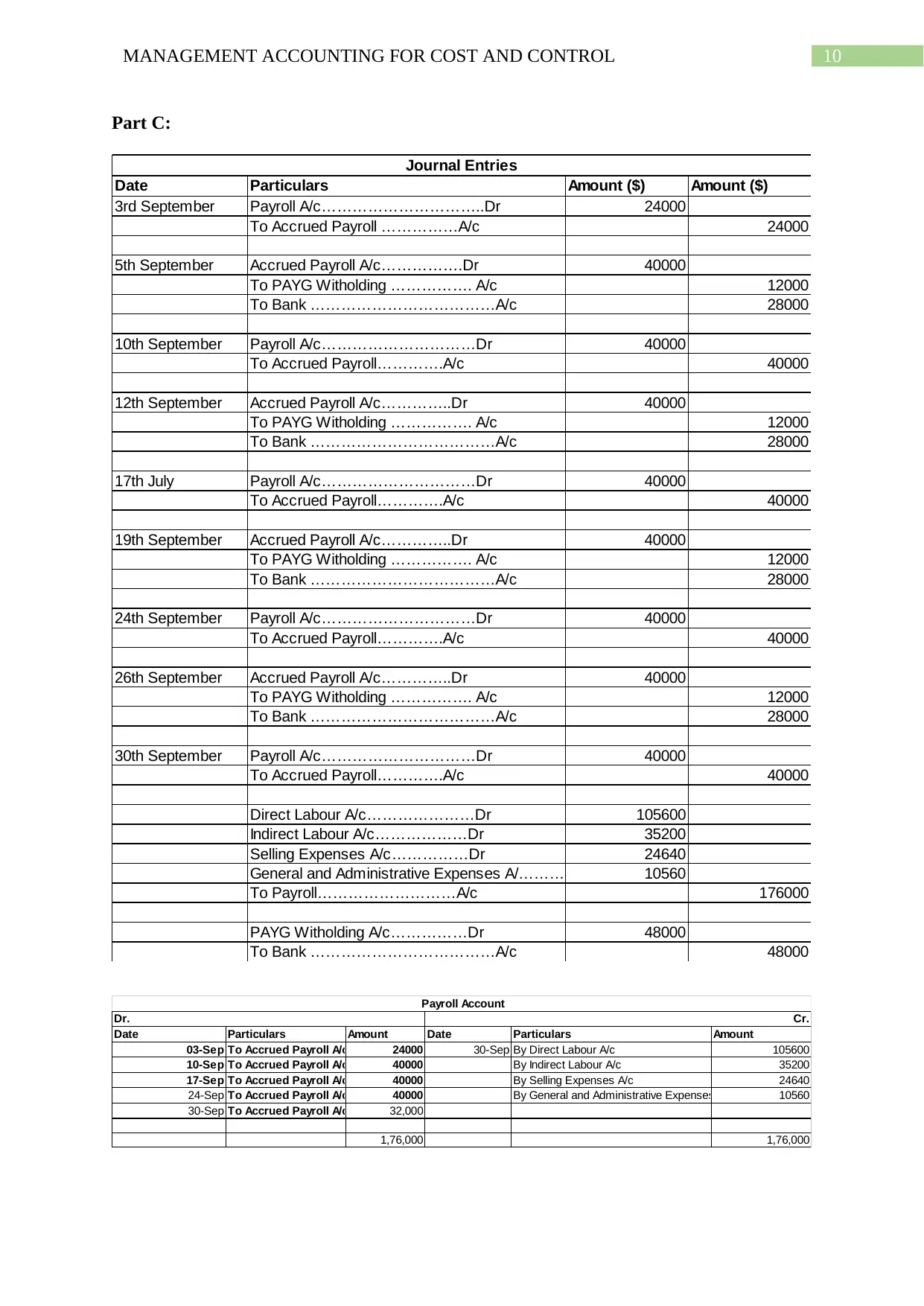

Part C:

Date Particulars Amount ($) Amount ($)

3rd September Payroll A/c…………………………..Dr 24000

To Accrued Payroll ……………A/c 24000

5th September Accrued Payroll A/c…………….Dr 40000

To PAYG Witholding ……………. A/c 12000

To Bank ………………………………A/c 28000

10th September Payroll A/c…………………………Dr 40000

To Accrued Payroll………….A/c 40000

12th September Accrued Payroll A/c…………..Dr 40000

To PAYG Witholding ……………. A/c 12000

To Bank ………………………………A/c 28000

17th July Payroll A/c…………………………Dr 40000

To Accrued Payroll………….A/c 40000

19th September Accrued Payroll A/c…………..Dr 40000

To PAYG Witholding ……………. A/c 12000

To Bank ………………………………A/c 28000

24th September Payroll A/c…………………………Dr 40000

To Accrued Payroll………….A/c 40000

26th September Accrued Payroll A/c…………..Dr 40000

To PAYG Witholding ……………. A/c 12000

To Bank ………………………………A/c 28000

30th September Payroll A/c…………………………Dr 40000

To Accrued Payroll………….A/c 40000

Direct Labour A/c…………………Dr 105600

Indirect Labour A/c………………Dr 35200

Selling Expenses A/c……………Dr 24640

General and Administrative Expenses A/………Dr 10560

To Payroll………………………A/c 176000

PAYG Witholding A/c……………Dr 48000

To Bank ………………………………A/c 48000

Journal Entries

Date Particulars Amount Date Particulars Amount

03-Sep To Accrued Payroll A/c 24000 30-Sep By Direct Labour A/c 105600

10-Sep To Accrued Payroll A/c 40000 By Indirect Labour A/c 35200

17-Sep To Accrued Payroll A/c 40000 By Selling Expenses A/c 24640

24-Sep To Accrued Payroll A/c 40000 By General and Administrative Expenses 10560

30-Sep To Accrued Payroll A/c 32,000

1,76,000 1,76,000

Payroll Account

Dr. Cr.

Part C:

Date Particulars Amount ($) Amount ($)

3rd September Payroll A/c…………………………..Dr 24000

To Accrued Payroll ……………A/c 24000

5th September Accrued Payroll A/c…………….Dr 40000

To PAYG Witholding ……………. A/c 12000

To Bank ………………………………A/c 28000

10th September Payroll A/c…………………………Dr 40000

To Accrued Payroll………….A/c 40000

12th September Accrued Payroll A/c…………..Dr 40000

To PAYG Witholding ……………. A/c 12000

To Bank ………………………………A/c 28000

17th July Payroll A/c…………………………Dr 40000

To Accrued Payroll………….A/c 40000

19th September Accrued Payroll A/c…………..Dr 40000

To PAYG Witholding ……………. A/c 12000

To Bank ………………………………A/c 28000

24th September Payroll A/c…………………………Dr 40000

To Accrued Payroll………….A/c 40000

26th September Accrued Payroll A/c…………..Dr 40000

To PAYG Witholding ……………. A/c 12000

To Bank ………………………………A/c 28000

30th September Payroll A/c…………………………Dr 40000

To Accrued Payroll………….A/c 40000

Direct Labour A/c…………………Dr 105600

Indirect Labour A/c………………Dr 35200

Selling Expenses A/c……………Dr 24640

General and Administrative Expenses A/………Dr 10560

To Payroll………………………A/c 176000

PAYG Witholding A/c……………Dr 48000

To Bank ………………………………A/c 48000

Journal Entries

Date Particulars Amount Date Particulars Amount

03-Sep To Accrued Payroll A/c 24000 30-Sep By Direct Labour A/c 105600

10-Sep To Accrued Payroll A/c 40000 By Indirect Labour A/c 35200

17-Sep To Accrued Payroll A/c 40000 By Selling Expenses A/c 24640

24-Sep To Accrued Payroll A/c 40000 By General and Administrative Expenses 10560

30-Sep To Accrued Payroll A/c 32,000

1,76,000 1,76,000

Payroll Account

Dr. Cr.

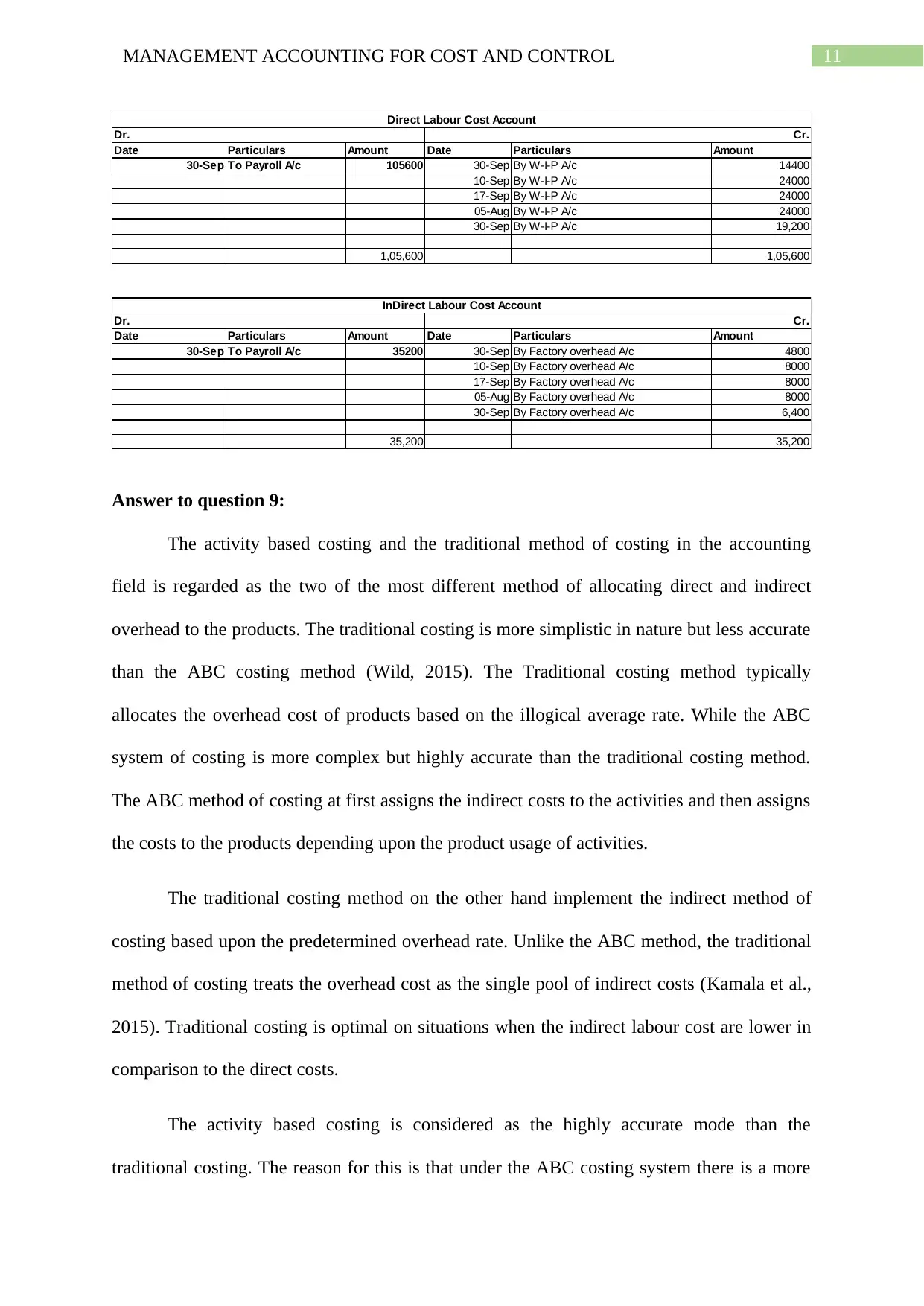

11MANAGEMENT ACCOUNTING FOR COST AND CONTROL

Date Particulars Amount Date Particulars Amount

30-Sep To Payroll A/c 105600 30-Sep By W-I-P A/c 14400

10-Sep By W-I-P A/c 24000

17-Sep By W-I-P A/c 24000

05-Aug By W-I-P A/c 24000

30-Sep By W-I-P A/c 19,200

1,05,600 1,05,600

Direct Labour Cost Account

Dr. Cr.

Date Particulars Amount Date Particulars Amount

30-Sep To Payroll A/c 35200 30-Sep By Factory overhead A/c 4800

10-Sep By Factory overhead A/c 8000

17-Sep By Factory overhead A/c 8000

05-Aug By Factory overhead A/c 8000

30-Sep By Factory overhead A/c 6,400

35,200 35,200

InDirect Labour Cost Account

Dr. Cr.

Answer to question 9:

The activity based costing and the traditional method of costing in the accounting

field is regarded as the two of the most different method of allocating direct and indirect

overhead to the products. The traditional costing is more simplistic in nature but less accurate

than the ABC costing method (Wild, 2015). The Traditional costing method typically

allocates the overhead cost of products based on the illogical average rate. While the ABC

system of costing is more complex but highly accurate than the traditional costing method.

The ABC method of costing at first assigns the indirect costs to the activities and then assigns

the costs to the products depending upon the product usage of activities.

The traditional costing method on the other hand implement the indirect method of

costing based upon the predetermined overhead rate. Unlike the ABC method, the traditional

method of costing treats the overhead cost as the single pool of indirect costs (Kamala et al.,

2015). Traditional costing is optimal on situations when the indirect labour cost are lower in

comparison to the direct costs.

The activity based costing is considered as the highly accurate mode than the

traditional costing. The reason for this is that under the ABC costing system there is a more

Date Particulars Amount Date Particulars Amount

30-Sep To Payroll A/c 105600 30-Sep By W-I-P A/c 14400

10-Sep By W-I-P A/c 24000

17-Sep By W-I-P A/c 24000

05-Aug By W-I-P A/c 24000

30-Sep By W-I-P A/c 19,200

1,05,600 1,05,600

Direct Labour Cost Account

Dr. Cr.

Date Particulars Amount Date Particulars Amount

30-Sep To Payroll A/c 35200 30-Sep By Factory overhead A/c 4800

10-Sep By Factory overhead A/c 8000

17-Sep By Factory overhead A/c 8000

05-Aug By Factory overhead A/c 8000

30-Sep By Factory overhead A/c 6,400

35,200 35,200

InDirect Labour Cost Account

Dr. Cr.

Answer to question 9:

The activity based costing and the traditional method of costing in the accounting

field is regarded as the two of the most different method of allocating direct and indirect

overhead to the products. The traditional costing is more simplistic in nature but less accurate

than the ABC costing method (Wild, 2015). The Traditional costing method typically

allocates the overhead cost of products based on the illogical average rate. While the ABC

system of costing is more complex but highly accurate than the traditional costing method.

The ABC method of costing at first assigns the indirect costs to the activities and then assigns

the costs to the products depending upon the product usage of activities.

The traditional costing method on the other hand implement the indirect method of

costing based upon the predetermined overhead rate. Unlike the ABC method, the traditional

method of costing treats the overhead cost as the single pool of indirect costs (Kamala et al.,

2015). Traditional costing is optimal on situations when the indirect labour cost are lower in

comparison to the direct costs.

The activity based costing is considered as the highly accurate mode than the

traditional costing. The reason for this is that under the ABC costing system there is a more

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.