Management Accounting: Cost Analysis, Budgetary Control and Reporting

VerifiedAdded on 2023/06/18

|12

|3395

|218

Report

AI Summary

This report provides an overview of management accounting, focusing on cost analysis and budgetary control within an organization, using Rowlinson Knitwear as a case study. It discusses various management accounting systems, including product costing, cost accounting, and job costing, highlighting their essential requirements. The report also examines different methods used for management accounting reporting, such as budget reports and account receivable reports. Furthermore, it includes a calculation of cost using marginal and absorption costing techniques to prepare an income statement. The advantages and disadvantages of budgetary control, including operational budgets, cash flow budgets, fixed budgets, and master budgets, are also discussed. Finally, the report touches upon how management accounting systems respond to financial problems, offering a comprehensive view of management accounting practices.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Management Accounting and their essential requirements...................................................3

P2 Different methods used for management accounting reporting.............................................4

TASK 2............................................................................................................................................5

P3 Calculation of cost by using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs...........................................................................5

TASK 3............................................................................................................................................9

P4 Budgetary control with their advantages and disadvantages.................................................9

TASK 4..........................................................................................................................................11

P5 Management accounting systems and their response towards financial problems..............11

CONCLUSION .............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Management Accounting and their essential requirements...................................................3

P2 Different methods used for management accounting reporting.............................................4

TASK 2............................................................................................................................................5

P3 Calculation of cost by using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs...........................................................................5

TASK 3............................................................................................................................................9

P4 Budgetary control with their advantages and disadvantages.................................................9

TASK 4..........................................................................................................................................11

P5 Management accounting systems and their response towards financial problems..............11

CONCLUSION .............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

The term accounting process relates with summarising, classifying and recording all

business transactions which are related with the financial accounts or monetary policy. Journal,

Ledger, trial balance, etc. are prepared which are easy to understand and this aids stakeholders to

compare them in order to monitor and check the account and profits of business. In simple terms,

management accounting is the process for summarising all details related with financial

statements of company. Rowlinson Knitwear is selected as an organisation for this report and

this is a well-known UK based cloth manufacturing business (Bleyen and et. al., 2017).

Moreover, this project will highlights on different types of management accounting systems with

their essential requirements and also different methods used for management accounting

reporting. In the present scenario, organisation is well-known for manufacture large corporate as

well as school wear so cost calculation method will also included in this report.

TASK 1

P1 Management Accounting and their essential requirements

The term management accounting is explained as the process of formulating management

accounts, reports and financial factors which provide accurate and reliable information related

with costing of data. Moreover, this is used by manager for control and manage constant

operations related with business. Management accounting also translate financial information

and data into useful information that are used for appropriate decision-making of business. In the

context of Rowlinson Knitwear, management is engaged in bulk production activities so it is

important for organisation to make accurate and effective decisions. Some types of management

accounting systems with their essential requirements are mention as follow:

Product costing- The term product cost management accounting aids to identify all cost

which is related with formulation of products so this aids the manager for understand and

analyse all cost and expenditures related with production of products (Bruno and Lapsley,

2018). From the perspective of Rowlinson Knitwear, product costing is used to manage

overheads of business through monitoring and allocating the raw-material as well as

financial resources in an organised manner.

Essential Requirements

The term accounting process relates with summarising, classifying and recording all

business transactions which are related with the financial accounts or monetary policy. Journal,

Ledger, trial balance, etc. are prepared which are easy to understand and this aids stakeholders to

compare them in order to monitor and check the account and profits of business. In simple terms,

management accounting is the process for summarising all details related with financial

statements of company. Rowlinson Knitwear is selected as an organisation for this report and

this is a well-known UK based cloth manufacturing business (Bleyen and et. al., 2017).

Moreover, this project will highlights on different types of management accounting systems with

their essential requirements and also different methods used for management accounting

reporting. In the present scenario, organisation is well-known for manufacture large corporate as

well as school wear so cost calculation method will also included in this report.

TASK 1

P1 Management Accounting and their essential requirements

The term management accounting is explained as the process of formulating management

accounts, reports and financial factors which provide accurate and reliable information related

with costing of data. Moreover, this is used by manager for control and manage constant

operations related with business. Management accounting also translate financial information

and data into useful information that are used for appropriate decision-making of business. In the

context of Rowlinson Knitwear, management is engaged in bulk production activities so it is

important for organisation to make accurate and effective decisions. Some types of management

accounting systems with their essential requirements are mention as follow:

Product costing- The term product cost management accounting aids to identify all cost

which is related with formulation of products so this aids the manager for understand and

analyse all cost and expenditures related with production of products (Bruno and Lapsley,

2018). From the perspective of Rowlinson Knitwear, product costing is used to manage

overheads of business through monitoring and allocating the raw-material as well as

financial resources in an organised manner.

Essential Requirements

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

◦ To consider overall market- With include overall revenue management consider

that all cost factors related with market are included and this aids an organisation to

manage expenses in the decided budget. By engage of all valuable factor management

compute cost as per item requirement.

◦ To divide expenses- Management of Rowlinson Knitwear perform an important rile

to understand and identify the diversified expenses related with business. This refers

that product costing help to identify both fixed and variable cost related with

business.

Cost accounting system- This is also explained as product costing system and it provide

the framework related with estimation of future cost (Grossi and et. al., 2019). From the

perspective of Rowlinson Knitwear this is understand that management accounting

analyse overall future cost and profitability of business. Within this cost accounting

accounting system provide appropriate costing and also budget cost that helps to allocate

various overheads of business.

Essential Requirements

◦ Forecasting- Future cost perform an important role for business because this aids an

organisation to formulate appropriate budget. From the perspective of Rowlinson

Knitwear cost accounting perform an important role to formulate budgets because this

helps by analyse cost of inventory, direct-material cost, fixed-cost, etc.

Job-costing- The term job costing is explained as a method of determining cost related

with each manufacture units. In the present scenario, organisation that are engaged in the

manufacturing of single units easily estimate or calculate cost of business. One of the

most effective process of job-costing is to deliver all products as per their task

requirements and order request.

Essential Requirements- One of the major benefit related with job-costing system is to

manufacture and engage all those factors which are important to manufacture the task according

to the order request (Hadiyanto, Puspitasari and Ghani, 2018). This aids Rowlinson Knitwear for

utilise all resources in an optimise manner.

P2 Different methods used for management accounting reporting

Management accounting plays a crucial role for the internal management of the

respective organisation. This is because they are used for formulate policies and also define all

that all cost factors related with market are included and this aids an organisation to

manage expenses in the decided budget. By engage of all valuable factor management

compute cost as per item requirement.

◦ To divide expenses- Management of Rowlinson Knitwear perform an important rile

to understand and identify the diversified expenses related with business. This refers

that product costing help to identify both fixed and variable cost related with

business.

Cost accounting system- This is also explained as product costing system and it provide

the framework related with estimation of future cost (Grossi and et. al., 2019). From the

perspective of Rowlinson Knitwear this is understand that management accounting

analyse overall future cost and profitability of business. Within this cost accounting

accounting system provide appropriate costing and also budget cost that helps to allocate

various overheads of business.

Essential Requirements

◦ Forecasting- Future cost perform an important role for business because this aids an

organisation to formulate appropriate budget. From the perspective of Rowlinson

Knitwear cost accounting perform an important role to formulate budgets because this

helps by analyse cost of inventory, direct-material cost, fixed-cost, etc.

Job-costing- The term job costing is explained as a method of determining cost related

with each manufacture units. In the present scenario, organisation that are engaged in the

manufacturing of single units easily estimate or calculate cost of business. One of the

most effective process of job-costing is to deliver all products as per their task

requirements and order request.

Essential Requirements- One of the major benefit related with job-costing system is to

manufacture and engage all those factors which are important to manufacture the task according

to the order request (Hadiyanto, Puspitasari and Ghani, 2018). This aids Rowlinson Knitwear for

utilise all resources in an optimise manner.

P2 Different methods used for management accounting reporting

Management accounting plays a crucial role for the internal management of the

respective organisation. This is because they are used for formulate policies and also define all

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

objectives according to the efficient functions of organisation. Moreover, management

accounting methods perform an important role for business because they include both financial

and non-financial transactions and this helps authorities to define and achieve all objectives in an

organised manner. Some methods of management accounting are mention as follow:

Budget Reports- In the present scenario, budget reports are formulated by organisation

in each aspect because it aids each departments to perform their work with decided cost

(Harris and et. al., 2020). In addition to this, Budget reports are very crucial for the

respective organisation because it aids management for achieve all task according to

decided knowledge. Also, budget report is formulated with motive of improving financial

factors of business and this helps to understand how an organisation deal in the upcoming

period.

Account Receivable Reports- This type of report are formulated by the financial

departments for analyse and identify the overall number of debtors which exists within

the current period. Rowlinson Knitwear formulate report because it helps to keep check

and monitor when the amount is received from debtors and which debtors are not clearing

their dues. In simple terms, account receivable report keep track and record the number of

doubtful debts.

With understand all systems or methods related with management accounting this is understand

that they are numerous relevance factors formulated and they relates with management

accounting methods. Decision-making is the first relevant factor related with accounting method

and this is used by internal organisation for make effective and appropriate decisions for business

(Koolmees, Bernstein and Makhni, 2021). Moreover, both budget and account receivable report

control the cost of business and this supports financial departments to improve overall

profitability of business that supports to achieve all objectives with no hindrance related with

monetary factors of business.

TASK 2

P3 Calculation of cost by using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs.

COST- The term cost is explained as an amount which is charged by organisation from

their buyers for their products or services. In the present scenario, one of the major task

accounting methods perform an important role for business because they include both financial

and non-financial transactions and this helps authorities to define and achieve all objectives in an

organised manner. Some methods of management accounting are mention as follow:

Budget Reports- In the present scenario, budget reports are formulated by organisation

in each aspect because it aids each departments to perform their work with decided cost

(Harris and et. al., 2020). In addition to this, Budget reports are very crucial for the

respective organisation because it aids management for achieve all task according to

decided knowledge. Also, budget report is formulated with motive of improving financial

factors of business and this helps to understand how an organisation deal in the upcoming

period.

Account Receivable Reports- This type of report are formulated by the financial

departments for analyse and identify the overall number of debtors which exists within

the current period. Rowlinson Knitwear formulate report because it helps to keep check

and monitor when the amount is received from debtors and which debtors are not clearing

their dues. In simple terms, account receivable report keep track and record the number of

doubtful debts.

With understand all systems or methods related with management accounting this is understand

that they are numerous relevance factors formulated and they relates with management

accounting methods. Decision-making is the first relevant factor related with accounting method

and this is used by internal organisation for make effective and appropriate decisions for business

(Koolmees, Bernstein and Makhni, 2021). Moreover, both budget and account receivable report

control the cost of business and this supports financial departments to improve overall

profitability of business that supports to achieve all objectives with no hindrance related with

monetary factors of business.

TASK 2

P3 Calculation of cost by using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs.

COST- The term cost is explained as an amount which is charged by organisation from

their buyers for their products or services. In the present scenario, one of the major task

performed by management is to manufacture their products with minimum cost. Furthermore,

this include all process and production values related with business.

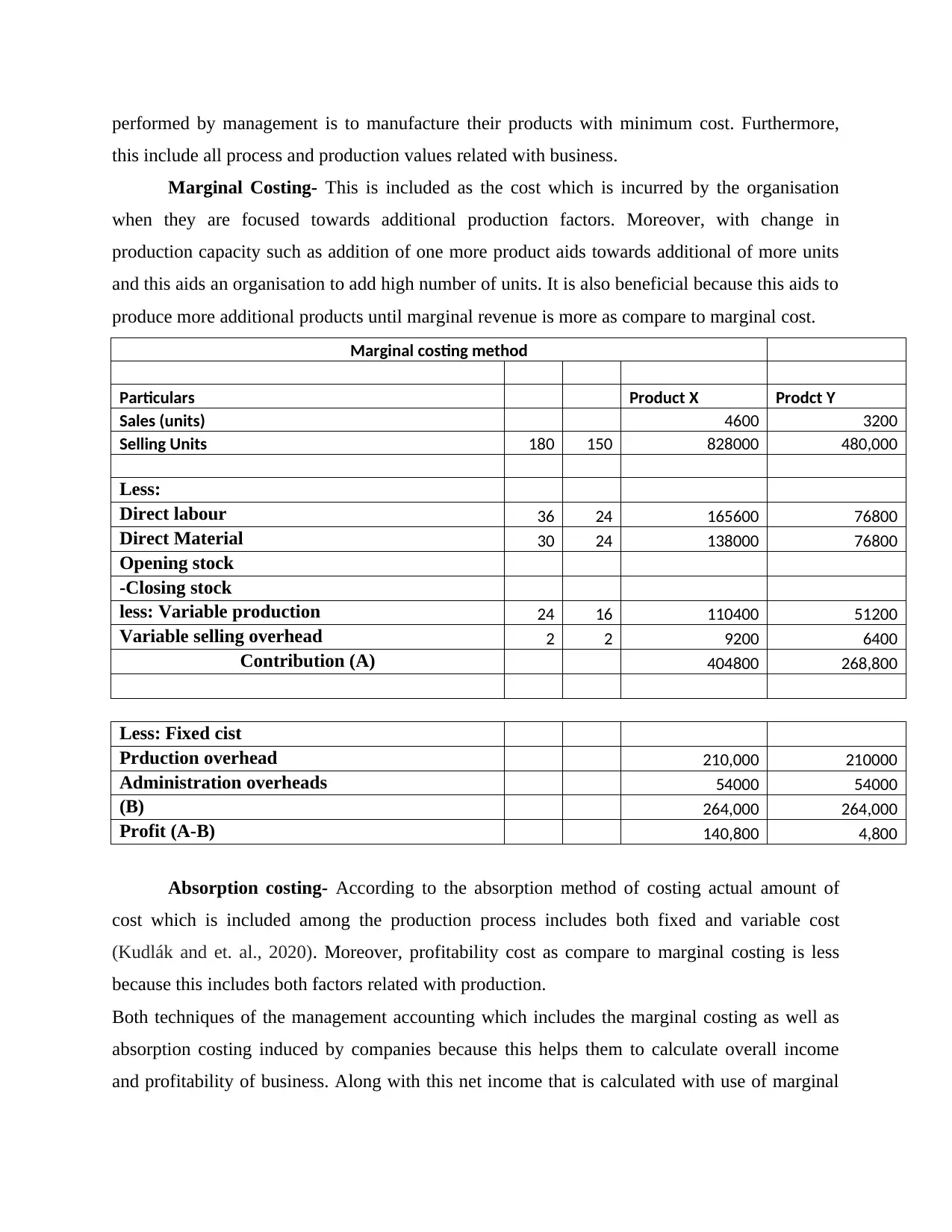

Marginal Costing- This is included as the cost which is incurred by the organisation

when they are focused towards additional production factors. Moreover, with change in

production capacity such as addition of one more product aids towards additional of more units

and this aids an organisation to add high number of units. It is also beneficial because this aids to

produce more additional products until marginal revenue is more as compare to marginal cost.

Marginal costing method

Particulars Product X Prodct Y

Sales (units) 4600 3200

Selling Units 180 150 828000 480,000

Less:

Direct labour 36 24 165600 76800

Direct Material 30 24 138000 76800

Opening stock

-Closing stock

less: Variable production 24 16 110400 51200

Variable selling overhead 2 2 9200 6400

Contribution (A) 404800 268,800

Less: Fixed cist

Prduction overhead 210,000 210000

Administration overheads 54000 54000

(B) 264,000 264,000

Profit (A-B) 140,800 4,800

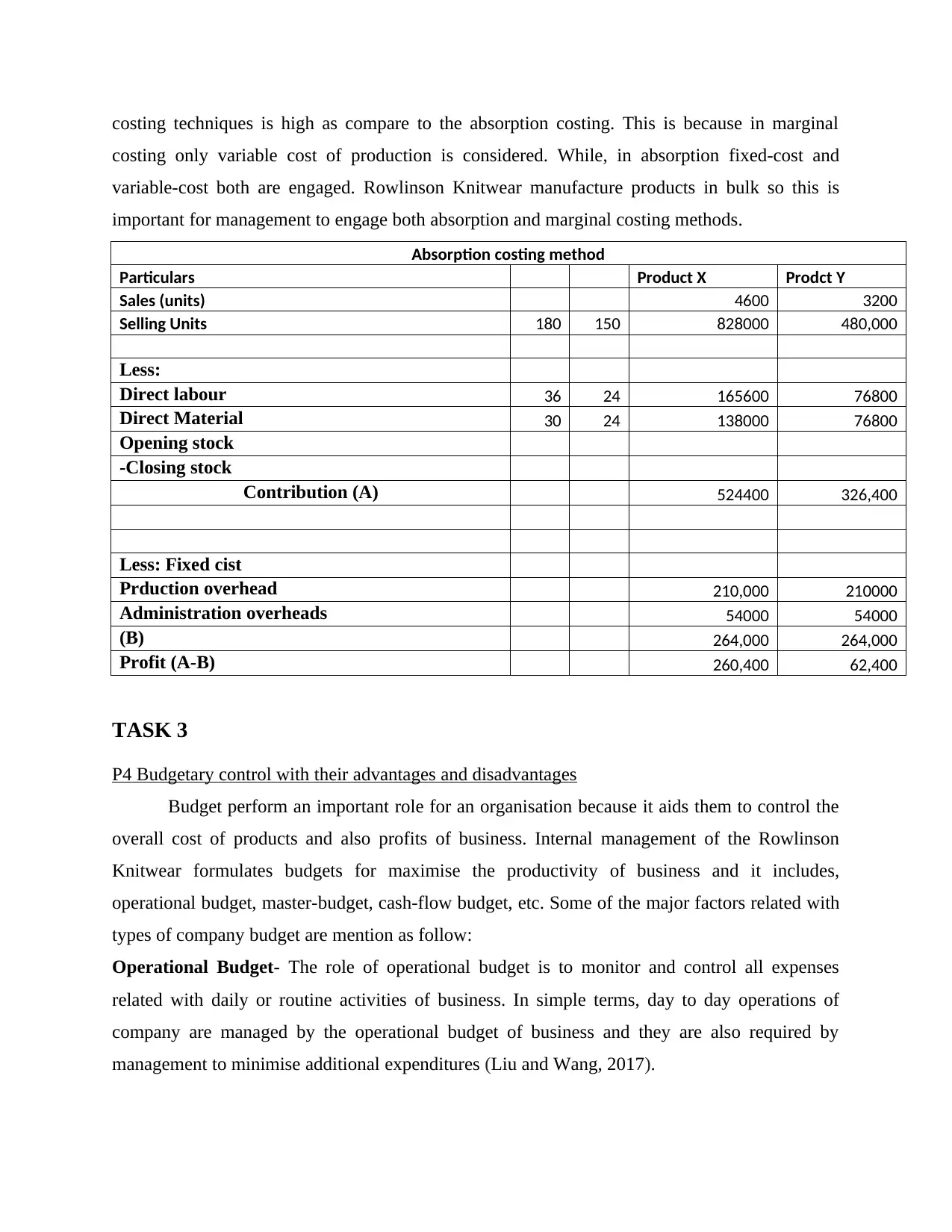

Absorption costing- According to the absorption method of costing actual amount of

cost which is included among the production process includes both fixed and variable cost

(Kudlák and et. al., 2020). Moreover, profitability cost as compare to marginal costing is less

because this includes both factors related with production.

Both techniques of the management accounting which includes the marginal costing as well as

absorption costing induced by companies because this helps them to calculate overall income

and profitability of business. Along with this net income that is calculated with use of marginal

this include all process and production values related with business.

Marginal Costing- This is included as the cost which is incurred by the organisation

when they are focused towards additional production factors. Moreover, with change in

production capacity such as addition of one more product aids towards additional of more units

and this aids an organisation to add high number of units. It is also beneficial because this aids to

produce more additional products until marginal revenue is more as compare to marginal cost.

Marginal costing method

Particulars Product X Prodct Y

Sales (units) 4600 3200

Selling Units 180 150 828000 480,000

Less:

Direct labour 36 24 165600 76800

Direct Material 30 24 138000 76800

Opening stock

-Closing stock

less: Variable production 24 16 110400 51200

Variable selling overhead 2 2 9200 6400

Contribution (A) 404800 268,800

Less: Fixed cist

Prduction overhead 210,000 210000

Administration overheads 54000 54000

(B) 264,000 264,000

Profit (A-B) 140,800 4,800

Absorption costing- According to the absorption method of costing actual amount of

cost which is included among the production process includes both fixed and variable cost

(Kudlák and et. al., 2020). Moreover, profitability cost as compare to marginal costing is less

because this includes both factors related with production.

Both techniques of the management accounting which includes the marginal costing as well as

absorption costing induced by companies because this helps them to calculate overall income

and profitability of business. Along with this net income that is calculated with use of marginal

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

costing techniques is high as compare to the absorption costing. This is because in marginal

costing only variable cost of production is considered. While, in absorption fixed-cost and

variable-cost both are engaged. Rowlinson Knitwear manufacture products in bulk so this is

important for management to engage both absorption and marginal costing methods.

Absorption costing method

Particulars Product X Prodct Y

Sales (units) 4600 3200

Selling Units 180 150 828000 480,000

Less:

Direct labour 36 24 165600 76800

Direct Material 30 24 138000 76800

Opening stock

-Closing stock

Contribution (A) 524400 326,400

Less: Fixed cist

Prduction overhead 210,000 210000

Administration overheads 54000 54000

(B) 264,000 264,000

Profit (A-B) 260,400 62,400

TASK 3

P4 Budgetary control with their advantages and disadvantages

Budget perform an important role for an organisation because it aids them to control the

overall cost of products and also profits of business. Internal management of the Rowlinson

Knitwear formulates budgets for maximise the productivity of business and it includes,

operational budget, master-budget, cash-flow budget, etc. Some of the major factors related with

types of company budget are mention as follow:

Operational Budget- The role of operational budget is to monitor and control all expenses

related with daily or routine activities of business. In simple terms, day to day operations of

company are managed by the operational budget of business and they are also required by

management to minimise additional expenditures (Liu and Wang, 2017).

costing only variable cost of production is considered. While, in absorption fixed-cost and

variable-cost both are engaged. Rowlinson Knitwear manufacture products in bulk so this is

important for management to engage both absorption and marginal costing methods.

Absorption costing method

Particulars Product X Prodct Y

Sales (units) 4600 3200

Selling Units 180 150 828000 480,000

Less:

Direct labour 36 24 165600 76800

Direct Material 30 24 138000 76800

Opening stock

-Closing stock

Contribution (A) 524400 326,400

Less: Fixed cist

Prduction overhead 210,000 210000

Administration overheads 54000 54000

(B) 264,000 264,000

Profit (A-B) 260,400 62,400

TASK 3

P4 Budgetary control with their advantages and disadvantages

Budget perform an important role for an organisation because it aids them to control the

overall cost of products and also profits of business. Internal management of the Rowlinson

Knitwear formulates budgets for maximise the productivity of business and it includes,

operational budget, master-budget, cash-flow budget, etc. Some of the major factors related with

types of company budget are mention as follow:

Operational Budget- The role of operational budget is to monitor and control all expenses

related with daily or routine activities of business. In simple terms, day to day operations of

company are managed by the operational budget of business and they are also required by

management to minimise additional expenditures (Liu and Wang, 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Advantages- One of the main advantage related with operational cost is that this

includes both cost and revenue which is incurred among daily operations. It aids to

control expenses that are not useful for business.

Disadvantages- Sometimes daily expenditures are uncertain in nature and also important

to implement. Also, manufacturing organisation such as Rowlinson Knitwear perform a

lot of activities so formulation of operational budget is a time-consuming process.

Cash Flow Budget- Cash of an organisation is managed and controlled through utilise the cash

flow budget and this is also used for determine the inflow as well as outflow of organisation.

This results it is easy for management to control the overall cash and business factors related

with daily operations of business. Also, for managing daily cash requirements in an organised

manner cash flow budget are used to acquire and utilise all funds in a proper manner.

Advantages- Budget aids an organisation for maintain the sufficient amount of cash

within the organisation and this results operational of company are not impacted due to

the monetary transactions of business.

Disadvantages- This is difficult for business to maintain the inflow and outflow of cash

because of different small transactions which are done on daily basis among company.

Fixed Budget- This types of budget are formulated in the initial period of year and they are

utilised by management for record the cost or expenses that are fixed or permanent in nature.

Furthermore, fixed-budget are complex to modify in those cases in which organisation want to

change their production capacity (Nikitina, Litovskaya and Ponomareva, 2018).

Advantages- With this budget an organisation is able to measure their overall growth

and profitability because of rigid or fixed nature of budget.

Disadvantages- The major drawback of fixed-budget is that they are not modify as per

the requirement of production due to this they are not effective in future.

Master-budget- This budget are formulated by the manager for forecast overall amount of sales

within decided factors and it is also useful to gather the overall capital which is required to invest

and execute. Moreover, master-budget are formulated with purpose of deciding the performance

standards and plans related with business operations.

Advantage- Budget perform an important role to determine the overall cost which is

related with the production process and it improves the total productivity of business.

includes both cost and revenue which is incurred among daily operations. It aids to

control expenses that are not useful for business.

Disadvantages- Sometimes daily expenditures are uncertain in nature and also important

to implement. Also, manufacturing organisation such as Rowlinson Knitwear perform a

lot of activities so formulation of operational budget is a time-consuming process.

Cash Flow Budget- Cash of an organisation is managed and controlled through utilise the cash

flow budget and this is also used for determine the inflow as well as outflow of organisation.

This results it is easy for management to control the overall cash and business factors related

with daily operations of business. Also, for managing daily cash requirements in an organised

manner cash flow budget are used to acquire and utilise all funds in a proper manner.

Advantages- Budget aids an organisation for maintain the sufficient amount of cash

within the organisation and this results operational of company are not impacted due to

the monetary transactions of business.

Disadvantages- This is difficult for business to maintain the inflow and outflow of cash

because of different small transactions which are done on daily basis among company.

Fixed Budget- This types of budget are formulated in the initial period of year and they are

utilised by management for record the cost or expenses that are fixed or permanent in nature.

Furthermore, fixed-budget are complex to modify in those cases in which organisation want to

change their production capacity (Nikitina, Litovskaya and Ponomareva, 2018).

Advantages- With this budget an organisation is able to measure their overall growth

and profitability because of rigid or fixed nature of budget.

Disadvantages- The major drawback of fixed-budget is that they are not modify as per

the requirement of production due to this they are not effective in future.

Master-budget- This budget are formulated by the manager for forecast overall amount of sales

within decided factors and it is also useful to gather the overall capital which is required to invest

and execute. Moreover, master-budget are formulated with purpose of deciding the performance

standards and plans related with business operations.

Advantage- Budget perform an important role to determine the overall cost which is

related with the production process and it improves the total productivity of business.

Disadvantage- Master-budget are prepared for achieve the specific production process

so after target overall accuracy and reliability of the information is minimised.

Various Pricing system Full cost pricing- According to the strategy of full cost pricing an organisation

determine the overall value of services or products which engage the direct-material,

direct-labour, etc. and also, all those systems cost that is incurred in process of

production.

Cost plus pricing- This pricing method is considered as all those cost related factors that

includes overall cost and also all those basis which helps to add more unit of products.

In addition to Rowlinson Knitwear cost plus pricing aids for calculate overall overheads

of business.

TASK 4

P5 Management accounting systems and their response towards financial problems

Balance Card Approach- The main role of balance card approach is to align all

activities of the business and they are related with policies and objectives. With induce of

balance card approach each activity of the organisation is coordinated and evaluated by the

authorities in an organised manner (Patterson, McDonald and Hardy, 2017). Furthermore,

Rowlin Knitwear and other organisation arrange training sessions for the engaged workforce and

this helps the company for perform their task or project with more efficiency.

Some perspective of balance card approach are mention as follow:

Customer and stakeholders- This relates with obligation of each organisation that are

performing their operations in the market. One of the main motive of the engaged

workforce is to offer good quality products that enhance overall wealth of stakeholders or

shareholders who are engaged in company operations.

Financial- The main purpose or goal of each organisation is to enhance their overall

profits of business. In the context of Rowlinson Knitwear the current focus of the

financial manager and authorities is to attain a strong financial position among the

market. This aids management to enhance their overall profits by engage profitable

projects.

so after target overall accuracy and reliability of the information is minimised.

Various Pricing system Full cost pricing- According to the strategy of full cost pricing an organisation

determine the overall value of services or products which engage the direct-material,

direct-labour, etc. and also, all those systems cost that is incurred in process of

production.

Cost plus pricing- This pricing method is considered as all those cost related factors that

includes overall cost and also all those basis which helps to add more unit of products.

In addition to Rowlinson Knitwear cost plus pricing aids for calculate overall overheads

of business.

TASK 4

P5 Management accounting systems and their response towards financial problems

Balance Card Approach- The main role of balance card approach is to align all

activities of the business and they are related with policies and objectives. With induce of

balance card approach each activity of the organisation is coordinated and evaluated by the

authorities in an organised manner (Patterson, McDonald and Hardy, 2017). Furthermore,

Rowlin Knitwear and other organisation arrange training sessions for the engaged workforce and

this helps the company for perform their task or project with more efficiency.

Some perspective of balance card approach are mention as follow:

Customer and stakeholders- This relates with obligation of each organisation that are

performing their operations in the market. One of the main motive of the engaged

workforce is to offer good quality products that enhance overall wealth of stakeholders or

shareholders who are engaged in company operations.

Financial- The main purpose or goal of each organisation is to enhance their overall

profits of business. In the context of Rowlinson Knitwear the current focus of the

financial manager and authorities is to attain a strong financial position among the

market. This aids management to enhance their overall profits by engage profitable

projects.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

KPI- Key performance indicators are identified as one of the most effective tool to

measure the performance and also to compare them with actual performance of employees. In

the present scenario, management of each organisation compare their actual outcomes or

performance with the decided standards (Wang and et. al., 2018). Moreover, internal

management of each organisation analyse all variations in order to take corrective actions that is

required for rectify the current challenges or problems related with business. Along with this KPI

is used in different stages to evaluate the capability and success for accomplish the desired goals

and objectives of business.

ISSUE

To deal with all financial issue manager of the Rowlinson Knitwear utilise management

accounting systems. One of the major issue faced by authorities is that the number of profits is

constantly reducing and the rational behind this is not use of company resources in an optimise

manner. Therefore, the main focus of organisation is to learn and induce KPI methods because it

helps for evaluate overall capability related with each department of organisation.

CONCLUSION

With the discussion of above report this is concluded that management accounting

perform an important role for internal management to formulate all those policies that define and

accomplish company objectives and goals. Financial positions and trends of the market are also

analysed through induce appropriate management accounting techniques. Furthermore, the report

also conclude about different budgets and this assist the manager of an organisation to decide

appropriate performance standards of business. Budget report, job-costing report, etc. perform an

important role to formulate policies and it support internal management to enhance overall

performance. In the last, absorption and marginal costing method are used for generate the

accurate income statement for business.

measure the performance and also to compare them with actual performance of employees. In

the present scenario, management of each organisation compare their actual outcomes or

performance with the decided standards (Wang and et. al., 2018). Moreover, internal

management of each organisation analyse all variations in order to take corrective actions that is

required for rectify the current challenges or problems related with business. Along with this KPI

is used in different stages to evaluate the capability and success for accomplish the desired goals

and objectives of business.

ISSUE

To deal with all financial issue manager of the Rowlinson Knitwear utilise management

accounting systems. One of the major issue faced by authorities is that the number of profits is

constantly reducing and the rational behind this is not use of company resources in an optimise

manner. Therefore, the main focus of organisation is to learn and induce KPI methods because it

helps for evaluate overall capability related with each department of organisation.

CONCLUSION

With the discussion of above report this is concluded that management accounting

perform an important role for internal management to formulate all those policies that define and

accomplish company objectives and goals. Financial positions and trends of the market are also

analysed through induce appropriate management accounting techniques. Furthermore, the report

also conclude about different budgets and this assist the manager of an organisation to decide

appropriate performance standards of business. Budget report, job-costing report, etc. perform an

important role to formulate policies and it support internal management to enhance overall

performance. In the last, absorption and marginal costing method are used for generate the

accurate income statement for business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Bleyen, P and et. al., 2017. Linking budgeting to results? Evidence about performance budgets in

European municipalities based on a comparative analytical model. Public Management

Review, 19(7), pp.932-953.

Bruno, A. and Lapsley, I., 2018. The emergence of an accounting practice: The fabrication of a

government accrual accounting system. Accounting, Auditing & Accountability Journal.

Crespo, N.F., Rodrigues, R., Samagaio, A. and Silva, G.M., 2019. The adoption of management

control systems by start-ups: Internal factors and context as determinants. Journal of

Business Research, 101, pp.875-884.

Grossi, G and et. al., 2019. Accounting, performance management systems and accountability

changes in knowledge-intensive public organizations: a literature review and research

agenda. Accounting, Auditing & Accountability Journal.

Hadiyanto, A., Puspitasari, E. and Ghani, E.K., 2018. The effect of accounting methods on

financial reporting quality. International Journal of Law and Management.

Harris, S and et. al., 2020. Low carbon cities in 2050? GHG emissions of European cities using

production-based and consumption-based emission accounting methods. Journal of

Cleaner Production, 248, p.119206.

Koolmees, D., Bernstein, D.N. and Makhni, E.C., 2021. Time-Driven Activity-Based Costing

Provides a Lower and More Accurate Assessment of Costs in the Field of Orthopaedic

Surgery Compared With Traditional Accounting Methods. Arthroscopy: The Journal of

Arthroscopic & Related Surgery, 37(5), pp.1620-1627.

Kudlák, A and et. al., 2020. Determination of the financial minimum in a municipal budget to

deal with crisis situations. Soft Computing, 24(12), pp.8607-8616.

Liu, J. and Wang, Q., 2017. Accounting methods research for ecological compensation standard

in the Three-River Headwaters Region based on supply cost. Research of

Environmental Sciences, 30(1), pp.82-90.

Nikitina, O.A., Litovskaya, Y.V. and Ponomareva, O.S., 2018. Development of the cost

management mechanism for metal products manufacturing based on budgeting

method. Academy of Strategic Management Journal, 17(5), pp.1-17.

Patterson, M., McDonald, G. and Hardy, D., 2017. Is there more in common than we think?

Convergence of ecological footprinting, emergy analysis, life cycle assessment and

other methods of environmental accounting. Ecological Modelling, 362, pp.19-36.

Schaltegger, S., Etxeberria, I.Á. and Ortas, E., 2017. Innovating corporate accounting and

reporting for sustainability–attributes and challenges. Sustainable Development, 25(2),

pp.113-122.

Wang, Z and et. al., 2018. Comparative analysis of regional carbon emissions accounting

methods in China: Production-based versus consumption-based principles. Journal of

Cleaner Production, 194, pp.12-22.

Yudina, T.A and et. al., 2017. Effectiveness of the methods of internal financial control as a

guarantee of sustainability of tourism companies' development. Journal of

Environmental Management & Tourism, 8(4 (20)), pp.861-866.

Books and Journals

Bleyen, P and et. al., 2017. Linking budgeting to results? Evidence about performance budgets in

European municipalities based on a comparative analytical model. Public Management

Review, 19(7), pp.932-953.

Bruno, A. and Lapsley, I., 2018. The emergence of an accounting practice: The fabrication of a

government accrual accounting system. Accounting, Auditing & Accountability Journal.

Crespo, N.F., Rodrigues, R., Samagaio, A. and Silva, G.M., 2019. The adoption of management

control systems by start-ups: Internal factors and context as determinants. Journal of

Business Research, 101, pp.875-884.

Grossi, G and et. al., 2019. Accounting, performance management systems and accountability

changes in knowledge-intensive public organizations: a literature review and research

agenda. Accounting, Auditing & Accountability Journal.

Hadiyanto, A., Puspitasari, E. and Ghani, E.K., 2018. The effect of accounting methods on

financial reporting quality. International Journal of Law and Management.

Harris, S and et. al., 2020. Low carbon cities in 2050? GHG emissions of European cities using

production-based and consumption-based emission accounting methods. Journal of

Cleaner Production, 248, p.119206.

Koolmees, D., Bernstein, D.N. and Makhni, E.C., 2021. Time-Driven Activity-Based Costing

Provides a Lower and More Accurate Assessment of Costs in the Field of Orthopaedic

Surgery Compared With Traditional Accounting Methods. Arthroscopy: The Journal of

Arthroscopic & Related Surgery, 37(5), pp.1620-1627.

Kudlák, A and et. al., 2020. Determination of the financial minimum in a municipal budget to

deal with crisis situations. Soft Computing, 24(12), pp.8607-8616.

Liu, J. and Wang, Q., 2017. Accounting methods research for ecological compensation standard

in the Three-River Headwaters Region based on supply cost. Research of

Environmental Sciences, 30(1), pp.82-90.

Nikitina, O.A., Litovskaya, Y.V. and Ponomareva, O.S., 2018. Development of the cost

management mechanism for metal products manufacturing based on budgeting

method. Academy of Strategic Management Journal, 17(5), pp.1-17.

Patterson, M., McDonald, G. and Hardy, D., 2017. Is there more in common than we think?

Convergence of ecological footprinting, emergy analysis, life cycle assessment and

other methods of environmental accounting. Ecological Modelling, 362, pp.19-36.

Schaltegger, S., Etxeberria, I.Á. and Ortas, E., 2017. Innovating corporate accounting and

reporting for sustainability–attributes and challenges. Sustainable Development, 25(2),

pp.113-122.

Wang, Z and et. al., 2018. Comparative analysis of regional carbon emissions accounting

methods in China: Production-based versus consumption-based principles. Journal of

Cleaner Production, 194, pp.12-22.

Yudina, T.A and et. al., 2017. Effectiveness of the methods of internal financial control as a

guarantee of sustainability of tourism companies' development. Journal of

Environmental Management & Tourism, 8(4 (20)), pp.861-866.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.