MAFI1A-8: Management Accounting & GTZ Group Efficiency Analysis

VerifiedAdded on 2023/04/19

|11

|2107

|185

Homework Assignment

AI Summary

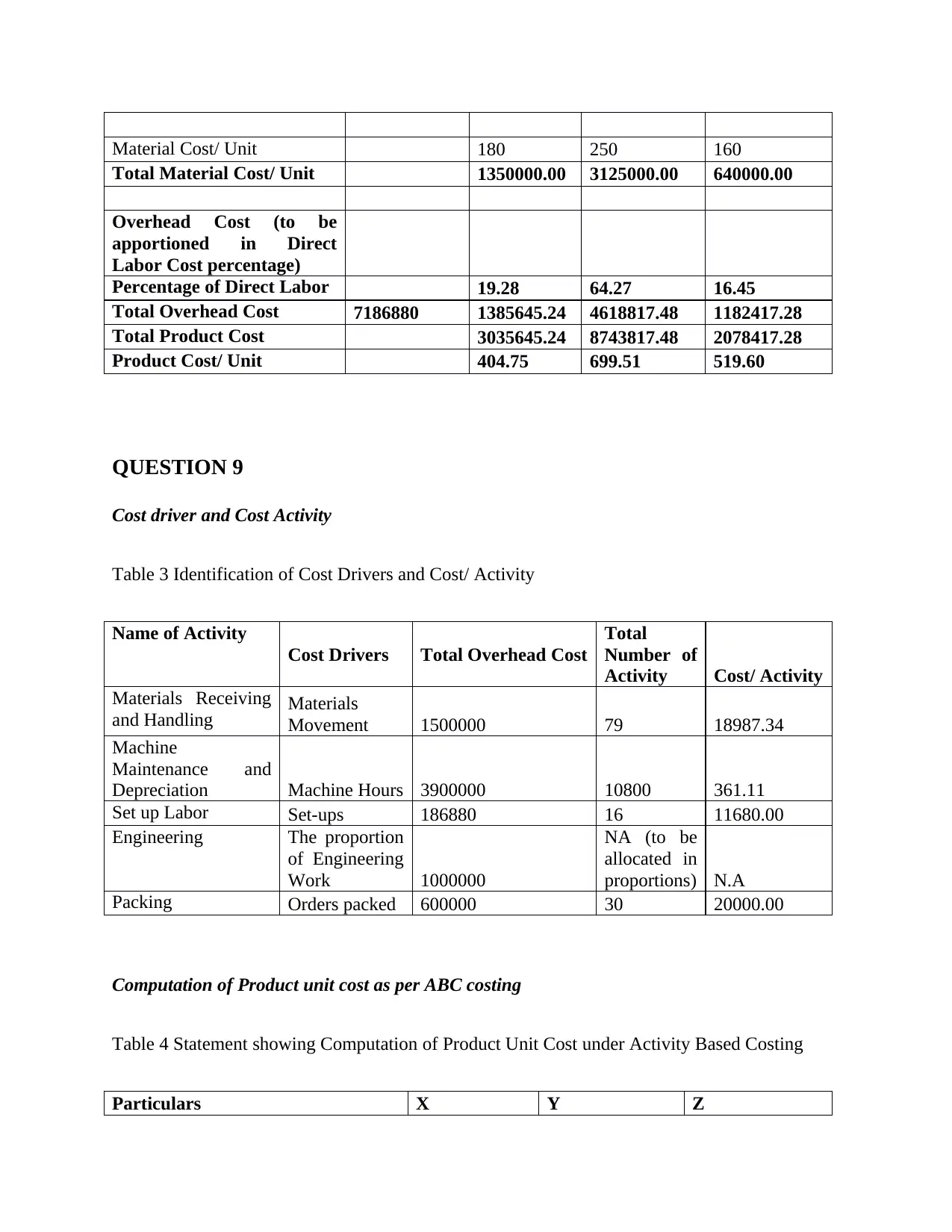

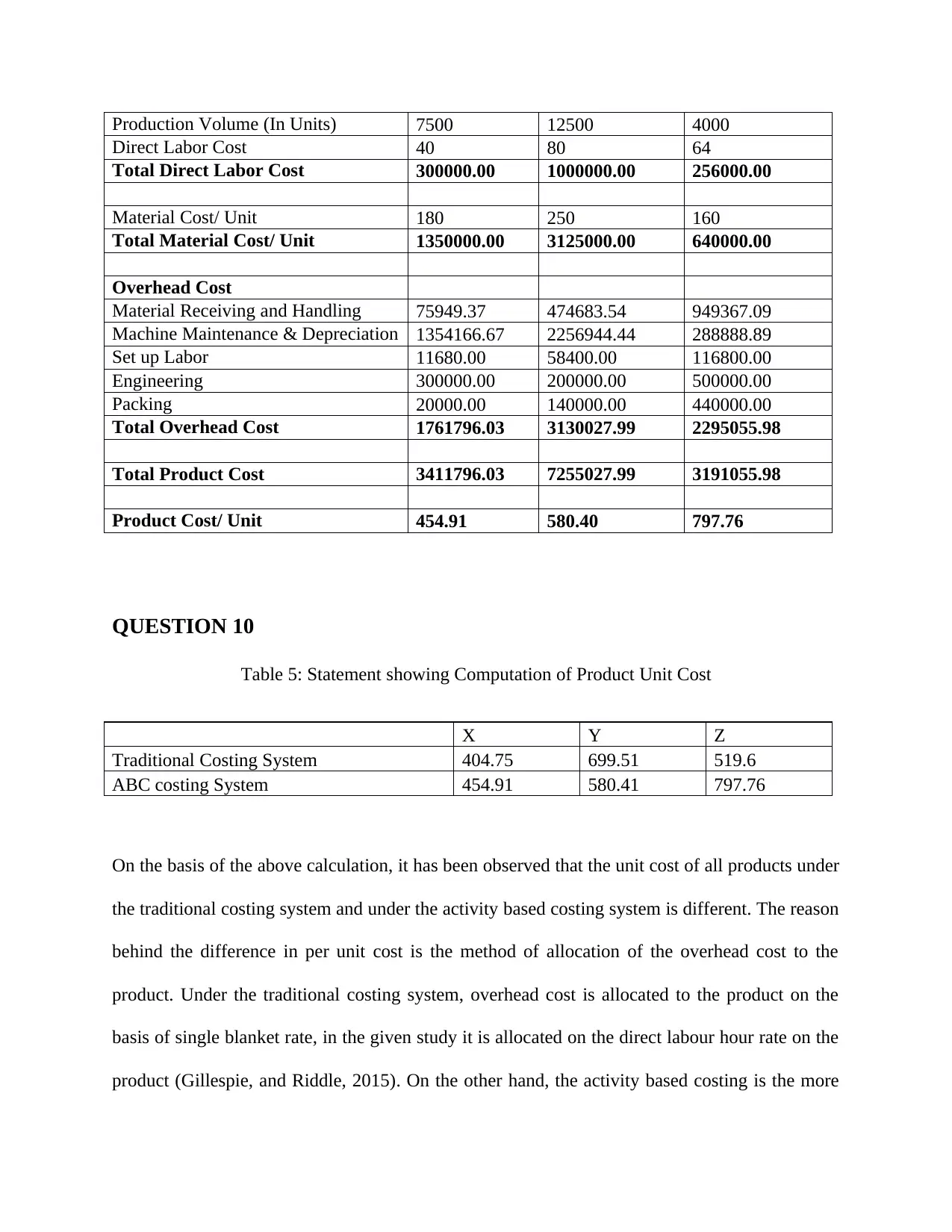

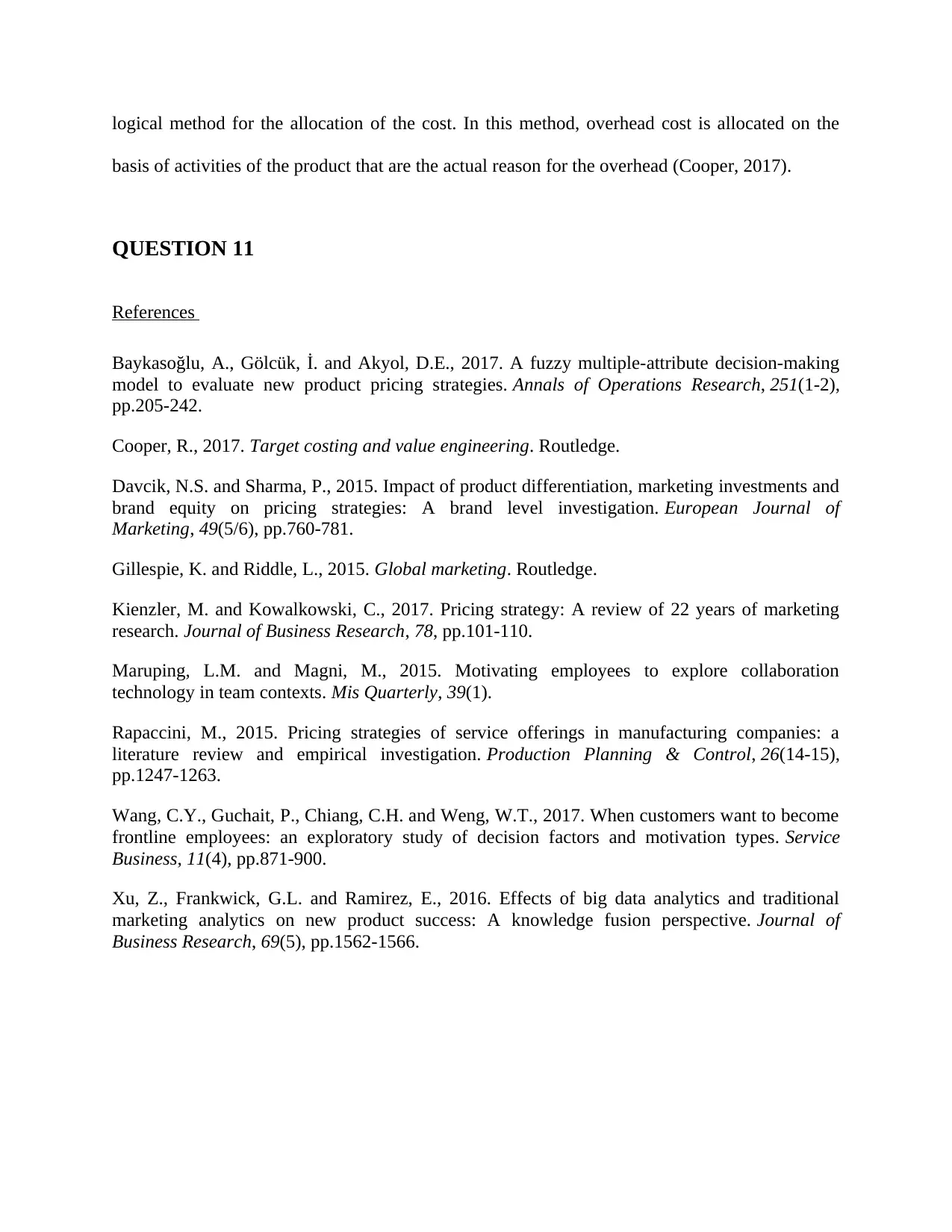

This assignment delves into various aspects of management accounting, focusing on enhancing business efficiency and performance within the context of the GTZ Group. It covers topics such as incremental revenue analysis for decision-making, motivational factors for employees, promotional pricing techniques, and pricing strategies like price skimming. The assignment includes a detailed calculation of profit-maximizing selling prices and a discussion on the importance of reconsidering pricing policies in response to market competition. Furthermore, it examines product lifecycle stages and their impact on pricing and cost management. The assignment also provides a comparative analysis of traditional costing systems versus activity-based costing (ABC) and their effects on product unit costs, along with a discussion on the rationale behind the differences observed. This comprehensive analysis is designed to provide practical insights into improving business operations through effective management accounting practices. Desklib offers a range of similar resources for students seeking further assistance.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.