Management Accounting: Planning & Control in Business - BTEC Level 4

VerifiedAdded on 2023/06/18

|21

|6487

|246

Report

AI Summary

This management accounting report focuses on ABC Ltd and covers various aspects of management accounting, including its definition, essential requirements, and different reporting methods. It discusses cash flow analysis, inventory turnover analysis, job costing systems, and price optimization systems. The report also highlights the benefits of management accounting systems, such as increased efficiency, profit maximization, and improved decision-making. Furthermore, it includes calculations of production cost per unit, total production cost, and total cost of sales, along with the application of techniques for preparing budget profit and loss statements. The advantages and disadvantages of different planning tools used in budgetary control are also explained. The report concludes by evaluating how management accounting systems help organizations respond to financial problems and achieve sustainable success. Desklib offers a variety of solved assignments and past papers for students.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENT

INTRODUCTION ..........................................................................................................................3

TASK 1............................................................................................................................................4

MAIN BODY...................................................................................................................................4

Defining Management accounting and also the essential requirements to the different types of

management accounting system..................................................................................................4

Different methods used for the management accounting reporting.............................................5

Benefits of management accounting systems..............................................................................6

Critical evaluation of management accounting systems and management accounting reporting

......................................................................................................................................................6

TASK 2............................................................................................................................................7

Calculation of the Production cost per unit, Total production cost and total cost of sales..........7

Application of techniques for the production of the budget profit and Loss statement...............9

Amount £..................................................................................................................9

Reconciliation statement of profit figures......................................................................................10

TASK 3..........................................................................................................................................11

Explaining advantages and disadvantages of different types of planning tools used in

budgetary control.......................................................................................................................11

Explaining use of different planning tools and their applications for preparing and.................13

forecasting budgets....................................................................................................................13

Evaluating planning tools for management accounting respond appropriately for...................14

solving financial problems to lead organizations to sustainable success..................................14

TASK 4..........................................................................................................................................15

Explaining how management accounting system is adopted by organization to respond to

financial problems .....................................................................................................................15

Responding to the financial problems can lead the organization to sustainability success.......16

Evaluation of planning tools for the management accounting for responding to the appropriate

solution of the financial problems..............................................................................................16

CONCLUSION..............................................................................................................................18

REFERENCES..............................................................................................................................19

INTRODUCTION ..........................................................................................................................3

TASK 1............................................................................................................................................4

MAIN BODY...................................................................................................................................4

Defining Management accounting and also the essential requirements to the different types of

management accounting system..................................................................................................4

Different methods used for the management accounting reporting.............................................5

Benefits of management accounting systems..............................................................................6

Critical evaluation of management accounting systems and management accounting reporting

......................................................................................................................................................6

TASK 2............................................................................................................................................7

Calculation of the Production cost per unit, Total production cost and total cost of sales..........7

Application of techniques for the production of the budget profit and Loss statement...............9

Amount £..................................................................................................................9

Reconciliation statement of profit figures......................................................................................10

TASK 3..........................................................................................................................................11

Explaining advantages and disadvantages of different types of planning tools used in

budgetary control.......................................................................................................................11

Explaining use of different planning tools and their applications for preparing and.................13

forecasting budgets....................................................................................................................13

Evaluating planning tools for management accounting respond appropriately for...................14

solving financial problems to lead organizations to sustainable success..................................14

TASK 4..........................................................................................................................................15

Explaining how management accounting system is adopted by organization to respond to

financial problems .....................................................................................................................15

Responding to the financial problems can lead the organization to sustainability success.......16

Evaluation of planning tools for the management accounting for responding to the appropriate

solution of the financial problems..............................................................................................16

CONCLUSION..............................................................................................................................18

REFERENCES..............................................................................................................................19

INTRODUCTION

Management accounting is the process which helps the business in the preparation of the

business operations which helps the managers in the short-term and long-term decision-making

with the help of financial analysis. The management accounting is the identification,

measurement, analysation and interpretation and communication of the financial information for

the better decision-making. In this project the chosen organization is the ABC Ltd for which the

management accounting will be discussed. This project helps the business in providing essential

requirements of the different types of management accounting systems. This project will also

provide the discussion of the different methods of management accounting reporting. In this

project the calculation of the costs which are used for the analysation of the appropriate

Management accounting is the process which helps the business in the preparation of the

business operations which helps the managers in the short-term and long-term decision-making

with the help of financial analysis. The management accounting is the identification,

measurement, analysation and interpretation and communication of the financial information for

the better decision-making. In this project the chosen organization is the ABC Ltd for which the

management accounting will be discussed. This project helps the business in providing essential

requirements of the different types of management accounting systems. This project will also

provide the discussion of the different methods of management accounting reporting. In this

project the calculation of the costs which are used for the analysation of the appropriate

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

techniques of the cost analysis and the preparation of the income statement for the application of

the marginal and absorption cost system has been utilized. This project also provides the

advantages and disadvantages of the different types of planning tools which is used for budgetary

control. In this project the comparison of how the organization is adapting to the management

accounting systems for responding to the financial problems.

TASK 1

MAIN BODY

Defining Management accounting and also the essential requirements to the different types of

management accounting system

The management accounting system is that process which helps in the preparation of

different reports about the business operations which help the managers for making short-term

and long-term decisions which helps the business in the pursuing the goals and also the

identification, measurement and analysation of the interpretation of the communicated

information to the managers of the organization (Quinn and et.al., 2018). This is also very

helpful for forecasting the future which helps the business in the management of the upcoming

issues. Management accounting also allows the business in the making the decision related to the

cost and production of the organization which allows the business in understanding the factors of

the purchasing choices of the data from the managerial and accounting empowerment of the

decision-making of the operations in the strategical level. Management accounting is known for

being very important for the analysation of the future cash inflows in the business. The essential

requirements in different types of management accounting system are,

Cash flow analysis :

In the management accounting the performance of the cash flow analysis for the

determination the cash which impacts the business decision of the organization. This

management accounting system helps in the analysation of the inflowing cash which allows the

business of in financial information which is considered to be the best way in which the future

performance of the business can be considered (Alabdullah, 2019.).

Inventory turnover analysis :

The Inventory turnover analysis is the part of the management accounting system which

helps the business in the calculation of how many times the company has sold all the stock which

it purchased. This cycle of inventory getting replaced is known as the turnover of the business

the marginal and absorption cost system has been utilized. This project also provides the

advantages and disadvantages of the different types of planning tools which is used for budgetary

control. In this project the comparison of how the organization is adapting to the management

accounting systems for responding to the financial problems.

TASK 1

MAIN BODY

Defining Management accounting and also the essential requirements to the different types of

management accounting system

The management accounting system is that process which helps in the preparation of

different reports about the business operations which help the managers for making short-term

and long-term decisions which helps the business in the pursuing the goals and also the

identification, measurement and analysation of the interpretation of the communicated

information to the managers of the organization (Quinn and et.al., 2018). This is also very

helpful for forecasting the future which helps the business in the management of the upcoming

issues. Management accounting also allows the business in the making the decision related to the

cost and production of the organization which allows the business in understanding the factors of

the purchasing choices of the data from the managerial and accounting empowerment of the

decision-making of the operations in the strategical level. Management accounting is known for

being very important for the analysation of the future cash inflows in the business. The essential

requirements in different types of management accounting system are,

Cash flow analysis :

In the management accounting the performance of the cash flow analysis for the

determination the cash which impacts the business decision of the organization. This

management accounting system helps in the analysation of the inflowing cash which allows the

business of in financial information which is considered to be the best way in which the future

performance of the business can be considered (Alabdullah, 2019.).

Inventory turnover analysis :

The Inventory turnover analysis is the part of the management accounting system which

helps the business in the calculation of how many times the company has sold all the stock which

it purchased. This cycle of inventory getting replaced is known as the turnover of the business

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

which is considered important factor that helps the business in the management of the

organizations importance and other operations.

Job costing system :

This is that part of the management accounting system which manages the accounts

receivable report of the organization that is considered to be categorized to have a very positive

effects on the company's bottom line (Zandi, 2019). The management of the accounts receivable

ageing report is said to be categorized in the AR invoices which helps the business in the length

of time of how outstanding this business can be.

Price optimization system :

Preparation of the budgets is very essential for the organization as it creates the

quantitative expression of the company's plan on what it wants to implement in its operations

that will allow the business in the utilization of the performance reports for noting the deviation

of the actual results from budgets and positive or negative deviations from the budget.

Different methods used for the management accounting reporting

Different types of management accounting reporting which this business needs to

consider in the management accounting are,

Budget Reports :

The managerial reports of the organization is directly related to the creation of the budget

managerial accounting reports that is considered to be very critical for the measurement of the

company's performance (Wahyuningsih and et.al., 2021.). These reports are prepared with the

help of the estimation of the previous experienced budget which can create an unforeseen

circumstance that might arise in the organization.

Account Receivable Ageing Reports :

The preparation of these reports is considered to be very dependent over the breaking

down of the customers remaining balances of what the business will receive. The corporate

culture of the organization is decided with the help of business to estimate how much the

business will receive.

Cost managerial accounting Reports :

Management of the cost reports is very essential for the business as it help the busies in

the estimation of how much expenditure it will for the generation of a certain revenue. This is the

organizations importance and other operations.

Job costing system :

This is that part of the management accounting system which manages the accounts

receivable report of the organization that is considered to be categorized to have a very positive

effects on the company's bottom line (Zandi, 2019). The management of the accounts receivable

ageing report is said to be categorized in the AR invoices which helps the business in the length

of time of how outstanding this business can be.

Price optimization system :

Preparation of the budgets is very essential for the organization as it creates the

quantitative expression of the company's plan on what it wants to implement in its operations

that will allow the business in the utilization of the performance reports for noting the deviation

of the actual results from budgets and positive or negative deviations from the budget.

Different methods used for the management accounting reporting

Different types of management accounting reporting which this business needs to

consider in the management accounting are,

Budget Reports :

The managerial reports of the organization is directly related to the creation of the budget

managerial accounting reports that is considered to be very critical for the measurement of the

company's performance (Wahyuningsih and et.al., 2021.). These reports are prepared with the

help of the estimation of the previous experienced budget which can create an unforeseen

circumstance that might arise in the organization.

Account Receivable Ageing Reports :

The preparation of these reports is considered to be very dependent over the breaking

down of the customers remaining balances of what the business will receive. The corporate

culture of the organization is decided with the help of business to estimate how much the

business will receive.

Cost managerial accounting Reports :

Management of the cost reports is very essential for the business as it help the busies in

the estimation of how much expenditure it will for the generation of a certain revenue. This is the

reason why it is considered that with the help of this cost managerial accounting the business is

able to fix a selling price which contains the margin of profit in the organization.

Inventory Reports :

In an organization which deals with a certain type of product it is important for the

business to manage its inventory which is considered to be the essential factors which helps the

business in the management of organizational performance. It also helps the business in gaining

fasted turnover (Astuty and Pasaribu, 2021).

Benefits of management accounting systems

The benefits of the management accounting system and their application for the business

are,

Increases Efficiency :

The management accounting system is considered to be one of the most effective way in

which the business can increase its efficiency. This happens as the business plans its expenses

according to the analysed reports of the company finances.

Maximization of profit :

The management accounting's budgetary control and capital budgeting tool helps the

business in the development of a plan which can be used by the business for creation of the

reduced costs and increasing the profit maximization.

Controlling Cash flow :

Controlling cash flow is very essential part of the management accounting as it helps the

business in creating a control of cash flow and also help it in the management of the cash which

is considered to be better with the foxed properties (Javed and Malik, 2021).

Decision-making :

Management accounting system is very important for this organization to develop a

decision-making process. Which is essential for the organization in the management of the

organization and also the development of a reliable management that is essential for the decision-

making of the business.

Simplification of financial statements :

In this business it is very important that the organization is able to manage the financial

statement as it is useful for the business to create comparison with other competitors that can

allow the business to grow.

able to fix a selling price which contains the margin of profit in the organization.

Inventory Reports :

In an organization which deals with a certain type of product it is important for the

business to manage its inventory which is considered to be the essential factors which helps the

business in the management of organizational performance. It also helps the business in gaining

fasted turnover (Astuty and Pasaribu, 2021).

Benefits of management accounting systems

The benefits of the management accounting system and their application for the business

are,

Increases Efficiency :

The management accounting system is considered to be one of the most effective way in

which the business can increase its efficiency. This happens as the business plans its expenses

according to the analysed reports of the company finances.

Maximization of profit :

The management accounting's budgetary control and capital budgeting tool helps the

business in the development of a plan which can be used by the business for creation of the

reduced costs and increasing the profit maximization.

Controlling Cash flow :

Controlling cash flow is very essential part of the management accounting as it helps the

business in creating a control of cash flow and also help it in the management of the cash which

is considered to be better with the foxed properties (Javed and Malik, 2021).

Decision-making :

Management accounting system is very important for this organization to develop a

decision-making process. Which is essential for the organization in the management of the

organization and also the development of a reliable management that is essential for the decision-

making of the business.

Simplification of financial statements :

In this business it is very important that the organization is able to manage the financial

statement as it is useful for the business to create comparison with other competitors that can

allow the business to grow.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Critical evaluation of management accounting systems and management accounting reporting

The management accounting system is the generates the information which helps in the

satisfaction the needs of the management which is towards the reporting of its financial

accounting and managerial accounting. It is that process which is essential for the preparation of

the reports and accounts required for the management of the business decision-making. It is that

branch which allows the business in the management of the accounting of the brand containing

the accounting information in a presented form towards the interested parties. Management

accounting system is very essential for the management of the financial information of the

managers for planning and controlling the different activities (Korhonen and et.al.,2020).

Management accounting reporting is the development of a dual role which performs in

the organization as the strategic partner towards providing the strategic based financial and

operational information. The management accountant plays a very prominent role in the

preparation of financial reports, risks and also the regulatory reporting for the aggregation of the

financial information. These reports also contain the performance cost analysis which is helpful

for the production and division which includes the variable and fixed costs.

TASK 2

Calculation of the Production cost per unit, Total production cost and total cost of sales

calculation of production cost per unit

Particulars January

Direct material 10

Direct labour 20

Variable production overhead 5

Fixed production overhead 5.5555555556

Total production cost 40.56

Total production cost

Particulars January

Direct material 180000

Direct Labour 360000

Variable production overhead 90000

The management accounting system is the generates the information which helps in the

satisfaction the needs of the management which is towards the reporting of its financial

accounting and managerial accounting. It is that process which is essential for the preparation of

the reports and accounts required for the management of the business decision-making. It is that

branch which allows the business in the management of the accounting of the brand containing

the accounting information in a presented form towards the interested parties. Management

accounting system is very essential for the management of the financial information of the

managers for planning and controlling the different activities (Korhonen and et.al.,2020).

Management accounting reporting is the development of a dual role which performs in

the organization as the strategic partner towards providing the strategic based financial and

operational information. The management accountant plays a very prominent role in the

preparation of financial reports, risks and also the regulatory reporting for the aggregation of the

financial information. These reports also contain the performance cost analysis which is helpful

for the production and division which includes the variable and fixed costs.

TASK 2

Calculation of the Production cost per unit, Total production cost and total cost of sales

calculation of production cost per unit

Particulars January

Direct material 10

Direct labour 20

Variable production overhead 5

Fixed production overhead 5.5555555556

Total production cost 40.56

Total production cost

Particulars January

Direct material 180000

Direct Labour 360000

Variable production overhead 90000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Fixed production overhead 100000

Total production cost 730000.00

Cost of good sold

Budgeted Actual

Particulars Amount £ Amount £ Amount £ Amount £

Opening

inventory

Add Production

18000×40.5

6 730080

19000×40.5

6 770640

Less

Closing

inventory 2000×40.56 81120 3000×40.56 121680

COGS 648960 648960

Production cost per unit :

The per unit cost of production is said to be the one which helps the business in the

management of the organization as the total cost of production cost is divided by the total

numbers of units produced. It is essential for the business to provide a different number of units

which can be considered to be productive and also be in relation to the concept that is

understands in the accumulation of the costs.

Total Production costs :

This project helps in the determination of the unit cost of the production which

helps the business in the understanding the to total cost it incurred in the manufacturing of its

products. The total production cost of the organization is considered to be the one which is very

important for the organization in the understanding what is the total cost which it incurs for the

production of a certain amount of units (Gomez-Conde, Lunkes and Rosa, 2019). This cost is

very useful in the preparation of the budget as it helps the business in understanding how much

Total production cost 730000.00

Cost of good sold

Budgeted Actual

Particulars Amount £ Amount £ Amount £ Amount £

Opening

inventory

Add Production

18000×40.5

6 730080

19000×40.5

6 770640

Less

Closing

inventory 2000×40.56 81120 3000×40.56 121680

COGS 648960 648960

Production cost per unit :

The per unit cost of production is said to be the one which helps the business in the

management of the organization as the total cost of production cost is divided by the total

numbers of units produced. It is essential for the business to provide a different number of units

which can be considered to be productive and also be in relation to the concept that is

understands in the accumulation of the costs.

Total Production costs :

This project helps in the determination of the unit cost of the production which

helps the business in the understanding the to total cost it incurred in the manufacturing of its

products. The total production cost of the organization is considered to be the one which is very

important for the organization in the understanding what is the total cost which it incurs for the

production of a certain amount of units (Gomez-Conde, Lunkes and Rosa, 2019). This cost is

very useful in the preparation of the budget as it helps the business in understanding how much

cost it needs to spend in the organization. It can also allow the business in understanding the

management of the organization.

Total cost sales :

The total cost of sales is the actual cost which is incurred in selling of the products of the

organization. It can be considered as the actual cost which includes both the direct and indirect

expenses of the organization. It includes the production cost and also the administrative cost

which are considered to be very essential for the organization in the management of the

organization (falih Chichan and Alabdullah, 2021).

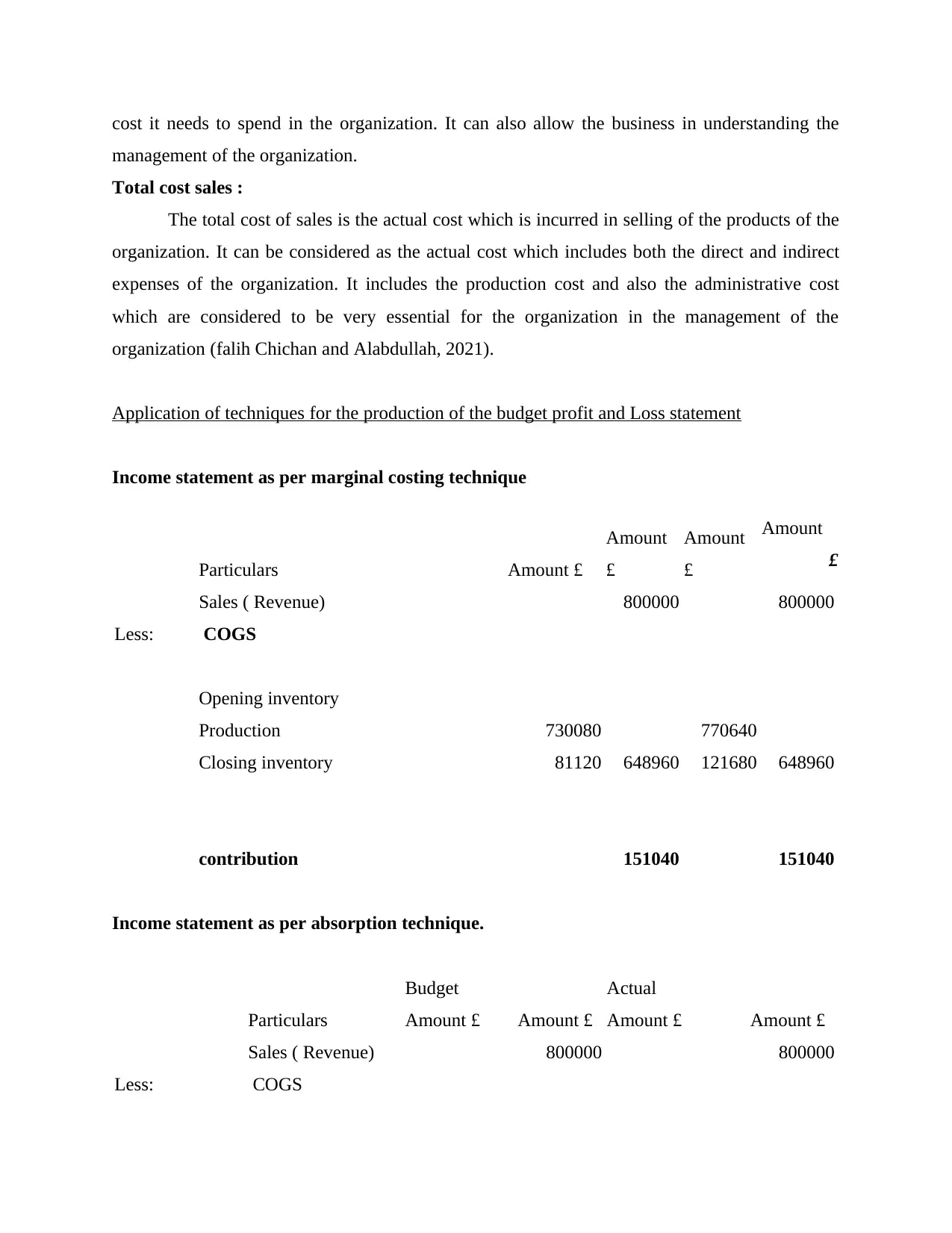

Application of techniques for the production of the budget profit and Loss statement

Income statement as per marginal costing technique

Particulars Amount £

Amount

£

Amount

£

Amount

£

Sales ( Revenue) 800000 800000

Less: COGS

Opening inventory

Production 730080 770640

Closing inventory 81120 648960 121680 648960

contribution 151040 151040

Income statement as per absorption technique.

Budget Actual

Particulars Amount £ Amount £ Amount £ Amount £

Sales ( Revenue) 800000 800000

Less: COGS

management of the organization.

Total cost sales :

The total cost of sales is the actual cost which is incurred in selling of the products of the

organization. It can be considered as the actual cost which includes both the direct and indirect

expenses of the organization. It includes the production cost and also the administrative cost

which are considered to be very essential for the organization in the management of the

organization (falih Chichan and Alabdullah, 2021).

Application of techniques for the production of the budget profit and Loss statement

Income statement as per marginal costing technique

Particulars Amount £

Amount

£

Amount

£

Amount

£

Sales ( Revenue) 800000 800000

Less: COGS

Opening inventory

Production 730080 770640

Closing inventory 81120 648960 121680 648960

contribution 151040 151040

Income statement as per absorption technique.

Budget Actual

Particulars Amount £ Amount £ Amount £ Amount £

Sales ( Revenue) 800000 800000

Less: COGS

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

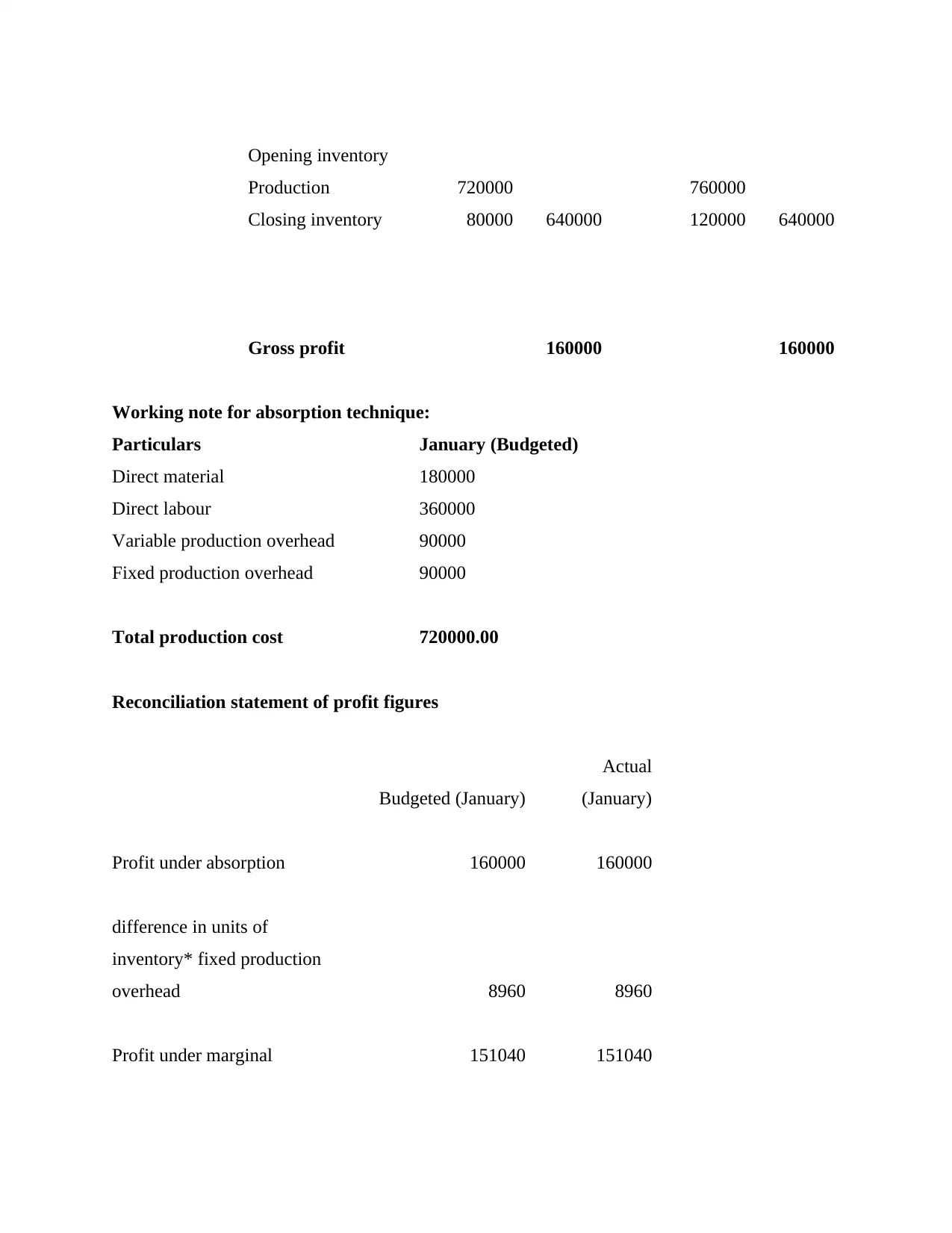

Opening inventory

Production 720000 760000

Closing inventory 80000 640000 120000 640000

Gross profit 160000 160000

Working note for absorption technique:

Particulars January (Budgeted)

Direct material 180000

Direct labour 360000

Variable production overhead 90000

Fixed production overhead 90000

Total production cost 720000.00

Reconciliation statement of profit figures

Budgeted (January)

Actual

(January)

Profit under absorption 160000 160000

difference in units of

inventory* fixed production

overhead 8960 8960

Profit under marginal 151040 151040

Production 720000 760000

Closing inventory 80000 640000 120000 640000

Gross profit 160000 160000

Working note for absorption technique:

Particulars January (Budgeted)

Direct material 180000

Direct labour 360000

Variable production overhead 90000

Fixed production overhead 90000

Total production cost 720000.00

Reconciliation statement of profit figures

Budgeted (January)

Actual

(January)

Profit under absorption 160000 160000

difference in units of

inventory* fixed production

overhead 8960 8960

Profit under marginal 151040 151040

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The income statement of the organization the following methods are used such as,

Marginal costing :

This method of marginal costing is known as the method in which the cos are considered

to be the production cost and fixed cost that allow the business in the analysation of the cost for

the given period. It is the technique which allows the business in assuming the variable costs and

production cost to be effective in the preparation of the income statement of the organization.

This method of preparation of the income statement is considered to be very essential for the

production cost and also the fixed cost of the organization that can allow the business in

assuming the cost for the given period. In this technique of management of the cost of the

organization. Both the fixed costs and the variable costs are considered that can allow the

business in the calculation of the income of the organization (Hertati and Safkaur, 2019). This

method also has the utilization of the P/V ratio which is the profit value ratio which is used by

the management to understand the efficiency of the organization. It helps in the determination of

the cost of the next unit as it allows the business in the management of its overheads. The

management costing method of this business is said to be very effective as it provides more

emphasis on the change on the opening stocks and the closing stocks which affects the per unit

cost of production. In this method the organization is able to understand the total contribution to

the per unit production. Contribution is shown as the main emphasis to the total production cost

in this method. The preparation of income statement which uses marginal costing utilizes the

total contribution of the organization.

Absorption costing :

On the other hand the absorption costing system is said to be yet another method which

allows the business with yet another method that utilizes the consideration of both the fixed costs

and variable costs that can be used as the production cost. In such a method of costing the

business considers it to be an effective way in which the purpose of the business can be

considered to be the essential factor for the reporting and inclusion of both the financial reporting

and tax reporting. It is that technique which is assumed to be the essential for both the fixed costs

and variable costs of the production. It can also be said as the technique which assumes both the

fixed costs and variable cost as the total production costs. In this method the overhead in the case

of absorption costing and also being able to be effective in a very uncertainty of the production

and distribution of the selling & administration of the organization (Pavlatos and Kostakis,

Marginal costing :

This method of marginal costing is known as the method in which the cos are considered

to be the production cost and fixed cost that allow the business in the analysation of the cost for

the given period. It is the technique which allows the business in assuming the variable costs and

production cost to be effective in the preparation of the income statement of the organization.

This method of preparation of the income statement is considered to be very essential for the

production cost and also the fixed cost of the organization that can allow the business in

assuming the cost for the given period. In this technique of management of the cost of the

organization. Both the fixed costs and the variable costs are considered that can allow the

business in the calculation of the income of the organization (Hertati and Safkaur, 2019). This

method also has the utilization of the P/V ratio which is the profit value ratio which is used by

the management to understand the efficiency of the organization. It helps in the determination of

the cost of the next unit as it allows the business in the management of its overheads. The

management costing method of this business is said to be very effective as it provides more

emphasis on the change on the opening stocks and the closing stocks which affects the per unit

cost of production. In this method the organization is able to understand the total contribution to

the per unit production. Contribution is shown as the main emphasis to the total production cost

in this method. The preparation of income statement which uses marginal costing utilizes the

total contribution of the organization.

Absorption costing :

On the other hand the absorption costing system is said to be yet another method which

allows the business with yet another method that utilizes the consideration of both the fixed costs

and variable costs that can be used as the production cost. In such a method of costing the

business considers it to be an effective way in which the purpose of the business can be

considered to be the essential factor for the reporting and inclusion of both the financial reporting

and tax reporting. It is that technique which is assumed to be the essential for both the fixed costs

and variable costs of the production. It can also be said as the technique which assumes both the

fixed costs and variable cost as the total production costs. In this method the overhead in the case

of absorption costing and also being able to be effective in a very uncertainty of the production

and distribution of the selling & administration of the organization (Pavlatos and Kostakis,

2018). This also helps the business in the analysation of the fixed costs of the product which also

allows the business in the getting the profit which is very essential for the generation of the

reduction of cost. It can be said that the cost of each unit of the product can be understood with

the help of this analysis of the organization. This method also help in the management of the

operations as it allows the business in providing emphasis over each unit which in charge of the

operation of the organization.

TASK 3

Explaining advantages and disadvantages of different types of planning tools used in budgetary

control

It becomes essential for the organization to pay attention on getting different types of

planning tools so that effective road map for carrying forward business practices can be derived.

ABC Ltd as being medium-sized enterprise require using planning tools of budgetary control so

that ability to plan strategically can become possible. Each technique of budgetary control has

few advantages and drawbacks which area as follows:

Cash Budget

It is widely taken into consideration by companies irrespective of their scale of

operations. Cash budget basically provides details regarding in & out flows which helps in

assessing the information regarding liquidity position of company (Cash Budget, 2021). ABC

Ltd can obtain following benefits and drawbacks which are as follows:

Benefits

It helps in assessing details regarding available cash which aids in conducting significant level of

evaluation of current financial status of firm so that appropriate sources for raising funds can be

identified.

Allocating, managing and controlling resource with help of cash budget can be exerted by ABC

Ltd in effective manner.

Identifying potential lacking areas to make significant evaluation of deficits functions of ABC

Ltd can be done to make identify appropriate course of action in order to make improvements.

Drawbacks

Cash budget as planning tool possessing few lacking areas which are essential to

recognize for gaining ability to make significant decision. ABC Ltd should pay attention on

following parts:

allows the business in the getting the profit which is very essential for the generation of the

reduction of cost. It can be said that the cost of each unit of the product can be understood with

the help of this analysis of the organization. This method also help in the management of the

operations as it allows the business in providing emphasis over each unit which in charge of the

operation of the organization.

TASK 3

Explaining advantages and disadvantages of different types of planning tools used in budgetary

control

It becomes essential for the organization to pay attention on getting different types of

planning tools so that effective road map for carrying forward business practices can be derived.

ABC Ltd as being medium-sized enterprise require using planning tools of budgetary control so

that ability to plan strategically can become possible. Each technique of budgetary control has

few advantages and drawbacks which area as follows:

Cash Budget

It is widely taken into consideration by companies irrespective of their scale of

operations. Cash budget basically provides details regarding in & out flows which helps in

assessing the information regarding liquidity position of company (Cash Budget, 2021). ABC

Ltd can obtain following benefits and drawbacks which are as follows:

Benefits

It helps in assessing details regarding available cash which aids in conducting significant level of

evaluation of current financial status of firm so that appropriate sources for raising funds can be

identified.

Allocating, managing and controlling resource with help of cash budget can be exerted by ABC

Ltd in effective manner.

Identifying potential lacking areas to make significant evaluation of deficits functions of ABC

Ltd can be done to make identify appropriate course of action in order to make improvements.

Drawbacks

Cash budget as planning tool possessing few lacking areas which are essential to

recognize for gaining ability to make significant decision. ABC Ltd should pay attention on

following parts:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.