ACC202 Management Accounting: Multinational Transfer Pricing Analysis

VerifiedAdded on 2023/06/11

|9

|1196

|193

Report

AI Summary

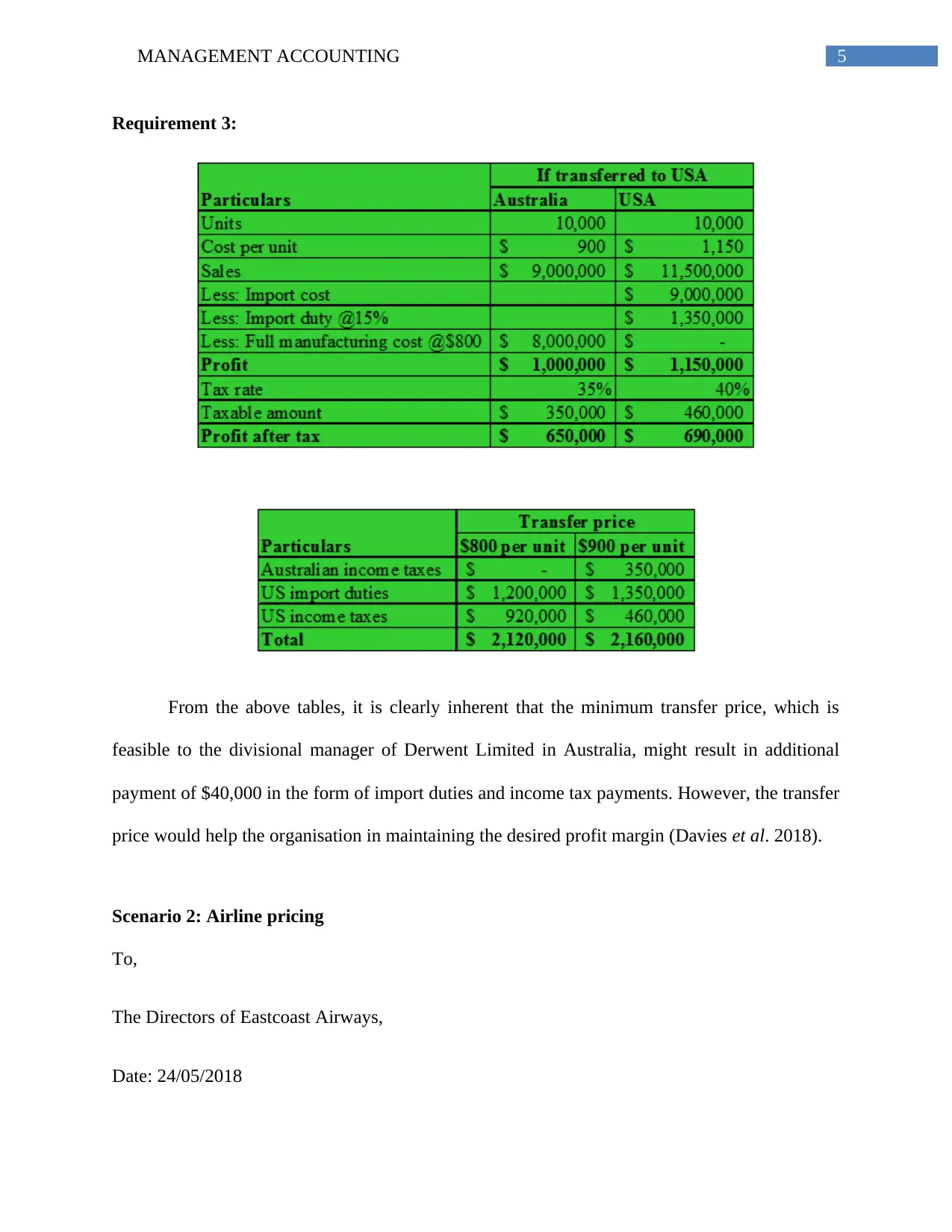

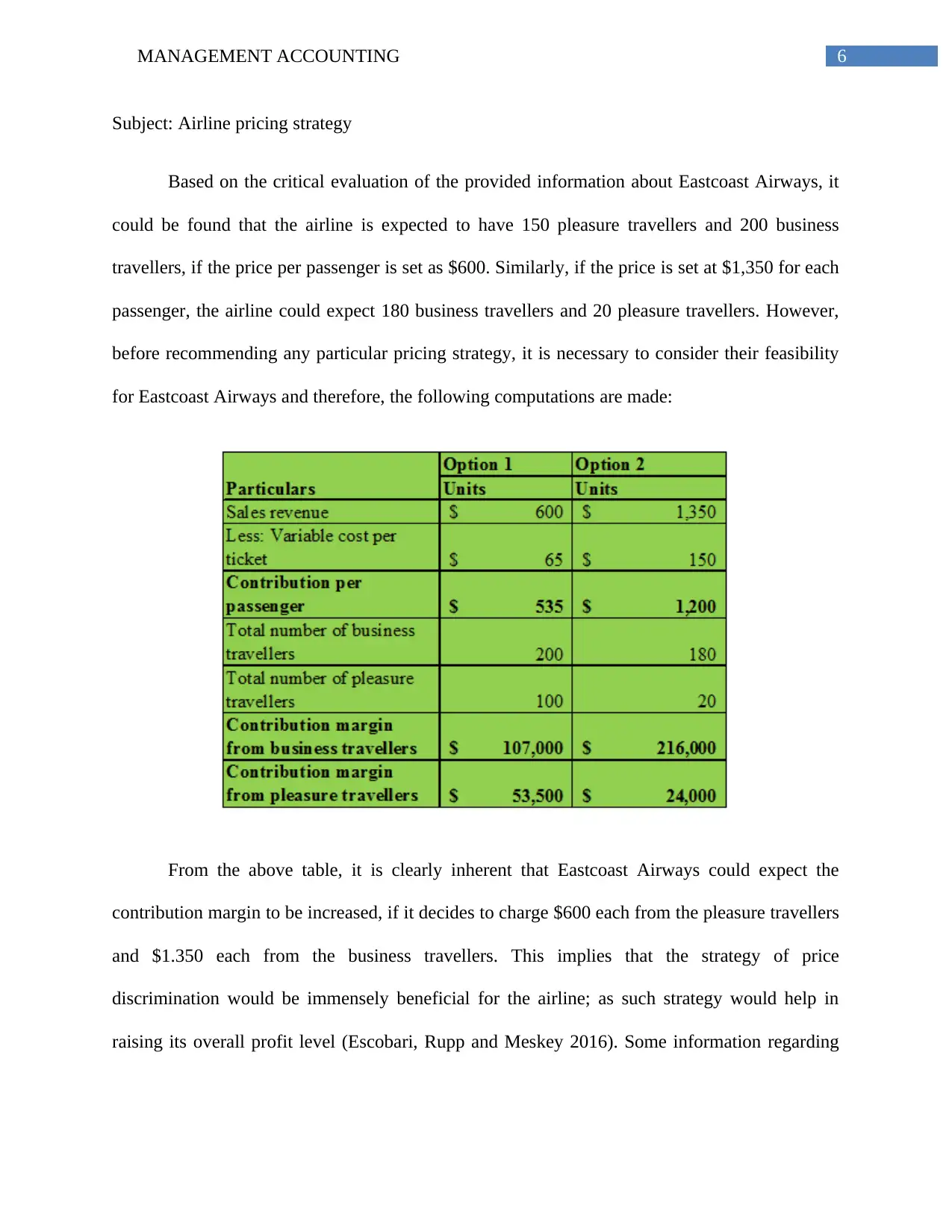

This management accounting report addresses multinational transfer pricing strategies for global tax minimization and goal congruence, along with airline pricing strategies. It analyzes the feasibility of different transfer pricing approaches for Derwent Limited, considering import duties and income tax implications. The report also evaluates airline pricing strategies for Eastcoast Airways, recommending price discrimination between pleasure and business travelers to maximize contribution margin. The analysis excludes certain costs deemed irrelevant to pricing strategy changes, such as lease, fuel, and ground service costs. The study concludes that price discrimination can significantly benefit the airline while remaining legally compliant.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.