Management Accounting: Principles, Techniques, and Integration Report

VerifiedAdded on 2023/06/04

|15

|4483

|332

Report

AI Summary

This report provides a comprehensive overview of management accounting, encompassing its principles, techniques, and practical applications. It begins by outlining the fundamental goals and principles of management accounting, emphasizing its role in decision-making and financial analysis. The report then delves into specific techniques, including absorption costing and marginal costing, with detailed income statements and a reconciliation statement demonstrating the differences between the two methods. Furthermore, the report examines the integration of management accounting within an organization, highlighting the benefits it provides, such as improved inventory management, cost control, and resource allocation. The report also includes a statement of cash flows to provide a comprehensive financial analysis. Through this exploration, the report underscores the importance of management accounting in supporting effective business strategies and sustainable success. The report is available on Desklib, a platform offering AI-powered study tools and past papers.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................2

MAIN BODY..................................................................................................................................2

PART – 1.........................................................................................................................................2

Principles of Management Accounting.......................................................................................2

Role of Management Accounting Systems..................................................................................3

Techniques and Methods.............................................................................................................4

Integration of Management Accounting within the Organisation...............................................7

Benefits of The Function.............................................................................................................7

Conclusion on Application of Management Accounting............................................................8

PART – 2.........................................................................................................................................8

Planning Tools Used in Management Accounting......................................................................8

Comparing organizations based on the way they adapt management accounting systems for the

financial problems they face......................................................................................................10

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

1

INTRODUCTION...........................................................................................................................2

MAIN BODY..................................................................................................................................2

PART – 1.........................................................................................................................................2

Principles of Management Accounting.......................................................................................2

Role of Management Accounting Systems..................................................................................3

Techniques and Methods.............................................................................................................4

Integration of Management Accounting within the Organisation...............................................7

Benefits of The Function.............................................................................................................7

Conclusion on Application of Management Accounting............................................................8

PART – 2.........................................................................................................................................8

Planning Tools Used in Management Accounting......................................................................8

Comparing organizations based on the way they adapt management accounting systems for the

financial problems they face......................................................................................................10

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

1

INTRODUCTION

Process of identifying, analysis, measuring and interpreting the accounting information

which ultimately, allows efficient and effective decision making and advising to the business

regarding strategies and driving the success of the business sustainably. It can also be said that

this practice of management accounting helps the leaders of the business in the management to

be able to be make sound and impactful financial decisions thereby, enhancing its ability of

management of the daily operations. Therefore, the following report contains and explains the

various principles of management accounting along with the analysis of role of such

management accounting and its system involved. The utilization of various methods and

techniques that are prominent in this practice of management accounting i.e., absorption cost

method and marginal costing method and the reconciliation of the difference between the profits

between profits from methods of absorption costing and marginal costing. Then, integration of

this function of management accounting with the organisation will be evaluated along with

explanation of the benefits to the organisation. Lastly, conclusion regarding the effective

implementation of the system of management accounting is explained.

MAIN BODY

PART – 1

Principles of Management Accounting

Maximization of profits and minimization of the losses are the primary goals of

management accounting. It involves presenting the data for prediction of any variation in

financial information for deciding on the primary decision making (Rikhardsson and

Yigitbasioglu, 2018). Therefore, it involves provisioning of the financial data for forming of a

fair advice to an organisation and thus, developing its business. Now, there are various principles

of management accounting which are explained as follows:

Designing & Compiling – It involves designing and compilation of the accounting information,

reports, records, etc. to address the specific request and requirements.

Management by Exception – It involves following the system of budgetary control and

techniques of standard costing for management accounting. Therefore, finding of variations in

actual performance becomes easy by comparing it with pre – determined data.

Control at Source Accounting – It says that cost can be controlled most efficiently at the point

of their incurrence over the aspects like employees, materials, etc.

2

Process of identifying, analysis, measuring and interpreting the accounting information

which ultimately, allows efficient and effective decision making and advising to the business

regarding strategies and driving the success of the business sustainably. It can also be said that

this practice of management accounting helps the leaders of the business in the management to

be able to be make sound and impactful financial decisions thereby, enhancing its ability of

management of the daily operations. Therefore, the following report contains and explains the

various principles of management accounting along with the analysis of role of such

management accounting and its system involved. The utilization of various methods and

techniques that are prominent in this practice of management accounting i.e., absorption cost

method and marginal costing method and the reconciliation of the difference between the profits

between profits from methods of absorption costing and marginal costing. Then, integration of

this function of management accounting with the organisation will be evaluated along with

explanation of the benefits to the organisation. Lastly, conclusion regarding the effective

implementation of the system of management accounting is explained.

MAIN BODY

PART – 1

Principles of Management Accounting

Maximization of profits and minimization of the losses are the primary goals of

management accounting. It involves presenting the data for prediction of any variation in

financial information for deciding on the primary decision making (Rikhardsson and

Yigitbasioglu, 2018). Therefore, it involves provisioning of the financial data for forming of a

fair advice to an organisation and thus, developing its business. Now, there are various principles

of management accounting which are explained as follows:

Designing & Compiling – It involves designing and compilation of the accounting information,

reports, records, etc. to address the specific request and requirements.

Management by Exception – It involves following the system of budgetary control and

techniques of standard costing for management accounting. Therefore, finding of variations in

actual performance becomes easy by comparing it with pre – determined data.

Control at Source Accounting – It says that cost can be controlled most efficiently at the point

of their incurrence over the aspects like employees, materials, etc.

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting for Inflation – It says that rate of inflation needs to be accounted for to calculate the

real performance of the business as time value of money is very essential.

Use of ROI – It shows the performance and efficiency of the business which is essential for

calculating capital employed.

Utility – It explains the utility of the system of management accounting to the business.

Integration – It says that all the data and information needs to be compiled and integrated so that

it can be used effectively.

Absorption of Overhead Costs – It comprises of the indirect material, indirect expenditures and

indirect labour therefore, appropriate method of absorption of overhead costs shall be utilized.

Utilization of Resources – It says that the available limited resources shall be utilized

effectively.

Controllable & Uncontrollable Costs – It says that proper steps shall be taken to control the

controllable costs of any organisation.

Forward Looking Approach – It covers the ability of the standard costing to forecast the future

issues and challenges and thus, overcome them.

Appropriate Means – It says the most effective means of accumulation and presentation of the

data and information shall be selected.

Role of Management Accounting Systems

Since management accounting is based on utilization of both financial as well as non –

financial data therefore, it is different from the financial accounting. Such financial as well as

non – financial data is utilized by the internal stakeholders of the entity whereas, financial

accounting will be involving utilization of financial data by both the internal as well as external

stakeholders (Pelz, 2019). Such management accounting information is presented to the users of

such information in the form of reports like budgetary statements.

In the context of Brakes Group, the key users of the data and information of the

management accounting mainly includes parties like employees, managerial personnel and

investors of the entity (Alabdullah, 2022). Thus, for the planning of this concern and for effective

process of decision making, system of management accounting examines information including

both financial as well as non – financial format. Also, there are numerous systems of

management accounting formulated and implemented in the Brakes Group each of which has

individual different necessities like:

3

real performance of the business as time value of money is very essential.

Use of ROI – It shows the performance and efficiency of the business which is essential for

calculating capital employed.

Utility – It explains the utility of the system of management accounting to the business.

Integration – It says that all the data and information needs to be compiled and integrated so that

it can be used effectively.

Absorption of Overhead Costs – It comprises of the indirect material, indirect expenditures and

indirect labour therefore, appropriate method of absorption of overhead costs shall be utilized.

Utilization of Resources – It says that the available limited resources shall be utilized

effectively.

Controllable & Uncontrollable Costs – It says that proper steps shall be taken to control the

controllable costs of any organisation.

Forward Looking Approach – It covers the ability of the standard costing to forecast the future

issues and challenges and thus, overcome them.

Appropriate Means – It says the most effective means of accumulation and presentation of the

data and information shall be selected.

Role of Management Accounting Systems

Since management accounting is based on utilization of both financial as well as non –

financial data therefore, it is different from the financial accounting. Such financial as well as

non – financial data is utilized by the internal stakeholders of the entity whereas, financial

accounting will be involving utilization of financial data by both the internal as well as external

stakeholders (Pelz, 2019). Such management accounting information is presented to the users of

such information in the form of reports like budgetary statements.

In the context of Brakes Group, the key users of the data and information of the

management accounting mainly includes parties like employees, managerial personnel and

investors of the entity (Alabdullah, 2022). Thus, for the planning of this concern and for effective

process of decision making, system of management accounting examines information including

both financial as well as non – financial format. Also, there are numerous systems of

management accounting formulated and implemented in the Brakes Group each of which has

individual different necessities like:

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

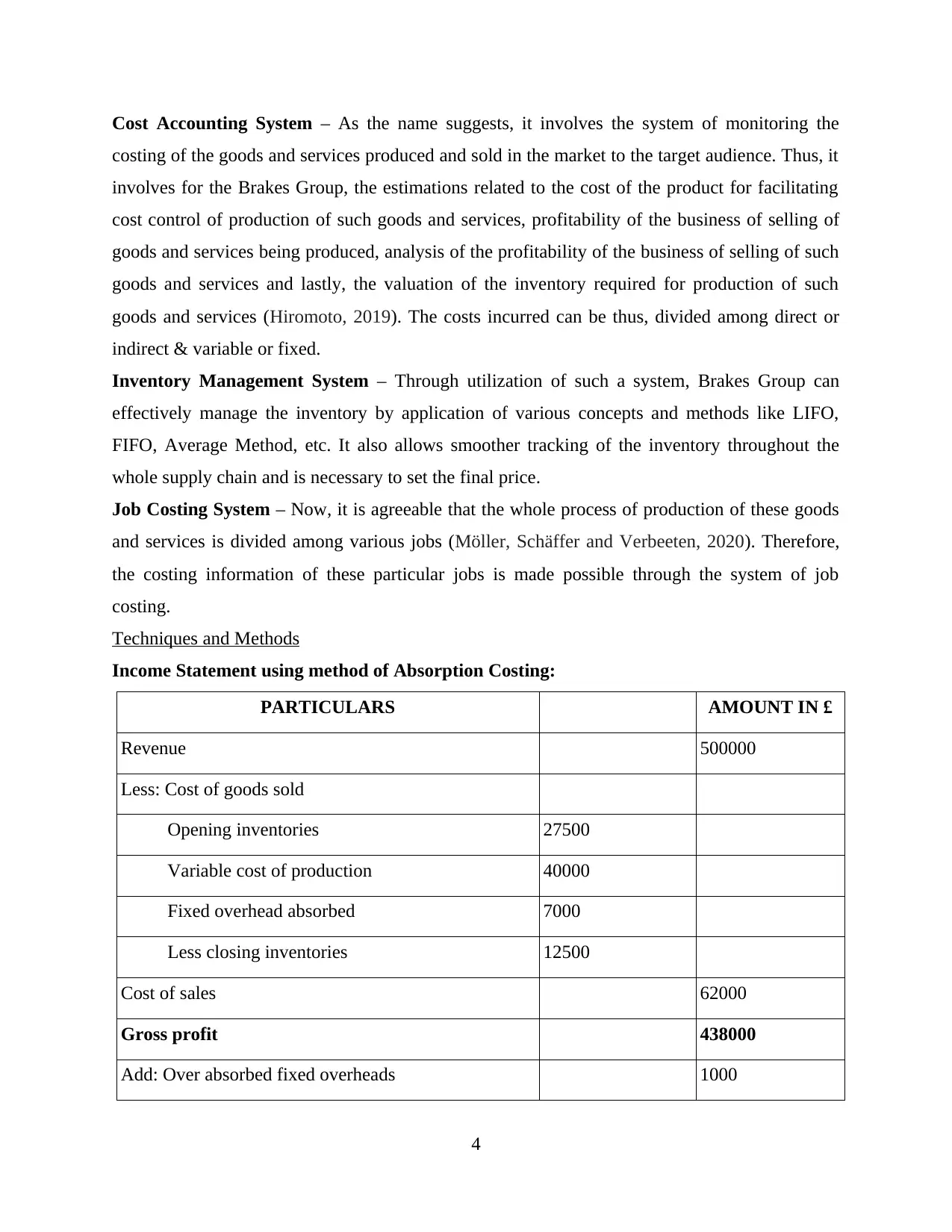

Cost Accounting System – As the name suggests, it involves the system of monitoring the

costing of the goods and services produced and sold in the market to the target audience. Thus, it

involves for the Brakes Group, the estimations related to the cost of the product for facilitating

cost control of production of such goods and services, profitability of the business of selling of

goods and services being produced, analysis of the profitability of the business of selling of such

goods and services and lastly, the valuation of the inventory required for production of such

goods and services (Hiromoto, 2019). The costs incurred can be thus, divided among direct or

indirect & variable or fixed.

Inventory Management System – Through utilization of such a system, Brakes Group can

effectively manage the inventory by application of various concepts and methods like LIFO,

FIFO, Average Method, etc. It also allows smoother tracking of the inventory throughout the

whole supply chain and is necessary to set the final price.

Job Costing System – Now, it is agreeable that the whole process of production of these goods

and services is divided among various jobs (Möller, Schäffer and Verbeeten, 2020). Therefore,

the costing information of these particular jobs is made possible through the system of job

costing.

Techniques and Methods

Income Statement using method of Absorption Costing:

PARTICULARS AMOUNT IN £

Revenue 500000

Less: Cost of goods sold

Opening inventories 27500

Variable cost of production 40000

Fixed overhead absorbed 7000

Less closing inventories 12500

Cost of sales 62000

Gross profit 438000

Add: Over absorbed fixed overheads 1000

4

costing of the goods and services produced and sold in the market to the target audience. Thus, it

involves for the Brakes Group, the estimations related to the cost of the product for facilitating

cost control of production of such goods and services, profitability of the business of selling of

goods and services being produced, analysis of the profitability of the business of selling of such

goods and services and lastly, the valuation of the inventory required for production of such

goods and services (Hiromoto, 2019). The costs incurred can be thus, divided among direct or

indirect & variable or fixed.

Inventory Management System – Through utilization of such a system, Brakes Group can

effectively manage the inventory by application of various concepts and methods like LIFO,

FIFO, Average Method, etc. It also allows smoother tracking of the inventory throughout the

whole supply chain and is necessary to set the final price.

Job Costing System – Now, it is agreeable that the whole process of production of these goods

and services is divided among various jobs (Möller, Schäffer and Verbeeten, 2020). Therefore,

the costing information of these particular jobs is made possible through the system of job

costing.

Techniques and Methods

Income Statement using method of Absorption Costing:

PARTICULARS AMOUNT IN £

Revenue 500000

Less: Cost of goods sold

Opening inventories 27500

Variable cost of production 40000

Fixed overhead absorbed 7000

Less closing inventories 12500

Cost of sales 62000

Gross profit 438000

Add: Over absorbed fixed overheads 1000

4

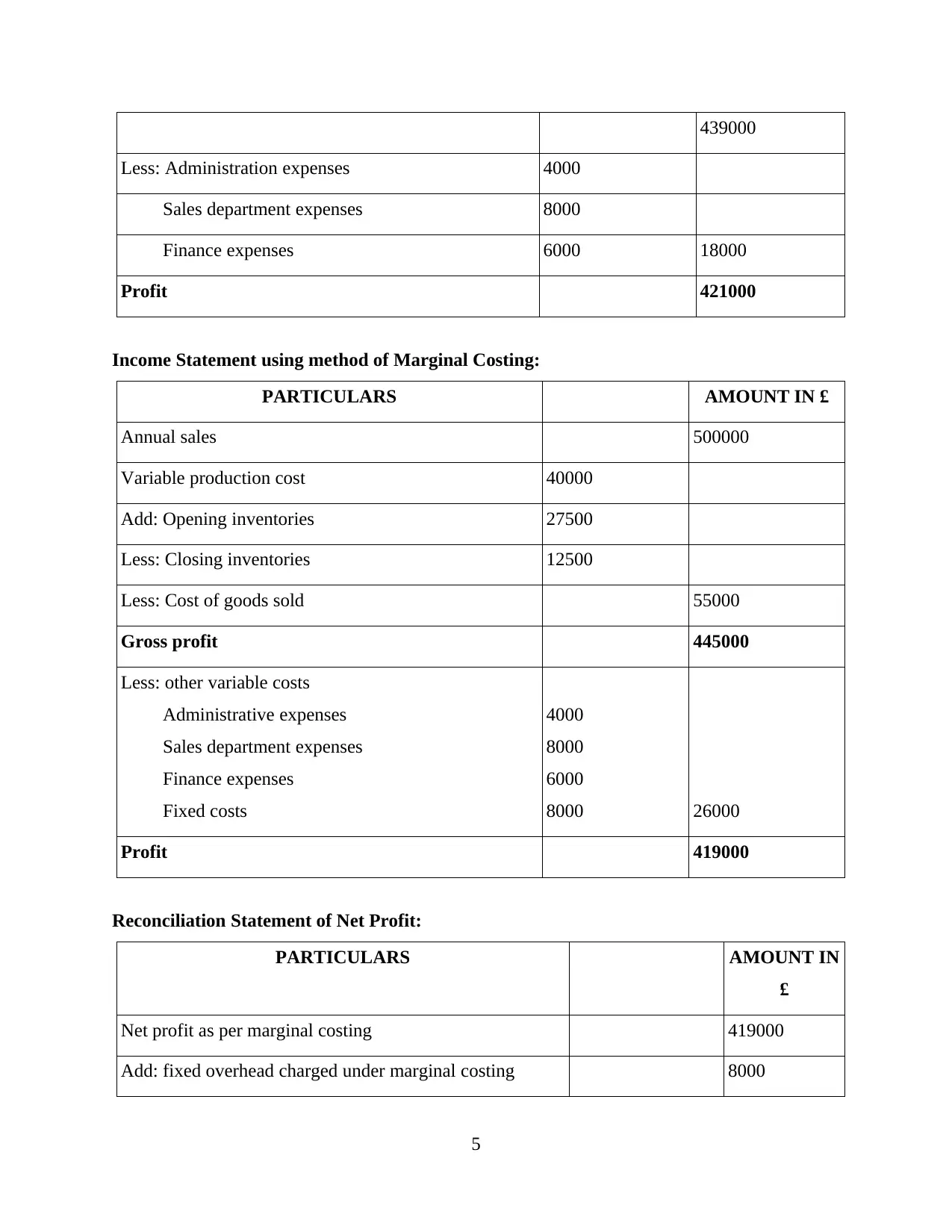

439000

Less: Administration expenses 4000

Sales department expenses 8000

Finance expenses 6000 18000

Profit 421000

Income Statement using method of Marginal Costing:

PARTICULARS AMOUNT IN £

Annual sales 500000

Variable production cost 40000

Add: Opening inventories 27500

Less: Closing inventories 12500

Less: Cost of goods sold 55000

Gross profit 445000

Less: other variable costs

Administrative expenses

Sales department expenses

Finance expenses

Fixed costs

4000

8000

6000

8000 26000

Profit 419000

Reconciliation Statement of Net Profit:

PARTICULARS AMOUNT IN

£

Net profit as per marginal costing 419000

Add: fixed overhead charged under marginal costing 8000

5

Less: Administration expenses 4000

Sales department expenses 8000

Finance expenses 6000 18000

Profit 421000

Income Statement using method of Marginal Costing:

PARTICULARS AMOUNT IN £

Annual sales 500000

Variable production cost 40000

Add: Opening inventories 27500

Less: Closing inventories 12500

Less: Cost of goods sold 55000

Gross profit 445000

Less: other variable costs

Administrative expenses

Sales department expenses

Finance expenses

Fixed costs

4000

8000

6000

8000 26000

Profit 419000

Reconciliation Statement of Net Profit:

PARTICULARS AMOUNT IN

£

Net profit as per marginal costing 419000

Add: fixed overhead charged under marginal costing 8000

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

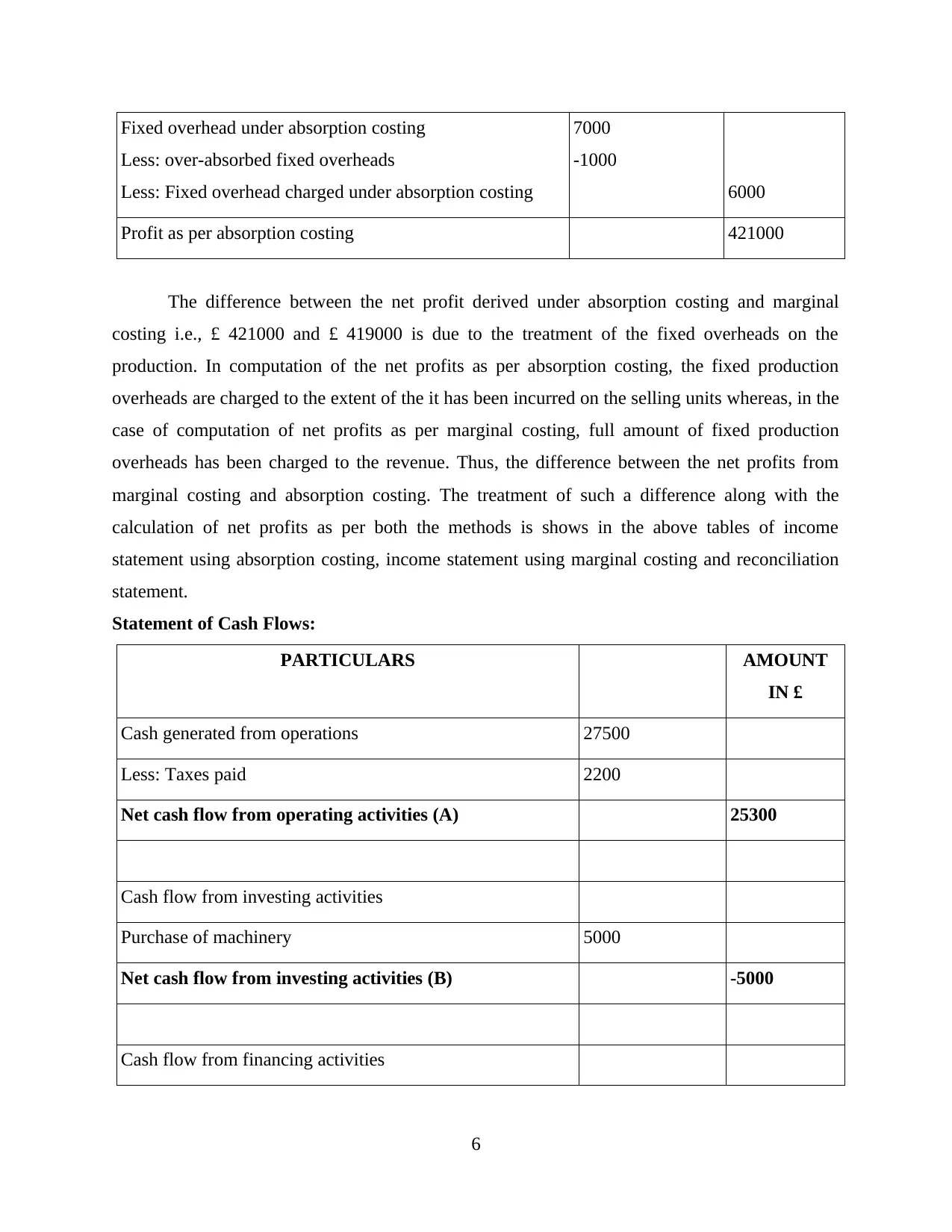

Fixed overhead under absorption costing

Less: over-absorbed fixed overheads

Less: Fixed overhead charged under absorption costing

7000

-1000

6000

Profit as per absorption costing 421000

The difference between the net profit derived under absorption costing and marginal

costing i.e., £ 421000 and £ 419000 is due to the treatment of the fixed overheads on the

production. In computation of the net profits as per absorption costing, the fixed production

overheads are charged to the extent of the it has been incurred on the selling units whereas, in the

case of computation of net profits as per marginal costing, full amount of fixed production

overheads has been charged to the revenue. Thus, the difference between the net profits from

marginal costing and absorption costing. The treatment of such a difference along with the

calculation of net profits as per both the methods is shows in the above tables of income

statement using absorption costing, income statement using marginal costing and reconciliation

statement.

Statement of Cash Flows:

PARTICULARS AMOUNT

IN £

Cash generated from operations 27500

Less: Taxes paid 2200

Net cash flow from operating activities (A) 25300

Cash flow from investing activities

Purchase of machinery 5000

Net cash flow from investing activities (B) -5000

Cash flow from financing activities

6

Less: over-absorbed fixed overheads

Less: Fixed overhead charged under absorption costing

7000

-1000

6000

Profit as per absorption costing 421000

The difference between the net profit derived under absorption costing and marginal

costing i.e., £ 421000 and £ 419000 is due to the treatment of the fixed overheads on the

production. In computation of the net profits as per absorption costing, the fixed production

overheads are charged to the extent of the it has been incurred on the selling units whereas, in the

case of computation of net profits as per marginal costing, full amount of fixed production

overheads has been charged to the revenue. Thus, the difference between the net profits from

marginal costing and absorption costing. The treatment of such a difference along with the

calculation of net profits as per both the methods is shows in the above tables of income

statement using absorption costing, income statement using marginal costing and reconciliation

statement.

Statement of Cash Flows:

PARTICULARS AMOUNT

IN £

Cash generated from operations 27500

Less: Taxes paid 2200

Net cash flow from operating activities (A) 25300

Cash flow from investing activities

Purchase of machinery 5000

Net cash flow from investing activities (B) -5000

Cash flow from financing activities

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

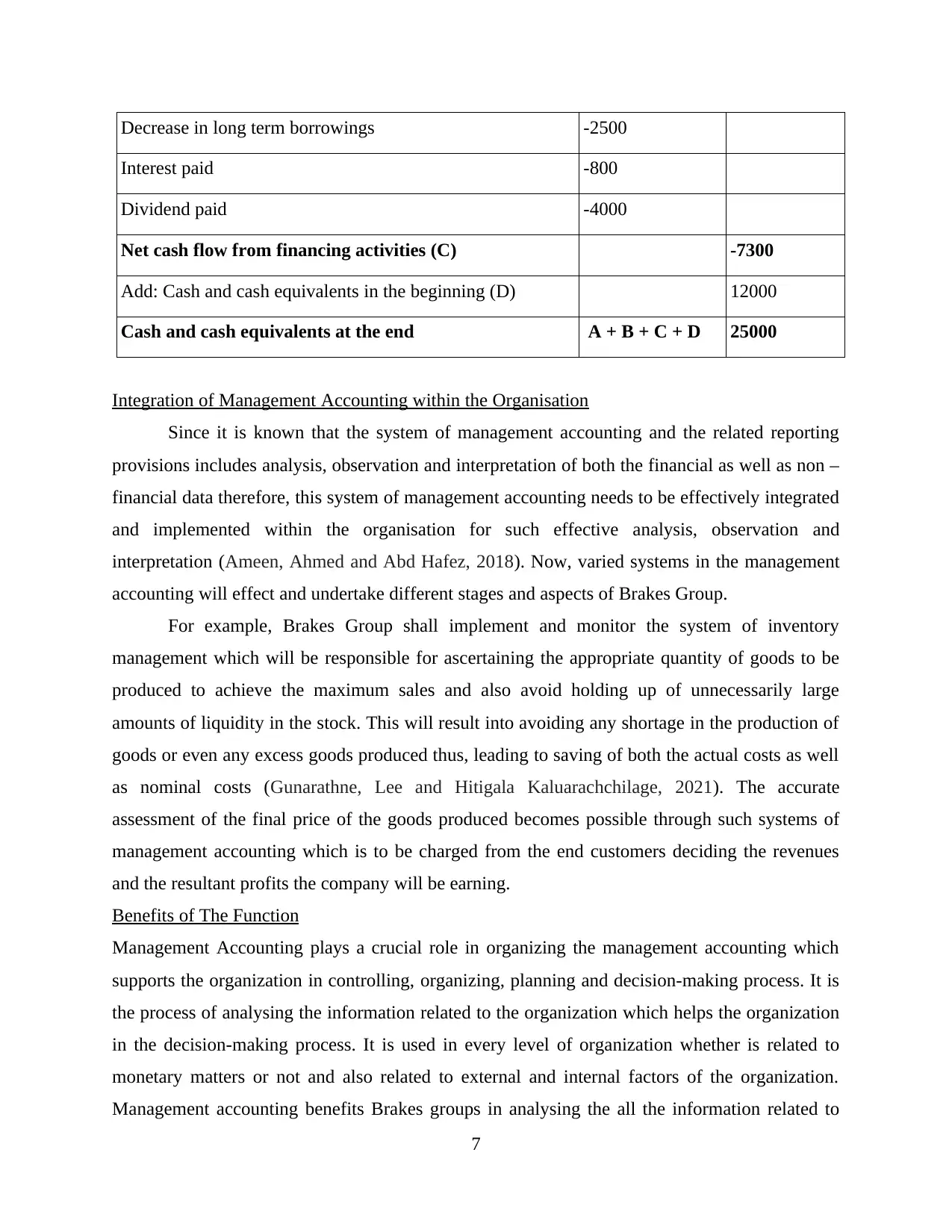

Decrease in long term borrowings -2500

Interest paid -800

Dividend paid -4000

Net cash flow from financing activities (C) -7300

Add: Cash and cash equivalents in the beginning (D) 12000

Cash and cash equivalents at the end A + B + C + D 25000

Integration of Management Accounting within the Organisation

Since it is known that the system of management accounting and the related reporting

provisions includes analysis, observation and interpretation of both the financial as well as non –

financial data therefore, this system of management accounting needs to be effectively integrated

and implemented within the organisation for such effective analysis, observation and

interpretation (Ameen, Ahmed and Abd Hafez, 2018). Now, varied systems in the management

accounting will effect and undertake different stages and aspects of Brakes Group.

For example, Brakes Group shall implement and monitor the system of inventory

management which will be responsible for ascertaining the appropriate quantity of goods to be

produced to achieve the maximum sales and also avoid holding up of unnecessarily large

amounts of liquidity in the stock. This will result into avoiding any shortage in the production of

goods or even any excess goods produced thus, leading to saving of both the actual costs as well

as nominal costs (Gunarathne, Lee and Hitigala Kaluarachchilage, 2021). The accurate

assessment of the final price of the goods produced becomes possible through such systems of

management accounting which is to be charged from the end customers deciding the revenues

and the resultant profits the company will be earning.

Benefits of The Function

Management Accounting plays a crucial role in organizing the management accounting which

supports the organization in controlling, organizing, planning and decision-making process. It is

the process of analysing the information related to the organization which helps the organization

in the decision-making process. It is used in every level of organization whether is related to

monetary matters or not and also related to external and internal factors of the organization.

Management accounting benefits Brakes groups in analysing the all the information related to

7

Interest paid -800

Dividend paid -4000

Net cash flow from financing activities (C) -7300

Add: Cash and cash equivalents in the beginning (D) 12000

Cash and cash equivalents at the end A + B + C + D 25000

Integration of Management Accounting within the Organisation

Since it is known that the system of management accounting and the related reporting

provisions includes analysis, observation and interpretation of both the financial as well as non –

financial data therefore, this system of management accounting needs to be effectively integrated

and implemented within the organisation for such effective analysis, observation and

interpretation (Ameen, Ahmed and Abd Hafez, 2018). Now, varied systems in the management

accounting will effect and undertake different stages and aspects of Brakes Group.

For example, Brakes Group shall implement and monitor the system of inventory

management which will be responsible for ascertaining the appropriate quantity of goods to be

produced to achieve the maximum sales and also avoid holding up of unnecessarily large

amounts of liquidity in the stock. This will result into avoiding any shortage in the production of

goods or even any excess goods produced thus, leading to saving of both the actual costs as well

as nominal costs (Gunarathne, Lee and Hitigala Kaluarachchilage, 2021). The accurate

assessment of the final price of the goods produced becomes possible through such systems of

management accounting which is to be charged from the end customers deciding the revenues

and the resultant profits the company will be earning.

Benefits of The Function

Management Accounting plays a crucial role in organizing the management accounting which

supports the organization in controlling, organizing, planning and decision-making process. It is

the process of analysing the information related to the organization which helps the organization

in the decision-making process. It is used in every level of organization whether is related to

monetary matters or not and also related to external and internal factors of the organization.

Management accounting benefits Brakes groups in analysing the all the information related to

7

the organization which helps in decision-making process of the organization. It impacts the

decision-making process of the company which leads to achieving the success of the company. It

analyses the prices and targets of company by keeping a reasonable profit margin to it. It also

predicts and prepares the budgets of the organization by estimating the expenses and income of

the company. Management accounting provides tools and techniques to company which

increases the efficiency and reliability of the functions which are performed in the organization

(Hiromoto, 2019). MA system plays important role in coordination by providing variety of tools

such as financial analysis and reporting and interpretation.

Brakes group uses the management accounting system in many aspects such as it helps in

inventory control system by controlling and managing stock which results in saving cost of the

products and in achieving the higher efficiency by implementing the system properly. It also

helps in cost accounting by analysing the accurate cost of the business, which allows it to create

effective budgets to ensure that it is cost effective and leads to higher profit margins. At last, job

costing system helps in utilization of resources by performing a profitable operation and by

increasing the overall productivity of the business. It also helps Brakes group in modifying the

data which helps in effective business management.

Conclusion on Application of Management Accounting

The functions performed in management accounting helps the Brakes groups in many

ways. Management accounting helps the organization to lowers the risk of losses by analysing

the market trends properly and by setting the cost accordingly. Accountant identifies the

potential areas which includes analysing of cash flows, management of inventory and job

costing. It helps the organization in managing the activities of the organization. Management

accounting helps the company in both finance and non finance matter which helps the company

in taking better decisions. It helps the organization by recording the transactions properly which

increases the ability to take decisions (Oyewo, 2021). Further, management accounting will

helps the company in managing the activities and performance of organization, which increases

the overall efficiency of the company. At last, it helps in creating budget friendly plans and

creates habits to work according to the budgets. Creating budget friendly plans helps in

identifying the future profits and expenses. It is known as the bases for the success of business.

8

decision-making process of the company which leads to achieving the success of the company. It

analyses the prices and targets of company by keeping a reasonable profit margin to it. It also

predicts and prepares the budgets of the organization by estimating the expenses and income of

the company. Management accounting provides tools and techniques to company which

increases the efficiency and reliability of the functions which are performed in the organization

(Hiromoto, 2019). MA system plays important role in coordination by providing variety of tools

such as financial analysis and reporting and interpretation.

Brakes group uses the management accounting system in many aspects such as it helps in

inventory control system by controlling and managing stock which results in saving cost of the

products and in achieving the higher efficiency by implementing the system properly. It also

helps in cost accounting by analysing the accurate cost of the business, which allows it to create

effective budgets to ensure that it is cost effective and leads to higher profit margins. At last, job

costing system helps in utilization of resources by performing a profitable operation and by

increasing the overall productivity of the business. It also helps Brakes group in modifying the

data which helps in effective business management.

Conclusion on Application of Management Accounting

The functions performed in management accounting helps the Brakes groups in many

ways. Management accounting helps the organization to lowers the risk of losses by analysing

the market trends properly and by setting the cost accordingly. Accountant identifies the

potential areas which includes analysing of cash flows, management of inventory and job

costing. It helps the organization in managing the activities of the organization. Management

accounting helps the company in both finance and non finance matter which helps the company

in taking better decisions. It helps the organization by recording the transactions properly which

increases the ability to take decisions (Oyewo, 2021). Further, management accounting will

helps the company in managing the activities and performance of organization, which increases

the overall efficiency of the company. At last, it helps in creating budget friendly plans and

creates habits to work according to the budgets. Creating budget friendly plans helps in

identifying the future profits and expenses. It is known as the bases for the success of business.

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

PART – 2

Planning Tools Used in Management Accounting

Cash budget

Cash budget is generally an estimation which deals with cash flow of the organization in

a certain time limit. Cash flow includes outflow and inflow of cash and proper estimation is takes

place in regular interval to time which may be weekly, monthly, annually or quarterly.

Organization used this tools for determine the sufficient amount of cash for continuation of

operation within given time limit.

Advantages Disadvantages

The main advantage from cash budget

is to identify shortage of cash in any

area of business within short or

particular period.

By this, organization easily find more

cash (surplus) and less cash (deficit)

region, and according to that company

focus on the even distribution of cash.

By this tools, danger of robbery or theft

is created by which company faces a

lose.

This basically eliminated reward.

The spending power is not in freedom

which means that there is limit of

expenditure.

Zero Based Budgeting

Zero Based Budgeting is basically a technique which is used as to justify all expenses for

a year and beginning from zero in the new year versus settling down all previous budget and

adjust them as needed (Hughes, 2020.). It majorly helps the organization to reduce cost &

promote responsibility. The budget generally starts from zero or scratch to zero in each year.

Advantages Disadvantages

It must be justified by managers for all

operational expenses that where money

is spent more or less in every

budgeting time period.

The main advantage of this type of

budgeting tools is to identifying actual

Zero Based Budgeting mainly lack in

time management as it consumes more

time in saturating the budget or cash in

an organization.

This also lack in the sudden expenses

of the company that means this budget

9

Planning Tools Used in Management Accounting

Cash budget

Cash budget is generally an estimation which deals with cash flow of the organization in

a certain time limit. Cash flow includes outflow and inflow of cash and proper estimation is takes

place in regular interval to time which may be weekly, monthly, annually or quarterly.

Organization used this tools for determine the sufficient amount of cash for continuation of

operation within given time limit.

Advantages Disadvantages

The main advantage from cash budget

is to identify shortage of cash in any

area of business within short or

particular period.

By this, organization easily find more

cash (surplus) and less cash (deficit)

region, and according to that company

focus on the even distribution of cash.

By this tools, danger of robbery or theft

is created by which company faces a

lose.

This basically eliminated reward.

The spending power is not in freedom

which means that there is limit of

expenditure.

Zero Based Budgeting

Zero Based Budgeting is basically a technique which is used as to justify all expenses for

a year and beginning from zero in the new year versus settling down all previous budget and

adjust them as needed (Hughes, 2020.). It majorly helps the organization to reduce cost &

promote responsibility. The budget generally starts from zero or scratch to zero in each year.

Advantages Disadvantages

It must be justified by managers for all

operational expenses that where money

is spent more or less in every

budgeting time period.

The main advantage of this type of

budgeting tools is to identifying actual

Zero Based Budgeting mainly lack in

time management as it consumes more

time in saturating the budget or cash in

an organization.

This also lack in the sudden expenses

of the company that means this budget

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

profit margin of the company.

tool only for routine expenditure.

Activity Based Budgeting

Activity based budgeting is a technique which analyse, research and records of all

activities that particularly related to cost for the company (ACA, ACTI and KWANGA, 2021.).

It basically increases the revenue rate by cutting cost and increasing in the selling rate of product.

The main purpose of this type of budgeting tool is to earn profit margin.

Advantages Disadvantages

This creates a competition in the

businesses

budget is managed in an appropriate

manner by which a company earns the

profit margin from the market.

This easily identify drivers of cost in

frequent manner.

Management easily evaluate

differences between business.

It is costly among all other tools and

require more time for process.

It requires more resource and that is not

possible for maintaining the cost.

As this require all technical details

which may create a mismatch and that

usually consumed more time

Comparing organizations based on the way they adapt management accounting systems for the

financial problems they face

Benchmarking

Benchmarking is process by which the organization effectively assess its own products &

services from that of the organizations operating in competition to such organization. Along with

products and services the process that involves in manufacturing of that products and services are

also measured for the assessment of the operational efficacy of the organization in the similar

way (Tasdemir, Gazo and Quesada, 2020). The organization from which the performance is

compared is the one which is leader in the industry in terms of efficiency and quality products

and services providing. The advantages of benchmarking are that it gives important details

regarding the improvements that can be made into the processes of the company that is again

linked to the better performance of products. The areas where enhancements can be made are

10

tool only for routine expenditure.

Activity Based Budgeting

Activity based budgeting is a technique which analyse, research and records of all

activities that particularly related to cost for the company (ACA, ACTI and KWANGA, 2021.).

It basically increases the revenue rate by cutting cost and increasing in the selling rate of product.

The main purpose of this type of budgeting tool is to earn profit margin.

Advantages Disadvantages

This creates a competition in the

businesses

budget is managed in an appropriate

manner by which a company earns the

profit margin from the market.

This easily identify drivers of cost in

frequent manner.

Management easily evaluate

differences between business.

It is costly among all other tools and

require more time for process.

It requires more resource and that is not

possible for maintaining the cost.

As this require all technical details

which may create a mismatch and that

usually consumed more time

Comparing organizations based on the way they adapt management accounting systems for the

financial problems they face

Benchmarking

Benchmarking is process by which the organization effectively assess its own products &

services from that of the organizations operating in competition to such organization. Along with

products and services the process that involves in manufacturing of that products and services are

also measured for the assessment of the operational efficacy of the organization in the similar

way (Tasdemir, Gazo and Quesada, 2020). The organization from which the performance is

compared is the one which is leader in the industry in terms of efficiency and quality products

and services providing. The advantages of benchmarking are that it gives important details

regarding the improvements that can be made into the processes of the company that is again

linked to the better performance of products. The areas where enhancements can be made are

10

highlighted with the help of benchmarking. The limitations of using benchmarking is that it just

highlights the areas of improvement but does not contribute in ultimate problem solving and also

the comparisons are that easy to find out. For instance, 2 Sisters Food Group use benchmarking

to compare its progress.

Key Performance Indicators

These are popularly known as KPIs that are used by business organizations to evaluate

their employees individually or in groups or teams. The objectives of a company are given

quantifiable terms for their easy measurement. Employees get the clarity of work that they are

supposed to perform in order to attain the roles that organizations expect from them. Some of the

advantages that the company gets are that it has the indicators that can be used for evaluation for

reflecting the performances of the employees collectively as well as combined. Accurate targets

are set by the company with the help of key performance indicators. These stimulates the process

of evaluation and areas with scope of improvement (Fatile and et.al., 2019). The major limitation

is that in case of the activities of the company deviates from what is required to arrive at the

targeted results then its performance is adversely affected.

Variance Analysis

Variance Analysis is a term that is more involving of mathematical computations.

The company using this type of management tool with the aim of resolving its financial

problems have to first set the targets of each element that is considered to be standard. The

elements concerned are factors of production mainly such as labour, equipment, machinery,

material, etc. Standards for the labour rate per hour, machinery cost per hour, material rate per

unit, material consumed per unit, labour hour used per unit, etc. are predetermined. After the

completion of activity, the actual consumption is known which is then compared with these

predetermined standards to calculate the deviation between both the values. For instance, this

technique is used by Bakkavor for evaluation of its performance. The calculated results are either

favourable for the organization or unfavourable. The advantage to the company by using this is

that the managerial attention is drawn towards the areas in need. Drawbacks are delays in the

reporting process and difficulties in assignment of responsibilities over a particular activity or

person accountable for the negative variances.

Financial Governance

11

highlights the areas of improvement but does not contribute in ultimate problem solving and also

the comparisons are that easy to find out. For instance, 2 Sisters Food Group use benchmarking

to compare its progress.

Key Performance Indicators

These are popularly known as KPIs that are used by business organizations to evaluate

their employees individually or in groups or teams. The objectives of a company are given

quantifiable terms for their easy measurement. Employees get the clarity of work that they are

supposed to perform in order to attain the roles that organizations expect from them. Some of the

advantages that the company gets are that it has the indicators that can be used for evaluation for

reflecting the performances of the employees collectively as well as combined. Accurate targets

are set by the company with the help of key performance indicators. These stimulates the process

of evaluation and areas with scope of improvement (Fatile and et.al., 2019). The major limitation

is that in case of the activities of the company deviates from what is required to arrive at the

targeted results then its performance is adversely affected.

Variance Analysis

Variance Analysis is a term that is more involving of mathematical computations.

The company using this type of management tool with the aim of resolving its financial

problems have to first set the targets of each element that is considered to be standard. The

elements concerned are factors of production mainly such as labour, equipment, machinery,

material, etc. Standards for the labour rate per hour, machinery cost per hour, material rate per

unit, material consumed per unit, labour hour used per unit, etc. are predetermined. After the

completion of activity, the actual consumption is known which is then compared with these

predetermined standards to calculate the deviation between both the values. For instance, this

technique is used by Bakkavor for evaluation of its performance. The calculated results are either

favourable for the organization or unfavourable. The advantage to the company by using this is

that the managerial attention is drawn towards the areas in need. Drawbacks are delays in the

reporting process and difficulties in assignment of responsibilities over a particular activity or

person accountable for the negative variances.

Financial Governance

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.