Comprehensive Management Accounting Report: Jeffrey and Son's Analysis

VerifiedAdded on 2020/01/28

|18

|5047

|35

Report

AI Summary

This report provides a detailed analysis of the management accounting practices of Jeffrey and Son's, a manufacturing company producing exquisite branded products. The report begins with a classification of different types of costs, including fixed, variable, and semi-variable costs, as well as costs based on function and nature. It then calculates unit costs and total job costs for a specific job (Job 444) and determines the cost of the Exquisite product. The report also covers the allocation and apportionment of overhead costs to production departments, calculating overhead absorption rates and analyzing cost data using various techniques. Furthermore, the report includes a cost report for September, analyzing material, labor, and overhead costs, and identifying variances. Finally, the report suggests performance indicators for potential improvements within the company, such as workforce motivation and training.

Management accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Management accounting is process of preparing the report that provide correct, accurate

and timely data related to finance and statistics (Elsevier Jones, 2008) These reports are prepared

by the managers in order to make short term and day to day decisions. In other words it could be

said that management accounting is the provision of all the financial data that is used by the

company fir its development and growth.

The following report is prepared in order to analyze the financial position of Jeffrey and

Son's. Jeffrey and Son's is a manufacture company that produces many popular branded products

known as exquisite. The following report is going to depict about the various cost that is incurred

by the company at the time of undertaking various operations. In addition to this cost of exquisite

is mentioned. In this report unit cost and job cost that is incurred by the company are also

interpreted.

In the following report purpose and nature of the budgetary process is also discussed. In

addition to this method of budgeting that can be used by the Jeffrey and Son's are also

mentioned. Thus, in order to find out the flow of cash of Jeffrey and Son's cash budget is

prepared. At last variance of the Jeffrey and Son's is also interpreted.

Task 1

1.1 Classification of different types of cost

On the basis of elements

Features

Fixed cost Fixed cost is the fixed amount of expenses that are required to be paid by the

company. The amount of fixed cost does not change with change in time. For

example: - rent of a building, factory and so on.

Semi-variable

cost

Semi variable cost is the mixture of fixed cost and variable cost. In case of

semi variable cost remain fixed up to a predetermined limit and when limit is

crossed the cost became the variable cost (Hooks and et. al. 2012). For

example: - electricity bills, telephone bills and so on.

1

Management accounting is process of preparing the report that provide correct, accurate

and timely data related to finance and statistics (Elsevier Jones, 2008) These reports are prepared

by the managers in order to make short term and day to day decisions. In other words it could be

said that management accounting is the provision of all the financial data that is used by the

company fir its development and growth.

The following report is prepared in order to analyze the financial position of Jeffrey and

Son's. Jeffrey and Son's is a manufacture company that produces many popular branded products

known as exquisite. The following report is going to depict about the various cost that is incurred

by the company at the time of undertaking various operations. In addition to this cost of exquisite

is mentioned. In this report unit cost and job cost that is incurred by the company are also

interpreted.

In the following report purpose and nature of the budgetary process is also discussed. In

addition to this method of budgeting that can be used by the Jeffrey and Son's are also

mentioned. Thus, in order to find out the flow of cash of Jeffrey and Son's cash budget is

prepared. At last variance of the Jeffrey and Son's is also interpreted.

Task 1

1.1 Classification of different types of cost

On the basis of elements

Features

Fixed cost Fixed cost is the fixed amount of expenses that are required to be paid by the

company. The amount of fixed cost does not change with change in time. For

example: - rent of a building, factory and so on.

Semi-variable

cost

Semi variable cost is the mixture of fixed cost and variable cost. In case of

semi variable cost remain fixed up to a predetermined limit and when limit is

crossed the cost became the variable cost (Hooks and et. al. 2012). For

example: - electricity bills, telephone bills and so on.

1

Variable cost Variable cost is the cost which keeps on changing. This cost changes with the

change in the level of production. For example: - cost of goods produced.

On the basis of function

Features

Production cost Production cost included all the cost that is incurred by the company during

the manufacturing and production of the product (Joshi, Al-Mudhaki and

Bremser, 2003).

Commercial cost Commercial cost is the cost which is incurred by the company at the time of

administration and selling & distribution of the product produced by them.

On the basis of nature

Features

Material Material cost is the cost that is incurred by the company at the time of

converting the raw material into the finished goods.

Labour Labour cost is the cost which is incurred by the company at the time of

paying salary and wages to the employees. Labour cost can be said as the

cost affiliated to the human resource (Lucey, 2002).

Overhead Overhead cost is the cost that is beard by the company at the time of

undertaking its various functions and operations into consideration.

On the basis of Behaviour

Features

Controllable cost Controllable cost is the cost that can be changed by the company. It is the

cost which can be increased or decreased by the company when they

2

change in the level of production. For example: - cost of goods produced.

On the basis of function

Features

Production cost Production cost included all the cost that is incurred by the company during

the manufacturing and production of the product (Joshi, Al-Mudhaki and

Bremser, 2003).

Commercial cost Commercial cost is the cost which is incurred by the company at the time of

administration and selling & distribution of the product produced by them.

On the basis of nature

Features

Material Material cost is the cost that is incurred by the company at the time of

converting the raw material into the finished goods.

Labour Labour cost is the cost which is incurred by the company at the time of

paying salary and wages to the employees. Labour cost can be said as the

cost affiliated to the human resource (Lucey, 2002).

Overhead Overhead cost is the cost that is beard by the company at the time of

undertaking its various functions and operations into consideration.

On the basis of Behaviour

Features

Controllable cost Controllable cost is the cost that can be changed by the company. It is the

cost which can be increased or decreased by the company when they

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

want. Controllable cost can be both fixed cost and variable cost.

Sunk cost Sunk cost is the cost that is incurred by the company in past and is not

relevant in the future decision making problems (Narayanan and Nanda,

2004).

Replacement cost Replacement cost is the cost that is beard by the company when changing

any method or policy of production or at the time of taking any decisions.

1.2Calculation of unit cost and total job cost for job 444

Cost sheet: It is the document which is prepared by the organization in order to estimate

the cost that is mandatory by every project and department in order to achieve their desired target

(Stoltz, 2007).

Job cost sheet for Job no. 444

Particulars Total cost

Direct material 40000

Direct Labour 54000

Fixed production overhead 24000

variable production overhead 36000

Total cost 154000

Unit cost 770

Working note:

Direct material cost

Material cost = Quantity * price per kg.

= 50kg* £4 per kg *200 units= £400000

Direct labour cost

Labour cost = Total working hours * rate per hour

Labour hours = 30 hours per unit*200 Units = 6000 Hours

Overhead

Fixed overhead = Total fixed production overhead/Total budgeted labour hours*Labour hours

for job

3

Sunk cost Sunk cost is the cost that is incurred by the company in past and is not

relevant in the future decision making problems (Narayanan and Nanda,

2004).

Replacement cost Replacement cost is the cost that is beard by the company when changing

any method or policy of production or at the time of taking any decisions.

1.2Calculation of unit cost and total job cost for job 444

Cost sheet: It is the document which is prepared by the organization in order to estimate

the cost that is mandatory by every project and department in order to achieve their desired target

(Stoltz, 2007).

Job cost sheet for Job no. 444

Particulars Total cost

Direct material 40000

Direct Labour 54000

Fixed production overhead 24000

variable production overhead 36000

Total cost 154000

Unit cost 770

Working note:

Direct material cost

Material cost = Quantity * price per kg.

= 50kg* £4 per kg *200 units= £400000

Direct labour cost

Labour cost = Total working hours * rate per hour

Labour hours = 30 hours per unit*200 Units = 6000 Hours

Overhead

Fixed overhead = Total fixed production overhead/Total budgeted labour hours*Labour hours

for job

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

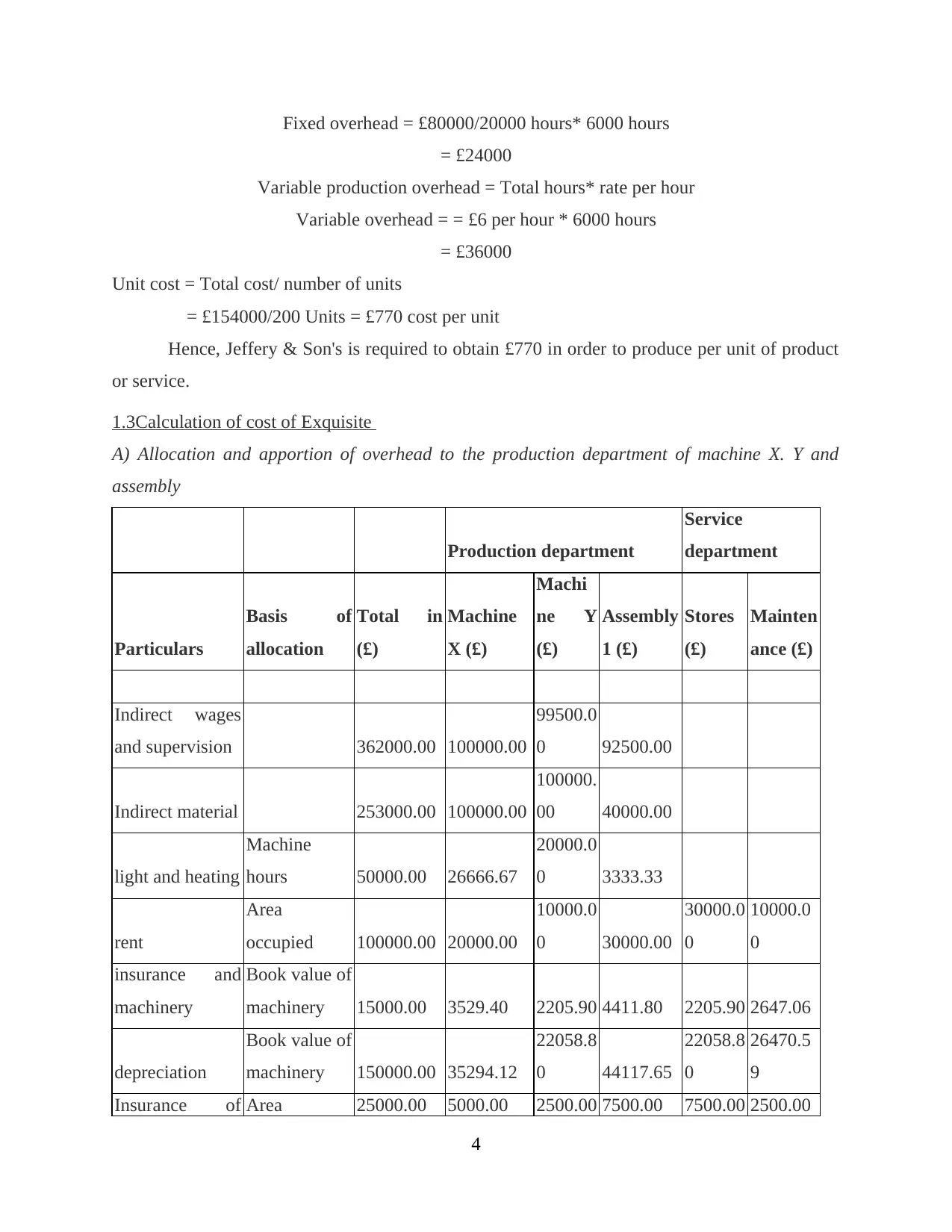

Fixed overhead = £80000/20000 hours* 6000 hours

= £24000

Variable production overhead = Total hours* rate per hour

Variable overhead = = £6 per hour * 6000 hours

= £36000

Unit cost = Total cost/ number of units

= £154000/200 Units = £770 cost per unit

Hence, Jeffery & Son's is required to obtain £770 in order to produce per unit of product

or service.

1.3Calculation of cost of Exquisite

A) Allocation and apportion of overhead to the production department of machine X. Y and

assembly

Production department

Service

department

Particulars

Basis of

allocation

Total in

(£)

Machine

X (£)

Machi

ne Y

(£)

Assembly

1 (£)

Stores

(£)

Mainten

ance (£)

Indirect wages

and supervision 362000.00 100000.00

99500.0

0 92500.00

Indirect material 253000.00 100000.00

100000.

00 40000.00

light and heating

Machine

hours 50000.00 26666.67

20000.0

0 3333.33

rent

Area

occupied 100000.00 20000.00

10000.0

0 30000.00

30000.0

0

10000.0

0

insurance and

machinery

Book value of

machinery 15000.00 3529.40 2205.90 4411.80 2205.90 2647.06

depreciation

Book value of

machinery 150000.00 35294.12

22058.8

0 44117.65

22058.8

0

26470.5

9

Insurance of Area 25000.00 5000.00 2500.00 7500.00 7500.00 2500.00

4

= £24000

Variable production overhead = Total hours* rate per hour

Variable overhead = = £6 per hour * 6000 hours

= £36000

Unit cost = Total cost/ number of units

= £154000/200 Units = £770 cost per unit

Hence, Jeffery & Son's is required to obtain £770 in order to produce per unit of product

or service.

1.3Calculation of cost of Exquisite

A) Allocation and apportion of overhead to the production department of machine X. Y and

assembly

Production department

Service

department

Particulars

Basis of

allocation

Total in

(£)

Machine

X (£)

Machi

ne Y

(£)

Assembly

1 (£)

Stores

(£)

Mainten

ance (£)

Indirect wages

and supervision 362000.00 100000.00

99500.0

0 92500.00

Indirect material 253000.00 100000.00

100000.

00 40000.00

light and heating

Machine

hours 50000.00 26666.67

20000.0

0 3333.33

rent

Area

occupied 100000.00 20000.00

10000.0

0 30000.00

30000.0

0

10000.0

0

insurance and

machinery

Book value of

machinery 15000.00 3529.40 2205.90 4411.80 2205.90 2647.06

depreciation

Book value of

machinery 150000.00 35294.12

22058.8

0 44117.65

22058.8

0

26470.5

9

Insurance of Area 25000.00 5000.00 2500.00 7500.00 7500.00 2500.00

4

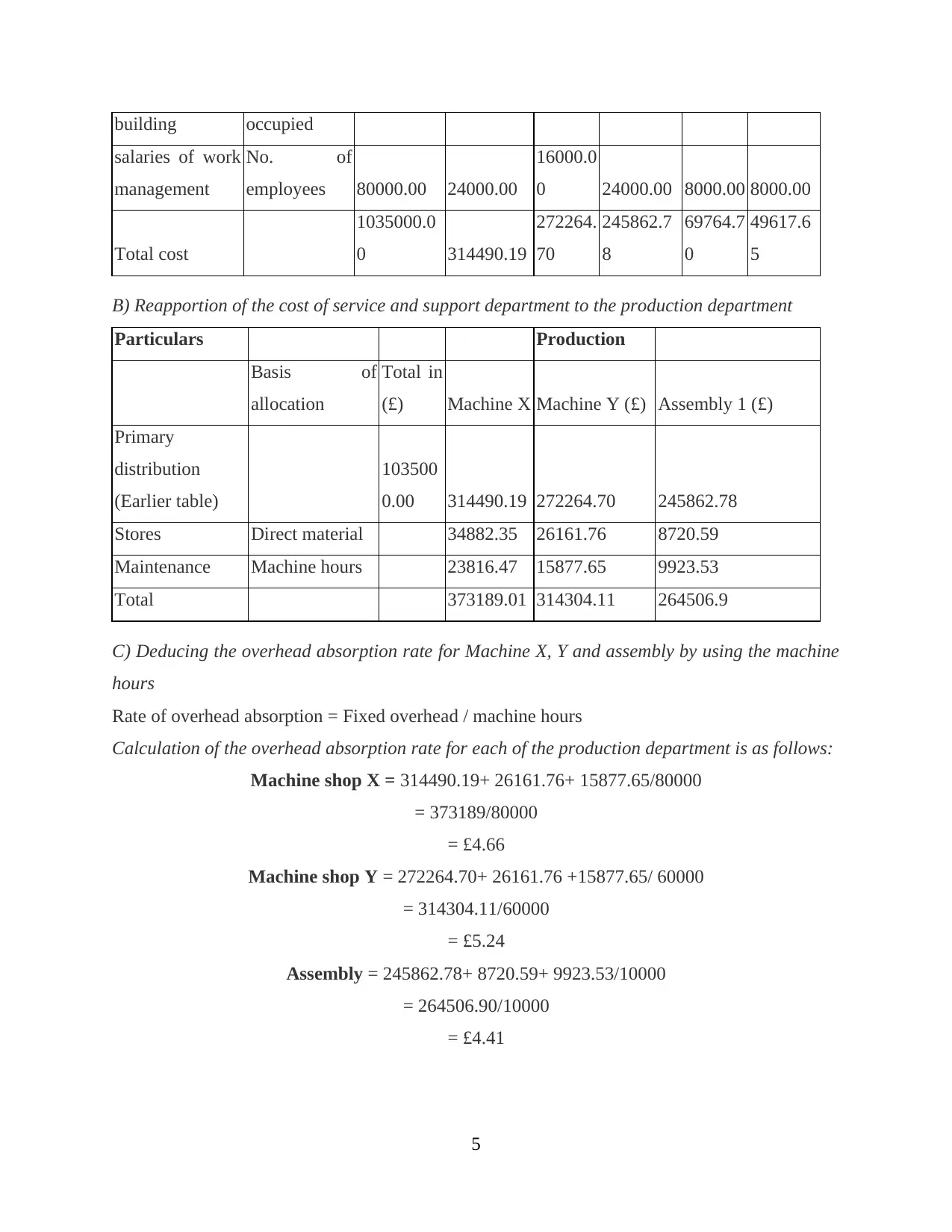

building occupied

salaries of work

management

No. of

employees 80000.00 24000.00

16000.0

0 24000.00 8000.00 8000.00

Total cost

1035000.0

0 314490.19

272264.

70

245862.7

8

69764.7

0

49617.6

5

B) Reapportion of the cost of service and support department to the production department

Particulars Production

Basis of

allocation

Total in

(£) Machine X Machine Y (£) Assembly 1 (£)

Primary

distribution

(Earlier table)

103500

0.00 314490.19 272264.70 245862.78

Stores Direct material 34882.35 26161.76 8720.59

Maintenance Machine hours 23816.47 15877.65 9923.53

Total 373189.01 314304.11 264506.9

C) Deducing the overhead absorption rate for Machine X, Y and assembly by using the machine

hours

Rate of overhead absorption = Fixed overhead / machine hours

Calculation of the overhead absorption rate for each of the production department is as follows:

Machine shop X = 314490.19+ 26161.76+ 15877.65/80000

= 373189/80000

= £4.66

Machine shop Y = 272264.70+ 26161.76 +15877.65/ 60000

= 314304.11/60000

= £5.24

Assembly = 245862.78+ 8720.59+ 9923.53/10000

= 264506.90/10000

= £4.41

5

salaries of work

management

No. of

employees 80000.00 24000.00

16000.0

0 24000.00 8000.00 8000.00

Total cost

1035000.0

0 314490.19

272264.

70

245862.7

8

69764.7

0

49617.6

5

B) Reapportion of the cost of service and support department to the production department

Particulars Production

Basis of

allocation

Total in

(£) Machine X Machine Y (£) Assembly 1 (£)

Primary

distribution

(Earlier table)

103500

0.00 314490.19 272264.70 245862.78

Stores Direct material 34882.35 26161.76 8720.59

Maintenance Machine hours 23816.47 15877.65 9923.53

Total 373189.01 314304.11 264506.9

C) Deducing the overhead absorption rate for Machine X, Y and assembly by using the machine

hours

Rate of overhead absorption = Fixed overhead / machine hours

Calculation of the overhead absorption rate for each of the production department is as follows:

Machine shop X = 314490.19+ 26161.76+ 15877.65/80000

= 373189/80000

= £4.66

Machine shop Y = 272264.70+ 26161.76 +15877.65/ 60000

= 314304.11/60000

= £5.24

Assembly = 245862.78+ 8720.59+ 9923.53/10000

= 264506.90/10000

= £4.41

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

As per the above calculation, it can be suggested that overhead absorption rate of

department X is £4.66 whereas for department Y, it is £5.24. Thus, in place of which assembly

needs to absorb their overhead rate at £4.41.

D) Calculating the overhead charge to the product by using the absorption rate

Total overhead cost = 4.66+ 5.24+ 4.41 = 14.31

Cost of product may be defined as the sum up of material, labour and overhead expenses.

Total cost of the product: Material + Labour + Overhead

= 8+ 15+ 14.31

= £37.31

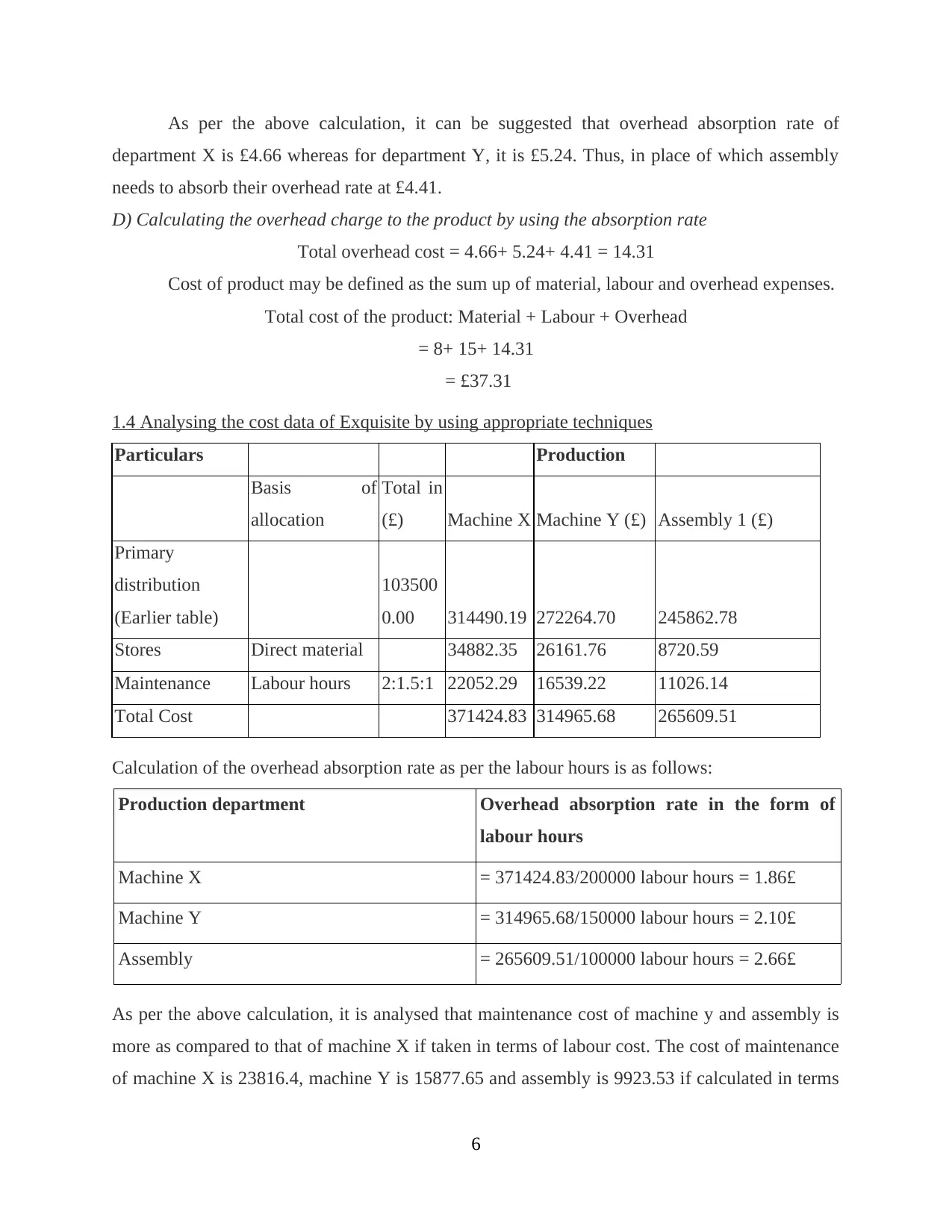

1.4 Analysing the cost data of Exquisite by using appropriate techniques

Particulars Production

Basis of

allocation

Total in

(£) Machine X Machine Y (£) Assembly 1 (£)

Primary

distribution

(Earlier table)

103500

0.00 314490.19 272264.70 245862.78

Stores Direct material 34882.35 26161.76 8720.59

Maintenance Labour hours 2:1.5:1 22052.29 16539.22 11026.14

Total Cost 371424.83 314965.68 265609.51

Calculation of the overhead absorption rate as per the labour hours is as follows:

Production department Overhead absorption rate in the form of

labour hours

Machine X = 371424.83/200000 labour hours = 1.86£

Machine Y = 314965.68/150000 labour hours = 2.10£

Assembly = 265609.51/100000 labour hours = 2.66£

As per the above calculation, it is analysed that maintenance cost of machine y and assembly is

more as compared to that of machine X if taken in terms of labour cost. The cost of maintenance

of machine X is 23816.4, machine Y is 15877.65 and assembly is 9923.53 if calculated in terms

6

department X is £4.66 whereas for department Y, it is £5.24. Thus, in place of which assembly

needs to absorb their overhead rate at £4.41.

D) Calculating the overhead charge to the product by using the absorption rate

Total overhead cost = 4.66+ 5.24+ 4.41 = 14.31

Cost of product may be defined as the sum up of material, labour and overhead expenses.

Total cost of the product: Material + Labour + Overhead

= 8+ 15+ 14.31

= £37.31

1.4 Analysing the cost data of Exquisite by using appropriate techniques

Particulars Production

Basis of

allocation

Total in

(£) Machine X Machine Y (£) Assembly 1 (£)

Primary

distribution

(Earlier table)

103500

0.00 314490.19 272264.70 245862.78

Stores Direct material 34882.35 26161.76 8720.59

Maintenance Labour hours 2:1.5:1 22052.29 16539.22 11026.14

Total Cost 371424.83 314965.68 265609.51

Calculation of the overhead absorption rate as per the labour hours is as follows:

Production department Overhead absorption rate in the form of

labour hours

Machine X = 371424.83/200000 labour hours = 1.86£

Machine Y = 314965.68/150000 labour hours = 2.10£

Assembly = 265609.51/100000 labour hours = 2.66£

As per the above calculation, it is analysed that maintenance cost of machine y and assembly is

more as compared to that of machine X if taken in terms of labour cost. The cost of maintenance

of machine X is 23816.4, machine Y is 15877.65 and assembly is 9923.53 if calculated in terms

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

of machine hours. Similarly cost of maintenance of machine X is 2205.29, machine y is

16539.22 and assembly is 11026.14 if calculated in terms of labour hours. Thus, it can be

concluded that cost of maintenance of changes as the cost per unit product changes. Moreover it

can be said that the cost of product changes as a when cost of maintenance changes.

Task 2

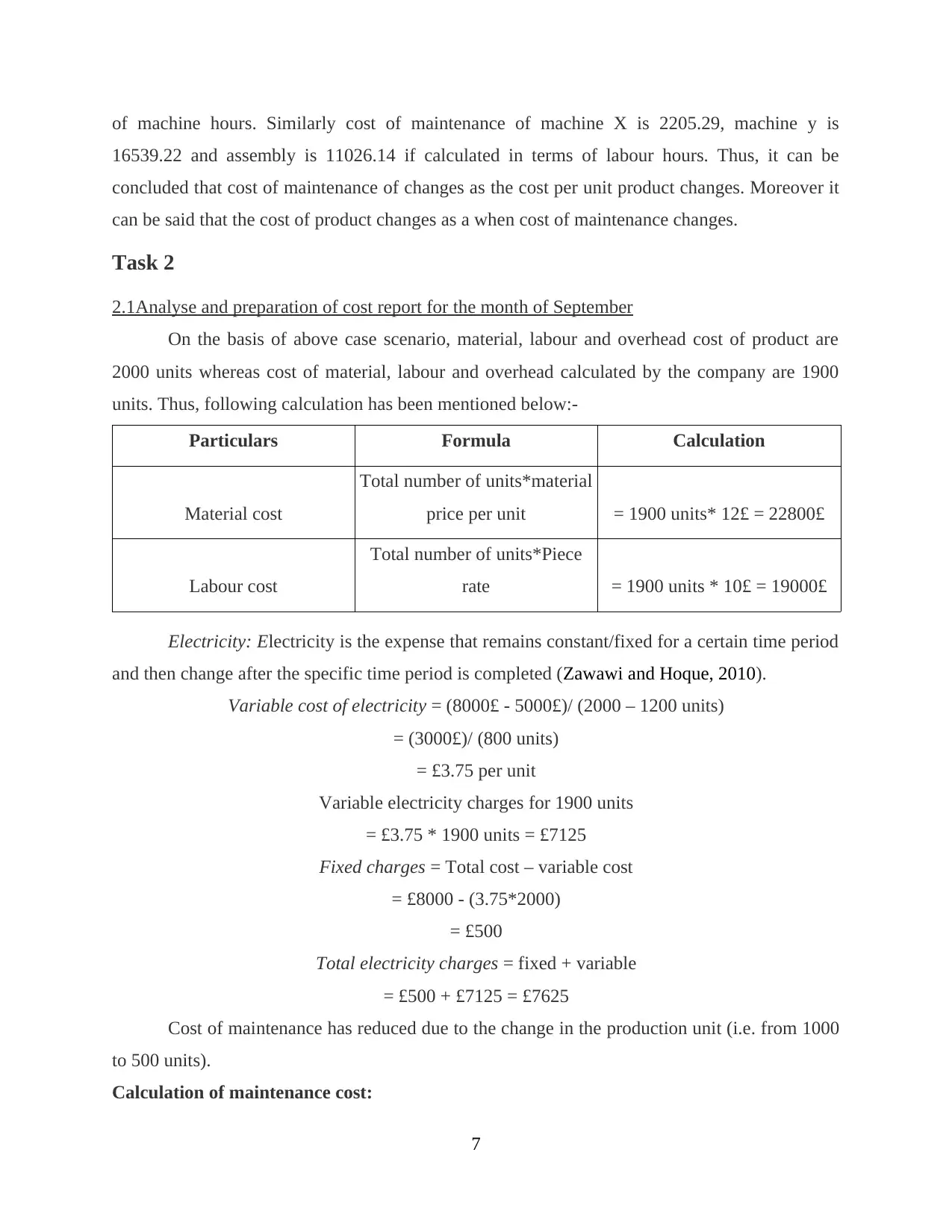

2.1Analyse and preparation of cost report for the month of September

On the basis of above case scenario, material, labour and overhead cost of product are

2000 units whereas cost of material, labour and overhead calculated by the company are 1900

units. Thus, following calculation has been mentioned below:-

Particulars Formula Calculation

Material cost

Total number of units*material

price per unit = 1900 units* 12£ = 22800£

Labour cost

Total number of units*Piece

rate = 1900 units * 10£ = 19000£

Electricity: Electricity is the expense that remains constant/fixed for a certain time period

and then change after the specific time period is completed (Zawawi and Hoque, 2010).

Variable cost of electricity = (8000£ - 5000£)/ (2000 – 1200 units)

= (3000£)/ (800 units)

= £3.75 per unit

Variable electricity charges for 1900 units

= £3.75 * 1900 units = £7125

Fixed charges = Total cost – variable cost

= £8000 - (3.75*2000)

= £500

Total electricity charges = fixed + variable

= £500 + £7125 = £7625

Cost of maintenance has reduced due to the change in the production unit (i.e. from 1000

to 500 units).

Calculation of maintenance cost:

7

16539.22 and assembly is 11026.14 if calculated in terms of labour hours. Thus, it can be

concluded that cost of maintenance of changes as the cost per unit product changes. Moreover it

can be said that the cost of product changes as a when cost of maintenance changes.

Task 2

2.1Analyse and preparation of cost report for the month of September

On the basis of above case scenario, material, labour and overhead cost of product are

2000 units whereas cost of material, labour and overhead calculated by the company are 1900

units. Thus, following calculation has been mentioned below:-

Particulars Formula Calculation

Material cost

Total number of units*material

price per unit = 1900 units* 12£ = 22800£

Labour cost

Total number of units*Piece

rate = 1900 units * 10£ = 19000£

Electricity: Electricity is the expense that remains constant/fixed for a certain time period

and then change after the specific time period is completed (Zawawi and Hoque, 2010).

Variable cost of electricity = (8000£ - 5000£)/ (2000 – 1200 units)

= (3000£)/ (800 units)

= £3.75 per unit

Variable electricity charges for 1900 units

= £3.75 * 1900 units = £7125

Fixed charges = Total cost – variable cost

= £8000 - (3.75*2000)

= £500

Total electricity charges = fixed + variable

= £500 + £7125 = £7625

Cost of maintenance has reduced due to the change in the production unit (i.e. from 1000

to 500 units).

Calculation of maintenance cost:

7

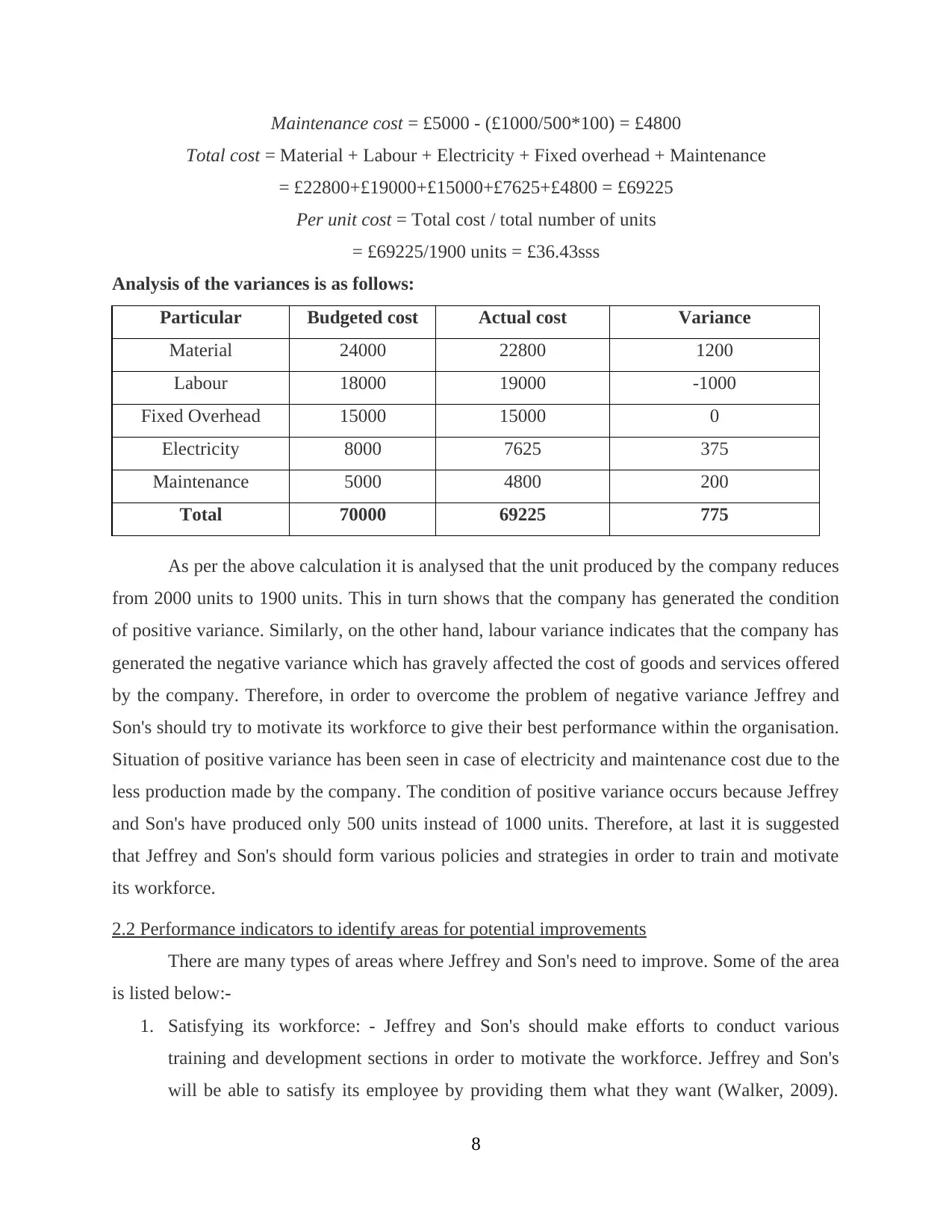

Maintenance cost = £5000 - (£1000/500*100) = £4800

Total cost = Material + Labour + Electricity + Fixed overhead + Maintenance

= £22800+£19000+£15000+£7625+£4800 = £69225

Per unit cost = Total cost / total number of units

= £69225/1900 units = £36.43sss

Analysis of the variances is as follows:

Particular Budgeted cost Actual cost Variance

Material 24000 22800 1200

Labour 18000 19000 -1000

Fixed Overhead 15000 15000 0

Electricity 8000 7625 375

Maintenance 5000 4800 200

Total 70000 69225 775

As per the above calculation it is analysed that the unit produced by the company reduces

from 2000 units to 1900 units. This in turn shows that the company has generated the condition

of positive variance. Similarly, on the other hand, labour variance indicates that the company has

generated the negative variance which has gravely affected the cost of goods and services offered

by the company. Therefore, in order to overcome the problem of negative variance Jeffrey and

Son's should try to motivate its workforce to give their best performance within the organisation.

Situation of positive variance has been seen in case of electricity and maintenance cost due to the

less production made by the company. The condition of positive variance occurs because Jeffrey

and Son's have produced only 500 units instead of 1000 units. Therefore, at last it is suggested

that Jeffrey and Son's should form various policies and strategies in order to train and motivate

its workforce.

2.2 Performance indicators to identify areas for potential improvements

There are many types of areas where Jeffrey and Son's need to improve. Some of the area

is listed below:-

1. Satisfying its workforce: - Jeffrey and Son's should make efforts to conduct various

training and development sections in order to motivate the workforce. Jeffrey and Son's

will be able to satisfy its employee by providing them what they want (Walker, 2009).

8

Total cost = Material + Labour + Electricity + Fixed overhead + Maintenance

= £22800+£19000+£15000+£7625+£4800 = £69225

Per unit cost = Total cost / total number of units

= £69225/1900 units = £36.43sss

Analysis of the variances is as follows:

Particular Budgeted cost Actual cost Variance

Material 24000 22800 1200

Labour 18000 19000 -1000

Fixed Overhead 15000 15000 0

Electricity 8000 7625 375

Maintenance 5000 4800 200

Total 70000 69225 775

As per the above calculation it is analysed that the unit produced by the company reduces

from 2000 units to 1900 units. This in turn shows that the company has generated the condition

of positive variance. Similarly, on the other hand, labour variance indicates that the company has

generated the negative variance which has gravely affected the cost of goods and services offered

by the company. Therefore, in order to overcome the problem of negative variance Jeffrey and

Son's should try to motivate its workforce to give their best performance within the organisation.

Situation of positive variance has been seen in case of electricity and maintenance cost due to the

less production made by the company. The condition of positive variance occurs because Jeffrey

and Son's have produced only 500 units instead of 1000 units. Therefore, at last it is suggested

that Jeffrey and Son's should form various policies and strategies in order to train and motivate

its workforce.

2.2 Performance indicators to identify areas for potential improvements

There are many types of areas where Jeffrey and Son's need to improve. Some of the area

is listed below:-

1. Satisfying its workforce: - Jeffrey and Son's should make efforts to conduct various

training and development sections in order to motivate the workforce. Jeffrey and Son's

will be able to satisfy its employee by providing them what they want (Walker, 2009).

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Highly motivated workforce will be able to produce the good and better quality of

product by reducing the wastage of the resources.

2. Jeffrey and Sons should prepare various types of accounting and financial statements in

order to analyse the position of the company. By preparing this statements company will

be able to reduce the cost of the production and at the time will help the company to

increase its level of profitability.

3. Jeffrey and Son's should prepare various budgets in advance in order to reduce the cost of

sales (Halbouni and Hassan, 2012). Along with this company will also be able to reduce

its cost of production and manufacturing.

2.3 Ways to reduce cost of production and to enhance the value and quality of the product

1. Jeffrey and Son's should make efforts to prepare various budgets in advance in order to

manage all its operations properly. Preparation of budgets will also aid the company to

monitor the growth of budget which in turn will help the company to estimate the actual

position of the company (Mirghani, 2001).

2. Jeffrey and Son’s company should also try to motivate its employees by organising

various training and development sections. Highly motivated and trained employee will

be produce better quality of goods and services. This in turn will take the company

towards the growth rate.

3. Jeffrey and Son's should also try to properly utilise the production process. This in turn

will assist the company to reduce the steps in the production process and easily generate

what they want.

4. Company should try to appoint the highly skilled and trained workers. This in turn will

help the company to reduce the value of its products (Bourne, Franco and Wilkes, 2003).

Task 3

3.1Purpose and nature of the budgeting process to the budget holders of Jeffrey and Son's

Budget is the plan that is prepared by the company in order to estimate the income

generated and expense made by the company during a certain time period.

Purpose of preparing the budgeting process.

9

product by reducing the wastage of the resources.

2. Jeffrey and Sons should prepare various types of accounting and financial statements in

order to analyse the position of the company. By preparing this statements company will

be able to reduce the cost of the production and at the time will help the company to

increase its level of profitability.

3. Jeffrey and Son's should prepare various budgets in advance in order to reduce the cost of

sales (Halbouni and Hassan, 2012). Along with this company will also be able to reduce

its cost of production and manufacturing.

2.3 Ways to reduce cost of production and to enhance the value and quality of the product

1. Jeffrey and Son's should make efforts to prepare various budgets in advance in order to

manage all its operations properly. Preparation of budgets will also aid the company to

monitor the growth of budget which in turn will help the company to estimate the actual

position of the company (Mirghani, 2001).

2. Jeffrey and Son’s company should also try to motivate its employees by organising

various training and development sections. Highly motivated and trained employee will

be produce better quality of goods and services. This in turn will take the company

towards the growth rate.

3. Jeffrey and Son's should also try to properly utilise the production process. This in turn

will assist the company to reduce the steps in the production process and easily generate

what they want.

4. Company should try to appoint the highly skilled and trained workers. This in turn will

help the company to reduce the value of its products (Bourne, Franco and Wilkes, 2003).

Task 3

3.1Purpose and nature of the budgeting process to the budget holders of Jeffrey and Son's

Budget is the plan that is prepared by the company in order to estimate the income

generated and expense made by the company during a certain time period.

Purpose of preparing the budgeting process.

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1. Budgets are prepared by the company in order to calculate the amount the income

generated and expenditure that are made company after the completion of the specific

time period (Burns, Hopper and Yazd far, 2004).

2. Budgets are prepared by the company in order to develop various strategies. Strategies

are developed by the company in order to achieve what they want by beating its

competitors.

3. These budgets are also prepared by the company in order calculate the difference

between the actual performance and the estimated performance.

Nature of budgeting process

1. In order to prepare new budget and estimate the financial environment company need to

compare its previous budgets in order to get the accurate results.

2. Once budgets are compared than company to define the amount of capital that is going

to be incurred by the company at the time of selling its products (Irwin, D. and Scott, M.

J., 2010).

3. After that company should define the cost of expenses that are going to be incurred by

the company at the time of undertaking the various promotional activities like

advertisement, sales distribution and so on.

4. Then at last company should subtract the estimated income from that of estimated

expense in order to find out whether the condition of deficit has arisen or surplus (Portz,

and Lere, 2010).

5. At last the following budget prepared should be submitted in order to implement it.

3.2Appropriate budgeting method need to be used by the organisation and its needs

Jeffrey and Son's prepare the incremental budgets with an aim to prepare various budgets.

In order to prepare new incremental budgets Jeffrey and Son's consider the previous budgets. But

the incremental budget that is prepared by Jeffrey and Son's is losing its existence now-days.

Thus, Jeffrey and Son's should prepare the realistic budget in order to analyse the actual

results. Therefore, in order to prepare the actual budget company should use Zero base budgeting

method. Zero based budgeting method is the budget that is prepared by the organisation in order

to incur the cost of expenses that can be incurred by the company during a financial year. This

type of budgets is prepared by the company keeping the Zero as a base.

10

generated and expenditure that are made company after the completion of the specific

time period (Burns, Hopper and Yazd far, 2004).

2. Budgets are prepared by the company in order to develop various strategies. Strategies

are developed by the company in order to achieve what they want by beating its

competitors.

3. These budgets are also prepared by the company in order calculate the difference

between the actual performance and the estimated performance.

Nature of budgeting process

1. In order to prepare new budget and estimate the financial environment company need to

compare its previous budgets in order to get the accurate results.

2. Once budgets are compared than company to define the amount of capital that is going

to be incurred by the company at the time of selling its products (Irwin, D. and Scott, M.

J., 2010).

3. After that company should define the cost of expenses that are going to be incurred by

the company at the time of undertaking the various promotional activities like

advertisement, sales distribution and so on.

4. Then at last company should subtract the estimated income from that of estimated

expense in order to find out whether the condition of deficit has arisen or surplus (Portz,

and Lere, 2010).

5. At last the following budget prepared should be submitted in order to implement it.

3.2Appropriate budgeting method need to be used by the organisation and its needs

Jeffrey and Son's prepare the incremental budgets with an aim to prepare various budgets.

In order to prepare new incremental budgets Jeffrey and Son's consider the previous budgets. But

the incremental budget that is prepared by Jeffrey and Son's is losing its existence now-days.

Thus, Jeffrey and Son's should prepare the realistic budget in order to analyse the actual

results. Therefore, in order to prepare the actual budget company should use Zero base budgeting

method. Zero based budgeting method is the budget that is prepared by the organisation in order

to incur the cost of expenses that can be incurred by the company during a financial year. This

type of budgets is prepared by the company keeping the Zero as a base.

10

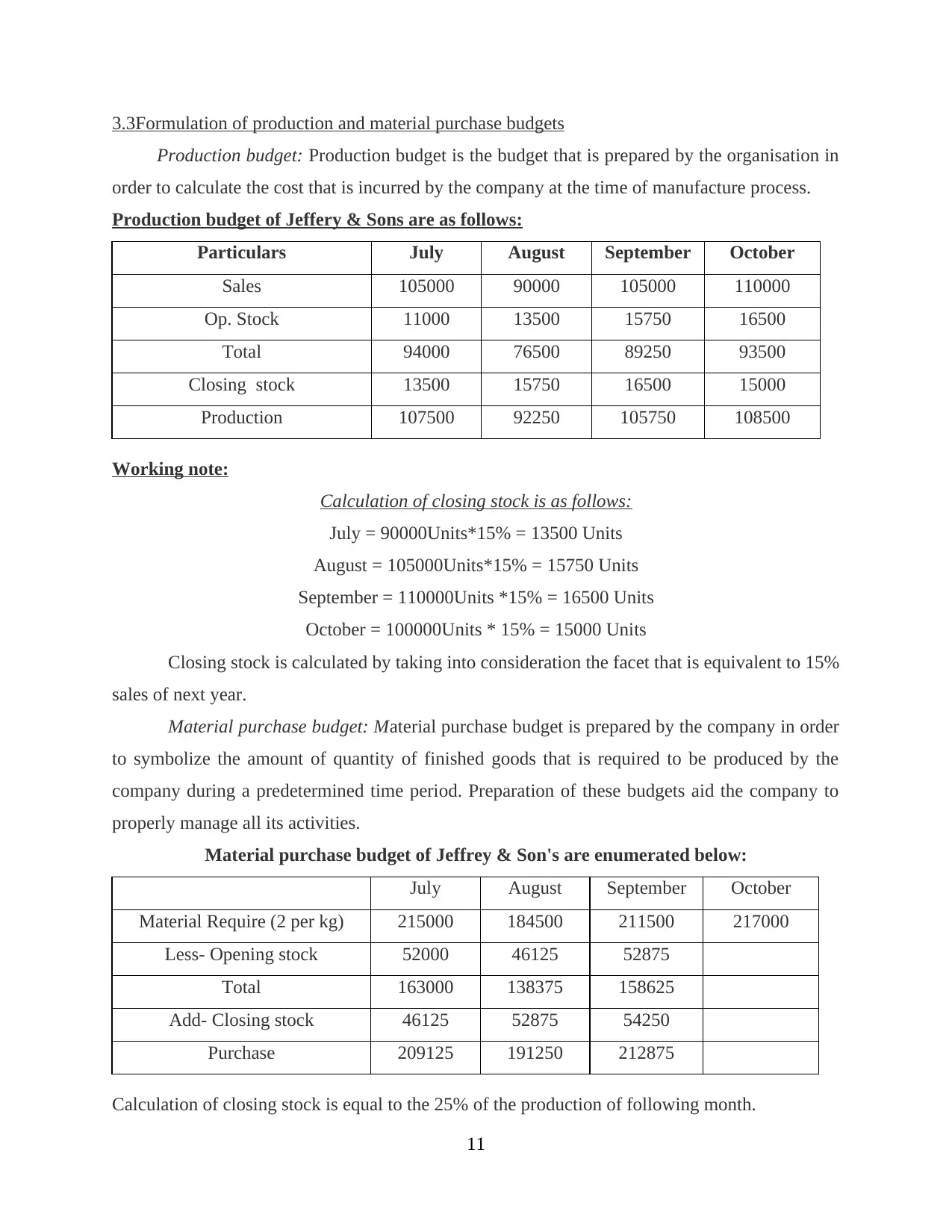

3.3Formulation of production and material purchase budgets

Production budget: Production budget is the budget that is prepared by the organisation in

order to calculate the cost that is incurred by the company at the time of manufacture process.

Production budget of Jeffery & Sons are as follows:

Particulars July August September October

Sales 105000 90000 105000 110000

Op. Stock 11000 13500 15750 16500

Total 94000 76500 89250 93500

Closing stock 13500 15750 16500 15000

Production 107500 92250 105750 108500

Working note:

Calculation of closing stock is as follows:

July = 90000Units*15% = 13500 Units

August = 105000Units*15% = 15750 Units

September = 110000Units *15% = 16500 Units

October = 100000Units * 15% = 15000 Units

Closing stock is calculated by taking into consideration the facet that is equivalent to 15%

sales of next year.

Material purchase budget: Material purchase budget is prepared by the company in order

to symbolize the amount of quantity of finished goods that is required to be produced by the

company during a predetermined time period. Preparation of these budgets aid the company to

properly manage all its activities.

Material purchase budget of Jeffrey & Son's are enumerated below:

July August September October

Material Require (2 per kg) 215000 184500 211500 217000

Less- Opening stock 52000 46125 52875

Total 163000 138375 158625

Add- Closing stock 46125 52875 54250

Purchase 209125 191250 212875

Calculation of closing stock is equal to the 25% of the production of following month.

11

Production budget: Production budget is the budget that is prepared by the organisation in

order to calculate the cost that is incurred by the company at the time of manufacture process.

Production budget of Jeffery & Sons are as follows:

Particulars July August September October

Sales 105000 90000 105000 110000

Op. Stock 11000 13500 15750 16500

Total 94000 76500 89250 93500

Closing stock 13500 15750 16500 15000

Production 107500 92250 105750 108500

Working note:

Calculation of closing stock is as follows:

July = 90000Units*15% = 13500 Units

August = 105000Units*15% = 15750 Units

September = 110000Units *15% = 16500 Units

October = 100000Units * 15% = 15000 Units

Closing stock is calculated by taking into consideration the facet that is equivalent to 15%

sales of next year.

Material purchase budget: Material purchase budget is prepared by the company in order

to symbolize the amount of quantity of finished goods that is required to be produced by the

company during a predetermined time period. Preparation of these budgets aid the company to

properly manage all its activities.

Material purchase budget of Jeffrey & Son's are enumerated below:

July August September October

Material Require (2 per kg) 215000 184500 211500 217000

Less- Opening stock 52000 46125 52875

Total 163000 138375 158625

Add- Closing stock 46125 52875 54250

Purchase 209125 191250 212875

Calculation of closing stock is equal to the 25% of the production of following month.

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.