Management Accounting Report: Costing, Budgeting, and Scorecard

VerifiedAdded on 2019/12/18

|10

|2527

|144

Report

AI Summary

This report provides a comprehensive overview of management accounting principles and practices. It begins by differentiating between management and financial accounting, highlighting their distinct purposes and applications. The report delves into various management accounting systems, including cost accounting, inventory management, and job costing. It then explores costing methods, comparing absorption and marginal costing through income statement preparation and analysis. Budgeting techniques are also discussed, encompassing fixed and flexible budgets, along with the process of budget preparation. Finally, the report examines the balance scorecard as a strategic tool, explaining its implementation, its role in identifying and solving financial problems, and its use in improving financial governance and developing effective strategies. The report aims to provide a thorough understanding of these key areas within management accounting.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Management accounting and financial accounting......................................................................3

Different type of management accounting systems.....................................................................4

TASK 2............................................................................................................................................5

Preparation of income statement by using absorption and marginal costing method.................5

TASK 3............................................................................................................................................6

Different type of budget...............................................................................................................6

TASK 4............................................................................................................................................8

Defining balance score card and implementation of same..........................................................8

Implementation of balance scorecard..........................................................................................8

Way in which balance scorecard can be used to identify and solving financial problems..........8

Use of balance scorecard to improve financial governance and development of effective

strategies......................................................................................................................................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Management accounting and financial accounting......................................................................3

Different type of management accounting systems.....................................................................4

TASK 2............................................................................................................................................5

Preparation of income statement by using absorption and marginal costing method.................5

TASK 3............................................................................................................................................6

Different type of budget...............................................................................................................6

TASK 4............................................................................................................................................8

Defining balance score card and implementation of same..........................................................8

Implementation of balance scorecard..........................................................................................8

Way in which balance scorecard can be used to identify and solving financial problems..........8

Use of balance scorecard to improve financial governance and development of effective

strategies......................................................................................................................................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION

Management accounting is the one of the important field that is used to measure the firm

performance in the systematic manner. In the current report difference between financial and

management accounting is explained in detail. Along with this, in the report different sort of

management accounting systems are discussed briefly. Additionally, cost and profit is also

computed by using marginal and absorption costing method and results are interpreted. At end of

the report, budget preparation process is explained and balance scorecard is discussed in detail.

TASK 1

Management accounting and financial accounting

1 Difference between management and financial accounting

There is a huge difference between the management and financial accounting.

Management accounting refers to the subject or area where entire cost related facts are recorded

and analyzed to measure the firm business performance. On other hand, financial management

refers to the subject wherein different things like capital structure and firm performance is

measured in respect to different areas like liquidity and cost control etc. It can be said that

management and financial accounting are different from each other in terms of use and

application (Zimmerman and Yahya-Zadeh, 2011). There are different sort of techniques that

comes in the management and financial accounting. In the management accounting some of the

methods that comes are variance analysis, break even analysis, budget and marginal as well as

absorption costing. On other hand, in case of financial accounting techniques that used are ratio

analysis and preparation of income statement and balance sheet etc. This reflects that there are

different methods that comes in both sort of accounting.

2Importance of management accounting as a decision making tool for department managers

Management accounting information have a due importance for the managers because by

using same they can make wise decisions in respect to their departments. There are two different

departments that make a very heavy use of the management accounting information like

production and material department (Macintosh and Quattrone, 2010). Production department

manager on the basis of available information that is related to the management accounting

determine number of units that must be produced and number of raw material units that will be

need to produce goods at the workplace. Similarly, on the basis of management accounting

Management accounting is the one of the important field that is used to measure the firm

performance in the systematic manner. In the current report difference between financial and

management accounting is explained in detail. Along with this, in the report different sort of

management accounting systems are discussed briefly. Additionally, cost and profit is also

computed by using marginal and absorption costing method and results are interpreted. At end of

the report, budget preparation process is explained and balance scorecard is discussed in detail.

TASK 1

Management accounting and financial accounting

1 Difference between management and financial accounting

There is a huge difference between the management and financial accounting.

Management accounting refers to the subject or area where entire cost related facts are recorded

and analyzed to measure the firm business performance. On other hand, financial management

refers to the subject wherein different things like capital structure and firm performance is

measured in respect to different areas like liquidity and cost control etc. It can be said that

management and financial accounting are different from each other in terms of use and

application (Zimmerman and Yahya-Zadeh, 2011). There are different sort of techniques that

comes in the management and financial accounting. In the management accounting some of the

methods that comes are variance analysis, break even analysis, budget and marginal as well as

absorption costing. On other hand, in case of financial accounting techniques that used are ratio

analysis and preparation of income statement and balance sheet etc. This reflects that there are

different methods that comes in both sort of accounting.

2Importance of management accounting as a decision making tool for department managers

Management accounting information have a due importance for the managers because by

using same they can make wise decisions in respect to their departments. There are two different

departments that make a very heavy use of the management accounting information like

production and material department (Macintosh and Quattrone, 2010). Production department

manager on the basis of available information that is related to the management accounting

determine number of units that must be produced and number of raw material units that will be

need to produce goods at the workplace. Similarly, on the basis of management accounting

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

information material manager decide the quantity of raw material that must be purchases so that

less amount of raw material remain unused on certain date. It can be said that it is the

management accounting information on basis of which decisions are taken by the department

managers. There are number of tools and methods in the management accounting by using which

different calculations are performed and decisions are taken by the department managers. This

reflects that there is huge importance of the management accounting for the managers.

Different type of management accounting systems

There are different sort of management accounting systems and same are explained below. Cost accounting systems: Cost accounting system is the one of the most important

accounting system under which all sort of expenses are recorded under different

classifications (Baldvinsdottir, Mitchell and Nørreklit, 2010). Thus, systematic report is

prepared on the basis of cost accounting systems under which overall cost of variable and

fixed expenses is calculated separately. Inventory management systems: Inventory management system is one under which data

related to inventory is recorded regularly and on basis of same information is generated

which is used to make inventory related decisions at Imda Tech. In the mentioned system

inventory records are prepared in terms of different type of raw material and finished

products. Thus, overall value of separate inventory that is in stock is revealed by

inventory management system. Job costing system: In the job order costing system for different orders that are received

from the customers costing is done separately. Thus, job costing system reveal the cost of

all product lines individually. Price optimizing systems: Pricing optimizing systems are used for the price optimization

of the products. It can be said that mentioned systems help managers in making price

related decisions (Ward, 2012). Management accounting systems and process are

interlinked to each other with organization process because with progress in production

process from these systems reports are generated and by considering same decisions are

taken by the managers.

less amount of raw material remain unused on certain date. It can be said that it is the

management accounting information on basis of which decisions are taken by the department

managers. There are number of tools and methods in the management accounting by using which

different calculations are performed and decisions are taken by the department managers. This

reflects that there is huge importance of the management accounting for the managers.

Different type of management accounting systems

There are different sort of management accounting systems and same are explained below. Cost accounting systems: Cost accounting system is the one of the most important

accounting system under which all sort of expenses are recorded under different

classifications (Baldvinsdottir, Mitchell and Nørreklit, 2010). Thus, systematic report is

prepared on the basis of cost accounting systems under which overall cost of variable and

fixed expenses is calculated separately. Inventory management systems: Inventory management system is one under which data

related to inventory is recorded regularly and on basis of same information is generated

which is used to make inventory related decisions at Imda Tech. In the mentioned system

inventory records are prepared in terms of different type of raw material and finished

products. Thus, overall value of separate inventory that is in stock is revealed by

inventory management system. Job costing system: In the job order costing system for different orders that are received

from the customers costing is done separately. Thus, job costing system reveal the cost of

all product lines individually. Price optimizing systems: Pricing optimizing systems are used for the price optimization

of the products. It can be said that mentioned systems help managers in making price

related decisions (Ward, 2012). Management accounting systems and process are

interlinked to each other with organization process because with progress in production

process from these systems reports are generated and by considering same decisions are

taken by the managers.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 2

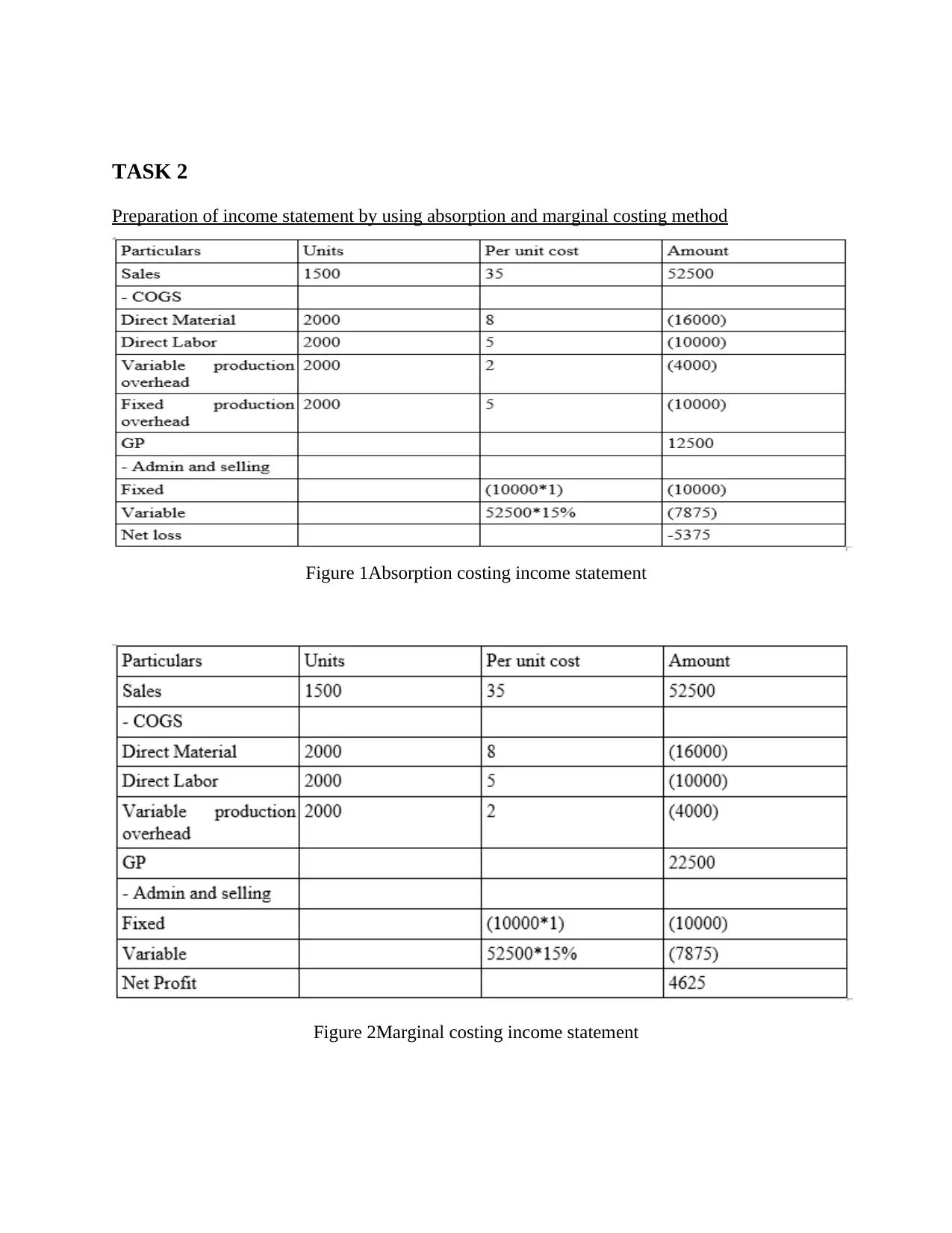

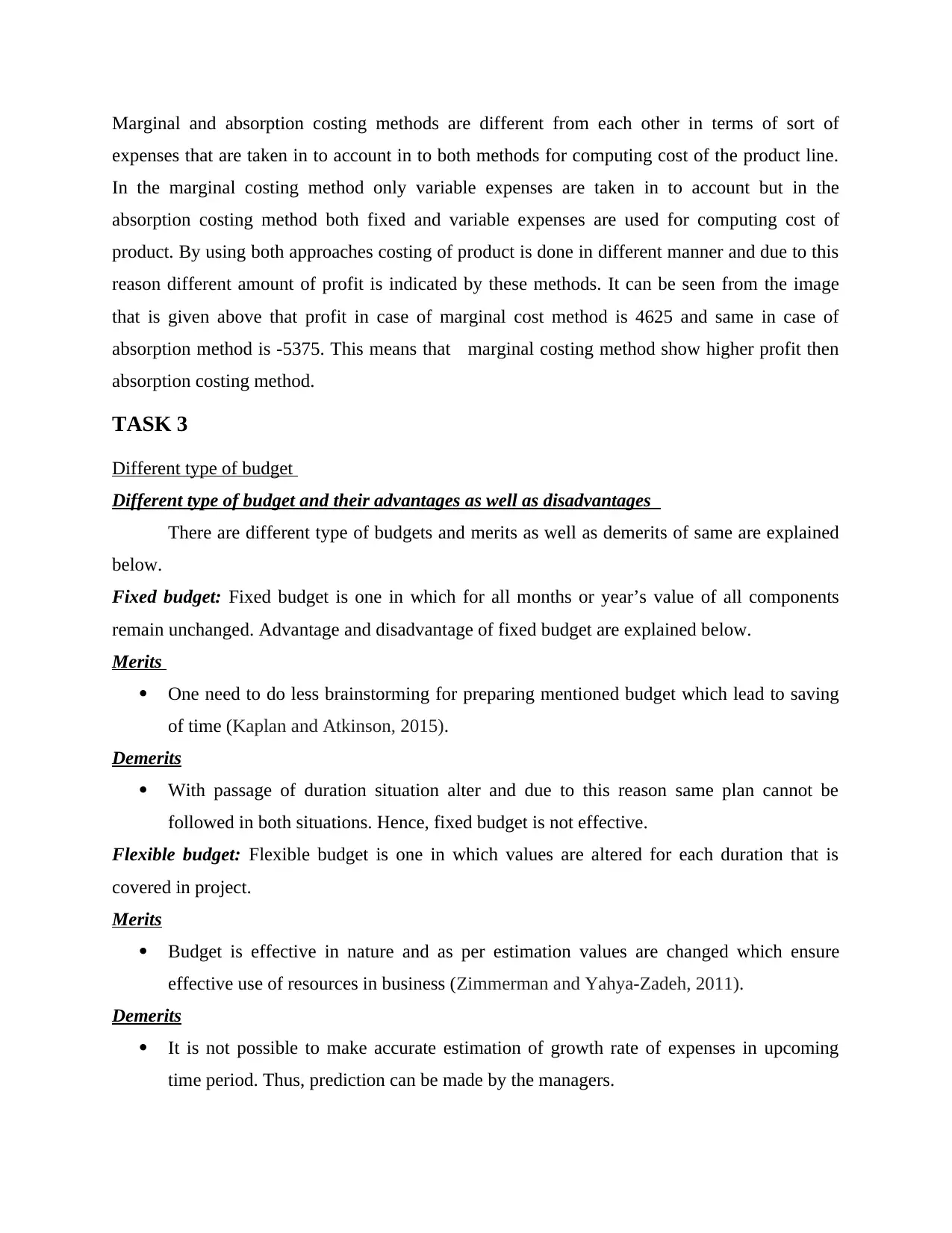

Preparation of income statement by using absorption and marginal costing method

Figure 1Absorption costing income statement

Figure 2Marginal costing income statement

Preparation of income statement by using absorption and marginal costing method

Figure 1Absorption costing income statement

Figure 2Marginal costing income statement

Marginal and absorption costing methods are different from each other in terms of sort of

expenses that are taken in to account in to both methods for computing cost of the product line.

In the marginal costing method only variable expenses are taken in to account but in the

absorption costing method both fixed and variable expenses are used for computing cost of

product. By using both approaches costing of product is done in different manner and due to this

reason different amount of profit is indicated by these methods. It can be seen from the image

that is given above that profit in case of marginal cost method is 4625 and same in case of

absorption method is -5375. This means that marginal costing method show higher profit then

absorption costing method.

TASK 3

Different type of budget

Different type of budget and their advantages as well as disadvantages

There are different type of budgets and merits as well as demerits of same are explained

below.

Fixed budget: Fixed budget is one in which for all months or year’s value of all components

remain unchanged. Advantage and disadvantage of fixed budget are explained below.

Merits

One need to do less brainstorming for preparing mentioned budget which lead to saving

of time (Kaplan and Atkinson, 2015).

Demerits

With passage of duration situation alter and due to this reason same plan cannot be

followed in both situations. Hence, fixed budget is not effective.

Flexible budget: Flexible budget is one in which values are altered for each duration that is

covered in project.

Merits

Budget is effective in nature and as per estimation values are changed which ensure

effective use of resources in business (Zimmerman and Yahya-Zadeh, 2011).

Demerits

It is not possible to make accurate estimation of growth rate of expenses in upcoming

time period. Thus, prediction can be made by the managers.

expenses that are taken in to account in to both methods for computing cost of the product line.

In the marginal costing method only variable expenses are taken in to account but in the

absorption costing method both fixed and variable expenses are used for computing cost of

product. By using both approaches costing of product is done in different manner and due to this

reason different amount of profit is indicated by these methods. It can be seen from the image

that is given above that profit in case of marginal cost method is 4625 and same in case of

absorption method is -5375. This means that marginal costing method show higher profit then

absorption costing method.

TASK 3

Different type of budget

Different type of budget and their advantages as well as disadvantages

There are different type of budgets and merits as well as demerits of same are explained

below.

Fixed budget: Fixed budget is one in which for all months or year’s value of all components

remain unchanged. Advantage and disadvantage of fixed budget are explained below.

Merits

One need to do less brainstorming for preparing mentioned budget which lead to saving

of time (Kaplan and Atkinson, 2015).

Demerits

With passage of duration situation alter and due to this reason same plan cannot be

followed in both situations. Hence, fixed budget is not effective.

Flexible budget: Flexible budget is one in which values are altered for each duration that is

covered in project.

Merits

Budget is effective in nature and as per estimation values are changed which ensure

effective use of resources in business (Zimmerman and Yahya-Zadeh, 2011).

Demerits

It is not possible to make accurate estimation of growth rate of expenses in upcoming

time period. Thus, prediction can be made by the managers.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Process of preparing budget Obtaining estimates: In the first stage estimates are prepared by the managers. In this

regard first of all past year data and conditions are taken in to account. Study is done on

variance analysis. Estimation is made about future time period and on the basis of overall

work estimates are prepared for the upcoming time period. Coordinating estimates: In the second stage different budget plans that are received from

the managers are reviewed and on that basis final budget is prepared (Herman, 2011). On

different parameters all received budget are evaluated by the managers. Communicating budget: After finalization of the budget same is send to the top

managers for the approval. According to the recommendation received from the top

manager modifications are done in the budget. Implementing budget plan: In the fourth stage budget that is prepared is implemented by

the managers and allocation of resources is done to different departments.

Preparing progress report: Progress report is prepared under which firm performance in

respect to budget standard is tracked and deviation in performance is identified.

Pricing strategy

Different pricing strategy that can be followed by the business firm are given below. Cost plus pricing: Cost plus pricing is the method under which to cost margin is added.

Most of the firms use this approach because costing for all is different to some extent. So

firms add target margin to the product cost and determine final price of the product. Competitor based pricing: Under this method price that is set by the competitors is taken

in to account to determine the price of the product (Marie and Rao, 2010). This strategy is

used where completion is very tough and there are number of rivals in the market. Penetration strategy: Penetration pricing is another method that is used to compete in the

market where there are number of rivals. Under this product is sold at very low price in

the market. It can be said that it is the one of the commonly used pricing strategy.

regard first of all past year data and conditions are taken in to account. Study is done on

variance analysis. Estimation is made about future time period and on the basis of overall

work estimates are prepared for the upcoming time period. Coordinating estimates: In the second stage different budget plans that are received from

the managers are reviewed and on that basis final budget is prepared (Herman, 2011). On

different parameters all received budget are evaluated by the managers. Communicating budget: After finalization of the budget same is send to the top

managers for the approval. According to the recommendation received from the top

manager modifications are done in the budget. Implementing budget plan: In the fourth stage budget that is prepared is implemented by

the managers and allocation of resources is done to different departments.

Preparing progress report: Progress report is prepared under which firm performance in

respect to budget standard is tracked and deviation in performance is identified.

Pricing strategy

Different pricing strategy that can be followed by the business firm are given below. Cost plus pricing: Cost plus pricing is the method under which to cost margin is added.

Most of the firms use this approach because costing for all is different to some extent. So

firms add target margin to the product cost and determine final price of the product. Competitor based pricing: Under this method price that is set by the competitors is taken

in to account to determine the price of the product (Marie and Rao, 2010). This strategy is

used where completion is very tough and there are number of rivals in the market. Penetration strategy: Penetration pricing is another method that is used to compete in the

market where there are number of rivals. Under this product is sold at very low price in

the market. It can be said that it is the one of the commonly used pricing strategy.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 4

Defining balance score card and implementation of same

Balance scorecard is the strategic planning tool that is used by the managers for managing

situation in better way. Balance scorecard is basically used public and private firms as well as

nonprofit organizations to align their business activities with the vision and strategy of the

business firm (Garrison and et.al., 2010). By using balanced scorecard approach performance of

the business firm is evaluated and on that basis the area where there is need to pay due attention

is identified. Balance scorecard is the model which have four components like financial,

customers, internal business process and learning as well as growth. Performance in these areas

is measured by using balance scorecard.

Implementation of balance scorecard

There is a systematic process under which balance scorecard approach is implemented in

the business. In this regard, first of all key performance indicators are determined for the

business in respect to finance, customer, business process and learning as well as growth. In the

second stage simple firm performance is measured and compared with the standards that are

determined in the balance scorecard. Strategy is formulated in respect to the area where firm

performance is weak. In this way, balance scorecard approach is implemented by the Imda Tech

in its business.

Way in which balance scorecard can be used to identify and solving financial problems

Balance scorecard can be used to identify and solving the financial problems. Under this

business firm can determine tough standards in the balance scorecard in respect to finance. Like

key performance indicator may be set in respect to cost of capital, debt equity ratio and other

areas that are related to finance (Noreen, Brewer. and Garrison, 2011). Actual values can be

compared with standard and by doing so performance of the firm can be measured in terms of

finance. Thus, in this way financial problems are identified and way that can be followed to solve

same are prepared to improve business performance.

Use of balance scorecard to improve financial governance and development of effective

strategies

Financial governance refers to the determination of roles and responsibilities of the

employees in respect to the management of finance in the organization. By doing so it is ensured

Defining balance score card and implementation of same

Balance scorecard is the strategic planning tool that is used by the managers for managing

situation in better way. Balance scorecard is basically used public and private firms as well as

nonprofit organizations to align their business activities with the vision and strategy of the

business firm (Garrison and et.al., 2010). By using balanced scorecard approach performance of

the business firm is evaluated and on that basis the area where there is need to pay due attention

is identified. Balance scorecard is the model which have four components like financial,

customers, internal business process and learning as well as growth. Performance in these areas

is measured by using balance scorecard.

Implementation of balance scorecard

There is a systematic process under which balance scorecard approach is implemented in

the business. In this regard, first of all key performance indicators are determined for the

business in respect to finance, customer, business process and learning as well as growth. In the

second stage simple firm performance is measured and compared with the standards that are

determined in the balance scorecard. Strategy is formulated in respect to the area where firm

performance is weak. In this way, balance scorecard approach is implemented by the Imda Tech

in its business.

Way in which balance scorecard can be used to identify and solving financial problems

Balance scorecard can be used to identify and solving the financial problems. Under this

business firm can determine tough standards in the balance scorecard in respect to finance. Like

key performance indicator may be set in respect to cost of capital, debt equity ratio and other

areas that are related to finance (Noreen, Brewer. and Garrison, 2011). Actual values can be

compared with standard and by doing so performance of the firm can be measured in terms of

finance. Thus, in this way financial problems are identified and way that can be followed to solve

same are prepared to improve business performance.

Use of balance scorecard to improve financial governance and development of effective

strategies

Financial governance refers to the determination of roles and responsibilities of the

employees in respect to the management of finance in the organization. By doing so it is ensured

that if any mistake is done then in that case there will be someone that can be assumed

responsible for the mistakes that is done in respect to finance in the business. In the balance

scorecard criteria can be determined in terms of responsibility and accountability of the

employees and current performance in respect to these areas can be compared with standards to

determine the level of financial governance in the firm (Financial governance, 2017). In case it

is identified that performance was not good then in that case strong monitoring system can be

developed and eye can be kept on performance of relevant candidate and it can be ensured that

relevant person it fulfilling all its responsibilities and accountability.

CONCLUSION

On the basis of above discussion it is concluded that management accounting is the vast

field under which there are number of methods that can be used by the managers to make their

management better with passage of time. It is also concluded that budget must be prepared in

proper manner because by doing so best use of resources can be made in the business. It is also

concluded that balance scorecard must be used to measure firm performance and strategy must

be formulated to improve performance.

responsible for the mistakes that is done in respect to finance in the business. In the balance

scorecard criteria can be determined in terms of responsibility and accountability of the

employees and current performance in respect to these areas can be compared with standards to

determine the level of financial governance in the firm (Financial governance, 2017). In case it

is identified that performance was not good then in that case strong monitoring system can be

developed and eye can be kept on performance of relevant candidate and it can be ensured that

relevant person it fulfilling all its responsibilities and accountability.

CONCLUSION

On the basis of above discussion it is concluded that management accounting is the vast

field under which there are number of methods that can be used by the managers to make their

management better with passage of time. It is also concluded that budget must be prepared in

proper manner because by doing so best use of resources can be made in the business. It is also

concluded that balance scorecard must be used to measure firm performance and strategy must

be formulated to improve performance.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and journals

Baldvinsdottir, G., Mitchell, F. and Nørreklit, H., 2010. Issues in the relationship between theory

and practice in management accounting. Management Accounting Research. 21(2). pp.79-82.

Garrison, R.H and et.al., 2010. Managerial accounting. Issues in Accounting Education. 25(4).

pp.792-793.

Herman, R.D., 2011. The Jossey-Bass handbook of nonprofit leadership and management. John

Wiley & Sons.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Macintosh, N.B. and Quattrone, P., 2010. Management accounting and control systems: An

organizational and sociological approach. John Wiley & Sons.

Marie, A. and Rao, A., 2010. Is Standard Costing Still Relevant? Evidence from

Dubai. Management Accounting Quarterly. 11(2).

Noreen, E.W., Brewer, P.C. and Garrison, R.H., 2011. Managerial accounting for managers.

McGraw-Hill Irwin.

Ward, K., 2012. Strategic management accounting. Routledge.

Zimmerman, J.L. and Yahya-Zadeh, M., 2011. Accounting for decision making and

control. Issues in Accounting Education. 26(1). pp.258-259.

Zimmerman, J.L. and Yahya-Zadeh, M., 2011. Accounting for decision making and

control. Issues in Accounting Education. 26(1). pp.258-259.

Online

Financial governance, 2017. [Online]. Available through :<

http://www.goodgovernance.org.au/financial-governance/>. [Accessed on 13th April 2017].

Books and journals

Baldvinsdottir, G., Mitchell, F. and Nørreklit, H., 2010. Issues in the relationship between theory

and practice in management accounting. Management Accounting Research. 21(2). pp.79-82.

Garrison, R.H and et.al., 2010. Managerial accounting. Issues in Accounting Education. 25(4).

pp.792-793.

Herman, R.D., 2011. The Jossey-Bass handbook of nonprofit leadership and management. John

Wiley & Sons.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Macintosh, N.B. and Quattrone, P., 2010. Management accounting and control systems: An

organizational and sociological approach. John Wiley & Sons.

Marie, A. and Rao, A., 2010. Is Standard Costing Still Relevant? Evidence from

Dubai. Management Accounting Quarterly. 11(2).

Noreen, E.W., Brewer, P.C. and Garrison, R.H., 2011. Managerial accounting for managers.

McGraw-Hill Irwin.

Ward, K., 2012. Strategic management accounting. Routledge.

Zimmerman, J.L. and Yahya-Zadeh, M., 2011. Accounting for decision making and

control. Issues in Accounting Education. 26(1). pp.258-259.

Zimmerman, J.L. and Yahya-Zadeh, M., 2011. Accounting for decision making and

control. Issues in Accounting Education. 26(1). pp.258-259.

Online

Financial governance, 2017. [Online]. Available through :<

http://www.goodgovernance.org.au/financial-governance/>. [Accessed on 13th April 2017].

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.