Management Accounting Report: Financial Problem Solutions

VerifiedAdded on 2020/10/05

|13

|3992

|252

Report

AI Summary

This report delves into the core concepts of management accounting, examining its role in internal decision-making and policy formulation within organizations. It explores the essential components of management accounting systems, including planning, organizing, controlling, and decision-making processes. The report details different costing systems such as actual, standard, and normal costing, as well as inventory management techniques like FIFO and LIFO, and job and batch costing. Furthermore, it analyzes various reporting methods employed in management accounting, such as budget reports, accounts receivable reports, and job cost reports, highlighting their importance in decision-making, cost reduction, and enhancing financial returns. The report also provides a practical application by calculating costs using marginal and absorption costing methods and preparing income statements. Finally, it discusses the merits and demerits of budgetary controls and how management accounting systems aid companies in addressing financial problems.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1:Demonstrating management accounting and requirements of systems of management

accounting...................................................................................................................................1

P2: Different methods used in management accounting reports.................................................3

TASK 2 ..........................................................................................................................................5

P3: Calculating cost using appropriate techniques and preparation of income statement..........5

TASK 3 ...........................................................................................................................................7

P4: Various types of budgets and their merits and demerits.......................................................7

TASK 4 ..........................................................................................................................................9

P5: Adapting management accounting systems in responding to financial problems................9

CONCLUSION ...............................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1:Demonstrating management accounting and requirements of systems of management

accounting...................................................................................................................................1

P2: Different methods used in management accounting reports.................................................3

TASK 2 ..........................................................................................................................................5

P3: Calculating cost using appropriate techniques and preparation of income statement..........5

TASK 3 ...........................................................................................................................................7

P4: Various types of budgets and their merits and demerits.......................................................7

TASK 4 ..........................................................................................................................................9

P5: Adapting management accounting systems in responding to financial problems................9

CONCLUSION ...............................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION

Management accounting is the process of accounting that is implemented in the

organisations for the internal management of the companies. The managers and supervisors of

the company uses the reports made by the management accountants for the decision making and

for formulating policies for the organisations. Management accounting reports consists of the

summaries of financial statements of the company, and the future economic and non economic

activities that may be implemented in the markets in future. The management accounting

reporting is quantitative in nature. This project report will discuss about the the various

management accounting systems and their requirements in the companies. Methods used in the

reporting of management accounting reports( Amoako, 2013 ). Analysing the techniques that are

used in the estimation of costs using marginal and absorption costing in preparing statements of

profit and loss. The merits and demerits of using planning tools that are utilised in budgetary

controls. And finally analysing how the management accounting systems helps the companies in

responding to financial problems.

TASK 1

P1:Demonstrating management accounting and requirements of systems of management

accounting

Management accounting, as the name implicates is the accounting that is done for the

internal management of the company. The management accounting is done by analysing and

summarising financial statements of the company and also uses the estimations of the future

economic and non economic policies in its reports that may be implemented in the markets and

which will impact the company.(Management accounting and its importance [Online]) The

managers then uses these reports in the decision making process and formulation of policies for

the companies according to future trends of the market. The essentials of management

accounting systems are discussed as under:

Planning: Planning is done by every company for the attainment of the objectives of the

organisation. It is done for the achievement of the short term as well as long term objectives of

the companies( Bushee, Carter, and Gerakos, 2013 ). The management accounting process helps

the mangers in the formation of the different budgets that are required to analyse the estimates of

costs and expenditure in the operations. These budgets also assists in setting performance

standards for the company as a whole and for the individual employees.

1

Management accounting is the process of accounting that is implemented in the

organisations for the internal management of the companies. The managers and supervisors of

the company uses the reports made by the management accountants for the decision making and

for formulating policies for the organisations. Management accounting reports consists of the

summaries of financial statements of the company, and the future economic and non economic

activities that may be implemented in the markets in future. The management accounting

reporting is quantitative in nature. This project report will discuss about the the various

management accounting systems and their requirements in the companies. Methods used in the

reporting of management accounting reports( Amoako, 2013 ). Analysing the techniques that are

used in the estimation of costs using marginal and absorption costing in preparing statements of

profit and loss. The merits and demerits of using planning tools that are utilised in budgetary

controls. And finally analysing how the management accounting systems helps the companies in

responding to financial problems.

TASK 1

P1:Demonstrating management accounting and requirements of systems of management

accounting

Management accounting, as the name implicates is the accounting that is done for the

internal management of the company. The management accounting is done by analysing and

summarising financial statements of the company and also uses the estimations of the future

economic and non economic policies in its reports that may be implemented in the markets and

which will impact the company.(Management accounting and its importance [Online]) The

managers then uses these reports in the decision making process and formulation of policies for

the companies according to future trends of the market. The essentials of management

accounting systems are discussed as under:

Planning: Planning is done by every company for the attainment of the objectives of the

organisation. It is done for the achievement of the short term as well as long term objectives of

the companies( Bushee, Carter, and Gerakos, 2013 ). The management accounting process helps

the mangers in the formation of the different budgets that are required to analyse the estimates of

costs and expenditure in the operations. These budgets also assists in setting performance

standards for the company as a whole and for the individual employees.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Organizing: This organisational process deals with managing the people of the company

in order to formulate well defined framework for the organisation and defining the roles and

responsibilities for each department and employee. This process assists in creating and

maintaining a proper hierarchy for the workplace and this is done with the help of management

accounting.

Controlling: This process of the companies deals with measuring the performances of

the departments and employees in the organisation by comparing their actual performances with

the standard performances as per pre-stated in the budgets of the companies. The controlling

process also measures the actual sales of the companies with standard sales then finding the

variations and taking corrective measures if required. This is all done because of the

management accounting as it helps in the preparation of budgets.

Decision making: The main purpose of management accounting reports is to assists

internal managers of the companies in the decision making process and making policies and

regulations for companies taking into consideration the market trends that may impact the

operations of the company by using the management accounting reports.( Chiarini, 2012 )

Different Costing systems:

Actual costing: This system of costing involves the measurement of actual expenditure

that is incurred in the process of production and other operations. This method of costing

considers the costs that is incurred in each job including the costs related to direct labour, direct

material and other overheads.

Standard Costing: This costing system estimates the standard cost that should be

incurred in the production process . The standard cost of various operations are analysed in the

company for different overheads such as material , labour etc. and then these are uses as

comparing tool for analysing the actual performances.

Normal costing: This method considers the original rates that are assigned to the

manufacturing heads such as labour, material etc. at the initial stage of the year. The material and

labour are assigned the actual rates and only overheads rate is fixed as earlier determined.

Inventory management systems: The management of inventories is very essential in the

organisations as it is necessary in the efficient production process and meeting customer

demands. The raw material inventories management helps companies to provide production

department with the goods as and when required without hindering the process. And finished

2

in order to formulate well defined framework for the organisation and defining the roles and

responsibilities for each department and employee. This process assists in creating and

maintaining a proper hierarchy for the workplace and this is done with the help of management

accounting.

Controlling: This process of the companies deals with measuring the performances of

the departments and employees in the organisation by comparing their actual performances with

the standard performances as per pre-stated in the budgets of the companies. The controlling

process also measures the actual sales of the companies with standard sales then finding the

variations and taking corrective measures if required. This is all done because of the

management accounting as it helps in the preparation of budgets.

Decision making: The main purpose of management accounting reports is to assists

internal managers of the companies in the decision making process and making policies and

regulations for companies taking into consideration the market trends that may impact the

operations of the company by using the management accounting reports.( Chiarini, 2012 )

Different Costing systems:

Actual costing: This system of costing involves the measurement of actual expenditure

that is incurred in the process of production and other operations. This method of costing

considers the costs that is incurred in each job including the costs related to direct labour, direct

material and other overheads.

Standard Costing: This costing system estimates the standard cost that should be

incurred in the production process . The standard cost of various operations are analysed in the

company for different overheads such as material , labour etc. and then these are uses as

comparing tool for analysing the actual performances.

Normal costing: This method considers the original rates that are assigned to the

manufacturing heads such as labour, material etc. at the initial stage of the year. The material and

labour are assigned the actual rates and only overheads rate is fixed as earlier determined.

Inventory management systems: The management of inventories is very essential in the

organisations as it is necessary in the efficient production process and meeting customer

demands. The raw material inventories management helps companies to provide production

department with the goods as and when required without hindering the process. And finished

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

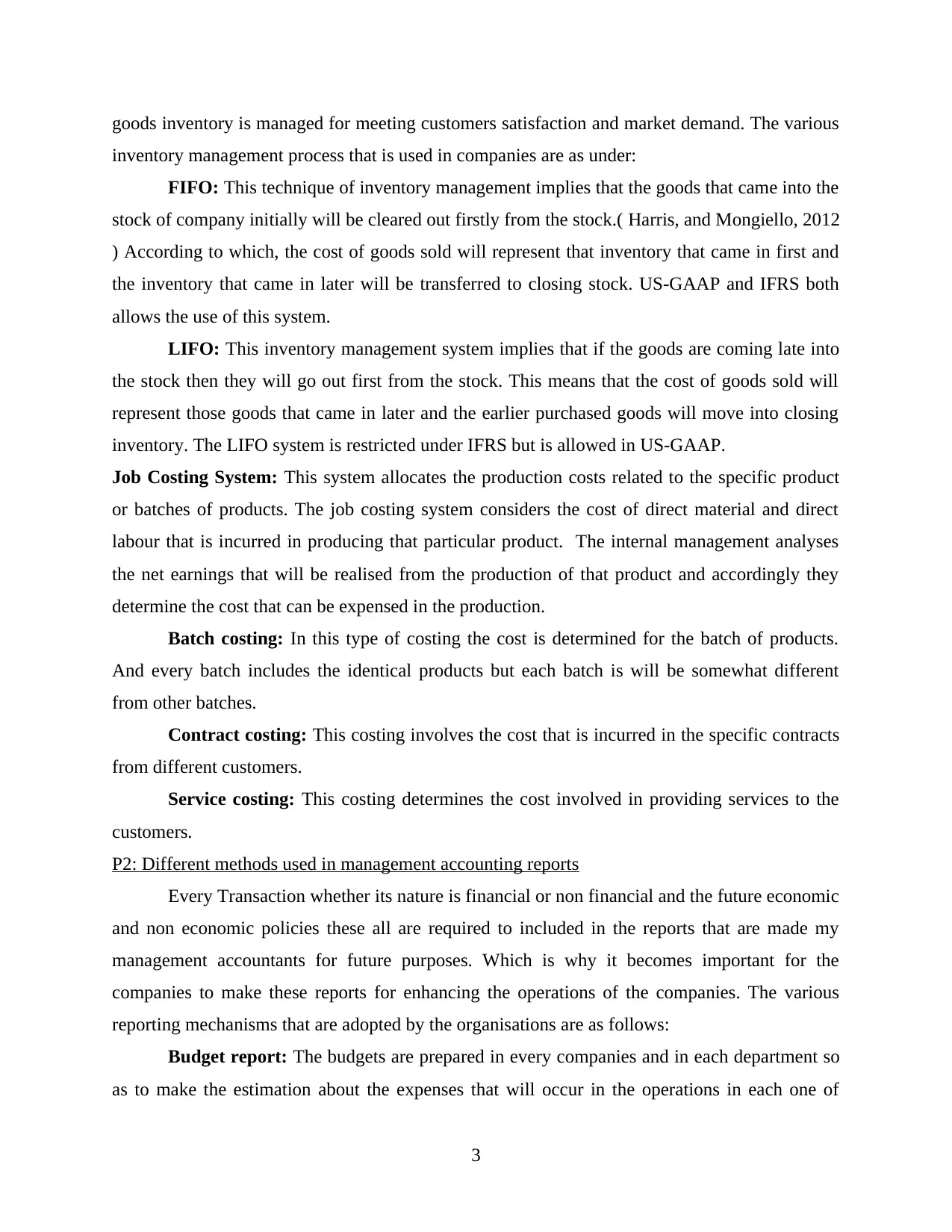

goods inventory is managed for meeting customers satisfaction and market demand. The various

inventory management process that is used in companies are as under:

FIFO: This technique of inventory management implies that the goods that came into the

stock of company initially will be cleared out firstly from the stock.( Harris, and Mongiello, 2012

) According to which, the cost of goods sold will represent that inventory that came in first and

the inventory that came in later will be transferred to closing stock. US-GAAP and IFRS both

allows the use of this system.

LIFO: This inventory management system implies that if the goods are coming late into

the stock then they will go out first from the stock. This means that the cost of goods sold will

represent those goods that came in later and the earlier purchased goods will move into closing

inventory. The LIFO system is restricted under IFRS but is allowed in US-GAAP.

Job Costing System: This system allocates the production costs related to the specific product

or batches of products. The job costing system considers the cost of direct material and direct

labour that is incurred in producing that particular product. The internal management analyses

the net earnings that will be realised from the production of that product and accordingly they

determine the cost that can be expensed in the production.

Batch costing: In this type of costing the cost is determined for the batch of products.

And every batch includes the identical products but each batch is will be somewhat different

from other batches.

Contract costing: This costing involves the cost that is incurred in the specific contracts

from different customers.

Service costing: This costing determines the cost involved in providing services to the

customers.

P2: Different methods used in management accounting reports

Every Transaction whether its nature is financial or non financial and the future economic

and non economic policies these all are required to included in the reports that are made my

management accountants for future purposes. Which is why it becomes important for the

companies to make these reports for enhancing the operations of the companies. The various

reporting mechanisms that are adopted by the organisations are as follows:

Budget report: The budgets are prepared in every companies and in each department so

as to make the estimation about the expenses that will occur in the operations in each one of

3

inventory management process that is used in companies are as under:

FIFO: This technique of inventory management implies that the goods that came into the

stock of company initially will be cleared out firstly from the stock.( Harris, and Mongiello, 2012

) According to which, the cost of goods sold will represent that inventory that came in first and

the inventory that came in later will be transferred to closing stock. US-GAAP and IFRS both

allows the use of this system.

LIFO: This inventory management system implies that if the goods are coming late into

the stock then they will go out first from the stock. This means that the cost of goods sold will

represent those goods that came in later and the earlier purchased goods will move into closing

inventory. The LIFO system is restricted under IFRS but is allowed in US-GAAP.

Job Costing System: This system allocates the production costs related to the specific product

or batches of products. The job costing system considers the cost of direct material and direct

labour that is incurred in producing that particular product. The internal management analyses

the net earnings that will be realised from the production of that product and accordingly they

determine the cost that can be expensed in the production.

Batch costing: In this type of costing the cost is determined for the batch of products.

And every batch includes the identical products but each batch is will be somewhat different

from other batches.

Contract costing: This costing involves the cost that is incurred in the specific contracts

from different customers.

Service costing: This costing determines the cost involved in providing services to the

customers.

P2: Different methods used in management accounting reports

Every Transaction whether its nature is financial or non financial and the future economic

and non economic policies these all are required to included in the reports that are made my

management accountants for future purposes. Which is why it becomes important for the

companies to make these reports for enhancing the operations of the companies. The various

reporting mechanisms that are adopted by the organisations are as follows:

Budget report: The budgets are prepared in every companies and in each department so

as to make the estimation about the expenses that will occur in the operations in each one of

3

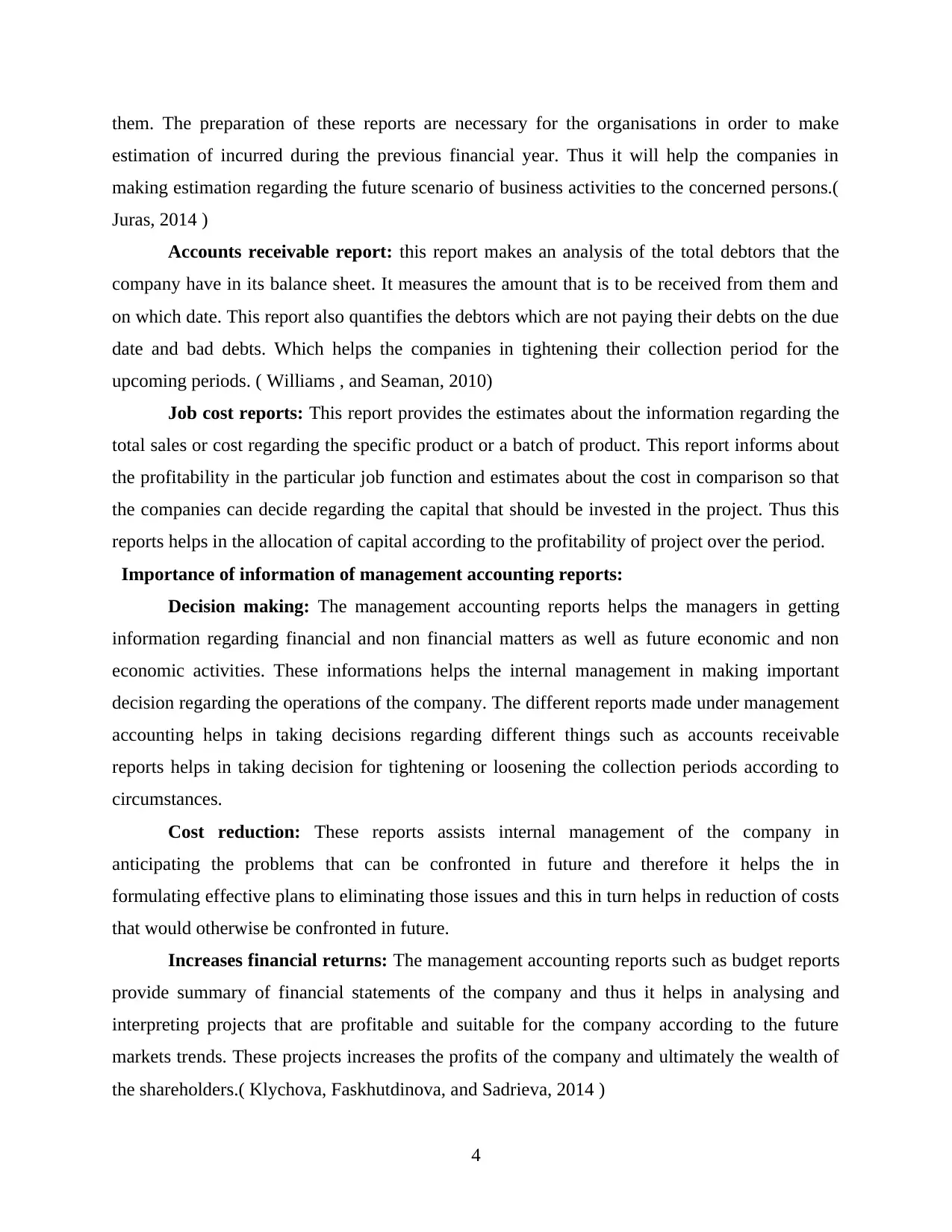

them. The preparation of these reports are necessary for the organisations in order to make

estimation of incurred during the previous financial year. Thus it will help the companies in

making estimation regarding the future scenario of business activities to the concerned persons.(

Juras, 2014 )

Accounts receivable report: this report makes an analysis of the total debtors that the

company have in its balance sheet. It measures the amount that is to be received from them and

on which date. This report also quantifies the debtors which are not paying their debts on the due

date and bad debts. Which helps the companies in tightening their collection period for the

upcoming periods. ( Williams , and Seaman, 2010)

Job cost reports: This report provides the estimates about the information regarding the

total sales or cost regarding the specific product or a batch of product. This report informs about

the profitability in the particular job function and estimates about the cost in comparison so that

the companies can decide regarding the capital that should be invested in the project. Thus this

reports helps in the allocation of capital according to the profitability of project over the period.

Importance of information of management accounting reports:

Decision making: The management accounting reports helps the managers in getting

information regarding financial and non financial matters as well as future economic and non

economic activities. These informations helps the internal management in making important

decision regarding the operations of the company. The different reports made under management

accounting helps in taking decisions regarding different things such as accounts receivable

reports helps in taking decision for tightening or loosening the collection periods according to

circumstances.

Cost reduction: These reports assists internal management of the company in

anticipating the problems that can be confronted in future and therefore it helps the in

formulating effective plans to eliminating those issues and this in turn helps in reduction of costs

that would otherwise be confronted in future.

Increases financial returns: The management accounting reports such as budget reports

provide summary of financial statements of the company and thus it helps in analysing and

interpreting projects that are profitable and suitable for the company according to the future

markets trends. These projects increases the profits of the company and ultimately the wealth of

the shareholders.( Klychova, Faskhutdinova, and Sadrieva, 2014 )

4

estimation of incurred during the previous financial year. Thus it will help the companies in

making estimation regarding the future scenario of business activities to the concerned persons.(

Juras, 2014 )

Accounts receivable report: this report makes an analysis of the total debtors that the

company have in its balance sheet. It measures the amount that is to be received from them and

on which date. This report also quantifies the debtors which are not paying their debts on the due

date and bad debts. Which helps the companies in tightening their collection period for the

upcoming periods. ( Williams , and Seaman, 2010)

Job cost reports: This report provides the estimates about the information regarding the

total sales or cost regarding the specific product or a batch of product. This report informs about

the profitability in the particular job function and estimates about the cost in comparison so that

the companies can decide regarding the capital that should be invested in the project. Thus this

reports helps in the allocation of capital according to the profitability of project over the period.

Importance of information of management accounting reports:

Decision making: The management accounting reports helps the managers in getting

information regarding financial and non financial matters as well as future economic and non

economic activities. These informations helps the internal management in making important

decision regarding the operations of the company. The different reports made under management

accounting helps in taking decisions regarding different things such as accounts receivable

reports helps in taking decision for tightening or loosening the collection periods according to

circumstances.

Cost reduction: These reports assists internal management of the company in

anticipating the problems that can be confronted in future and therefore it helps the in

formulating effective plans to eliminating those issues and this in turn helps in reduction of costs

that would otherwise be confronted in future.

Increases financial returns: The management accounting reports such as budget reports

provide summary of financial statements of the company and thus it helps in analysing and

interpreting projects that are profitable and suitable for the company according to the future

markets trends. These projects increases the profits of the company and ultimately the wealth of

the shareholders.( Klychova, Faskhutdinova, and Sadrieva, 2014 )

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 2

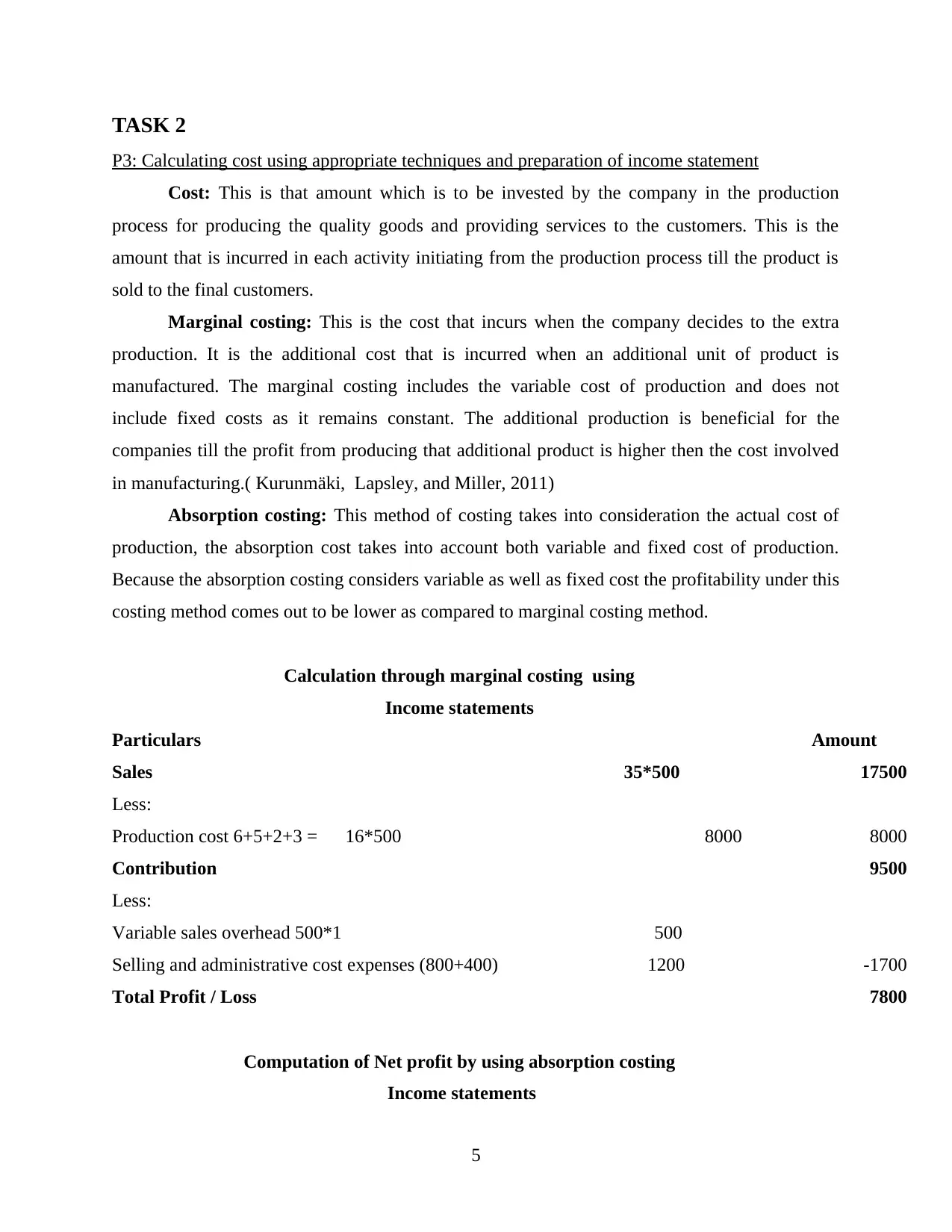

P3: Calculating cost using appropriate techniques and preparation of income statement

Cost: This is that amount which is to be invested by the company in the production

process for producing the quality goods and providing services to the customers. This is the

amount that is incurred in each activity initiating from the production process till the product is

sold to the final customers.

Marginal costing: This is the cost that incurs when the company decides to the extra

production. It is the additional cost that is incurred when an additional unit of product is

manufactured. The marginal costing includes the variable cost of production and does not

include fixed costs as it remains constant. The additional production is beneficial for the

companies till the profit from producing that additional product is higher then the cost involved

in manufacturing.( Kurunmäki, Lapsley, and Miller, 2011)

Absorption costing: This method of costing takes into consideration the actual cost of

production, the absorption cost takes into account both variable and fixed cost of production.

Because the absorption costing considers variable as well as fixed cost the profitability under this

costing method comes out to be lower as compared to marginal costing method.

Calculation through marginal costing using

Income statements

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2+3 = 16*500 8000 8000

Contribution 9500

Less:

Variable sales overhead 500*1 500

Selling and administrative cost expenses (800+400) 1200 -1700

Total Profit / Loss 7800

Computation of Net profit by using absorption costing

Income statements

5

P3: Calculating cost using appropriate techniques and preparation of income statement

Cost: This is that amount which is to be invested by the company in the production

process for producing the quality goods and providing services to the customers. This is the

amount that is incurred in each activity initiating from the production process till the product is

sold to the final customers.

Marginal costing: This is the cost that incurs when the company decides to the extra

production. It is the additional cost that is incurred when an additional unit of product is

manufactured. The marginal costing includes the variable cost of production and does not

include fixed costs as it remains constant. The additional production is beneficial for the

companies till the profit from producing that additional product is higher then the cost involved

in manufacturing.( Kurunmäki, Lapsley, and Miller, 2011)

Absorption costing: This method of costing takes into consideration the actual cost of

production, the absorption cost takes into account both variable and fixed cost of production.

Because the absorption costing considers variable as well as fixed cost the profitability under this

costing method comes out to be lower as compared to marginal costing method.

Calculation through marginal costing using

Income statements

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2+3 = 16*500 8000 8000

Contribution 9500

Less:

Variable sales overhead 500*1 500

Selling and administrative cost expenses (800+400) 1200 -1700

Total Profit / Loss 7800

Computation of Net profit by using absorption costing

Income statements

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

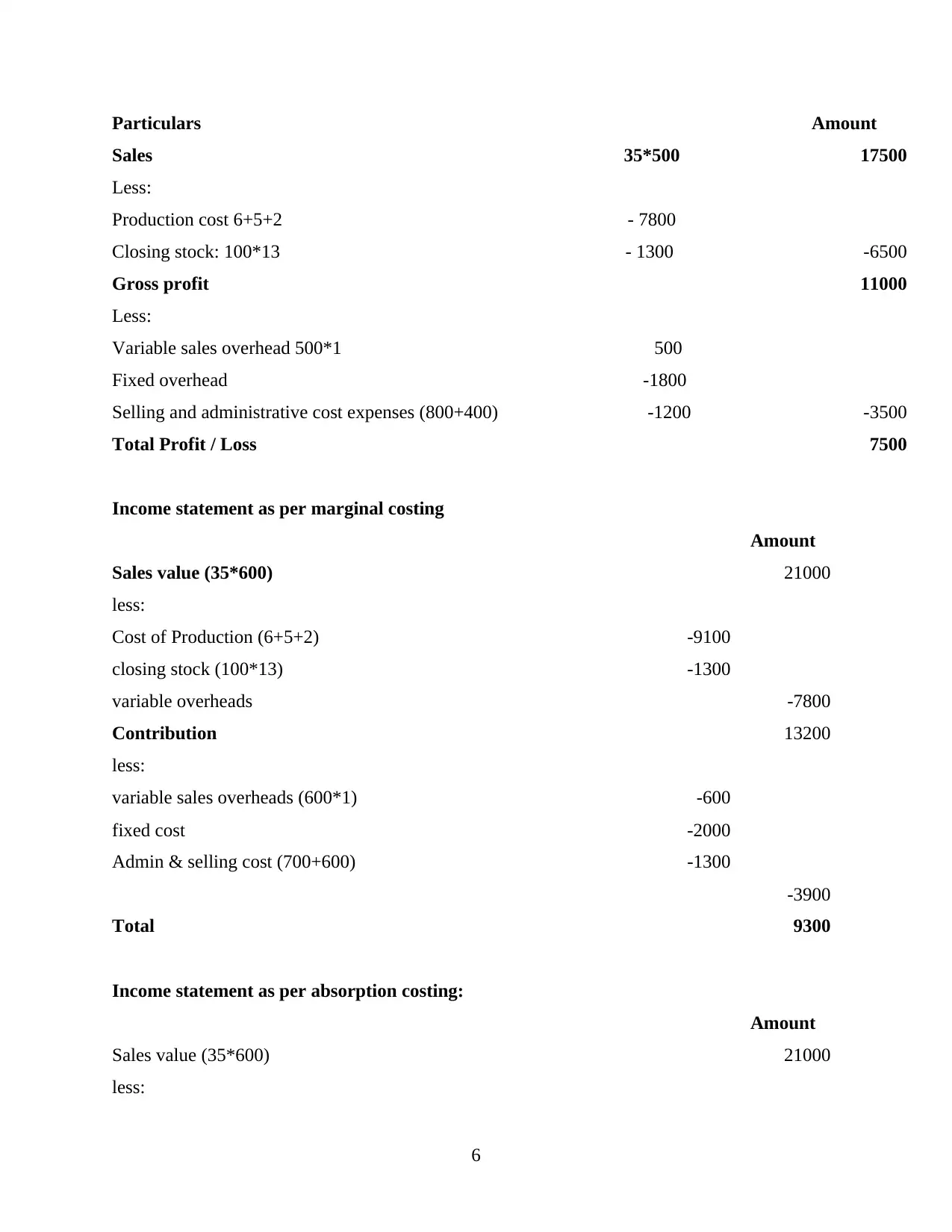

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2 - 7800

Closing stock: 100*13 - 1300 -6500

Gross profit 11000

Less:

Variable sales overhead 500*1 500

Fixed overhead -1800

Selling and administrative cost expenses (800+400) -1200 -3500

Total Profit / Loss 7500

Income statement as per marginal costing

Amount

Sales value (35*600) 21000

less:

Cost of Production (6+5+2) -9100

closing stock (100*13) -1300

variable overheads -7800

Contribution 13200

less:

variable sales overheads (600*1) -600

fixed cost -2000

Admin & selling cost (700+600) -1300

-3900

Total 9300

Income statement as per absorption costing:

Amount

Sales value (35*600) 21000

less:

6

Sales 35*500 17500

Less:

Production cost 6+5+2 - 7800

Closing stock: 100*13 - 1300 -6500

Gross profit 11000

Less:

Variable sales overhead 500*1 500

Fixed overhead -1800

Selling and administrative cost expenses (800+400) -1200 -3500

Total Profit / Loss 7500

Income statement as per marginal costing

Amount

Sales value (35*600) 21000

less:

Cost of Production (6+5+2) -9100

closing stock (100*13) -1300

variable overheads -7800

Contribution 13200

less:

variable sales overheads (600*1) -600

fixed cost -2000

Admin & selling cost (700+600) -1300

-3900

Total 9300

Income statement as per absorption costing:

Amount

Sales value (35*600) 21000

less:

6

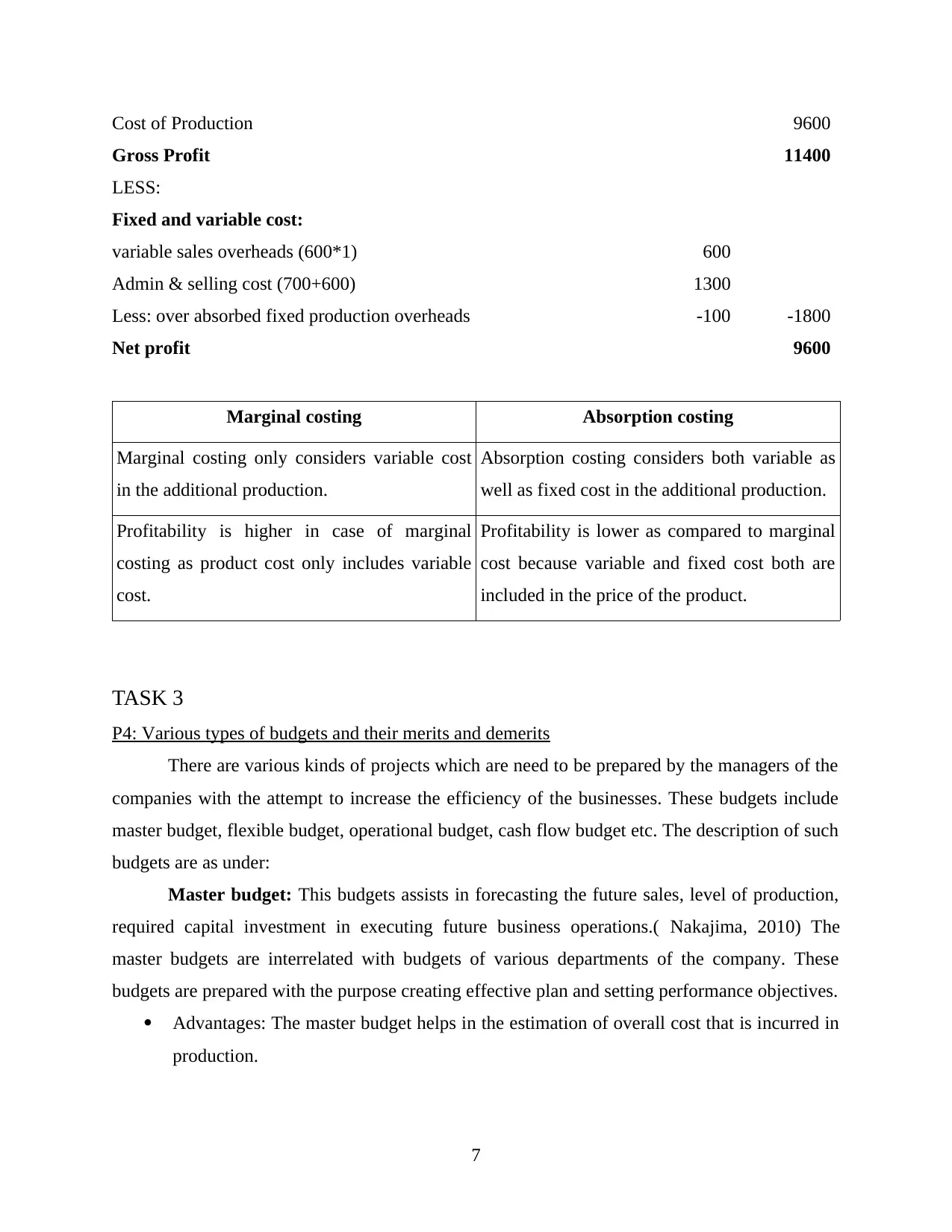

Cost of Production 9600

Gross Profit 11400

LESS:

Fixed and variable cost:

variable sales overheads (600*1) 600

Admin & selling cost (700+600) 1300

Less: over absorbed fixed production overheads -100 -1800

Net profit 9600

Marginal costing Absorption costing

Marginal costing only considers variable cost

in the additional production.

Absorption costing considers both variable as

well as fixed cost in the additional production.

Profitability is higher in case of marginal

costing as product cost only includes variable

cost.

Profitability is lower as compared to marginal

cost because variable and fixed cost both are

included in the price of the product.

TASK 3

P4: Various types of budgets and their merits and demerits

There are various kinds of projects which are need to be prepared by the managers of the

companies with the attempt to increase the efficiency of the businesses. These budgets include

master budget, flexible budget, operational budget, cash flow budget etc. The description of such

budgets are as under:

Master budget: This budgets assists in forecasting the future sales, level of production,

required capital investment in executing future business operations.( Nakajima, 2010) The

master budgets are interrelated with budgets of various departments of the company. These

budgets are prepared with the purpose creating effective plan and setting performance objectives.

Advantages: The master budget helps in the estimation of overall cost that is incurred in

production.

7

Gross Profit 11400

LESS:

Fixed and variable cost:

variable sales overheads (600*1) 600

Admin & selling cost (700+600) 1300

Less: over absorbed fixed production overheads -100 -1800

Net profit 9600

Marginal costing Absorption costing

Marginal costing only considers variable cost

in the additional production.

Absorption costing considers both variable as

well as fixed cost in the additional production.

Profitability is higher in case of marginal

costing as product cost only includes variable

cost.

Profitability is lower as compared to marginal

cost because variable and fixed cost both are

included in the price of the product.

TASK 3

P4: Various types of budgets and their merits and demerits

There are various kinds of projects which are need to be prepared by the managers of the

companies with the attempt to increase the efficiency of the businesses. These budgets include

master budget, flexible budget, operational budget, cash flow budget etc. The description of such

budgets are as under:

Master budget: This budgets assists in forecasting the future sales, level of production,

required capital investment in executing future business operations.( Nakajima, 2010) The

master budgets are interrelated with budgets of various departments of the company. These

budgets are prepared with the purpose creating effective plan and setting performance objectives.

Advantages: The master budget helps in the estimation of overall cost that is incurred in

production.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

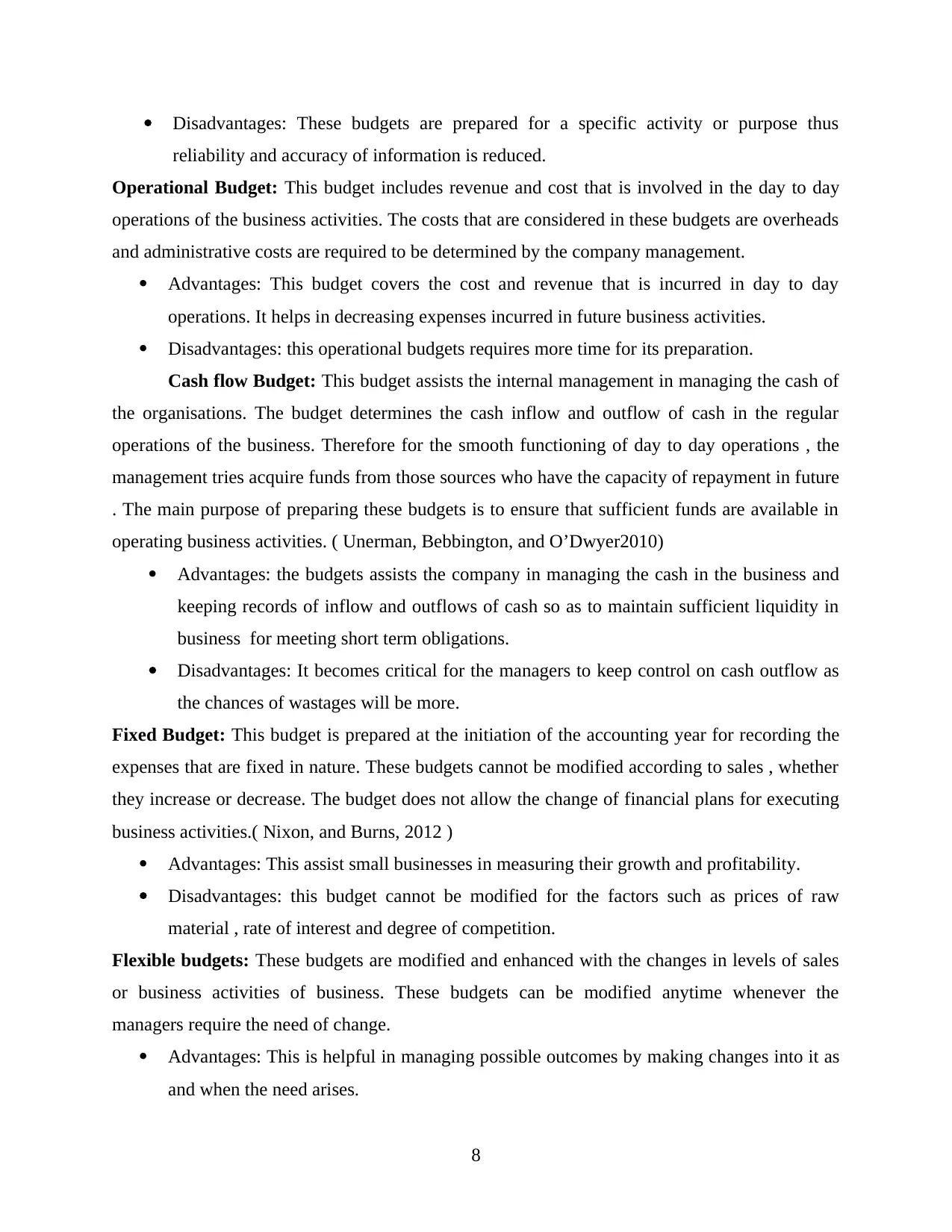

Disadvantages: These budgets are prepared for a specific activity or purpose thus

reliability and accuracy of information is reduced.

Operational Budget: This budget includes revenue and cost that is involved in the day to day

operations of the business activities. The costs that are considered in these budgets are overheads

and administrative costs are required to be determined by the company management.

Advantages: This budget covers the cost and revenue that is incurred in day to day

operations. It helps in decreasing expenses incurred in future business activities.

Disadvantages: this operational budgets requires more time for its preparation.

Cash flow Budget: This budget assists the internal management in managing the cash of

the organisations. The budget determines the cash inflow and outflow of cash in the regular

operations of the business. Therefore for the smooth functioning of day to day operations , the

management tries acquire funds from those sources who have the capacity of repayment in future

. The main purpose of preparing these budgets is to ensure that sufficient funds are available in

operating business activities. ( Unerman, Bebbington, and O’Dwyer2010)

Advantages: the budgets assists the company in managing the cash in the business and

keeping records of inflow and outflows of cash so as to maintain sufficient liquidity in

business for meeting short term obligations.

Disadvantages: It becomes critical for the managers to keep control on cash outflow as

the chances of wastages will be more.

Fixed Budget: This budget is prepared at the initiation of the accounting year for recording the

expenses that are fixed in nature. These budgets cannot be modified according to sales , whether

they increase or decrease. The budget does not allow the change of financial plans for executing

business activities.( Nixon, and Burns, 2012 )

Advantages: This assist small businesses in measuring their growth and profitability.

Disadvantages: this budget cannot be modified for the factors such as prices of raw

material , rate of interest and degree of competition.

Flexible budgets: These budgets are modified and enhanced with the changes in levels of sales

or business activities of business. These budgets can be modified anytime whenever the

managers require the need of change.

Advantages: This is helpful in managing possible outcomes by making changes into it as

and when the need arises.

8

reliability and accuracy of information is reduced.

Operational Budget: This budget includes revenue and cost that is involved in the day to day

operations of the business activities. The costs that are considered in these budgets are overheads

and administrative costs are required to be determined by the company management.

Advantages: This budget covers the cost and revenue that is incurred in day to day

operations. It helps in decreasing expenses incurred in future business activities.

Disadvantages: this operational budgets requires more time for its preparation.

Cash flow Budget: This budget assists the internal management in managing the cash of

the organisations. The budget determines the cash inflow and outflow of cash in the regular

operations of the business. Therefore for the smooth functioning of day to day operations , the

management tries acquire funds from those sources who have the capacity of repayment in future

. The main purpose of preparing these budgets is to ensure that sufficient funds are available in

operating business activities. ( Unerman, Bebbington, and O’Dwyer2010)

Advantages: the budgets assists the company in managing the cash in the business and

keeping records of inflow and outflows of cash so as to maintain sufficient liquidity in

business for meeting short term obligations.

Disadvantages: It becomes critical for the managers to keep control on cash outflow as

the chances of wastages will be more.

Fixed Budget: This budget is prepared at the initiation of the accounting year for recording the

expenses that are fixed in nature. These budgets cannot be modified according to sales , whether

they increase or decrease. The budget does not allow the change of financial plans for executing

business activities.( Nixon, and Burns, 2012 )

Advantages: This assist small businesses in measuring their growth and profitability.

Disadvantages: this budget cannot be modified for the factors such as prices of raw

material , rate of interest and degree of competition.

Flexible budgets: These budgets are modified and enhanced with the changes in levels of sales

or business activities of business. These budgets can be modified anytime whenever the

managers require the need of change.

Advantages: This is helpful in managing possible outcomes by making changes into it as

and when the need arises.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

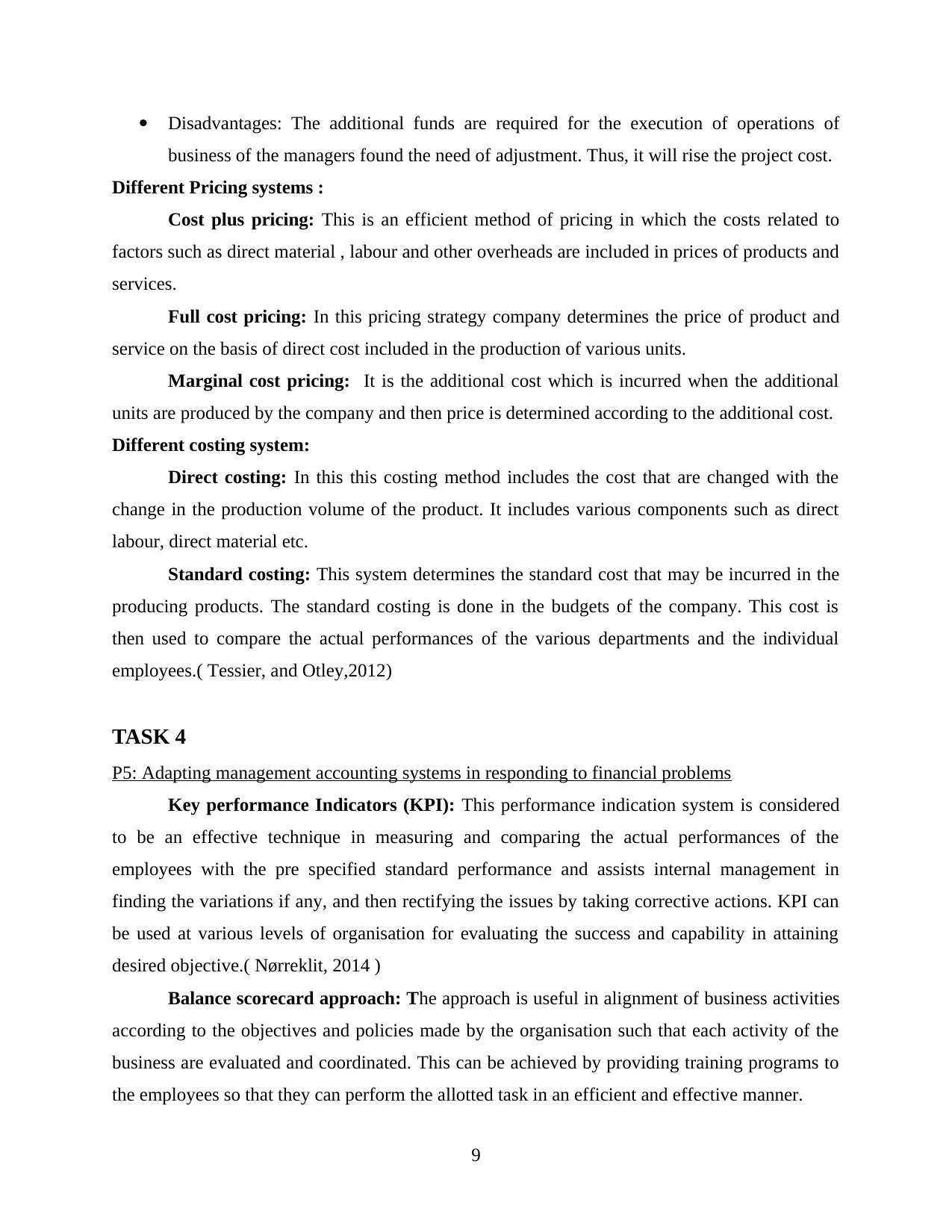

Disadvantages: The additional funds are required for the execution of operations of

business of the managers found the need of adjustment. Thus, it will rise the project cost.

Different Pricing systems :

Cost plus pricing: This is an efficient method of pricing in which the costs related to

factors such as direct material , labour and other overheads are included in prices of products and

services.

Full cost pricing: In this pricing strategy company determines the price of product and

service on the basis of direct cost included in the production of various units.

Marginal cost pricing: It is the additional cost which is incurred when the additional

units are produced by the company and then price is determined according to the additional cost.

Different costing system:

Direct costing: In this this costing method includes the cost that are changed with the

change in the production volume of the product. It includes various components such as direct

labour, direct material etc.

Standard costing: This system determines the standard cost that may be incurred in the

producing products. The standard costing is done in the budgets of the company. This cost is

then used to compare the actual performances of the various departments and the individual

employees.( Tessier, and Otley,2012)

TASK 4

P5: Adapting management accounting systems in responding to financial problems

Key performance Indicators (KPI): This performance indication system is considered

to be an effective technique in measuring and comparing the actual performances of the

employees with the pre specified standard performance and assists internal management in

finding the variations if any, and then rectifying the issues by taking corrective actions. KPI can

be used at various levels of organisation for evaluating the success and capability in attaining

desired objective.( Nørreklit, 2014 )

Balance scorecard approach: The approach is useful in alignment of business activities

according to the objectives and policies made by the organisation such that each activity of the

business are evaluated and coordinated. This can be achieved by providing training programs to

the employees so that they can perform the allotted task in an efficient and effective manner.

9

business of the managers found the need of adjustment. Thus, it will rise the project cost.

Different Pricing systems :

Cost plus pricing: This is an efficient method of pricing in which the costs related to

factors such as direct material , labour and other overheads are included in prices of products and

services.

Full cost pricing: In this pricing strategy company determines the price of product and

service on the basis of direct cost included in the production of various units.

Marginal cost pricing: It is the additional cost which is incurred when the additional

units are produced by the company and then price is determined according to the additional cost.

Different costing system:

Direct costing: In this this costing method includes the cost that are changed with the

change in the production volume of the product. It includes various components such as direct

labour, direct material etc.

Standard costing: This system determines the standard cost that may be incurred in the

producing products. The standard costing is done in the budgets of the company. This cost is

then used to compare the actual performances of the various departments and the individual

employees.( Tessier, and Otley,2012)

TASK 4

P5: Adapting management accounting systems in responding to financial problems

Key performance Indicators (KPI): This performance indication system is considered

to be an effective technique in measuring and comparing the actual performances of the

employees with the pre specified standard performance and assists internal management in

finding the variations if any, and then rectifying the issues by taking corrective actions. KPI can

be used at various levels of organisation for evaluating the success and capability in attaining

desired objective.( Nørreklit, 2014 )

Balance scorecard approach: The approach is useful in alignment of business activities

according to the objectives and policies made by the organisation such that each activity of the

business are evaluated and coordinated. This can be achieved by providing training programs to

the employees so that they can perform the allotted task in an efficient and effective manner.

9

The perspective of balance card approach are discussed below:

Financial: The main purpose of any business entity is to attain a strong financial position

in the market , and this can be possible only when the funds are allocated to profitable projects

are it is utilised efficiently.

Customers and stakeholders: The duty of every business is to provide good quality

product and services to the customers and increasing the wealth of the shareholders of the

company.( Quagli, 2011 )

CONCLUSION

It has been concluded by the above research on the project management accounting , that this

form of accounting is very important for providing necessary information to the internal

management so that they can make decisions and formulate better policies that are in relation

with the trends of the market. This project report discusses about various management

accounting reports such as budget reports , accounts receivable report which helps the companies

in managing the operations and increasing the profitability of the organisation. The use of

marginal and absorption costing in formations of statement of profit and loss. And at the end

discussion about tools that helps in responding to financial problems such as key performance

indicator and balance scorecard approach to prevent financial problems.

10

Financial: The main purpose of any business entity is to attain a strong financial position

in the market , and this can be possible only when the funds are allocated to profitable projects

are it is utilised efficiently.

Customers and stakeholders: The duty of every business is to provide good quality

product and services to the customers and increasing the wealth of the shareholders of the

company.( Quagli, 2011 )

CONCLUSION

It has been concluded by the above research on the project management accounting , that this

form of accounting is very important for providing necessary information to the internal

management so that they can make decisions and formulate better policies that are in relation

with the trends of the market. This project report discusses about various management

accounting reports such as budget reports , accounts receivable report which helps the companies

in managing the operations and increasing the profitability of the organisation. The use of

marginal and absorption costing in formations of statement of profit and loss. And at the end

discussion about tools that helps in responding to financial problems such as key performance

indicator and balance scorecard approach to prevent financial problems.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.