Management Accounting Report: Cost Analysis and Budgeting, Sept

VerifiedAdded on 2020/07/23

|20

|6081

|292

Report

AI Summary

This report on management accounting analyzes the costs incurred by Jeffrey & Son's Ltd. It begins with categorizing various types of costs and calculating unit costs using different costing methods, including job costing and absorption costing. The report then delves into cost analysis, focusing on exquisite costs and preparing a cost report for the month of September. Performance indicators are used to identify areas for improvement, and options to reduce costs and enhance value are suggested. The report also covers the purpose and nature of the budgeting process, selecting appropriate budgeting methods, preparing budgets, and creating a cash budget. Furthermore, the report includes variance analysis, possible causes of variances, and recommended actions. Finally, it presents an operating statement reconciling the budget and actual results and reports the findings to management, adhering to identified responsibility centers. The report concludes with an overview of the findings and recommendations.

Management Accounting

B

7

9

?

9

6

4

C

M

a

i

!

#

B

7

9

?

9

6

4

C

M

a

i

!

#

B

7

9

?

9

6

4

C

M

a

i

!

#

B

7

9

?

9

6

4

C

M

a

i

!

#

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1: Categorise of various types of cost .....................................................................................1

1.2: Calculation of units cost through various costing method ..................................................3

1.3 Calculation of cost of exquisite by using absorption costing techniques..............................4

1.4 Analysation of Exquisite cost for Jeffrey & Son’s Ltd.........................................................6

TASK 2............................................................................................................................................6

2.1 Preparation and analysis of cost report.................................................................................6

2.2 Use of performance indicators for identify areas for potential improvements.....................8

2.3 Suggested options to reduce cost, enhancing value and quality...........................................8

TASK 3............................................................................................................................................9

P3.1: Purpose and nature of the budgeting process to the budget holders of Jeffrey and Son's

Ltd...............................................................................................................................................9

3.2: Select the appropriate budgeting methods for the organisation and its needs...................10

3.3: Preparation of budgets.......................................................................................................11

3.4: Cash budget........................................................................................................................12

TASK 4..........................................................................................................................................13

4.1 variances analysis, possible causes and recommended actions...........................................13

4.2 operating Statement reconciling budget and actual budget.................................................14

4.3 Report the findings to management in accordance with identified responsibility centres..15

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................17

...................................................................................................................................................18

.......................................................................................................................................................18

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1: Categorise of various types of cost .....................................................................................1

1.2: Calculation of units cost through various costing method ..................................................3

1.3 Calculation of cost of exquisite by using absorption costing techniques..............................4

1.4 Analysation of Exquisite cost for Jeffrey & Son’s Ltd.........................................................6

TASK 2............................................................................................................................................6

2.1 Preparation and analysis of cost report.................................................................................6

2.2 Use of performance indicators for identify areas for potential improvements.....................8

2.3 Suggested options to reduce cost, enhancing value and quality...........................................8

TASK 3............................................................................................................................................9

P3.1: Purpose and nature of the budgeting process to the budget holders of Jeffrey and Son's

Ltd...............................................................................................................................................9

3.2: Select the appropriate budgeting methods for the organisation and its needs...................10

3.3: Preparation of budgets.......................................................................................................11

3.4: Cash budget........................................................................................................................12

TASK 4..........................................................................................................................................13

4.1 variances analysis, possible causes and recommended actions...........................................13

4.2 operating Statement reconciling budget and actual budget.................................................14

4.3 Report the findings to management in accordance with identified responsibility centres..15

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................17

...................................................................................................................................................18

.......................................................................................................................................................18

INTRODUCTION

Accounting is one of the tool of business management and operation to accomplish the

goals and objectives of organisation. This is one of the supporting factors helps to communicate

the managers and departments properly (Pärl, 2012). Basically the accounting reports are the part

of managerial accounting and helps to make strategies and plans for better operations and

formations. Business environment is changing gradually and various type of records need to

maintained by the organisation in present scenario and business environment. These records are

helpful in decision making to analyse critical sources and situations in summarised way. This

report defines the objects and motives of budgetary control, difference between management

accounting and financial accounting. Elements, functions and nature are defined in this report to

analyse the behaviour of cost classification. Different types of cost and variances analysis done

in respect of reducing cost. Purpose of budgeting process and calculation of profir by using

absorption costing techniques explained in this report.

TASK 1

1.1: Categorise of various types of cost

In every business organisation, it is necessary for the company to determine there costs

those are incur during production of product and services (Grabner and Moers, 2013). It is

known as the amount which is use by company in order to manage there business transactions.

On the other hand, plenty of expenses that are generate at time of production units. All these are

company's operating costs which are mainly known as cost. It is divided into various parts which

are based on functions, attitude behaviour and type of expenses etc.

1

Accounting is one of the tool of business management and operation to accomplish the

goals and objectives of organisation. This is one of the supporting factors helps to communicate

the managers and departments properly (Pärl, 2012). Basically the accounting reports are the part

of managerial accounting and helps to make strategies and plans for better operations and

formations. Business environment is changing gradually and various type of records need to

maintained by the organisation in present scenario and business environment. These records are

helpful in decision making to analyse critical sources and situations in summarised way. This

report defines the objects and motives of budgetary control, difference between management

accounting and financial accounting. Elements, functions and nature are defined in this report to

analyse the behaviour of cost classification. Different types of cost and variances analysis done

in respect of reducing cost. Purpose of budgeting process and calculation of profir by using

absorption costing techniques explained in this report.

TASK 1

1.1: Categorise of various types of cost

In every business organisation, it is necessary for the company to determine there costs

those are incur during production of product and services (Grabner and Moers, 2013). It is

known as the amount which is use by company in order to manage there business transactions.

On the other hand, plenty of expenses that are generate at time of production units. All these are

company's operating costs which are mainly known as cost. It is divided into various parts which

are based on functions, attitude behaviour and type of expenses etc.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

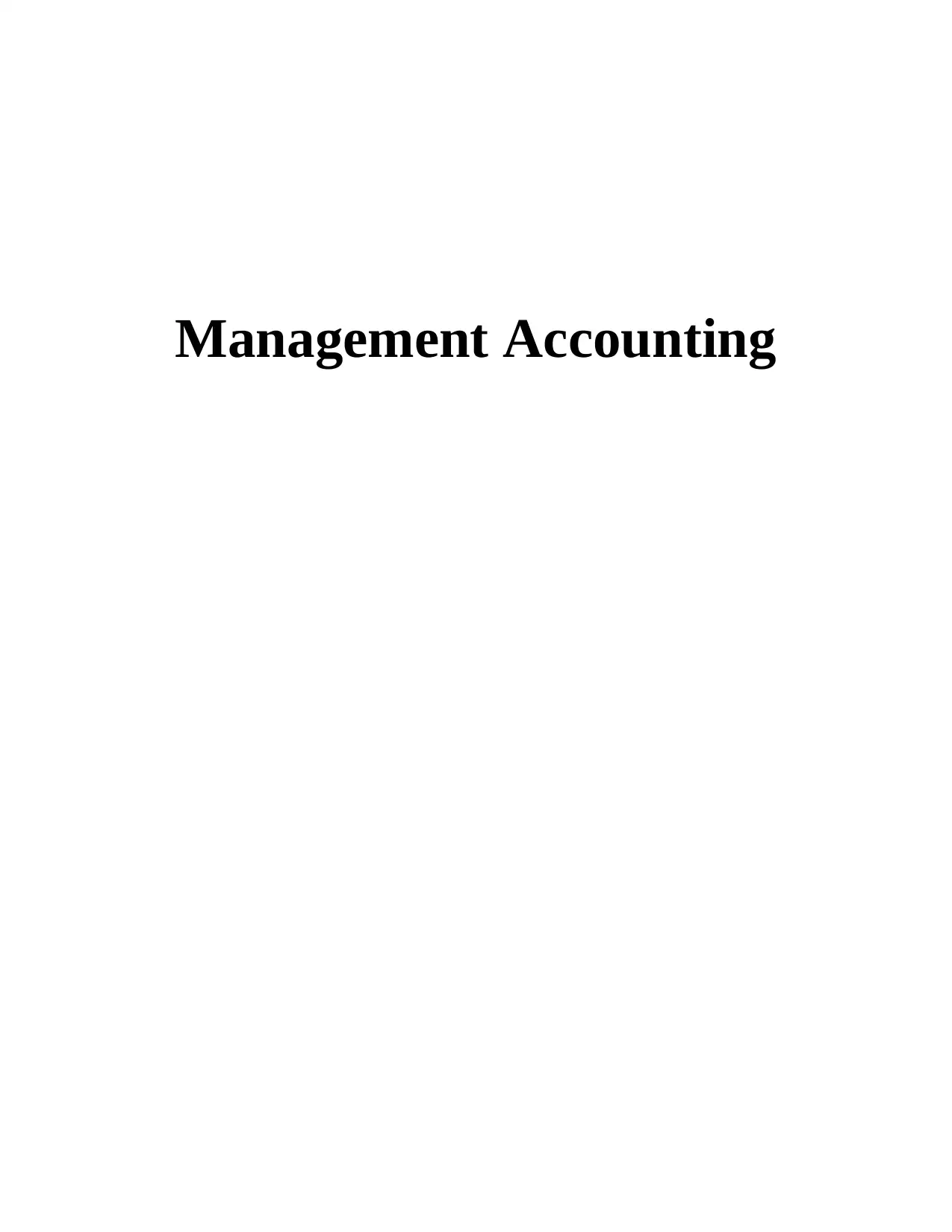

Illustration 1: Different types of costs

(Source: Elements of Costs, 2012)

Element: Some of the key component of costs such as material, labour and expenses. All

these are more vital for the company take necessary decision regarding coming aims and

objectives. Material is an essential aspects which is considered by project managers in

formulation of finish goods. Whereas, labour cost is related with expenses that are made on

human power those engage in production process (Lennox, Francis and Wang, 2011). Moreover,

all expenses collected during the manufacturing of products and services are considered as

important part of cost.

Nature of expenses: It has been seen that most manufacturing company's are paying

wages to labour forces. In order to make effectively completion of projects the company need to

have proper skill and capability in labours. Hence, salaries and remuneration is require to have

knowledge and ability to labour and have to pay according to their performance.

Function: There are various department that are been carried out by an organisation.

Thus, every department incur certain individual costs which are affecting performances of a firm.

According to the functions, some costs is divided into as selling cost, selling and distribution

costs.

Behaviour: It is based on production volume of the company. These are termed as those

costs that consists of total volume and units of manufacturing. It is primarily depend upon market

2

(Source: Elements of Costs, 2012)

Element: Some of the key component of costs such as material, labour and expenses. All

these are more vital for the company take necessary decision regarding coming aims and

objectives. Material is an essential aspects which is considered by project managers in

formulation of finish goods. Whereas, labour cost is related with expenses that are made on

human power those engage in production process (Lennox, Francis and Wang, 2011). Moreover,

all expenses collected during the manufacturing of products and services are considered as

important part of cost.

Nature of expenses: It has been seen that most manufacturing company's are paying

wages to labour forces. In order to make effectively completion of projects the company need to

have proper skill and capability in labours. Hence, salaries and remuneration is require to have

knowledge and ability to labour and have to pay according to their performance.

Function: There are various department that are been carried out by an organisation.

Thus, every department incur certain individual costs which are affecting performances of a firm.

According to the functions, some costs is divided into as selling cost, selling and distribution

costs.

Behaviour: It is based on production volume of the company. These are termed as those

costs that consists of total volume and units of manufacturing. It is primarily depend upon market

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

demand and other external factors those are affecting the performance and growth of the

company. It include fixed, variable and semi-variable costs. The cost of material is perfect

example as it did not remain same for very long time.

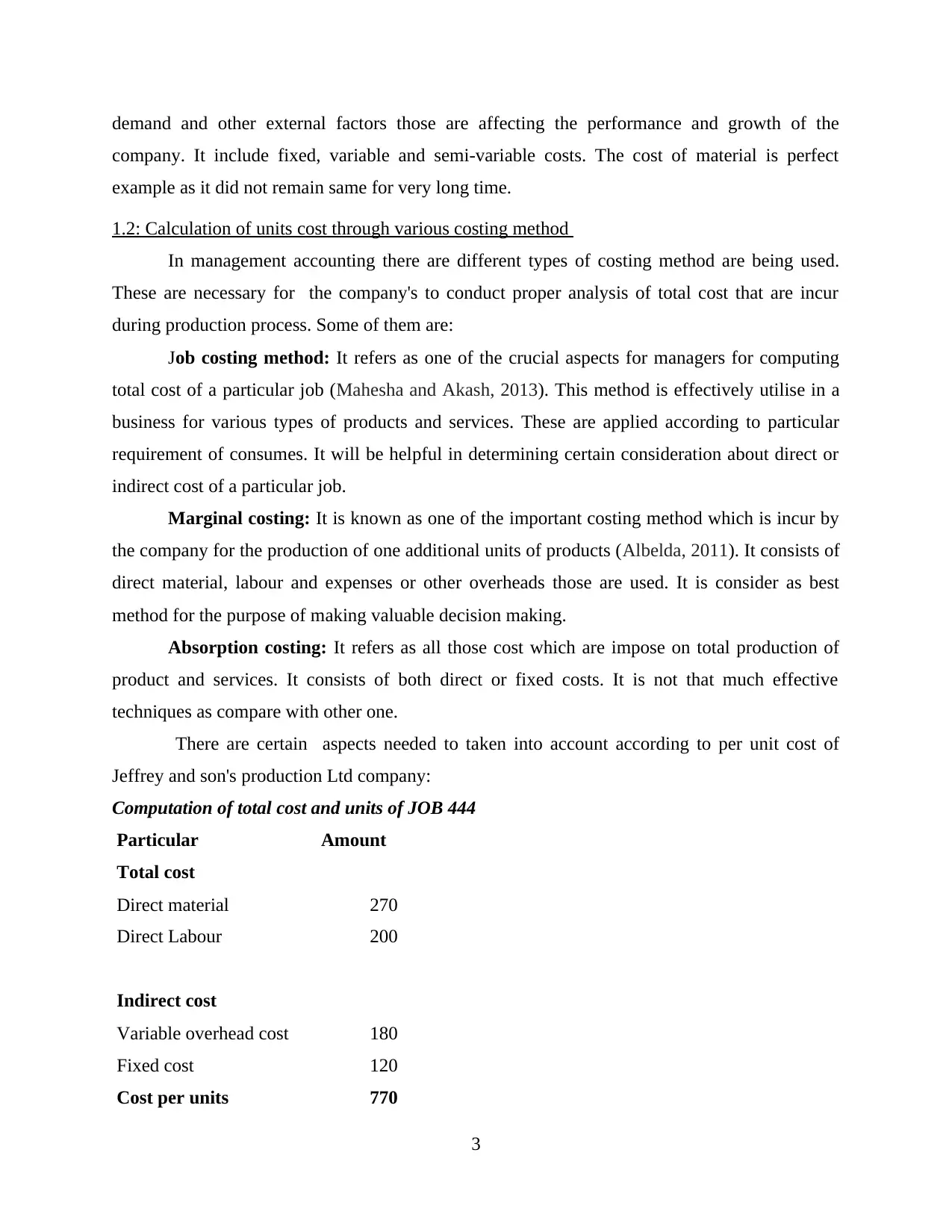

1.2: Calculation of units cost through various costing method

In management accounting there are different types of costing method are being used.

These are necessary for the company's to conduct proper analysis of total cost that are incur

during production process. Some of them are:

Job costing method: It refers as one of the crucial aspects for managers for computing

total cost of a particular job (Mahesha and Akash, 2013). This method is effectively utilise in a

business for various types of products and services. These are applied according to particular

requirement of consumes. It will be helpful in determining certain consideration about direct or

indirect cost of a particular job.

Marginal costing: It is known as one of the important costing method which is incur by

the company for the production of one additional units of products (Albelda, 2011). It consists of

direct material, labour and expenses or other overheads those are used. It is consider as best

method for the purpose of making valuable decision making.

Absorption costing: It refers as all those cost which are impose on total production of

product and services. It consists of both direct or fixed costs. It is not that much effective

techniques as compare with other one.

There are certain aspects needed to taken into account according to per unit cost of

Jeffrey and son's production Ltd company:

Computation of total cost and units of JOB 444

Particular Amount

Total cost

Direct material 270

Direct Labour 200

Indirect cost

Variable overhead cost 180

Fixed cost 120

Cost per units 770

3

company. It include fixed, variable and semi-variable costs. The cost of material is perfect

example as it did not remain same for very long time.

1.2: Calculation of units cost through various costing method

In management accounting there are different types of costing method are being used.

These are necessary for the company's to conduct proper analysis of total cost that are incur

during production process. Some of them are:

Job costing method: It refers as one of the crucial aspects for managers for computing

total cost of a particular job (Mahesha and Akash, 2013). This method is effectively utilise in a

business for various types of products and services. These are applied according to particular

requirement of consumes. It will be helpful in determining certain consideration about direct or

indirect cost of a particular job.

Marginal costing: It is known as one of the important costing method which is incur by

the company for the production of one additional units of products (Albelda, 2011). It consists of

direct material, labour and expenses or other overheads those are used. It is consider as best

method for the purpose of making valuable decision making.

Absorption costing: It refers as all those cost which are impose on total production of

product and services. It consists of both direct or fixed costs. It is not that much effective

techniques as compare with other one.

There are certain aspects needed to taken into account according to per unit cost of

Jeffrey and son's production Ltd company:

Computation of total cost and units of JOB 444

Particular Amount

Total cost

Direct material 270

Direct Labour 200

Indirect cost

Variable overhead cost 180

Fixed cost 120

Cost per units 770

3

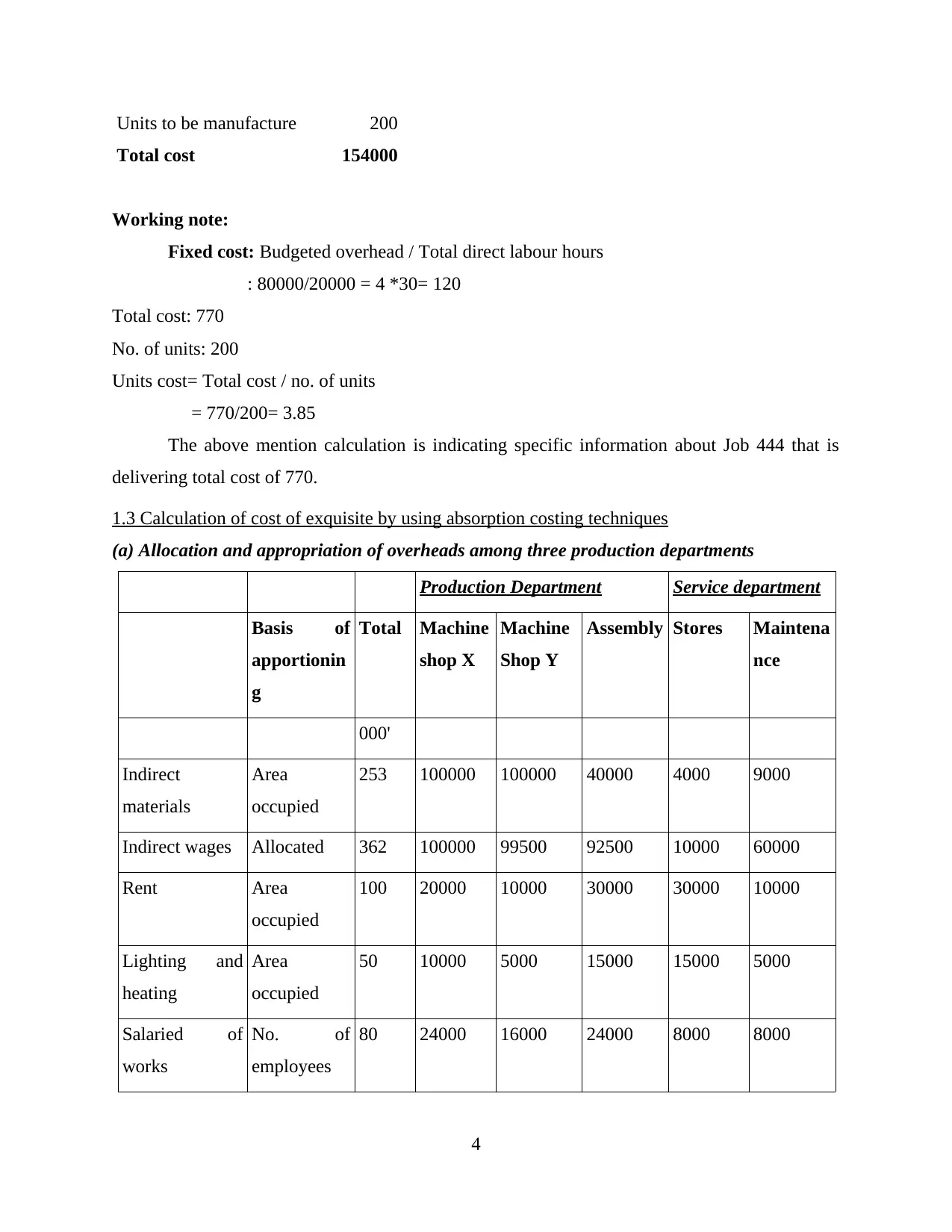

Units to be manufacture 200

Total cost 154000

Working note:

Fixed cost: Budgeted overhead / Total direct labour hours

: 80000/20000 = 4 *30= 120

Total cost: 770

No. of units: 200

Units cost= Total cost / no. of units

= 770/200= 3.85

The above mention calculation is indicating specific information about Job 444 that is

delivering total cost of 770.

1.3 Calculation of cost of exquisite by using absorption costing techniques

(a) Allocation and appropriation of overheads among three production departments

Production Department Service department

Basis of

apportionin

g

Total Machine

shop X

Machine

Shop Y

Assembly Stores Maintena

nce

000'

Indirect

materials

Area

occupied

253 100000 100000 40000 4000 9000

Indirect wages Allocated 362 100000 99500 92500 10000 60000

Rent Area

occupied

100 20000 10000 30000 30000 10000

Lighting and

heating

Area

occupied

50 10000 5000 15000 15000 5000

Salaried of

works

No. of

employees

80 24000 16000 24000 8000 8000

4

Total cost 154000

Working note:

Fixed cost: Budgeted overhead / Total direct labour hours

: 80000/20000 = 4 *30= 120

Total cost: 770

No. of units: 200

Units cost= Total cost / no. of units

= 770/200= 3.85

The above mention calculation is indicating specific information about Job 444 that is

delivering total cost of 770.

1.3 Calculation of cost of exquisite by using absorption costing techniques

(a) Allocation and appropriation of overheads among three production departments

Production Department Service department

Basis of

apportionin

g

Total Machine

shop X

Machine

Shop Y

Assembly Stores Maintena

nce

000'

Indirect

materials

Area

occupied

253 100000 100000 40000 4000 9000

Indirect wages Allocated 362 100000 99500 92500 10000 60000

Rent Area

occupied

100 20000 10000 30000 30000 10000

Lighting and

heating

Area

occupied

50 10000 5000 15000 15000 5000

Salaried of

works

No. of

employees

80 24000 16000 24000 8000 8000

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Insurance of

building

Area

occupied

25 5000 2500 7500 7500 2500

Insurance and

machinery

Book value

of

machinery

15 7947 4967 993 497 596

Depreciation of

machinery

Book value

of

machinery

150 79470 49669 9934 4967 5960

Sub totals 1035 346417 287636 219927 79964 101056

Maintenance 48507 32338 20211 -101056

Stores

departments

39982 29987 9995 -79964

Totals 434906 349961 250133 0 0

Allocation of overheads and cost are based upon the ratios. There are major three parts

are defined in this report. Fixed overheads are as depreciation allocated in book value of

machinery. Indirect wages and material cost are allocated as per area occupied by the machine X

and Y. Rent, lightning and heating, salaries are allocated as per the area occupied by the

machines. Insurance of machinery and depreciation are charged in respect of book value of

machinary.

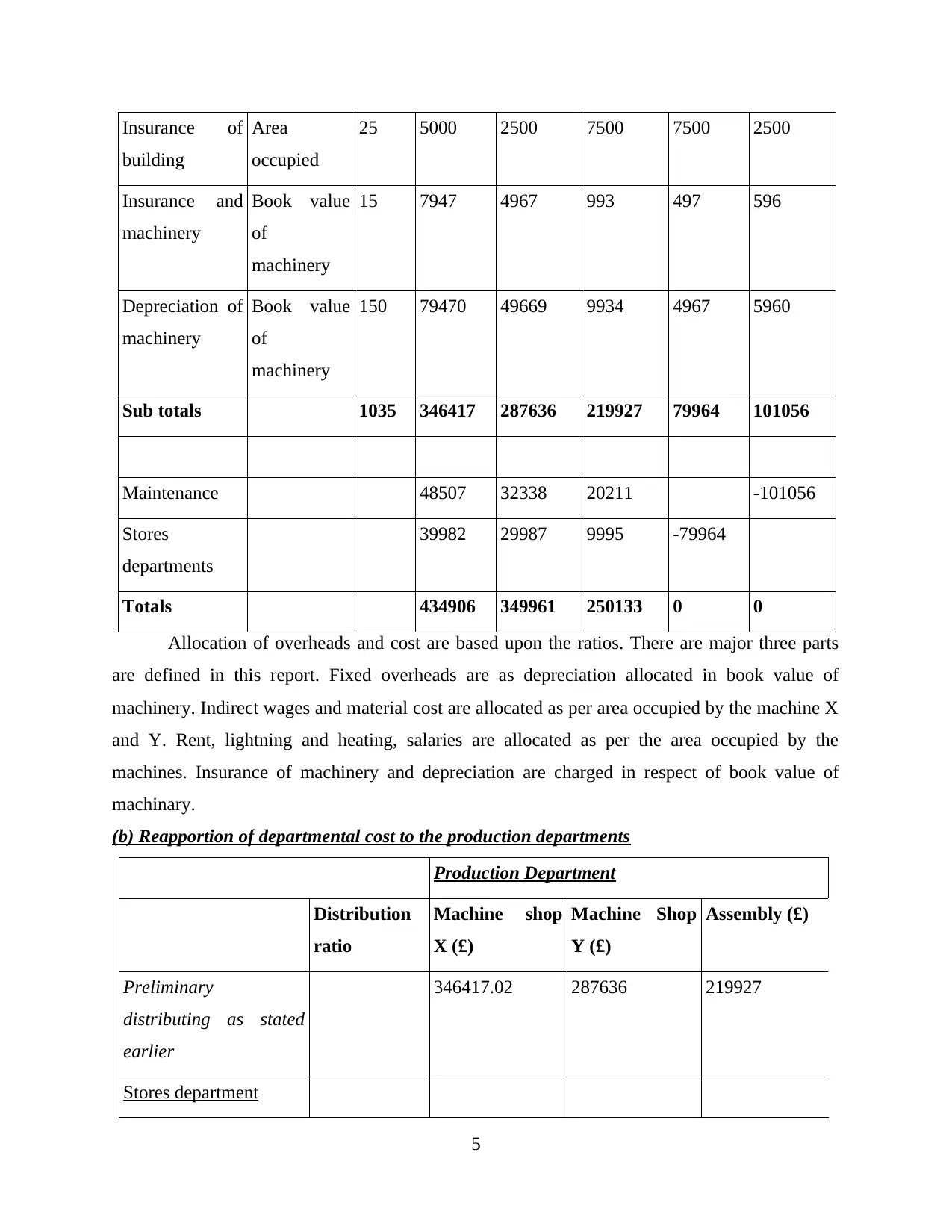

(b) Reapportion of departmental cost to the production departments

Production Department

Distribution

ratio

Machine shop

X (£)

Machine Shop

Y (£)

Assembly (£)

Preliminary

distributing as stated

earlier

346417.02 287636 219927

Stores department

5

building

Area

occupied

25 5000 2500 7500 7500 2500

Insurance and

machinery

Book value

of

machinery

15 7947 4967 993 497 596

Depreciation of

machinery

Book value

of

machinery

150 79470 49669 9934 4967 5960

Sub totals 1035 346417 287636 219927 79964 101056

Maintenance 48507 32338 20211 -101056

Stores

departments

39982 29987 9995 -79964

Totals 434906 349961 250133 0 0

Allocation of overheads and cost are based upon the ratios. There are major three parts

are defined in this report. Fixed overheads are as depreciation allocated in book value of

machinery. Indirect wages and material cost are allocated as per area occupied by the machine X

and Y. Rent, lightning and heating, salaries are allocated as per the area occupied by the

machines. Insurance of machinery and depreciation are charged in respect of book value of

machinary.

(b) Reapportion of departmental cost to the production departments

Production Department

Distribution

ratio

Machine shop

X (£)

Machine Shop

Y (£)

Assembly (£)

Preliminary

distributing as stated

earlier

346417.02 287636 219927

Stores department

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Direct material [4:3:1] 39982 29987 9995

Maintenance

Department

Maintenance machine

hours

[12:8:5] 48506.88 32377.92 20211.2

Total 434905.9 349960.92 250133.2

(c) reduction of overhead absorption rates for each of the production department X,Y and

assembly

This allocation remain divided in three steps

First step: Allocation of available cost among production department

formula = total cost / machine hours on particular shop

Department Total cost Machine hours Calculation Results

Dept. X £434,906 80,000 hours £434,906/80,000 hours £5.83/hours

Dept. Y £349,959 60,000 hours £349,959/60,000 hours £5.44/hours

Assembly Dept. £250,133.47 10,000 hours £250,133.47/10,000 hours £25.01/hours

Second step: Allocation of service cost among manufacturing department

Overheads are calculated below

Production department Overhead rates

Machine Shop X £5.83/Hr.

Machine Shop Y £5.44/Hr.

Assembly £25.01/Hr.

Third step: Allocation of manufacturing department cost as per machine hours and absorption

of overheads

1.4 Analysation of Exquisite cost for Jeffrey & Son’s Ltd

Below are the rates given in respect of production departments of company.

Particulars Calculation Cost

Direct material £8

Labour £15

6

Maintenance

Department

Maintenance machine

hours

[12:8:5] 48506.88 32377.92 20211.2

Total 434905.9 349960.92 250133.2

(c) reduction of overhead absorption rates for each of the production department X,Y and

assembly

This allocation remain divided in three steps

First step: Allocation of available cost among production department

formula = total cost / machine hours on particular shop

Department Total cost Machine hours Calculation Results

Dept. X £434,906 80,000 hours £434,906/80,000 hours £5.83/hours

Dept. Y £349,959 60,000 hours £349,959/60,000 hours £5.44/hours

Assembly Dept. £250,133.47 10,000 hours £250,133.47/10,000 hours £25.01/hours

Second step: Allocation of service cost among manufacturing department

Overheads are calculated below

Production department Overhead rates

Machine Shop X £5.83/Hr.

Machine Shop Y £5.44/Hr.

Assembly £25.01/Hr.

Third step: Allocation of manufacturing department cost as per machine hours and absorption

of overheads

1.4 Analysation of Exquisite cost for Jeffrey & Son’s Ltd

Below are the rates given in respect of production departments of company.

Particulars Calculation Cost

Direct material £8

Labour £15

6

Overheads: Machine shop X £2.17*2 £4

Machine shop Y £2.33*1.5 £3.50

Assembly Department £1.25*1 £1.25

Total £32.09

Analysis

As per the analysis the cost of per production is calculated and overall cost is measured

£32.09. as per above analysis there of absorption cost in respect of machine hours production

hours are divided on machine shop X £5.83/hr., machine shop Y £5.44/hr. and assembly

department £25.01/hr.

TASK 2

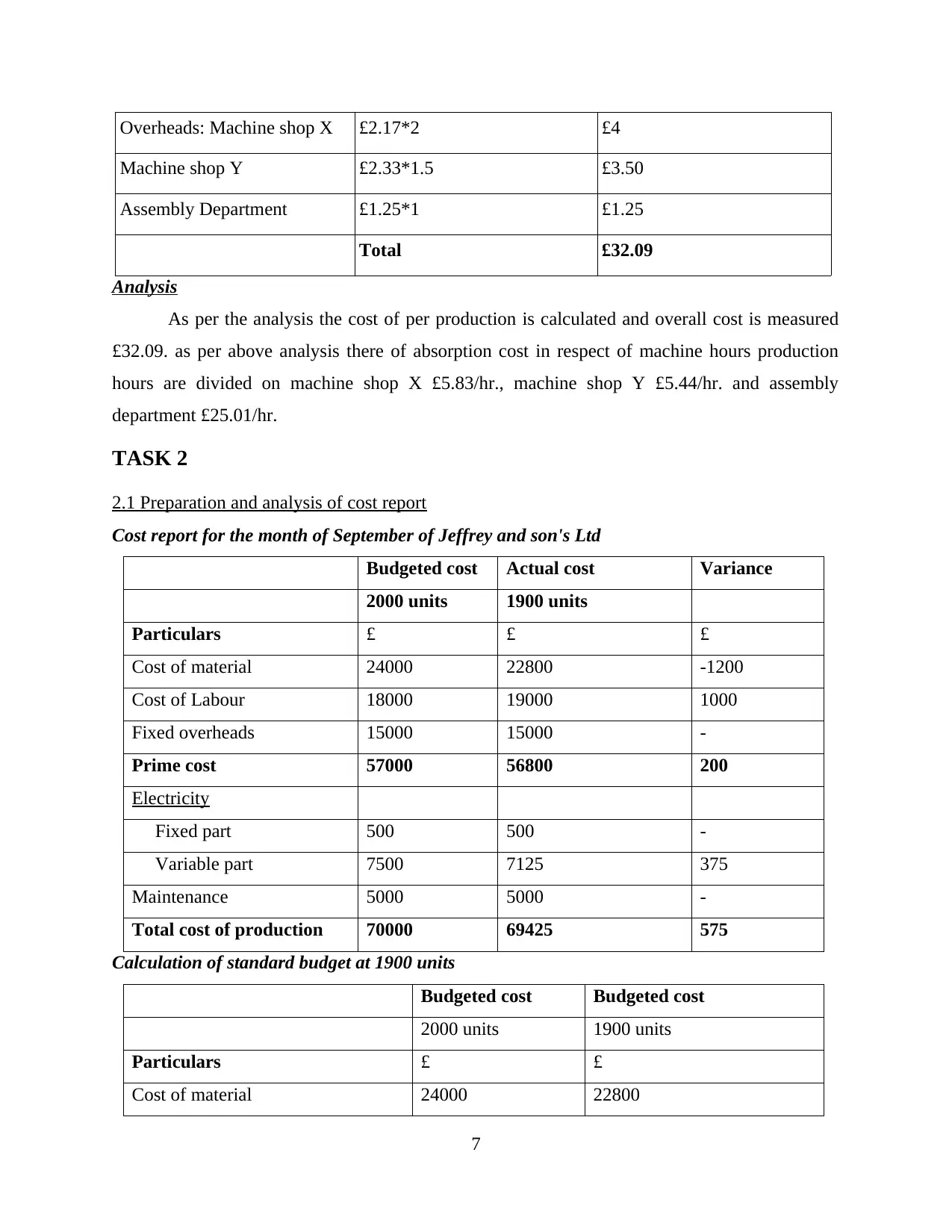

2.1 Preparation and analysis of cost report

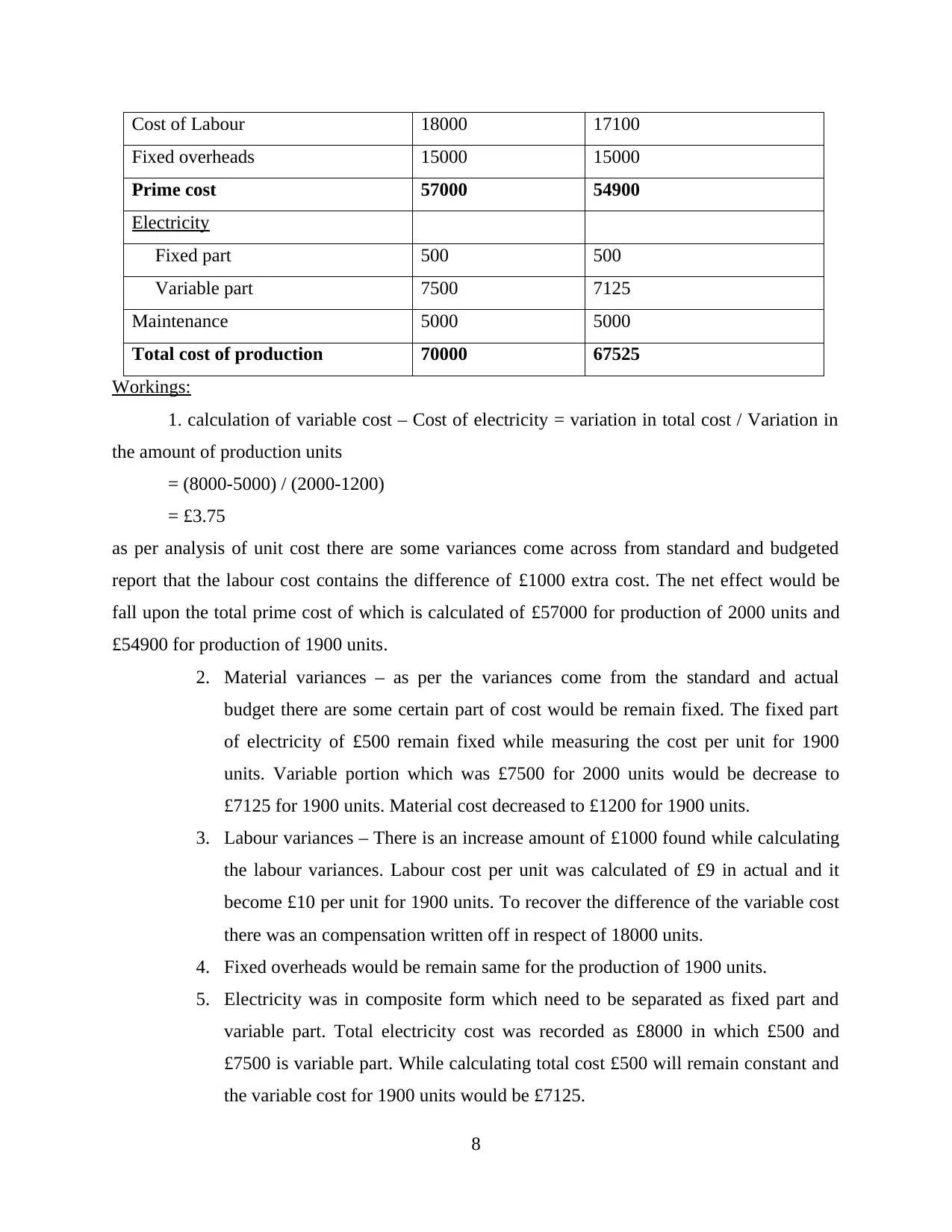

Cost report for the month of September of Jeffrey and son's Ltd

Budgeted cost Actual cost Variance

2000 units 1900 units

Particulars £ £ £

Cost of material 24000 22800 -1200

Cost of Labour 18000 19000 1000

Fixed overheads 15000 15000 -

Prime cost 57000 56800 200

Electricity

Fixed part 500 500 -

Variable part 7500 7125 375

Maintenance 5000 5000 -

Total cost of production 70000 69425 575

Calculation of standard budget at 1900 units

Budgeted cost Budgeted cost

2000 units 1900 units

Particulars £ £

Cost of material 24000 22800

7

Machine shop Y £2.33*1.5 £3.50

Assembly Department £1.25*1 £1.25

Total £32.09

Analysis

As per the analysis the cost of per production is calculated and overall cost is measured

£32.09. as per above analysis there of absorption cost in respect of machine hours production

hours are divided on machine shop X £5.83/hr., machine shop Y £5.44/hr. and assembly

department £25.01/hr.

TASK 2

2.1 Preparation and analysis of cost report

Cost report for the month of September of Jeffrey and son's Ltd

Budgeted cost Actual cost Variance

2000 units 1900 units

Particulars £ £ £

Cost of material 24000 22800 -1200

Cost of Labour 18000 19000 1000

Fixed overheads 15000 15000 -

Prime cost 57000 56800 200

Electricity

Fixed part 500 500 -

Variable part 7500 7125 375

Maintenance 5000 5000 -

Total cost of production 70000 69425 575

Calculation of standard budget at 1900 units

Budgeted cost Budgeted cost

2000 units 1900 units

Particulars £ £

Cost of material 24000 22800

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost of Labour 18000 17100

Fixed overheads 15000 15000

Prime cost 57000 54900

Electricity

Fixed part 500 500

Variable part 7500 7125

Maintenance 5000 5000

Total cost of production 70000 67525

Workings:

1. calculation of variable cost – Cost of electricity = variation in total cost / Variation in

the amount of production units

= (8000-5000) / (2000-1200)

= £3.75

as per analysis of unit cost there are some variances come across from standard and budgeted

report that the labour cost contains the difference of £1000 extra cost. The net effect would be

fall upon the total prime cost of which is calculated of £57000 for production of 2000 units and

£54900 for production of 1900 units.

2. Material variances – as per the variances come from the standard and actual

budget there are some certain part of cost would be remain fixed. The fixed part

of electricity of £500 remain fixed while measuring the cost per unit for 1900

units. Variable portion which was £7500 for 2000 units would be decrease to

£7125 for 1900 units. Material cost decreased to £1200 for 1900 units.

3. Labour variances – There is an increase amount of £1000 found while calculating

the labour variances. Labour cost per unit was calculated of £9 in actual and it

become £10 per unit for 1900 units. To recover the difference of the variable cost

there was an compensation written off in respect of 18000 units.

4. Fixed overheads would be remain same for the production of 1900 units.

5. Electricity was in composite form which need to be separated as fixed part and

variable part. Total electricity cost was recorded as £8000 in which £500 and

£7500 is variable part. While calculating total cost £500 will remain constant and

the variable cost for 1900 units would be £7125.

8

Fixed overheads 15000 15000

Prime cost 57000 54900

Electricity

Fixed part 500 500

Variable part 7500 7125

Maintenance 5000 5000

Total cost of production 70000 67525

Workings:

1. calculation of variable cost – Cost of electricity = variation in total cost / Variation in

the amount of production units

= (8000-5000) / (2000-1200)

= £3.75

as per analysis of unit cost there are some variances come across from standard and budgeted

report that the labour cost contains the difference of £1000 extra cost. The net effect would be

fall upon the total prime cost of which is calculated of £57000 for production of 2000 units and

£54900 for production of 1900 units.

2. Material variances – as per the variances come from the standard and actual

budget there are some certain part of cost would be remain fixed. The fixed part

of electricity of £500 remain fixed while measuring the cost per unit for 1900

units. Variable portion which was £7500 for 2000 units would be decrease to

£7125 for 1900 units. Material cost decreased to £1200 for 1900 units.

3. Labour variances – There is an increase amount of £1000 found while calculating

the labour variances. Labour cost per unit was calculated of £9 in actual and it

become £10 per unit for 1900 units. To recover the difference of the variable cost

there was an compensation written off in respect of 18000 units.

4. Fixed overheads would be remain same for the production of 1900 units.

5. Electricity was in composite form which need to be separated as fixed part and

variable part. Total electricity cost was recorded as £8000 in which £500 and

£7500 is variable part. While calculating total cost £500 will remain constant and

the variable cost for 1900 units would be £7125.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2.2 Use of performance indicators for identify areas for potential improvements

As per above analysis there are some recommendations mentioned below which would be

helpful for potential investors.

Financial analysis of company indicates the level of performance and which provides the

information and supports related to improvement.

There are significant change are required in respect of controlling the cost and effective

evaluation is required.

Variable overheads and classifications are required to analyse and bifurcate the expenses

in different type of production departments.

Budgeted sales records shows the possibilities of less production due to less requirement

and demand of product (Hasniza Haron and et. al., 2013). It will effect the amount of sale

and will decrease the sales amount. Organisation need to change the policies in respect of

labour cost and variances analysation. Some of the fixed overheads in respect of

electricity and depreciations are irrelevant need to rectify and analysed in effective

manner.

2.3 Suggested options to reduce cost, enhancing value and quality

Below are some methods and tools are given in respect of reducing the cost of production

and maximise the amount of profitability.

TQM which is known as total quality management technique which would help to insure

the amount of goods and better use of improved techniques (Lachmann, Knauer and

Trapp, 2013.). This method is considered as most effective and important part in respect

of reducing the cost and maximising profit.

Company need to measure the factors and areas in respect of improve the quality of

products.

Organisation need to reduce the cost of operations and valuation of products for assets.

TASK 3

P3.1: Purpose and nature of the budgeting process to the budget holders of Jeffrey and Son's Ltd

Budget is essentially required to prepare by the top authority of company through which they can

formulate, allocate resources in important areas and direction in order to achieve efficiency in the

business activities which further help them in making effective decisions with a motive of

9

As per above analysis there are some recommendations mentioned below which would be

helpful for potential investors.

Financial analysis of company indicates the level of performance and which provides the

information and supports related to improvement.

There are significant change are required in respect of controlling the cost and effective

evaluation is required.

Variable overheads and classifications are required to analyse and bifurcate the expenses

in different type of production departments.

Budgeted sales records shows the possibilities of less production due to less requirement

and demand of product (Hasniza Haron and et. al., 2013). It will effect the amount of sale

and will decrease the sales amount. Organisation need to change the policies in respect of

labour cost and variances analysation. Some of the fixed overheads in respect of

electricity and depreciations are irrelevant need to rectify and analysed in effective

manner.

2.3 Suggested options to reduce cost, enhancing value and quality

Below are some methods and tools are given in respect of reducing the cost of production

and maximise the amount of profitability.

TQM which is known as total quality management technique which would help to insure

the amount of goods and better use of improved techniques (Lachmann, Knauer and

Trapp, 2013.). This method is considered as most effective and important part in respect

of reducing the cost and maximising profit.

Company need to measure the factors and areas in respect of improve the quality of

products.

Organisation need to reduce the cost of operations and valuation of products for assets.

TASK 3

P3.1: Purpose and nature of the budgeting process to the budget holders of Jeffrey and Son's Ltd

Budget is essentially required to prepare by the top authority of company through which they can

formulate, allocate resources in important areas and direction in order to achieve efficiency in the

business activities which further help them in making effective decisions with a motive of

9

generating huge revenue and market share in competitive market world. The management should

follow budgeting process to prepare effective budget (Lavia López and Hiebl, 2014).

The purpose of preparing budgeting process of Jeffrey and Son's Ltd: The main

purpose of setting budget is to forecast the income and expenditure that to be incurred in future

business activities. The manager also predict the complex environment which can influence and

affect the business operations so that they are prepared in advance by formulating corrective

measures in order to reduce the impact when such complex situation occurs. Preparing budgeting

process help company top analyse and evaluate the performance by comparing actual

performance with the standard performance which will bring positive result for the company. It

also helps in making optimum utilisation of resources by appointing skilled and knowledgeable

employees which can allocate available resources in those important field which can bring

positive outcome in future (Kotas, 2014). This will directly help in minimising cost and

expenditure incurred while execution of business operations. Through budgeting process the

management can effectively communicate and coordinate with all departments which help them

in performing various functions such as planning, organising, staffing, controlling and directing.

Employees feels motivated by getting effective support and motivation from the management of

company regarding their roles and responsibilities. This will help in production of company.

Nature of budgeting process: The company Jeffrey and Son's Ltd should use their

budgeting process in formulating effective decision through using pats performance data and

comparing the actual and current result in business activities which help them to identify the

changes that to be required in future business activities (Caglio and Ditillo, 2012). By taking

previous data the manager can easily forecast the income and expenditure incurred in near future

and accordingly implement effective decision in order to achieve growth and success. The

budgeting nature provide a structure of roles and responsibilities to every members in an

organisation which help them to perform well and achieve best possible result.

3.2: Select the appropriate budgeting methods for the organisation and its needs

Jeffrey and Son's Ltd need to utilize following budgeting methods in order to achieve positive

result in future business activities:

Zero based budgeting method: While following this method the management of

company need to fresh budget without utilising any previous year data as they start from zero

(Granlund, 2011). This method is mostly used by new company or firm but Jeffrey and Son's Ltd

10

follow budgeting process to prepare effective budget (Lavia López and Hiebl, 2014).

The purpose of preparing budgeting process of Jeffrey and Son's Ltd: The main

purpose of setting budget is to forecast the income and expenditure that to be incurred in future

business activities. The manager also predict the complex environment which can influence and

affect the business operations so that they are prepared in advance by formulating corrective

measures in order to reduce the impact when such complex situation occurs. Preparing budgeting

process help company top analyse and evaluate the performance by comparing actual

performance with the standard performance which will bring positive result for the company. It

also helps in making optimum utilisation of resources by appointing skilled and knowledgeable

employees which can allocate available resources in those important field which can bring

positive outcome in future (Kotas, 2014). This will directly help in minimising cost and

expenditure incurred while execution of business operations. Through budgeting process the

management can effectively communicate and coordinate with all departments which help them

in performing various functions such as planning, organising, staffing, controlling and directing.

Employees feels motivated by getting effective support and motivation from the management of

company regarding their roles and responsibilities. This will help in production of company.

Nature of budgeting process: The company Jeffrey and Son's Ltd should use their

budgeting process in formulating effective decision through using pats performance data and

comparing the actual and current result in business activities which help them to identify the

changes that to be required in future business activities (Caglio and Ditillo, 2012). By taking

previous data the manager can easily forecast the income and expenditure incurred in near future

and accordingly implement effective decision in order to achieve growth and success. The

budgeting nature provide a structure of roles and responsibilities to every members in an

organisation which help them to perform well and achieve best possible result.

3.2: Select the appropriate budgeting methods for the organisation and its needs

Jeffrey and Son's Ltd need to utilize following budgeting methods in order to achieve positive

result in future business activities:

Zero based budgeting method: While following this method the management of

company need to fresh budget without utilising any previous year data as they start from zero

(Granlund, 2011). This method is mostly used by new company or firm but Jeffrey and Son's Ltd

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.