Management Accounting Analysis: Jumper Jackfruit Company Report

VerifiedAdded on 2020/03/16

|19

|5117

|61

Report

AI Summary

This report provides a detailed analysis of management accounting principles, using the Jumper Jackfruit Company as a case study. It begins with an email discussing errors in the 2018 profit budget, including incorrect revenue calculations and understated sales figures, leading to revisions in the profit and cash flow budgets. The report examines direct material purchases, direct labor costs, and overhead budgets, highlighting the impact of these costs on overall financial performance. It then delves into cash flow management, emphasizing the importance of accurate sales figures and cost control for achieving positive operating cash flows. The report also explores the significance of analyzing financial statements such as income statements, balance sheets, and cash flow statements for informed decision-making. Additionally, the report discusses the importance of differentiation, execution, and strategic planning for business success, particularly in the context of two companies making dice, emphasizing the need for innovation, customer focus, and competitive advantage through effective strategies and continuous improvement. The report concludes by underscoring the significance of understanding market dynamics, adapting to changing circumstances, and prioritizing customer needs in order to achieve long-term business success.

Running head: MANAGEMENT ACCOUNTING 1

Management Accounting

Name:

Institution:

Date:

Management Accounting

Name:

Institution:

Date:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT ACCOUNTING 2

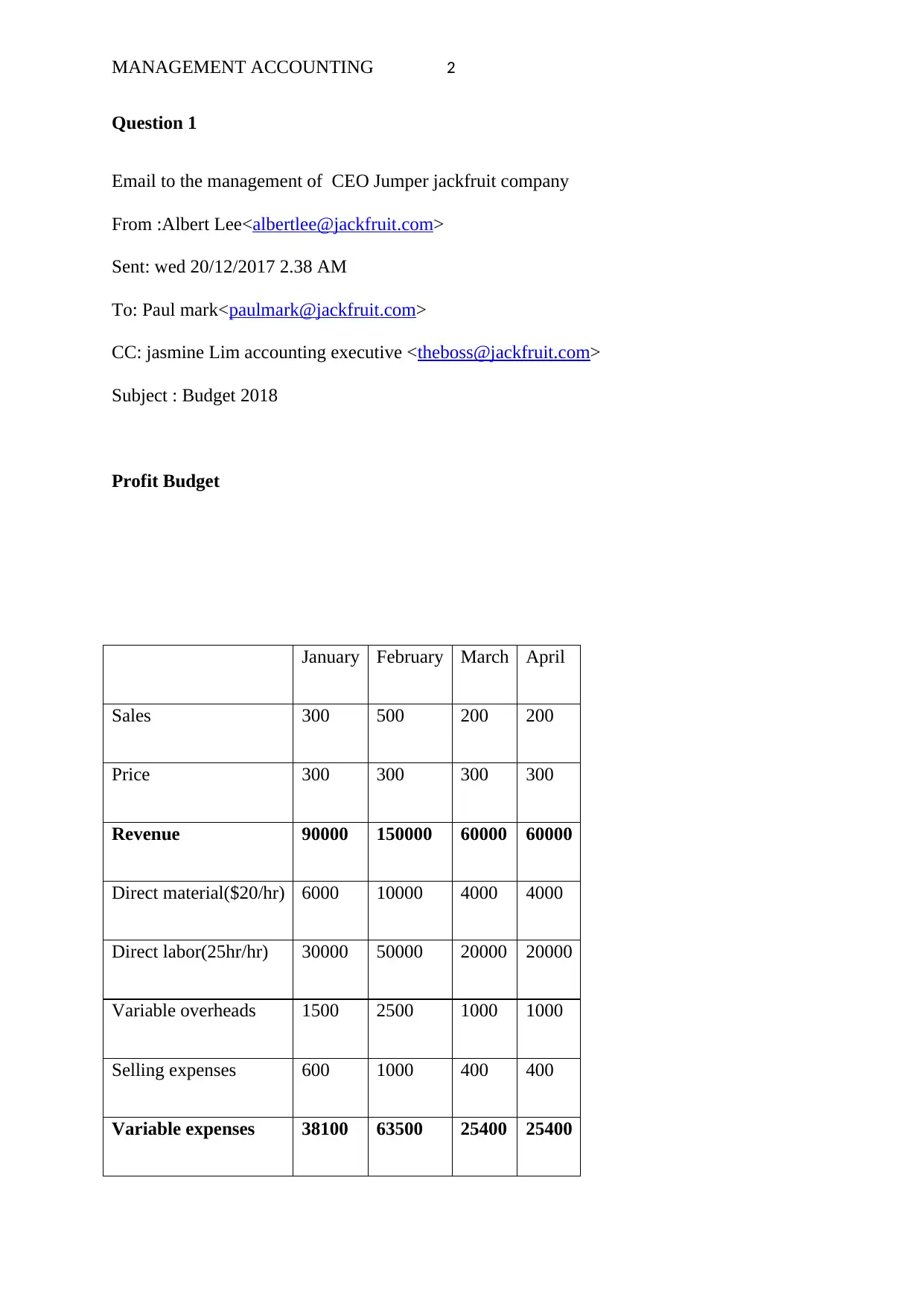

Question 1

Email to the management of CEO Jumper jackfruit company

From :Albert Lee<albertlee@jackfruit.com>

Sent: wed 20/12/2017 2.38 AM

To: Paul mark<paulmark@jackfruit.com>

CC: jasmine Lim accounting executive <theboss@jackfruit.com>

Subject : Budget 2018

Profit Budget

January February March April

Sales 300 500 200 200

Price 300 300 300 300

Revenue 90000 150000 60000 60000

Direct material($20/hr) 6000 10000 4000 4000

Direct labor(25hr/hr) 30000 50000 20000 20000

Variable overheads 1500 2500 1000 1000

Selling expenses 600 1000 400 400

Variable expenses 38100 63500 25400 25400

Question 1

Email to the management of CEO Jumper jackfruit company

From :Albert Lee<albertlee@jackfruit.com>

Sent: wed 20/12/2017 2.38 AM

To: Paul mark<paulmark@jackfruit.com>

CC: jasmine Lim accounting executive <theboss@jackfruit.com>

Subject : Budget 2018

Profit Budget

January February March April

Sales 300 500 200 200

Price 300 300 300 300

Revenue 90000 150000 60000 60000

Direct material($20/hr) 6000 10000 4000 4000

Direct labor(25hr/hr) 30000 50000 20000 20000

Variable overheads 1500 2500 1000 1000

Selling expenses 600 1000 400 400

Variable expenses 38100 63500 25400 25400

MANAGEMENT ACCOUNTING 3

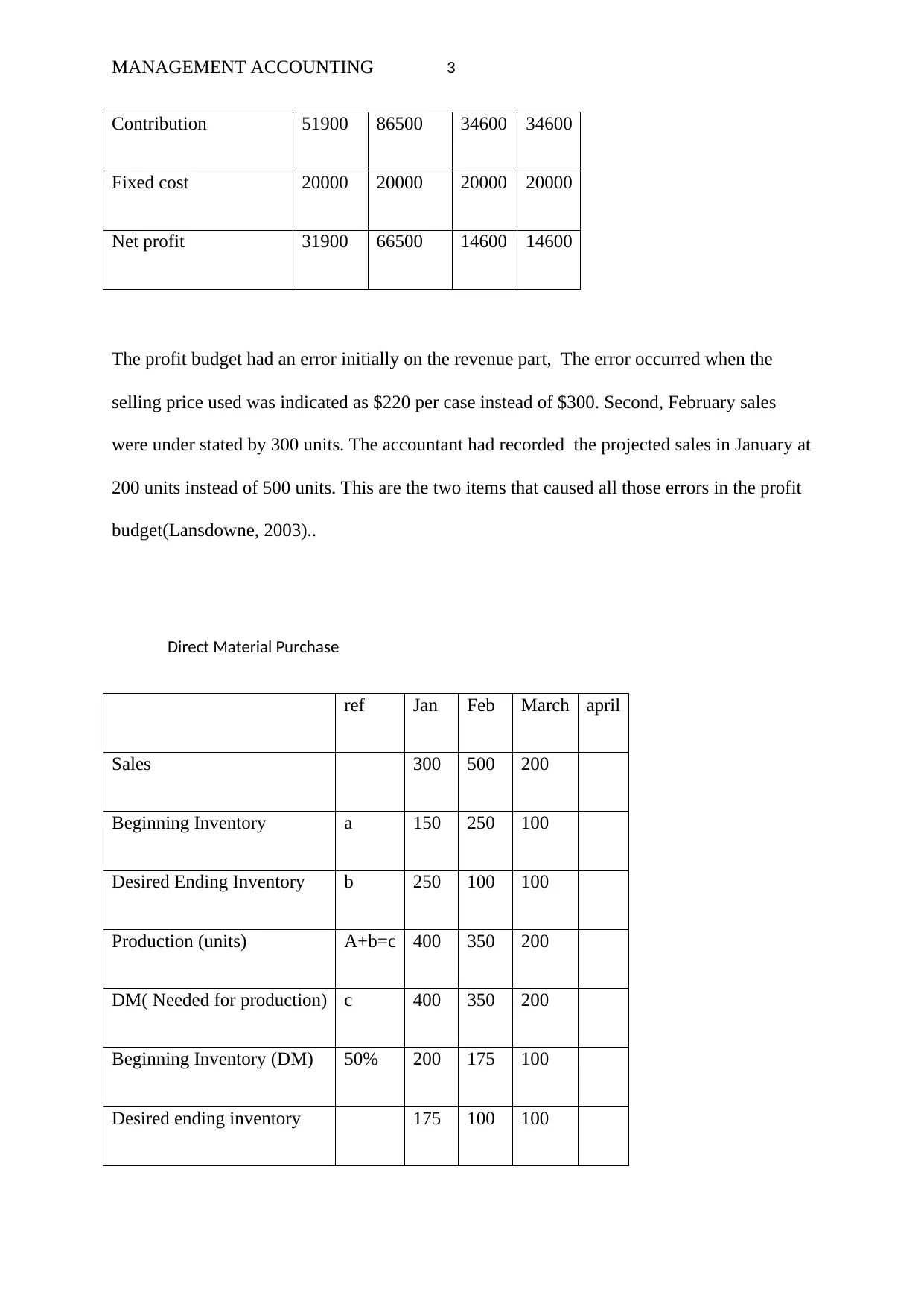

Contribution 51900 86500 34600 34600

Fixed cost 20000 20000 20000 20000

Net profit 31900 66500 14600 14600

The profit budget had an error initially on the revenue part, The error occurred when the

selling price used was indicated as $220 per case instead of $300. Second, February sales

were under stated by 300 units. The accountant had recorded the projected sales in January at

200 units instead of 500 units. This are the two items that caused all those errors in the profit

budget(Lansdowne, 2003)..

Direct Material Purchase

ref Jan Feb March april

Sales 300 500 200

Beginning Inventory a 150 250 100

Desired Ending Inventory b 250 100 100

Production (units) A+b=c 400 350 200

DM( Needed for production) c 400 350 200

Beginning Inventory (DM) 50% 200 175 100

Desired ending inventory 175 100 100

Contribution 51900 86500 34600 34600

Fixed cost 20000 20000 20000 20000

Net profit 31900 66500 14600 14600

The profit budget had an error initially on the revenue part, The error occurred when the

selling price used was indicated as $220 per case instead of $300. Second, February sales

were under stated by 300 units. The accountant had recorded the projected sales in January at

200 units instead of 500 units. This are the two items that caused all those errors in the profit

budget(Lansdowne, 2003)..

Direct Material Purchase

ref Jan Feb March april

Sales 300 500 200

Beginning Inventory a 150 250 100

Desired Ending Inventory b 250 100 100

Production (units) A+b=c 400 350 200

DM( Needed for production) c 400 350 200

Beginning Inventory (DM) 50% 200 175 100

Desired ending inventory 175 100 100

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGEMENT ACCOUNTING 4

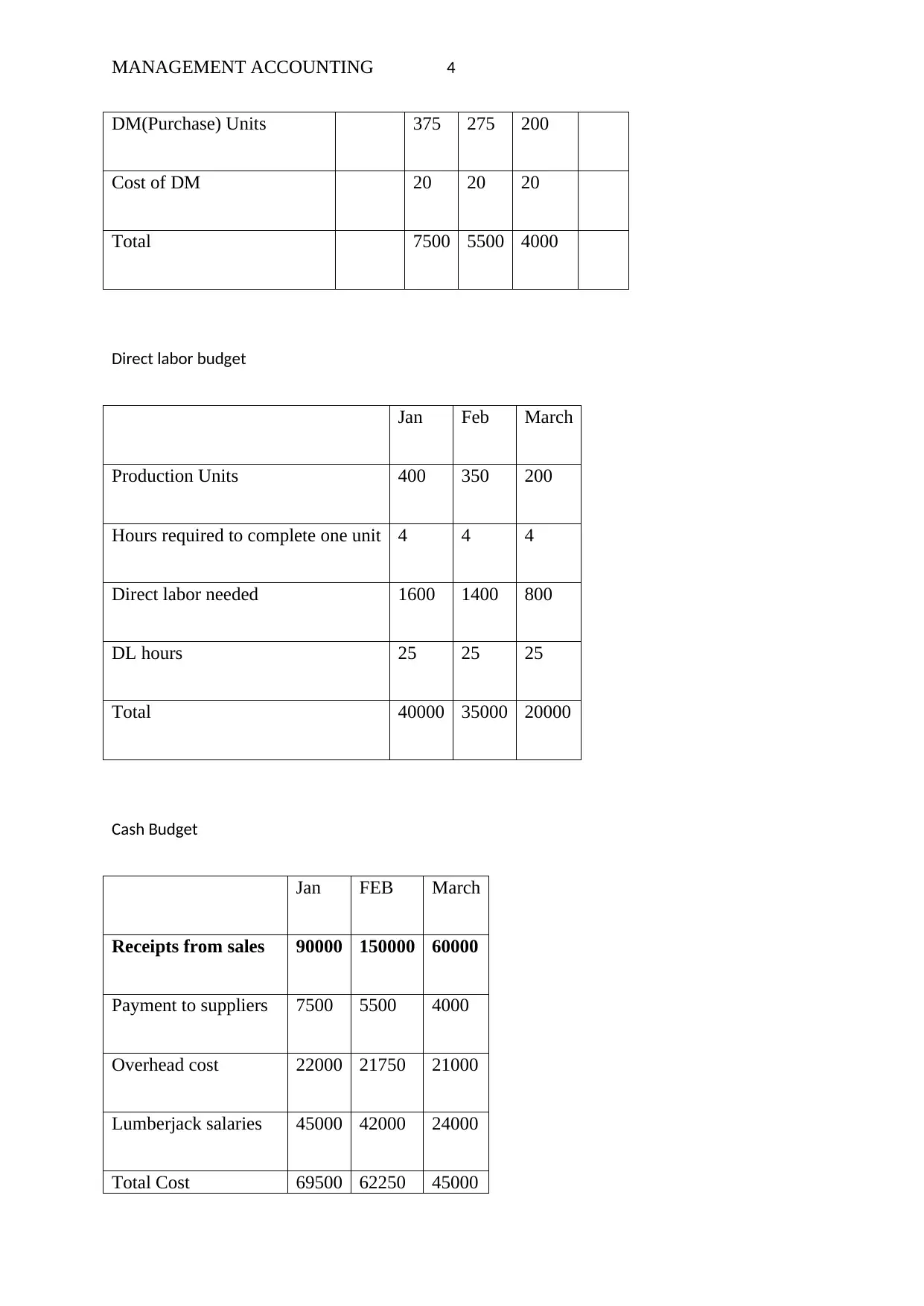

DM(Purchase) Units 375 275 200

Cost of DM 20 20 20

Total 7500 5500 4000

Direct labor budget

Jan Feb March

Production Units 400 350 200

Hours required to complete one unit 4 4 4

Direct labor needed 1600 1400 800

DL hours 25 25 25

Total 40000 35000 20000

Cash Budget

Jan FEB March

Receipts from sales 90000 150000 60000

Payment to suppliers 7500 5500 4000

Overhead cost 22000 21750 21000

Lumberjack salaries 45000 42000 24000

Total Cost 69500 62250 45000

DM(Purchase) Units 375 275 200

Cost of DM 20 20 20

Total 7500 5500 4000

Direct labor budget

Jan Feb March

Production Units 400 350 200

Hours required to complete one unit 4 4 4

Direct labor needed 1600 1400 800

DL hours 25 25 25

Total 40000 35000 20000

Cash Budget

Jan FEB March

Receipts from sales 90000 150000 60000

Payment to suppliers 7500 5500 4000

Overhead cost 22000 21750 21000

Lumberjack salaries 45000 42000 24000

Total Cost 69500 62250 45000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT ACCOUNTING 5

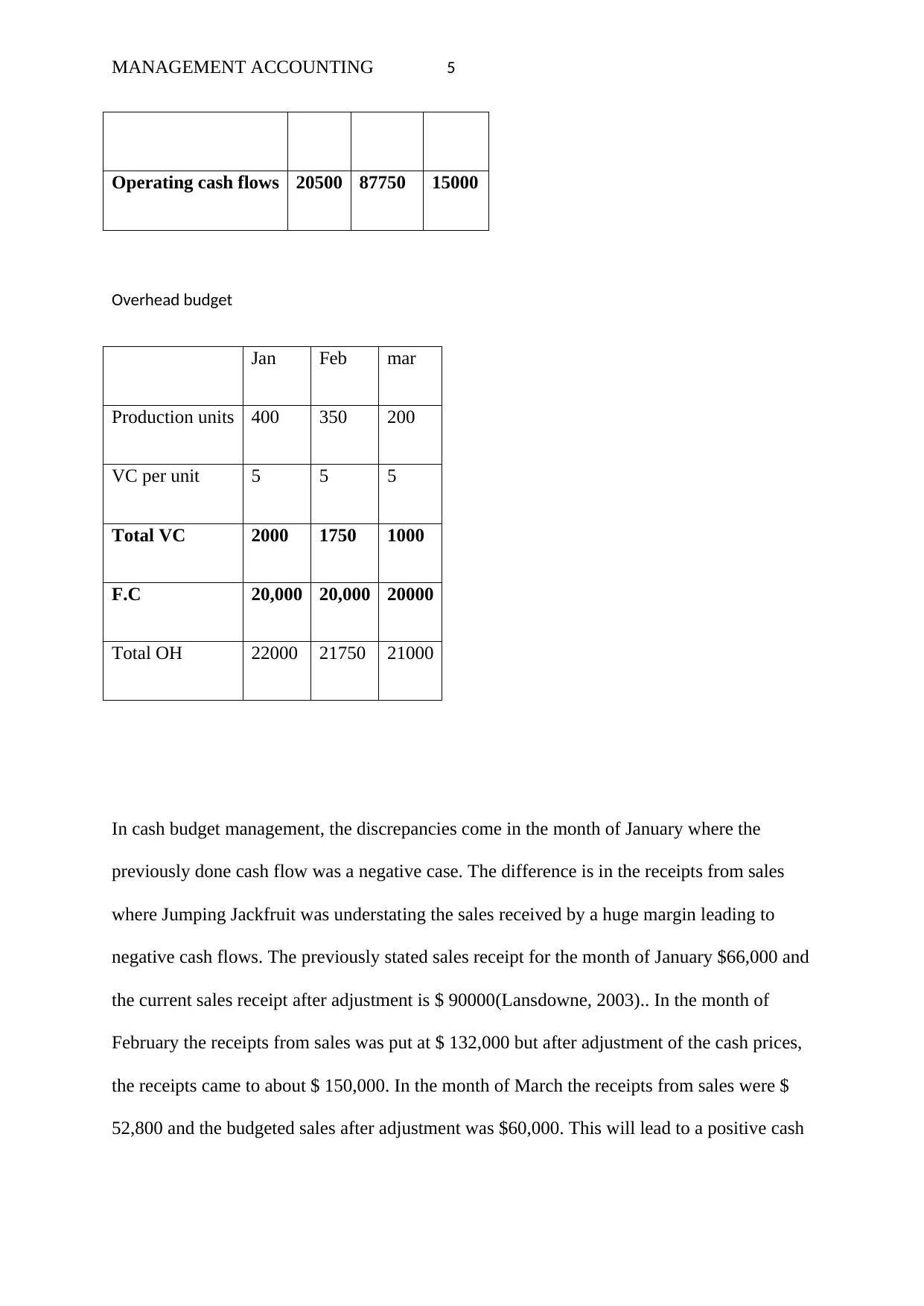

Operating cash flows 20500 87750 15000

Overhead budget

Jan Feb mar

Production units 400 350 200

VC per unit 5 5 5

Total VC 2000 1750 1000

F.C 20,000 20,000 20000

Total OH 22000 21750 21000

In cash budget management, the discrepancies come in the month of January where the

previously done cash flow was a negative case. The difference is in the receipts from sales

where Jumping Jackfruit was understating the sales received by a huge margin leading to

negative cash flows. The previously stated sales receipt for the month of January $66,000 and

the current sales receipt after adjustment is $ 90000(Lansdowne, 2003).. In the month of

February the receipts from sales was put at $ 132,000 but after adjustment of the cash prices,

the receipts came to about $ 150,000. In the month of March the receipts from sales were $

52,800 and the budgeted sales after adjustment was $60,000. This will lead to a positive cash

Operating cash flows 20500 87750 15000

Overhead budget

Jan Feb mar

Production units 400 350 200

VC per unit 5 5 5

Total VC 2000 1750 1000

F.C 20,000 20,000 20000

Total OH 22000 21750 21000

In cash budget management, the discrepancies come in the month of January where the

previously done cash flow was a negative case. The difference is in the receipts from sales

where Jumping Jackfruit was understating the sales received by a huge margin leading to

negative cash flows. The previously stated sales receipt for the month of January $66,000 and

the current sales receipt after adjustment is $ 90000(Lansdowne, 2003).. In the month of

February the receipts from sales was put at $ 132,000 but after adjustment of the cash prices,

the receipts came to about $ 150,000. In the month of March the receipts from sales were $

52,800 and the budgeted sales after adjustment was $60,000. This will lead to a positive cash

MANAGEMENT ACCOUNTING 6

flow budgeted for jumper jackfruit. Total costs will decrease increasing the net cash flows in

each month(Lansdowne, 2003).

In determining the operating cash flows of a business, the total cost and the sales revenues are

the determining factors. For the accountant, the main reason for the disparity in operating

cash flow is the misrepresentation of figures especially in the revenue.

In order to interpret the statement of flows, you must start with the final part of the balance

that you can identify as the increase or decrease of cash, the starting and ending balance of all

cash that includes cash balances, have maturity for collection in a period greater than 90

days(Lansdowne, 2003).

It is important that you independently analyze the results of increases or decreases in the

amount of funds and conclude the behavior of each of the categories and their impact on the

final result.

The operational activity shows the management of the company in the generation of cash

from the operation cycle (purchasing, supply, production, delivery, sale and collection), ie if

the results are positive or surplus, the company can be considered to be managed optimally

and is getting its resources from the same operation, not based on debts and leverage. To

perform the representation of the flow obtained by the operations, two methods can be used

to calculate cash flow as we saw in the previous article, the direct or indirect

method(Lansdowne, 2003).

With respect to investment activities, these relate to the acquisition or disposal of fixed assets.

Because most companies usually acquire more assets than those who sell the effect of these

activities on the cash flow is usually negative.

flow budgeted for jumper jackfruit. Total costs will decrease increasing the net cash flows in

each month(Lansdowne, 2003).

In determining the operating cash flows of a business, the total cost and the sales revenues are

the determining factors. For the accountant, the main reason for the disparity in operating

cash flow is the misrepresentation of figures especially in the revenue.

In order to interpret the statement of flows, you must start with the final part of the balance

that you can identify as the increase or decrease of cash, the starting and ending balance of all

cash that includes cash balances, have maturity for collection in a period greater than 90

days(Lansdowne, 2003).

It is important that you independently analyze the results of increases or decreases in the

amount of funds and conclude the behavior of each of the categories and their impact on the

final result.

The operational activity shows the management of the company in the generation of cash

from the operation cycle (purchasing, supply, production, delivery, sale and collection), ie if

the results are positive or surplus, the company can be considered to be managed optimally

and is getting its resources from the same operation, not based on debts and leverage. To

perform the representation of the flow obtained by the operations, two methods can be used

to calculate cash flow as we saw in the previous article, the direct or indirect

method(Lansdowne, 2003).

With respect to investment activities, these relate to the acquisition or disposal of fixed assets.

Because most companies usually acquire more assets than those who sell the effect of these

activities on the cash flow is usually negative.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGEMENT ACCOUNTING 7

In the case of financing activities, the effect of these transactions with creditors, suppliers and

shareholders is included(Jeremko, 2004).. The bank interest earned on the loans and the

investments that the investors make in the company are reflected as a positive flow of funds,

while the amortization of said loans and the payment of the dividends are considered a

negative cash flow, that is to say a money outflow(Lansdowne, 2003). It is essential that you

analyze the investment needs of the company depending on your business turnover, for

example in companies that are engaged in the manufacturing industry you may have a higher

capital requirement than a consulting company might need.

Cash Flow

By having the information of all the categories it is time to look for a relation between the

financing activities and the investment activities since this will give you a guideline of

whether the active acquisitions that you are realizing are being supported by the company or

are owned by your creditors. An important fact to consider in the case of financing is to

consider that when an asset is acquired through a loan, the useful life of the loan is not less

than the financing term. This will assure you that you will not be allocating amounts of cash

to payments that during that period are not leaving you any benefit for the operation of the

company(Jeremko, 2004)..

As you can see, the analysis of the various financial statements such as the income statement,

the balance sheet and the cash flow provide valuable information for investors and for

In the case of financing activities, the effect of these transactions with creditors, suppliers and

shareholders is included(Jeremko, 2004).. The bank interest earned on the loans and the

investments that the investors make in the company are reflected as a positive flow of funds,

while the amortization of said loans and the payment of the dividends are considered a

negative cash flow, that is to say a money outflow(Lansdowne, 2003). It is essential that you

analyze the investment needs of the company depending on your business turnover, for

example in companies that are engaged in the manufacturing industry you may have a higher

capital requirement than a consulting company might need.

Cash Flow

By having the information of all the categories it is time to look for a relation between the

financing activities and the investment activities since this will give you a guideline of

whether the active acquisitions that you are realizing are being supported by the company or

are owned by your creditors. An important fact to consider in the case of financing is to

consider that when an asset is acquired through a loan, the useful life of the loan is not less

than the financing term. This will assure you that you will not be allocating amounts of cash

to payments that during that period are not leaving you any benefit for the operation of the

company(Jeremko, 2004)..

As you can see, the analysis of the various financial statements such as the income statement,

the balance sheet and the cash flow provide valuable information for investors and for

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT ACCOUNTING 8

making decisions about the management of the company. It is important to be able to

distinguish what type of data you can present each of them and in this way to form a

complete report with different perspectives about the operation and use of resources(Jeremko,

2004)..

Regards

Accountant

Question 2

As long as the customers get the convenience of purchasing both the case and the dice, then

they would be willing to pay premium for the product. Hence the two companies should

come together join effort to make a product that any consumer would demand and like. This

is important because of cost cutting(Hubbard, 2014).

As competition increasingly focuses on differentiation and execution, CEOs will have to steer

their companies toward rapid experimentation and innovation, better insight into customer

insights, effective pricing and promotions, and great customer service. The big challenges

will be to diagnose what the qualities are missing in a company and to develop them

quickly(Jeremko, 2004).

The actions of differentiation are being seen by the two companies making dice. We know

that there may be several aspects that hamper business improvement. In the commercial many

times it feels that the organizations do not find the return to him to progress in being different

or special. They are encyst in a way to perceive more of the same without being able to see

different alternatives. That our organization has a different product, service or brand is a

making decisions about the management of the company. It is important to be able to

distinguish what type of data you can present each of them and in this way to form a

complete report with different perspectives about the operation and use of resources(Jeremko,

2004)..

Regards

Accountant

Question 2

As long as the customers get the convenience of purchasing both the case and the dice, then

they would be willing to pay premium for the product. Hence the two companies should

come together join effort to make a product that any consumer would demand and like. This

is important because of cost cutting(Hubbard, 2014).

As competition increasingly focuses on differentiation and execution, CEOs will have to steer

their companies toward rapid experimentation and innovation, better insight into customer

insights, effective pricing and promotions, and great customer service. The big challenges

will be to diagnose what the qualities are missing in a company and to develop them

quickly(Jeremko, 2004).

The actions of differentiation are being seen by the two companies making dice. We know

that there may be several aspects that hamper business improvement. In the commercial many

times it feels that the organizations do not find the return to him to progress in being different

or special. They are encyst in a way to perceive more of the same without being able to see

different alternatives. That our organization has a different product, service or brand is a

MANAGEMENT ACCOUNTING 9

capacity that does not die, and can be recreated by developing new ways of perceiving to find

solutions in each case(García-Alcaraz, Oropesa-Vento &Maldonado-Macías, n.d.) .

Execution

The two companies should prioritize Specific advertising of "special offers" and the use of

simple and prominent posters allow retail establishments to credit the value they offer and are

likely to become increasingly visible elements of the competitive landscape(HILL, 2016). It

is important to undertake the promotional initiatives and verify that they are sustainable. In

their attempt to compete against value-oriented Japanese companies, for example, American

automakers discovered the dangers of announcing large discounts that were valuable but also

undermined future margins, as they induced customers to postpone the purchase until that the

cars were lowered. Ultimately, the ability to offer competitive prices, even selectively,

depends on keeping costs at bay. In view of the virtuous circle that reinforces the solid

financial figures of many value-based companies, it is impossible to stand or stand by them

through isolated price-cutting initiatives(HILL, 2016). Continuous improvement is necessary,

suggesting the importance of one company in the dice making business adopting and

simplified lean manufacturing methods, which reduces costs and improves quality

consistently and simultaneously.

Much of the market has asked for some alternative to make a difference, given that in recent

years there was a rapid growth and generally had structure to support it, which has been

resorted to or intensified these professional benefits, since there are already many challenges

for different market issues, and when the market is good, the concerns are different, and there

is our challenge, but not only in the professional, but also in the personal to bring a tool as the

Public Relations to give a true added value(Mika, 2006).

capacity that does not die, and can be recreated by developing new ways of perceiving to find

solutions in each case(García-Alcaraz, Oropesa-Vento &Maldonado-Macías, n.d.) .

Execution

The two companies should prioritize Specific advertising of "special offers" and the use of

simple and prominent posters allow retail establishments to credit the value they offer and are

likely to become increasingly visible elements of the competitive landscape(HILL, 2016). It

is important to undertake the promotional initiatives and verify that they are sustainable. In

their attempt to compete against value-oriented Japanese companies, for example, American

automakers discovered the dangers of announcing large discounts that were valuable but also

undermined future margins, as they induced customers to postpone the purchase until that the

cars were lowered. Ultimately, the ability to offer competitive prices, even selectively,

depends on keeping costs at bay. In view of the virtuous circle that reinforces the solid

financial figures of many value-based companies, it is impossible to stand or stand by them

through isolated price-cutting initiatives(HILL, 2016). Continuous improvement is necessary,

suggesting the importance of one company in the dice making business adopting and

simplified lean manufacturing methods, which reduces costs and improves quality

consistently and simultaneously.

Much of the market has asked for some alternative to make a difference, given that in recent

years there was a rapid growth and generally had structure to support it, which has been

resorted to or intensified these professional benefits, since there are already many challenges

for different market issues, and when the market is good, the concerns are different, and there

is our challenge, but not only in the professional, but also in the personal to bring a tool as the

Public Relations to give a true added value(Mika, 2006).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGEMENT ACCOUNTING 10

Quality and service are phenomena driven by many factors, which have been emerging for

some time and is manifested according to the times, creating winners and losers.

We all have something personal and corporate that makes us special and different. The new

business era demands to be innovative, so that to help our company we must achieve success

by developing tools and solutions designed to make the most of it. Nowadays, organizations

are growing and the fundamental factors that explain the phenomenon are related to the

increase in productivity, forging a successful business culture, centered simultaneously on the

generation of economic and social value(Jeremko, 2004).

But then; How to differentiate and anticipate these movements?

In a context of intense competition, demand for short-term results, in an effort to grow, etc.,

companies fight for competitive advantage, fought real battles to win market shares and

struggle to differentiate themselves. At present, so loaded with players the flow is reduced

and everyone is competing(Burman&Slemrod, 2013).

Knowing the public, the market and the competition, a first step would be to propose

abandoning the battles and going out in search of new market spaces that are still unclaimed.

A systematic and particular approach to making competition an irrelevant factor. So the two

companies should understand an old concept of the Prussian armies during the First World

War; "The strategy does not consist of a long plan of action, it is the idea steadily throughout

changing circumstances(Mika, 2006).

Strategy, a concrete fact

Quality and service are phenomena driven by many factors, which have been emerging for

some time and is manifested according to the times, creating winners and losers.

We all have something personal and corporate that makes us special and different. The new

business era demands to be innovative, so that to help our company we must achieve success

by developing tools and solutions designed to make the most of it. Nowadays, organizations

are growing and the fundamental factors that explain the phenomenon are related to the

increase in productivity, forging a successful business culture, centered simultaneously on the

generation of economic and social value(Jeremko, 2004).

But then; How to differentiate and anticipate these movements?

In a context of intense competition, demand for short-term results, in an effort to grow, etc.,

companies fight for competitive advantage, fought real battles to win market shares and

struggle to differentiate themselves. At present, so loaded with players the flow is reduced

and everyone is competing(Burman&Slemrod, 2013).

Knowing the public, the market and the competition, a first step would be to propose

abandoning the battles and going out in search of new market spaces that are still unclaimed.

A systematic and particular approach to making competition an irrelevant factor. So the two

companies should understand an old concept of the Prussian armies during the First World

War; "The strategy does not consist of a long plan of action, it is the idea steadily throughout

changing circumstances(Mika, 2006).

Strategy, a concrete fact

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT ACCOUNTING 11

We should note that if we have a problem with our strategy there is so much competition,

there is more tactical, more action and less time. Evaluating stocks and models in times of

greater business bonanza and adapting the current ones can be a good benchmark.

The consumer is at the center of the strategy, it is the engine of the small and continuous

adaptations that are being implemented to the business plan. There is not much secret, it is the

creativity and the local knowledge of the market that can give us the competitive advantage.

The strategy is to have a vision to know where we stand and what our destiny will

be(Jeremko, 2004). In these times you must be ready to seduce, creativity, quality and level

of products enrich the market. Improvisation ceases to be the priority in every company and

passes the scepter to professionalism and training, problems must be identified immediately

and honestly, facilitating a strategy and taking appropriate countermeasures. Part of our

responsibility is to look at where we want to be positioned and differentiated, and

consequently what steps to take in the area of Public Relations (PR) and how to be in the

market(Medinilla, n.d.). The most conspicuous advantage of innovations is an increase of

sales in the main areas. At the commercial level, being creative and innovative can be part of

the difference; In fact, intelligent innovations can punish competition. But can the application

of differences help companies to sell more, gain market share and generate added value? In

general differentiation is more an art than a science, we can establish what works and what

does not work for us as well for competition. Companies are growing, at the same time there

is an effect that makes each area work in its own sector; but if you do not execute and speak

the strategy to each other, however elaborate it may be, it will not succeed if it is not

implemented in the whole.(Jeremko, 2004)

.Always maintain control of the organization, optimizing its ability to identify, prevent and

respond to possible and constant threats that threaten against your products. The companies

can no longer operate with disintegrated information. It requires data and information

We should note that if we have a problem with our strategy there is so much competition,

there is more tactical, more action and less time. Evaluating stocks and models in times of

greater business bonanza and adapting the current ones can be a good benchmark.

The consumer is at the center of the strategy, it is the engine of the small and continuous

adaptations that are being implemented to the business plan. There is not much secret, it is the

creativity and the local knowledge of the market that can give us the competitive advantage.

The strategy is to have a vision to know where we stand and what our destiny will

be(Jeremko, 2004). In these times you must be ready to seduce, creativity, quality and level

of products enrich the market. Improvisation ceases to be the priority in every company and

passes the scepter to professionalism and training, problems must be identified immediately

and honestly, facilitating a strategy and taking appropriate countermeasures. Part of our

responsibility is to look at where we want to be positioned and differentiated, and

consequently what steps to take in the area of Public Relations (PR) and how to be in the

market(Medinilla, n.d.). The most conspicuous advantage of innovations is an increase of

sales in the main areas. At the commercial level, being creative and innovative can be part of

the difference; In fact, intelligent innovations can punish competition. But can the application

of differences help companies to sell more, gain market share and generate added value? In

general differentiation is more an art than a science, we can establish what works and what

does not work for us as well for competition. Companies are growing, at the same time there

is an effect that makes each area work in its own sector; but if you do not execute and speak

the strategy to each other, however elaborate it may be, it will not succeed if it is not

implemented in the whole.(Jeremko, 2004)

.Always maintain control of the organization, optimizing its ability to identify, prevent and

respond to possible and constant threats that threaten against your products. The companies

can no longer operate with disintegrated information. It requires data and information

MANAGEMENT ACCOUNTING 12

integrity, with the ability to add functionality to users and to handle all the information that

represents the business, its processes and the market in which it competes. It must represent

everything that gives life and movement to the business of the company, each and every one

of the parties must be related according to the needs of each business and be part of

it(Medinilla, n.d.)

Explore and consolidate planning activities is a priority. Marketing, promotions, press, public

relations and other tools are extremely useful and necessary in all plans of companies that

want to survive(Halevi, 2010). The best public relations in a service company is the service

that the people who perform in our company has a good vocation of service. Not only do it

because it is your obligation but feel that by giving service the way the other is requiring it

also produces satisfaction. Differentiation, a constant journey At the present time it is no

longer possible to impose or position a brand or product on the public, but these must be

adopted by the people; knowing that the real challenge is to confirm the relevance(Stewart,

2012).. We must reflect, pause, look carefully at the context in which we must survive.

Try to perceive changes in customer requirements, review marketing channels, advertise, and

public relations do not become obsolete; not clinging to products and concepts just because

they fit into established business models(Sower & Sower, n.d.).

The organization must optimize the performance of its resources almost permanently,

accelerate the releases of services, taking into account that innovation is the ability to

differentiate to excel in the rest, knowing which are the processes that must be supported,

evaluating how to consolidate and optimize what already exists(Stewart, 2012).

The scheme of work is of cooperation and collaboration which allows to maintain an image, a

name and a brand. Providing good technique, great innovation and the best service is

undoubtedly what allows the company to generate contribution in front of others. People

integrity, with the ability to add functionality to users and to handle all the information that

represents the business, its processes and the market in which it competes. It must represent

everything that gives life and movement to the business of the company, each and every one

of the parties must be related according to the needs of each business and be part of

it(Medinilla, n.d.)

Explore and consolidate planning activities is a priority. Marketing, promotions, press, public

relations and other tools are extremely useful and necessary in all plans of companies that

want to survive(Halevi, 2010). The best public relations in a service company is the service

that the people who perform in our company has a good vocation of service. Not only do it

because it is your obligation but feel that by giving service the way the other is requiring it

also produces satisfaction. Differentiation, a constant journey At the present time it is no

longer possible to impose or position a brand or product on the public, but these must be

adopted by the people; knowing that the real challenge is to confirm the relevance(Stewart,

2012).. We must reflect, pause, look carefully at the context in which we must survive.

Try to perceive changes in customer requirements, review marketing channels, advertise, and

public relations do not become obsolete; not clinging to products and concepts just because

they fit into established business models(Sower & Sower, n.d.).

The organization must optimize the performance of its resources almost permanently,

accelerate the releases of services, taking into account that innovation is the ability to

differentiate to excel in the rest, knowing which are the processes that must be supported,

evaluating how to consolidate and optimize what already exists(Stewart, 2012).

The scheme of work is of cooperation and collaboration which allows to maintain an image, a

name and a brand. Providing good technique, great innovation and the best service is

undoubtedly what allows the company to generate contribution in front of others. People

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.